Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

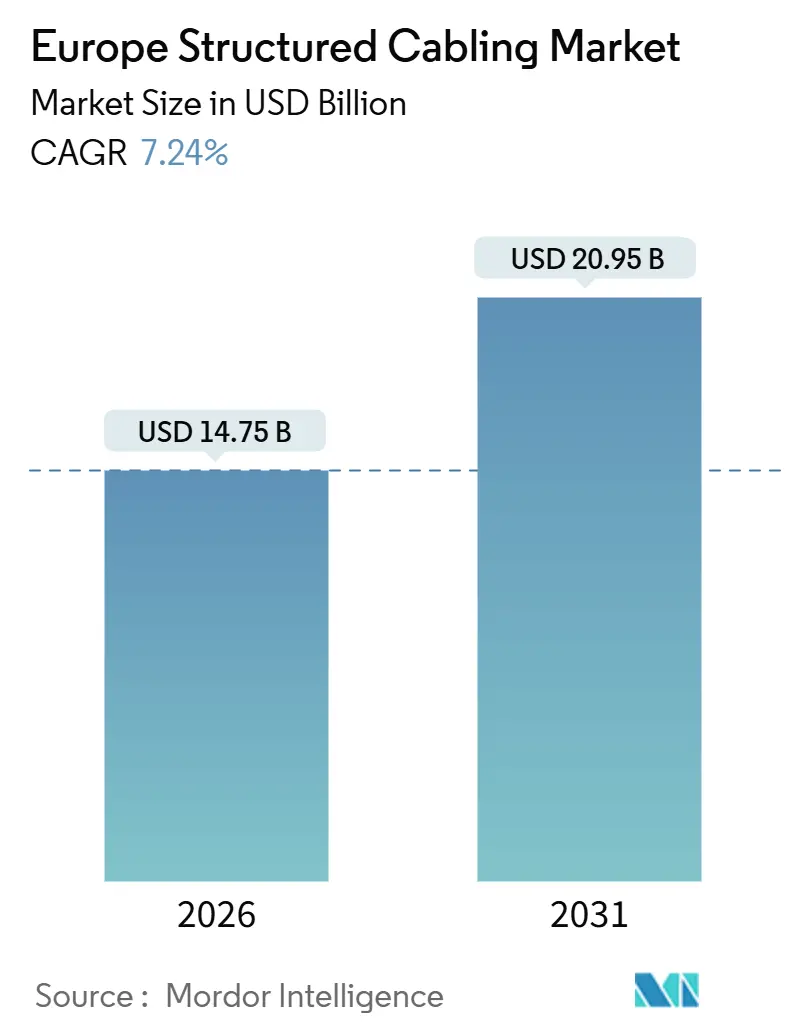

| Market Size (2026) | USD 14.75 Billion |

| Market Size (2031) | USD 20.95 Billion |

| Growth Rate (2026 - 2031) | 7.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Structured Cabling Market Analysis by Mordor Intelligence

The Europe structured cabling market size stands at USD 14.75 billion in 2026 and is projected to reach USD 20.92 billion by 2031, reflecting a 7.24% CAGR over the forecast period. Rising hyperscale data center construction, aggressive EU digital infrastructure funding, and the electrification of industrial automation networks underpin this expansion. Edge computing rollouts on factory floors, dense 5G back-haul fiber builds, and stricter green-building codes are steering specifications toward higher-bandwidth Category 6A, Category 8, and single-mode fiber systems. Vendors capable of delivering pre-terminated, low-smoke, zero-halogen (LSZH) assemblies are gaining competitive traction as European operators prioritize faster time-to-service and compliance with the Construction Products Regulation. Meanwhile, persistent raw-material price swings, for instance, copper averaged USD 9,513 per metric ton in Q2 2025, squeeze mid-tier installers’ margins.[1]Federal Reserve Bagnk of St. Louis, “Global Price of Copper,” FRED, fred.stlouisfed.org Labor shortages for Category 8-certified technicians further complicate project timelines as hyperscalers accelerate build-outs in Frankfurt, Amsterdam, and Paris.

Key Report Takeaways

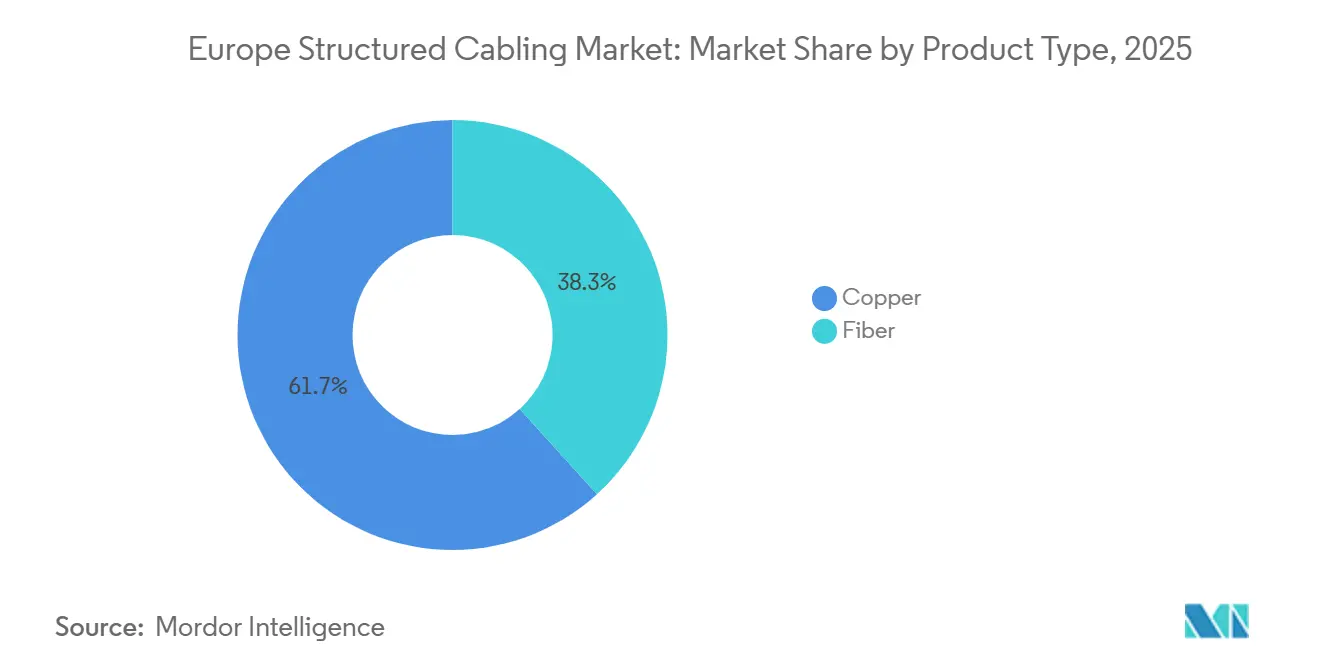

- By product type, copper systems led with 61.72% revenue share in 2025 in the Europe structured cabling market, while fiber solutions are forecast to expand at a 9.02% CAGR through 2031.

- By cable category, Category 6 held 38.63% of Europe structured cabling market share in 2025 whereas Category 8 is projected to grow at 7.98% CAGR between 2026-2031.

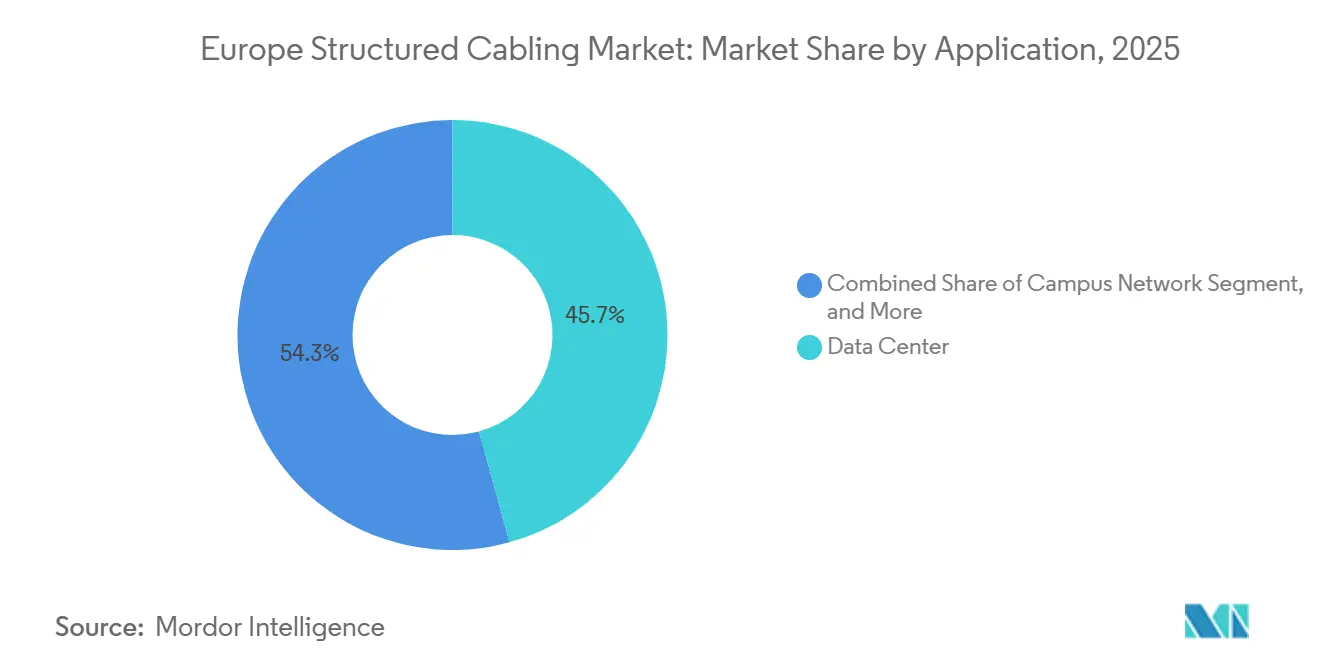

- By application, data-center deployments accounted for 45.73% of Europe structured cabling market size in 2025 while industrial automation networks will advance at an 8.44% CAGR over the same period.

- By industry vertical, IT and telecom dominated with 32.94% revenue share in 2025 of Europe structured cabling market and is estimated to register an 8.14% CAGR to 2031.

- By country, the United Kingdom captured 38.73% of Europe structured cabling market revenue in 2025, while Germany is poised for the fastest 8.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Structured Cabling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale data-center build-outs across Europe | +1.8% | Germany, France, Netherlands, Nordics | Medium term (2-4 years) |

| Rapid adoption of PoE and IoT driving higher-bandwidth cabling | +1.3% | United Kingdom, Germany, France | Short term (≤ 2 years) |

| EU digital-infrastructure funding (CEF-Digital, Recovery Fund) | +1.5% | Pan-European, with emphasis on Spain, Italy, Eastern Europe | Long term (≥ 4 years) |

| 5G back-haul densification requiring fiber-rich cabling | +1.2% | United Kingdom, Germany, Nordics | Medium term (2-4 years) |

| Stricter EU green-building codes favoring LSZH cable | +0.9% | Pan-European, led by Germany, Netherlands, Nordics | Long term (≥ 4 years) |

| Edge micro-data-center rollout in Industry 4.0 plants | +1.1% | Germany, Italy, France manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hyperscale Data-Center Build-Outs Across Europe

Google’s EUR 5.5 billion (USD 6.0 billion) commitment to Dietzenbach and Hanau and Schwarz Group’s EUR 11 billion (USD 12.1 billion) AI hub in Lübbenau epitomize how hyperscale programs embed structured cabling budgets of 8-12% of total capital outlays.[2]Schwarz Digits, “Lübbenau AI Hub Project,” schwarz-it.com Each campus specifies Category 8 copper for top-of-rack links and single-mode fiber trunks exceeding 100 meters, driving demand for 864-fiber MPO assemblies. Data4’s 180 MW Hanau complex and Colt DCS’s 117 MW German pipeline reinforce a multi-year order book that installers must service with pre-staged inventory and certified labor. The Netherlands amplifies regional demand as new trans-Atlantic cables terminate in Amsterdam, necessitating high-density connectivity that fits within tight colocation footprints. Collectively, these mega-projects significantly expand the addressable Europe structured cabling market beyond historical enterprise LAN refresh cycles.

Rapid Adoption of PoE and IoT Driving Higher-Bandwidth Cabling

IEEE 802.3bt’s 90-watt PoE standard ignited large-scale deployments after 2024, when European logistics warehouses and smart-city pilots converged lighting, cameras, and Wi-Fi 6E on unified cabling. Category 6A became the default because its 500 MHz bandwidth supports 10GBASE-T across 100 meters while minimizing voltage drop for devices such as pan-tilt-zoom cameras. The Connecting Europe Facility Digital program earmarked funds for smart-city pilots in Barcelona, Amsterdam, and Copenhagen, multiplying near-term demand for shielded Category 6A bundles.[3]European Commission, “Connecting Europe Facility Digital Programme,” europa.eu Panduit and Siemon are capitalizing by offering 10GBASE-T and TERA connector systems that reduce channel insertion loss and simplify remote powering strategies. Rising PoE currents also require recalculating cable-bundle fill ratios because thermal derating can impair adjacent conductors when conduit occupancy exceeds 40%, nudging facility managers toward higher-grade LSZH jackets.

EU Digital-Infrastructure Funding Programs

The European Parliament Research Service projects EUR 148-200 billion (USD 162-219 billion) in cumulative investment is required to achieve full fiber-to-premises coverage and ubiquitous 5G by 2030. National recovery plans supplement the EUR 2.07 billion CEF-Digital envelope, directing resources to rural fiber rollouts, 5G corridors, and smart-manufacturing clusters. France’s Très Haut Débit program channels EUR 3.5 billion (USD 3.8 billion) into suburban fiber builds, while the United Kingdom’s Project Gigabit allocates GBP 800 million (USD 1.0 billion) to connect 312,000 premises with pre-terminated drop fibers. Spain’s 5G corridor program densifies small-cell sites every 200-300 meters, each requiring Category 6A fronthaul links. Structured cabling vendors positioned in outdoor-rated single-mode fiber and hardened splice closures stand to benefit over the long term.

5G Back-Haul Densification

Europe’s shift from microwave backhaul to fiber transport is accelerating as mid-band 5G spectrum demands fronthaul throughput exceeding 25 Gbps and latency of less than 10 milliseconds. Colt Technology Services’ 2025 Channel Tunnel fiber, engineered for sub-2-millisecond London-to-Paris paths, consumed 400 kilometers of bend-insensitive single-mode fiber. Prysmian and Nexans are scaling their submarine and terrestrial fiber output, with Prysmian’s IOEMA system and Nexans’ hybrid power-fiber cables addressing backhaul densification and grid monitoring simultaneously. High-fiber-count trunks (288-864 strands) and modular cassettes enable mobile operators to aggregate multiple radio sectors onto centralized baseband sites, driving premium demand inside the Europe structured cabling market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward enterprise-class Wi-Fi and virtualized networks | -0.7% | United Kingdom, Germany, France | Short term (≤ 2 years) |

| High retrofit cost of fiber in brownfield buildings | -0.9% | Italy, Spain, United Kingdom urban cores | Medium term (2-4 years) |

| Raw-material price volatility (copper and optical glass) | -1.1% | Pan-European | Short term (≤ 2 years) |

| Shortage of Cat-8-certified installers and test gear | -0.6% | Germany, Netherlands, Nordics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Enterprise-Class Wi-Fi and Virtualized Networks

Wi-Fi 6E and emerging Wi-Fi 7 devices deliver multi-gigabit throughput in the 6 GHz band, allowing some brownfield offices to reduce the density of new copper drops. Financial firms in Frankfurt and London are piloting software-defined WAN overlays that mix 5G and satellite links, marginally limiting commercial real-estate demand for Category 6A. Private 5G standards published by ETSI in 2024 enable factories to bypass wired Ethernet for certain mobile assets. However, latency-critical workloads, high-frequency trading, machine-vision quality control, still rely on deterministic wired links, preserving a sizable core addressable to structured cabling vendors.

High Retrofit Cost of Fiber in Brownfield Buildings

Historic cores of Rome, Barcelona, and London exhibit retrofit costs of EUR 150-300 (USD 164-329) per meter due to heritage permits, asbestos abatement, and congested conduits. Resulting payback periods exceed 15 years without subsidies, deterring private investors. Consequently, demand for structured cabling skews toward greenfield data centers and industrial parks, while aging office towers rely on incremental upgrades or wireless substitutes. Vendors must navigate lumpy public-sector tender cycles and allocate inventory toward faster-moving hyperscale and industrial projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fiber Moves to the Spine

Fiber connectivity captured accelerating demand in 2026 as hyperscale operators specified single-mode runs for every inter-rack and spine-leaf link exceeding 100 meters, lifting the segment toward a 9.02% CAGR through 2031. Within data centers, 864-fiber MPO trunks enable modular growth while reducing floor-space by 30%, directly contributing to improved power-usage effectiveness metrics. Copper still held 61.72% Europe structured cabling market share in 2025, anchored by vast installed bases of Category 6 and 6A that support PoE lighting and Wi-Fi 6E upgrades. Copper also offers the unique ability to deliver data and 90-watt power over the same medium, an advantage fiber cannot replicate without expensive hybrid cables. The growing Europe structured cabling market continues to see fiber displacing copper in Germany’s megacampuses, where Google and Data4 mandate single-mode only architectures. Yet in logistics warehouses and legacy campuses, Category 6A remains the cost-performance sweet spot, highlighting a bifurcated adoption curve that vendors must balance.

Copper’s outlook is buoyed by PoE trends and the relative simplicity of RJ45 terminations compared to fusion-spliced LC connectors. However, Category 8’s emergence imposes new certification hurdles; test gear costing up to EUR 25,000 (USD 27,400) constrains installer capacity, particularly in Frankfurt and Amsterdam build-hotspots. Fiber’s immunity to electromagnetic interference makes it indispensable in automotive and pharmaceutical plants where variable-frequency drives operate alongside precision robots. Corning’s 2024 bend-insensitive launch, allowing 5-millimeter radii, further reduces cabinet footprints in space-constrained colocation halls. This technology convergence positions fiber to capture higher value per rack even as copper clings to PoE-heavy building networks.

By Cable Category: Category 8 Targets Top-of-Rack Density

Category 8 is projected to log a 7.98% CAGR to 2031, because hyperscalers view its 2 GHz bandwidth and 30-meter reach as an economical bridge to 400 Gbps without overhauling entire spine fabrics. Early adopters include Schwarz Group’s Lübbenau AI hub, where 100,000 GPUs necessitate compact high-speed copper to facilitate rack airflow. Category 6 dominated 38.63% of Europe structured cabling market share in 2025, reflecting its entrenched use across office LANs and education sites. Category 6A, with alien-crosstalk shielding and 500 MHz headroom, remains the go-to for 10GBASE-T and 60-90-watt PoE, accounting for most new commercial renovations. Category 7 and 7A linger in niche industrial settings due to GG45 connector incompatibilities that deter broader adoption.

Certification bottlenecks hamper Category 8 acceleration. BICSI only folded 2 GHz testing into curricula in late 2025, so few technicians can validate the stringent channel limits. As hyperscale sites in Germany outstrip local labor pools, contractors import certified staff or stretch schedules, neither of which aligns with investors’ fast-track targets. Conversely, Category 5e’s residual footprint is shrinking because 100 MHz channels cannot sustain modern PoE budgets or 10GBASE-T, catalyzing upgrade cycles where office landlords opt directly for Category 6A. EU CPR LSZH mandates add 10-15% material cost on Category 6A and Category 8, but compliance is non-negotiable in Germany, Netherlands, and Nordics, prompting vendors to standardize LSZH production.

By Application: Industrial Automation Accelerates

Data-center deployments remained the single largest slice, holding 45.73% of 2025 revenue, but industrial automation networks are poised to grow faster, at 8.44% CAGR to 2031. Automotive and pharmaceutical clusters in Germany and Italy require deterministic sub-1-millisecond latency, achieved through Time-Sensitive Networking over Category 6A or fiber backbones. Belden’s Hirschmann switches and Siemens’ TSN-capable PLCs integrate seamlessly with LSZH copper, shortening commissioning cycles in harsh plant environments. Campus LAN applications expand more slowly because Wi-Fi adoption softens the need for dedicated drops at endpoints, although Power over Ethernet nurse-call systems and hybrid learning labs still draw steady volumes.

Industrial automation’s edge-micro data center model concentrates servers adjacent to production lines, creating localized demand for single-mode fiber spines and Category 8 aggregation switches in ruggedized enclosures. While each factory consumes less cabling than a hyperscale hall, aggregate volume across thousands of plants rivals large data-center rollouts. Data-center projects compress vendor margins due to procurement scale; by contrast, industrial clients value tailored technical support, allowing premium pricing on pre-terminated harnesses and armored fiber.

By Industry Vertical: IT and Telecom Sets the Pace

IT and telecom commanded 32.94% of 2025 revenue and are expected to grow at an 8.14% CAGR, mirroring hyperscale and 5G investments.

Government, utilities, and education round out demand diversity. Grid operators embed fiber in high-voltage power cables, a hybrid Prysmian and Nexans specialty that streams real-time diagnostics into control centers. Universities adopting hybrid learning need 25 Gbps uplinks from lecture halls, but budget cycles fluctuate with public funding. Retail and hospitality favor lower-cost Category 6 for point-of-sale terminals and guest Wi-Fi, yielding modest revenue per site.

Geography Analysis

The United Kingdom generated 38.73% of 2025 revenue as London’s trading floors required dual-diverse 100 Gbps fiber paths and Category 8 aggregation switches to shave microseconds off execution latency. Colt DCS’s Slough expansions and Openreach’s rural fiber-to-premises program keep demand robust, yet higher electricity tariffs versus continental Europe and Brexit-related data-sovereignty questions nudge incremental hyperscale builds toward Frankfurt and Amsterdam. Germany, expanding at an 8.44% CAGR, hosts massive greenfield campuses where structured cabling budgets exceed USD 300 million per site. Data-center projects in Dietzenbach, Hanau, and Lübbenau specify LSZH single-mode fiber exclusively for inter-building links, spurring local demand for fusion splicers and optical time-domain reflectometers. Industrial plants in Bavaria and Baden-Württemberg upgrade to TSN Ethernet, bundling Category 6A with fiber to orchestrate robotics and vision systems.

France’s Très Haut Débit initiative and Colt’s 170 MW Paris pipeline fuel moderate growth, bolstered by EDF’s site-selection drive for low-carbon campuses near nuclear stations. Italy and Spain channel recovery funds into suburban fiber builds yet face costly retrofits in dense city blocks, elongating deployment timelines. The Netherlands capitalizes on new trans-Atlantic cables to Amsterdam, necessitating high-density MPO cassettes that shrink patch-panel real estate. Nordic nations attract capital with carbon-neutral grids; Brookfield’s 750 MW Stockholm project alone will require hundreds of kilometers of outdoor-rated single-mode fiber with low-temperature jackets. Rest-of-Europe markets, from Poland to Portugal, pitch lower land prices and renewable power, luring edge deployments that diversify regional demand.

Competitive Landscape

Global incumbents Belden, CommScope, and Corning maintain their entrenched positions through multi-year hyperscale frameworks; however, pricing power erodes as operators source multiple assemblies to mitigate supply risk. European specialists Prysmian, Nexans, and Datwyler leverage LSZH manufacturing expertise and proximity to customer sites, shortening lead times for custom fiber counts. Schneider Electric and Siemens bundle cabling with power and cooling in turnkey data center packages, boosting wallet share and locking in customers early in the design cycle. Legrand and Panduit differentiate themselves through intelligent patch panels and cassette ecosystems that enable remote port monitoring, a feature gaining favor among colocation players as they chase operational efficiency.

White-space entrants target edge industrial sites. TE Connectivity and ABB ruggedize transceivers for high-temperature, high-vibration zones, securing early wins in automotive plants. Software-defined connectivity overlays threaten commoditization at the access layer, but latency-sensitive trades and machine-vision lines remain firmly tethered to wired mediums. The Siemon Company and RandM invest in field-terminable Category 8 connectors and advanced certification kits to ease labor bottlenecks in Germany’s construction clusters. Upcoming IEEE 800 GbE and 1.6 TbE standards promise another refresh wave favoring IP-rich stalwarts such as Corning and CommScope.

Europe Structured Cabling Industry Leaders

Belden Inc.

The Siemon Company

Corning Incorporated

CommScope Holding Company, Inc.

Anixter International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Google began construction of its EUR 5.5 billion German campuses, ordering single-mode fiber trunk kits worth an estimated USD 80 million.

- November 2025: Schwarz Group confirmed Category 8 copper and 400 GbE single-mode fiber for its EUR 11 billion Lübbenau AI hub, allocating roughly USD 120 million to structured cabling.

- October 2025: Data4 secured EUR 2 billion to build a 180 MW Hanau campus, accelerating demand for liquid-cooled direct-attach copper assemblies.

- September 2025: Colt DCS announced 117 MW across Frankfurt and Berlin plus 170 MW in Paris, awarding Category 6A and single-mode fiber contracts to Panduit and Datwyler.

Europe Structured Cabling Market Report Scope

The Europe Structured Cabling Market Report is Segmented by Product Type (Copper Cable, Copper Connectivity, Single-Mode Fiber Cable, Multi-Mode Fiber Cable, Fiber Connectivity), Cable Category (Category 5e, Category 6, Category 6A, Category 7, Category 8), Application (LAN, Data Center, Campus Network, Industrial Automation Networks), Industry Vertical (IT and Telecom, BFSI, Healthcare, Manufacturing, Government, Education, Energy, Other), and Geography (UK, Germany, France, Italy, Spain, Netherlands, Nordics, Rest of Europe). Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Copper | Copper Cable |

| Copper Connectivity | |

| Fiber | Single-Mode Fiber Cable |

| Multi-Mode Fiber Cable | |

| Fiber Connectivity |

By Cable Category

| Category 5e |

| Category 6 |

| Category 6A |

| Category 7 |

| Category 8 |

By Application

| Local Area Network (LAN) |

| Data Center |

| Campus Network |

| Industrial Automation Networks |

By Industry Vertical

| IT and Telecom |

| BFSI |

| Healthcare |

| Manufacturing |

| Government and Public Sector |

| Education |

| Energy and Utilities |

| Other Industry Verticals |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Nordics (Denmark, Sweden, Norway, Finland) |

| Rest of Europe |

| By Product Type | Copper | Copper Cable |

| Copper Connectivity | ||

| Fiber | Single-Mode Fiber Cable | |

| Multi-Mode Fiber Cable | ||

| Fiber Connectivity | ||

| By Cable Category | Category 5e | |

| Category 6 | ||

| Category 6A | ||

| Category 7 | ||

| Category 8 | ||

| By Application | Local Area Network (LAN) | |

| Data Center | ||

| Campus Network | ||

| Industrial Automation Networks | ||

| By Industry Vertical | IT and Telecom | |

| BFSI | ||

| Healthcare | ||

| Manufacturing | ||

| Government and Public Sector | ||

| Education | ||

| Energy and Utilities | ||

| Other Industry Verticals | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Nordics (Denmark, Sweden, Norway, Finland) | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What CAGR is forecast for the Europe structured cabling market to 2031?

The market is projected to expand at a 7.24% CAGR from 2026 to 2031.

Which product type is growing fastest in Europe’s cabling landscape?

Single-mode fiber is set to rise at a 9.02% CAGR as hyperscale data centers migrate to 100-400 Gbps architectures.

Why is Germany outpacing the United Kingdom in new installations?

Mega campuses backed by Google, Schwarz Group, and Data4, along with federal digital-sovereignty policies, are driving an 8.44% CAGR in Germany.

How are PoE trends influencing cable choices?

IEEE 802.3bt 90-watt power budgets make Category 6A the default for new PoE deployments because it balances 10GBASE-T performance with thermal headroom.

What is the main supply-side challenge facing cable vendors?

A shortage of Category 8-certified installers and high-cost test gear is slowing rollouts in Frankfurt and Amsterdam hubs.

Page last updated on: