Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

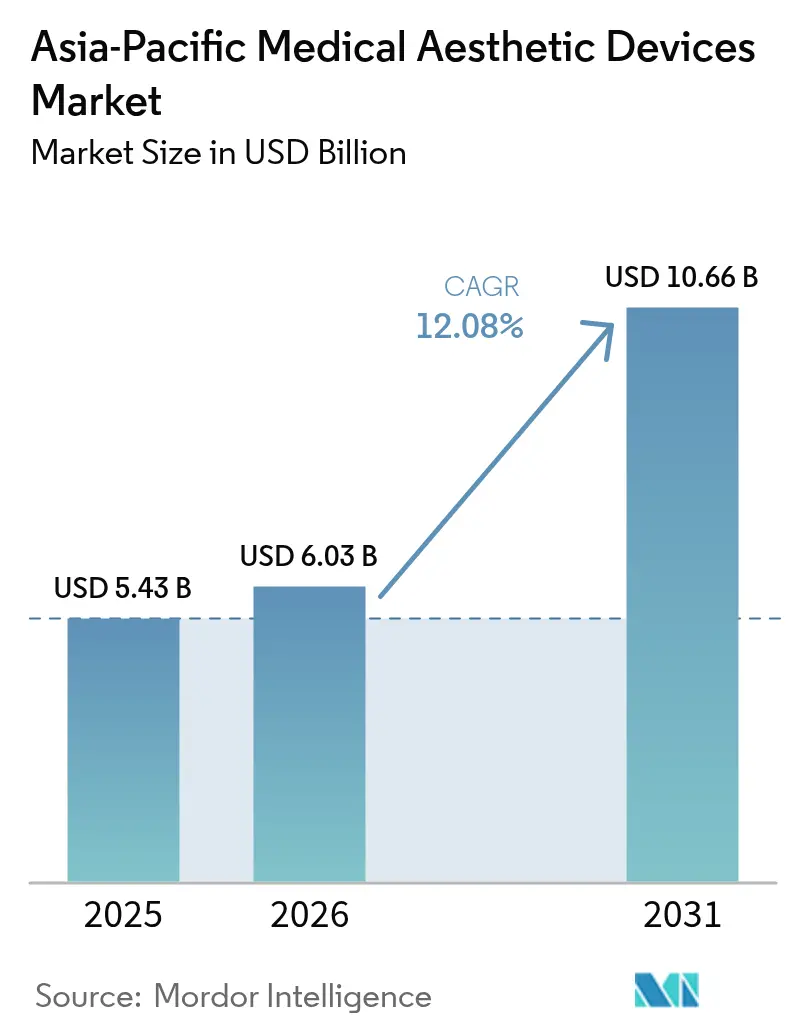

| Base Year Market Size (2025) | USD 5.43 Billion |

| Market Size (2026) | USD 6.03 Billion |

| Market Size (2031) | USD 10.66 Billion |

| Growth Rate (2026 - 2031) | 12.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Medical Aesthetic Devices Market Analysis by Mordor Intelligence

The Asia-Pacific Medical Aesthetic Devices Market size is projected to expand from USD 5.43 billion in 2025 and USD 6.03 billion in 2026 to USD 10.66 billion by 2031, registering a CAGR of 12.08% between 2026 to 2031.

Robust momentum reflects synchronized regulatory tightening that eliminates sub-standard equipment, domestic manufacturing incentives that shorten lead times, and a demographic pivot toward preventive aesthetics among consumers under 35.[1]National Medical Products Administration, “NMPA Announcement No. 30 on Radiofrequency Beauty Devices,” NMPA, nmpa.gov.cn China’s forthcoming Class III mandate for radiofrequency platforms and India’s 2024 reclassification of 1 178 devices have raised market-entry barriers, channeling volumes toward certified suppliers.[2]Central Drugs Standard Control Organisation, “Medical Device Reclassification 2024,” CDSCO, cdsco.gov.in Parallel advances in high-intensity focused ultrasound, picosecond lasers, and hybrid RF-microneedling systems compress downtime, making “lunchtime” procedures feasible for working professionals. Medical-tourism hubs in Seoul, Bangkok, and Singapore operate at elevated utilization rates, accelerating equipment amortization and widening the Asia‐Pacific medical aesthetic devices market’s installed base.

Key Report Takeaways

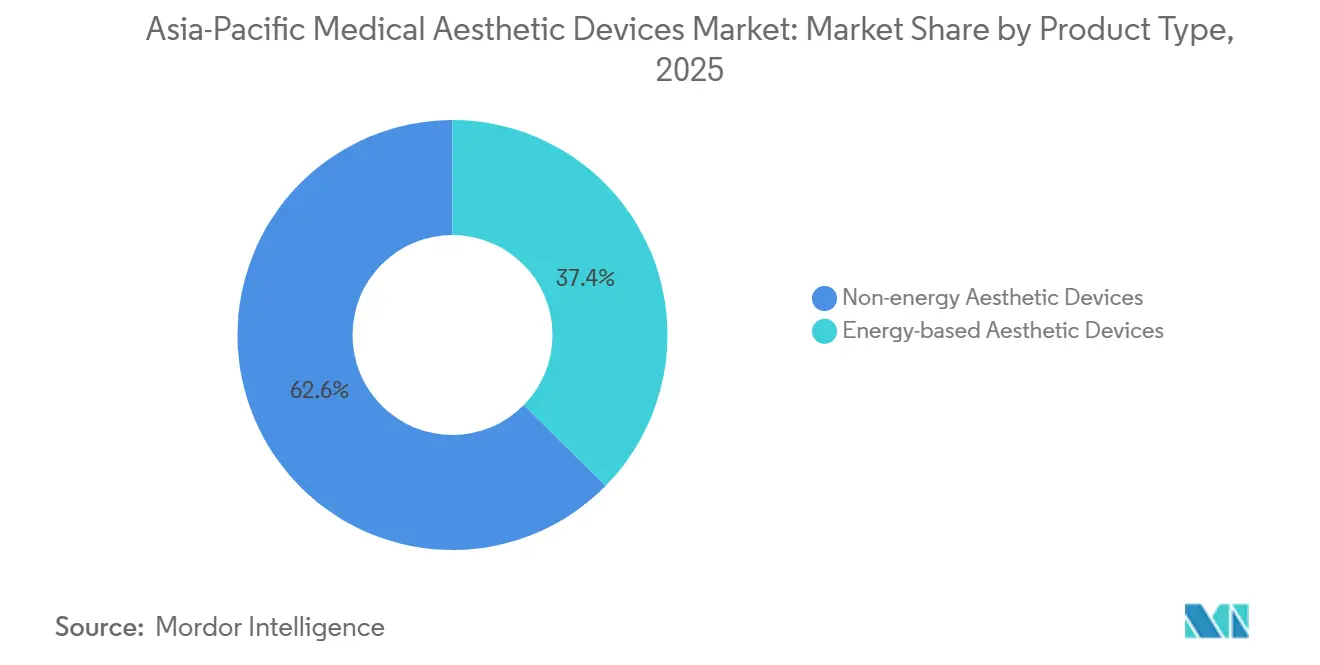

- By product type, energy-based aesthetic devices led with 37.36% revenue share in 2025, while non-energy-based devices are projected to expand at a 14.72% CAGR through 2031.

- By application, facial and body contouring accounted for 32.57% of the Asia-Pacific medical aesthetic devices market share in 2025; hair removal is forecast to grow at a 15.13% CAGR to 2031.

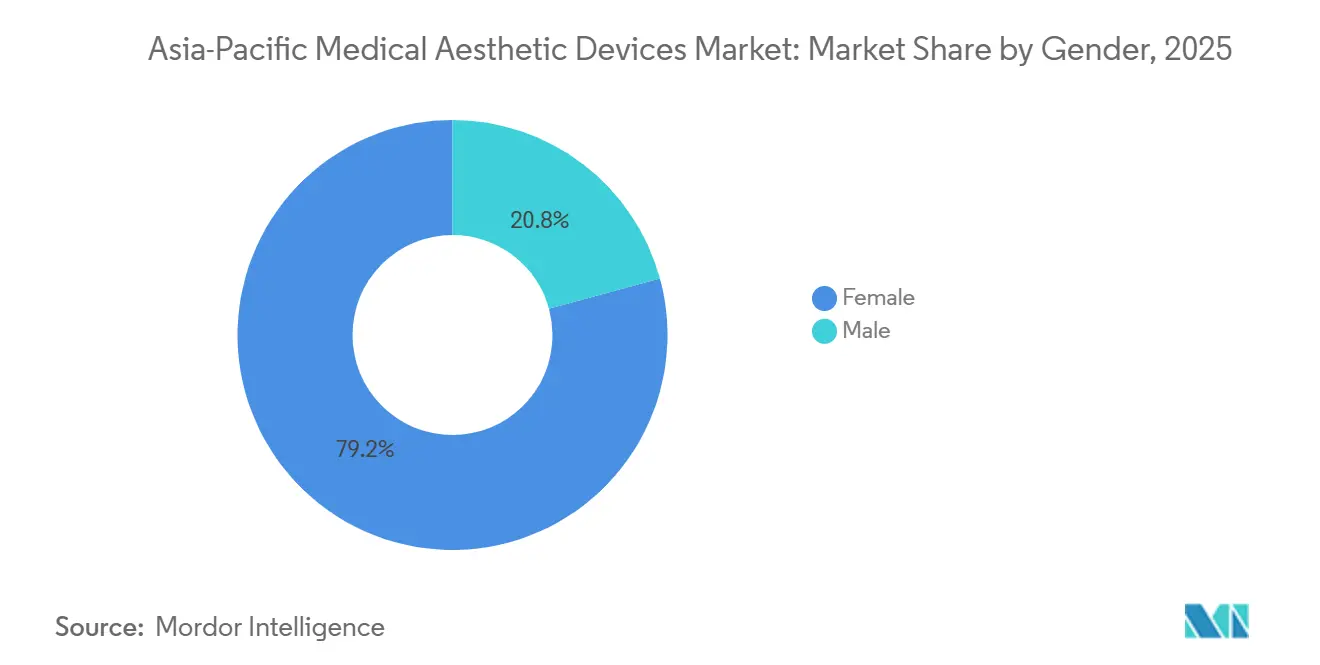

- By gender, female patients represented 79.24% of procedures in 2025, while the male segment is advancing at a 15.03% CAGR over 2026-2031.

- By age group, the 35-50 bracket commanded 45.82% of the Asia-Pacific medical aesthetic devices market size in 2025, and the 18-34 segment is projected to rise at a 14.68% CAGR to 2031.

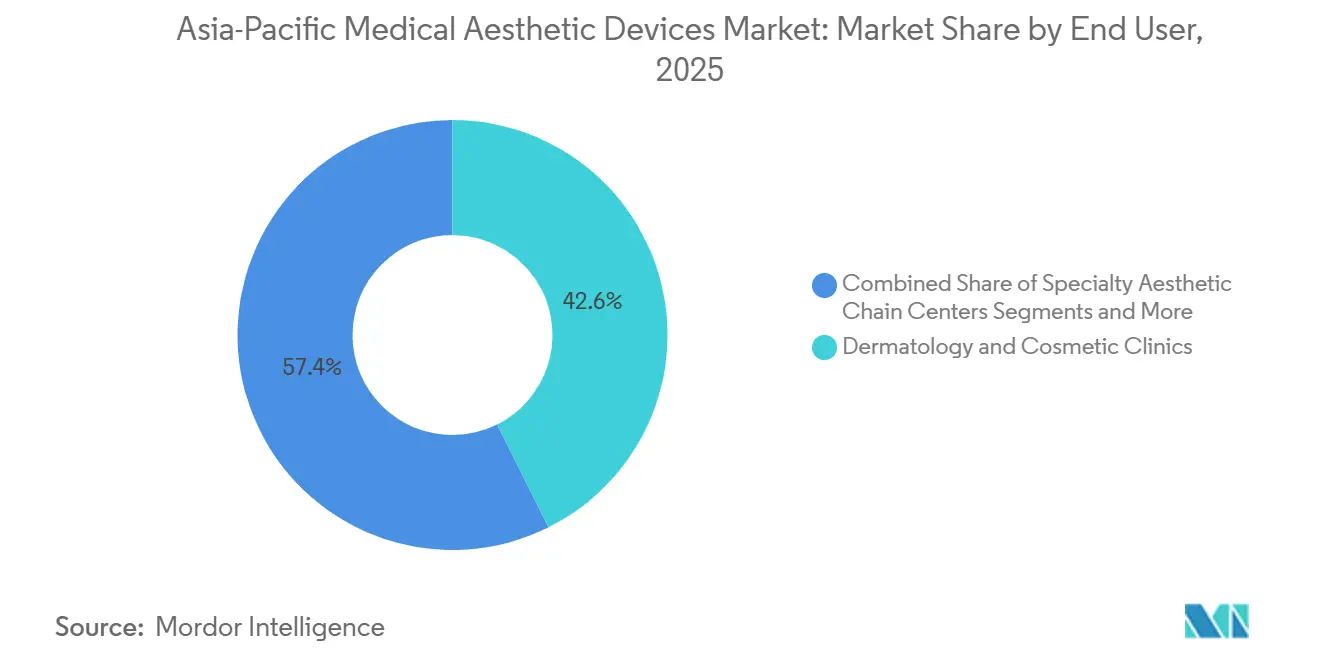

- By end-user, dermatology and cosmetic clinics held 42.63% revenue share in 2025; medical spas and wellness centers are set to expand at 14.72% CAGR through 2031.

- By geography, China contributed 33.72% country-level share in 2025, while India is expected to record the fastest CAGR at 14.22% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Medical Aesthetic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Disposable Incomes & Aesthetic Awareness | +2.1% | China, India, Vietnam, Indonesia, Philippines, Thailand | Medium term (2-4 years) |

| Expansion of Medical Tourism Hubs | +1.8% | South Korea, Thailand, Singapore, Bali, Malaysia | Short term (≤ 2 years) |

| Aging Population Seeking Anti-Aging Solutions | +1.6% | Japan, Australia, coastal China, South Korea | Long term (≥ 4 years) |

| Rapid Tech Advances in Minimally Invasive Systems | +2.3% | South Korea, Japan, urban China, global early adopters | Medium term (2-4 years) |

| China’s Domestic Device-Manufacturing Incentives | +1.9% | China, spillover across APAC | Medium term (2-4 years) |

| Social-Commerce-Fueled Demand in Tier-3 Asian Cities | +1.5% | China, Vietnam, Indonesia, Philippines | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes & Aesthetic Awareness

Per-capita disposable income in urban China exceeded CNY 50 000 (USD 7 000) in 2024, and India’s middle class could reach 580 million by 2030, enlarging the Asia-Pacific medical aesthetic devices market’s consumption base. Vietnam’s personal-care device segment rose 23.7% between 2022 and 2024, led by Korean-branded lasers online. Social media influencers on Douyin and TikTok normalize preventive treatments for users in their twenties. Bali logged a 21% jump in plastic-surgery tourism in 2024, underscoring cross-border willingness to spend on aesthetics.[3]Bali Tourism Board, “Plastic Surgery Tourism Growth 2024,” Bali Tourism Board, balitourismboard.or.id Clinics respond with “skin-health” packages that bundle laser rejuvenation with nutrient IV drips, extending the Asia-Pacific medical aesthetic devices market’s procedural breadth.

Expansion of Medical Tourism Hubs

South Korea hosted more than 600 000 foreign patients in 2024, most seeking skincare and plastic-surgery procedures that rely on premium energy platforms. Thailand and Singapore leverage international accreditation and multilingual staff to sustain throughput that shortens payback cycles. Bali positions itself as a wellness retreat, fusing spa experiences with minimally invasive procedures. The model elevates device utilization but highlights follow-up care gaps once travelers return home, driving interest in teledermatology. Continued tourist inflows reinforce stable demand across the Asia-Pacific medical aesthetic devices market.

Aging Population Seeking Anti-Aging Solutions

Japan’s median age tops 49, and seniors invest in non-surgical skin tightening to maintain workplace vitality. Coastal China, Australia, and South Korea exhibit similar trends, anchoring a base of collagen-stimulating procedures. A Seoul National University Hospital study showed fractional CO₂ laser plus platelet-rich plasma improved skin elasticity 40% over laser-alone therapy, cementing combination protocols. Vendors enhance ergonomics and cooling to accommodate older physicians and sensitive skin, extending replacement demand within the Asia-Pacific medical aesthetic devices market.

Heightened Beauty Awareness Via Social Media Influence

Hybrid RF-microneedling, picosecond lasers, and ultrasound with real-time imaging deliver results once possible only with surgery. Japan cleared HIFU systems that visualize tissue layers, reducing adverse events. Chinese makers such as Sincoheren embedded AI algorithms that auto-adjust pulse width, shrinking the skill gap with global brands. Continuous innovation compresses upgrade cycles and enlarges cumulative installations, supporting sustained growth in the Asia-Pacific medical aesthetic devices market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Procedure & Device Costs Beyond Metro Areas | -1.4% | India, Indonesia, Philippines, Vietnam | Medium term (2-4 years) |

| Fragmented & Evolving Regulatory Regimes | -1.2% | ASEAN, India, China (provincial) | Long term (≥ 4 years) |

| Proliferation of Counterfeit/Grey-Market Devices | -1.0% | China, India, Southeast Asia | Short term (≤ 2 years) |

| Shortage of Certified Aesthetic Practitioners | -1.6% | India, Indonesia, Vietnam, Philippines, rural Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Procedure & Device Costs Beyond Metro Areas

Picosecond and HIFU systems list above USD 100 000, prices rural clinics in India or Indonesia struggle to finance. Import duties inflate costs by up to 60%, forcing operators to rely on older IPL units that offer lower efficacy. Pay-per-pulse contracts are emerging yet hinge on dependable credit enforcement, which remains patchy across ASEAN, restraining the Asia-Pacific medical aesthetic devices market.

Fragmented & Evolving Regulatory Regimes

ASEAN states maintain divergent dossier formats, while India delegates some inspections to state agencies, creating regional inconsistencies. China’s provincial audits add another compliance layer post-NMPA clearance. The resulting complexity raises overhead for innovators and slows product launches, dampening the Asia-Pacific medical aesthetic devices market’s velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type : Non-Energy Platforms Dominate, Energy Devices Surges

Energy platforms commanded 37.36% of Asia-Pacific medical aesthetic devices market size in 2025, led by lasers that cover hair removal, pigmentation, and vascular lesions. Competitive pressure from Shenzhen and Seoul lowers unit prices, driving brands to differentiate via AI-guided spot sizing and cloud analytics. HIFU systems with imaging layers reduce adverse events, helping Japan and South Korea refresh installed fleets. Fractional RF-microneedling devices gain traction in urban China for cellulite and acne-scar repair. Cryolipolysis faces post-patent price erosion yet widens access in tier-3 Chinese cities. Light and IPL systems appeal to budget clinics despite efficacy limits on darker skin types. Plasma pens, electroporation wands, and LED masks capture niche demand on social-commerce sites. Non-energy segments—breast implants, thread lifts, injector pens—diversify revenue; thread-lift kits resurge among patients seeking quick facelifts in Seoul and Bangkok. Vendors bundle multi-modality workstations that lock clinics into proprietary consumables, anchoring lifetime value inside the Asia-Pacific medical aesthetic devices market.

By Application : Hair Removal Accelerates, Facial Contouring Leads

Facial and body contouring held 32.57% of Asia-Pacific medical aesthetic devices market share in 2025 as consumers pursued jawline sculpting and muscle toning. Radiofrequency, HIFU, and cryolipolysis platforms dominate, now incorporating impedance sensors for safety. Hair removal is projected to expand at 15.13% through 2031 on male grooming trends and falling diode-laser costs. Compact units optimized for Fitzpatrick IV-V drive adoption in Ho Chi Minh City and Bangalore. Picosecond lasers, validated by Shanghai Jiao Tong University’s 2025 study, propel tattoo and pigmented-lesion removal. Acne, vascular, and scar treatments rely on pulsed-dye lasers and microneedling. Breast augmentation stays hospital-centric but supports adjunct RF scar-management sales. Stretch-mark and intimate-rejuvenation niches grow as social stigma wanes, broadening the Asia-Pacific medical aesthetic devices market’s procedure mix.

By Gender : Male Segment Outpaces Female Growth

Female patients delivered 79.24% of procedures in 2025, a stable base that underpins consumable revenue. The male cohort, however, is advancing at 15.03% CAGR to 2031, transforming the Asia-Pacific medical aesthetic devices market. Men enter via beard-line laser hair removal, neuromodulators, and fat-freezing for abdomen definition. Clinics host barbershop pop-ups and corporate seminars to destigmatize treatments. Device settings adjust for thicker dermis and higher sebum, prompting vendors to issue male-specific protocols. Home-use LED masks marketed to gamers extend brand reach and normalize ongoing maintenance.

By Age Group : Youth Drives Preventive Shift

The 35-50 segment owned 45.82% of Asia-Pacific medical aesthetic devices market size in 2025 through anti-aging regimens that bundle fractional CO₂ lasers with dermal fillers. The 18-34 group is growing at 14.68% CAGR, fueled by “pre-juvenation” culture and lighter diode or LED routines. Compact desktop lasers priced under USD 30 000 target first-time clinic owners chasing Gen-Z clientele. Patients over 50 choose higher-energy devices yet remain price sensitive, limiting volume to top-tier cities. Loyalty memberships lock younger users into decade-long maintenance plans, embedding recurring revenue inside the Asia-Pacific medical aesthetic devices market.

By End-User : Medical Spas Gain Share

Dermatology and cosmetic clinics captured 42.63% of revenue in 2025, acting as reference sites for new technology launches. Hospitals handle invasive procedures but face capacity limits. Medical spas and wellness centers are forecast to grow at 14.72% CAGR, bundling IV drips, nutrition counseling, and mindfulness apps to frame aesthetics as self-care. Home-use gadgets open consumer-electronics channels; specialty franchise chains standardize protocols across tier-2 Chinese and South Korean cities. China’s Class III RF mandate may force under-capitalized spas to upgrade fleets or exit, consolidating the Asia-Pacific medical aesthetic devices market around compliant operators.

Geography Analysis

China supplied 33.72% of Asia-Pacific medical aesthetic devices market share in 2025, driven by localization incentives and social-commerce conversion in tier-3 cities. NMPA’s April 2026 Class III deadline is expected to purge non-compliant devices, although provincial enforcement varies. Japan maintains premium pricing but slower rollouts owing to PMDA approval lags of up to 18 months. Australia’s Therapeutic Goods Administration ensures safety through rigorous reviews, sustaining steady demand in Sydney, Melbourne, and Brisbane.

India is poised for the fastest CAGR at 14.22% through 2031 on rising incomes and CDSCO streamlining, despite 70-80% import dependence that inflates landed costs. Tier-2 cities embrace vendor leasing and bank financing, expanding the Asia-Pacific medical aesthetic devices market’s footprint. South Korea regained medical-tourism momentum with 600,000 foreign patients in 2024, though upcoming tax-refund removal in 2025 prompts clinics to bundle loyalty perks. Korean device makers extend RF and HIFU exports into ASEAN.

Rest of Asia-Pacific—Thailand, Vietnam, Indonesia, Malaysia, and the Philippines—offers mixed growth. Thailand and Singapore attract Middle Eastern clients via JCI-accredited centers. Vietnam’s e-commerce channels funnel Korean lasers to provincial buyers. Bali’s 21% jump in 2024 plastic-surgery tourism drives local clinic upgrades. Malaysia and the Philippines tighten regulatory oversight, improving investor confidence yet tempering short-term volume. Geographic diversification cushions macro shocks, supporting a resilient Asia-Pacific medical aesthetic devices market.

Regulatory Landscape

Regulation across Asia-Pacific is tightening around aesthetic technologies, which is raising entry barriers and shifting demand toward certified suppliers. In China, the National Medical Products Administration (NMPA) requires Class III certification for radiofrequency (RF) aesthetic platforms by April 1, 2026, and provincial audits add another enforcement layer beyond national clearance. India has also increased oversight by reclassifying a set of medical devices in 2024 under the Central Drugs Standard Control Organisation (CDSCO), which elevates compliance requirements for importers and local distributors.

Several markets are formalizing oversight of devices that previously sat in borderline categories. Malaysia’s Medical Device (Designated Medical Device) Order 2026, under the Medical Device Act 2012, takes effect June 1, 2026 and explicitly brings aesthetic-purpose devices such as HIFU and liposuction equipment into the regulated medical device framework. In Australia, the Therapeutic Goods Administration (TGA) extended the transition deadline to July 1, 2029 for certain devices that are substances introduced into the body via a body orifice or applied to the skin, covering parts of the injectable and topical-applied device ecosystem. In parallel, China’s revised medical device Good Manufacturing Practice requirements take effect on November 1, 2026, lifting quality-system expectations for domestic production and contract manufacturing.

Value Chain Analysis

The value chain runs from platform R&D (energy delivery, cooling, imaging, and software) through precision component sourcing (laser diodes, optics, RF generators, ultrasound transducers), device assembly and quality control, and then commercialization via distributors, direct sales teams, and clinic-group procurement. Asia-Pacific manufacturing and engineering hubs such as China, South Korea, Taiwan, Singapore, and Malaysia support export-oriented production as well as regional customization. Post-sales service, including installation, calibration, preventive maintenance, and operator training, is a recurring differentiator because device uptime directly affects clinic economics.

Distribution and service models are moving toward tighter channel control and more localized capability. For example, Solta Medical (Bausch Health) completed the acquisition of its longtime China distribution partner, the Shibo Group, in December 2025, which supports more direct customer access and after-sales coverage in a high-volume market. Logistics volatility is also affecting planning, with medical cargo re-routing around the Cape of Good Hope reported to add roughly 10 to 14 days of transit time, increasing the need for regional inventory buffers, local assembly, and faster spare-parts availability for clinics and chains.

Competitive Landscape

The Asia-Pacific medical aesthetic devices market features moderate fragmentation. AbbVie’s Allergan Aesthetics, Lumenis, Candela, and Cynosure defend premium tiers, while South Korean challengers Jeisys Medical, Classys, and Hironic and Chinese makers Sincoheren and Sanhe Tongfei scale aggressively. The Cynosure–Lutronic merger in Q1 2024 produced a 130-country distribution footprint and a portfolio spanning picosecond lasers, RF microneedling, and cryolipolysis. Korean firms translate domestic clinical insights into competitively priced export models, gaining traction in India and Southeast Asia. Private-equity investors such as Bain Capital and KKR finance factory expansions and regional sales hubs.

Chinese manufacturers close technology gaps through AI-driven pulse modulation and impedance feedback that lower operator-skill thresholds. Sincoheren’s planned IPO will fund overseas regulatory filings, intensifying price pressure while widening the Asia-Pacific medical aesthetic devices market. Regulatory compliance acts as a competitive moat; Class III certification and ASEAN dossier alignment favor companies with robust quality systems. Hybrid workstations that stitch laser, RF, and ultrasound into one chassis lock clinics into consumable ecosystems. Cloud analytics enable usage-based invoicing, easing capital hurdles for smaller spas. Differentiation now centers on reduced downtime, patient comfort, and regenerative-medicine integrations such as platelet-rich plasma kits.

Asia-Pacific Medical Aesthetic Devices Industry Leaders

Lumenis Inc.

Cutera Inc.

AbbVie (Allergan Aesthetics)

Cynosure LLC

Johnson and Johnson Services LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace is most visible where regulatory tightening and clinical demand overlap, especially for clinics and chain operators seeking compliant RF and multi-modality consoles as enforcement tightens (notably China’s April 1, 2026 Class III RF requirement), and in premium markets where safety and workflow improvements carry pricing power. Continued platform refresh is reflected in February 2026 dual approvals for Cynosure Lutronic’s Clarity II laser platform in both China and Japan, supporting a more synchronized regional rollout across two of the region’s most tightly regulated countries. This expands the addressable base for premium systems targeting high-throughput indications such as hair removal and pigmentation in dermatology and cosmetic clinics.

Commercial opportunity is also growing in the services-and-consumables layer that sits above hardware, including training, protocol standardization, and direct operations that increase attachment of disposables and skincare adjacencies. In April 2026, Classys announced expansion of direct operations in Japan, which signals a stronger focus on brand control and downstream recurring revenue in a market where PMDA review processes can shape launch sequencing. At-home and clinic-adjacent maintenance devices are another active whitespace area in Asia-Pacific consumer ecosystems, supported by disclosed scale such as APR (Medicube) reporting cumulative AGE-R at-home aesthetic device sales exceeding 6 million units globally as of January 2026, highlighting the opportunity for vendors to connect professional treatments with follow-on maintenance routines through integrated device and consumable programs.

Recent Industry Developments

- March 2026: Lumenis announced the commercial launch of triLIFT 2.0, a platform positioned around facial and body muscle stimulation, unveiled around the 2026 AAD annual meeting. The update broadens the companys non-invasive offering and supports upsell cycles for clinics seeking differentiated treatment categories beyond conventional lasers and RF.

- December 2025: Solta Medical (Bausch Health) completed the acquisition of the Shibo Group, its longtime distribution partner in China. Moving distribution in-house strengthens customer coverage, installation and service responsiveness, and pricing control in one of the regions largest device markets.

- July 2024: Cutera and its Japanese subsidiary, Cutera KK, signed a three-year strategic partnership with LOreal Japan to distribute SkinCeuticals products to medical and physician-led clinics in Japan. The agreement deepens clinic channel access and ties device-driven procedures more closely to complementary skincare regimens, supporting bundled offerings and higher share of wallet at the provider level.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers medical aesthetic devices sold and used across Asia-Pacific for cosmetic improvement procedures, mainly in dermatology, plastic surgery, and related care settings. It includes energy-based systems like laser, light/IPL, RF, ultrasound/HIFU, cryolipolysis, and also select non-energy devices used for aesthetic procedures.

Scope exclusions: We exclude ordinary consumer beauty gadgets and topical skincare products that are not regulated or marketed as medical aesthetic devices.

Segmentation Overview

- By Product Type

- Energy-based Aesthetic Devices

- Laser-based Devices

- Light / Intense Pulsed Light (IPL) Devices

- Radiofrequency Devices

- Ultrasound / HIFU Devices

- Cryolipolysis Devices

- Plasma & Electroporation Devices

- LED & Photodynamic Therapy Devices

- Non-energy Aesthetic Devices

- Breast Implants (Silicone & Saline)

- Tissue Expanders

- Dermal Injector Systems

- Microdermabrasion Devices

- Thread-Lift Devices

- Others

- Energy-based Aesthetic Devices

- By Application

- Facial & Body Contouring

- Skin Rejuvenation & Resurfacing

- Hair Removal

- Tattoo, Pigmented & Scar Lesion Removal

- Breast Augmentation & Reconstruction

- Acne & Vascular Lesion Treatment

- Others

- By Gender

- Female

- Male

- By Age Group

- 18–34 Years

- 35–50 Years

- Above 50 Years

- By End-User

- Dermatology & Cosmetic Clinics

- Hospitals & Ambulatory Surgery Centers

- Medical Spas & Wellness Centers

- Home-use / Direct-to-Consumer

- Academic & Research Institutes

- Specialty Aesthetic Chain Centers

- By Country

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping the APAC country coverage, then building out the procedure and device landscape, and aligning it to what is actually sold through clinical channels. We refer to public sources such as national health ministries and statistical offices across APAC, customs and trade portals, the World Bank and OECD macro series, and clinical literature indexed on PubMed to understand adoption and procedure patterns.

We also review listed-company filings, annual reports, investor presentations, and reputable press coverage to track product launches, pricing direction, and channel expansion in key countries like China, Japan, India, South Korea, and Australia. Where needed, we supplement with paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export tracking to cross-check the direction and realism of unit and value assumptions. These examples are not exhaustive, and many other public and paid references were used for data collection, validation, and clarification during the research.

Primary Interviews and Surveys

Primary work is used to test what desk sources cannot show clearly, especially pricing bands, real utilization rates, and where demand is shifting between clinics, hospitals, and medical spas. We interview a mix of manufacturers, distributors, service providers, and clinicians across APAC so device mix and procedure volume assumptions can be validated and, where necessary, adjusted before the final numbers are signed off.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 13% | |

| Mid tier: 51% | Functional/Unit leaders: 36% | |

| Smaller Players: 19% | Managers: 51% |

Market-Sizing & Forecasting

Our sizing logic uses a top-down build where procedure volumes and treatment setting activity are reconstructed by country, and then translated into device demand using penetration and replacement cycles for major modalities. To keep the totals realistic, the outputs are then checked through selective bottom-up checks, such as sampled ASP ranges by device type, distributor channel checks, and supplier-side revenue cues for the region.

Key inputs that move the model include the number of aesthetic clinics and hospital departments actively offering procedures, procedure mix shifts between hair removal, skin resurfacing and tightening, and body contouring, and the installed base replacement timing for laser, RF, ultrasound/HIFU, and cryolipolysis platforms. We track pricing direction by modality, including service and consumable attachment expectations where relevant, along with regulatory approvals and guideline updates by country, and macro indicators tied to discretionary health spend that influence elective procedure demand.

For forecasting, scenario analysis is applied around country-level demand drivers and regulatory pace, and then refined using expert consensus on near-term adoption for newer modalities like plasma and electroporation, and LED and photodynamic therapy systems. Where bottom-up signals are thin for smaller APAC countries, gaps are handled through peer-market proxies using similar clinic density and procedure intensity, followed by a final normalization to keep regional totals consistent.

Data Validation & Update Cycle

Validation is done through multiple passes, where model results are compared against independent signals such as trade flows for relevant device categories, public company regional commentary, and the expected relationship between procedure growth and device replacement demand. When a large variance shows up, we re-check the assumption chain and re-contact a small set of respondents to confirm whether it reflects a real market shift or a data artifact.

Before sign-off, the numbers and the written story are reviewed by another analyst to catch outliers, unit issues, and inconsistent country totals. The dataset is refreshed annually, with interim updates made when material events happen, such as regulatory changes or major pricing resets. Right before delivery, a fresh pass is completed so clients receive an up-to-date view instead of an older snapshot.

Mordor Intelligence's Asia Pacific Medical Aesthetic Devices Market Market Size Measured Against Other Published Estimates

Published market sizes for APAC medical aesthetic devices can look far apart, even when the topic title sounds the same. This usually happens because the included product set differs, the year and currency timing are not aligned, and the demand indicators chosen for sizing are not the same.

The biggest gap driver here is scope, since some sources blend in injectables and other non-device cosmetic products, while others keep the market closer to device hardware and capital equipment categories. Differences also come from how ASP changes are applied across energy-based platforms, how fast home settings are assumed to expand, and how country totals are updated when China or Japan procedure trends move quickly, which can shift the regional total by a meaningful amount.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.43 B (2025) | |

| Industry Publisher A | USD 3.35 B (2024) | Uses an earlier base year and a broader framing that can mix procedure-led buckets with device revenues, which can understate fast-growing energy-based systems if country updates are not synchronized. |

| Industry Publisher B | USD 3.95 B (2024) | Often reports a wider aesthetic category set and may include adjacent non-device product lines under facial aesthetics, and then applies uniform growth rates that smooth out modality-level price and replacement cycle differences. |

The spread in the table is mainly explained by year alignment and what gets counted as a device versus adjacent aesthetic products, and then by how pricing and replacement cycles are treated across modalities. By keeping the scope tied to APAC device categories such as laser, IPL, RF, ultrasound/HIFU, cryolipolysis, and defined non-energy device types, and by re-validating country assumptions when procedure and clinic signals change, the estimate stays easier to trace and repeat, which is the approach applied by Mordor Intelligence.

Key Questions Answered in the Report

How large will Asia-Pacific medical aesthetic devices spending be by 2031?

The market is forecast to reach USD 10.66 billion by 2031, expanding at a 12.08% CAGR over 2026-2031.

Which product category is growing fastest?

Non-invasive body-contouring systems are projected to grow at 14.72% per year, outpacing all other device types.

Why is India considered the fastest expanding country opportunity?

Rising disposable incomes plus CDSCO regulatory streamlining push India toward a 14.22% CAGR through 2031.

How are social-commerce platforms influencing demand?

Douyin, TikTok, and similar apps normalize preventive procedures among younger users, generating appointment surges in tier-2 and tier-3 Asian cities.

What regulatory change will impact China in 2026?

NMPA requires all radiofrequency aesthetic platforms to hold Class III certification by April 1 2026, eliminating non-compliant devices.

Which end-user segment is set for the quickest growth?

Medical spas and wellness centers are expected to advance at a 14.72% CAGR as they pair aesthetic treatments with holistic wellness services.

Page last updated on: