Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

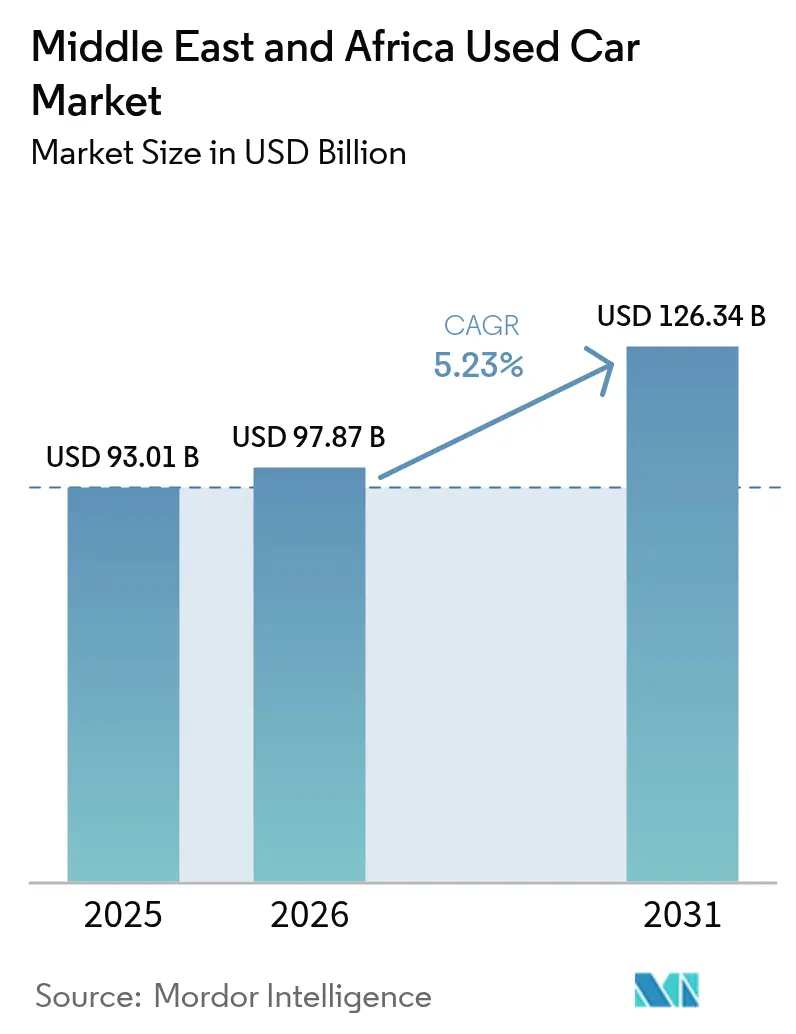

| Base Year Market Size (2025) | USD 93.01 Billion |

| Market Size (2026) | USD 97.87 Billion |

| Market Size (2031) | USD 126.34 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Used Car Market Analysis by Mordor Intelligence

The Middle East and Africa used car market size was valued at USD 93.01 billion in 2025 and estimated to grow from USD 97.87 billion in 2026 to reach USD 126.34 billion by 2031, at a CAGR of 5.23% during the forecast period (2026-2031). Market growth is fueled by persistent new-vehicle supply constraints, accelerated digital adoption, and government import-liberalization measures that collectively reshape demand dynamics. Elevated new-car prices following Red Sea shipping disruptions, rapid mobile-internet penetration, and the influx of competitively priced Chinese brands amplify consumer migration toward the Middle East and Africa used car market[1]“Red Sea Disruptions Extend Vehicle Delivery Times,” Reuters, reuters.com. Organized vendors gain momentum through certified pre-owned programs, while inspection and history-verification services improve buyer confidence and catalyze formalization. SUVs dominate sales as harsh-terrain adaptability remains paramount, and battery-electric vehicles emerge as the fastest-growing fuel class despite heat-induced battery-degradation concerns.

Key Report Takeaways

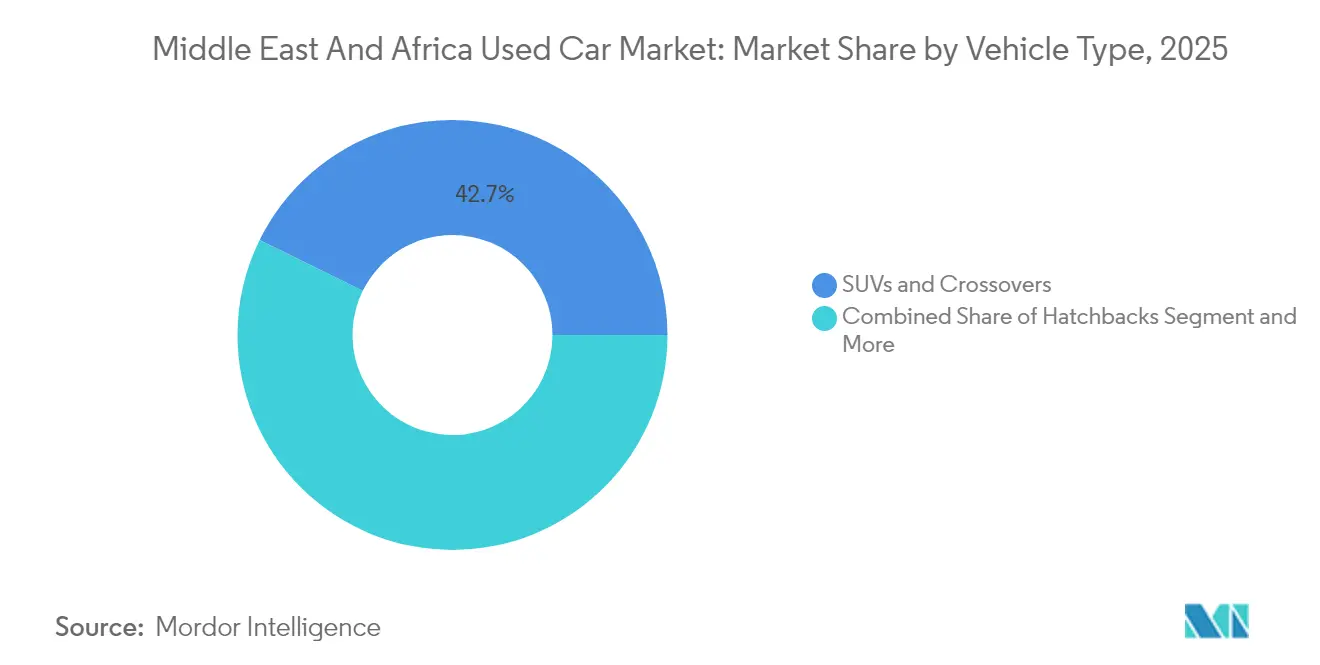

- By vehicle type, SUVs and crossovers led with 42.72% revenue share in 2025; the segment is projected to advance at a 5.55% CAGR through 2031.

- By vendor type, unorganized channels held 61.70% of the Middle East and Africa used car market share in 2025, while organized vendors are growing at a 6.55% CAGR to 2031.

- By fuel type, petrol vehicles captured 78.60% of the Middle East and Africa used car market size in 2025 while battery-electric vehicles are poised to expand at a 9.92% CAGR through 2031.

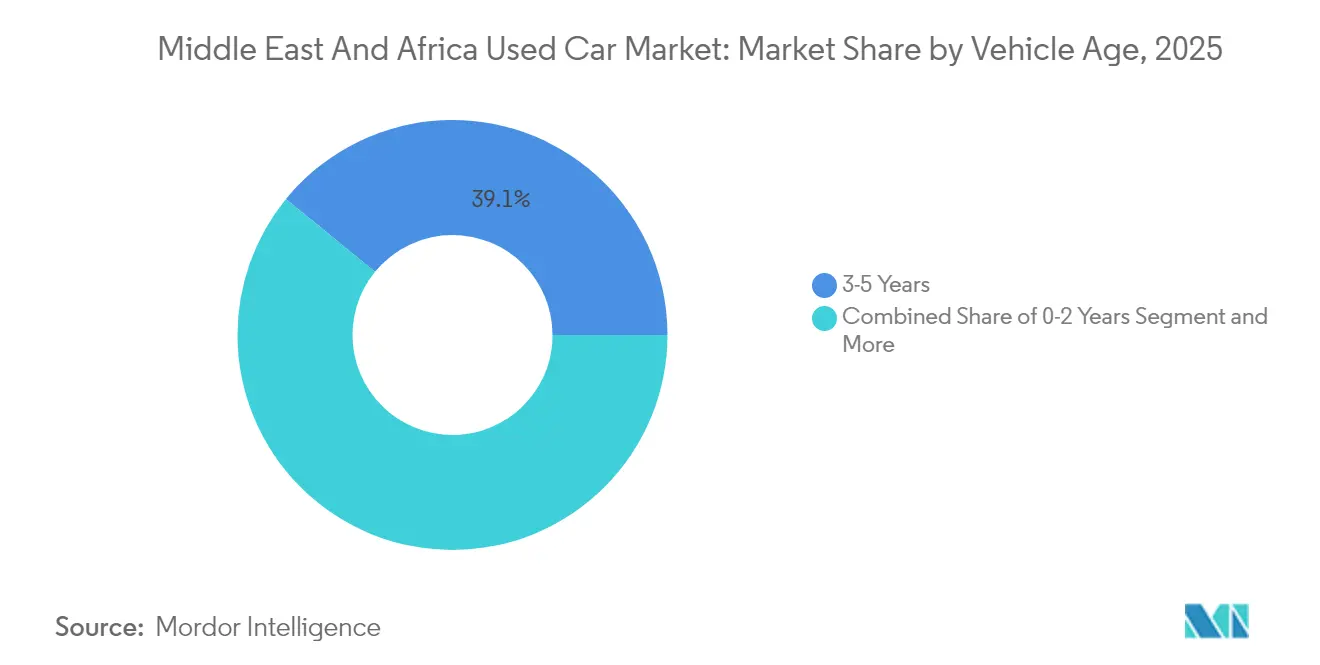

- By vehicle age, the 3-5 year category accounted for 39.10% share of the Middle East and Africa used car market size in 2025 and 0-2 year category is rising at a 7.45% CAGR through 2031.

- By distribution channel, online classified and e-commerce platforms commanded 73.60% share of the Middle East and Africa used car market size in 2025 and continue to grow at a 6.05% CAGR through 2031.

- By country, Saudi Arabia held 34.20% of the Middle East and Africa used car market share in 2025, whereas the United Arab Emirates posts the highest 6.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High New-Vehicle Prices, Supply Delays | +1.2% | GCC and North Africa | Short term (≤ 2 years) |

| Influx of Affordable Chinese Brands | +0.9% | Egypt, Ethiopia, GCC | Medium term (2–4 years) |

| Digital Classifieds and O2O Platforms | +0.8% | United Arab Emirates, Saudi Arabia, Egypt | Medium term (2–4 years) |

| SUV and Pickup Preference | +0.6% | Middle East and North Africa | Long term (≥ 4 years) |

| Expansion of Inspection Services | +0.4% | GCC | Medium term (2–4 years) |

| Early Electrified Fleets Supply | +0.3% | Urban GCC and Egypt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High New-Vehicle Prices and Supply-Chain Delays

Red Sea shipping bottlenecks have extended delivery lead times by up to six weeks, prompting regional distributors to raise new-car prices during 2024 and pushing budget-sensitive buyers into the Middle East and Africa used car market. Affordability gaps intensify demand for 2–3-year-old vehicles, while corporate fleets shorten replacement cycles to lock in residual values ahead of further price inflation. Dealer inventories of popular models remain tight for four to six months, compelling consumers to consider used options previously out of scope. Leasing companies capitalize by remarketing low-mileage returns, creating a steady pipeline of nearly-new stock. Collectively, these factors elevate transaction volumes and sustain premium resale values across high-demand nameplates.

Influx of Affordable Chinese Brands Boosts Turnover

Aggressive expansion by BYD, Geely, and Chery delivers attractively priced alternatives often below legacy competitors, stoking new-vehicle uptake that swiftly filters into secondary channels. Local assembly joint ventures shorten supply cycles and raise model familiarity among service workshops, lowering perceived ownership risk. Fleet operators embrace Chinese sedans and SUVs to contain capital outlays, thereby feeding a pipeline of 2–4-year returns. Competitive feature sets—such as panoramic cameras and advanced infotainment—heighten appeal to tech-savvy buyers. Consequently, turnover accelerates, deepening inventory across price tiers within the Middle East and Africa used car market.

Digital Classifieds and O2O Platforms Proliferation

Platform consolidation is redefining supply chains as Dubizzle Motors, CarSwitch, and Syarah scale verification and financing solutions that reduce friction and widen the buyer pool. Data-driven pricing algorithms equalize information asymmetry, boosting consumer trust and compressing negotiation spreads. Online-to-offline (O2O) fulfillment unlocks cross-border sourcing that broadens inventory diversity, while mobile-first interfaces resonate with digital-native demographics. Strategic funding rounds, such as Syarah’s USD 60 million Series C, bankroll regional expansion and technology upgrades. Traditional dealers, recognizing foot-traffic erosion, fast-track digital storefronts and hybrid models to retain relevance and capture incremental share within the Middle East and Africa used car market.

SUV and Pickup Preference for Harsh Terrain

Desert environments shape purchasing behavior as consumers prioritize vehicles offering superior cooling, elevated ride height, and sand-resistant components. Certified Toyota Land Cruiser and Nissan Patrol models attract 15–20% premiums over sedan counterparts due to proven durability [2]“Certified SUVs Command Premium in Desert Conditions,” AutoTraders UAE, autotraders-uae.com. Commercial operators in construction, oil services, and tourism sectors extend demand beyond private-use contexts. Aftermarket upfitters specialize in grille guards, ceramic coatings, and reinforced suspensions that bolster resale values. Chinese OEMs capitalize by releasing lower-priced SUVs equipped with region-specific thermal management systems. The enduring preference fortifies segment leadership in the Middle East and Africa used car market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dominance of Unorganized Vendors | −0.8% | Sub-Saharan and North Africa | Long term (≥ 4 years) |

| Restrictive Cross-Border Regulations | −0.6% | Pan-African corridors and GCC | Short term (≤ 2 years) |

| Odometer Fraud and Limited Transparency | −0.5% | Africa and select Middle East | Medium term (2–4 years) |

| Heat-Induced Battery Degradation | −0.4% | Gulf and North Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Dominance of Unorganized Vendors in Africa

Informal street-level traders retain control over a majority of transactions across key African economies, perpetuating cash-only dealings and opaque pricing that hinder credit penetration. Absence of standardized inspections allows quality variance that suppresses consumer confidence and limits regional export prospects. Regulatory agencies struggle with enforcement owing to limited resources and entrenched familial trading networks. Although digital classifieds gain traction, resistance to registration and taxation slows formalization. Foreign investors remain cautious, citing legal uncertainties that dilute return predictability in the Middle East and Africa used car market.

Restrictive Cross-Border Import Regulations

Several governments maintain tight import‐age caps, environmental standards, and document-authentication rules that slow vehicle inflows and elevate compliance costs. Nigeria’s enforcement of a 12-year age limit in 2025 redirected older inventory toward neighboring states and trimmed regional supply, squeezing price-sensitive buyers and reducing transaction volumes along major corridors. GCC authorities periodically raise inspection fees and require origin certificates that lengthen clearance times, compelling dealers to hold higher working capital and pass the burden to consumers. Fragmented tariff structures across East African Community and Economic Community of West African States members complicate multi-country sourcing strategies, undermining economies of scale for organized retailers. Traders respond by channeling stock through informal border points, but heightened patrols and digital customs systems are raising seizure risks and discouraging gray-market flows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: SUVs Sustain Superiority

SUVs posted 42.72% share of the Middle East and Africa used car market in 2025, outpacing sedans and hatchbacks and expanding at a 5.55% CAGR to 2031. The Middle East and Africa used car market size for SUVs in 2025, reflected entrenched demand for high-ground-clearance designs that withstand desert terrains. Durability advantages translate into slower depreciation, enabling certified pre-owned SUVs to command premiums over equivalent mileage sedans. Emerging Chinese SUV models introduce competitive price tiers, enticing fleet managers to broaden procurement beyond traditional Japanese nameplates.

Growing aftermarket sectors-from ceramic protective coatings to adaptive suspension kits-further elevate perceived value, contributing to higher turnover velocity. Sedans hold a stable share, driven by urban commuters prioritizing fuel economy and compact parking footprints, while hatchbacks remain the entry point for budget-constrained first-time buyers. MPVs cater to large families and niche commercial segments. Nevertheless, SUV dominance is expected to persist as infrastructure expansions in construction, oil, and tourism sectors sustain off-road-capable vehicle requirements across the Middle East and Africa used car market.

By Vendor Type: Organized Momentum Builds

Unorganized dealers accounted for 61.70% of transactions in 2025, but organized vendors are growing with fastest 6.55% CAGR by 2031, underscoring shifting consumer preferences toward structured warranties and transparent pricing. The Middle East and Africa used car market size recorded significant organized sales during 2025, reflecting rising adoption of certified pre-owned programs. Regulatory reforms in GCC states compel dealers to digitize inventories and provide inspection documentation, reducing asymmetry and increasing lender confidence.

Digital platforms empower organized vendors to syndicate listings across borders, tapping inventory pools previously constrained by geography. Conversely, informal traders face punitive penalties for non-compliance, enhancing the relative attractiveness of formal channels. Momentum is most evident in Saudi Arabia, where removal of the customs-broker requirement trims import processing times, enabling organized players to rotate stock faster. The share shift is expected to accelerate as banks deepen auto-finance penetration, tethering credit approvals to verifiable vehicle data.

By Fuel Type: Electrification Gains Ground

Petrol vehicles dominate the Middle East and Africa used car market with 78.60% share, but battery-electric vehicles register the highest CAGR at 9.92% through 2031. The Middle East and Africa used car market size for electric cars in 2025 was low, yet early fleet dispositions by ride-hailing and logistics firms seed supply channels. Hybrid powertrains serve as transitional options for buyers favoring fuel efficiency without range constraints.

Thermal-management challenges constrain secondary EV uptake, particularly in Gulf states where high ambient temperatures accelerate battery wear. Nonetheless, policy incentives including reduced import duties and free-parking privileges foster incremental demand. Investment in liquid-cooled charging infrastructure and battery-reconditioning start-ups promises to mitigate longevity concerns over the forecast horizon. The enduring predominance of internal-combustion vehicles will gradually erode as technology costs fall and climate-adapted battery chemistries enter OEM portfolios.

By Vehicle Age: Premium on Youth

Vehicles aged 3-5 years captured 39.10% share in 2025, positioning this bracket as the volume anchor of the Middle East and Africa used car market. Buyers perceive the category as balancing modern features with palatable capital outlays. Yet the 0-2-year cohort grows fastest at 7.45% CAGR, as supply-chain disruptions nudge consumers toward nearly new alternatives available immediately. The Middle East and Africa used car market share for 0-2-year models climbed in 2025, supported by extended OEM warranties and advanced climate-adaptation technologies.

Older brackets, spanning 6-8 years and above 8 years, maintain relevance among budget-focused segments, especially in Sub-Saharan Africa where purchasing power lags GCC levels. Nigeria’s enforcement of a 12-year import age cap curtails inflows of high-mile vehicles, gradually elevating fleet quality and pressuring informal vendors to source newer stock. Over time, tightening regulatory regimes across Africa are likely to prune the aging tail of the vehicle-age distribution.

By Distribution Channel: Digital Ascendancy

Online Classified and E-commerce controlled 73.60% of the Middle East and Africa used car market in 2025 and sustain a 6.05% CAGR through 2031. Convenience, comprehensive listing data, and integrated financing propel adoption among millennials and Generation Z. Mobile-optimized portals facilitate rapid cross-border sourcing, expanding buyer choice and pressuring offline dealers to match pricing transparency. The Middle East and Africa used car market size transacted through online channels expected to grow further, underpinning platform profitability and attracting continued venture funding.

Offline showrooms retain cultural resonance in select markets where physical inspection and interpersonal negotiation remain embedded norms. Hybrid O2O models flourish, blending digital lead-generation with on-site verification centers that reassure risk-averse buyers. Regulatory bodies increasingly mandate digital record-keeping for tax compliance, inadvertently steering transactions onto traceable platforms. Consequently, brick-and-mortar dealerships accelerate digitization efforts, integrating CRM systems and virtual showrooms to remain competitive.

Geography Analysis

Saudi Arabia commanded 34.20% share of the Middle East and Africa used car market in 2025, underpinned by high disposable incomes, an extensive highway network, and Vision 2030 diversification projects that elevate commercial-fleet turnover. Customs-procedure simplification introduced has shortened import cycles and widened model availability, elevating transaction liquidity. Organized retailers leverage the kingdom’s mature financing ecosystem to scale certified pre-owned operations, capturing aspirational buyers seeking warranty-covered vehicles.

The United Arab Emirates posts the region’s fastest 6.82% CAGR through 2031, reflecting its role as a trade nexus and early adopter of digital classifieds. Free-zone logistics enable efficient re-export to African buyers, while progressive consumer-protection rules enhance confidence in cross-border online transactions. Platform operators pilot blockchain-based vehicle-history passports, strengthening resale propositions and drawing regional demand onto UAE hubs within the Middle East and Africa used car market. Egypt, with its sizeable population and growing middle class, ranks among the top volume contributors despite price sensitivity. Local assembly agreements with Chinese OEMs guarantee future inflows of competitively priced models into secondary channels.

Currency volatility encourages consumers to hedge against future price hikes by locking in used-car purchases, lifting volumes in the 3-5-year bracket. In sub-Saharan Africa, Kenya and South Africa exhibit robust informal trading networks, though gradual digitization fosters transparency improvements. Policy interventions such as Nigeria’s 12-year import-age restriction elevate fleet quality but redirect older vehicles to neighboring jurisdictions with lenient rules, reshaping intra-African trade flows. Morocco benefits from proximity to Europe and an established manufacturing base, while Kuwait and Oman maintain high per-capita ownership but smaller absolute volumes.

Competitive Landscape

The Middle East and Africa used car market remains fragmented. Digital consolidation intensifies competitive pressure as Dubizzle Motors scales verification, financing, and logistics into a one-stop ecosystem. Al-Futtaim Automotive leverages its OEM franchises to extend certified pre-owned warranties, creating differentiation on quality assurance. Syarah’s Series C infusion funds inventory expansion and AI-driven pricing tools that compress dealer margins in Saudi Arabia [3]“Syarah Secures USD 60 Million to Scale Used-Car Platform,” Arabian Business, arabianbusiness.com.

White-space opportunities center on cross-border transaction facilitation, AI-enabled valuation algorithms, and battery-health analytics for EV resale. Chinese OEMs such as BYD and Geely cultivate residual-value confidence by partnering with inspection firms and offering extended battery guarantees. Fintech lenders penetrate underserved demographics by integrating platform-verified data into credit-scoring models, lowering default risk and capturing incremental market share.

Traditional unorganized vendors grapple with tightening compliance requirements that favor formal operators. The competitive environment rewards entities adept at combining localized market intelligence with scalable digital infrastructure, accelerating sector formalization within the Middle East and Africa used car market.

Middle East And Africa Used Car Industry Leaders

Dubizzle Motors (OLX UAE)

Al-Futtaim Automotive

Abdul Latif Jameel Motors

Kayishha (SellAnyCar KSA)

DubiCars

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The Kuwaiti Ministry of Public Works moved the Amghara Car Auction Project into the tendering phase, signaling imminent construction of a centralized, regulated hub for Kuwait’s pre-owned vehicle trade.

- November 2024: Carabia unveiled a wait-list for its premium used-car marketplace in the United Arab Emirates, promising rigorous vetting and professional inspections to deliver a transparent buying experience.

- September 2024: Syarah raised SAR 225 million (USD 60 million) in Series C funding to accelerate national expansion and reinforce its digital leadership in Saudi Arabia’s pre-owned segment.

Middle East And Africa Used Car Market Report Scope

The Used Car Market is segmented by Vehicle Type (Hatchback, Sedan, and Sports Utility Vehicle(SUV)), Vendor Type (Organized and Unorganized), and By Country (United Arab Emirates, Saudi Arabia, Kenya, Egypt, and the Rest of Middle-East and Africa). The Report Offers Market Size and Forecast in Value (USD billion) for the above-mentioned Segments.

In addition, all the regulatory policies shaping the purchase of used electric vehicles in the Middle-East and African region have been portrayed in the report for a deep and comprehensive understanding of market dynamics.

By Vehicle Type

| Hatchbacks |

| Sedans |

| SUVs and Crossovers |

| MPVs |

By Vendor Type

| Organized (Dealerships and CPO) |

| Unorganized (Independents and P2P) |

By Fuel Type

| Petrol |

| Diesel |

| Hybrid |

| Battery-Electric |

By Vehicle Age

| 0-2 Years |

| 3-5 Years |

| 6-8 Years |

| Above 8 Years |

By Distribution Channel

| Online Classified and E-commerce |

| Offline / Brick-and-Mortar |

By Country

| United Arab Emirates |

| Saudi Arabia |

| Egypt |

| Kenya |

| South Africa |

| Morocco |

| Nigeria |

| Kuwait |

| Oman |

| Rest of Middle East and Africa |

| By Vehicle Type | Hatchbacks |

| Sedans | |

| SUVs and Crossovers | |

| MPVs | |

| By Vendor Type | Organized (Dealerships and CPO) |

| Unorganized (Independents and P2P) | |

| By Fuel Type | Petrol |

| Diesel | |

| Hybrid | |

| Battery-Electric | |

| By Vehicle Age | 0-2 Years |

| 3-5 Years | |

| 6-8 Years | |

| Above 8 Years | |

| By Distribution Channel | Online Classified and E-commerce |

| Offline / Brick-and-Mortar | |

| By Country | United Arab Emirates |

| Saudi Arabia | |

| Egypt | |

| Kenya | |

| South Africa | |

| Morocco | |

| Nigeria | |

| Kuwait | |

| Oman | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the forecast value of the Middle East and Africa used car market by 2031?

The market is expected to reach USD 126.34 billion by 2031, reflecting a 5.23% CAGR.

Which vehicle type leads regional used-car sales?

SUVs and crossovers hold the top position with 42.72% share in 2025 due to superior desert adaptability.

How dominant are digital platforms in used-car transactions?

Online classifieds and e-commerce sites controlled 73.60% of transactions in 2025 and continue to expand.

Why are battery-electric vehicles the fastest-growing segment?

Early fleet electrification and supportive incentives drive a 9.92% CAGR, even though heat-induced degradation remains a challenge.

Which country shows the highest growth rate in regional used-car sales?

The United Arab Emirates leads with a 6.82% CAGR through 2031, supported by advanced digital marketplaces and favorable regulations.

How is vendor formalization progressing?

Organized channels are growing faster than the overall market at 6.55% CAGR, driven by certified pre-owned programs and regulatory support.

Page last updated on: