Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

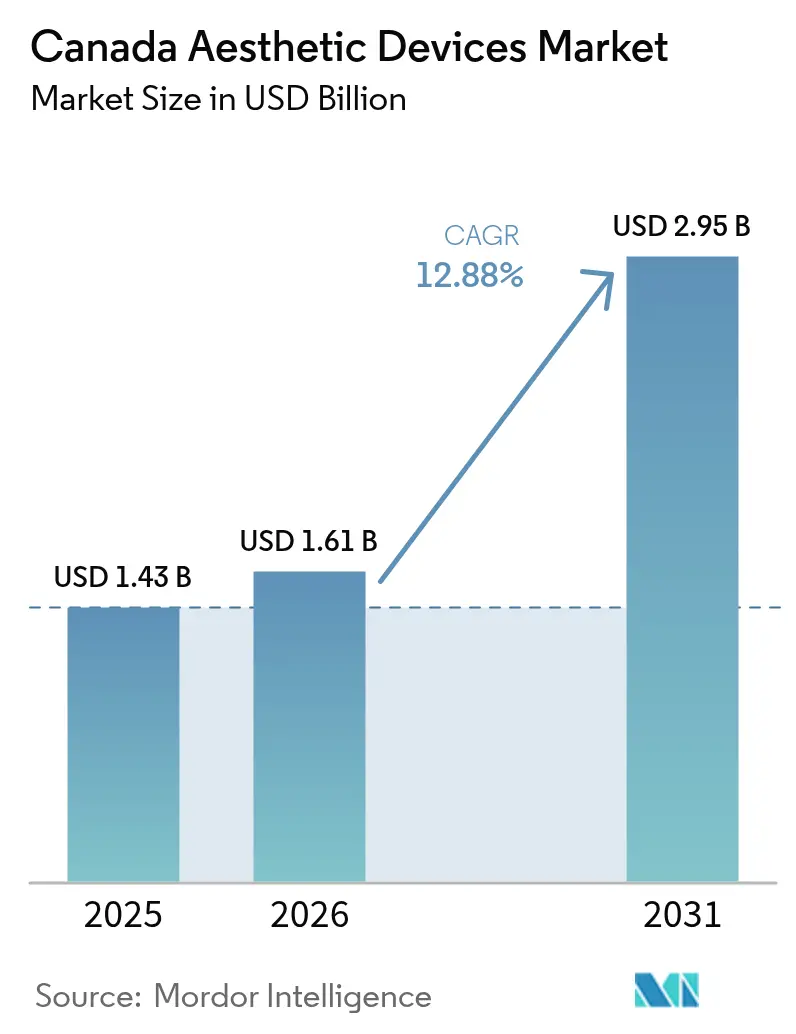

| Base Year Market Size (2025) | USD 1.43 Billion |

| Market Size (2026) | USD 1.61 Billion |

| Market Size (2031) | USD 2.95 Billion |

| Growth Rate (2026 - 2031) | 12.88% CAGR |

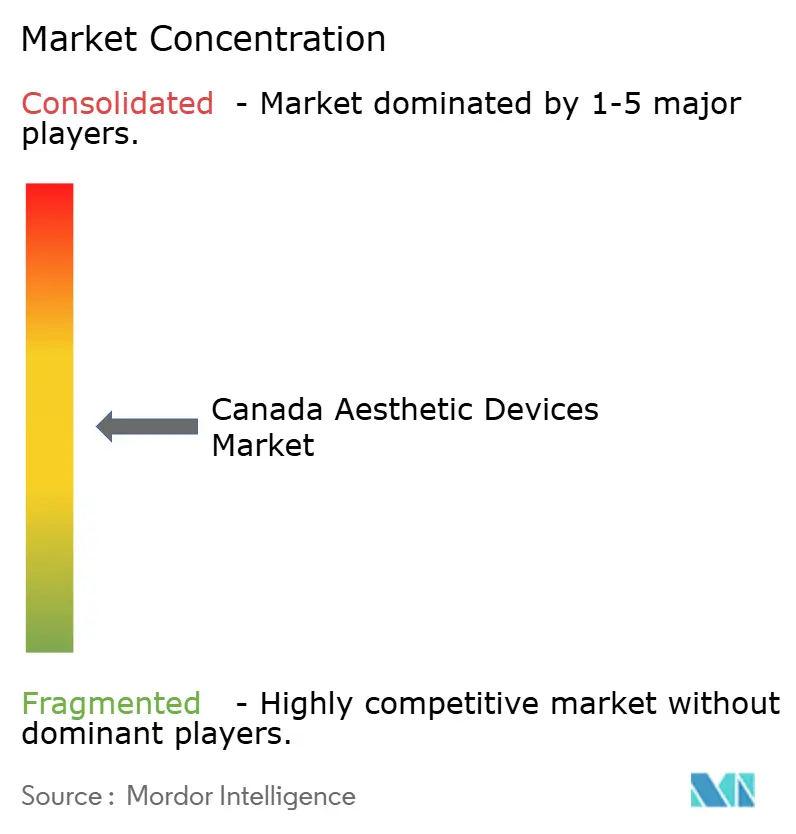

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Aesthetic Devices Market Analysis by Mordor Intelligence

Canada Aesthetic Devices Market size market size in 2026 is estimated at USD 1.61 billion, growing from 2025 value of USD 1.43 billion with 2031 projections showing USD 2.95 billion, growing at 12.88% CAGR over 2026-2031.

Gains reflect Canada’s position as an early-adopter environment where Health Canada’s risk-based classification and lifecycle management rules accelerate approvals for energy-based equipment and hybrid systems. Multimodal platforms that fuse laser, radio-frequency, and ultrasound deliver broader clinical versatility, while artificial-intelligence (AI) engines embedded in next-generation consoles shorten learning curves for newly trained practitioners. Private equity inflows are reshaping the competitive landscape by backing chain-building strategies that standardize device fleets and leverage centralized marketing. Meanwhile, cross-border patient flows from the United States, combined with Canadians’ rising preference for minimally invasive care, expand addressable procedure volumes across large urban centers.

Key Report Takeaways

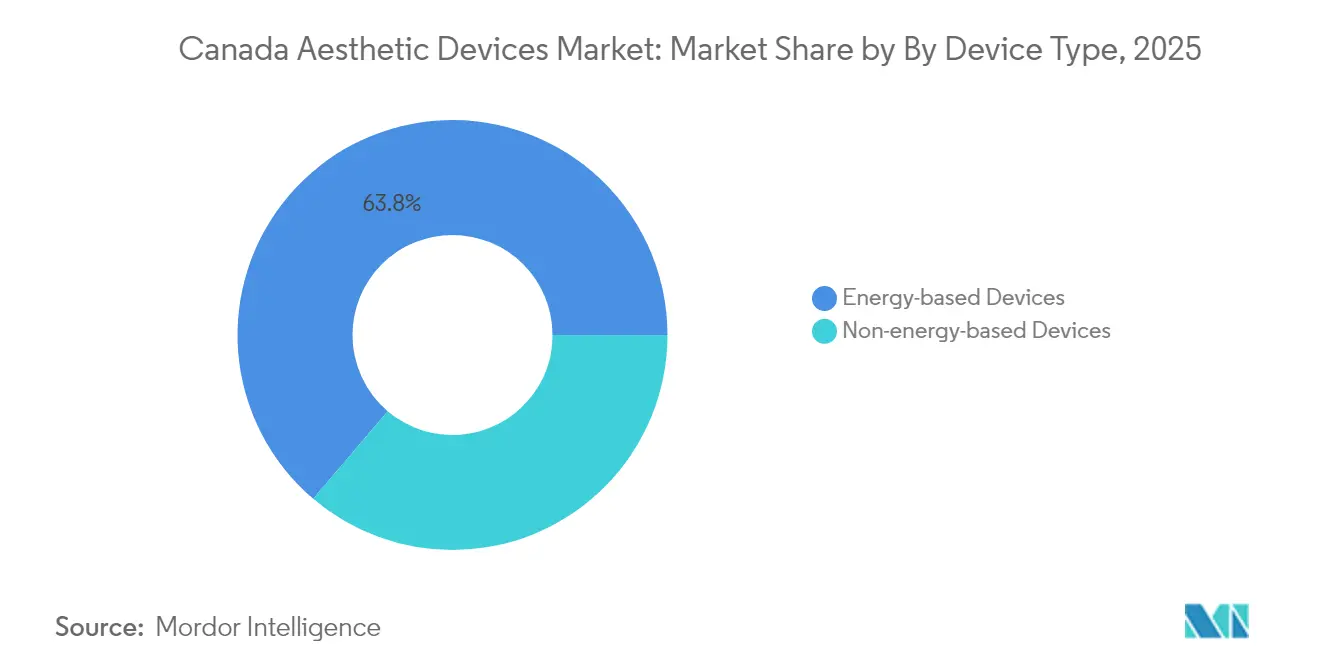

- By device type, energy-based units accounted for 63.78% revenue share in 2025 and ultrasound-guided systems are advancing at a 15.98% CAGR through 2031.

- By application, skin resurfacing and tightening represented 36.71% share of the Canada aesthetic devices market size in 2025 while body contouring and cellulite reduction is projected to grow at a 14.45% CAGR to 2031.

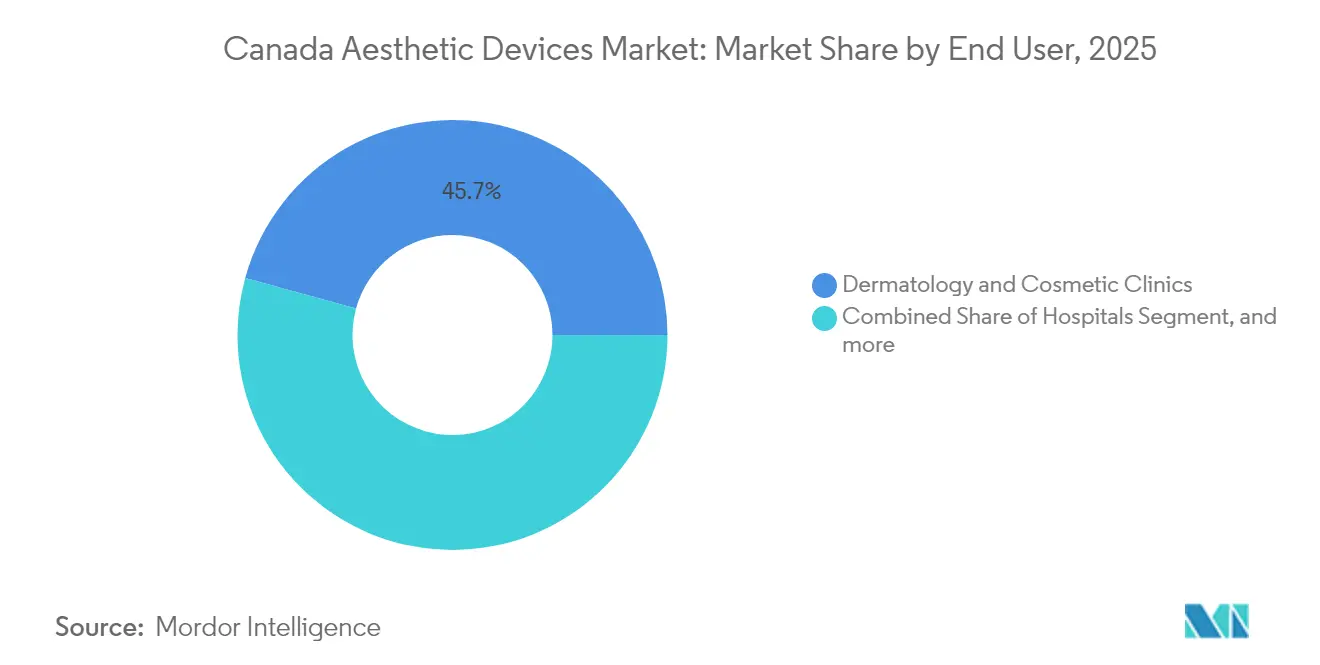

- By end user, dermatology and cosmetic clinics captured 45.72% Canada aesthetic devices market share in 2025, whereas the home-use segment is expected to post a 13.34% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Aesthetic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancements in Multimodal Platforms Integrating Technologies | +2.1% | National, with early gains in Toronto, Vancouver, Calgary | Medium term (2-4 years) |

| Rising Obesity Rates Driving Demand for Non-Invasive Body-Contouring Solutions | +2.8% | National, concentrated in urban centers | Short term (≤ 2 years) |

| Increasing Consumer Preference for Minimally-Invasive Aesthetic Procedures | +3.2% | National, strongest in Ontario and British Columbia | Medium term (2-4 years) |

| Expanding Medical Tourism Boosting Patient Volumes | +1.9% | National, with concentration in major metropolitan areas | Long term (≥ 4 years) |

| Growing Adoption of AI-Guided Treatment Planning Enhancing Precision | +1.7% | National, early adoption in academic medical centers | Long term (≥ 4 years) |

| Broader Societal Acceptance of Aesthetic Enhancements Across Age Groups | +1.3% | National, particularly strong in millennial and Gen Z demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Advancements in Multimodal Platforms Integrating Technologies

The integration of laser, radio-frequency, and ultrasound within single workstations cuts capital outlay while widening procedure menus. Candela’s Profound Matrix, cleared in 2023, bundles three applicators and Depth Intelligence software that automate energy delivery, trimming device-specific training time by 40%.[1]Candela, “Candela Announces Health-Canada Clearance of the New Profound Matrix™ System,” candela.com Small practices benefit because one platform now tackles resurfacing, tightening, and volumization tasks that previously required multiple devices. Health Canada’s Medical Device Single Review Program further hastens approvals for such combination products, closing the gap between prototype and clinic adoption.

Rising Obesity Rates Driving Demand for Non-Invasive Body-Contouring Solutions

Urban obesity prevalence steers patients toward cryolipolysis and focused-ultrasound systems that can remove stubborn adipose layers without surgery. Clinical evidence shows cryolipolysis delivering 0.69 cm mean circumference reduction at three months and strong satisfaction levels despite moderate measurement gains.[2]Lee H.J. et al., “The Efficacy and Safety of Cryolipolysis for Subcutaneous Fat Reduction,” Annals of Dermatology, ncbi.nlm.nih.gov Ultrasound-based platforms now penetrate up to 10 cm into subcutaneous tissue, mobilizing lipids through acoustic cavitation while avoiding thermal injury. Regulatory clarity is still evolving, offering a first-mover edge to firms demonstrating safety under Health Canada’s energy-based fat-reduction guidelines.

Increasing Consumer Preference for Minimally Invasive Aesthetic Procedures

Social-media exposure and the “pre-juvenation” ethos spur interest in subtle corrections that carry little downtime. Hyaluronic-acid micro-droplet techniques and micro-coring methods such as Cytrellis’s ellacor, approved in 2025, treat wrinkles by removing micro-columns of skin without scarring and with rapid recovery. Clinics that combine energy devices with injectables can therefore address preventive aesthetics as well as corrective care, capturing younger patient cohorts and expanding lifetime value.

Expanding Medical Tourism Boosting Patient Volumes

Canada’s reputation for rigorous yet innovation-friendly regulation attracts overseas patients looking for advanced technology and predictable quality. Academic centers in Toronto, Vancouver, and Montréal highlight compliance with ISO 13485 under the Medical Device Single Audit Program, reassuring foreign visitors. Favorable currency exchange further lowers procedure costs relative to the United States or Europe, elevating occupancy rates at high-end clinics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Reimbursement Policies for Aesthetic and Elective Procedures | -1.8% | National, affecting all provinces equally | Long term (≥ 4 years) |

| High Capital Investment Required for Advanced Energy-Based Systems | -2.3% | National, particularly impacting smaller practices | Medium term (2-4 years) |

| Shortage of Certified Laser-Safety Personnel Impacting Operational Compliance | -1.4% | National, acute in rural and smaller urban centers | Short term (≤ 2 years) |

| Rising Presence of Counterfeit Injectables in Grey-Market Channels | -0.9% | National, concentrated in major metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Reimbursement Policies for Aesthetic and Elective Procedures

Canada’s single-payer insurance excludes elective aesthetics, pushing consumers to pay out-of-pocket. Clinics therefore rely on higher-income demographics and financing plans, slowing penetration among middle-income patients. Although some reconstructive cases qualify for reimbursement, elective skin renewal and body-contouring remain patient-funded, constraining unit sales of premium hardware.

High Capital Investment Required for Advanced Energy-Based Systems

Flagship multimodal workstations can cost more than CAD 500,000 (USD 379,000) at 2024 average exchange rates, straining independent clinics’ budgets. Leasing mitigates upfront expenditure yet introduces interest and depreciation pressure that lengthen payback periods. As a result, private-equity backed chains and hospital-based centers dominate early uptake, while rural sites lag.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Energy-Based Dominance Driven by Ultrasound Innovation

Energy-based devices maintain 63.78% market share in 2025, with ultrasound-based technologies leading growth at 15.98% CAGR through 2031. This segment's expansion reflects technological maturation, where focused ultrasound systems like Alma TED achieve noticeable results within 2 weeks without topical anesthetics, addressing patient comfort concerns that historically limited adoption. Laser-based devices continue dominating current revenue streams through established hair removal and skin resurfacing applications, while radio-frequency systems gain traction for skin tightening procedures that complement injectable treatments. Light-based IPL devices serve entry-level market segments where lower capital requirements enable broader clinic adoption.

Cryolipolysis and plasma-based technologies face regulatory scrutiny that creates market uncertainty, with Health Canada issuing warnings about unauthorized plasma pens following safety complaints from Calgary and North York spas. Non-energy-based devices capture the remaining market share through established injectable portfolios, though growth rates lag behind energy-based alternatives due to treatment frequency limitations and adverse reaction concerns documented in Health Canada's MedEffect database . The segment benefits from Galderma's introduction of Restylane SHAYPE for chin augmentation in February 2024, demonstrating how specialized applications drive market expansion within mature product categories.

By Application: Body Contouring Emerges as Growth Leader

Body contouring and cellulite reduction applications experience a 14.45% CAGR through 2031, outpacing skin resurfacing and tightening's 36.71% market share in 2025. This growth acceleration stems from non-invasive body contouring technologies achieving 521% growth since 1997, with clinical studies demonstrating 2-4 cm circumference reductions across multiple treatment modalities. Hair removal maintains steady demand through established laser protocols, while tattoo and pigmentation removal benefits from advanced laser wavelengths that reduce treatment sessions and improve clearance rates. Breast augmentation applications face increased safety scrutiny following advocacy for a national breast implant registry, creating market uncertainty for device manufacturers in this segment.

Acne and scar treatment applications gain momentum through combination therapies that integrate radiofrequency with hyaluronic acid mesotherapy, demonstrating superior skin hydration and barrier function improvements compared to single-modality treatments. Other applications encompass emerging treatments like micro-coring technology and LED light therapy, where devices like the Nanoleaf LED mask achieve FDA Class II certification for home-use applications targeting multiple skin concerns simultaneously. The application diversity creates opportunities for specialized device manufacturers while challenging generalist companies to develop comprehensive treatment platforms.

By End User: Home-Use Settings Disrupt Traditional Care Models

Dermatology and cosmetic clinics hold 45.72% market share in 2025, yet home-use settings achieve 13.34% CAGR through 2031, signaling a fundamental shift in aesthetic care delivery models. This growth reflects Health Canada's evolving regulatory approach toward consumer-grade devices that meet Class I medical device standards while enabling unsupervised use. Professional clinics benefit from consolidation trends where private equity firms like Persistence Capital Partners acquire established practices to create multi-location platforms with standardized device portfolios and treatment protocols.

Hospitals represent the smallest end-user segment but maintain importance for complex procedures requiring medical supervision and emergency response capabilities. Medical spas experience rapid expansion through franchise models and corporate backing, though regulatory compliance challenges emerge as non-physician operators require specialized training for energy-based device operation. The Canadian Medical Association reports 634 dermatologists nationwide, creating capacity constraints that drive demand for alternative care delivery models including medical spas and home-use devices. Home-use segment growth accelerates through devices like the Juvasonic system that enhance topical treatment absorption without requiring professional supervision, expanding market reach beyond traditional clinical settings.

Geography Analysis

Ontario, Quebec, British Columbia, and Alberta together account for more than 80% of device installations, mirroring the broader life-science cluster distribution in Canada. Toronto’s high patient throughput fosters rapid adoption of minimally invasive “pre-juvenation” protocols among millennials, while Vancouver clinics position natural-finish rejuvenation as a core differentiator. British Columbia also benefits from inbound U.S. patients who combine treatment with leisure travel, taking advantage of the exchange rate differential.

Central provinces host medical-device manufacturers and contract assemblers that support local refurbishment and servicing, shortening downtime for clinic fleets. Prairie provinces and the Atlantic region remain under-penetrated but offer upside as tele-dermatology and mobile aesthetic units extend reach. The Medical Device Single Audit Program raises Canada’s international profile, enabling straightforward mutual-recognition of quality systems and attracting European device makers.

Quebec’s French-language labeling and documentation rules impose localization overheads for newcomers yet reward early entrants with limited competition. Alberta and Saskatchewan show accelerated demand for body-contouring services tied to higher obesity prevalence and disposable income from resource industries. Overall, urban-centric deployment persists, but provincial incentives aimed at rural healthcare infrastructure may open new device placement channels over the forecast horizon.

Regulatory Landscape

Aesthetic devices marketed in Canada are regulated by Health Canada under the Food and Drugs Act and the Medical Devices Regulations (SOR/98-282). Risk-based classification spans Class I to Class IV, with Class II to IV devices requiring a Medical Device Licence supported by safety and effectiveness evidence proportional to risk. Manufacturers also typically need a quality management system certificate to CAN/CSA-ISO 13485 (aligned to ISO 13485) as part of licensing expectations.

For lifecycle compliance, licensees use Health Canada pathways for changes (licence amendments) and align clinical evidence packages to Health Canada guidance on clinical evidence requirements. Dermal fillers are explicitly within premarket licensing requirements under the Medical Devices Regulations (including sections 32 and 34), reflecting heightened scrutiny for cosmetic procedures. On the trade side, many aesthetic systems fall under Chapter 90 of the Customs Tariff. Importers can seek advance tariff rulings through the Canada Border Services Agency (CBSA) and manage related compliance through CBSA digital processes such as the CARM portal, which can influence clearance timelines for imported platforms and consumables.

Competitive Landscape

The Canada aesthetic devices market features a semi-consolidated that is tightening through acquisitions and private-equity roll-ups. Galderma leads injectables with net sales hitting USD 2.2 billion in H1 2024, underpinned by double-digit growth in hyaluronic-acid fillers. In energy-based hardware, Candela, Bausch Health’s Solta Medical arm, and Alma Lasers compete on technological differentiation such as dual-wavelength fractional lasers and proprietary ultrasound modulation.

MedSpa Partners and GraceMed illustrate the consolidation wave, each acquiring leading clinics to forge multi-location platforms with standardized device menus and centralized marketing. Device manufacturers increasingly pursue vertical integration by purchasing or franchising clinic networks, thereby capturing procedure revenue in addition to capital equipment sales. AI add-on modules serve as new competitive moats; vendors bundle software upgrades that refine protocols and lock customers into annual subscription ecosystems.

Compliance expertise remains a market entry hurdle: Health Canada demands ISO 13485 adherence that in some areas exceeds U.S. Food and Drug Administration requirements. Firms able to navigate Class II and III evidence submission processes gain first-mover advantages. Smaller entrants with patented micro-focused technologies (e.g., Cytrellis micro-coring) often license distribution rights to established players to leverage their regulatory infrastructure.

Canada Aesthetic Devices Industry Leaders

Allergan PLC

Bausch & Lomb Incorporated

Cutera Inc.

Cynosure

Lumenis

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities center on shorter portfolio refresh cycles for energy-based platforms that document safety and performance under Health Canada clinical-evidence expectations, alongside provider demand for multi-application systems that consolidate procedure menus into a single capital purchase. Bausch Health's Solta Medical launched the Clear + Brilliant Touch laser in Canada in February 2026, after Health Canada approval granted on May 20, 2025. The rollout highlights Canada as an active commercialization market for newly cleared fractional and multi-wavelength laser solutions.

White space remains in scaling compliant delivery beyond major urban cores, where shortages of trained personnel and fragmented provider ownership can slow standardization. Clinic consolidation in dermatology and medical aesthetics creates openings for manufacturers to support chain-level device fleet standardization, training, and software-enabled protocol management. In parallel, home-use settings form a distinct channel for Class I consumer-grade devices that meet Health Canada's device requirements. For imports and distribution, clearer Chapter 90 tariff classification planning and advance rulings via CBSA can reduce supply disruptions for high-value consoles and accessories, supporting broader geographic placement and higher uptime for installed fleets.

Recent Industry Developments

- June 2026: Allergan Aesthetics announced Health Canada approval of Boey (trenibotulinumtoxinE) for the temporary improvement of frown lines (glabellar lines) in adult patients. The approval expands branded neurotoxin options in Canada and broadens the provider choice set for clinic injectables.

- May 2026: Allergan Aesthetics launched HArmonyCa with Lidocaine in Canada, a dual-action injectable combining hyaluronic acid with calcium hydroxyapatite. The introduction broadens collagen-stimulating offerings for clinics and creates cross-selling leverage alongside existing filler and toxin portfolios.

- April 2024: Cutera announced the North America launch of the xeo+ multi-application platform, available to physicians in Canada. Multi-application workstations support clinic preference for versatile capital equipment that can be deployed across multiple aesthetic indications, shaping replacement and upgrade decisions for installed device fleets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Canada aesthetic devices market is defined as revenues from medical devices used to perform cosmetic or appearance-improving procedures in Canada, across energy-based and non-energy-based categories, and across clinical and home-use settings.

Scope exclusions: We exclude topical consumables, injectable drugs, and pure skincare services that are billed without a device-led procedure.

Segmentation Overview

- By Device Type

- Energy-based Devices

- Laser-based

- Light-based (IPL)

- Radio-frequency-based

- Ultrasound-based

- Cryolipolysis & Plasma-based

- Non-energy-based Devices

- Botulinum Toxin

- Dermal Fillers & Threads

- Chemical Peels

- Microdermabrasion

- Implants

- Mesotherapy & Others

- Energy-based Devices

- By Application

- Skin Resurfacing & Tightening

- Body Contouring & Cellulite Reduction

- Hair Removal

- Tattoo & Pigmentation Removal

- Breast Augmentation

- Acne & Scar Treatment

- Other Applications

- By End User

- Hospitals

- Dermatology & Cosmetic Clinics

- Medical Spas

- Home-use Settings

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a clean list of what gets counted as an aesthetic device sale in Canada, and where demand is coming from across clinics and home-use channels. We used public sources such as Health Canada device licensing and safety notice databases, Statistics Canada demographic and income indicators, and the Canadian Institute for Health Information for broader healthcare delivery context.

To translate activity into market signals, we also reviewed sources such as peer-reviewed dermatology and plastic surgery journals, provincial health and professional association websites, and reputable press coverage on procedure adoption and new device rollouts. Company annual reports, investor presentations, and import-export shipment-level database outputs were used selectively to sanity-check supplier presence, pricing direction, and shipment momentum. These examples are not exhaustive, and many other sources were referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what drives device revenue in Canada and how quickly pricing and utilization change when new systems are adopted. We spoke with a mix of manufacturers and channel participants, along with dermatology and cosmetic clinics, medical spas, and hospital-linked aesthetic centers, so the model reflects how procedures are actually performed and billed.

Feedback from respondents helped confirm average selling price ranges, typical replacement cycles, installed-base utilization, and how much demand shifts between energy-based and non-energy-based procedures over the year.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 19% | |

| Mid tier: 44% | Functional/Unit leaders: 21% | |

| Smaller Players: 22% | Managers: 60% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where procedure demand and capacity signals were reconstructed into an addressable device revenue pool for Canada, and then broken into device-led revenue lines that match how suppliers price and ship. Once the first cut was ready, it was checked with selective bottom-up approximations such as sampled ASP times estimated unit shipments, channel checks on mix, and a light roll-up of visible supplier activity to keep totals realistic.

Key inputs included the share of aesthetic procedures that are device-based, the installed base and replacement cycle for major systems, typical utilization per device in clinics, pricing progression by technology generation, and the split between clinic and home-use device revenue. For forecasting, scenario analysis was used so adoption speed, pricing pressure, and clinic throughput could be flexed in a controlled way, and then aligned to what experts described as the most likely path for the next five years. Where bottom-up signals were thin, gaps were handled by using conservative ranges and then revalidating those ranges through follow-up checks with channel participants.

Data Validation & Update Cycle

Outputs were validated through multiple checks so the final numbers do not rely on one single assumption. We compared results against independent indicators like procedure growth signals, clinic expansion activity, and supplier commentary on Canada performance, and then investigated any variance that looked out of line with pricing or utilization reality.

Before sign-off, the model goes through an analyst review pass that focuses on unit economics, year-over-year movement, and segment mix consistency, and respondents are re-contacted if a key input shifts. Reports are refreshed annually, with interim updates when material events occur that can move demand or pricing, and a final pre-delivery pass is completed so clients receive the most current view.

Mordor Intelligence's Canada Aesthetic Devices Market Size Versus Other Published Estimates

Published market sizes for Canada aesthetic devices often do not match because the counted product set is not always the same, and the base year and currency timing can differ. Differences also show up when one estimate leans more on supplier revenue statements, while another leans more on procedure activity and installed-base utilization.

The main gap comes from whether home-use devices and non-energy-based devices are counted alongside clinic systems, where Mordor Intelligence includes both categories only when revenues tie back to device-led aesthetic procedures performed or enabled within Canada, and not adjacent skincare-only spending.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.61 B (2026) | |

| Market Publisher A | USD 1.50 B (2023) | Uses an older base year and typically applies a smoother growth path, which can understate recent adoption spikes in energy-based systems and replacement-driven demand. |

| Industry Databook B | USD 0.26 B (2024) | Covers energy-based devices only, so it excludes non-energy-based systems and broader device categories that contribute meaningful revenue in Canada. |

The spread in the table is mostly explained by scope choices and timing choices, rather than math errors. When the same device set is counted and the base year is aligned, the estimates tend to move closer, which is why we keep assumptions traceable to procedure signals, utilization, and realistic pricing steps.

Key Questions Answered in the Report

What is the current value of the Canada aesthetic devices market?

The market is valued at USD 1.61 billion in 2026 and is on track to reach USD 2.95 billion by 2031.

Which device category leads sales in Canada?

Energy-based systems lead with 63.78% revenue share, led by ultrasound-guided platforms growing at 15.98% CAGR.

Which application segment is growing fastest?

Body contouring and cellulite reduction treatments are forecast to expand at a 14.45% CAGR through 2031.

How quickly is home-use equipment expanding in Canada?

Consumer home-use devices are posting a 13.34% CAGR as Health Canada’s Class I pathway streamlines approvals.

What role does AI play in the Canadian market?

AI engines embedded in devices personalize energy delivery, reduce operator variability, and are considered a key growth driver.

Are reimbursement policies supportive of aesthetics in Canada?

No, provincial health plans exclude elective aesthetic procedures, so patients typically self-fund treatments.

Page last updated on: