Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

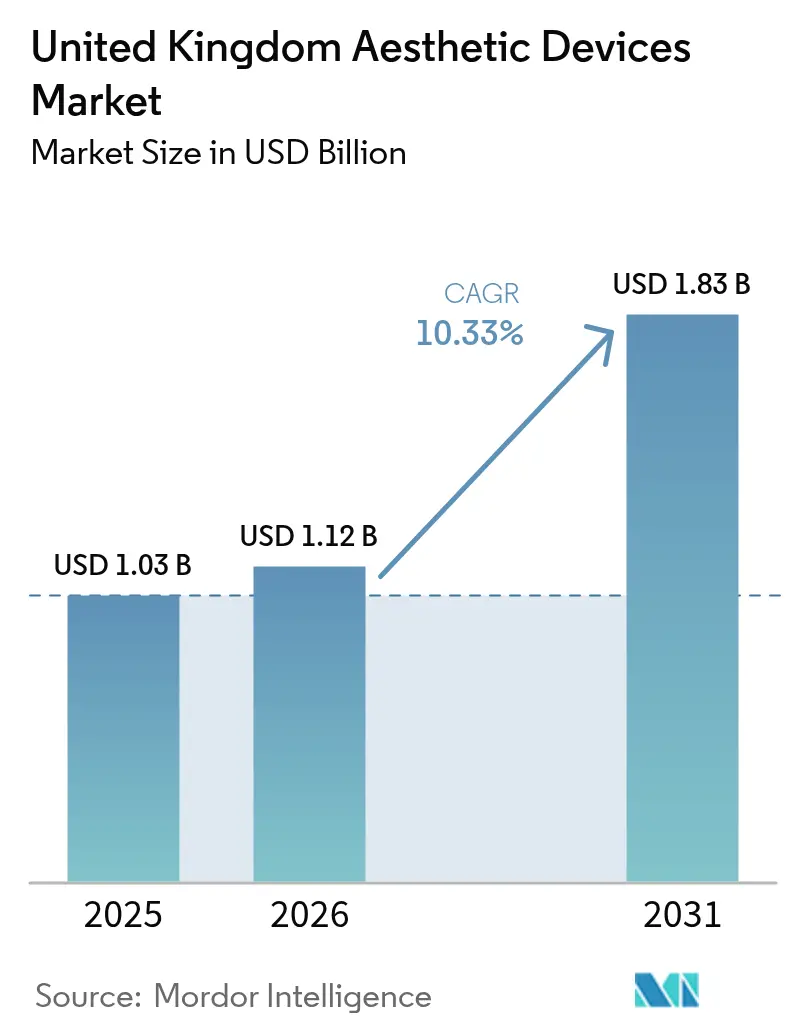

| Base Year Market Size (2025) | USD 1.03 Billion |

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 1.83 Billion |

| Growth Rate (2026 - 2031) | 10.33% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Aesthetic Devices Market Analysis by Mordor Intelligence

The United Kingdom Aesthetic Devices Market size is projected to expand from USD 1.03 billion in 2025 and USD 1.12 billion in 2026 to USD 1.83 billion by 2031, registering a CAGR of 10.33% between 2026 to 2031.

A sustained pivot toward minimally- and non-invasive procedures, rapid upgrades that bundle laser, radiofrequency and ultrasound modalities into a single console, and the emergence of at-home LED and microcurrent tools keep the United Kingdom aesthetic devices market on a double-digit growth path. Regulatory clarity—through Medicines and Healthcare products Regulatory Agency (MHRA) approvals and impending non-surgical licensing rules—has reduced gray-market imports, giving fully compliant manufacturers clearer access to clinics and medical spas. Private operators also benefit from the National Health Service (NHS) Provider Selection Regime, which outsources selected laser treatments and supplies a predictable patient pipeline during traditionally slow summer quarters. Meanwhile, rising wait lists for gender-affirming care and medical-tourism complications have heightened consumer awareness around MHRA-registered devices, encouraging domestic spend.

Key Report Takeaways

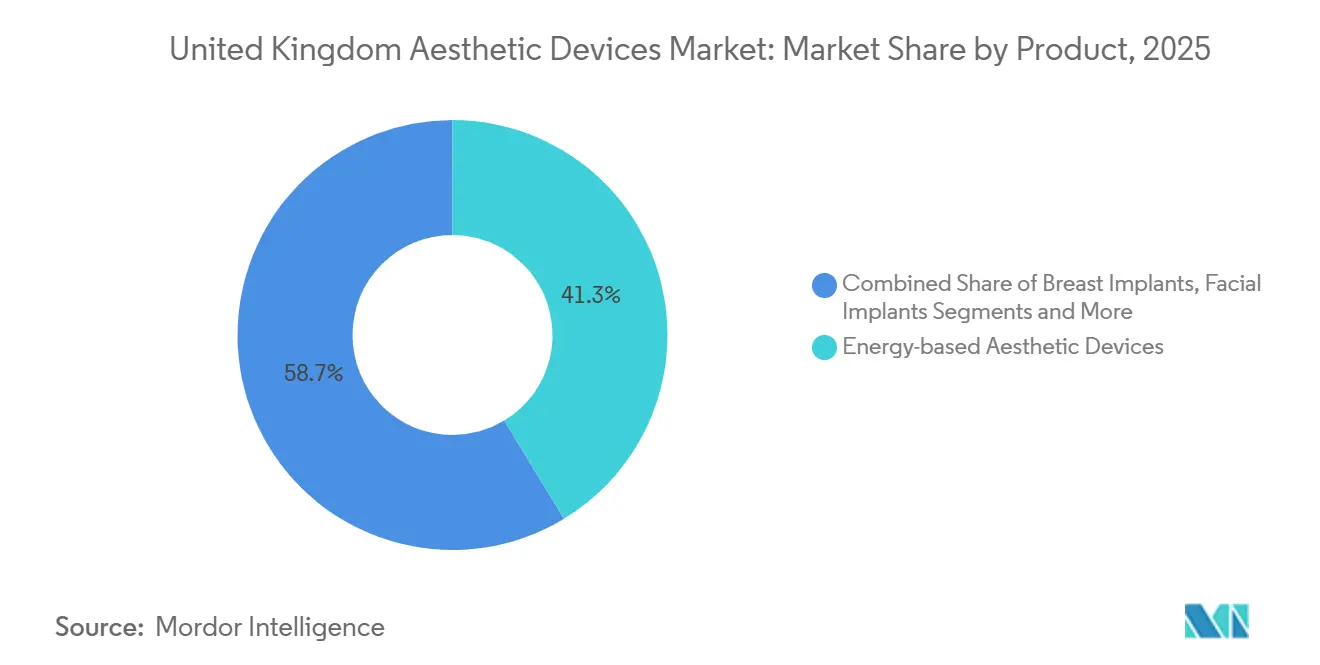

- By product, energy-based platforms led with 41.32% revenue in 2025, while thread-lift devices are projected to expand at a 12.52% CAGR through 2031.

- By application, facial contouring and skin rejuvenation commanded 36.64% of 2025 sales; tattoo and scar removal is forecast to post a 13.24% CAGR to 2031.

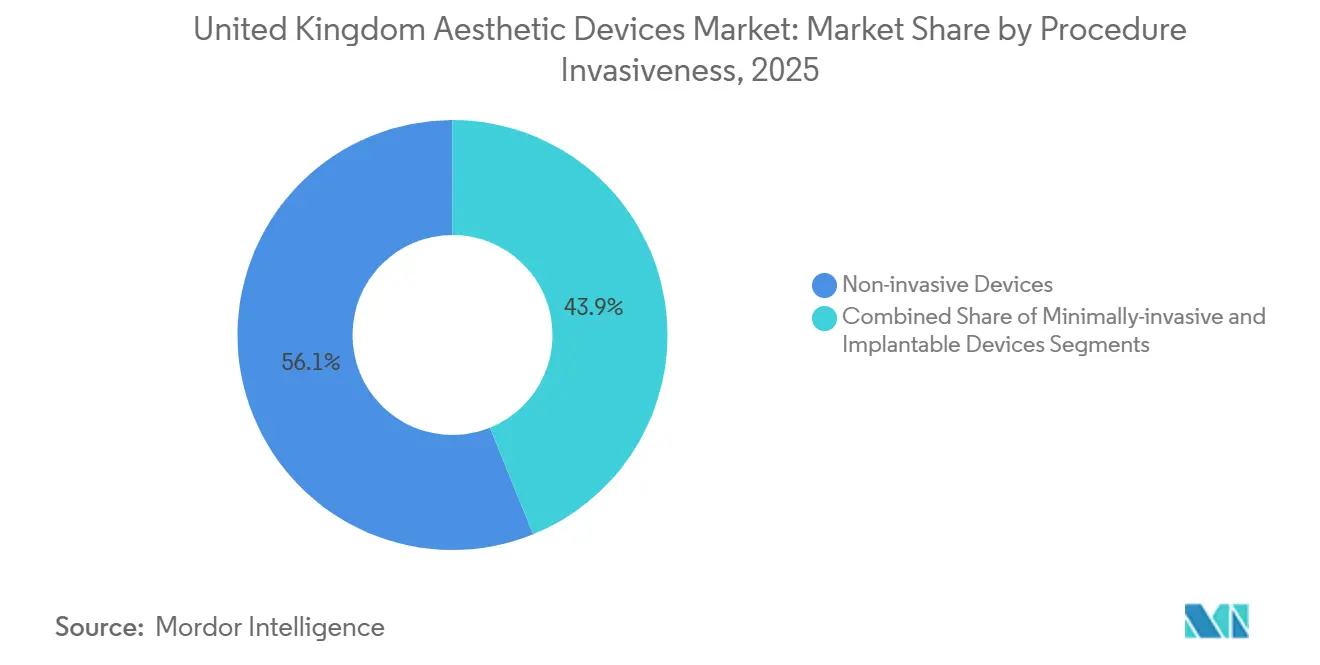

- By procedure invasiveness, non-invasive solutions held 56.12% of 2025 demand, yet minimally-invasive systems are on track for a 14.32% CAGR during the outlook period.

- By end-user, dermatology and cosmetic clinics contributed 44.21% of 2025 spending, whereas home-use settings are expected to grow at a 12.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Aesthetic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Minimally-Invasive Cosmetic Procedures | +2.1% | National, concentrated in London, Manchester, Birmingham metropolitan areas | Short term (≤ 2 years) |

| Aging Population with Higher Discretionary Income | +1.8% | National, with elevated spending in South East England, Edinburgh, Bristol | Medium term (2-4 years) |

| Rapid Technology Upgrades in Energy-Based Devices | +1.6% | National, early adoption in specialist dermatology hubs (Harley Street, Manchester) | Short term (≤ 2 years) |

| Expansion of Cosmetic Clinics & Medical Spas | +1.4% | National, accelerated growth in Sheffield, Belfast, Glasgow | Medium term (2-4 years) |

| NHS Outsourcing of Aesthetic Laser Services | +1.2% | England-focused, pilot schemes in Midlands and North West NHS trusts | Long term (≥ 4 years) |

| Growth in Gender-Affirming Body-Contouring Needs | +0.9% | National, concentrated in urban centers with specialized gender clinics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Minimally-Invasive Cosmetic Procedures

Consumers continue to favor treatments that avoid general anesthesia, produce little to no scarring and allow same-day discharge. BAAPS reported a 5% rise in non-surgical volumes in 2024, driven by protocols that pair radiofrequency microneedling with platelet-rich plasma for collagen remodeling without incisions.[1]British Association of Aesthetic Plastic Surgeons Staff, “BAAPS Audit 2024,” BAAPS, baaps.org.uk Thread-lift technology typifies this shift; Care Quality Commission guidelines now require surgical registration, weeding out poorly trained providers and boosting public confidence. Since 2016, the Association of PDO Thread Practitioners has certified more than 640 clinicians, standardizing technique and lowering complication rates. Combination plans that blend absorbable sutures with fillers or polynucleotides can extend visible results beyond 30 months, improving clinic retention rates.

Aging Population with Higher Discretionary Income

Individuals aged 50-64 hold median household wealth topping GBP 500,000, positioning them as the financial engine behind the United Kingdom aesthetic devices market.[2]Emily Jones, “Household Wealth Statistics 2024,” Office for National Statistics, ons.gov.uk Many prefer in-office radiofrequency or high-intensity focused ultrasound sessions over one-time surgery, valuing minimal downtime and natural-looking outcomes. Cynosure’s ELITE iQ PRO, introduced in 2024, cuts session length by a third yet delivers higher fluence, appealing to busy professionals. Real-time melanin-reader adjustments broaden suitability to Fitzpatrick IV-VI skin types, enlarging the market’s demographic base.

Rapid Technology Upgrades in Energy-Based Devices

Device makers increasingly fuse multiple energy sources—laser, radiofrequency, ultrasound and electromagnetic muscle stimulation—into modular workstations that reduce capital outlay while expanding treatment menus. Lumenis’ LightSheer QUATTRO dual-wavelength system shortens hair-removal plans from as many as 10 sessions to as few as 6, trimming per-patient variable costs.[3]Lumenis, “LightSheer QUATTRO Dual-Wavelength Platform,” Lumenis, lumenis.comBTL’s Emface Submentum couples synchronized RF heat with muscle stimulation to treat submental fat in under 20 minutes. InMode’s IgniteRF integrates microneedling and surface heating, giving clinics a single platform for acne scars, striae and laxity, all while avoiding lengthy CO2 downtime.

Expansion of Cosmetic Clinics & Medical Spas

Secondary cities with lower real-estate prices but solid disposable incomes are attracting clinic investment. Sk:n Clinics channeled GBP 500,000 into its July 2025 Belfast opening, debuting energy-based hair removal and body-contouring capabilities in a 2,000-square-foot space. Sheffield’s Wellness Space launched in spring 2025, focusing on polynucleotide injectables for Yorkshire professionals. Lorena Cosmetics’ acquisition of Sk:n and Harley Medical Group created a 30-site network that cross-sells aesthetic services alongside Optical Express vision correction, tightening margins for independent dermatologists.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent MHRA & EU-MDR Compliance Costs | -1.3% | National, disproportionate burden on small-to-midsize device importers | Short term (≤ 2 years) |

| High Treatment Cost to Consumers | -1.1% | National, acute in regions with below-median household income (North East, Wales) | Medium term (2-4 years) |

| Sustainability & Re-Processing Scrutiny | -0.7% | National, regulatory focus on single-use device waste reduction | Long term (≥ 4 years) |

| "Natural Look" Social-Media Backlash | -0.6% | National, strongest among Gen Z demographic (ages 18-27) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent MHRA & EU-MDR Compliance Costs

Manufacturers and importers must now appoint UK Responsible Persons, submit exhaustive technical files and undertake annual post-market surveillance to satisfy MHRA and EU-MDR rules. Smaller suppliers face yearly compliance bills between GBP 50,000 and GBP 150,000, often prompting portfolio cuts or market exits. New sustainability guidance adds environmental-impact assessments for single-use applicators, stretching approval timelines by up to a year.

High Treatment Cost to Consumers

Laser hair-removal packages run GBP 800-2,500, thread lifts GBP 1,200-3,000, and RF skin-tightening sessions GBP 300-800. With negligible NHS reimbursement, many households outside affluent corridors defer aesthetic spend. Finance plans help spread costs but borrow-rate premiums of 9-15% APR can add 30% to the final bill. Complication costs from overseas surgery—NHS spent GBP 110,690 in 2024—do generate some “buy local” momentum, yet price still curbs penetration in lower-income regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Energy Platforms Dominate, Thread Lifts Surge

Energy-based platforms controlled 41.32% of 2025 revenue, highlighting continued preference for laser hair removal, intense-pulsed-light photofacials and radiofrequency skin-tightening. The United Kingdom aesthetic devices market share for energy-based systems stems from their versatility and short learning curves, letting clinics amortize capital quicker than implant or injectable devices. Cynosure’s ELITE iQ PRO illustrates the arms race for higher power and larger spot sizes, shaving treatment times and lifting margin per staff hour.

Thread-lift kits are the breakout category, forecast to rise at 12.52% CAGR thanks to polydioxanone and poly-L-lactic sutures that suspend tissue without general anesthesia. The Care Quality Commission’s ruling that thread placement requires surgical registration removed unqualified operators and lifted consumer trust. As a result, the United Kingdom aesthetic devices market size for thread-lift systems is projected to expand from USD 48 million in 2026 to USD 87 million by 2031. Breast and facial implants face headwinds as patients favor autologous fat transfer, yet Allergan’s 2025 acquisition of Northwood Medical and its earFold implant shows niche hardware can still thrive when it addresses specific aesthetic pain points.

By Application: Facial Rejuvenation Leads, Tattoo Removal Accelerates

Facial contouring and skin-rejuvenation represented 36.64% of 2025 turnover, reflecting demand for collagen-boosting lasers, fractional RF and injectables that postpone surgical facelifts. Tattoo and scar removal is the fastest accelerator, set for 13.24% CAGR as picosecond lasers slash session counts by 75% versus older Q-switched systems.

Body-contouring maintains double-digit growth through radiofrequency-assisted lipolysis, cryolipolysis and high-intensity EM muscle stimulation, but competes with surgical liposuction for dramatic fat-loss seekers. Hair removal remains the United Kingdom aesthetic devices market workhorse by volume, yet commoditization pressures per-session prices. Breast-enhancement devices battle textured-implant scrutiny, while port-wine-stain laser therapies gain stability from NHS outsourcing agreements.

By Procedure Invasiveness: Minimally-Invasive Gains Ground

Non-invasive options captured 56.12% of 2025 demand, underscoring patient appetite for zero-downtime treatments. Nevertheless, minimally-invasive systems—which include RF microneedling, fractional CO2 and thread lifts—are pacing the field with a 14.32% CAGR. Their ability to penetrate deeper layers without general anesthesia positions them as the future backbone of the United Kingdom aesthetic devices market.

Combination procedures are fueling uptake. InMode’s IgniteRF delivers fractional microneedling plus bipolar RF in a single 20-minute visit, letting clinics treat scarring, laxity and striae simultaneously. BTL’s Emface Submentum applies RF and EM muscle stimulation under the chin, achieving fat reduction and lift without cryolipolysis plates. Regulatory restrictions on textured implants further tilt patient choices toward reversible, small-incision procedures.

By End-User: Clinics Dominate, Home-Use Expands

Dermatology and cosmetic clinics relied on specialist staff and Class IIb devices to capture 44.21% of 2025 value. The United Kingdom aesthetic devices market share among clinics remains under threat from vertical integrations such as Lorena Cosmetics’ takeover of Sk:n and Harley Medical Group, which cross-sell treatments to Optical Express eye-surgery customers. Hospitals occupy a niche centered on reconstructive indications, buoyed by NHS outsourcing that fills empty operating-room blocks with reimbursed laser cases.

Home-use gadgets—LED masks, microcurrent toners, percussive devices—are breaking beyond early-adopter circles. CurrentBody, NuFACE and TheraFace PRO lead, aided by social-media tutorials that demystify usage. Although capped at lower power outputs, these devices prolong in-clinic results and entice price-sensitive households that cannot finance a full professional course

Geography Analysis

London and the broader South East remain the locus of premium demand, supported by Harley Street’s specialist ecosystem and proximity to high-net-worth communities in Surrey and Berkshire. Manchester and Birmingham serve as northern and Midlands anchors, where clinic networks benefit from airport connectivity that pulls patients from surrounding counties. Edinburgh has emerged as Scotland’s aesthetic capital, with professional-grade facilities such as The Wellness Space satisfying clients who prefer to avoid travel to London.

Belfast entered the high-growth roster after Sk:n Clinics invested GBP 500,000 in its 2025 flagship, making energy-based hair removal and fractional RF treatments locally accessible. Wales and North East England continue to trail in per-capita spend due to below-median incomes; nonetheless, pockets of affluence in Cardiff and Newcastle underpin boutique practices. Across the United Kingdom aesthetic devices market, clinics face a compliance mosaic: England’s licensing consultation, Scotland’s draft framework and separate standards in Wales and Northern Ireland require multi-site operators to maintain jurisdiction-specific protocols that inflate legal and training budgets.

Medical tourism remains a challenge. Cut-price procedures in Turkey or Spain lure value-driven patients, yet NHS data on complication management costs are turning the narrative toward “stay-home, stay-safe.” Gender-affirming services add another regional layer: London, Manchester and Brighton clinics report steady bookings from transgender clients unable to secure timely NHS slots. These dynamics combine to keep the United Kingdom aesthetic devices market on a resilient regional growth footing.

Competitive Landscape

Market concentration is moderate. Allergan, Galderma and Merz Pharma dominate injectables through entrenched relationships with dermatologists, while BTL Aesthetics and InMode accelerate share in energy-based equipment by introducing multi-modal consoles that lower clinic capital outlay. Allergan’s May 2025 purchase of earFold developer Northwood Medical underscores interest in procedure-specific hardware that bypasses traditional otoplasty, whereas Galderma invests heavily in extended-duration hyaluronic acid fillers to fend off erosive price competition.

Lorena Cosmetics’ December 2024 takeover of Sk:n and Harley Medical Group stitched together more than 30 sites and rehired 150 staff, creating an integrated chain able to leverage Optical Express footfall. CurrentBody, NuFACE and TheraFace PRO ride e-commerce prowess to cement first-mover advantage in home-use LED and microcurrent tools. Cynosure rolled out the CynoGlow protocol in 2025, pairing Picosure Pro lasers with Potenza RF microneedling in a single visit, trimming patient journeys from six to four appointments and giving partner clinics a throughput edge.

Cutera’s partnership with the Medical Aesthetics Training Academy embeds AviClear acne lasers in Ofqual-regulated curricula, capturing device loyalty at the career outset. Meanwhile, 4T Medical’s modular Eve platform lets practices add or swap handpieces without purchasing a full console, curbing long-term capital expenditures by 30-40%. These strategies illustrate that the United Kingdom aesthetic devices industry rewards both scale and nimble engineering.

United Kingdom Aesthetic Devices Industry Leaders

BTL Aesthetics

Hologic (Cynosure)

Galderma

Lumenis

Abbvie

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: iSMART Developments signed a strategic partnership with L’Oréal Groupe to co-engineer professional LED face and eye masks, combining iSMART’s light-therapy expertise with L’Oréal’s skincare R&D pipeline.

- January 2026: InMode UK entered a collaboration with Cure Medical and appointed Adam Bashir as Managing Director to strengthen its presence across the United Kingdom and Ireland.

- July 2025: The Joint Council for Cosmetic Practitioners and BAAPS executed a Memorandum of Understanding aimed at elevating clinical standards and improving public safety in the aesthetic sector.

United Kingdom Aesthetic Devices Market Report Scope

Aesthetic devices are tools used for non-surgical or minimally invasive cosmetic procedures to improve appearance through technologies like lasers, radiofrequency, ultrasound, and light.

The United Kingdom Aesthetic Devices Market Report is segmented by Product, Application, Procedure Invasiveness, and End User. By Product, the market is segmented into Energy-based Aesthetic Devices, Breast Implants, Facial Implants, Dermal Filler/Injectable Delivery Devices, Microdermabrasion Devices, Thread-lift Devices, and Other Products. By Application, the market is segmented into Facial Contouring & Skin Rejuvenation, Body Contouring & Cellulite Reduction, Hair Removal, Breast Enhancement, Tattoo & Scar Removal, and Other Applications. By Procedure Invasiveness, the market is segmented into Non-invasive Devices, Minimally-invasive Devices, and Invasive/Implantable Devices. By End User, the market is segmented into Hospitals, Dermatology & Cosmetic Clinics, Medical Spas, and Home-use Settings. The Market Forecasts are Provided in Terms of Value (USD).

By Product

| Energy-based Aesthetic Devices |

| Breast Implants |

| Facial Implants |

| Dermal Filler/Injectable Delivery Devices |

| Microdermabrasion Devices |

| Thread-lift Devices |

| Other Products |

By Application

| Facial Contouring & Skin Rejuvenation |

| Body Contouring & Cellulite Reduction |

| Hair Removal |

| Breast Enhancement |

| Tattoo & Scar Removal |

| Other Applications |

By Procedure Invasiveness

| Non-invasive Devices |

| Minimally-invasive Devices |

| Invasive / Implantable Devices |

By End-User

| Hospitals |

| Dermatology & Cosmetic Clinics |

| Medical Spas |

| Home-use Settings |

| By Product | Energy-based Aesthetic Devices |

| Breast Implants | |

| Facial Implants | |

| Dermal Filler/Injectable Delivery Devices | |

| Microdermabrasion Devices | |

| Thread-lift Devices | |

| Other Products | |

| By Application | Facial Contouring & Skin Rejuvenation |

| Body Contouring & Cellulite Reduction | |

| Hair Removal | |

| Breast Enhancement | |

| Tattoo & Scar Removal | |

| Other Applications | |

| By Procedure Invasiveness | Non-invasive Devices |

| Minimally-invasive Devices | |

| Invasive / Implantable Devices | |

| By End-User | Hospitals |

| Dermatology & Cosmetic Clinics | |

| Medical Spas | |

| Home-use Settings |

Key Questions Answered in the Report

What is the 2031 value forecast for the United Kingdom aesthetic devices market?

It is projected to reach USD 1.83 billion, expanding at a 10.3% CAGR over 2026-2031.

Which product category is growing fastest?

Thread-lift devices are set for a 12.52% CAGR through 2031, driven by demand for minimally-invasive facial rejuvenation.

How large is the market for tattoo and scar removal platforms?

Picosecond-laser adoption is expected to lift the segment above USD 120 million by 2031, reflecting a 13.24% CAGR.

Why are minimally-invasive systems gaining traction?

They penetrate deeper tissue without general anesthesia, leading to a 14.32% projected CAGR and strong clinic adoption.

What regions show the highest clinic density?

London and the South East lead, followed by Manchester, Birmingham and Edinburgh, due to higher disposable incomes and specialist hubs.

How is NHS outsourcing affecting private providers?

The Provider Selection Regime supplies guaranteed laser-treatment volumes, stabilizing clinic revenue while requiring efficient operations.

Page last updated on: