Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

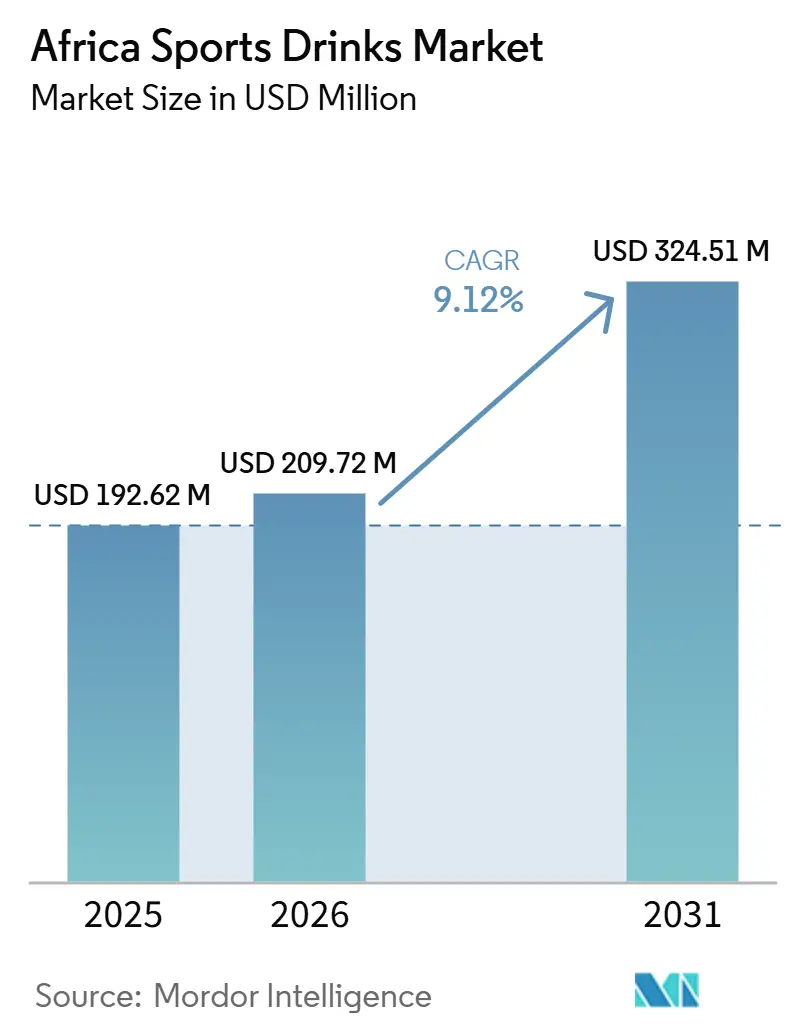

| Base Year Market Size (2025) | USD 192.62 Million |

| Market Size (2026) | USD 209.72 Million |

| Market Size (2031) | USD 324.51 Million |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

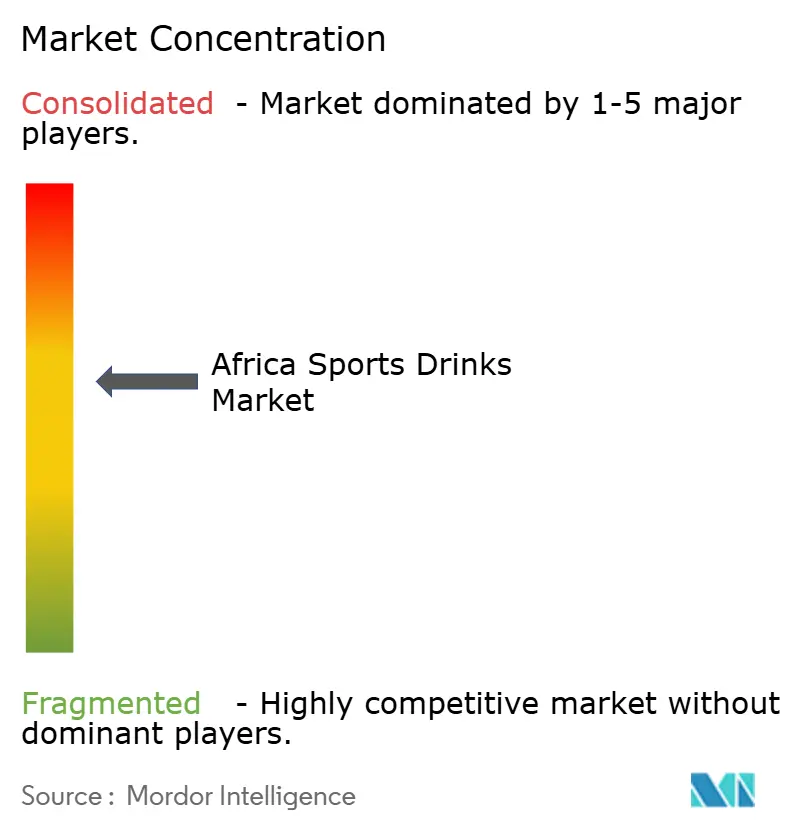

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Africa Sports Drinks Market Analysis by Mordor Intelligence

The Africa sports drinks market size is expected to grow from USD 192.62 billion in 2025 to USD 209.72 billion in 2026 and is forecast to reach USD 324.51 billion by 2031, at a 9.12% CAGR over 2026-2031. The Africa sports drinks market is gaining structural momentum, supported by a young consumer base, rapid urbanization, and an expanding fitness culture. Demand is shifting toward active-lifestyle hydration solutions that bottled water cannot fully address. Urbanization is concentrating retail infrastructure and sports-related activities in emerging cities, creating favorable conditions for single-serve formats. Major continental events, including the Dakar 2026 Summer Youth Olympic Games and the Fédération Internationale de Football Association (FIFA) World Cup 2030, which Morocco, Portugal, and Spain will jointly host, are further driving investment in sports and wellness infrastructure. As gym chains expand across Nigeria, Ghana, and Morocco, and wellness tourism continues to grow, sports drinks are becoming increasingly integrated into Africa’s lifestyle ecosystem. This trend positions the category as a natural complement to the continent’s evolving consumer behavior and aspirational health trends.

Key Report Takeaways

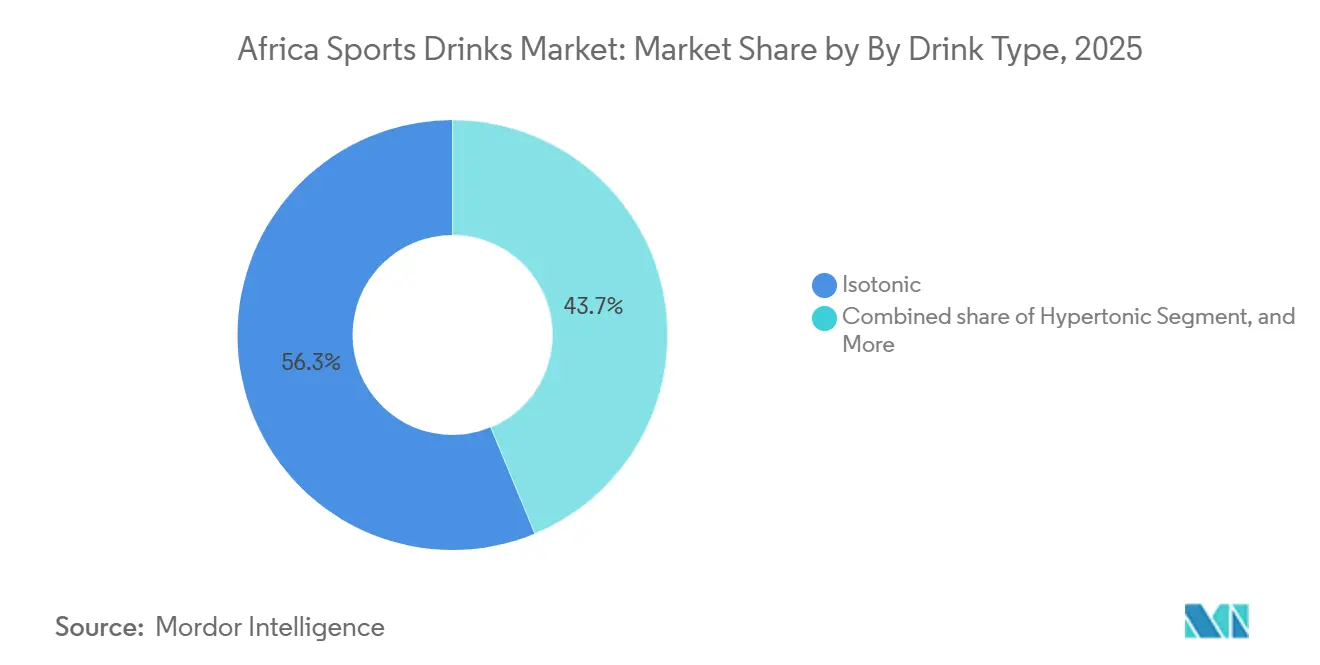

- By drink type, isotonic led the Africa sports drinks market with a share of 56.26% in 2025, whereas hypotonic is anticipated to register the fastest CAGR of 11.01% during 2026-2031.

- By functionality, post-workout retained a 46.27% share in 2025; pre-workout is forecast to expand at a 10.90% CAGR through 2031.

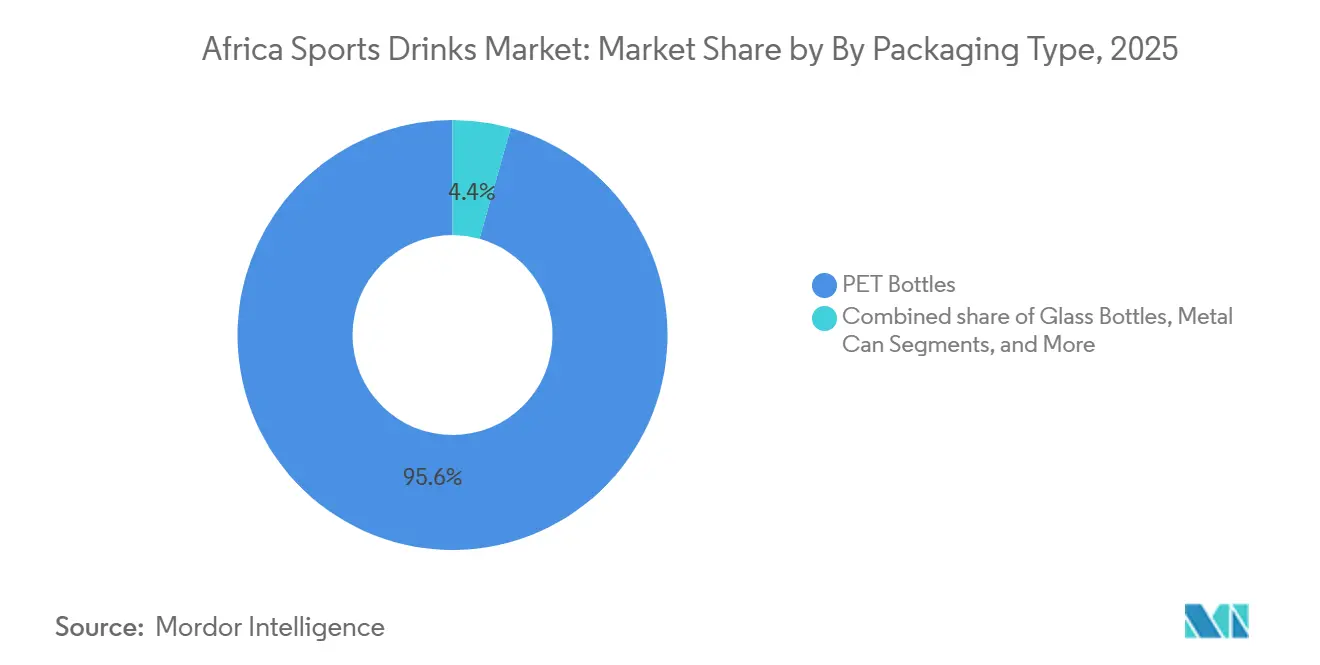

- By packaging type, PET bottles held 95.63% of 2025 revenue, but metal cans are expected to grow fastest at 11.43% through 2031.

- By distribution channel, off-trade led the Africa sports drinks market with a share of 82.72% in 2025, whereas on-trade is anticipated to register the fastest CAGR of 10.96% during 2026-2031.

- By country, South Africa led the Africa sports drinks market with a share of 84.36% in 2025; however, Nigeria is anticipated to register the fastest CAGR of 11.38% during 2026-2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Sports Drinks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising participation in organized sports and fitness activities | +2.8% | South Africa, Nigeria, Kenya, Egypt | Medium term (2–4 years) |

| Increasing demand for hydration solutions in hot climatic conditions | +2.1% | Highest impact in Egypt, Nigeria, Ghana | Short term (≤ 2 years) |

| Expansion of gyms, fitness centers, and health clubs across urban areas | +1.5% | South Africa, Nigeria, Morocco, Kenya | Medium term (2–4 years) |

| Rising adoption of low- and zero-sugar sports drinks among health-conscious consumers | +1.6% | South Africa, Egypt, Morocco | Medium term (2–4 years) |

| Rising urbanization supporting on-the-go beverage consumption | +1.2% | Nigeria, Kenya, Ghana, Morocco | Long term (≥ 4 years) |

| Increasing government and private investment in sports infrastructure and athletics | +1.3% | Kenya, Uganda, Morocco, South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising participation in organized sports and fitness activities

The expansion of fitness chains is supporting growth in the Africa sports drinks market by increasing repeat purchase occasions within the continent’s active-lifestyle economy. Smart Fit’s planned entry into Morocco with five fitness centers in 2025 and iFitness’ confirmed expansion into Ghana and Côte d’Ivoire in 2026 highlight how international and regional operators are investing in fitness infrastructure to address increasing demand for organized fitness services. These developments are increasing sports drink consumption occasions in branded, high-frequency fitness environments, where the products align closely with workout and recovery routines. Meanwhile, the growth of group formats, such as CrossFit, functional training, and parkrun, is creating new on-trade distribution sub-channels and extending the category’s reach beyond traditional retail channels. Together, these trends indicate that fitness chain expansion is reshaping the demand landscape and positioning sports drinks as an important product category within Africa’s evolving wellness and lifestyle ecosystem.

Increasing demand for hydration solutions in hot climatic conditions

The Africa sports drinks market is increasingly influenced by demand for hydration solutions suited to hot climatic conditions, where plain water often does not meet baseline electrolyte needs. This demand is most evident among the informal urban workforce, including laborers, vendors, and transport operators in cities such as Lagos, Cairo, Nairobi, and Accra. Their hydration requirements often resemble those of endurance athletes, but mainstream brands continue to underserve this consumer base. Electrolyte-enhanced water variants are well positioned to capture this opportunity if companies can expand their presence in informal trade channels at accessible price points. At the same time, Africa’s wellness tourism sector and outdoor endurance sports are increasing demand for high-intensity hydration solutions in climate-vulnerable environments. In addition, National Library of Medicine data dated September 2025 indicate that only 20% of African adolescents meet recommended physical activity guidelines, with girls significantly less active than boys[2]Source: National Library of Medicine, “Promoting Adolescent and Youth Health Through Physical Activity Initiatives and Interventions in Sub-Saharan Africa: The ARISE-NUTRINT and DASH Initiatives,” pmc.ncbi.nlm.nih.gov. This trend creates a latent demand pool as governments and nongovernmental organizations invest in youth sports programs. Together, these factors show how climate conditions, workforce dynamics, and youth engagement initiatives are converging to expand the structural demand base for sports drinks across Africa.

Rising adoption of low- and zero-sugar sports drinks among health-conscious consumers

The Africa sports drinks market is undergoing a strategic shift as health-conscious consumers increasingly adopt low- and zero-sugar formulations, making sugar reduction a critical product reformulation priority for manufacturers. South Africa's proposed labeling regulations (Regulation R3337) would require warning labels on approximately 58.7% of all beverages with high sugar content and/or artificial sweeteners [Journal of South African Clinical Nutrition, 2025], directly pressuring manufacturers to reformulate products or risk reduced retail visibility[3]Source: South African Journal of Clinical Nutrition, "Over half of South African beverages will require warning labels for high sugar and/or artificial sweeteners," sajcn.co.za. Kenya’s Nutrient Profile Model further reinforces this regulatory momentum by supporting front-of-pack warning labels across most packaged drinks in East Africa. Against this backdrop, brands such as iPRO Hydrate, which launched in South Africa with stevia-based formulations and sponsored parkrun in March 2025, reflect the market’s reformulation trajectory. This trend positions low- and zero-sugar sports drinks as the segment most strategically aligned with Africa’s evolving health-conscious consumer base, placing them at the intersection of regulatory compliance, lifestyle wellness, and category expansion.

Increasing government and private investment in sports infrastructure and athletics

The Africa sports drinks market is gaining momentum as governments increase investments in sports infrastructure, expanding the category’s addressable consumption base. In July 2025, Kenya’s national government is expected to raise KES 44.875 billion (~USD 347 million) through an infrastructure bond subscription to fund Talanta Sports City in Nairobi, a multi-sport complex targeted for completion ahead of the Africa Cup of Nations (AFCON) 2027. Uganda’s December 2024 agreement with Egypt’s SAMCO National Construction Company for the Akii-Bua Olympic Stadium in Lira City and Angola’s planned rollout of Federation Internationale de Football Association (FIFA)-standard provincial stadiums in March 2026 further demonstrate how sovereign investment strategies are creating recurring hydration consumption opportunities across training, competition, and fan engagement environments. Each new venue creates high-value demand channels beyond traditional retail, positioning sports drinks as a natural beneficiary of Africa’s expanding sports ecosystem and aligning the category with the continent’s long-term infrastructure pipeline.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong competition from bottled water, energy drinks, and other functional alternatives | -0.7% | South Africa, Egypt, Nigeria | Short term (≤ 2 years) |

| Regulatory variations and labeling requirements across countries | -0.4% | Nigeria, Kenya, South Africa | Medium term (2–4 years) |

| Underdeveloped cold chain and distribution infrastructure | -0.5% | Nigeria, Ghana, Kenya, Rest of Africa | Long term (≥ 4 years) |

| Limited consumer awareness in rural and semi-urban markets | -0.3% | Sub-Saharan Africa (rural), Rest of Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong competition from bottled water, energy drinks, and other functional alternatives

The Africa sports drinks market faces a structural restraint due to strong competition from bottled water, energy drinks, and other functional beverage alternatives, which continue to command consumer attention, retail shelf space, and marketing expenditure. Bottled water provides a cost-effective and widely available hydration option, while energy drinks, such as Red Bull and Monster, appeal to a broader consumer base by emphasizing alertness and mood enhancement, without being tied to exercise-led consumption occasions that support sports drink demand. This positioning challenge limits impulse purchase opportunities for sports drinks primarily to self-identified active consumers, making category expansion more challenging. In South Africa, global companies use extensive distribution networks and aggressive marketing investments to sustain brand visibility, while local beverage companies compete on pricing, flavor variety, and accessibility, increasing competitive intensity across the market landscape. Without the financial and operational resources to match the sponsorship programs and brand-building initiatives of multinational energy drink companies, sports drinks remain exposed to margin pressure and slower adoption compared to more versatile beverage alternatives.

Underdeveloped cold chain and distribution infrastructure

The Africa sports drinks market faces constraints from underdeveloped cold chain and distribution infrastructure, which remain among the most significant barriers to expansion outside South Africa. Nigeria operates fewer than 1,000 cold trucks against a requirement of approximately 25,000, meeting less than 4% of its cold chain capacity needs, as of 2025[1]Source: Doing Business In Nigeria "Nigeria’s N160bn Cold Chain Opportunity For Investors," doingbusinessinnigeria.org. This gap generates estimated annual losses of NGN 3.5 trillion across perishable-adjacent product categories, including chilled beverages. As consumers overwhelmingly consume sports drinks chilled, products that arrive warm at retail outlets in Lagos or Accra fail to trigger the impulse purchases that support category economics. East Africa has attracted proportionally more cold chain investment than West Africa, widening the intra-continental distribution gap. This deficit favors large incumbents such as Coca-Cola’s Nigerian Bottling Company (NBC) and PepsiCo’s Seven-Up Bottling Company (SBC) Kenya, which already control extensive ambient distribution networks and can expand into chilled formats incrementally. In contrast, smaller or new entrants face capital-intensive barriers at the point of entry. As a result, the lack of robust cold chain infrastructure continues to limit the ability of sports drinks to scale beyond premium urban enclaves, reinforcing a structural restraint on category growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drink Type: Isotonic Leadership Tested by Hypotonic's Low-Sugar Pivot

In the Africa sports drinks market, isotonic drinks remain the largest category, accounting for a 56.26% share in 2025. Their leadership reflects their suitability for moderate- to high-intensity exercise and their long-standing positioning as the standard hydration format in African sports culture. Established brands continue to support strong distribution and market visibility, while isotonic drinks shape mainstream consumer perceptions of sports hydration. Hypertonic formulas address a more limited endurance-focused consumer base, and adjacent formats, such as electrolyte-enhanced water and protein-based drinks, are only beginning to develop distinct consumer segments among urban fitness enthusiasts. This established leadership positions isotonic drinks as the benchmark against which consumers and brands assess all other formats.

By contrast, hypotonic drinks are the fastest-growing segment and are forecast to expand at a CAGR of 11.01% through 2031. The segment’s growth is supported by low-sugar reformulation priorities, the increasing participation of casual exercisers, and demand from broader wellness-oriented consumers seeking lighter hydration solutions. Commercial launches, such as naturally sweetened and zero-calorie ranges, have positioned hypotonic drinks as a key response to regulatory pressure and rising consumer health awareness. Notably, hypotonic drink growth extends beyond athletic use into everyday hydration occasions, including office, travel, and outdoor leisure, broadening the category’s relevance beyond traditional sports environments. This shift signals a structural evolution in the market, as hypotonic drinks redefine the boundaries of sports hydration.

By Functionality: Recovery Dominates, Pre-Workout Accelerates

In the Africa sports drinks market, post-workout functionality remained the largest segment, accounting for a 46.27% share in 2025. This leadership reflects consumers’ established preference for post-exercise replenishment, making recovery the most common consumption occasion across geographies and income levels. Sports culture has long reinforced recovery-led positioning, with post-workout drinks serving as the default hydration choice for both recreational exercisers and competitive athletes. Intra-workout hydration, although smaller, is gradually gaining traction among endurance athletes and high-volume gym users. However, recovery continues to support the category’s mainstream relevance and retail visibility.

By contrast, pre-workout functionality is the fastest-growing segment and is forecast to expand at a CAGR of 10.90% through 2031. This growth reflects the increasing maturity of Africa’s urban gym population, as consumer awareness of workout timing develops alongside fitness culture. A large share of first-generation gym participants is only beginning to adopt pre-workout supplementation protocols, creating opportunities for demand generation and awareness building. Brands that invest in in-gym communication, fitness influencer partnerships, and product education strategies are well positioned to capture this growth opportunity. As gym ecosystems expand across Lagos, Nairobi, and Cairo, the pre-workout segment is expected to gain further momentum, redefine consumption patterns, and emerge as a key driver of category growth.

By Packaging Type: PET Bottles' Structural Lead, Metal Cans Redefining Premium

In the Africa sports drinks market, PET bottles remained the dominant packaging format, accounting for a 95.63% share in 2025. Their leadership reflects cost efficiency, established supply chains, and suitability for the off-trade channel, which continues to account for most volumes. Investments in recycling infrastructure further reinforce polyethylene terephthalate’s entrenched position. These include South Africa’s planned recycled polyethylene terephthalate (rPET) plant in Cape Town in October 2025 and the International Finance Corporation’s (IFC) partnership with Mohinani Group to build polyethylene terephthalate recycling facilities in Ghana and Nigeria in February 2025. These developments strengthen polyethylene terephthalate’s sustainability credentials and support compliance with international packaging standards, making polyethylene terephthalate bottles the structural backbone of the category’s distribution model.

In contrast, metal cans are the fastest-growing packaging format and are forecast to expand at a CAGR of 11.43% through 2031. Premiumization trends, in-venue consumption across gyms and sports facilities, and alignment with global sports drink aesthetics that polyethylene terephthalate bottles cannot replicate drive this growth. The on-trade channel, which is also the fastest-growing distribution segment, naturally favors cans, as chilled single-serve cans sold in gyms or sports venues command higher unit prices and face lower price sensitivity than polyethylene terephthalate bottles sold in supermarkets. This trajectory positions cans as the format redefining premium sports drink consumption in Africa, signaling a shift toward higher-value occasions and lifestyle-driven demand.

By Distribution Channel: Off-Trade Structural Leader, On-Trade an Underdeveloped Opportunity

In the Africa sports drinks market, off-trade channels remained the structural leader, holding 82.72% of the market in 2025. This leadership is supported by supermarkets and hypermarkets across South Africa, Egypt, and Morocco, along with the increasing penetration of convenience stores in Nigeria and Kenya. The off-trade channel benefits from established retail infrastructure, broad consumer reach, and cost-efficient distribution, making it the backbone of category volumes. Specialty stores, such as health food outlets and gym pro shops, are also emerging as premium-positioning sub-channels, enabling select brands to secure margin-rich footholds before expanding through mainstream retail. Online retail, while still nascent in most African markets, is gaining traction in South Africa and Egypt, where e-commerce infrastructure supports direct-to-consumer delivery for sports nutrition products.

By contrast, on-trade distribution is the fastest-growing channel and is forecast to expand at a CAGR of 10.96% through 2031. This segment includes gyms, fitness centers, sports venues, stadiums, cafés, and hospitality environments, which align with the sports infrastructure investment accelerating across Africa. Unlike supermarket shelves, on-trade environments create high-value, high-frequency consumption occasions, with chilled single-serve formats commanding premium pricing and showing lower price sensitivity. Major sporting events, such as the Africa Cup of Nations 2027, further amplify this opportunity, as official sports drink designations at venues across Kenya, Uganda, and Tanzania could secure both volume and sustained brand visibility among concentrated live-sports audiences. As gym culture and venue infrastructure expand across urban hubs, the on-trade channel is positioned to redefine the category’s growth trajectory, shifting sports drinks from a retail-driven purchase to an embedded lifestyle consumption occasion.

Geography Analysis

South Africa held the leading position, accounting for an 84.36% share in 2025. This leadership reflects the depth of its sports culture, the maturity of its retail infrastructure, and the strong presence of global leaders such as Coca-Cola and Tiger Brands. Strategic investments, including Coca-Cola Beverages Africa’s planned Midrand bottling line in July 2025 and Coca-Cola’s multi-billion expansion commitment, are expected to further strengthen the country’s position. However, functional waters and reformulated soft drinks are emerging as competitive threats, challenging the long-term sustainability of South Africa’s dominance.

By contrast, Nigeria is projected to be the fastest-growing market, with an 11.38% compound annual growth rate through 2031. A young and urbanizing population, along with the rapid expansion of organized fitness into middle-class residential areas in Lagos, Abuja, and Port Harcourt, is driving this growth. Coca-Cola’s USD 1 billion investment commitment in Nigeria in 2024 highlights multinational confidence in West Africa’s consumer goods growth. Egypt also presents a strong growth corridor, supported by persistent heat-driven hydration demand, a robust football and gym culture, and increasing modern retail penetration.

Beyond these core markets, Kenya, Morocco, Ghana, and the Rest of Africa are developing credible bases for expansion. Kenya’s Talanta Sports City investment ahead of the Africa Cup of Nations 2027, combined with brand-community activations such as iPRO Hydrate’s parkrun sponsorship, demonstrates the convergence of infrastructure development and consumer engagement. In Morocco, the entry of international gym operators such as Smart Fit signals the market’s readiness to adopt premium European formats. Meanwhile, Ghana and francophone West Africa are integrating sports drinks into broader urbanization and functional beverage growth trends. Côte d’Ivoire’s double-digit growth in functional beverage consumption confirms that the region is building the foundation for category expansion.

Competitive Landscape

The Africa sports drinks market remains highly fragmented, with competitive dynamics varying by country. Coca-Cola Beverages Africa (CCBA) leads the competitive landscape through Powerade in South Africa and PowerPlay across East Africa, leveraging a distribution network that regional players cannot easily replicate. Coca-Cola Hellenic Bottling Company’s (Coca-Cola HBC) pending USD 2.6 billion acquisition of CCBA in 2025 would place the continent’s largest bottler under a more commercially aggressive parent, potentially accelerating distribution investment and product innovation. Smaller incumbents, such as Kingsley Beverages, Ekhamanzi Springs, and AJE Group, will need to differentiate through pricing, localized formulations, or niche channel strategies.

Strategic opportunities exist in the on-trade gym and venue channel, where no single player has secured exclusivity. Additional growth opportunities are emerging in the low-sugar and functional hydration sub-category, where regulatory-driven reformulation is creating openings for early movers. Innovation remains largely formulation-led, with brands focusing on low-sugar electrolyte profiles and natural sweeteners. This trend creates room for well-funded regional entrants to establish differentiated market positions. At the same time, functional waters and fortified hydration products are emerging as competitive threats, attracting health-oriented, non-athlete consumers who represent the broadest potential expansion pool.

Regulatory developments are reshaping the competitive balance. Nigeria’s National Agency for Food and Drug Administration and Control (NAFDAC) labeling disclosure requirements and South Africa’s proposed front-of-pack warning label regulation create compliance obligations that favor international brands with established low-sugar portfolios. Local competitors that rely on legacy high-sugar formulations face structural disadvantages, as reformulation requires both capital and technical expertise. This regulatory shift, combined with fragmented competition and evolving consumer preferences, positions the Africa sports drinks market as a competitive battleground where global incumbents, regional challengers, and functional beverage disruptors will continue to test the limits of distribution and brand positioning.

Africa Sports Drinks Industry Leaders

-

PepsiCo, Inc.

-

Suntory Holdings Limited

-

The Coca-Cola Company

-

Tiger Brands Ltd.

-

Kingsley Beverages Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The Coca-Cola Company and its two authorized bottlers, Coca-Cola Beverages South Africa and Coca-Cola Peninsula Beverages, plan to invest South African rand 17.6 billion (United States dollar 1.05 billion) in South Africa through 2030 to support the expansion of production capacity.

- March 2025: iPRO Hydrate, a leading functional hydration brand, launched in South Africa, representing a key milestone in its global expansion strategy. This launch is supported by an exclusive partnership with Gordon Sweets, a reputable distributor serving independent retailers and the impulse sector. Based in Cape Town's Western Province, Gordon Sweets offers nationwide distribution, ensuring iPRO Hydrate's accessibility to consumers throughout the country.

- February 2025: BigTree Beverages Ltd, an independent subsidiary of the Trade Kings Group, introduced FIT by Vatra, a sports drink designed to support the fitness goals of athletes and enthusiasts in Zambia. This launch represents an important addition to the company’s beverage portfolio, emphasizing its focus on wellness and sports development in the region. FIT by Vatra is formulated to provide optimal hydration and replenishment, offering a balanced combination of essential minerals, carbohydrates, and electrolytes, with a controlled sugar content to enhance performance.

Africa Sports Drinks Market Report Scope

A sports drink is a functional beverage designed to rehydrate and replenish electrolytes and carbohydrates lost during strenuous exercise, making it distinct from energy drinks that focus on stimulants.

The Africa sports drinks market is segmented based on drink type, functionality, packaging type, distribution channel, and country. By drink type, the market is segmented into isotonic, hypertonic, hypotonic, electrolyte-enhanced water, and protein-based sport drinks. By functionality, the market is segmented into pre-workout, intra-workout, post-workout, and others. By packaging type, the market is segmented into pet bottles, glass bottles, metal can, aseptic packages, and disposable cups. By distribution channel, the market is segmented into on-trade and off-trade. By country, the market is segmented into South Africa, Egypt, Nigeria, Kenya, Morocco, Ghana, and Rest of Africa. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Liters).

By Drink Type

| Isotonic |

| Hypertonic |

| Hypotonic |

| Electrolyte-Enhanced Water |

| Protein-based Sports Drinks |

By Functionality

| Pre-Workout |

| Intra-Workout |

| Post-Workout |

| Others |

By Packaging Type

| PET Bottles |

| Glass Bottles |

| Metal Can |

| Aseptic packages |

| Disposable Cups |

By Distribution Channel

| On-Trade |

| Off-Trade |

| Supermarket/Hypermarket |

| Convenience Stores |

| Specialty Stores |

| Online Retail |

| Other Distribution Channels |

By Country

| South Africa |

| Egypt |

| Nigeria |

| Kenya |

| Morocco |

| Ghana |

| Rest of Africa |

| By Drink Type | Isotonic |

| Hypertonic | |

| Hypotonic | |

| Electrolyte-Enhanced Water | |

| Protein-based Sports Drinks | |

| By Functionality | Pre-Workout |

| Intra-Workout | |

| Post-Workout | |

| Others | |

| By Packaging Type | PET Bottles |

| Glass Bottles | |

| Metal Can | |

| Aseptic packages | |

| Disposable Cups | |

| By Distribution Channel | On-Trade |

| Off-Trade | |

| Supermarket/Hypermarket | |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail | |

| Other Distribution Channels | |

| By Country | South Africa |

| Egypt | |

| Nigeria | |

| Kenya | |

| Morocco | |

| Ghana | |

| Rest of Africa |

Market Definition

- Carbonated Soft Drinks (CSDs) - Carbonated soft drinks (CSDs) refer to non-alcoholic beverages that are carbonated and typically flavored, containing dissolved carbon dioxide to create effervescence. These beverages commonly include cola, lemon-lime, orange, and various fruit-flavored sodas. Marketed in cans, bottles, or fountain dispense.

- Juices - We have considered packaged juices which encompass non-alcoholic beverages derived from fruits, vegetables, or a combination thereof, processed and sealed in various packaging formats such as bottles, cartons, or pouches. Excluding fresh juices, this market segment involves commercially prepared and preserved juices, often with added preservatives and flavors.

- Ready-to-Drink (RTD) Tea and RTD Coffee - Ready-to-Drink (RTD) tea and RTD coffee are pre-packaged, non-alcoholic beverages that are brewed and prepared for consumption without further dilution. RTD tea typically includes various tea varieties, infused with flavors and sweeteners, and comes in bottles, cans, or cartons. Similarly, RTD coffee involves pre-brewed coffee formulations, often mixed with milk, sugar, or flavorings, and is conveniently packaged for on-the-go consumption.

- Energy Drinks - Energy drinks are non-alcoholic beverages formulated to provide a quick boost of energy and alertness. Whereas, sports drinks are beverages designed to hydrate and replenish electrolytes, particularly after physical exertion, exercise, or intense activity

| Keyword | Definition |

|---|---|

| Carbonated Soft Drinks | Carbonated soft drinks (CSDs) are a combination of carbonated water and flavouring, sweetened by sugar or a non-sugar sweeteners. |

| Standard Cola | Standard Cola is defined as the original flavor of cola soda. |

| Diet Cola | A cola-based soft drink containing no or low amounts of sugar |

| Fruit Flavored Carbonates | A carbonated beverage prepared from fruit juice/fruit flavor with carbonated water and containing sugar, dextrose, invert sugar or liquid glucose either singly or in combination. It may contain peel oil and fruit essences. |

| Juice | Juice is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| 100% Juice | Fruit/vegetable juice made from fruit in the form of its juice with no water added to make up the volume. It is not permitted to add sugars, sweeteners, preservatives, flavourings or colourings to fruit juice. |

| Juice Drinks (up to 24% Juice) | Fruit/vegetable juice drinks with up to 24% fruits/vegetable extract. |

| Nectars (25-99% Juice) | Juices that can have between 25 and 99% of fruit, with the minimum legal limits defined depending on the type of fruit |

| Juice concentrates | Juice Concentrates are those form of juices when most of this liquid is removed resulting in a thick, syrupy product known as juice concentrate. |

| RTD Coffee | Packaged coffee beverages that are sold in a prepared form and are ready for consumption at the time of purchase. |

| Iced Coffee | An iced coffee is a cold version of coffee, usually a combination of hot espresso and milk with ice added to it. |

| Cold Brew Coffee | Cold brew also called cold water extraction or cold pressing is made by steeping ground coffee in room-temperature water for several hours. |

| RTD Tea | Ready-to-drink (RTD) tea is a packaged tea product ready for immediate consumption without brewing or preparation |

| Iced Tea | Ice tea or iced tea is a drink made from tea without milk but with sugar and sometimes fruit flavourings, drunk cold. |

| Green Tea | Green tea is a tea beverage which promotes mental alertness, relieving digestive symptoms and promoting weight loss. |

| Herbal Tea | Herbal tea beverages are made from the infusion or decoction of herbs, spices, or other plant material in hot water. |

| Energy Drink | A type of drink containing stimulant compounds, usually caffeine, which is marketed as providing mental and physical stimulation. They may or may not be carbonated and may also contain sugar, other sweeteners, or herbal extracts, among numerous possible ingredients. |

| Sugar-free or Low-calories Energy Drinks | Sugar-free or Low-calories Energy Drinks are sugar-free, artificially sweetened energy drinks with few or no calories. |

| Traditional Energy Drink | Traditional Energy Drinks are functional soft drinks containing ingredients designed to boost the consumer's energy. |

| Natural/Oraganic Energy Drinks | Natural/Organic energy drinks are energy drinks free of artificial sweeteners and synthetic colorings. Instead, they contain naturally derived ingredients such as green tea, yerba mate, and botanical extracts. |

| Energy Shots | A small but highly concentrated energy drink that contains large amounts of caffeine and/or other stimulants. The quantity is comparatively smaller compared to energy drinks. |

| Sports Drink | Sports drinks are beverages designed specifically for the rapid supply of fluid, carbohydrates, and electrolytes before, during or after exercise. |

| Isotonic | Isotonic drinks contain similar concentrations of salt and sugar as in the human body, and are designed to quickly replace fluids lost during exercise but with an increase of carbohydrate. |

| Hypertonic | Hypertonic drinks have a higher concentration of salt and sugar than the human body. They are best drunk after exercise as it is important to replace glycogen levels quickly after exercise. |

| Hypotonic | Hypotonic drinks are designed to quickly replace fluids lost during exercise. They have very low carbohydrate content and a lower concentration of salt and sugar than the human body. |

| Electrolyte-Enhanced Water | Electrolyte water is water infused with electrically-charged minerals, such as sodium, potassium, calcium, and magnesium. |

| Protein-based Sport Drinks | Protein-based sports drinks are those sports drinks which has added protein in it that will improve performance and reduce muscle protein breakdown. |

| On-Trade | The on-trade refers to places that sell beverages for immediate consumption on the premises like bars, restaurants, and pubs |

| Off-Trade | Off-trade usually means places like liquor stores, supermarkets and other places where you don't consume the beverage right away. |

| Convenience Store | A retail business that provides the public with a convenient location to quickly purchase a wide variety of consumable products and services, generally food and gasoline. |

| Specialty store | A specialty store is a shop/store that carries a deep assortment of brands, styles, or models within a relatively narrow category of goods |

| Online Retail | Online retail is a type of eCommerce whereby a business sells goods or services directly to consumers from a website. |

| Aseptic Packaging | Aseptic packaging refers to the filling of a cold, commercially sterile product under sterile conditions into a presterilized container and closure under sterile conditions to form a seal that effectively excludes microorganisms. These includes tetra packs, cartons, pouches etc. |

| PET Bottle | PET bottle means a bottle made of polyethylene terephthalate. |

| Metal Cans | Metal containers made of aluminum or tin- plated or zinc-plated steel, which are commonly used for packaging food, beverages or other products. |

| Disposable Cups | Disposable Cup means a cup or other container designed for single use to serve beverages, such as water, cold drinks, hot drinks and alcoholic beverages. |

| Gen Z | A way of referring to the group of people who were born in the late 1990s and early 2000s. |

| Millenial | Anyone born between 1981 and 1996 (ages 23 to 38 in 2019) is considered a Millennial |

| Taurine | Taurine is an amino acid that supports immune health and nervous system function. |

| Bars & Pubs | It is a drinking establishment licensed to serve alcoholic drinks for consumption on the premises. |

| Café | It is a foodservice establishment serving refreshments (mainly coffee) and light meals. |

| On the go | It means doing / dealing with while busily engaged with something and not diverting plans in order to accommodate. |

| Internet Penetration | The Internet Penetration Rate corresponds to the percentage of the total population of a given country or region that uses the Internet. |

| Vending Machine | A machine that dispenses small articles such as food, drinks, or cigarettes when a coin or token is inserted |

| Discount store | A discount store or discounter offers a retail format in which products are sold at prices that are in principle lower than an actual or supposed "full retail price". Discounters rely on bulk purchasing and efficient distribution to keep down costs. |

| Clean Label | Clean label on the beverage market are drinks that are made from few ingredients of natural origin and are not or only slightly processed. |

| Caffeine | An alkaloid compound which is a stimulant of the central nervous system. It is mainly used recreationally, as a mild cognitive enhancer to increase alertness and attentional performance. |

| Extreme sport | Action sports, adventure sports or extreme sports are activities perceived as involving a high degree of risk. |

| High-intensity interval training | It incorporates several rounds that alternate between several minutes of high intensity movements to significantly increase the heart rate to at least 80% of one's maximum heart rate, followed by short periods of lower intensity movements. |

| Shelf life | The length of time for which an item remains usable, fit for consumption, or saleable. |

| Cream Soda | Cream soda is a sweet soft drink. Generally flavored with vanilla and based on the taste of an ice cream float |

| Root Beer | Root beer is a sweet North American soft drink traditionally made using the root bark of the sassafras tree Sassafras albidum or the vine of Smilax ornata as the primary flavor. Root beer is typically, but not exclusively, non-alcoholic, caffeine-free, sweet, and carbonated. |

| Vanilla Soda | A carbonated soft drink flavoured with vanilla. |

| Dairy-Free | A product that does not contain any milk or milk products from cows, sheep or goats. |

| Caffeine-Free Energy Drinks | Caffeine-free energy drinks rely on other ingredients to boost the energy. Popular choices include amino acids, B vitamins, and electrolytes. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated reports, custom consulting assignments, databases & subscription platforms