Agriculture In Uganda Market Analysis by Mordor Intelligence

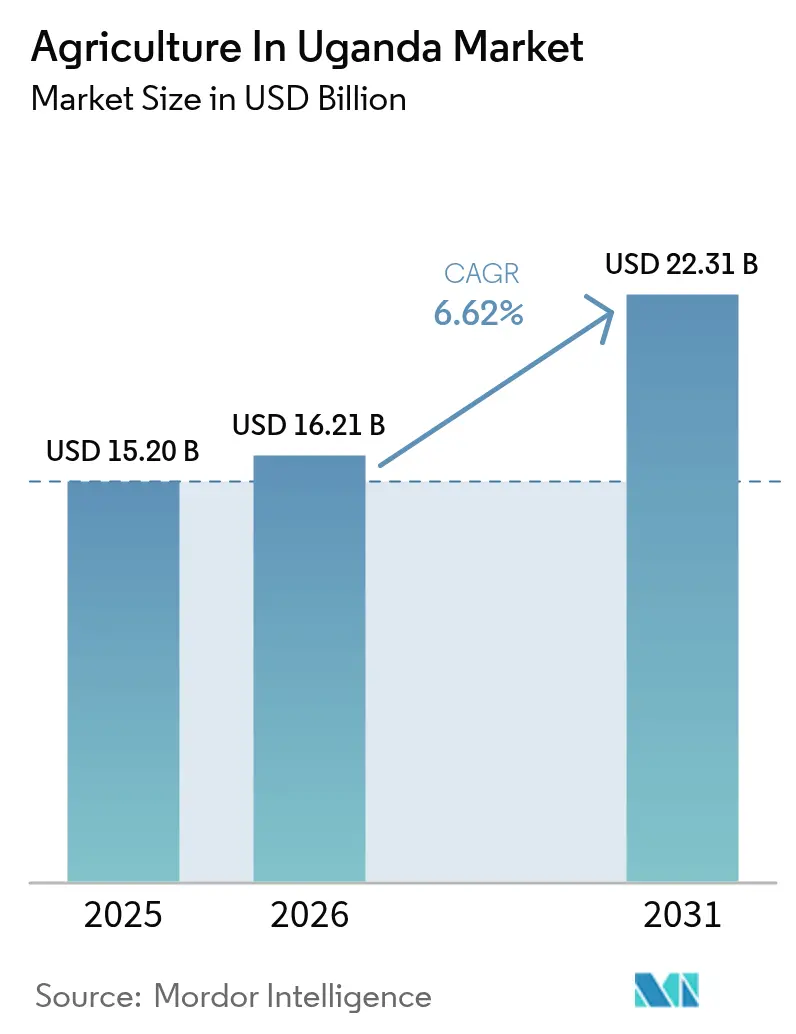

Agriculture in Uganda market size in 2026 is estimated at USD 16.21 billion, growing from 2025 value of USD 15.20 billion with 2031 projections showing USD 22.31 billion, growing at 6.62% CAGR over 2026-2031. Government funding, infrastructure upgrades, and digital agriculture programs are reshaping farming practices, expanding access to inputs, and catalyzing commercialization across all major crop groups. Public-private financing partnerships, including the one in 2022, a World Bank’s USD 96 million climate-smart agriculture project, and Stanbic Bank’s commitment of UGX 750 billion (USD 203 million), provide the capital base required to modernize production and post-harvest systems [1].Source: Ministry of Finance Planning and Economic Development, “Finance Minister Kasaija Delivers Budget Strategy for FY 2025/2026,” finance.go.ug Rising regional demand for cereals, tariff-free access for horticulture, and fast-growing livestock feed requirements reinforce positive price signals, while widespread digital adoption lowers transaction costs and improves market transparency. Together, these elements sustain a strong growth runway for the agriculture market in Uganda through 2030.

Key Report Takeaways

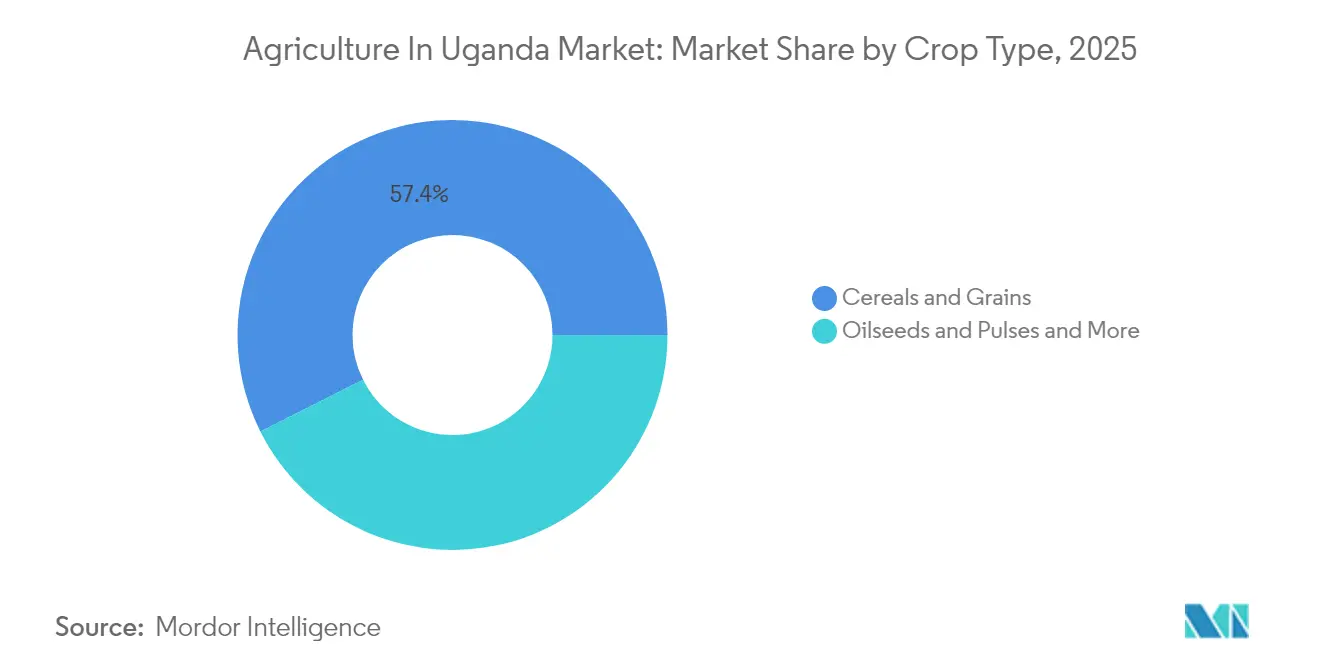

- By crop type, cereals and grains led with a 57.40% share in the Uganda market in 2025, while fruits and vegetables are forecast to expand at a robust 8.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Agriculture In Uganda Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government PDM funding accelerates smallholder commercialization | +1.8% | National, central and eastern regions | Medium term (2-4 years) |

| Cold-chain build-out at Entebbe and regional hubs | +1.2% | National, spillover to East Africa | Medium term (2-4 years) |

| Mobile price/logistics apps expand market access | +0.9% | National, highest adoption in central regions | Short term (≤ 2 years) |

| Anti-tick and livestock health programs spur oilseed demand | +0.7% | National, cattle corridor regions | Medium term (2-4 years) |

| Digital grain-trade platforms (EAGC GSoko) cut transaction costs | +0.6% | National, commercial farming areas | Short term (≤ 2 years) |

| Tariff-free access for Hass avocado and exotic fruits | +0.5% | National, southwestern highlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government PDM Funding Accelerates Smallholder Commercialization

The Parish Development Model represents Uganda's most ambitious rural transformation initiative, deploying over UGX 2 trillion (USD 540 million) to shift 6.78 million livestock-keeping households from subsistence to commercial agriculture [2]Source: Uganda Bureau of Statistics, “National Livestock Census 2021,” ubos.org . This funding mechanism directly addresses the historical constraint of limited access to inputs and extension services, with 56.5% of livestock-keeping households now accessing extension services compared to previous coverage gaps. The program's impact extends beyond direct beneficiaries, as increased market participation by smallholders creates upstream demand for processing facilities and downstream supply for urban markets, fundamentally altering value chain dynamics across cereals, oilseeds, and horticultural crops.

Cold-Chain Build-Out at Entebbe and Regional Hubs

Infrastructure investments in cold storage and logistics are unlocking Uganda's export potential, particularly for high-value horticultural products that previously faced post-harvest losses exceeding 40%. The Entebbe Airport expansion, nearing completion in 2024, includes enhanced cargo handling facilities specifically designed for fresh produce exports, positioning Uganda to capture growing European and Middle Eastern demand for tropical fruits. Private sector investments complement government infrastructure, with companies like Alvan Blanch installing multiple 1,000 metric tons grain storage facilities across Busunju, Masindi, and Kampala, equipped with advanced drying and cleaning systems that maintain quality standards required for export markets.

Mobile Price/Logistics Apps Expand Market Access

In 2023, digital transformation in agriculture accelerates through targeted funding programs, with the AYuTe Africa Challenge distributing UGX 112 million (USD 30,000) in grants to Ugandan agritech startups developing mobile-based solutions for price discovery and logistics coordination [3].Source: Uganda Coffee Development Authority, “In the News,” ugandacoffee.go.ug These platforms address information asymmetries that historically disadvantaged smallholder farmers, enabling direct market access and reducing intermediary costs by an estimated 15-20%. The AIRTEA program, supported by EUR 298,000 (USD 322,000) in EU funding, demonstrates the international recognition of Uganda's digital agriculture potential, focusing on IoT and precision farming technologies that optimize resource use and improve yield predictability across diverse agro-ecological zones.

Anti-Tick and Livestock Health Programs Spur Oilseed Demand

Rising cattle, pig, and dairy herds need high-protein feed from soybean and sunflower meal, with animal health campaigns boosting productivity and increasing feed uptake, reinforcing growth in the market. Government-led animal health programs, including mass anti-tick and foot-and-mouth disease vaccination campaigns, improve livestock productivity and create sustained demand for high-protein feed supplements derived from soybean and sunflower processing. The sector's commercial orientation increases, with pig farming showing 50% commercial participation rates, while milk production surged fivefold to 3.73 billion liters annually, necessitating consistent feed supply chains that favor locally-produced oilseed cake over imported alternatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rainfall variability and drought-linked yield swings | -1.4% | Northern and eastern regions | Short term (≤ 2 years) |

| Less Than 1 % irrigated area limits scale-up | -1.1% | National, commercial farming areas | Long term (≥ 4 years) |

| Aflatoxin rejections in maize and groundnuts | -0.8% | Humid regions | Medium term (2-4 years) |

| High cost / low availability of hermetic storage | -0.6% | Remote farming areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rainfall Variability and Drought-Linked Yield Swings

Climate volatility poses the most immediate threat to agricultural productivity, with the March-May 2024 season recording one of the driest periods since 1981 in northern Uganda, causing widespread crop failures and livestock losses. The Katakwi District drought from November 2024 to March 2025 resulted in over 1,000 livestock deaths, highlighting the sector's vulnerability to weather extremes that can swing cereal output by more than 20% year-over-year. This variability undermines investment confidence and complicates supply chain planning, as processors and exporters struggle to maintain consistent volumes and quality standards required for international markets.

Less Than 1% Irrigated Area Limits Scale-Up

Uganda's irrigation coverage remains critically low at less than 1% of cultivated area, constraining the sector's ability to achieve consistent high-value crop production required for export market penetration. This infrastructure deficit becomes more pronounced as climate change intensifies rainfall variability, forcing farmers to rely on rain-fed production that limits crop selection and harvest timing flexibility. In 2022, the World Bank's USD 96 million Uganda Climate Smart Agriculture Transformation Project addresses this constraint through planned desilting of 300 dams and creation of water management infrastructure, but implementation timelines extend beyond the immediate forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Crop Type: Cereals Drive Volume, Fruits Capture Value

Cereals and grains contributed 57.40% of the market share in 2025, led by maize crops serving domestic and regional buyers in South Sudan, the Democratic Republic of Congo, and Kenya. Sorghum and millet acreage expands in northern districts as climate-resilient options, while wheat remains a niche. Input vouchers and extension agents under the Parish Development Model lower production costs, yet post-harvest losses weigh on farm margins, underscoring the need for quality storage.

Fruits and vegetables forecast to register 8.92% CAGR through 2031, benefiting from improved cold-chain logistics at Entebbe Airport. Banana and plantain production serve domestic consumption, while Hass avocados, pineapples, and specialty Arabica coffee command premium export prices. Contract farming, aggregation centers, and digital trading platforms continue to reinforce growth across all crop groups, sustaining momentum for the market.

Geography Analysis

The central region’s proximity to Kampala creates a dense cluster of commercial farms, feed mills, and processing plants that capture economies of scale and distribute output throughout the agriculture market channels in Uganda. Western Uganda, notably the Ankole sub-region, produced 1.2 billion liters of milk in 2024 and hosts large coffee estates such as Kaweri Coffee Plantation, underlining its role in value-added exports. Eastern districts dominate cereal acreage and face heightened climate risk, having endured the driest March-May season in four decades in 2024.

Northern Uganda, including Karamoja, receives intensive public and donor support. UNDP’s Green Belts initiative shows how women-led cooperatives scaled from six-acre plots to 400-acre operations cultivating sorghum, green gram, and sunflower, demonstrating the inclusiveness of the market. Cross-border trade continues to buoy grain income as Uganda exports maize and beans to Kenya and the Democratic Republic of Congo, though political disruptions occasionally interrupt flows. The southwestern highlands’ altitude favors specialty coffee and Hass avocado production, positioning the region to capitalize on EU tariff exemptions and premium pricing.

The agriculture in Uganda market also gains from expanded trade with China, India, and other non-traditional partners, cushioning the loss of some AGOA preferences in the United States. While logistics corridors are improving, remote district roads remain vulnerable during rainy seasons, keeping transport costs high. Implementation of regional infrastructure, such as the Standard Gauge Railway extension, is projected to further reduce freight costs and reinforce Uganda’s role as an agricultural supplier to East and Central Africa.

Recent Industry Developments

- May 2023: Lusha Coffee obtained an export license from Uganda Coffee Development Authority to export specialty Arabica beans from Bududa to Canada and Europe, marking the expansion of direct-to-consumer premium coffee trade, bypassing traditional commodity channels.

- October 2022: The Government of Uganda, through the Ministry of Agriculture, Animal Industries, and Fisheries (MAAIF), together with development partners, released biological control agents for the Mango mealybug (Rastococcus invaders).

Agriculture In Uganda Market Report Scope

The study identifies the agriculture scenario of Uganda and estimates the growth of the crop production and agricultural sector in the country as a whole.

The Ugandan agriculture market includes production analysis (volume), consumption analysis (value and volume), export analysis (value and volume), import analysis (value and volume), and price trend analysis. The market is segmented by type into cereals and grains, oilseeds and pulses, and fruits and vegetables. The report offers market sizing and forecasts in value (USD thousand) and volume (metric tons).

By Crop Type (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis)

| Cereals and Grains |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| By Crop Type (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis) | Cereals and Grains |

| Oilseeds and Pulses | |

| Fruits and Vegetables |

Key Questions Answered in the Report

What is the anticipated value of Uganda agriculture sector by 2031?

Forecasts point to USD 22.31 billion in 2031, up from USD 15.20 billion in 2025.

How fast is the fruits and vegetables segment growing?

It is projected to post a 8.92% CAGR through 2031, the fastest among all crop groups.

Which crop group currently holds the largest share?

Cereals and grains lead with 57.40% share as of 2025.

What climate risk poses the biggest threat to production?

Rainfall variability and drought can swing cereal output by more than 20% year-over-year.

Page last updated on: