Africa Heavy-duty Truck Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.73 Billion |

| Market Size (2026) | USD 2.85 Billion |

| Market Size (2031) | USD 3.52 Billion |

| Growth Rate (2026 - 2031) | 4.35% CAGR |

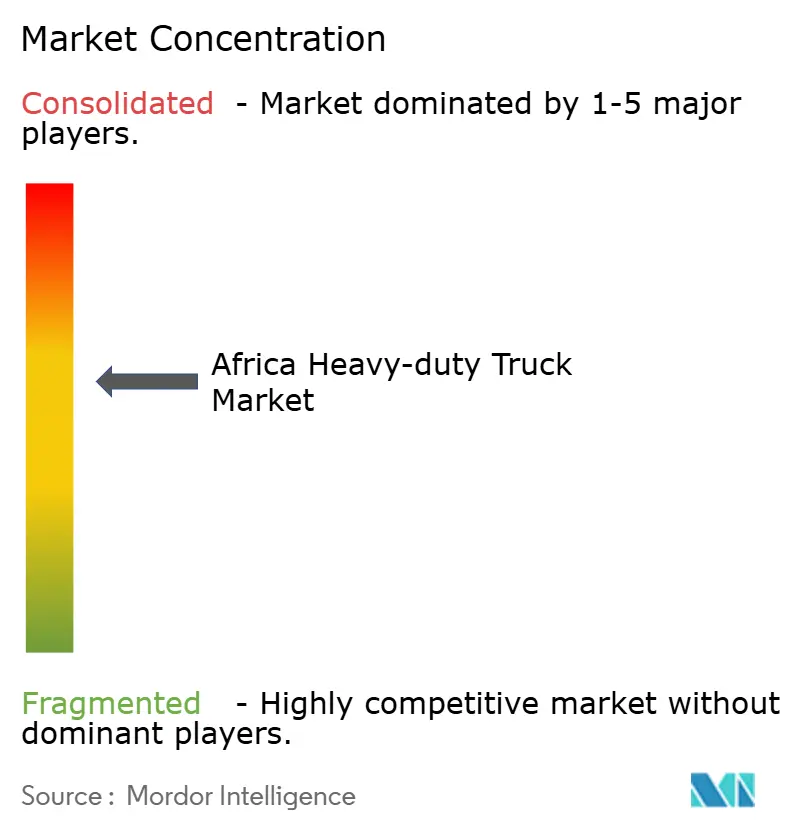

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Heavy-duty Truck Market Analysis by Mordor Intelligence

The Africa heavy-duty truck market size was valued at USD 2.73 billion in 2025 and estimated to grow from USD 2.85 billion in 2026 to reach USD 3.52 billion by 2031, at a CAGR of 4.35% during the forecast period (2026-2031). Infrastructure programs, e-commerce logistics, alternative-fuel incentives, and regional trade liberalization have shifted purchasing behaviour from ad-hoc replacement toward long-term capacity building. Operators are equipping fleets with telematics and fuel-flexible powertrains to offset high diesel prices while still meeting payload requirements. Localized Chinese CKD assembly has reduced landed costs and lowered the barrier to entry for small and mid-sized carriers. Meanwhile, fragmented road networks and foreign-exchange shortages weigh on maintenance budgets and parts availability. Despite these structural headwinds, the African heavy-duty truck market remains on a steady growth trajectory as sovereign corridors and mining projects expand freight volumes

Key Report Takeaways

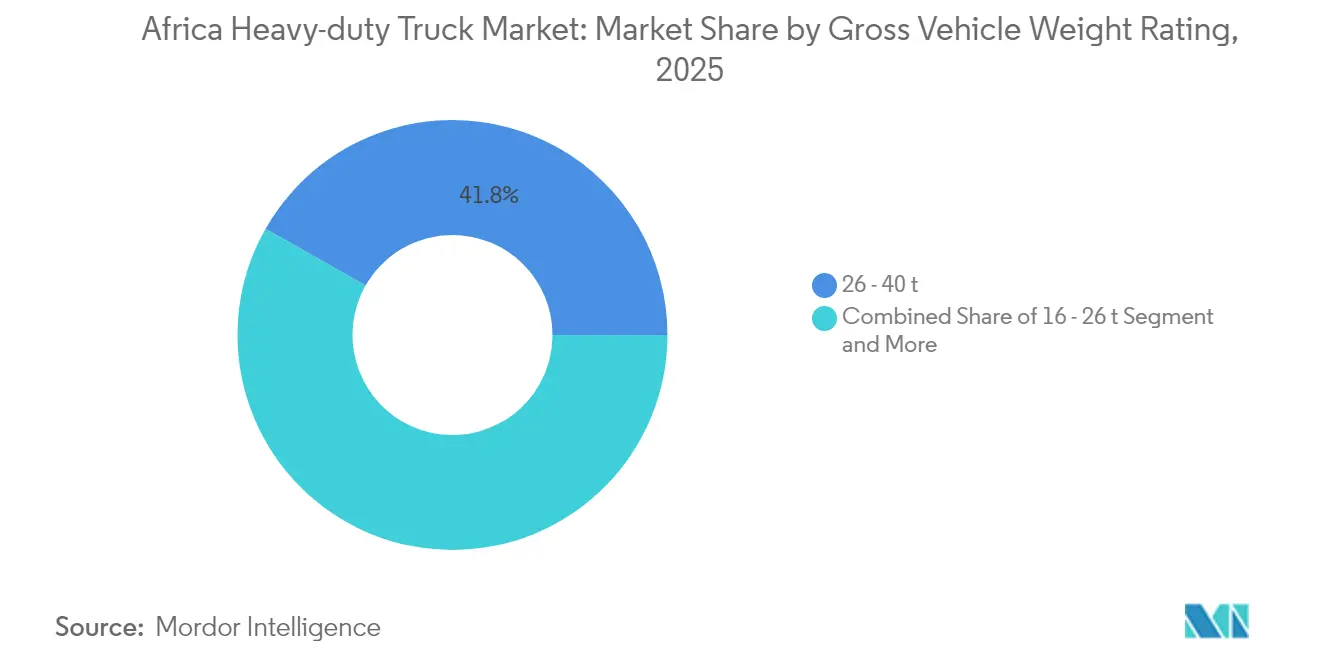

- By GVWR, the 26–40 ton segment accounted for 41.78% of the Africa heavy-duty truck market size in 2025; the >40 ton category is projected to grow at a 7.16% CAGR to 2031.

- By propulsion, internal-combustion engines captured 86.10% of the Africa heavy-duty truck market size in 2025, whereas electric trucks are set to expand at a 9.09% CAGR.

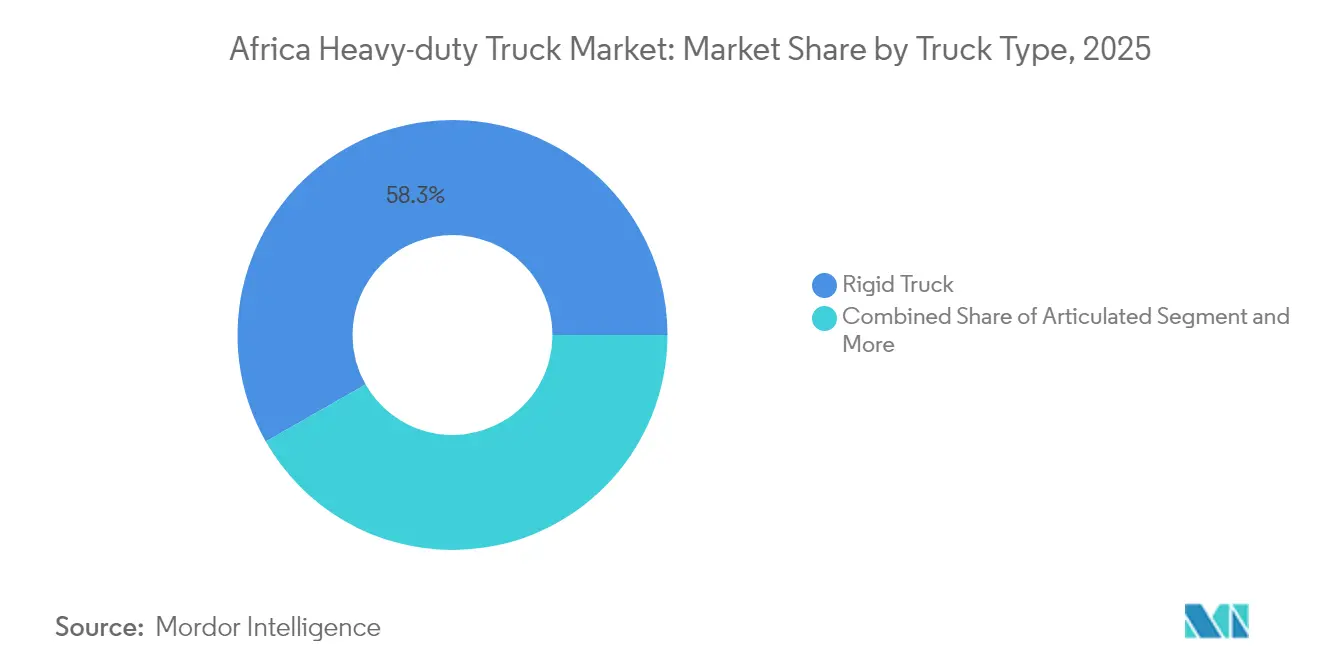

- By truck type, rigid trucks led with 58.25% revenue share in 2025; articulated units record the fastest 6.67% CAGR to 2031.

- By axle configuration, 6×4 models held 34.12% share in 2025, while 8×8 variants are growing at a 7.17% CAGR.

- By application, freight logistics represented 42.86% of the African heavy-duty truck market size in 2025, and mining is climbing at a 7.60% CAGR to 2031.

- By geography, South Africa held 31.02% of the Africa heavy-duty truck market share in 2025, while Zambia is advancing at a 6.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Proportional positioning is established by comparing regional contributions against the global total, including that of Africa. The heavy duty trucks market share in our global report expresses these relative weights.

Africa Heavy-duty Truck Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure Corridors | +1.2% | West & Southern Africa | Long term (≥ 4 years) |

| E-commerce Middle-Mile | +0.8% | Nigeria, Kenya, South Africa | Medium term (2-4 years) |

| Chinese CKD Cost Cuts | +0.7% | Nigeria, Ghana, Kenya, South Africa | Medium term (2-4 years) |

| Diesel-CNG Incentives | +0.6% | Nigeria, Egypt | Short term (≤ 2 years) |

| Euro VI Fleet Renewal | +0.4% | South Africa, wider SADC | Medium term (2-4 years) |

| Solar-Powered Mining Trucks | +0.3% | DRC, Zambia, South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pan-African Infrastructure Corridor Investments Drive Fleet Modernization

Projects such as the USD 15.6 billion West African Coastal Highway and the Lobito Corridor add high-quality pavement and intermodal linkages, prompting operators to procure heavier, more durable units suited to higher utilization rates[1]“West African Coastal Highway to Transform Trade,”, BBC, bbc.com. Rising corridor standards are also pushing manufacturers to design Africa-specific specifications that balance torque, suspension travel, and fuel efficiency across mixed surfaces[2]“Lobito Corridor as Catalyst for Growth,”, D+C Development and Cooperation, dandc.eu.

E-commerce Expansion Accelerates Middle-Mile Logistics Demand

Digital brokers like Kobo360 have lowered empty-mile ratios by matching loads in real time, cutting logistics costs that previously reached 50-75% of retail prices. The African Continental Free Trade Area removes tariff frictions and stimulates cross-border parcel flows, requiring trucks equipped with telematics and cold-chain add-ons for perishables[3]“AfCFTA Logistics Opportunities,”, International Finance Corporation, ifc.org. Egypt’s logistics pipeline underscores online retail spawning modern distribution hubs, favoring medium-range heavy trucks.

Localized Chinese CKD Assembly Lowers Landed Cost

Sinotruk’s USD 100 million Nigerian plant and FAW’s South African lines reduce import duties, shorten delivery lead times, and localize component sourcing, cutting retail prices by double digits. CKD output also creates local jobs, strengthening political support for further incentives that widen the buyer pool, especially among small hauliers previously priced out of new-build purchases.

Off-Grid Solar Micro-Grids Enable Electric Mining Trucks

Mining pits in DRC and Zambia deploy containerized solar arrays and lithium-ion storage to charge 100-ton electric haul trucks, trimming diesel logistics costs while meeting ESG targets[4]“Battery-Electric Mining Trucks for Africa,”, Liebherr Group, liebherr.com. Reduced ventilation needs in underground sites add another cost advantage, encouraging procurement of high-capacity battery trucks despite higher sticker prices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High TCO & Diesel | -1.8% | Nigeria, Ethiopia, Kenya | Short term (≤ 2 years) |

| Poor Rural Roads | -1.1% | Landlocked Sub-Saharan regions | Long term (≥ 4 years) |

| FX Parts Shortages | -0.7% | Nigeria, Ethiopia | Medium term (2-4 years) |

| Weak Grid for BEVs | -0.5% | Urban and mining hubs | Medium term (2-4 years |

| Source: Mordor Intelligence | |||

Elevated Total Cost of Ownership Constrains Fleet Expansion

Import duties in Nigeria climbed 40%, pushing heavy-truck landing prices past USD 1.1 million and stretching replacement cycles[5]“Import Duties Stifle Nigeria’s Truck Sector,”, ISS Africa, issafrica.org. Ethiopia’s tax bands of up to 500% on used units drive operators to refurbish ageing fleets rather than import newer, more efficient trucks. Currency volatility inflates loan servicing and spare-parts costs, forcing smaller carriers to prioritize liquidity over expansion.

Rural Road Infrastructure Deficiencies Limit Market Penetration

Sub-Saharan Africa averages 31 km of paved road per 100 km², with construction costing USD 300,000–1,000,000 per km [6]“Africa’s Road Investment Gap,”, Center for Global Development, cgdev.org. Poor surfaces boost transport costs to five times developed-market levels. Seasonal inaccessibility for 60% of rural residents cuts asset utilization and accelerates wear, compelling buyers to favor rugged, lower-capacity units that forgo sophisticated electronics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Gross Vehicle Weight Rating: Heavier Units Gain Momentum

The 26–40 ton band held a 41.78% share of the Africa heavy-duty truck market in 2025, reflecting its versatility for corridor freight and construction tasks. Mining-led demand is propelling the above 40-ton segment at a 7.16% CAGR, supported by corridor upgrades that allow denser axle loads.

Ultra-heavy orders are clustering around copper and cobalt pits in Zambia and the DRC, where solar-assisted electric drivelines lower lifetime fuel spend. Mid-weight units remain critical in West Africa, where bridge limits and axle taxes restrict super-heavy operations.

By Propulsion: ICE Rules, Electric Emerges

Internal-combustion engines commanded 86.10% of the Africa heavy-duty truck market in 2025 thanks to diesel’s ubiquity and a continent-wide repair ecosystem. Electric trucks, however, are registering 9.09% annual growth as mining companies adopt zero-emission haulage to satisfy offtaker ESG clauses.

Nigeria’s CNG incentive has spurred dual-fuel retrofits, while Ethiopia’s 2024 ban on new fossil-fuel imports funnels buyers toward duty-free battery trucks. Hybrid platforms are gaining in urban garbage collection, where stop-start duty cycles amplify fuel savings.

By Axle Configuration: Multi-Axle Uptake Accelerates

6×4 rigs comprised 34.12% of 2025 sales, balancing payload and maneuverability for mixed-road operations. Demand for 8×8 chassis is climbing at 7.17% CAGR due to opencast mining and heavy construction, which require full-time all-wheel drive.

4×2 tractors serve high-density corridors such as the N1 in South Africa, whereas 6×6 units cater to forestry and pipeline projects. Suspension innovations and electric axle integrations are reshaping vehicle-selection criteria beyond mere traction.

By Truck Type: Rigid Dominance, Articulated Upswing

Rigid designs captured 58.25% of the Africa heavy-duty truck market in 2025 due to their simpler maintenance footprint and superior urban agility. Articulated tractors, however, post a 6.67% CAGR as corridor surfaces improve and cross-border haulage extends average trip lengths.

South African motorway quality underpins multi-trailer configurations, whereas West African operators still favor rigids to cope with pothole-ridden feeder roads. OEMs now offer modular platforms that toggle between rigid and tractor setups, enhancing residual values.

By Application: Freight Leads, Mining Surges

Freight and logistics operations represented 42.86% of the Africa heavy-duty truck market in 2025, supplying consumer goods, foodstuffs, and construction inputs across regional hubs. Mining applications grow fastest at 7.60% CAGR as critical-mineral extraction scales up to meet global battery demand.

Specialized tipper bodies, autonomous haul kits, and high-capacity battery packs cater to mining’s harsh duty cycles, while refrigerated freight units expand alongside e-grocery penetration.

Geography Analysis

South Africa retained a 31.02% slice of the Africa heavy-duty truck market in 2025, supported by mature manufacturing clusters. The country exports knock-down kits across SADC, underpinning after-sales networks that drive repeat purchases.

Zambia is the fastest-growing market at 6.32% CAGR through 2031 as copper output and the Lobito rail corridor unlock heavier-haul opportunities. Nigeria shows latent volume, yet foreign-exchange rationing and 40% duty hikes curb fresh imports.

Egypt’s USD 6.6 billion logistics pipeline cements its role as North Africa’s demand hotspot, while Kenya and Ghana leverage Chinese CKD plants for cost-competitive supply. Morocco, now Africa’s most significant auto producer, is scaling exports into the Sahel and diversifying sourcing for fleet buyers. Ethiopia’s fossil-fuel import ban positions it as a proving ground for electric heavy trucks.

Mordor Intelligence examines the heavy duty trucks market across diverse other regional markets as well, including Europe, while also offering granular country-level perspectives for United States, Mexico, and Saudi Arabia and more.

Competitive Landscape

Competition is moderately fragmented as European stalwarts battle price-driven Chinese entrants and regional Indian brands. CKD localization by Sinotruk and FAW trims retail tags and shortens spare-parts lead times, eroding the premium once held by imported units. Mercedes-Benz, Volvo, and Scania defend their share through Euro VI technology, fuel-cell R&D, and autonomous pilot programs.

Daimler Truck has partnered with Volvo Group on fuel-cell stacks and continent-wide charging corridors, offering fleets a decarbonization route without sacrificing range. Tata Motors and Ashok Leyland apply emerging-market experience to launch simplified, high-ground-clearance rigs suited to rural African conditions.

Telematics, predictive maintenance, and over-the-air updates are emerging as battlegrounds for differentiation, while after-sales finance packages soften high upfront costs. Mining electrification and rural logistics niches provide white space for newcomers, but tariff volatility and FX risk remain formidable entry barriers.

Africa Heavy-duty Truck Industry Leaders

Daimler Trucks (Mercedes-Benz)

Volvo Trucks

Scania AB

MAN Truck & Bus

Sinotruk (CNHTC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Mahindra has entered into a Memorandum of Understanding (MoU) with South Africa's Industrial Development Corporation (IDC) to assess the feasibility of establishing a Completely Knocked Down (CKD) vehicle assembly facility in the country.

- October 2024: KamAZ, a prominent Russian company, has inaugurated a production facility in Senegal, focusing on trucks and MRAPs. The establishment of this KamAZ plant in Senegal underscores a pivotal moment in the economic partnership between Senegal and Russia. This move is in harmony with Russia's expansive investment blueprint across Africa, seeking to enhance the economic and industrial ties between the two continents.

- August 2024: Ogihara Thailand and Toyota Tsusho Africa have teamed up in South Africa, investing over R1.1 billion to enhance local automotive parts manufacturing.

Africa Heavy-duty Truck Market Report Scope

| 16 - 26 t |

| 26 - 40 t |

| Above 40 t |

| Internal-Combustion (ICE) | Diesel |

| Natural Gas (CNG/LNG) | |

| Electrified | Battery-Electric (BEV) |

| Hybrid & Plug-in Hybrid (HEV & PHEV) | |

| Fuel-Cell Electric (FCEV) |

| 4×2 |

| 6×2 |

| 6×4 |

| 6×6 |

| 8×6 |

| 8×8 |

| Others |

| Rigid |

| Articulated |

| Others |

| Construction & Mining |

| Freight & Logistics |

| Long-Haul |

| Other |

| Algeria |

| Angola |

| Egypt |

| Ethiopia |

| Kenya |

| Morocco |

| Nigeria |

| South Africa |

| Tanzania |

| Rest of Africa |

| By Gross Vehicle Weight Rating (Value) | 16 - 26 t | |

| 26 - 40 t | ||

| Above 40 t | ||

| By Propulsion (Value) | Internal-Combustion (ICE) | Diesel |

| Natural Gas (CNG/LNG) | ||

| Electrified | Battery-Electric (BEV) | |

| Hybrid & Plug-in Hybrid (HEV & PHEV) | ||

| Fuel-Cell Electric (FCEV) | ||

| By Axle Type (Volume) | 4×2 | |

| 6×2 | ||

| 6×4 | ||

| 6×6 | ||

| 8×6 | ||

| 8×8 | ||

| Others | ||

| By Truck Type (Value) | Rigid | |

| Articulated | ||

| Others | ||

| By Application (Value) | Construction & Mining | |

| Freight & Logistics | ||

| Long-Haul | ||

| Other | ||

| By Country (Value) | Algeria | |

| Angola | ||

| Egypt | ||

| Ethiopia | ||

| Kenya | ||

| Morocco | ||

| Nigeria | ||

| South Africa | ||

| Tanzania | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the Africa heavy-duty truck market in 2026?

It is estimated at USD 2.85 billion and is projected to grow at a 4.35% CAGR to USD 3.52 billion by 2031.

Which country is the fastest-growing buyer of heavy trucks in Africa?

Zambia leads with a 6.32% CAGR through 2031, driven by copper mining and new logistics corridors.

What segment holds the highest market share by GVWR?

The 26–40 ton class controls 41.78% of demand thanks to its versatility for corridor freight and construction.

How dominant are internal-combustion engines in the current fleet?

ICE trucks hold 86.10% share, though electric models are growing quickly at a 9.09% CAGR (2026-2031).

What is the key restraint affecting fleet expansion?

High total cost of ownership driven by expensive credit, diesel prices and import duties is shaving 1.8 percentage points off forecast CAGR.

Page last updated on: