Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

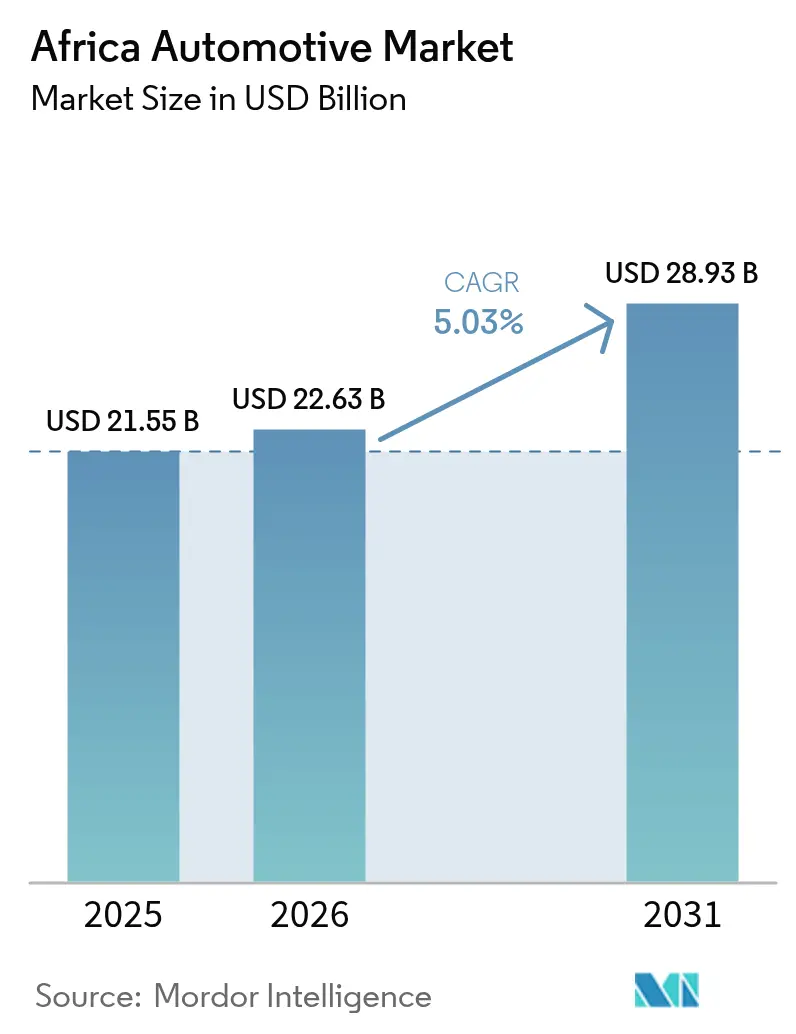

| Base Year Market Size (2025) | USD 21.55 Billion |

| Market Size (2026) | USD 22.63 Billion |

| Market Size (2031) | USD 28.93 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

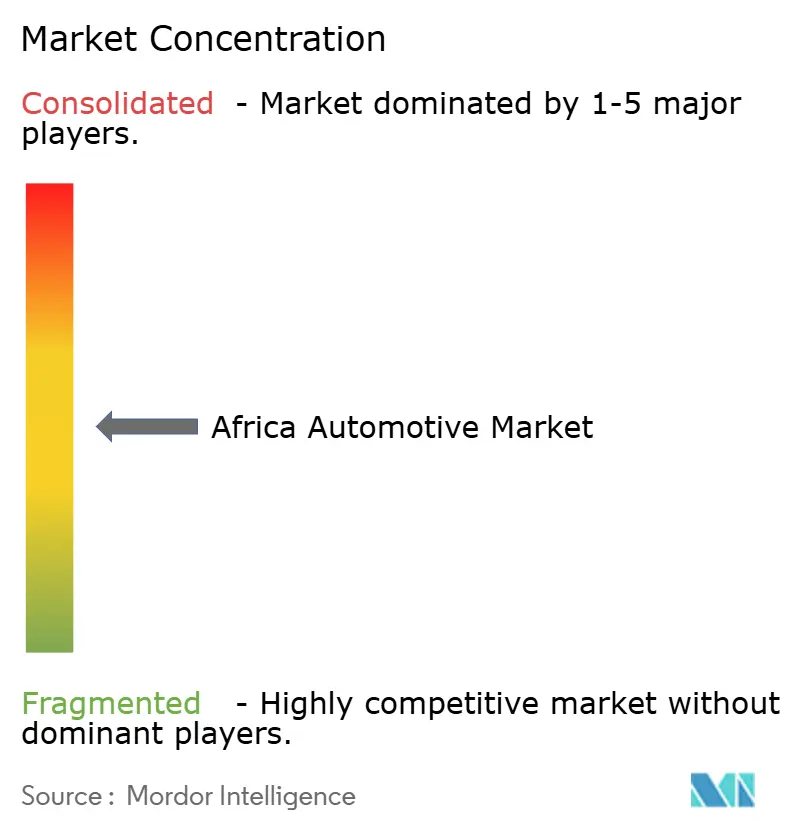

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Automotive Market Analysis by Mordor Intelligence

Africa automotive market size in 2026 is estimated at USD 22.63 billion, growing from 2025 value of USD 21.55 billion with 2031 projections showing USD 28.93 billion, growing at 5.03% CAGR over 2026-2031. Rising urban middle-class spending, accelerated Chinese CKD/SKD investments, and AfCFTA tariff liberalization collectively set a positive demand trajectory for the Africa automotive market [1]“Africa’s Emerging Consumer Class,”, Finance & Development, imf.org. Digital remittance platforms channeling diaspora funds into vehicle purchases and ride-hailing and last-mile delivery fleet expansion further widen addressable volumes. Regional OEMs benefit from policy incentives prioritizing local value addition, while miners’ pilot programs for electric pickups in the copper-belt introduce a specialist commercial niche. Logistics bottlenecks, currency volatility, and grey-market used-car inflows remain the critical headwinds that can temper growth momentum in the Africa automotive market.

Key Report Takeaways

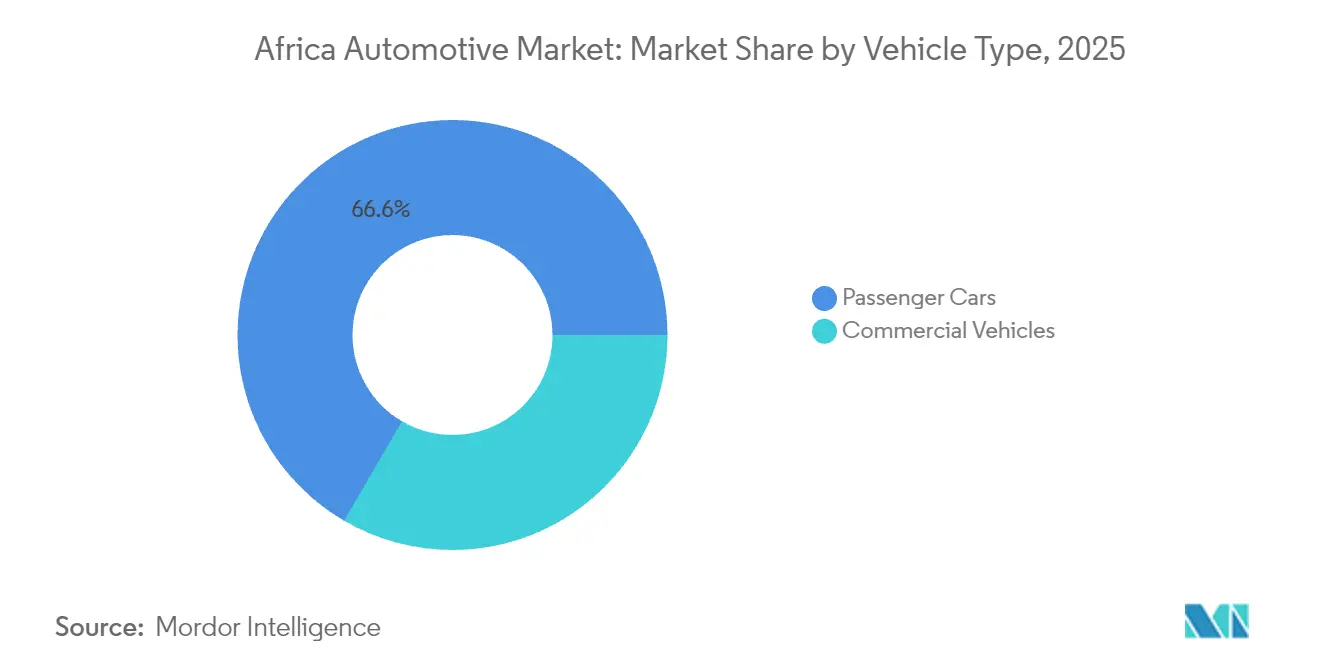

- By vehicle type, passenger cars held 66.58% of Africa automotive market share in 2025; commercial vehicles are projected to expand at an 8.36% CAGR to 2031.

- By propulsion type, internal combustion engines led with 90.68% share in 2025, while battery electric vehicles are forecast to rise at a 10.12% CAGR through 2031.

- By end-use, personal ownership represented 62.05% of Africa automotive market size in 2025, whereas fleet and leasing should advance at a 9.33% CAGR over the forecast period.

- By sales channel, completely built-up imports captured 49.15% share of Africa automotive market size in 2025; SKD/CKD assembly is set to progress at an 8.19% CAGR by 2031.

- By Country, South Africa dominated with a 37.85% share in 2025, while Nigeria is anticipated to post the fastest 8.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Automotive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Urban Middle Class Car Ownership | +1.2% | Pan-African, concentrated in Nigeria, Kenya, Ghana | Medium term (2-4 years) |

| Chinese OEM CKD/SKD Investments | +0.8% | South Africa, Morocco, Kenya, Rwanda | Short term (≤ 2 years) |

| AfCFTA Tariff Reductions | +0.6% | All 54 member states, early gains in West Africa | Long term (≥ 4 years) |

| Ride-Hailing and Delivery Fleet Expansion | +0.4% | Urban centers across Nigeria, Kenya, South Africa, Ghana | Medium term (2-4 years) |

| Diaspora-Financed Vehicle Purchases | +0.3% | Nigeria, Ghana, Kenya, with spillover to rural areas | Short term (≤ 2 years) |

| Mining-Sector EV Pilot Programs | +0.2% | Zambia, DRC, with expansion potential to Zimbabwe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Passenger-Car Ownership Among Africa's Urban Middle Class

Vehicle ownership closely tracks income gains, and Africa’s middle class is projected to swell toward 1.1 billion people by 2060. Driving incremental demand for personal mobility. Aspirational buyers gravitate toward entry-level and compact passenger models that balance affordability with urban practicality. Financing innovations such as longer-tenor auto loans and subscription models improve affordability, reinforcing the upward demand cycle across the Africa automotive market.

AfCFTA Tariff Reductions Stimulating Intra-Regional Trade

The African Continental Free Trade Area (AfCFTA) will phase out tariffs on 90% of goods, with most non-LDC nations obliged to comply within five years[2]“AfCFTA and Automotive Rules of Origin,”, MONDAQ, mondaq.com. Automotive OEMs stand to gain lower input costs on regional parts procurement, while clear rules of origin encourage local value addition that unlocks preferential tariffs. Forty-six countries have already submitted concession schedules, translating trade liberalization into tangible cost relief for CKD operations. Non-tariff barrier reforms—customs digitization, harmonized standards, and streamlined border procedures—are expected to release an extra USD 20 billion in trade value, a direct boon for the Africa automotive market.

Expansion of Ride-Hailing and Last-Mile Delivery Fleets

Urban congestion and smartphone penetration underpin the meteoric rise of ride-hailing and e-commerce logistics. Uber’s tie-up with Opibus for 3,000 electric motorcycles showcases fleet electrification momentum in Nairobi and Lagos. Ghana-based YomYom is scaling an all-electric fleet to 200 units, proving that route optimization and lower energy costs can cut operating expenses for last-mile operators. These commercial use-cases unlock consistent multi-vehicle orders, supporting sustained growth for light commercial vehicles within the Africa automotive market.

Mining-Sector EV Pilot Programs in Copper-Belt Nations

Zambia and DRC control approximately 70% of global battery minerals, prompting Afreximbank and UNECA to back a transboundary EV Special Economic Zone[3]“Battery Minerals and Regional EV Zone,”, UNECA, uneca.org. Mining houses now test electric pickups for underground operations where zero-emission requirements align with lower ventilation costs. Proximity to cathode materials trims battery logistics expenses, giving regional OEMs a compelling cost advantage. The success of these pilots can catalyze a broader pivot toward electrified commercial vehicles inside the Africa automotive market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Port Congestion and Logistics Bottlenecks | -0.9% | South Africa, Nigeria, Ghana, Kenya | Short term (≤ 2 years) |

| Currency Volatility on Import Costs | -0.7% | Nigeria, Ghana, Kenya, Zambia | Medium term (2-4 years) |

| Grey-Market Used-Vehicle Competition | -0.5% | West Africa corridor, Zimbabwe, Tanzania | Long term (≥ 4 years) |

| Auto-Grade Steel Capacity Shortage | -0.3% | Nigeria, Ghana, Côte d'Ivoire | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic Port Congestion and Inland Logistics Bottlenecks

Durban and Lagos ports rank among the world’s slowest for automotive throughput, inflating dwell times and demurrage fees. Rail under-utilization and aging rolling stock shift traffic onto roads where high tolls and security risks push up landed vehicle costs. For CKD assemblers, inconsistent component arrivals disrupt just-in-time production, while exporters face missed sailing windows that erode supplier credibility. Unless ongoing corridor upgrades and single-window customs systems deliver measurable efficiencies, logistics friction will remain a drag on the Africa automotive market.

Currency Volatility Elevating Import Costs for CKD Kits

Ghanaian importers reported sharp profit erosions when the cedi depreciated, swelling dollar-denominated parts invoices[4]“Currency Risk for Importers,”, University of Cape Coast, ucc.edu.gh. Hedging strategies are expensive, and thinner working-capital buffers make smaller dealers particularly vulnerable. Exchange-rate swings also impair consumers’ price visibility, dampening showroom footfall. Countries with low foreign-currency reserves sporadically tighten import licensing, delaying kit clearances and introducing forecasting uncertainty for plants across the Africa automotive market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Vehicles Accelerate on Logistics Demand

Passenger cars dominated the Africa automotive market with a 66.58% share in 2025, reflecting personal mobility’s appeal across sprawling urban centers. However, freight growth under AfCFTA and booming e-commerce pivot attention toward vans, pickups, and heavy trucks that are forecast to outpace passenger models at an 8.36% CAGR. Light commercial vehicles benefit from last-mile parcel volumes, whereas medium and heavy trucks haul regionally traded goods under harmonized customs corridors. Mining firms quickly test battery-electric dumpers, signaling future substitution opportunities in heavy-duty fleets.

Commercial vehicle assemblers leverage government incentives that waive import duties on chassis and drivetrains, narrowing price gaps versus grey-market used imports. Global production reallocations also matter: Morocco surpassed South Africa in 2024 with 614,000 units, creating a deep supplier base that can pivot toward freight platforms. As logistics players formalize operations, fleet replenishment cycles shorten, sustaining momentum in this segment of the Africa automotive market.

By Propulsion Type: Electric Uptake Gathers Pace from a Low Base

Internal combustion engines retained a 90.68% share in 2025, underscoring affordable fuel and servicing ecosystems. Nevertheless, battery electrics are projected to post a 10.12% CAGR on the back of Chinese OEM launches and fiscal incentives in Rwanda, Kenya, and Egypt. Pre-owned hybrid imports from Japan seed early consumer familiarity with electrified drivetrains, while duty exemptions on EV components lower the total cost of ownership for commercial fleets.

Grid stability constraints slow rollout outside major metros, yet copper-belt mining sites deploy off-grid solar-battery hubs to power electric pickups. Over time, diminishing battery costs and wider charging corridors could unlock a steeper adoption curve, gradually trimming ICE dominance in the African automotive market.

By End-Use: Fleets Outpace Private Ownership

Personal buyers still command 62.05% of 2025 volumes, but institutional demand grows faster as corporates decarbonize mobility profiles and ride-hailing apps finance multi-vehicle acquisitions via revenue-share models. Fleet managers exploit bulk-procurement discounts and telematics to optimize uptime, while residual-value guarantees shorten replacement cycles to four years or less.

Government leasing programs stipulate minimum local content, nudging CKD plants toward higher localization thresholds. This virtuous loop reinforces assembly economies of scale, widening the addressable fleet base for the Africa automotive market.

By Sales Channel: Assembly Gains Policy Tailwinds

Completely built-up imports held a 49.15% share in 2025, yet SKD/CKD assembly is forecast to climb at an 8.19% CAGR as tariff differentials widen under local-manufacturing mandates. Nigeria’s updated NAIDP targets 40% local content by 2033, offering VAT waivers on tools and parts to qualifying investors. Kenya enforces age caps on used imports, channeling demand toward locally assembled models while granting excise rebates to dealers that meet employment thresholds.

Chinese OEMs capitalize by shipping knock-down kits to avoid restrictive tariffs applied to finished vehicles. This deepens the Africa automotive market’s manufacturing base and gradually weans customers away from fully imported choices.

Geography Analysis

South Africa contributed 37.85% of regional volumes in 2025, anchored by a mature supplier ecosystem and preferential EU trade access. Yet Nigeria’s 8.94% forecast CAGR reflects pent-up demand in Africa’s most populous nation, supported by AfCFTA-linked duty waivers on parts and vehicles. Morocco’s coastal plants now export SUVs and compact cars to Europe tariff-free under the Agadir Agreement, diversifying Africa’s production footprint beyond the southern cone.

Regional hubs like Ghana and Kenya leverage automotive policies to court investors, banking on strategic port locations and growing consumer bases. Collectively, these markets amplify growth for the African automotive market by spreading production risk and stimulating healthy competition among investment destinations. East Africa gains traction through harmonized customs codes and shared infrastructure. Kenya restricts used-car imports over eight years old, steering buyers toward new or locally built options, while Ethiopia orders thousands of EVs for state fleets to cut fuel import bills. Rwanda’s incentive package for electric buses catalyzes BYD and Chery deployments, forming a demonstrator corridor for zero-emission public transport. These policy moves collectively shape an ecosystem that fosters healthy geographic diversification for the Africa automotive market.

Regulatory Landscape

Africa automotive regulation is converging around regional trade and assembly frameworks alongside country-level industrial policy. In February 2026, the African Union adopted AfCFTA automotive Rules of Origin for HS 8701-8716, anchoring preferential treatment to a minimum 40% African originating content threshold (with an interim ceiling on non-originating materials). This approach raises the compliance bar for assemblers and parts suppliers operating across borders.

Sub-regional and national measures also shape market access and localization requirements. The East African Community issued the EAC Assembling and Manufacturing of Products Regulations, 2025, which come into force on July 1, 2026, and establish a structured assembly framework for motor vehicles and e-mobility to reduce regulatory fragmentation across partner states. In South Africa, the Department of Trade, Industry and Competition signaled a review of APDP 2 via a May 2026 notice, including measures linked to EV battery manufacturing support. Homologation requirements are also influenced by ARS 1595-2021, with additional model requirements referenced for vehicles manufactured or imported for sale from January 1, 2028.

Value Chain Analysis

The Africa automotive value chain remains import-dependent for upstream inputs and kit-based assembly, with deeper manufacturing concentrated in a limited number of hubs. Vehicle and component production clusters in Morocco and South Africa sit alongside expanding assembly footprints in Egypt, Kenya, and Ghana. At the same time, powertrain components, electronics, and many stamped parts continue to be sourced from outside the region due to limited auto-grade materials and uneven supplier capability.

AfCFTA implementation is a key enabler for shifting the chain from CKD/SKD toward localized components and cross-border supplier networks. The February 2026 adoption of AfCFTA automotive Rules of Origin (HS 8701-8716) provides an origin-based pathway for intra-African trade, strengthening incentives to localize sub-assemblies such as wiring harnesses, interiors, and selected chassis components where feasible. Industry coordination is also visible through the African Association of Automotive Manufacturers (AAAM), which set 2026 priorities including enabling legislation for new-energy vehicles, linking mineral beneficiation to automotive manufacturing, and attracting new component investments. This alignment ties upstream mining capabilities to downstream vehicle and battery-related opportunities.

Competitive Landscape

Competition is moderate and intensifying. Toyota, Volkswagen, and Hyundai still leverage long-standing dealer networks, robust after-sales, and brand trust to command showroom traffic. However, Chinese entrants expanded their share from 2% in 2019 to 9% in 2024 by coupling aggressive pricing with advanced tech features and extended warranties [CNBCAF RICA.COM]. BYD’s vertical integration—from battery chemistry to semiconductor design—keeps costs low, allowing the company to broaden its South African line-up to six models by April 2025.

Local manufacturers exploit niche opportunities. Nigeria’s Innoson Vehicle Manufacturing produces minibuses tailored for West African road conditions, while Kenyan startups assemble electric motorcycles for courier fleets. Strategic alliances—such as BYD partnering with Associated Vehicle Assemblers in Mombasa—merge global technology with local assembly knowledge, reinforcing value addition inside the Africa automotive market.

Policy and technology convergence will reshape the competitive set. AfCFTA’s origin rules favor companies with regional footprints, while digital retail platforms allow newcomers to bypass legacy showrooms. Winners will be those that blend cost-effective assembly, accessible financing, and service networks attuned to rugged operating environments. Given current shares, the Africa automotive market exhibits a balanced rivalry where no single player holds overwhelming dominance.

Africa Automotive Industry Leaders

Volkswagen AG

Toyota Motor Corporation

Groupe Renault

Hyundai Motor Corporation

Ford Motor Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

AfCFTA-compliant localization and cross-border supply chains offer a tangible opportunity set as the preferential trade basis tightens. The African Union adoption of AfCFTA automotive Rules of Origin in February 2026 (HS 8701-8716, minimum 40% African content) creates room for suppliers to support assemblers in meeting origin thresholds, including sub-assemblies and components that move efficiently within the region (such as harnesses, seats, plastics, and selected metal parts). AAAMs 2026 agenda to secure additional component investments and advance mineral beneficiation also supports the case for placing intermediate manufacturing near major assembly nodes rather than relying only on imported kits.

Policy-backed electrification and fleet procurement programs create clearer growth lanes for hybrids, EVs, and mass transit platforms. The EAC Assembling and Manufacturing of Products Regulations, 2025, which take effect on July 1, 2026, formalize an assembly framework that explicitly covers e-mobility and helps standardize market entry for OEMs and local assemblers across East Africa. Demand-side and manufacturing incentives add momentum: Nigeria directed a waiver of import duties for electric vehicles and mass transit buses in 2026, while South Africa introduced a 150% tax deduction incentive for new-energy vehicle production under the Automotive Masterplan 2035, and Ghana initiated consultations in February 2026 on a revised Ghana Automotive Development Policy Phase II to incorporate EVs and two-wheelers. Together, these programs expand the pipeline for localized assembly, charging-adjacent services, and fleet-oriented financing models in the Africa automotive market.

Recent Industry Developments

- June 2026: CFAO Mobility Kenya commissioned a new Toyota HiAce assembly line at Kenya Vehicle Manufacturers (KVM) in Thika, supported by a total Sh2.4 billion investment and linked to its increased stake in KVM. The project expands local assembly capacity for a high-volume commercial model and strengthens East Africa as an assembly node aligned with regional localization objectives.

- March 2025: Ford South Africa commenced full-scale production of the Ranger Plug-in Hybrid Electric Vehicle (PHEV) at the Silverton Manufacturing Plant, positioned as the global production hub for the model. This adds electrified powertrain manufacturing capability in the region and supports fleet decarbonization demand, reinforcing South Africa's role in export-oriented vehicle production.

- April 2024: Volkswagen announced a ZAR 4 billion investment to upgrade its Kariega plant in South Africa, including preparations associated with adding a third model line targeted for 2027. The upgrade lifts the plant's competitiveness for multi-model production and supports regional supply-chain demand for locally sourced components and services tied to higher throughput.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this outlook, the market covers the value of vehicles sold across Africa, counted at the point of sale into the market and captured in USD for the stated base year.

Scope exclusions: Aftermarket parts, standalone repair services, and insurance are not counted unless they are bundled into a vehicle sale price.

Segmentation Overview

- By Vehicle Type

- Passenger Cars

- Hatchback

- Sedan

- SUV & Crossover

- MPV & Others

- Commercial Vehicles

- Light Commercial Vehicles (LCV)

- Medium & Heavy Trucks

- Buses & Coaches

- Passenger Cars

- By Propulsion Type

- Internal Combustion Engine (ICE)

- Hybrid Electric Vehicle (HEV)

- Battery Electric Vehicle (BEV)

- Alternative Fuels (CNG/LPG, Flex-fuel, FCEV)

- By End-Use

- Personal Ownership

- Fleet & Leasing

- Ride-hailing / Mobility Service Providers

- Government & Institutional

- By Sales Channel

- Completely Built-up Imports (CBU)

- Semi/Completely Knocked-down Assembly (SKD/CKD)

- Used-Vehicle Imports

- By Country

- South Africa

- Morocco

- Algeria

- Egypt

- Nigeria

- Ghana

- Kenya

- Rest of Africa

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the boundaries of the Africa vehicle market and to build a practical demand and supply picture before any modeling started. We referenced public sources such as national statistics offices and customs authorities for registration and trade signals, and transport and road-safety agencies for parc and licensing context.

To anchor country trends, we also used sources such as OICA-style production and sales releases, African development and macro indicators from institutions such as the World Bank and the IMF, and tariff and policy notes published by governments. Company annual reports, investor decks, and reputable press were reviewed to understand assembly plans, import dependence, and pricing direction, and then a paid subscription database for company financials, news, and import-export shipment patterns was used selectively to cross-check directional assumptions. The sources listed here are illustrative only, and additional public and paid references were used for data collection, clarification, and validation.

Primary Interviews and Surveys

Primary work focused on validating what the desk research could not reliably show, especially how imported CBU volumes compare with CKD and SKD assembly flows and how pricing is moving by fuel type. We spoke with a mix of OEM-side and channel-side experts, plus fleet and financing stakeholders across key auto markets. Inputs were then used to confirm conversion factors, remove double counting, and stress-test the final totals by region.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 12% | |

| Mid tier: 52% | Functional/Unit leaders: 29% | |

| Smaller Players: 15% | Managers: 59% |

Market-Sizing & Forecasting

The sizing starts from a top-down reconstruction of the addressable vehicle sales pool across Africa using a country build guided by registration direction, imports and exports, and local assembly output, which are then translated into value using observed price bands. Once the regional totals are shaped, we corroborate them with selective bottom-up checks such as sampled ASP times volume logic by vehicle type, and a reasonableness roll-up of reported revenue exposure for relevant suppliers and assemblers.

Key inputs used in the model include new vehicle sales momentum, used-vehicle import intensity, the mix shift between passenger and commercial vehicles, the fuel mix transition (petrol, diesel, electric, and alternative fuels), and policy signals such as tariff changes or local content rules that affect price and availability. Where country-level datapoints were missing, gaps were handled using peer-market proxies within Africa and then rechecked with interview feedback so outliers did not drive the regional curve.

For forecasting, scenario analysis was used around macro growth, currency pressure, and policy changes, and it was paired with a simple time-series smoothing step to keep year-to-year movement practical. Assumptions on volume growth and price progression were reviewed with primary respondents so the trajectory reflects typical lead times for imports, assembly ramp-ups, and financing conditions.

Data Validation & Update Cycle

Outputs are validated through multiple checks before sign-off, including cross-verifying the implied vehicle volumes against independent registration and trade signals and confirming that the value trend matches the direction of pricing and mix shifts. When a country shows an unusual jump or drop, analysts revisit inputs, recheck calculations, and re-contact sources to confirm whether the change is policy-led, currency-led, or data noise.

A second analyst review is completed to test sensitivity to key assumptions, and then a final consistency review is done across countries so the Africa total is not driven by one market artifact. Reports are refreshed annually, with interim updates triggered when material events occur, and before delivery a final pass is done to ensure the latest policy and trade developments are reflected.

Mordor Intelligence's Africa Automotive Industry Outlook Market Estimate Compared With Other Published Estimates

Published market sizes for Africa automotive can look different because the underlying boundaries are not always aligned, even when the titles sound similar. The gaps usually come from whether the value is built from unit flows or from broad revenue proxies, how used-vehicle imports are treated, and whether assembly formats are counted consistently.

Registration trends, import and export direction, and announced assembly output are the checks that keep Mordor Intelligence's estimate tied to a traceable demand pool, instead of being driven mainly by high-level macro ratios. Differences also show up when other publishers use a different base year, apply a faster ASP uplift without checking currency timing, or refresh less often after policy moves in major markets.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 21.55 B (2025) | |

| Trade Portal A | USD 20.50 B (2024) | Uses a 2024 base year and can understate value when mix shifts and currency timing push realized prices up in 2025, and scope detail on used imports and assembly formats is not clearly stated. |

| Regional Publisher B | USD 22.16 B (2025) | Often applies broad regional growth and ASP progression across countries, which can over-smooth markets where tariff changes and import constraints create uneven year-to-year volumes. |

The spread in the table is mainly explained by base-year choice and how price and mix are translated from unit signals into USD value. By keeping the build tied to observable trade, registration, and assembly indicators and then pressure-testing the price curve with interview feedback, the final number stays transparent and repeatable for planning use.

Key Questions Answered in the Report

What is the current value of the Africa automotive market?

The market is valued at USD 22.63 billion in 2026 and is forecast to reach USD 28.93 billion by 2031.

Which country holds the largest share of vehicle production on the continent?

Morocco produced 614,000 units in 2024, edging past South Africa to become Africa’s largest producer.

Which segment is expanding quickest in terms of vehicle type?

Commercial vehicles, propelled by e-commerce and logistics demand, are set to grow at an 8.36% CAGR to 2031.

Why are Chinese automakers investing heavily in Africa?

Trade barriers elsewhere and AfCFTA tariff advantages make Africa an attractive growth frontier, allowing Chinese OEMs to capture share through CKD/SKD assembly and competitive pricing.

What are the main challenges limiting faster market growth?

Chronic port congestion, currency volatility, widespread used-vehicle imports, and limited local supply of ISO-certified auto-grade steel are the primary hurdles.

Page last updated on: