Aerospace And Defense Carbon Brake Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 6.60 Billion |

| Market Size (2030) | USD 8.5 Billion |

| Growth Rate (2025 - 2030) | 5.19% CAGR |

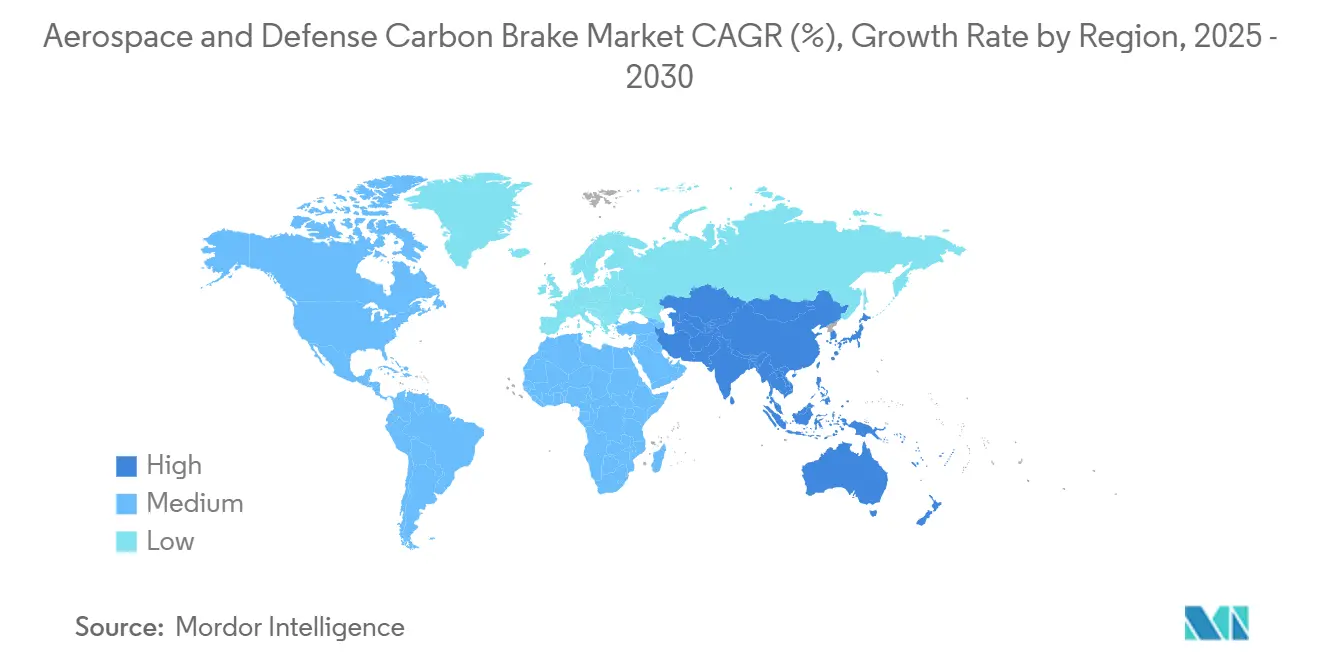

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerospace And Defense Carbon Brake Market Analysis by Mordor Intelligence

The aerospace and defense carbon brake market size reached USD 6.60 billion in 2025 and is forecasted to climb to USD 8.50 billion by 2030, advancing at a 5.19% CAGR. The upward trajectory mirrors the aviation sector’s recovery, the acceleration of commercial narrowbody assembly lines, and multi-year defense modernization programs. Lightweight braking systems are now a default specification on new aircraft because they reduce landing-weight emissions and increase fuel efficiency. OEM backlog levels above 17,000 aircraft have compressed procurement cycles, pushing brake suppliers to expand forging capacity while adopting circular-economy processes that remanufacture worn discs. Although raw material costs for aerospace-grade carbon fiber remain volatile, long-term airline contracts and defense budgets anchor demand visibility.

Key Report Takeaways

- By aircraft class, commercial aviation led with 60.45% revenue share in 2024; spacecraft applications are projected to expand at a 6.21% CAGR through 2030.

- By material type, carbon-carbon composites commanded 70.54% of the aerospace and defense carbon brake market share in 2024, while carbon-ceramic composites are expected to post the fastest growth at 6.65% CAGR.

- By fitment, linefit installations accounted for 54.24% of the aerospace and defense carbon brake market size in 2024, and retrofit demand is advancing at a 5.89% CAGR to 2030.

- By Geography, North America retained a 37.75% share of the aerospace and defense carbon brake market size in 2024, and Asia-Pacific is forecasted to record a 6.25% CAGR over the outlook period.

Global Aerospace And Defense Carbon Brake Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in global commercial aircraft production rates | +1.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Expansion of the global in-service fleet of military transport and combat aircraft | +1.2% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Regulatory focus on reducing landing-weight emissions through lightweight components | +0.9% | Global | Medium term (2-4 years) |

| Rising demand for widebody and long range aircraft in growth markets | +0.7% | Asia-Pacific, Middle East, South America | Medium term (2-4 years) |

| Adoption of advanced lightweight braking systems in next-generation military and space-launch vehicles | +0.4% | North America, Europe | Long term (≥ 4 years) |

| Advancements in carbon brake recycling and remanufacturing technologies | +0.2% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in global commercial aircraft production rates

OEM orderbooks exceed 17,000 units, prompting Boeing and Airbus to raise monthly build targets for single-aisle programs. Each delivered jet requires a complete carbon brake ship-set, and weight savings of up to 40% versus steel alternatives make carbon systems the preferred option for airlines focused on operating-cost reduction. Suppliers are investing in additional autoclaves, densification furnaces, and finishing lines; Collins Aerospace recently committed USD 225 million to enlarge landing-system capacity in the United States and Asia. Accelerated assembly schedules shorten qualification windows, so established vendors with certified designs capture the bulk of incremental demand.

Expansion of global in-service fleet of military transport and combat aircraft

The US allocated nearly USD 10 billion for F-22 upgrades under its Next Generation Air Dominance roadmap, and similar modernization initiatives are underway in Europe and Asia. Honeywell’s Carbenix brakes equip more than 2,400 military airframes, including F-35, F-15, and F-16 variants, underscoring the widening adoption of carbon technology across legacy and new platforms.[1]Honeywell Aerospace, “Carbenix Carbon Brakes,” honeywell.com Longer overhaul intervals relative to commercial cycles support stable aftermarket revenue streams, while foreign military sales (FMS) programs amplify unit growth in allied nations.

Regulatory focus on reducing landing-weight emissions through lightweight components

The Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA) have embedded component mass targets into performance-based certification rules, linking aircraft weight to lifecycle emissions.[2]Federal Aviation Administration, “Performance-based regulations,” faa.gov Airlines, therefore, specify carbon brakes in purchase agreements to improve fuel burn and meet internal decarbonization goals. Evolving standards also reward materials with lower particulate emissions during ground operations, accelerating R&D in carbon-ceramic formulations that dissipate heat more effectively than legacy discs.

Rising demand for widebody and long-range aircraft in growth markets

Asia-Pacific carriers expect double-digit annual traffic growth on intercontinental routes, prompting record orders for B787 and Airbus A350 families. Widebody brake packs are larger and face higher thermal loads during high-energy landings, lifting content per aircraft to the USD 150,000-USD 300,000 range. The B777X completed a 63-day brake-qualification campaign in 2025, highlighting the stringent testing required for next-generation platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of carbon brakes compared to traditional steel alternatives | -1.1% | Global | Short term (≤ 2 years) |

| Supply chain consolidation among carbon disc forging and processing vendors | -0.8% | North America, Europe | Medium term (2-4 years) |

| Lengthy certification and qualification cycles for next-generation brake materials | -0.5% | Global | Long term (≥ 4 years) |

| Raw material cost volatility, especially aerospace grade carbon fiber | -0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High capital cost of carbon brakes compared to traditional steel alternatives

Purchase prices are three to four times higher than those of steel systems, with a narrowbody shipset often exceeding USD 100,000. Operators in cost-sensitive regions sometimes delay upgrades despite lifecycle savings, and lessors frequently standardize on steel to hold residual values.

Supply chain consolidation among carbon disc forging and processing vendors

Safran’s USD 1.8 billion acquisition of Collins Aerospace’s actuation unit exemplifies vertical integration that limits the field to fewer than ten global forgers. Concentrated capacity heightens exposure to any single-facility disruption, and OEMs face reduced bargaining leverage when scheduling ramp-ups.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Class: Commercial aviation underpins current dominance

Commercial programs generated 60.45% of the aerospace and defense carbon brake market size in 2024, equating to USD 3.99 billion, because airlines universally select carbon brakes for new single-aisle and widebody deliveries. The retrofit wave on narrowbody fleets reinforces demand, while the spacecraft segment shows the fastest CAGR at 6.21% as launch frequencies climb. Carbon brake durability enables 2-3 times more extended operating periods between overhauls than steel, reducing life-cycle maintenance costs for high-cycle passenger jets.

Commercial jet output will add more than 44,000 aircraft by 2043, sustaining a resilient replacement pipeline. Military fleets, meanwhile, adopt carbon brakes to extend payload range; the F-35, F-15EX, and A400M each integrate carbon-carbon discs as standard equipment. Growth across general aviation, particularly super-mid business jets, complements volume because operators seek maximum range without sacrificing cabin load.

By Material Type: Carbon-carbon remains dominant, carbon-ceramic accelerates

Carbon-carbon composites captured 70.54% of the aerospace and defense carbon brake market share in 2024, equaling USD 4.66 billion of revenue. The legacy material offers proven thermal performance at high kinetic energy stops. However, carbon-ceramic composites are forecast to expand at a 6.65% CAGR, outpacing the overall aerospace and defense carbon brake market, because their fabrication cycle is shorter and their heat‐dissipation rate diminishes runway-overrun risk during heavy-weight landings.[3]SGL Carbon, “Carbon solutions for aerospace,” sglcarbon.com

The material shift also stems from supply chain resilience; carbon-ceramic discs require less virgin fiber, lowering exposure to precursor price spikes. Recycled fiber demonstration programs have passed preliminary dynamometer tests, pointing to broader adoption once certification hurdles are cleared.

By Fitment: Linefit maintains lead while retrofit demand climbs

Linefit installations represented 54.24% of 2024 revenue, roughly USD 3.58 billion, because OEMs specify carbon brakes for every new delivery, embedding them into maintenance planning from day one. Retrofit activity, 45.76% of revenue, is growing faster at 5.89% CAGR as carriers modernize in-service fleets to meet carbon-offset cost pressures and fuel-burn targets.

Safran’s LandingLife program refurbishes and recycles worn discs, reducing retrofit downtime and supporting airline sustainability reporting. MRO providers in Malaysia and the United Arab Emirates have opened carbon brake overhaul lines to handle regional retrofit demand, lowering logistics costs for airlines outside North America and Europe.

Geography Analysis

North America held 37.75% of the aerospace and defense carbon brake market in 2024, translating to USD 2.49 billion, buoyed by robust defense budgets, high passenger volumes, and a dense maintenance, repair, and overhaul network. Long-term F-35 and KC-46 procurement ensures a stable military backlog, while domestic air-travel demand has already surpassed pre-pandemic levels.

Europe maintains a sizable share supported by Airbus output and strict environmental regulations, accelerating lightweight-component adoption. The European Union’s Fit-for-55 package and corresponding EASA guidance encourage airlines to retrofit older narrow-body fleets with carbon brakes to meet emissions-trading obligations.

Asia-Pacific is the fastest-growing region, posting a 6.25% CAGR as China, India, and Southeast Asian carriers expand fleets to serve burgeoning middle-class traffic. Regional MRO expansion in Malaysia and Singapore enables local disc refurbishment, improving turnaround time for operators. Similar growth dynamics exist in the Middle East, propelled by widebody orders linked to Saudi Vision 2030 and other national diversification programs. South America and Africa are smaller but offer upside through emerging low-cost carriers transitioning from steel to carbon brakes as fuel prices rise.

Competitive Landscape

The aerospace and defense carbon brake industry features moderate concentration. Safran, Collins Aerospace, Honeywell International Inc., and Meggitt PLC held over 50% of 2024 revenue through long-term supply contracts with Boeing, Airbus, and leading defense primes. Safran alone equips most active commercial aircraft with carbon brakes and operates 20 MRO shops worldwide.[4]Safran Group, “Landing systems global footprint,” safran-group.com

Collins Aerospace recently committed USD 225 million to enlarge US and Asian forging sites, indicating that incumbents continue to invest in captive production to guard against supply interruptions. Honeywell focuses on military niches, leveraging its Carbenix brand across fighters, transports, and rotorcraft. Emerging competitors target niche programs such as urban-air-mobility vehicles, yet certification costs and forging-press capital requirements remain formidable entry barriers.

Vertical integration is intensifying. Safran’s acquisition of an actuation business extends its control over adjacent landing-gear components and creates cross-selling opportunities. Digital analytics platforms are another battleground; predictive-maintenance algorithms help airlines optimize disc replacement intervals, locking customers into proprietary service ecosystems.

Aerospace And Defense Carbon Brake Industry Leaders

Honeywell International Inc.

Crane Aerospace & Electronics (Crane Co.)

Meggitt Limited (Parker-Hannifin Corporation)

Collins Aerospace (RTX Corporation)

Safran SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Safran's EUR 450 million (USD 528.57 million) investment in a new 30,000 square meter aircraft carbon brake facility in France will begin operations in 2030. The expansion will increase production capacity by 25% by 2037, strengthening the company's aerospace and defense carbon brake market position.

- April 2025: Spirit Airlines and Safran Landing Systems renewed their agreement for wheel and carbon brake supply and maintenance services for Spirit's A320 fleet, covering operational A320ceo and A320neo aircraft and future deliveries.

Global Aerospace And Defense Carbon Brake Market Report Scope

| Commercial Aviation | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aviation | Combat |

| Transport | |

| Special Mission | |

| Military Helicopters | |

| General Aviation | Business Jets |

| Commercial Helicopters | |

| Spacecraft |

| Carbon–Carbon Composite |

| Carbon–Ceramic Composite |

| Linefit |

| Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Aircraft Class | Commercial Aviation | Narrowbody | |

| Widebody | |||

| Regional Jets | |||

| Military Aviation | Combat | ||

| Transport | |||

| Special Mission | |||

| Military Helicopters | |||

| General Aviation | Business Jets | ||

| Commercial Helicopters | |||

| Spacecraft | |||

| By Material Type | Carbon–Carbon Composite | ||

| Carbon–Ceramic Composite | |||

| By Fitment | Linefit | ||

| Retrofit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the aerospace and defense carbon brake market be in 2030?

It is projected to reach USD 8.50 billion, reflecting a 5.19% CAGR from 2025.

Which region offers the fastest growth for carbon brakes?

Asia-Pacific is forecasted to post a 6.25% CAGR through 2030, driven by fleet expansion in China, India, and Southeast Asia.

Why are airlines retrofitting older aircraft with carbon brakes?

Retrofit installations cut landing weight emissions, lower fuel burn, and align fleets with sustainability regulations.

Do carbon-ceramic brakes compete with carbon-carbon systems?

Yes; carbon-ceramic discs offer faster heat dissipation and lower production cost, enabling a 6.65% CAGR that outpaces legacy materials.

What limits new entrants in this sector?

High forging-press capital cost and multi-year certification requirements create substantial barriers to entry.

Page last updated on: