Africa Orange Market Analysis by Mordor Intelligence

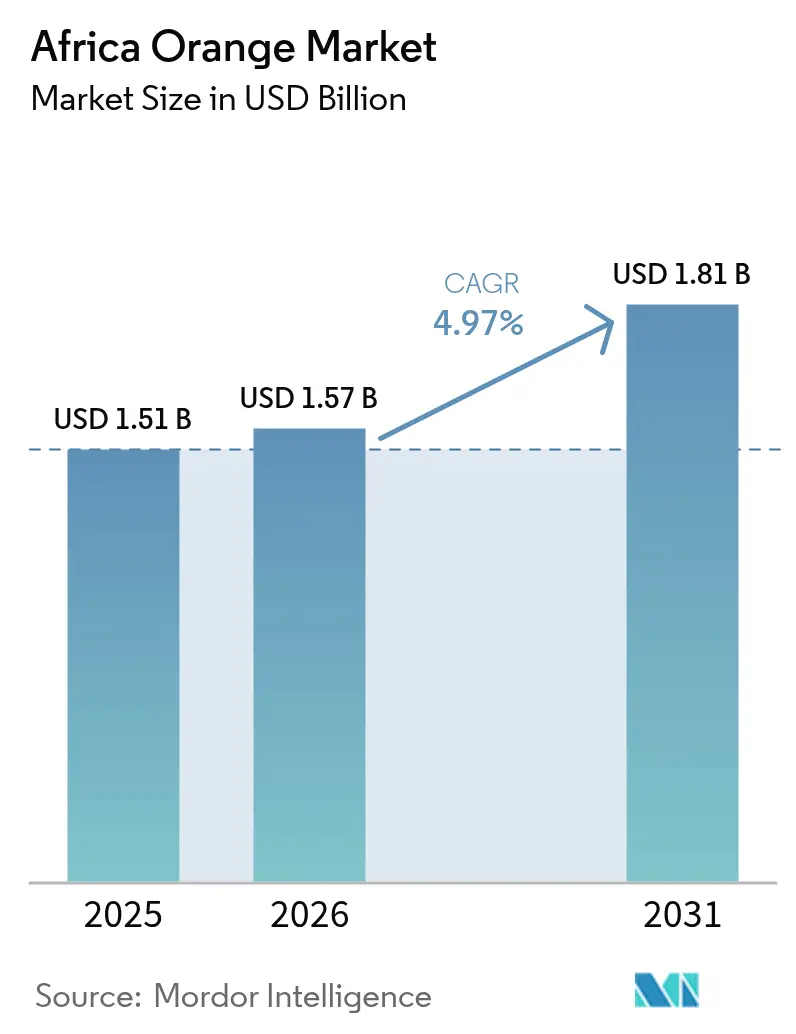

The Africa orange market size was valued at USD 1.51 billion in 2025 and estimated to grow from USD 1.57 billion in 2026 to reach USD 1.81 billion by 2031, at a CAGR of 4.97% during the forecast period (2026-2031). Rising global orange-juice prices, irrigation upgrades in Egypt and Morocco, and expanding supermarket penetration across urban hubs are supporting the steady advance of the Africa orange market. Valencia cultivars dominate both juice processing and fresh export channels, yet blood oranges are capturing premium shelf space as retailers differentiate their assortments. Government incentives for climate-smart irrigation and processing investments are improving yield stability and value capture, while phytosanitary barriers and load-shedding remain prominent operational challenges.

Key Report Takeaways

- By geography, Egypt led with 43.5% of Africa orange market share in 2025, and Morocco is the fastest-growing country at a 6.8% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Orange Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-smart irrigation scale-up | +0.8% | Egypt, and Morocco | Medium term (2-4 years) |

| Record-high global orange-juice prices lifting farm-gate margins | +1.2% | South Africa, Egypt, and Morocco | Short term (≤ 2 years) |

| New China-Africa cold-treatment protocol | +0.5% | Morocco, and South Africa | Medium term (2-4 years) |

| Emergence of pan-African commodity exchanges | +0.3% | Kenya, Ethiopia, and Nigeria | Long term (≥ 4 years) |

| Adoption of high-yield Valencia Late cultivars | +0.6% | South Africa, and Morocco | Medium term (2-4 years) |

| On-farm solar micro-grids reducing post-harvest losses | +0.4% | Ethiopia, Kenya, rural South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Climate-Smart Irrigation Scale-Up

Egypt and Morocco are equipping thousands of hectares with subsidized drip systems that lift per-hectare yields by up to 20%, reduce water stress, and support export-grade sizing. Morocco’s 2024/25 orange crop rose 17% year on year to 960,000 metric tons as drip adoption widened[1]Source: United States Department of Agriculture Foreign Agricultural Service, “Morocco: Citrus Annual,” fas.usda.gov. In Egypt's Noubaria reclamation zone, Magrabi Agriculture manages 3,360 hectares of integrated citrus farms, utilizing centralized drip irrigation systems and tissue-culture propagation to ensure export-grade quality. In Morocco, the government provides per-hectare aggregation incentives, ranging from USD 75 for large conventional growers to USD 300 for small organic farms, promoting technology adoption among smallholders.

Record-High Global Orange-Juice Prices Lifting Farm-Gate Margins

Orange juice futures exceeded USD 4,200 per ton in 2024, keeping February 2026 prices significantly above the five-year average and increasing African farm-gate returns by (15-20%). Production shortfalls in Brazil and Florida, caused by citrus greening and hurricane damage, tightened the global concentrate supply and directly impacted price signals for African growers. Egyptian exporters, including Wadi El Nour, noted that overproduction during the 2023/24 season had lowered prices. The 2024/25 season experienced improved profitability as government subsidy reductions phased out less efficient operators, while demand from Russia, Saudi Arabia, and Brazil strengthened.

New China-Africa Cold-Treatment Protocol

Morocco, Egypt, and South Africa now access Chinese ports under harmonized cold-treatment rules that lower rejection risk, supporting diversification away from the European Union. The Standards and Trade Development Facility established COMESA-wide standard operating procedures for citrus phytosanitary inspections in 2024, standardizing protocols across member states and minimizing border delays. This regulatory alignment is especially beneficial for Morocco, which encounters early-season competition from Chilean mandarins and relies on reliability and traceability to achieve premium pricing in the Shanghai and Guangzhou distribution hubs.

Emergence of Pan-African Commodity Exchanges

Platforms like AFEX and the Ethiopian Commodity Exchange are testing citrus forward contracts to provide transparent price discovery for smallholders not integrated into supermarket supply chains. These platforms are particularly significant for smallholders excluded from supermarket procurement systems, which increasingly require consistent year-round supply, strict food safety certifications, and centralized distribution. According to the United Nations Conference on Trade and Development (UNCTAD) report on supermarket supply chains in sub-Saharan Africa, major South African retailers such as Shoprite and Pick 'n Pay source over 90% of their fresh produce from commercial producers. As a result, smallholders often rely on brokers or local wholesale markets unless they can aggregate their produce and obtain necessary certifications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Citrus greening spread beyond Limpopo | -0.9% | South Africa | Medium term (2-4 years) |

| Fertilizer-price pass-through on grower margins | -0.6% | Egypt, Morocco, and South Africa | Short term (≤ 2 years) |

| European Unipn CBS (citrus black-spot) phytosanitary barrier | -0.5% | South Africa | Short term (≤ 2 years) |

| Cold-chain power-supply volatility | -0.4% | South Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Citrus Greening Spread Beyond Limpopo

Huanglongbing, also known as citrus greening, has spread from South Africa's Limpopo province into Mpumalanga's orchards, posing a risk to the country's status as Africa's largest citrus exporter. South Africa's Department of Agriculture, Land Reform and Rural Development reported the detection of infected trees at multiple sites in Mpumalanga in 2024, leading to the implementation of mandatory removal protocols and the establishment of quarantine zones[2]Source: South African Government, “Inquiry makes recommendations to improve competition in fresh produce market,” sanews.gov.za. According to the Citrus Growers' Association, an uncontrolled spread could decrease export volumes by 15% to 20% over the next decade, threatening the industry's Vision 260 goal of achieving 260 million cartons by 2030.

Fertilizer-Price Pass-Through on Grower Margins

Urea and NPK values remain (20–25) over 2023 levels. Precision-agriculture tools and soil testing are mitigating some cost escalation, but squeezed margin effects persist. Morocco's fertilizer market, which relies heavily on imports, has experienced price volatility driven by global natural gas price fluctuations and geopolitical supply disruptions. In January 2025, South Africa's Competition Commission Fresh Produce Market Inquiry highlighted high fertilizer and seed costs as structural barriers for small-scale and historically disadvantaged farmers, restricting their access to formal retail and export markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Egypt commanded 43.5% of Africa orange market share in 2025, with output of about 3.7 million metric tons and exports above 1.8 million metric tons. Alternate-bearing and heatwave stress trimmed 2024/25 yields by (10–15%), yet drip-irrigation upgrades and a USD 300 million processing complex in Sadat City will absorb more Valencia flow, easing export price swings. Export incentives are tapering, prioritizing quality over volume, an approach that aligns with premium market expectations and sustains Egypt’s anchor role in the Africa orange market[3]Source: Elsewedy Industrial Development, “Middle East’s largest agricultural food industries complex,” elsewedyelectric.com.

Morocco is the fastest-growing geography at 6.8% CAGR through 2031, propelled by Souss-Massa irrigation expansion, MAD 1,000 (USD 100) per metric tons export subsidies, and Valencia Late cultivation aimed at the European shoulder season. Production reached 960,000 metric tons in 2024/25, up 17% year on year, though water scarcity remains a structural threat. Solar farms, desalination, and wastewater projects are cushioning the effects of drought and ensuring that Africa's orange market supply from Morocco maintains quality standards even in dry years.

South Africa faces infrastructure challenges, but continues to be a major global citrus exporter. Hapag-Lloyd's service expansion at Cape Town aims to reduce berthing times, while bilateral agreements with Vietnam and China help mitigate destination risks. The proposed hydrogen bunkering at Port Elizabeth has the potential to reduce reefer emissions, supporting exporters in complying with the upcoming Europe Union Carbon Border Adjustment Mechanisms (CBAMs).

Competitive Landscape

Three established exporters, Capespan Group, Sundays River Citrus Company, and Elwadi Export Company, control the largest share of container traffic to Europe, the Middle East, and Asia, giving the Africa orange market a moderate concentration profile. Sundays River Citrus Company, representing 120 growers, shipped 8.5 million cartons in 2025, 70% of which went offshore. Capespan’s multi-continent sourcing smooths retailer supply gaps, and its precision-agriculture support tools help growers manage fertilizer and water constraints. Elwadi specializes in high-brix Valencia loads for juice and fresh channels across the Gulf.

Elsewedy and MAFI’s USD 300 million concentrate complex marks a pivot toward value capture through processing. Digital platforms such as AWASAM are aggregating Kenyan and Tanzanian growers, providing access to European buyers and shrinking brokerage spreads. Hazard Analysis Critical Control Points (HACCP) certifications have become baseline entry tickets, compelling mid-tier producers to invest in traceability and cold-chain upgrades. The Africa orange industry is also witnessing rising solar adoption at packhouses, pairing carbon reduction with energy security and sharpening competitive differentiation.

Intra-African trade remains under-exploited, the African Continental Free Trade Area could unlock non-tariff savings and encourage varietal specialization. Smaller cooperatives in Ethiopia and Nigeria are leveraging donor-funded irrigation and certification projects to break into regional supermarket chains, introducing fresh competition at the lower end of the Africa orange market.

Recent Industry Developments

- June 2025: Food and Agriculture Organization of the United Nations (FAO) and the International Plant Protection Convention (IPPC), in collaboration with the Government of South Africa, represented by the Department of Agriculture, launched the second phase of the Africa Phytosanitary Programme (APP). This initiative aims to prevent the spread of plant pests and diseases in Africa by leveraging advanced digital tools, with a focus on citrus crops, including oranges.

- May 2025: Moroccan government implemented a subsidy plan aimed at enhancing exports of fresh citrus fruits in response to growing competition from Egypt and other suppliers. This plan, applicable to all varieties except Nadorcott mandarins, establishes a financial support framework for a five-year period from 2024 to 2028. It offers a subsidy of MAD 1,000 (USD 109.59) per metric ton for fresh citrus exports to the European Union, the United Kingdom, and African countries.

- March 2025: Morocco completed its first citrus shipment to Japan, representing a significant expansion into Asian markets. This development followed extensive negotiations and aligns with Morocco's strategy to expand beyond its traditional European export markets.

Africa Orange Market Report Scope

Oranges, with their yellowish to reddish-orange rind, are round, juicy citrus fruits enjoyed worldwide. The Africa Orange Market Report is Segmented by Geography (Egypt, Morocco, and South Africa). The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Import Analysis (Value and Volume), Export Analysis (Value and Volume), Wholesale Price Trend Analysis and Forecast, List of Key Players, and More. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

By Geography

| Egypt | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | |

| Key Supplying Markets | |||

| Export Market Analysis | Export Value and Volume | ||

| Key Destination Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| Logistic and Infrastructure | |||

| Seasonality Analysis | |||

| Morocco | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destination Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| Logistic and Infrastructure | |||

| Seasonality Analysis | |||

| South Africa | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destination Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| Logistic and Infrastructure | |||

| Seasonality Analysis | |||

| By Geography | Egypt | Production Analysis | Production Volume | |

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | ||

| Key Supplying Markets | ||||

| Export Market Analysis | Export Value and Volume | |||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| Logistic and Infrastructure | ||||

| Seasonality Analysis | ||||

| Morocco | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| Logistic and Infrastructure | ||||

| Seasonality Analysis | ||||

| South Africa | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| Logistic and Infrastructure | ||||

| Seasonality Analysis | ||||

Key Questions Answered in the Report

How large is the Africa orange market in 2026?

Africa orange market reached USD 1.57 billion 2026 to reach USD 1.81 billion by 2031, at a CAGR of 4.97% during the forecast period (2026-2031).

Which variety accounts for the largest share of African orange sales?

Valencia oranges led with 37.8% share in 2025, serving both fresh and juice channels.

Which country is growing fastest in African orange production?

Morocco is advancing at a 6.8% CAGR through 2031, supported by irrigation and subsidies.

How are supermarkets influencing African orange distribution?

Modern Retail channels are gaining share at 6.8% CAGR as urban consumers favor certified, pre-packed fruit.

What is a major threat to long-term South African orange exports?

The spread of citrus greening from Limpopo into Mpumalanga endangers yield stability and could trim exports by up to 20% over the next decade.

Page last updated on: