Europe Heavy-Duty Truck Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 33.99 Billion |

| Market Size (2026) | USD 35.75 Billion |

| Market Size (2031) | USD 46.02 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

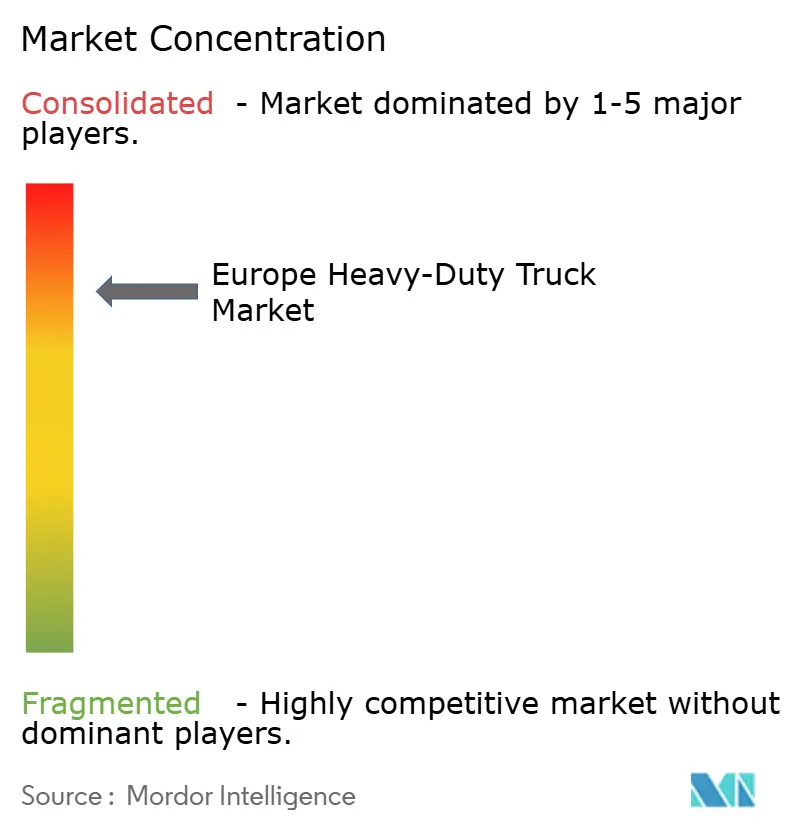

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Heavy-Duty Truck Market Analysis by Mordor Intelligence

The European heavy-duty truck market size is expected to grow from USD 33.99 billion in 2025 to USD 35.75 billion in 2026 and is forecast to reach USD 46.02 billion by 2031 at 5.18% CAGR over 2026-2031. Regulations that require a 90% CO₂ reduction by 2040, fast-rising total cost of ownership parity between battery-electric and diesel trucks, and the build-out of hydrogen corridors are reshaping purchase decisions. Fleet renewal is occurring earlier than normal depreciation schedules because penalty structures under the EU’s Phase-3 CO₂ framework sharply increase non-compliance costs. Manufacturers respond with modular platforms that shorten development cycles, while logistics operators accelerate orders to secure vehicle allocations ahead of expected production bottlenecks. Germany anchors demand thanks to extensive low-emission zones, whereas the Nordics record the fastest uptake as green power availability and carbon pricing sweeten zero-emission economics.

Key Report Takeaways

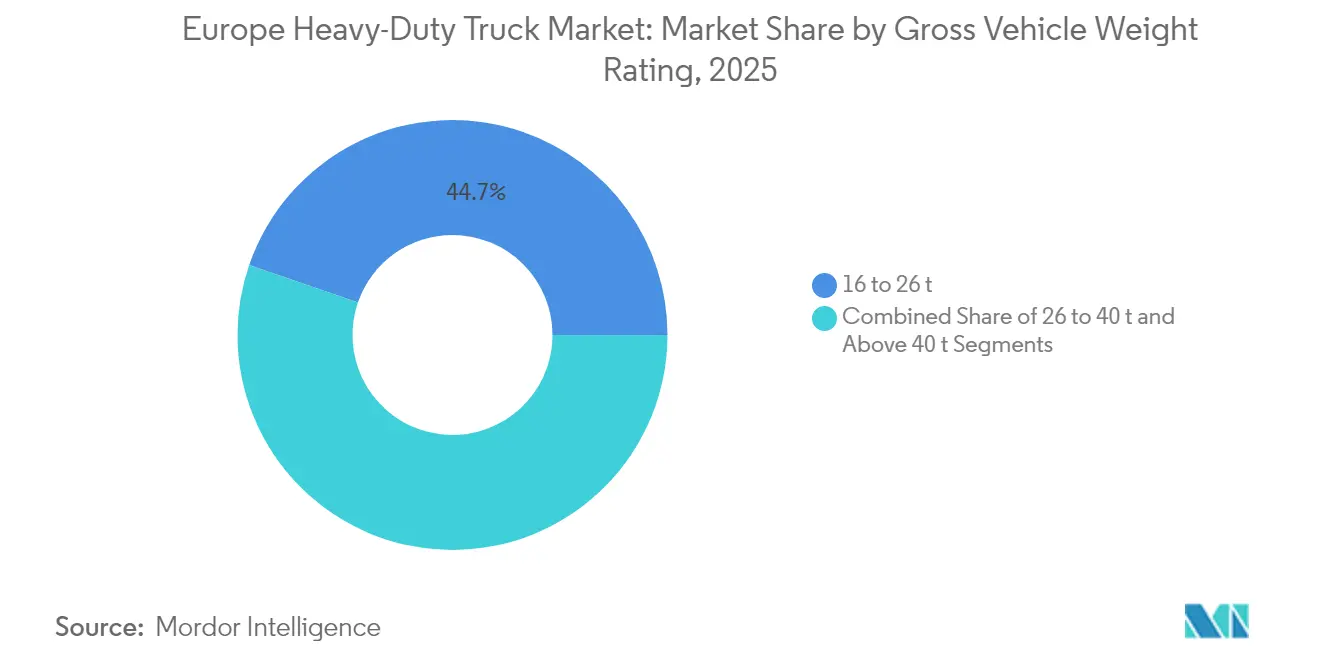

- By gross vehicle weight rating, the above-40 t class recorded the fastest expansion at an 8.73% CAGR through 2031 in the European heavy-duty truck market, while the 16 to 26 t class held the largest share, accounting for 44.73% of total revenue in 2025.

- By propulsion, battery-electric trucks posted a 16.12% CAGR, while internal-combustion engines retained 92.84% of the European heavy-duty truck market share in 2025.

- By axle type, 6×2 configurations led growth at a 7.15% CAGR, whereas 4×2 layouts captured 41.88% of the market in 2025.

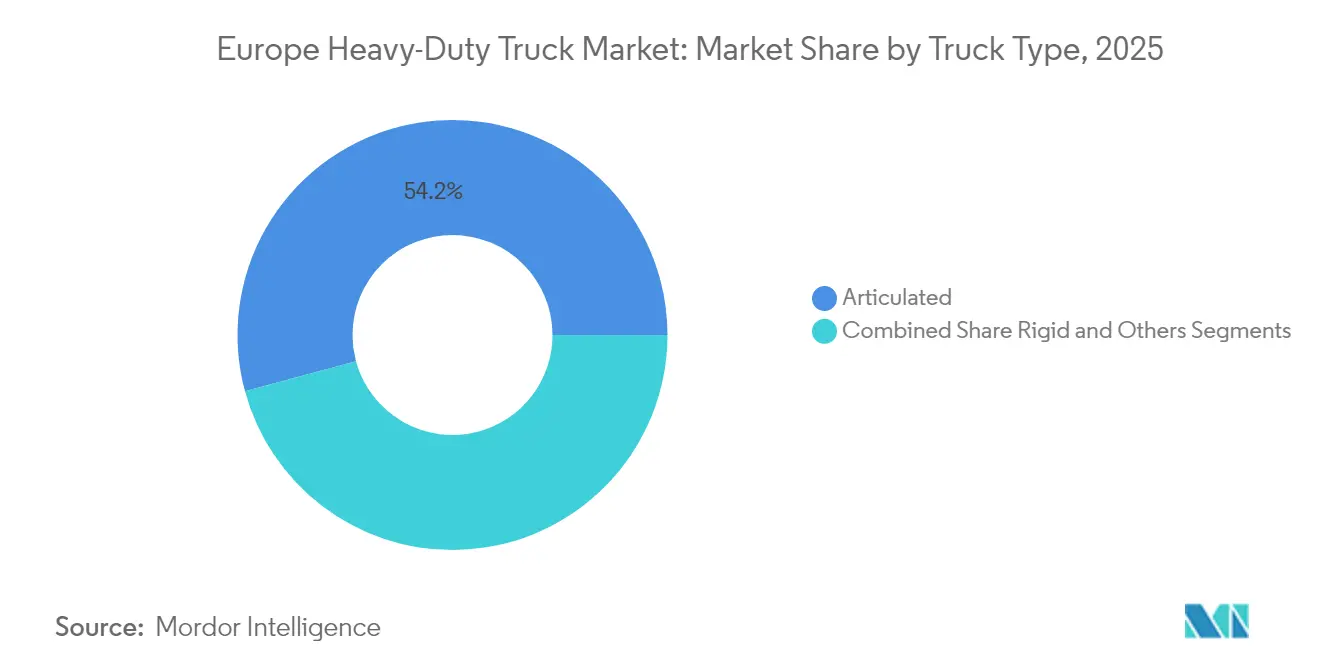

- By truck type, articulated units controlled 54.21% revenue in 2025 in the European heavy-duty truck market; rigid trucks, however, are forecast to rise at a 6.37% CAGR through 2031.

- By application, freight and logistics held 47.39% of the European heavy-duty truck market size in 2025, but long-haul use cases are on track for an 8.03% CAGR.

- By geography, Germany accounted for a 19.32% slice in 2025 in the European heavy-duty truck market, while the Nordic countries are projected to register a 6.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on heavy duty trucks market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Heavy-Duty Truck Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Phase-3 CO₂ Standards Tightening | +1.8% | Germany, France, Netherlands, Nordic Countries | Medium term (2-4 years) |

| TCO Parity of BEV Trucks | +1.2% | Germany, Benelux, Northern Italy | Short term (≤ 2 years) |

| E-commerce Driven Regional Distribution | +0.9% | Germany, France, UK, Netherlands | Short term (≤ 2 years) |

| Urban Low-Emission Zones | +0.7% | Germany, France, Italy, Netherlands | Medium term (2-4 years) |

| Hydrogen Corridor Projects | +0.6% | Germany, Netherlands, Nordic Countries | Long term (≥ 4 years) |

| OEM Modular Platforms | +0.4% | Germany, France, Italy, Spain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Phase-3 Co₂ Standards Tightening (2025-2030)

Penalties of EUR 6,800 per gram of excess CO₂ place heavy financial pressure on manufacturers, forcing fleet averages downward and sending a clear market signal that zero-emission trucks must scale rapidly[1]International Council on Clean Transportation, "THE EUROPEAN COMMISSION’S PROPOSED CO2 STANDARDS FOR HEAVY-DUTY VEHICLES", theicct.org. Early-adopting fleets gain competitive advantage by locking in supply commitments and preferential electricity tariffs before grid constraints intensify.

TCO Parity of BEV Trucks in Regional Haul Routes

Total cost of ownership calculations for battery-electric trucks reach parity with diesel equivalents in 2025 for routes under 400 kilometers. Regional haul applications benefit from predictable route patterns that enable optimized charging schedules and reduce range anxiety, while overnight depot charging eliminates the premium associated with public fast-charging infrastructure. Maintenance cost advantages of electric drivetrains compound the energy savings, as electric trucks eliminate oil changes, diesel particulate filter regeneration, and exhaust gas recirculation system maintenance that typically costs EUR 8,000-12,000 annually for heavy-duty diesel engines.

E-Commerce Driven Regional Distribution Boom

Parcel volumes continue to climb, shifting freight patterns toward high-frequency, medium-distance deliveries that align with current BEV range capabilities in the European heavy-duty truck market. Regional fulfillment networks favor rigid trucks in the 16-26 t class, boosting orders for electrified chassis. By adopting a regional distribution model, average daily distances have been curtailed to a range of 250-350 kilometers. This range aligns seamlessly with the capabilities of today's electric trucks. DHL's strategic rollout of electric trucks at its European hubs serves as a testament to the potential for logistics operators. Through adept route optimization and synchronized charging, they can realize substantial emission cuts without compromising service quality.

Urban Low-Emission Zones Accelerating Electrified Adoption

European cities are tightening low-emission zones, effectively sidelining diesel trucks. These zones act as unofficial mandates for electric trucks in urban logistics. Given that city centers account for 40-60% of delivery volumes in regional networks, operators are compelled to adapt. The financial repercussions are significant: beyond just losing access, operators face the dilemma of maintaining dual fleets or navigating less efficient routes, leading to a 15-25% spike in operational costs.

High Up-front Cost of ZEV Trucks

Electric trucks still cost 2.5-3 times more than diesels, pressuring cash-flow-constrained operators despite total cost advantages over the vehicle life in the European heavy-duty truck market. Battery packs alone can account for half of the price premium. While leasing arrangements help ease the initial financial burden, monthly payments for electric trucks still surpass those of their diesel counterparts. This cost disparity poses challenges, especially in specialized sectors such as construction and mining. Hence, electric trucks not only come with a premium price tag, but also face heightened costs due to their limited production volumes and ruggedized specifications, which curtail potential economies of scale.

Slow Roll-out of Public Charging and H₂ Refuelling

Truck electrification timelines outpace the rollout of charging infrastructure in Europe. By 2030, the Alternative Fuels Infrastructure Regulation requires public refuelling stations to be spaced no more than 200 km apart on the TEN-T core and comprehensive networks. However, Eastern European nations are falling notably short of these deployment targets.[2]European Commission, "Alternative fuels for sustainable mobility in Europe", transport.ec.europa.eu

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Gross Vehicle Weight Rating: Operators Push Above-40 t Payloads

The 16-26 t band remained the volume leader at 44.73% of 2025 demand due to its suitability for urban delivery and regional routes. The 26-40 tonne category serves as a transition zone where operators balance payload requirements against urban access restrictions, with many European cities implementing weight-based access controls that favor lighter configurations. Modular frames introduced by leading OEMs allow component sharing between classes, lowering incremental costs and smoothing production ramp-ups.

The above-40 t category expanded fastest at an 8.73% CAGR as companies sought to maximize payloads per trip and take advantage of regulatory axle-weight concessions for zero-emission trucks. Within the class, electrified trucks enjoy exemptions from weekend driving bans in several member states, further enhancing asset utilization. Adoption varies across weight classes because heavier trucks require larger battery packs, yet economies of scale in freight revenue offset the mass penalty.

By Propulsion: Battery-Electric Leads the Transition

Internal-combustion engines still dominated with 92.84% share in 2025, but electric trucks delivered a 16.12% CAGR that places them at the forefront of drivetrain change. Early deployments concentrate on regional haul where depot charging matches operating patterns. Natural gas engines hold niche appeal as a bridging solution, although rising biomethane prices temper growth prospects.

Fuel cell electric vehicles occupy a niche position focused on long-haul applications where hydrogen's energy density advantages offset infrastructure limitations. Tighter Euro 7 limits inflate diesel after-treatment costs, accelerating the switch to electric drivetrains. Despite holding a modest share in the market, electric truck manufacturers are grappling with order backlogs stretching 12 to 18 months, underscoring a demand that outpaces their production capabilities.

By Axle Type: 6×2 Configurations Gain Traction

4×2 trucks retained 41.88% of the European heavy-duty truck market share in 2025, reflecting their efficiency on highway and urban distribution routes where traction demands are moderate. Electric adoption is strongest in this layout because battery weight can be managed without exceeding axle limits, and existing depot charging networks are already configured around two-axle rigs. Even so, market momentum is shifting toward multi-axle designs that better accommodate heavier zero-emission drivetrains without compromising payload. Operators closely monitor residual values, and the relative simplicity of the 4×2 arrangement keeps long-term ownership costs predictable.

The 6×2 segment is expanding at a 7.15% CAGR for 2026-2031, driven by its ability to distribute battery mass across an additional axle while retaining lower rolling resistance than a full 6×4 drivetrain. OEM e-axle systems integrate seamlessly into this layout, enabling torque vectoring and regenerative braking that improve range. Specialized 6×4 and 6×6 chassis remain essential for construction and off-road transport, where maximum traction overrides efficiency goals, while heavy-haul 8×6 and 8×8 configurations occupy a niche with limited electrification prospects. Across all variants, new frames include pre-engineered mounting points and high-voltage routing to future-proof diesel models for later battery or fuel-cell conversions.

By Truck Type: Rigid Trucks Benefit from Urban Focus

Articulated combinations commanded 54.21% of European heavy-duty truck market share in 2025, underscoring the region’s dependence on long-haul, trailer-based freight models. Fleets value the operational flexibility of dropping trailers at intermodal hubs, and diesel trucks continue to dominate this space. Nonetheless, battery integration poses packaging challenges for articulated rigs because the trucks must carry most of the energy storage, and charging schedules must coordinate with trailer swapping and driver rest periods. These constraints temper the near-term electrification rate in the highest-volume configuration.

Rigid trucks are growing at a 6.37% CAGR through 2031 as e-commerce accelerates urban and regional delivery demand. A single-body chassis simplifies battery placement, boosts usable cargo space, and enables overnight depot charging without trailer logistics, reducing total cost of ownership. Logistics operators prefer rigid formats for city-center access under low-emission zone rules, and modular van-to-truck bodies allow rapid reconfiguration of payload requirements. The launch of the IVECO S-eWay Artic demonstrates that technology is catching up for articulated use cases, but current infrastructure economics still favor rigid deployments in densely populated corridors

By Application: Long-Haul Segment Embraces Zero-Emission Technology

Freight and logistics applications held 47.39% of the European heavy-duty truck market size in 2025, reflecting the broad spectrum of goods movement that underpins regional commerce. Urban parcel delivery and regional distribution dominate mileage, aligning naturally with battery-electric ranges and depot charging models. Operators in these segments achieve quick payback periods because predictable route profiles optimize energy use and battery cycling. Tight delivery windows also favor electric drivetrains that offer instant torque and regenerative stopping in stop-and-go traffic.

Long-haul missions are projected to grow at an 8.03% CAGR from 2026-2031 as fuel-cell systems and higher-density batteries extend zero-emission range past 500 km. Hydrogen corridor funding along the TEN-T network supports refueling infrastructure suited to cross-border freight, easing prior constraints on intercity routes. Construction and mining applications lag because harsh duty cycles accelerate battery degradation and require ruggedized designs that remain costly at low production volumes. Meanwhile, pilots such as Scania’s electric truck with a fuel-powered range extender illustrate hybrid pathways that let fleets meet urban zero-emission mandates while preserving long-haul flexibility

Geography Analysis

Germany commanded 19.32% of 2025 demand, driven by dense freight networks, expansive supplier bases and generous purchase incentives. Low-emission zones covering most major cities compel earlier replacement of legacy diesel fleets, while access to reliable grid power accelerates depot charging roll-outs. Funding programs lower acquisition costs by up to half, and domestic OEM presence anchors local employment and political backing.

The Nordic region is expected to post a 6.92% CAGR through 2031, buoyed by abundant renewable electricity, toll exemptions and pilot electric road systems that extend range capability. Government-backed carbon pricing raises diesel operating expenses, tipping life-cycle economics in favor of BEVs even in cold climates.

Spain, Poland and the Benelux states illustrate the next wave of adoption as port-centric logistics corridors demand cleaner trucks. The Netherlands leverages the Port of Rotterdam’s electrification projects to create concentrated charging clusters, while Poland’s rapid economic growth aligns freight modernization with EU emission rules. Eastern Europe trails on infrastructure readiness but represents a sizable long-term volume pool once grid upgrades progress.

Mordor Intelligence provides coverage of the heavy duty trucks market across other key regional markets, including Africa, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United States, Mexico, and Saudi Arabia incorporating local coverage and market participation, as required.

Competitive Landscape

In the European heavy-duty truck market, the top three players dominate, holding a majority share and fostering an oligopolistic environment. This concentration paves the way for synchronized technology advancements and strategic infrastructure investments. Daimler Truck AG leads, leveraging its Mercedes-Benz brand strength and early electric truck commercialization through the eActros platform, while Volvo Group's share reflects its leadership in safety technology and sustainable transport solutions.

Strategic focus has shifted from hardware differentiation to software, connectivity and uptime services. Predictive maintenance suites lower unplanned downtime, while route-planning algorithms cut empty miles. These digital value-adds lock customers into OEM ecosystems, raising switching costs above the initial vehicle price premium.

Emerging competitors, particularly Chinese brands, test market defenses through price-aggressive electric trucks. Incumbents counter with localized production, aftersales networks and tailored financing. Opportunities still exist for specialist manufacturers in construction, mining and municipal niches where mainstream OEMs prioritize higher-volume segments.

Europe Heavy-Duty Truck Industry Leaders

-

Daimler Truck AG

-

Volvo Group

-

Traton Group

-

DAF Trucks NV

-

Iveco Group NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: IVECO introduces the S-eWay Artic featuring 600 km range, signaling diesel-parity capability on core European corridors.

- June 2025: MAN debuts the eTGS in the UK, pairing vehicle launch with turnkey depot-charging solutions to alleviate infrastructure concerns.

- February 2025: Daimler Truck partners with Paul Nutzfahrzeuge to commercialize hydrogen trucks across Europe, broadening long-haul zero-emission options.

- August 2024: Volvo Group secures USD 208 million in funding to scale electric truck production capacity.

Europe Heavy-Duty Truck Market Report Scope

| 16 to 26 t |

| 26 to 40 t |

| Above 40 t |

| Internal-Combustion Engine (ICE) | Diesel |

| Natural Gas (CNG/LNG) | |

| Electric | Battery-Electric (BEV) |

| Hybrid and Plug-in Hybrid (HEV and PHEV) | |

| Fuel-Cell Electric (FCEV) |

| 4x2 |

| 6x2 |

| 6x4 |

| 6x6 |

| 8x6 |

| 8x8 |

| Others |

| Rigid |

| Articulated |

| Others |

| Construction and Mining |

| Freight and Logistics |

| Long Haul |

| Other |

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Poland |

| Nordics |

| Benelux |

| Rest of Europe |

| By Gross Vehicle Weight Rating (GVW) | 16 to 26 t | |

| 26 to 40 t | ||

| Above 40 t | ||

| By Propulsion | Internal-Combustion Engine (ICE) | Diesel |

| Natural Gas (CNG/LNG) | ||

| Electric | Battery-Electric (BEV) | |

| Hybrid and Plug-in Hybrid (HEV and PHEV) | ||

| Fuel-Cell Electric (FCEV) | ||

| By Axle Type | 4x2 | |

| 6x2 | ||

| 6x4 | ||

| 6x6 | ||

| 8x6 | ||

| 8x8 | ||

| Others | ||

| By Truck Type | Rigid | |

| Articulated | ||

| Others | ||

| By Application | Construction and Mining | |

| Freight and Logistics | ||

| Long Haul | ||

| Other | ||

| By Country/ Region | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Poland | ||

| Nordics | ||

| Benelux | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current European heavy-duty truck market size and growth outlook?

The market was valued at USD 35.75 billion in 2026 and is forecast to reach USD 46.02 billion by 2031, translating to a 5.18% CAGR over 2026-2031.

When do battery-electric heavy-duty trucks reach total cost of ownership parity with diesel?

On regional haul routes under 400 km, TCO parity is already achieved in 2025, supported by lower energy and maintenance expenses.

Which country leads adoption of zero-emission heavy-duty trucks in Europe?

Germany holds the largest share at 19.32% owing to extensive low-emission zones, incentives and manufacturing presence.

What segment is growing fastest within the European heavy-duty truck market?

Battery-electric propulsion exhibits the highest CAGR at 16.12%, propelled by regulatory drivers and improving vehicle economics.

Which axle configuration shows the strongest growth?

The 6×2 layout is projected to advance at a 7.15% CAGR as it balances payload capacity with e-axle compatibility.

Page last updated on: