Tanzania Agriculture Market Analysis by Mordor Intelligence

The Tanzanian agriculture market size is expected to grow from USD 22.9 billion in 2025 to USD 24.12 billion in 2026 and is forecast to reach USD 31.26 billion by 2031 at 5.33% CAGR over 2026-2031. Government outlays through the Agricultural Sector Development Programme (ASDP) and allied donor finance are modernizing farming systems, accelerating irrigation expansion, and promoting youth engagement[1]Source: African Development Bank Group, “Tanzania Agricultural Transformation,” afdb.org. Tanzania’s 128% food self-sufficiency permits surplus exports across the East African Community (EAC), while policy incentives target a shift from raw commodity sales toward in-country processing, most visibly in cashews. Foreign direct investment in agro-industrial parks and block-farm schemes is also reshaping production hubs, though infrastructure shortfalls and climate volatility remain pronounced headwinds.

Key Report Takeaways

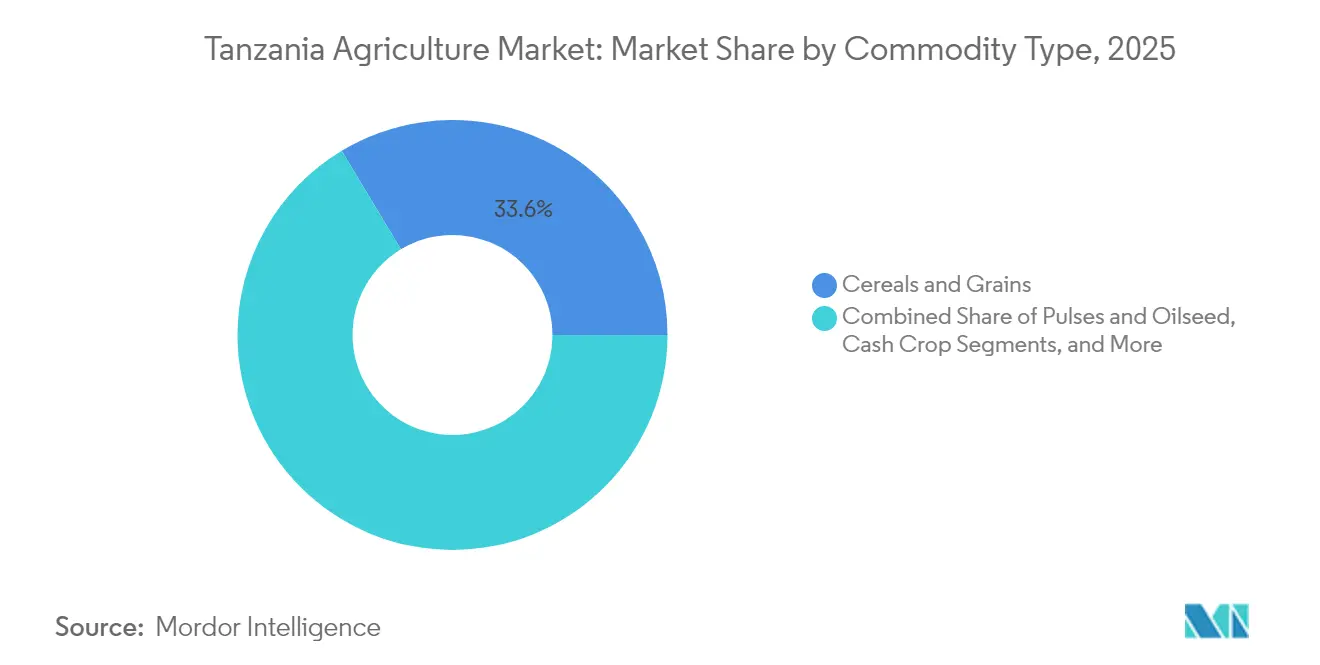

- By commodity type, cereals and grains led with 33.62% of Tanzanian agriculture market share in 2025, while fruits and vegetables are projected to advance at a 11.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Tanzania Agriculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government investments and ASDP rollout | +1.2% | National, with priority regions including the Southern Highlands and the Coastal zones | Medium term (2-4 years) |

| Expanding demand for staple and cash crops | +0.8% | Global export markets, regional EAC trade corridors | Long term (≥ 4 years) |

| Rapid uptake of mobile-enabled extension and fintech | +0.6% | Rural areas with mobile network coverage, concentrated in the Dar es Salaam and Dodoma regions. | Short term (≤ 2 years) |

| EU phytosanitary alignment opening premium export channels | +0.4% | Export-oriented regions, including Mtwara, Lindi, and Ruvuma, for cashews | Medium term (2-4 years) |

| Climate-smart irrigation funding via the Green Climate Fund | +0.7% | Semi-arid regions, including Simiyu, Dodoma, and Tabora | Long term (≥ 4 years) |

| Rise of contract farming and commodity exchanges | +0.5% | Commercial farming zones and areas with established value chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Investments and ASDP Rollout

ASDP Phase II channels public finance into fertilizers, certified seed, and mechanization, directly reversing years of underinvestment. The program anchors the broader Kilimo Kwanza framework and has already raised national fertilizer usage, a move credited with Tanzania’s food self-sufficiency target. Revival of the Tanzania Fertilizer Company underscores the intent to stabilize input pricing, while the ruling CCM’s 2025–2030 manifesto commits to higher producer prices for cashews, coffee, and cotton. Priority spending covers feeder-road upgrades, grain storage, and on-farm solar pumps, all of which link remote growers to markets.

Expanding Demand for Staple and Cash Crops

Agricultural exports reached USD 2.9 billion in Q4 2024, buoyed by coffee, tobacco, and cotton price rallies. Coffee earnings jumped 41.38% year-on-year to USD 227.9 million, while tobacco sales climbed 90.68% to USD 340.41 million. Emerging products such as sunflower seed cake and chilies have opened fresh corridors into China, and avocado shipments are gaining momentum following government-financed pack-houses[2]Source: MARKUP, “EAC Agri-Food Exports to the EU,” eacmarkup.org. EAC trade value grew 13.3% in 2024 to 1.825 trillion Tanzanian shillings as regional food shortages lifted import demand.

Rapid Uptake of Mobile-Enabled Extension and Fintech

Platforms like eKichabi v2 deliver agronomic tips and price data via both USSD and Android, reaching households lacking smartphones. Complementary fintech offerings from Laina Finance and Mipango Finance target women farmers, easing the gender credit gap. The Tanzania Mercantile Exchange’s zero-data-cost portal allows smallholders to sell crops without middlemen. AI-driven services from Kilimo Fresh report 27% yield gains and 35% pesticide cuts, echoing early digital dividends.

EU Phytosanitary Alignment Opening Premium Export Channels

The EU lifted its ban on Tanzanian bitter gourd after authorities demonstrated compliance with traceability and pesticide limits. Ninety-two EU firms already invest in Tanzanian floriculture, horticulture, and beverage crops, giving local exporters ready distribution. The MARKUP initiative links small and medium enterprises to EU buyers, and agri-food shipments from the EAC into Europe grew 7.7% in 2021, with coffee, tea, and spices up 35.5%. Firms such as Viridium TZ upgraded into cardamom processing after securing EU certifications and now sell at premium differentials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Poor rural roads and cold-chain coverage | -0.9% | Rural areas nationwide, particularly remote farming regions | Long term (≥ 4 years) |

| Volatile rainfall and El Niño frequency spikes | -0.7% | Rain-dependent regions, concentrated in central and northern Tanzania | Short term (≤ 2 years) |

| Land tenure uncertainty amid the BBT block-farm program | -0.5% | Areas designated for block farming, primarily in the Southern and Eastern regions | Medium term (2-4 years) |

| Sub-scale local processing capacity for perishables | -0.6% | Processing hubs and areas with high perishable production | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Poor Rural Road and Cold-Chain Coverage

Tanzania’s rural road density trails regional peers, leaving many villages reachable only during dry seasons. Perishable crops suffer 30–40% post-harvest losses, yet the country operates fewer than 50 cold stores compared with Kenya’s 7,000. The World Bank places the investment gap above USD 3 billion. Local grants, co-funded by the EU and Sweden, finance small bridges and pack sheds, but scale remains inadequate for horticulture’s growth trajectory.

Volatile Rainfall and El Niño Frequency Spikes

Roughly 75% of the output depends on rainfall. The 2024–2025 wet-season forecast forced authorities to draft drought mitigation and early-warning protocols. Projections suggest maize yields may drop 8–13% by 2050 if adaptation stalls, shaving 4% from GDP and pushing 2.6 million Tanzanians below the poverty line. GCF irrigation schemes and drought-resistant seed programs aim to cushion these shocks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Commodity Type: Cereals Lead While Fruits Drive Innovation

Cereals and grains accounted for 33.62% of the Tanzanian agriculture market share in 2025, confirming their centrality to staple diets and national reserves. Maize output hit 5.9 million metric tons in 2023 courtesy of seed subsidies, yet average fertilizer use trails regional benchmarks at 9 kg/ha. Rice yields have improved through International Rice Research Institute partnerships that distribute high-yield varieties across Southern Highlands paddies. Wheat cultivation, though modest, is inching upward in cooler highlands, while sorghum and millet maintain relevance in drought-prone central belts. Simultaneously, pulses and oilseeds gain policy favor because domestic sunflower oil meets only 30–45% of edible oil demand.

Fruits and vegetables recorded a 11.35% CAGR outlook to 2031, the fastest among all groupings. Government support for avocado pack-houses, chili processing lines, and mobile disease-diagnosis apps is accelerating the segment’s modernization. Banana orchards battle Fusarium Wilt and Black Sigatoka, prompting trials of convolutional neural network apps that diagnose infections at 90% accuracy.

Geography Analysis

Regional contrasts shape the Tanzanian agriculture market across its diverse agroecologies. The Southern Highlands around Mbeya and Iringa supply almost 40% of maize and host expanding wheat farms. Cooler elevations and comparatively better trunk roads attract combine-harvester contractors and warehouse investors. Despite that advantage, land degradation affects 19 million people and continues to erode topsoil, compelling renewed focus on conservation tillage and contour farming.

The Coastal zone, comprising Mtwara, Lindi, and Ruvuma, produces more than 90% of the national cashews. Here, the BBT block-farm model is poised to reorganize production into export-oriented estates. Cold-store deficits still hamper high-quality kernel output, but investments under the Egyptian Industrial City promise refrigerated logistics and shell-waste bioenergy plants. Zanzibar’s spice-dominated system generated a 13.3% trade-value lift in 2024 to 1.825 trillion shillings, underscoring island-economy specialization.

Central semi-arid regions such as Dodoma and Singida present the country’s largest climate-resilience laboratory. The Simiyu Climate Resilient Project channels USD 196.1 million into piped water and drip kits, directly benefiting 3 million residents. Solar-powered pumps now irrigate cucumbers and okra in Mpwapwa, illustrating the viability of smallholder horticulture under erratic rainfall.

Recent Industry Developments

- June 2025: Tanzania’s shilling appreciated on record gold prices and dollar inflows from agriculture, tourism, and transport, elevating import purchasing power.

- May 2025: IIT Madras and GRID-India signed an MoU to bolster Tanzania’s grid capacity and renewable integration, supporting energy-intensive irrigation VIF.

- November 2024: Tanzania attained 128% food self-sufficiency and became a net cashew-kernel exporter African Development Bank Group.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines Tanzania's agriculture market as the cumulative economic value generated within the country from the cultivation of food crops and cereals, pulses and oilseeds, fruits and vegetables, and cash crops, measured at the farm gate in constant 2024 dollars.

Scope Exclusion: Live animal production and fisheries are out of scope to keep the model consistent with crop-centric GDP reporting.

Segmentation Overview

- By Commodity Type

- Cereals and Grains

- Production Analysis

- Consumption Analysis

- Export Analysis

- Import Analysis

- Price Trend Analysis

- Pulses and Oilseed

- Production Analysis

- Consumption Analysis

- Export Analysis

- Import Analysis

- Price Trend Analysis

- Fruits and Vegetables

- Production Analysis

- Consumption Analysis

- Export Analysis

- Import Analysis

- Price Trend Analysis

- Cash Crop

- Production Analysis

- Consumption Analysis

- Export Analysis

- Import Analysis

- Price Trend Analysis

- Cereals and Grains

Detailed Research Methodology and Data Validation

Primary Research

We subsequently conduct semi-structured interviews and pulse surveys with input dealers, district agronomists, warehouse operators, and produce traders across key producing zones, Northern Highlands, Southern Corridor, and the Lake region. Their insights on seed uptake, post-harvest losses, informal trade volumes, and average selling prices sharpen assumptions flagged during desk work and help triangulate any discrepancies before model lock-in.

Desk Research

Our analysts first assemble a structured library of open data, trade flows from FAOSTAT, harvested area and yield series from the National Bureau of Statistics, input price trackers from the Tanzania Fertilizer Regulatory Authority, export earnings disclosed by the Bank of Tanzania, and regional climate bulletins issued by FEWS NET. Company filings, budget speeches, and reputable press articles then add on-ground context, while subscription databases such as D&B Hoovers and Dow Jones Factiva provide firm-level revenue signals.

These sources reveal production baselines, consumption elasticities, and farm gate pricing trends that anchor the initial top-down market view. The list above is illustrative rather than exhaustive; numerous additional publications, customs records, and association white papers were referenced to validate figures and clarify definitions.

Market-Sizing & Forecasting

The model begins with a top-down reconstruction of agricultural gross output using historical crop production volumes, average farm gate prices, and projected shifts in cropped area. Results are stress tested through selective bottom-up checks, sampled milling capacity roll-ups and regional channel checks on maize and rice volumes, to close evident gaps.

Key variables include irrigated area expansion, fertilizer application intensity, rural population growth, producer price inflation, farm credit disbursement, and climate-adjusted yield trends. A multivariate regression, coupled with three-scenario ARIMA projections for each driver, produces the 2025-2030 value outlook. Gap areas in bottom-up evidence, such as unrecorded cross-border sales, are bridged by applying conservative discount factors vetted with supply chain stakeholders.

Data Validation & Update Cycle

Before release, every dataset passes anomaly scans, variance diagnostics against prior editions, and a peer review. Reports refresh annually; material shocks, for example, fertilizer subsidy surges, trigger interim revisions, and a final analyst pass ensures clients receive the latest calibrated view.

Why Mordor's Tanzania Agriculture Baseline Commands Reliability

Published estimates often diverge because firms mix livestock with crops, apply dissimilar farm gate pricing, or use outdated exchange rates.

Key gap drivers here stem from scope breadth, differing base years, and how each publisher escalates farm gate prices into market value. Some models push aggressive mechanization uptake, whereas Mordor retains empirically observed adoption curves, and that restraint keeps our 2025 baseline aligned with verifiable field evidence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 22.90 B (2025) | Mordor Intelligence | |

| USD 16.03 B (2024) | Regional Consultancy A | Includes livestock and aquaculture; uses nominal 2024 shilling-denominated GDP without inflation adjustment. |

| USD 17.44 B (2023) | Industry Association B | Excludes fruits and vegetables; extrapolates a single-year export receipt spike to whole market. |

Methodology gaps are identified relative to Mordor's clearly bounded, crop-only scope and dual validation approach.

In summary, estimates vary when definitions or price escalators shift, yet Mordor's disciplined variable set, dual validation, and yearly refresh deliver a balanced baseline that decision makers can replicate and trust.

Key Questions Answered in the Report

What is the current value of the Tanzanian agriculture market?

The Tanzanian agriculture market is valued at USD 24.12 billion in 2026 and is projected to reach USD 31.26 billion by 2031.

Which commodity segment holds the largest share?

Cereals and grains lead with 33.62% of Tanzanian agriculture market share in 2025, anchored by maize output of 5.9 million metric tons.

Which segment is growing fastest?

Fruits and vegetables post the highest growth, forecast to expand at a 11.35% CAGR to 2031 due to export demand and dietary shifts.

How extensive is smallholder participation?

Smallholders cultivate 80–90% of Tanzania’s farmland, highlighting both fragmentation and the importance of aggregation solutions.

What major risk threatens near-term growth?

Inadequate rural roads and cold-chain facilities drive 30–40% post-harvest losses for perishables, trimming sectoral margins.

How is digital technology transforming the sector?

Mobile-enabled platforms such as eKichabi v2 and the Tanzania Mercantile Exchange improve market information, credit access and price transparency for thousands of growers.

Page last updated on: