Africa Cashew Market Analysis by Mordor Intelligence

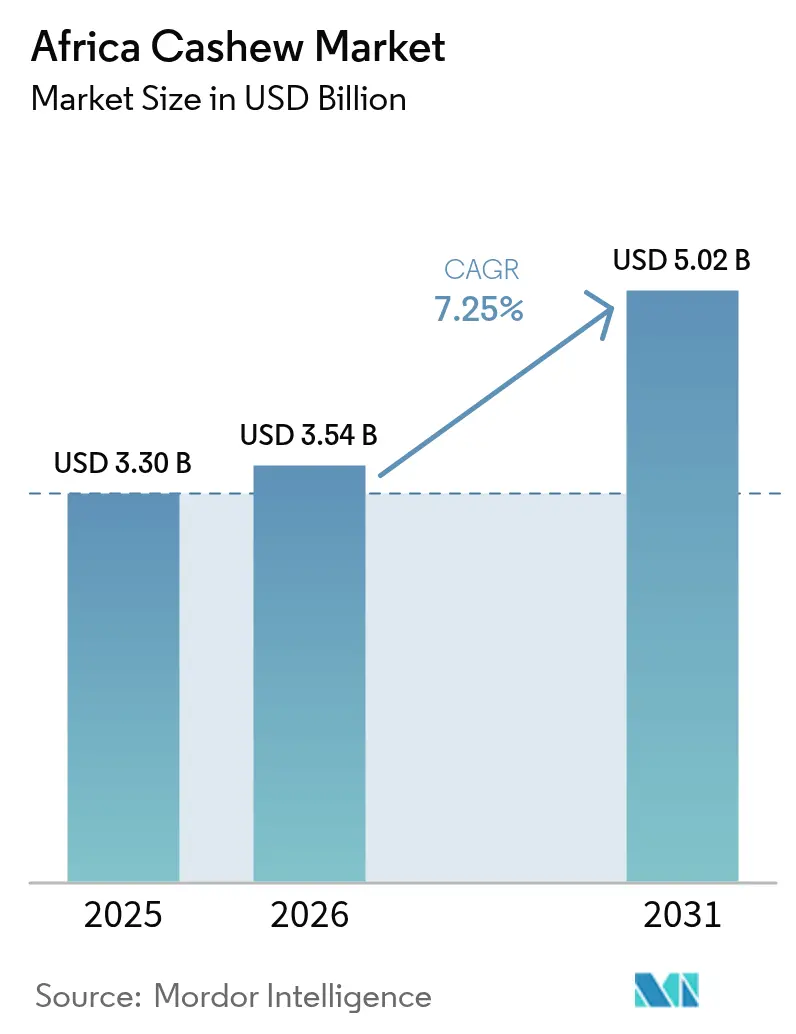

The Africa Cashew market size was valued at USD 3.3 billion in 2025 and estimated to grow from USD 3.54 billion in 2026 to reach USD 5.02 billion by 2031, at a CAGR of 7.25% during the forecast period (2026-2031). The market growth is driven by a transition from raw-nut exports to value-added kernel processing, supported by government incentives and European sustainability requirements. Increased farm-gate prices, traceability systems yielding 8-10% retail premiums, and climate-resilient cultivars encourage processors to enhance capacity and obtain certifications for premium market access. Ivory Coast (Côte d'Ivoire) is Africa's largest cashew-producing country and the global leader in raw cashew nut production and exports. According to the Food and Agriculture Organization (FAO), Côte d'Ivoire's cashew nut production increased from 1,028,172 metric tons in 2022 to 1,044,449.95 metric tons in 2023[1]Source: Food and Agriculture Organization of the United Nations, “FAOSTAT Crops and Livestock Products Database – Cashew Nuts, Côte d’Ivoire,” fao.org. Cashew plants begin fruit production four to five years after planting and maintain optimal productivity for approximately 15 years. In Côte d'Ivoire, more than 10% of cashew trees are less than ten years old, resulting in higher yields. The country continues to expand its cashew acreage annually with improved varieties, strengthening its position as Africa's primary cashew exporter.

Key Report Takeaways

- By country, Côte d’Ivoire led with 35.45% revenue share of the Africa Cashew market size in 2025, while Nigeria is projected to grow the fastest at a 8.85% CAGR through 2031.

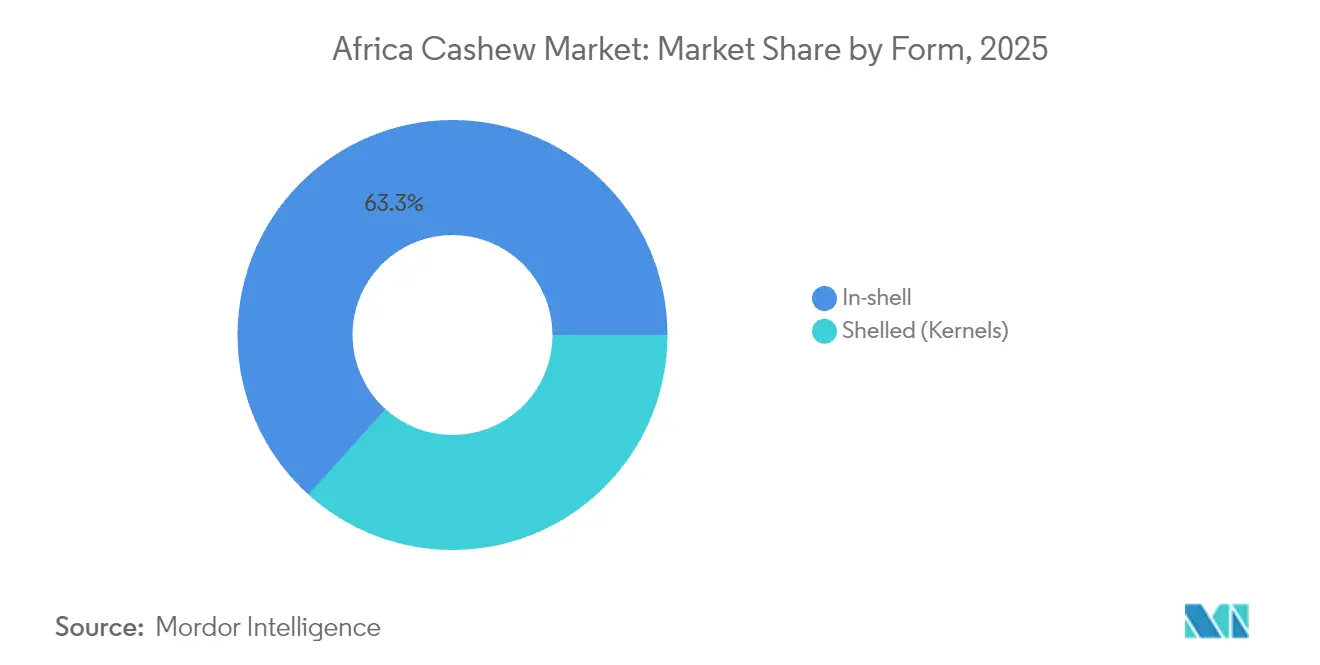

- By form, in-shell cashews accounted for 63.30% of the Africa Cashew market size in 2025, shelled kernels are anticipated to advance at an 10.83% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Cashew Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher demand for African cashews from European healthy-snack brands | +1.2% | Europe, and West Africa | Medium term (2-4 years) |

| Rising farm-gate prices spurring farmland expansion | +1.0% | West Africa, and East Africa | Short term (≤ 2 years) |

| Government processing incentives across West Africa | +1.5% | West Africa | Medium term (2-4 years) |

| Climate-resilient cashew cultivars boosting yields | +0.8% | Sahel, and East Africa | Long term (≥ 4 years) |

| Blockchain-based traceability commanding price premiums | +0.6% | Global premium markets | Medium term (2-4 years) |

| European Union and United States sustainability sourcing mandates | +1.1% | Global export regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Demand For African Cashews from European Healthy-Snack Brands

European healthy-snack brands are turning to African cashews to supply plant-based, low-sugar product lines that attract consumers seeking sustainable ingredients. Import volumes have surged in Nordic markets and Germany, where traceable organic kernels sell at sizable premiums, motivating African processors to secure certifications and direct-trade agreements that bypass commodity intermediaries [2].Source: CBI, “Entering the European Market for Cashew Nuts,” cbi.eu Processing firms now tailor safety protocols to BRCGS (British Retail Consortium Global Standards) standards, enabling consistent quality that satisfies European retailers. Investment priorities across West African plants increasingly favor HACCP (Hazard Analysis and Critical Control Points) programs and allergen-control systems that support premium positioning. These upgrades consolidate long-term contracts that stabilize processor cash flows and underpin continued expansion of the Africa Cashew market.

Government Processing Incentives Across West Africa

West African governments are launching five-year tax holidays, duty-free machinery imports, and preferential land leases to spur domestic kernel production. The Cotton and Cashew Council in Côte d’Ivoire orchestrates sector policies that taper export levies on processed nuts, while Sierra Leone’s Finance Act 2025 exempts qualifying processors from corporate income tax and customs duties. Burkina Faso’s outright export ban on raw nuts redirects 200,000 metric tons to domestic factories, providing reliable throughput that justifies further plant investments[3]Source: United Nations Conference on Trade and Development, “Sierra Leone – The Finance Act 2025 Introduces New Investment Incentives,” Investment Policy Monitor, investmentpolicy.unctad.org. These coordinated measures reduce reliance on Asian processing centers, keeping more value inside Africa and reinforcing the growth trajectory of the African cashew market.

Climate-Resilient Cashew Cultivars Boosting Yields

Research alliances have released drought-tolerant varieties that yield 20% more in semi-arid zones, shielding farmers from rainfall volatility that once limited acreage expansion. Field trials in Benin show survival advantages during prolonged dry spells, and adoption rates are climbing as extension services supply elite seedlings. Complementary water-management and mulching practices, already used by 71.8% of growers, amplify cultivar gains, strengthening production growth that underpins future Africa Cashew market supply.

Blockchain-Based Traceability Commanding Price Premiums

Quick Response (QR)-enabled blockchain ledgers nowadays trace kernels from plot coordinates to retail shelves, meeting European Union Deforestation Regulation requirements and earning processors 8-10% higher shelf prices. Firms like Tolaro Global embed lot-level data in smart contracts that cannot be altered, satisfying retailer audits and consumer transparency expectations. Over 5,400 Ghanaian farmers receive mobile payments through Olam’s direct-purchase app, cutting intermediaries and lifting household earnings. These digital systems elevate Africa’s reputation for reliably sourced cashews, fortifying the premium tier of the Africa Cashew market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited domestic processing capacity | -1.8% | West and East Africa | Medium term (2-4 years) |

| Persistent price disparity from farm-gate to retail | -1.2% | Smallholder regions | Long term (≥ 4 years) |

| Quality losses from inadequate post-harvest handling | -0.9% | Rural production areas | Short term (≤ 2 years) |

| Port-side logistics bottlenecks and container shortages | -0.7% | Coastal export hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Domestic Processing Capacity

Africa still processes only 15-20% of its crop, forfeiting kernel-level margins to Asian plants. Tanzania illustrates the shortfall: despite an annual production of roughly 200,000-250,000 metric tons, domestic factories treat as little as 5-15%, forcing exporters to ship raw nuts that attract lower prices. Ghana exports more than 80% of its 180,000 metric tons of unprocessed, even though kernels would earn multiple times the raw-nut price. High interest rates and unreliable electricity raise operating costs, while scale disadvantages keep per-unit costs above those of mature Asian competitors. Such constraints slow the transition toward value-added activities that would otherwise accelerate the Africa Cashew market.

Quality Losses From Inadequate Post-Harvest Handling

Improper drying, storage, and sorting expose nuts to mold and moisture that trigger EU border rejections and damage supplier reputations. Studies in coastal Kenya found that 22.22% of Aspergillus isolates from cashew samples were aflatoxigenic, confirming widespread contamination risks. Without adequate warehouses or moisture meters, smallholders struggle to achieve reliable kernel grades, eroding processor throughput and increasing quality-related losses. Tackling this issue requires joint investments in village-level drying racks, hermetic bags, and farmer training, a capital-intensive fix that many fragmented supply chains cannot fund, restraining overall Africa Cashew market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Processing Shift Accelerates Kernel Growth

In-shell cashews dominated with a 63.30% share in 2025, mirroring the historic emphasis on raw-nut exports to Asia, where kernel splitting is concentrated. The segment is slowly ceding ground as African factories gain scale. The Africa Cashew market size for in-shell nuts is likely to plateau as more volume is diverted to domestic processors.

Shelled kernels represent the fastest-growing form at an 10.83% CAGR through 2031, spurred by domestic incentives, concessional financing, and sustainability-linked premiums. New facilities, such as Burkina Faso’s USD 11.5 million plant in Péni that processes 5,000 metric tons annually and creates 1,000 jobs, exemplify the shift. Kernel processors increasingly seek organic and BRCGS (Brand Reputation through Compliance Global Standards) certification, enabling direct sales into European snack channels that prize traceable supply chains. The African Cashew Alliance’s Quality and Sustainability Seal further reduces buyer risk and accelerates contract commitments. Growing kernel output is therefore set to capture a larger slice of the African cashew market share over the outlook period.

Geography Analysis

West Africa commanded 84.55% of the Africa Cashew market in 2025 and is poised to expand at an 7.92% CAGR to 2031. The region benefits from favorable agro-ecological conditions and harmonized policy frameworks that collectively aim to process a higher proportion of the crop locally. Côte d’Ivoire’s output exceeds 1.25 million metric tons, while Benin and Nigeria are pushing ministry-level roadmaps to align export restrictions with factory expansion projects. Regional bodies promote shared shell-oil extraction and apple fermentation facilities to unlock ancillary revenue streams, further deepening the Africa Cashew market.

East Africa holds a 10.65% share, led by Tanzania’s 7.2% contribution and USD 340 million export receipts, but processing ratios remain below 15% of production. Policy makers are revisiting tax concessions and power-reliability incentives to attract kernel investors. Kenya’s coastal orchards offer growth potential provided farmers adopt disease-resistant varieties that combat powdery mildew. The ComCashew initiative demonstrates the gains possible when donor and government programs coordinate inputs, credit, and training, yielding rapid income uplift for participating households

Central and Southern African producers remain minor contributors but represent long-run upside. Burundi and Mozambique are experimenting with climate-resilient cultivars suited to their latitudes, while Angola is piloting intercropped cashew-maize systems that stabilize farmer revenue. Although their current combined share is below 5%, improvements in logistics infrastructure and regional trade agreements could integrate these countries more deeply into the Africa Cashew market over the next decade.

Regulatory Landscape

Cashew policy across Africa is increasingly designed to retain more value domestically by directing raw cashew nuts (RCN) toward local processing. In Togo, a ministerial order issued in December 2025 required licensed buyers and cooperatives to supply at least one-third of collected RCN to domestic processors before exporting, and an export tax on raw cashew nuts took effect from January 1, 2026, reinforcing a processing-first approach.

Price setting and compliance enforcement are also becoming more formalized. Ghana approved a minimum producer price of GH12 per kilogram for the 2025/2026 season under the Tree Crops Development Authority (TCDA) framework (Tree Crops Development Authority Act, 2019 (Act 1010) and Regulations L.I. 2471 (2023)), and in 2026 the TCDA commissioned Compliance and Enforcement Officers to work with security agencies and District Assemblies to curb smuggling and illegal trading. In Cote d'Ivoire, the Cotton and Cashew Council (CCA) supported local processors in 2025 by reserving exclusive raw cashew procurement windows at the start of the season, alongside measures that favor local transformation over raw exports.

Value Chain Analysis

The Africa cashew value chain runs from smallholder input supply (seedlings, extension, agrochemicals) to orchard production, collection by aggregators and licensed buyers, primary trading, and then either export of in-shell RCN or domestic processing into kernels and by-products, notably cashew nut shell liquid (CNSL). Post-harvest handling (drying, storage, sorting) is a key value-preservation step because quality defects can trigger buyer claims and border rejections, while traceability requirements for premium channels increasingly add geolocation and lot-level data capture to the chain.

Processing and export are concentrated in West Africa, where scale and policy incentives have expanded capacity, led by Cote d'Ivoire. The country increased processing capacity from about 68,500 tonnes in 2015 to about 350,000 tonnes in 2024. Working-capital constraints remain a recurring bottleneck for processors during the harvest buying season, contributing to liquidity-driven behaviors such as exporting semi-processed kernels to finance operations. Cross-border trade also faces friction from fragmented sanitary and phytosanitary rules and differing testing standards, while EU deforestation-related due diligence is accelerating adoption of digital traceability systems that link farmers, volumes, and origin documentation through the supply chain.

Market Opportunities and Future Outlook

Local kernel manufacturing and by-product valorization present a clear expansion opportunity, since Africa still processes only a minority share of its crop even as governments tighten incentives and mandates to keep raw nuts onshore. Investment and credit-enhancement activity provides an evidence-backed pathway for scaling plants: in February 2026, GuarantCo backed a USD 75 million debt facility for Robust International to build a new processing plant in Ogun State, Nigeria, targeting an increase in daily processing capacity from 100 MT to 220 MT. Policy-driven demand for local throughput is also visible in Togo, where measures introduced around January to March 2026, including an export tax and a one-third local supply quota for licensed buyers, aim to secure raw material for domestic factories.

Premium-market access built on traceability and compliance is another opportunity area, supported by observed price premiums for verifiable supply chains and the growing role of digital systems and standards, including BRCGS and HACCP programs in export-facing plants. Sector-wide scale-up in West Africa is already visible through processing volumes reported at 732,000 tons in 2025, up 51% from 2024, led by Cote d'Ivoire. The region also has a growing plant base, with 37 operational processors in Cote d'Ivoire in 2025 and 830,000 tons of installed capacity, which supports more bankable expansions, contract manufacturing for international brands, and higher utilization of existing assets.

Recent Industry Developments

- May 2026: Dorado SA secured a loan of up to USD 60 million (EUR 51 million) from the European Bank for Reconstruction and Development to support sustainable cashew value chains in Cote d'Ivoire, including expanded processing capacity. The transaction highlights continued use of development finance to de-risk capex and working-capital needs in the region's largest producing and processing hub.

- February 2026: Robust International secured a USD 75 million debt facility backed by a 100% guarantee from GuarantCo to construct a new cashew processing plant in Ogun State, Nigeria, doubling planned daily processing capacity from 100 MT to 220 MT. The credit-enhancement structure lowers financing barriers for industrial-scale processing and strengthens Nigeria's local value-add push.

- June 2024: Cashew Coast raised EUR 9 million from AgDevCo to expand its traceable organic cashew processing business in Cote d'Ivoire, including new warehouses and a target to increase processed volumes to 19,000 tonnes per year. The investment supports higher-throughput processing and better post-harvest logistics aligned with premium, traceable kernel demand.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Africa cashew market is measured as the value generated from cashew nuts traded and consumed across African countries, covering in-shell nuts and shelled kernels. The sizing is built around production, trade flows, and price formation that connect farm output to domestic use and exports.

Scope exclusions: Cashew-derived byproducts such as cashew nut shell liquid and apple-based beverages are excluded from the market value in this methodology.

Segmentation Overview

- By Country (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis)

- Nigeria

- Côte d'Ivoire

- Benin

- Tanzania

- Burundi

- Ghana

- Guinea-Bissau

- Burkina Faso

- By Form (Value)

- In-shell

- Shelled (Kernels)

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the measurable cashew value chain in Africa and to set the starting points for volumes, trade direction, and price ranges. We relied on public sources such as FAOSTAT for agricultural output, UN Comtrade for import-export patterns, and International Trade Centre dashboards for trade structure and unit values.

To keep the inputs practical at the country level, supporting references were reviewed from sources such as national agriculture ministries and statistics offices, central bank or customs releases, and publications from cashew and nut trade associations. Company annual reports, investor presentations, and reputable press were used to understand processing capacity additions and export market shifts. In addition, a paid subscription for company financials and an import-export shipment-level dataset were used selectively to sanity-check company scale and shipment timing. These examples are illustrative, and many other public and paid sources were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was carried out through expert interviews and structured surveys with stakeholders across farming-linked buying, processing, exporting, and distribution, so the key gaps from desk research could be closed. These conversations were also used to confirm country differences in farm-gate pricing, kernel recovery and processing yield expectations, and the split between in-shell sales versus processed kernels, and then to cross-check the logic across major producing and trading corridors in Africa.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 16% | |

| Mid tier: 56% | Functional/Unit leaders: 41% | |

| Smaller Players: 16% | Managers: 43% |

Market-Sizing & Forecasting

The market model starts with a top-down build where production and trade data are used to reconstruct the available supply pool by country, which is then aligned with consumption and export channels using observed unit values. Once that core structure is in place, we corroborate it with selective bottom-up approximations such as sampled exporter volumes, processor capacity-to-throughput checks, and price times volume calculations for in-shell and kernel flows.

A few market fingerprints were used as key inputs because they move the value materially and can be cross-verified. These include national production volumes, export and import volumes, kernel recovery and processing yield expectations, average unit values by form, and the share of output that is processed locally versus shipped as raw nuts. Where a data point is missing for a smaller origin, proxy assumptions were applied from nearby markets with similar harvesting season and trade routes, then adjusted after expert feedback.

For forecasting, scenario analysis was used so the outlook could flex with plausible shifts in processing capacity utilization, farm-gate price direction, export demand, and logistics constraints. The final forward view was then tuned using consensus ranges heard in interviews, so the annual progression stays realistic rather than being driven by a single aggressive or conservative assumption.

Data Validation & Update Cycle

Outputs were validated through triangulation across production, trade, and pricing signals, followed by variance checks at the country and regional total levels. When a country showed an unusual jump in value, the drivers were re-tested against export volumes, unit value movement, and known processing expansions, and then reviewed again before sign-off.

Reports are refreshed annually, and interim updates are made when material events occur, such as major policy shifts, supply shocks, or step-changes in processing capacity. Before delivery, a final pass is completed so the numbers and commentary reflect the latest available public data and the most recent primary feedback.

Mordor Intelligence's Africa Cashew Market Size Compared With Other Published Estimates

Published market sizes for Africa cashew do not always match because the underlying counting can vary, even when the topic name looks the same. Differences usually come from what is included in the value chain, which year is treated as the base, and whether the estimate is tied back to observable production and trade signals.

Cashew byproducts and cashew-apple based items are often folded into some totals, and that item sits outside Mordor Intelligence's scope for this market, which keeps the value closer to in-shell and kernel economics. Gaps also show up when one estimate leans heavily on a single price series or a single trade lens, instead of reconciling production volumes, export flows, and unit values together, followed by a slower refresh cadence that misses recent capacity and price shifts.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.30 B (2025) | |

| Trade Platform Summary A | USD 0.82 B (2024) | Uses a different base year and appears to reflect a narrower value capture that can behave more like traded kernel and selected channel value, which can undercount in-shell volumes and broader Africa coverage. |

| Regional Consultancy B | USD 0.89 B (2025) | Often reported with a smaller scope of countries and segment framing that can emphasize packaged or downstream channels, which shifts the total away from production and export-linked valuation. |

The spread in the table is mainly explained by how far up or down the value chain each publisher counts, and how directly the totals are reconciled to production, trade, and price checks. By keeping the steps traceable to repeatable inputs and re-checking the totals against independent signals, the estimate remains a practical number for planning and comparisons.

Key Questions Answered in the Report

How large will Africa's cashew sector be by 2031?

The Africa Cashew market is forecast to reach USD 5.02 billion by 2031, growing at a 7.25% CAGR from 2026

Which African country processes the most cashews today?

Côte d'Ivoire leads with 35.45% share and has surpassed India in processed-kernel exports

What is driving premium pricing for African kernels in Europe?

Blockchain-based traceability and sustainability certifications command 8-10% retail premiums in European healthy-snack channels

Why is Nigeria considered the fastest-growing producer?

Afrexim banks USD 20.8 million financing and expanding factory base underpin Nigeria's 8.85% forecast CAGR.

What limits Africa's processing capacity?

High equipment financing costs, unreliable power supply, and quality-control gaps restrict factories to treating only 15-20% of the crop locally

How are governments encouraging local value addition?

Policies such as five-year tax holidays, export bans on raw nuts, and duty-free imports of machinery are designed to shift value capture toward domestic processing

Page last updated on: