Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 17.15 Billion |

| Market Size (2031) | USD 21.55 Billion |

| Growth Rate (2026 - 2031) | 4.68% CAGR |

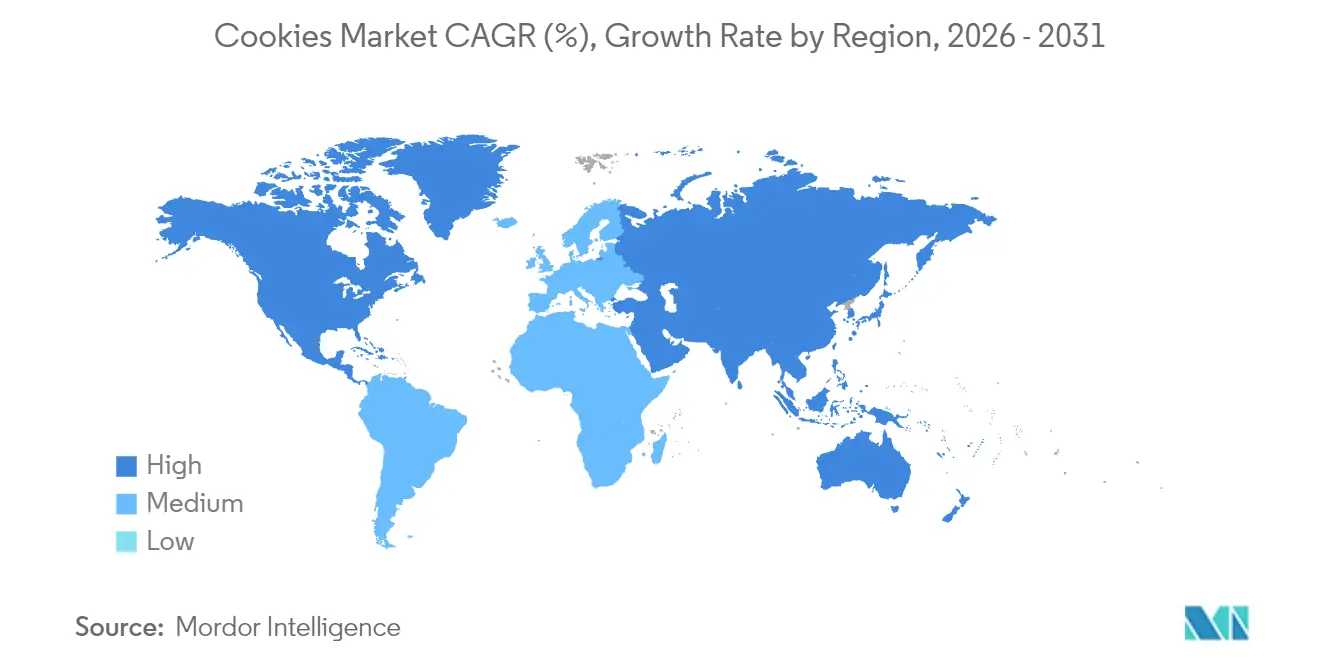

| Fastest Growing Market | South America |

| Largest Market | Europe |

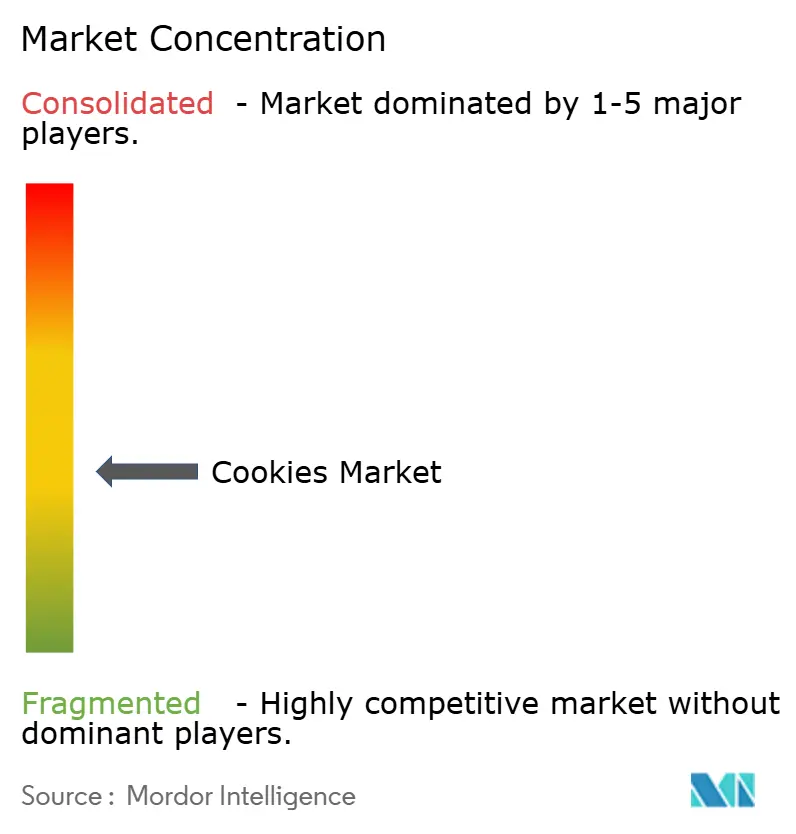

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cookies Market Analysis by Mordor Intelligence

The cookies market size was valued at USD 16.38 billion in 2025 and estimated to grow from USD 17.15 billion in 2026 to reach USD 21.55 billion by 2031, at a CAGR of 4.68% during the forecast period (2026-2031). Growth rests on steady snacking demand, a pivot to premium lines, and health-focused reformulations that keep indulgence relevant while aligning with new labeling rules fda.gov. Conventional formats still dominate sales, yet portion-controlled, fortified, and plant-based varieties capture incremental value that lifts the overall cookies market despite raw-material inflation. Digital commerce, especially brand-run subscription programs, deepens consumer reach and offsets shelf-space limits in modern retail. Meanwhile, strategic mergers signal the need for scale to absorb higher compliance costs and volatile ingredient pricing.

Key Report Takeaways

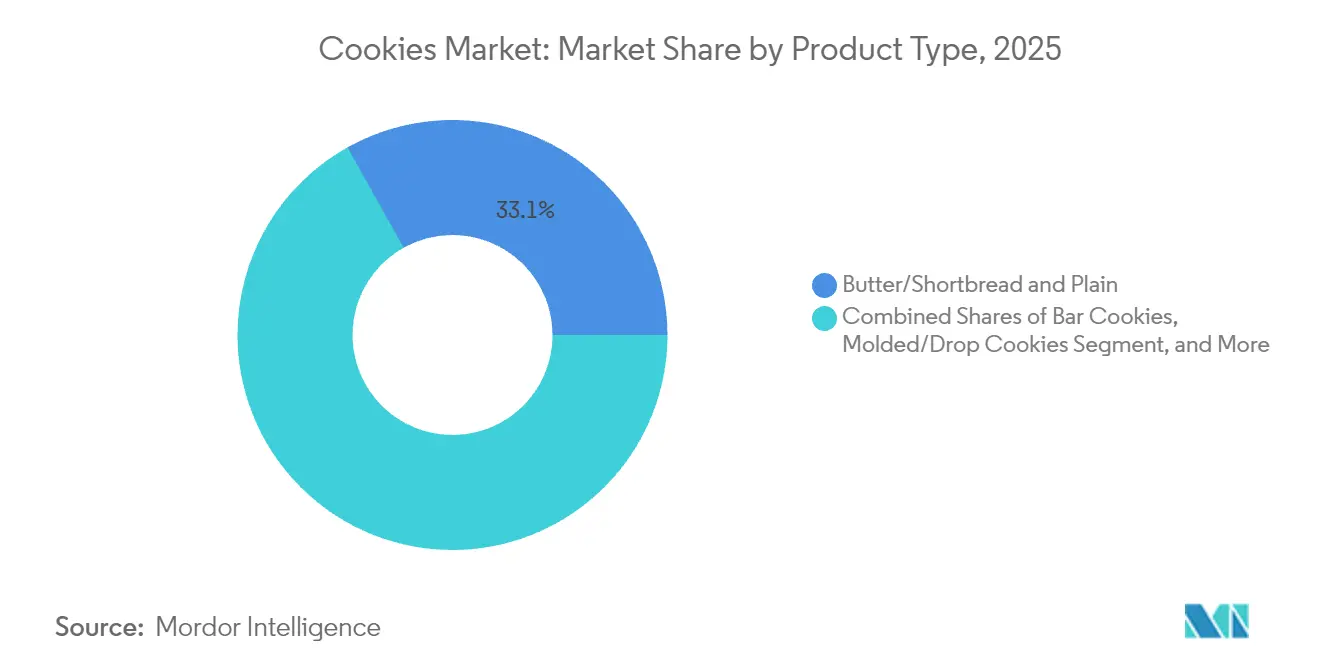

- By product type, butter/shortbread and plain lines led with 33.12% market share in 2025, while bar cookies are forecast to grow at 5.85% CAGR to 2031.

- By category, the conventional segment held 91.70% of 2025 shares; the free-from segment is predicted to expand at 6.55% CAGR through 2031.

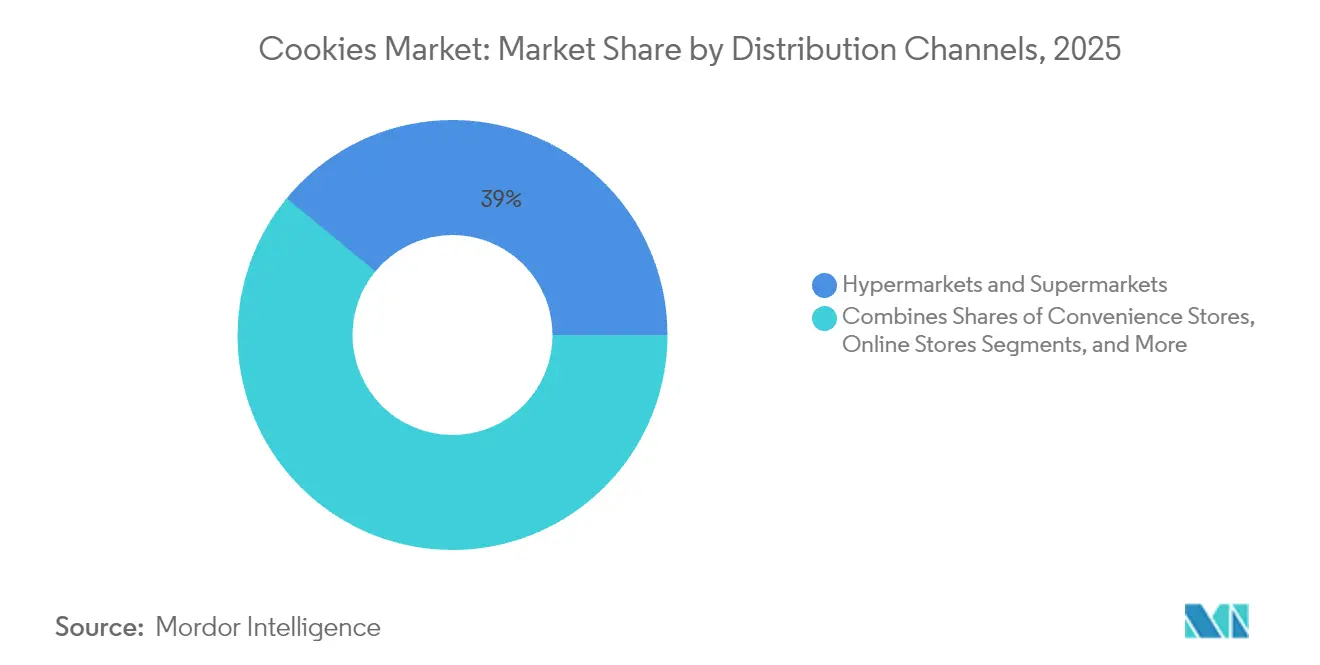

- By distribution channel, hypermarkets and supermarkets captured 39.02% share in 2025, whereas online retail is expected to post a 6.46% CAGR.

- By packaging format, pouches and sachets accounted for 62.95% of the 2025 share, and cartons are anticipated to register a 5.74% CAGR.

- By geography, Europe contributed 29.85% of the 2025 market share, while South America is projected to achieve a 6.63% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cookies Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Portion-Controlled Indulgence Snacks | +0.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Accelerated Urban On-the-Go Breakfast Culture in Metropolitan Hubs | +0.6% | Asia-Pacific core, spill-over to Latin America | Short term (≤ 2 years) |

| Fortification and Nutrient Enhancement Drive Cookies Market Growth | +0.5% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Plant-Based Fat Reformulation Driving Growth | +0.4% | Europe and North America, early adoption in urban APAC | Medium term (2-4 years) |

| Direct-to-Consumer Subscription Surge for Gourmet Cookies | +0.3% | North America and Europe, emerging in urban Asia | Short term (≤ 2 years) |

| Gifting and Premiumization as Emotional Positioning | +0.3% | Global, with emphasis on Asia-Pacific and the Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Portion-Controlled Indulgence Snacks

Consumer behavior analysis reveals a strategic shift toward portion-controlled indulgence as health-conscious consumers seek guilt-free satisfaction without complete category abandonment. This trend manifests in the rapid expansion of single-serve packaging formats and mini-cookie varieties that allow controlled consumption while maintaining the emotional satisfaction associated with cookie consumption. The FDA's[1]Food and Drug Administration, "FDA Finalizes Updated 'Healthy' Nutrient Content Claim", www.fda.gov new "healthy" food labeling rules, effective February 2028, will require foods to meet specific criteria for food group equivalents and limits on saturated fat, sodium, and added sugars, compelling manufacturers to reformulate products for smaller portion sizes that meet regulatory thresholds. Major food companies report that portion-controlled products command premium pricing while reducing per-unit ingredient costs, creating favorable margin dynamics that support sustained investment in this segment. The trend particularly resonates with millennial and Gen Z consumers who prioritize mindful eating practices while maintaining lifestyle flexibility.

Accelerated Urban On-the-Go Breakfast Culture in Metropolitan Hubs

Metropolitan lifestyle evolution drives fundamental changes in breakfast consumption patterns, with traditional sit-down meals increasingly replaced by portable, convenient options that fit compressed morning schedules. This transformation particularly impacts Asia-Pacific markets, where rapid urbanization and extended commuting times create demand for grab-and-go breakfast solutions that provide sustained energy and satisfaction. Cookies positioned as breakfast alternatives benefit from this trend, especially varieties fortified with proteins, fibers, and essential nutrients that address nutritional concerns while maintaining convenience. The phenomenon extends beyond traditional breakfast cookies to include premium artisanal varieties that serve as meal replacements for time-constrained professionals. The market players are launching new breakfast cookies in the market, owing to the rising demand across the world. For instance, in January 2024, Olyra Foods introduced fruit-filled breakfast biscuits. The soft-baked snacks contain ancient Greek grains and are available in strawberry and raspberry flavors. The products feature high fiber content and low sugar levels.

Fortification and Nutrient Enhancement Drive Cookies Market Growth

Nutritional fortification represents a strategic response to consumer demands for functional foods that deliver health benefits beyond basic sustenance, transforming cookies from indulgent treats to purposeful nutrition vehicles. This trend gains momentum as manufacturers incorporate proteins, vitamins, minerals, probiotics, and plant-based nutrients into traditional cookie formulations without compromising taste or texture characteristics. Advanced food technology enables seamless integration of functional ingredients, allowing manufacturers to address specific consumer segments such as children's nutrition, senior health, and athletic performance. The fortification trend particularly benefits, as manufacturers combine allergen-free formulations with nutritional enhancement to create differentiated products that command premium pricing. Success in this space requires sophisticated supply chain management and quality control systems to ensure consistent nutrient delivery while maintaining shelf stability and sensory appeal.

Gifting and Premiumization as Emotional Positioning

Cookie gifting culture expands beyond traditional holiday seasons to encompass year-round occasions, corporate gifting, and personal celebration markets that value premium packaging, unique flavors, and artisanal presentation. The premiumization strategy enables manufacturers to capture higher margins while building brand equity through association with special occasions and thoughtful gestures. Success in gifting markets requires a comprehensive understanding of cultural preferences, seasonal patterns, and presentation standards that vary significantly across geographic markets. The trend particularly benefits established brands with heritage positioning and newer artisanal brands that emphasize craftsmanship and unique flavor profiles. Gifting market development requires specialized distribution channels, including corporate sales teams, online gifting platforms, and partnerships with complementary luxury brands that share similar target demographics. In November 2024, La Monarca Bakery introduced a new collection of Mexican cookies. The assortment features six varieties: wedding cookies, cinnamon cookies, butter cookies, Polvorones, Orejitos, and chocolate butter cookies.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Price Volatility Affecting Cookie Margins | -0.7% | Global, with acute impact in emerging markets | Short term (≤ 2 years) |

| Stricter HFSS Labeling Hindering Growth | -0.5% | Europe and UK core, expanding to other developed markets | Medium term (2-4 years) |

| Stringent Food Safety Regulations | -0.3% | Global, with varying compliance costs by region | Long term (≥ 4 years) |

| Competition from Alternative Snacks | -0.4% | Global, with intensity in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility Affecting Cookie Margins

Commodity price instability creates sustained margin pressure as key ingredients experience significant cost fluctuations that manufacturers struggle to pass through to consumers without damaging volume performance. Cocoa prices surged 35% between 2021 and 2023, while sugar costs increased 33% during the same period, creating input cost inflation that outpaced consumer price acceptance in many markets, according to the World Bank[2]World Bank, “Commodity Markets Outlook,” worldbank.org. General Mills reported input cost inflation of 3-4% for fiscal 2025, necessitating cost savings initiatives of 4-5% of cost of goods sold to maintain profitability. The volatility particularly impacts smaller manufacturers who lack hedging capabilities and supply chain scale to absorb cost fluctuations, potentially accelerating market consolidation as companies seek operational efficiencies through merger and acquisition activities. Agricultural commodity markets face additional pressure from geopolitical tensions, climate change impacts, and biofuel demand that competes with food applications, suggesting sustained volatility rather than temporary disruption.

Stricter HFSS Labeling Hindering Growth

High-fat, sugar, and salt labeling regulations create formulation challenges and marketing restrictions that limit growth opportunities for traditional cookie products, particularly in European markets where obesity prevention policies drive increasingly stringent requirements. The UK government's [3]UK Government, “National Food Strategy Policy Paper,” gov.ukcomprehensive food strategy emphasizes reshaping food environments through advertising restrictions on HFSS products, mandatory nutrition labeling, and support for healthier alternatives. These regulations force manufacturers to choose between reformulation costs that may compromise taste and texture characteristics or accept marketing limitations that restrict promotional activities and retail placement opportunities. The regulatory trend extends beyond Europe as other developed markets consider similar measures, creating compliance complexity for multinational manufacturers who must manage different standards across markets. Front-of-package nutrition labeling requirements, as proposed by the FDA, will further increase transparency around nutritional content, potentially influencing consumer purchasing decisions away from traditional cookie formulations toward healthier alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Butter/Shortbread and Plain Cookies Dominates the Market

Butter/shortbread and plain cookies maintain market leadership with 33.12% share in 2025, reflecting consumer preference for familiar flavors and textures that deliver consistent satisfaction across diverse demographic segments. However, bar cookies emerge as the fastest-growing segment at 5.85% CAGR through 2031, driven by portion-control trends and nutritional transparency that aligns with health-conscious consumption patterns. This growth trajectory suggests fundamental shifts in consumer expectations, where convenience and nutritional awareness increasingly influence purchasing decisions over traditional taste preferences alone.

The molded/drop cookies segment benefits from manufacturing efficiency and flavor versatility, enabling cost-effective production of diverse varieties that appeal to different taste preferences and dietary requirements. Sandwiches and cream-filled cookies maintain steady performance through premium positioning and indulgent positioning that appeals to treat-seeking consumers, while wafer and rolled cookies capture niche markets through unique textures and premium ingredients. The market players have been innovating new types of cookies in the market. For instance, in March 2025, NuStef Baking launched TeaFusions™ Waffle Cookies in four flavors: Chai Apple, Black Tea and Currant, Earl Grey and Passion Fruit, and White Tea and Peach.

By Category: Free-From Segment Accelerates Despite Conventional Dominance

The conventional cookie category commands overwhelming market dominance at 91.70% share in 2025, reflecting mainstream consumer preferences and established manufacturing infrastructure that supports cost-effective production and distribution. Despite this dominance, the free-from segment accelerates at 6.55% CAGR through 2031, indicating substantial growth opportunities for manufacturers willing to invest in specialized formulations and supply chain capabilities. This growth disparity suggests market bifurcation, where conventional products serve mass-market needs while free-from varieties capture premium segments with specific dietary requirements or lifestyle preferences.

Free-from product development requires sophisticated ingredient sourcing and manufacturing processes to achieve acceptable taste, texture, and shelf life characteristics without traditional binding agents, flavor enhancers, and preservatives. The segment benefits from increasing awareness of food allergies, dietary restrictions, and lifestyle choices such as veganism that drive demand for specialized products. Success in free-from categories demands premium pricing strategies to offset higher ingredient and processing costs, while building consumer education and trust around product quality and nutritional benefits. The EU's regulation on contaminant levels in food, including cookies, emphasizes strict standards to protect vulnerable populations, creating additional compliance requirements that benefit established manufacturers with robust quality control systems

By Distribution Channel: E-commerce Disrupts Traditional Retail Patterns

Hypermarkets and supermarkets retain distribution leadership with a 39.02% share in 2025, leveraging extensive geographic coverage, promotional capabilities, and consumer shopping habits that favor one-stop shopping experiences for household staples, including cookies. However, online retail emerges as the fastest-growing channel at 6.46% CAGR through 2031, reflecting accelerated e-commerce adoption and direct-to-consumer strategies that enable brands to capture higher margins while building direct customer relationships. This channel evolution creates opportunities for both established brands seeking margin enhancement and emerging brands lacking traditional retail access.

Convenience stores maintain steady performance through impulse purchasing and location advantages near transportation hubs, offices, and residential areas where consumers seek immediate satisfaction and portion-controlled options. Specialist retailers serve niche markets through curated product selections and expert knowledge that appeal to premium and artisanal cookie segments, while other distribution channels encompass foodservice, vending, and institutional sales that provide volume opportunities with different margin structures. The shift toward online retail requires sophisticated fulfillment capabilities, packaging innovations for shipping protection, and digital marketing expertise that traditional manufacturers must develop or acquire through partnerships.

By Packaging Type: Sustainability Drives Format Innovation

Pouches and sachets dominate packaging preferences with a 62.95% share in 2025, reflecting consumer demand for convenience, portion control, and product freshness that these formats deliver effectively across diverse consumption occasions. The format particularly benefits from manufacturing efficiency and supply chain optimization that enables cost-effective production and distribution while maintaining product quality during extended shelf life periods. However, cartons experience the fastest growth at 5.74% CAGR through 2031, driven by sustainability concerns, gifting applications, and premium positioning that justify higher packaging costs through enhanced consumer experience.

The packaging evolution reflects broader consumer trends toward environmental responsibility and premium experiences that extend beyond product quality to encompass entire brand interactions. Carton packaging enables sophisticated graphics, product protection, and unboxing experiences that support premium pricing and brand differentiation in competitive markets. The "others" packaging category encompasses innovative formats such as resealable containers, eco-friendly materials, and specialty gift packaging that serve niche markets with specific functional or aesthetic requirements. Success in packaging innovation requires balancing cost considerations with consumer preferences, regulatory requirements, and sustainability goals that increasingly influence purchasing decisions across demographic segments. General Mills' commitment to 100% recyclable or reusable packaging by 2030 demonstrates how sustainability initiatives drive packaging innovation while addressing consumer environmental concerns

Geography Analysis

Europe maintains market leadership with a 29.85% share in 2025, supported by established cookie consumption traditions, premium product positioning, and regulatory frameworks that emphasize quality over volume growth. The region benefits from diverse national preferences that create opportunities for both local specialties and international brands, while sophisticated retail infrastructure and high disposable incomes support premium pricing strategies. European manufacturers leverage heritage positioning and artisanal craftsmanship to differentiate products in competitive markets, while regulatory compliance capabilities provide advantages in export markets with similar quality standards. The region's mature market characteristics drive innovation toward health-conscious formulations and sustainable packaging that align with consumer environmental awareness and dietary preferences.

South America emerges as the primary growth engine at 6.63% CAGR through 2031, propelled by the rising consumer inclination towards healthy snacking. Consumers are seeking flavorful cookies. Additionally, the market players are expanding their market reach through various strategies like expansions, acquisitions, and others. For instance, in August 2023, Nestle invested USD 550.8 million in its cookies and confectionery manufacturing in Brazil. In Asia-Pacific, China and India represent particularly significant opportunities, with expanding middle-class populations and increasing exposure to international food brands through travel and digital media.

North America faces mature market dynamics with moderate growth expectations, as established consumption patterns and market saturation limit expansion opportunities compared to emerging regions. The market emphasizes innovation through health-conscious formulations, premium positioning, and direct-to-consumer channels that enable margin enhancement despite volume constraints. The Middle East and Africa are also showing mature growth in these regions, with regional and global players dominating the market. The market players are launching new products in the market to cater to the rising demand. For Instance, in June 2025, Ben's Cookies launched its mini versions in the United Arab Emirates. The products are available on Talabat.

Regulatory Landscape

Cookies manufacturers operate under tightening labeling and food-safety regimes that increasingly influence formulation and pack-claims strategy. In the United States, the FDA set a uniform compliance date of December 31, 2026, for food labeling regulations published between January 1, 2025, and December 31, 2026, creating a defined window for packaging artwork updates and coordinated SKU transitions across channels.

In Europe, Regulation (EU) No 1169/2011 continues to anchor mandatory consumer information and allergen labeling, with consolidated updates in April 2025 reinforcing the centrality of compliant ingredient, allergen, and nutrition communication for cross-border trade. At the global standard-setting level, the Codex Alimentarius Commission adopted new guidance on precautionary allergen labeling ("may contain") in July 2026, supporting movement toward more harmonized, risk-based approaches that can reduce label fragmentation for exporters and private label manufacturers serving multiple geographies.

Value Chain Analysis

The cookies value chain starts with agricultural and commodity inputs (wheat flour, sugar, vegetable fats such as palm oil, cocoa, eggs, and dairy ingredients), followed by formulation and processing (mixing, sheeting/molding, baking, cooling), and then packaging, warehousing, and distribution through modern trade, convenience, specialist retail, and online retail. Volatility in core inputs and contracting complexity (notably for chocolate and eggs during 2024 to early 2025) places emphasis on procurement scale, multi-origin sourcing, and quality assurance to maintain consistent taste, texture, and costs across high-volume core lines and premium or better-for-you SKUs.

Downstream, packaging choice and fulfillment capability shape margin delivery and channel reach, particularly as pouches/sachets dominate volume formats while cartons gain relevance for premiumization and gifting. As labeling and allergen controls tighten, manufacturers increasingly depend on end-to-end traceability, supplier documentation, and robust change-control between ingredient suppliers, co-manufacturers, and brand owners to support claims (free-from, reduced sugar) and to manage cross-contact risk in shared facilities.

Competitive Landscape

The cookies market exhibits moderate concentration, characterized by a mix of global conglomerates and strong regional players competing across price tiers and product categories. Strategic patterns reveal an increasing focus on premium positioning and health-oriented innovations, with major players like Mondelēz, Nestlé, and Ferrero expanding their portfolios through both organic development and strategic partnerships.

White-space opportunities exist in the convergence of indulgence and health, particularly products that deliver premium taste experiences with improved nutritional profiles or functional benefits. Emerging disruptors are gaining traction through direct-to-consumer models that bypass traditional retail gatekeepers, allowing for higher margins and direct customer relationships that inform rapid product innovation.

Technology is increasingly deployed as a competitive advantage, with leading manufacturers investing in digital marketing, e-commerce capabilities, and data analytics to understand and respond to shifting consumer preferences. The competitive intensity is heightened by the entry of private equity firms into the sector, which are investing in niche brands and enhancing their distribution and market reach, creating additional pressure on established players to innovate and differentiate.

Cookies Industry Leaders

-

Mondelēz International, Inc.

-

Ferrero International S.A.

-

Britannia Industries Ltd.

-

Grupo Bimbo S.A.B. de C.V.

-

General Mills Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity expansion and localization programs create whitespace for both global and regional players to shorten lead times, support rapid innovation cycles, and protect margins amid input volatility. In June 2026, Bauducco opened its largest US production facility in Zephyrhills, Florida (160,000 sq ft, designed for phased expansion), while Grupo La Moderna began construction of a USD 40 million cookie factory in Irapuato, Mexico, tied to Bajio-region wheat supply chains. In Europe, Lotus Bakeries started building a high-capacity production hall at Lembeke, Belgium (May 2026), and Ferrero announced a EUR 60 million upgrade program in France, including a dedicated Nutella Cookies line at the Nieppe plant (June 2026), signaling sustained investment behind branded cookie/biscuit platforms.

Product and ingredient innovation is increasingly framed around benefit-defined claims and compliance-ready reformulation rather than flavor-only novelty. FDA nutrient-claim modernization (with the updated "healthy" claim effective February 2028, per the report context) and wider HFSS-style pressures in developed markets reinforce opportunities in portion-controlled formats, reduced-sugar recipes, and fortified or free-from cookies that can maintain indulgence cues. Supplier-side programs and solutions, such as Puratos highlighting a "beyond clean label" approach at IDDBA 2026 (including fermentation-based ingredients and sustainability programs like Cacao-Trace), also expand the toolkit for brands targeting premiumization with cleaner ingredient decks and traceable sourcing.

Recent Industry Developments

- June 2026: Mondelz International announced the global launch of limited-edition OREO & BTS Cookies across 80+ markets, featuring a brown sugar pancake flavor inspired by Korean street food. The rollout demonstrates how large brands use entertainment collaborations to drive short-cycle demand spikes and secure incremental shelf and digital visibility across regions.

- November 2025: Mondelz International began local manufacturing and commercial launch of Lotus Biscoff cookies in India, offering packs starting at INR 10. Local production supports broader distribution and sharper price architecture, enabling mass-premium penetration for an imported-origin brand.

- October 2024: Zydus Wellness expanded Sugar Free into packaged foods by launching Sugar Free D'lite cookies positioned around no added sugar. The move widens competition in the better-for-you segment and increases shelf presence for no added sugar options.

Research Methodology Framework and Report Scope

Market Definition and Coverage

We define the cookies market as the value of cookies sold to end users through retail and similar channels, counted in USD, across major consuming regions, and covering everyday and specialty cookie formats.

Scope exclusions: This sizing excludes in-store bakery desserts sold as unpackaged items and non-cookie sweet snacks where cookies are not the primary product form.

Segmentation Overview

-

By Product Type

- Bar Cookies

- Molded/Drop Cookies

- Sandwich and Cream-Filled Cookies

- Wafer and Rolled Cookies

- Butter/Shortbread and Plain

- Others (Macarons, Meringue, etc.)

-

By Category

- Conventional

- Free-From

-

By Distribution Channel

- Hypermarkets/Supermarkets

- Convenience Stores

- Specialist Retailers

- Online Retailers

- Other Distribution Channels

-

By Packaging Type

- Pouches, Sachets

- Cartons

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- France

- United Kingdom

- Netherlands

- Italy

- Sweden

- Poland

- Belgium

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

-

Middle East and Africa

- United Arab Emirates

- South africa

- Nigeria

- Saudi Arabia

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping how cookies are produced, traded, and consumed across key regions, so the market boundaries stayed consistent through the model. We relied on public datasets and references such as USDA and ERS food-related series, UN Comtrade trade codes for baked goods, FAOSTAT supply side indicators, and national statistics offices that publish household expenditure and CPI baskets.

After that, the desk phase was used to set initial ranges for category mix and pricing direction, using sources such as company annual reports, investor presentations, retailer news, and association or standards bodies that track packaged foods. Where needed, paid subscription coverage for company financials and intelligence, plus a shipment-level import and export database, helped sanity check smaller-country visibility. This source list is illustrative only, and many other references were also used for data collection, cross-checks, and clarifications.

Primary Interviews and Surveys

Primary work was used to test what desk data could not show clearly, for example how free-from positioning changes price realization and how online mix is shifting by region. We spoke with a range of manufacturers, distributors, and retail-facing specialists, and we also included packaging and ingredient perspectives so assumptions on pack sizes and cost pass-through could be checked across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 12% | APAC: 41% |

| Mid tier: 52% | Functional/Unit leaders: 43% | EMEA: 34% |

| Smaller Players: 16% | Managers: 45% | Americas: 25% |

Market-Sizing & Forecasting

Sizing was built using a top-down structure where packaged cookies demand was reconstructed from country-level consumption proxies, retail snack spending direction, and trade and production signals, then filtered through category splits. In parallel, we corroborated totals with selective bottom-up checks, like sampled brand and channel price points multiplied by plausible volumes. We then applied distributor and retailer sense checks, and adjusted where the ranges did not line up.

Key inputs used in the model included average selling price movement by pack format, the share shift between offline and online retail, the mix across cookie types (such as sandwich and cream-filled, wafer and rolled, and butter or shortbread styles), and the share of free-from products within the overall basket. Packaging cues (pouches, sachets, and cartons) were also used as a practical cross-check because they tie closely to typical pack sizes and price ladders. For forecasting, we used scenario analysis supported by variable-level expectations gathered in interviews, so near-term inflation and premiumization were separated from longer-run volume growth.

Data Validation & Update Cycle

Validation was done by checking whether final market totals stay consistent with independent signals, such as food CPI patterns, household snack expenditure direction, and trade balances for relevant baked goods categories. When unusual jumps appeared, they were reviewed, and assumptions were traced back to the input series. Follow-up questions were then raised with industry contacts before sign-off.

Each report goes through multi-step internal review so that scope, unit handling, and conversion logic are applied the same way across geographies. The study is refreshed annually, and interim updates are made when major events change pricing, distribution, or category mix. Before delivery, we run a final pass to ensure the latest public indicators are reflected in the numbers clients receive.

Mordor Intelligence's Cookies Market Estimate Compared With Other Published Estimates

Published market values for cookies can look far apart even when they are trying to describe the same industry, because the measurement choices are not the same. Differences usually come from what is counted as cookies versus adjacent baked snacks, how pricing is converted into USD, and how often assumptions are refreshed when inflation and pack sizes change.

In this study, the gap is often driven by refresh cadence and currency timing, because price ladders and exchange rates can swing the USD total quickly, and then that effect compounds over a forecast window, which is a discipline emphasized in Mordor Intelligence. Another common driver is ASP logic, where some estimates assume a single global price progression, even though premium formats and free-from products move differently by region and channel. Finally, validation checks vary, and totals can drift if they are not anchored back to consumption signals and channel mix shifts.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 17.15 B (2026) | |

| Global Consultancy A | USD 35.44 B (2024) | Uses an earlier base year and a broader value pool in practice, and the USD figure is more sensitive to the chosen currency conversion window and assumed global ASP progression. |

| Industry Research House B | USD 39.60 B (2023) | Anchors on a different historical base and can blend cookies with wider biscuit categories, which lifts the starting value and reduces transparency on pack-format level ASP and channel-mix adjustments. |

The comparison shows that the spread is less about math and more about boundary and timing choices that influence price and currency in USD terms. When scope is kept tight to cookies and the inputs are refreshed and cross-checked against channel and consumption signals, the resulting size is easier to follow and repeat using the same steps.

Key Questions Answered in the Report

What is the current value of the cookies market?

The cookies market stands at USD 17.15 billion in 2026.

How fast is the cookies market expected to grow?

It is forecast to expand at a 4.68% CAGR, reaching USD 21.55 billion by 2031.

Which product type has the highest cookies market share today?

Butter/shortbread and plain cookies lead with 33.12% share in 2025.

Which region offers the strongest growth prospects?

South America shows the highest regional CAGR at 6.63% through 2031.

Page last updated on: