South Africa Alfalfa Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

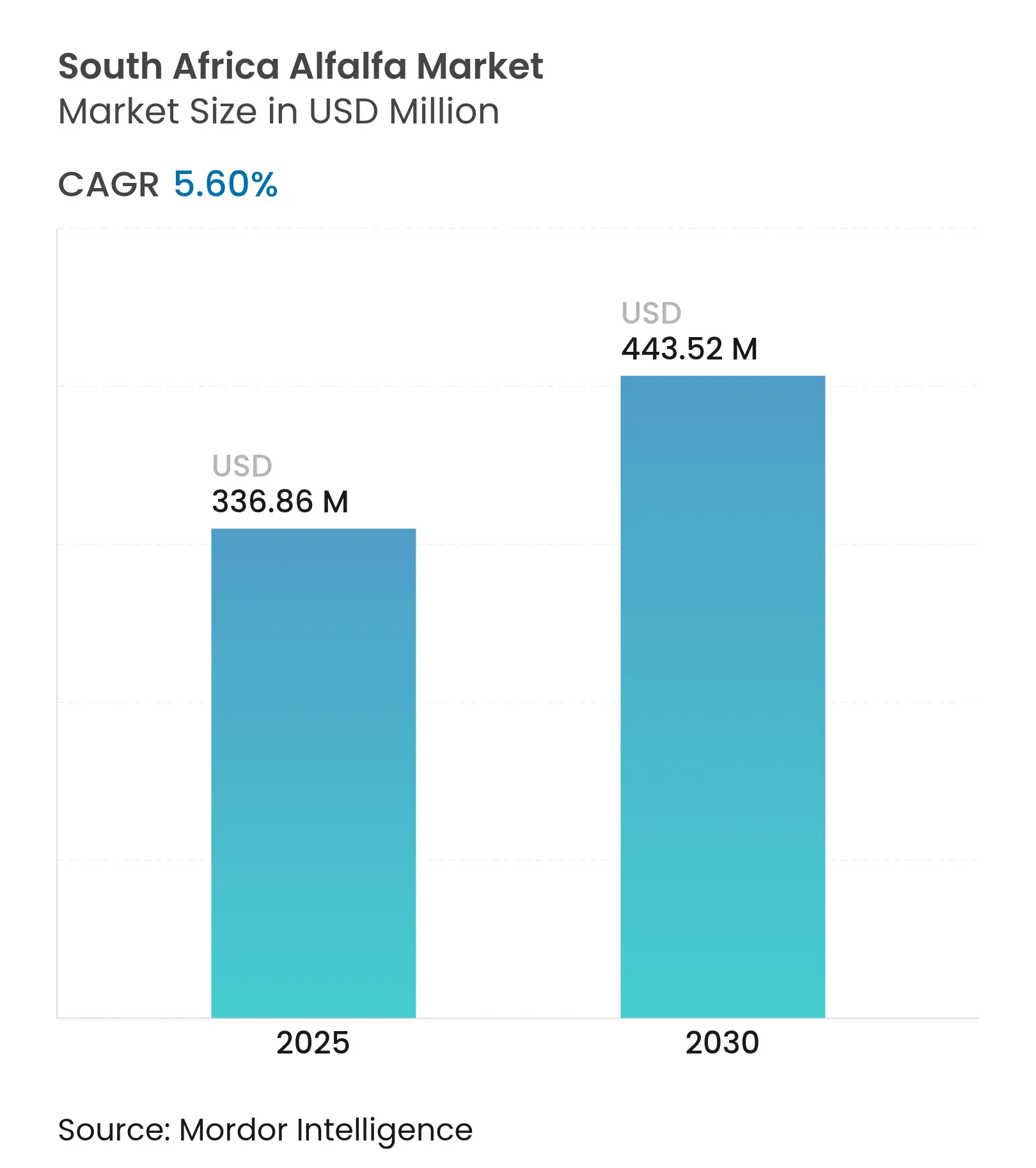

| Market Size (2025) | USD 336.86 Million |

| Market Size (2030) | USD 443.52 Million |

| Growth Rate (2025 - 2030) | 5.60 % CAGR |

South Africa Alfalfa Market Analysis by Mordor Intelligence

The South Africa alfalfa market size is valued at USD 336.86 million in 2025 and is projected to reach USD 443.52 million by 2030, advancing at a 5.6% CAGR during the forecast period. Growth momentum reflects persistent demand from dairy intensification, export incentives linked to Gulf feed deficits, and a gradual roll-out of precision irrigation that lowers unit-costs in semi-arid zones. Structural drivers include protein-dense rations for ruminant herds, freight arbitrage created by shorter sailing distances to the United Arab Emirates and Saudi Arabia, and government grants that close the capital gap for smallholder irrigation. Counter-pressures arise from rail bottlenecks that raise port-handling charges, volatile El Niño-linked droughts, and double-digit electricity tariff hikes that squeeze pumping margins. Competitive intensity remains moderate as cooperatives, hay processors, and vertically integrated livestock companies race to secure irrigation finance, export certifications, and technology upgrades, all of which reshape acreage allocation across key provinces.

Key Report Takeaways

- By production province, Free State and Western Cape jointly controlled 60% of the cultivated area and generated the largest 2024 revenue pool in the South Africa alfalfa market.

South Africa Alfalfa Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising domestic dairy herd expansion Rising domestic dairy herd expansion | +1.2% | Western Cape, Free State, Eastern Cape | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:Western Cape, Free State, Eastern Cape | Impact Timeline:Medium term (2-4 years) |

Surge in on-farm water-efficient irrigation adoption Surge in on-farm water-efficient irrigation adoption | +0.9% | Western Cape, Northern Cape, Free State | Long term (≥ 4 years) | |||

Government fodder-crop incentive grants Government fodder-crop incentive grants | +0.7% | National, with early gains in Free State, Limpopo, North West | Short term (≤ 2 years) | |||

Growing demand from race-horse and equine sector Growing demand from race-horse and equine sector | +0.5% | Western Cape (Cape Town, Stellenbosch), Gauteng (Johannesburg) | Medium term (2-4 years) | |||

Feed cost-hedging by integrated protein producers Feed cost-hedging by integrated protein producers | +1.0% | Mpumalanga, Western Cape, KwaZulu-Natal | Medium term (2-4 years) | |||

Export parity pricing gaps with Gulf states Export parity pricing gaps with Gulf states | +1.3% | National, with export hubs in Western Cape, Northern Cape | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Domestic Dairy Herd Expansion

Milk output is set to rise in 2025 as softer maize prices follow the 2024 harvest rebound [1]Source: United States Department of Agriculture Foreign Agricultural Service, “Livestock and Products Annual,” USDA, apps.fas.usda.gov. Ruminant and dairy units already consume an increased share of national feed volumes, and management teams are introducing higher-protein rations that replace grass hay with alfalfa, delivering 18–22% crude protein. Eastern Cape’s September 2024 framework earmarked a huge amount for irrigation lines on 100 dairy-ready farms, ensuring incremental alfalfa demand. Provincial feed manufacturers project steady throughput growth that supports long-run acreage expansion in the Free State and Western Cape.

Surge in On-Farm Water-Efficient Irrigation Adoption

Severe drought from October 2023 to March 2024 intensified the shift from flood to drip and micro-sprinkler systems, which curb water use by as much as 40%. Western Cape growers expanded shade netting and tunnels between 2018 and 2023 despite high capital costs per hectare [2]Source: GreenCape, “Sustainable Agriculture Market Intelligence Report 2025,” greencape.co.za. A five-year agreement with Case IH, signed in September 2024, is field-testing variable-rate irrigation on seven research farms and will publish blueprints for commercial roll-out by 2027. Water-smart protocols lengthen stand life, cut electricity bills, and sharpen the export cost curve for the South Africa alfalfa market.

Government Fodder-Crop Incentive Grants

The Comprehensive Agricultural Support Programme, Blended Finance Scheme, and Ilima/Letsema grants supply subsidized seed and irrigation kits that lower entry barriers for emerging growers. Eastern Cape’s Land Development Grants target 38 land-claim farms, while the Agricultural Research Council plans several field trials to release drought-tolerant cultivars within the next year. Subsidies are most influential in Free State, Limpopo, and North West, where land costs are significantly high per hectare.

Growing Demand from Race-Horse and Equine Sector

South Africa’s thoroughbred industry, concentrated around Cape Town and Johannesburg, demands leaf-grade alfalfa exceeding 20% protein and nearly dust-free texture. Although smaller volumes of the total offtake, price premiums over dairy-grade hay lift processor margins, and stabilize revenues during economic downturns. Producers seek halal certificates and phytosanitary clearances to capture equestrian demand in the United Arab Emirates and Saudi Arabia, leveraging the Department of Agriculture’s alfalfa hay database to simplify export paperwork. This premium niche is anticipated to widen as Middle Eastern buyers diversify away from United States-sourced forage.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Recurring drought cycles in Northern provinces Recurring drought cycles in Northern provinces | -1.1% | Limpopo, North West, Free State, Northern Cape | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.1% | Geographic Relevance:Limpopo, North West, Free State, Northern Cape | Impact Timeline:Short term (≤ 2 years) |

Escalating electricity tariffs for irrigation pumps Escalating electricity tariffs for irrigation pumps | -0.8% | National, acute in Western Cape, Free State | Medium term (2-4 years) | |||

Limited rail logistics for bulk hay movement Limited rail logistics for bulk hay movement | -0.6% | National, export routes from Western Cape, Northern Cape | Long term (≥ 4 years) | |||

Expenses Incurred by Developers of Protected Plant Varieties Expenses Incurred by Developers of Protected Plant Varieties | -0.4% | National | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Recurring Drought Cycles in Northern Provinces

The 2023/24 El Niño was the most severe in four decades, pushing river flows to 20% of normal and causing stand establishment failures across Limpopo and North West [3]Source: Southern African Development Community, “Regional Drought Bulletin,” sadc.int. Maize output projections fell in April 2024, exposing feed deficits and dampening new alfalfa plantings. While alfalfa’s taproot offers drought tolerance, first-season moisture is critical, making rain-fed expansion risky without irrigation investment. Yield swings from 12 metric tons per hectare in favorable seasons to as low as 3 metric tons in drought years, stall bank lending, and curb acreage growth across the northern belt.

Escalating Electricity Tariffs for Irrigation Pumps

Eskom lifted power tariffs in 2023/24 and in 2024/25, and frequent load-shedding forces growers to resort to diesel or solar backups. Alfalfa’s seasonal water demand of 800–1,200 millimeters now costs significantly per hectare in electricity, equal to one-fifth of operating expenses. Solar-powered pivots cost high for a 100-kilowatt system with a four-year payback, yet collateral constraints block adoption for many smallholders.

Geography Analysis

Free State and Western Cape anchor national production and together command roughly 60% of cultivated acreage, translating into the largest provincial slice of the South Africa alfalfa market size. Free State leverages extensive pivot and drip systems that support profitable maize–alfalfa rotations, while average significant land prices keep large operations cost-competitive. Western Cape benefits from short haulage to Cape Town port and logged a big jump in shade-net and tunnel acreage between 2018 and 2023, signaling strong grower appetite for water-efficient technology.

Northern Cape and Mpumalanga supply a further large acreage and serve distinct demand nodes. Northern Cape attracts drought-tolerant plantings owing to the land, though limited water rights cap upside. Mpumalanga holds a significant share of national maize output and of feed sales, so integrated poultry groups are adding alfalfa fields to hedge protein costs. The Eastern Cape is the fastest mover in Land Development Grants for irrigation on 38 land-claim farms, a step that could lift its share of national acreage by 2028.

Limpopo, North West, KwaZulu-Natal, and Gauteng together account for a smaller share of the South Africa alfalfa market share and face divergent challenges. Limpopo and North West suffered the worst drought in forty years during the 2023–2024 season, with river flows at just 20% of normal and maize yields projected lower, forcing many growers to defer alfalfa plantings. KwaZulu-Natal’s higher rainfall favors grass pastures over alfalfa, limiting uptake despite strong dairy demand. Gauteng remains a minor contributor because urban expansion restricts farmland. Without major investments in water storage and distribution, these northern provinces are likely to lose a small fraction of acreage to better-resourced southern regions during the forecast period.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

South Africa Alfalfa Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Western Cape Department of Agriculture and Case IH began a five-year precision farming project covering seven research farms. By harnessing advanced technologies like Global Positioning System (GPS) and Artificial Intelligence (AI), this initiative seeks to boost crop yields and minimize waste through informed, data-driven decisions, marking a pivotal move towards modernizing the province's agricultural landscape.

- October 2024: Eastern Cape launched an Agriculture Investment Framework with ZAR 220 million (USD 11.5 million) in grants. Nonkqubela Pieters, the Member of the Executive Council (MEC) for Eastern Cape's Rural Development and Agrarian Reform (DRDAR), announced grants for 38 land-claim farms under the new framework.

- March 2023: Joint Research Centre (JRC) reported river flows at 20% of normal during the 2023/24 drought. A JRC report highlighted this statistic, emphasizing the repercussions of the unusually dry and warm winter and sounding the alarm for a challenging summer for water resources.

Table of Contents for South Africa Alfalfa Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising domestic dairy herd expansion

- 4.2.2Surge in on-farm water-efficient irrigation adoption

- 4.2.3Government fodder-crop incentive grants

- 4.2.4Growing demand from race-horse and equine sector

- 4.2.5Feed cost-hedging by integrated protein producers

- 4.2.6Export parity pricing gaps with Gulf states

- 4.3Market Restraints

- 4.3.1Recurring drought cycles in Northern provinces

- 4.3.2Escalating electricity tariffs for irrigation pumps

- 4.3.3Limited rail logistics for bulk hay movement

- 4.3.4Expenses Incurred by Developers of Protected Plant Varieties

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Value/Supply-Chain Analysis

- 4.7PESTEL Analysis

5. Market Size and Growth Forecasts (Value and Volume)

- 5.1By Country

- 5.1.1Production Analysis (Volume)

- 5.1.2Consumption Analysis (Volume and Value)

- 5.1.3Import Analysis (Volume and Value)

- 5.1.4Export Analysis (Volume and Value)

- 5.1.5Price Trend Analysis

6. Competitive Landscape

- 6.1List of Stakeholders

- 6.1.1GWK

- 6.1.2Suidwes Holdings

- 6.1.3Overberg Agri Bedrywe Pty Ltd.

- 6.1.4 Klein Karoo Seed Marketing (Pty) Ltd

- 6.1.5Senwes Limited

- 6.1.6De Heus (Pty) Ltd

- 6.1.7Nutri Feeds

- 6.1.8Karoo Valley Lucerne (Pty) Ltd

- 6.1.9RSA Seed and Grain

7. Market Opportunities and Future Outlook