Advanced Distribution Management System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

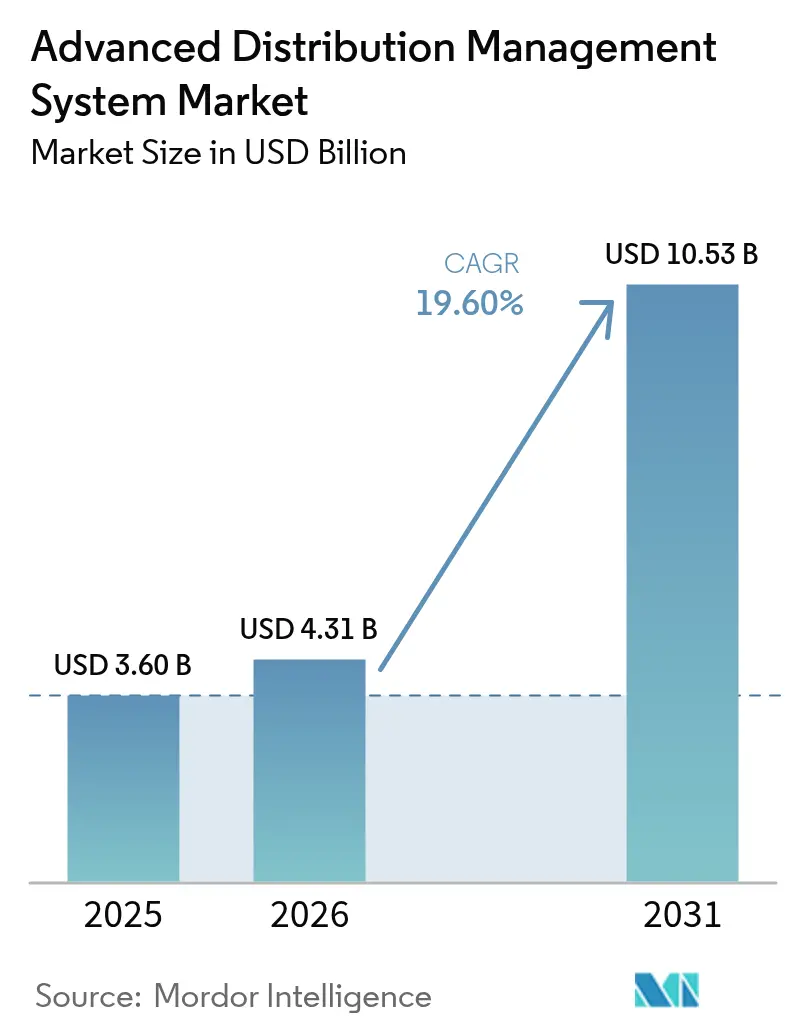

| Market Size (2026) | USD 4.31 Billion |

| Market Size (2031) | USD 10.53 Billion |

| Growth Rate (2026 - 2031) | 19.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Distribution Management System Market Analysis by Mordor Intelligence

The Advanced Distribution Management System market size in 2026 is estimated at USD 4.31 billion, growing from 2025 value of USD 3.60 billion with 2031 projections showing USD 10.53 billion, growing at 19.60% CAGR over 2026-2031. Grid operators are channeling capital into platforms that fuse outage management, distribution automation, and distributed energy resource orchestration in a single control environment. North America remains the revenue anchor due to FERC Order 2222 compliance programs, yet Asia-Pacific exhibits the steepest growth curve as China and India accelerate smart-grid build-outs and utility digitalization. Cloud-native software, artificial intelligence modules, and edge analytics reinforce the business case, while copper shortages, semiconductor lead-time spikes, and a shrinking utility workforce threaten roll-out velocity. Competition is moderate; industrial automation majors still dominate but face pressure from cloud specialists that promise quicker time-to-value.

Key Report Takeaways

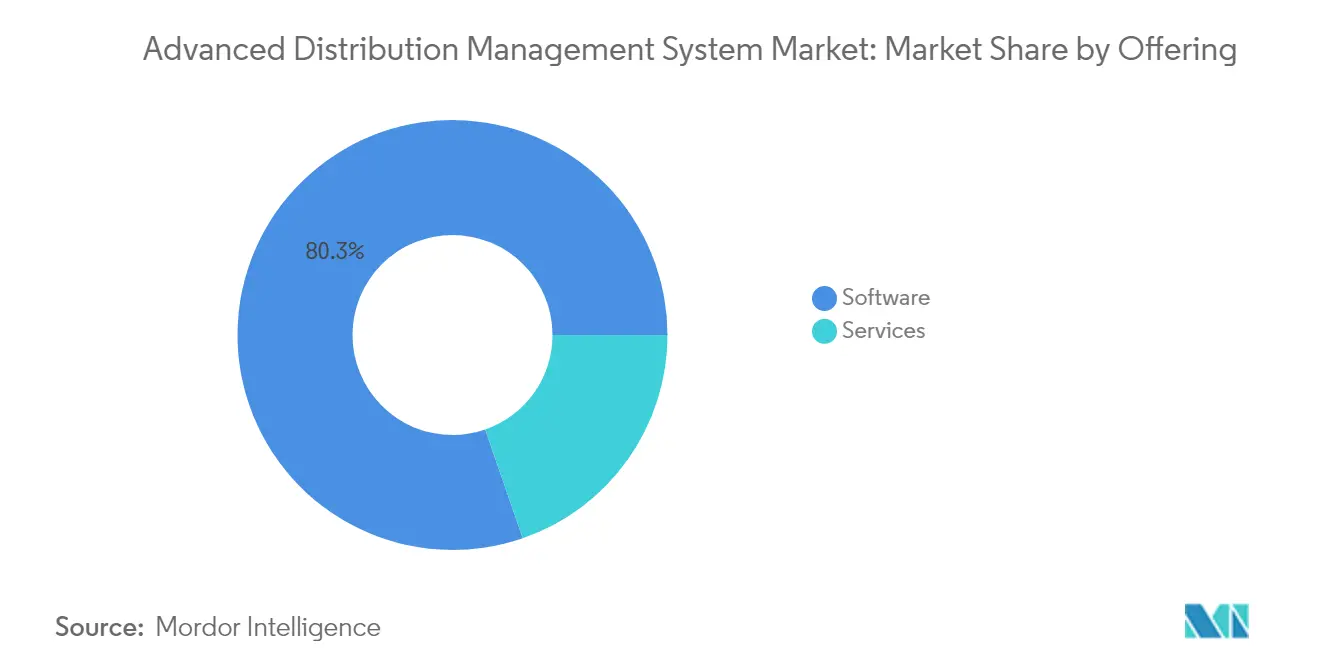

- By offering, software held 80.30% of the Advanced Distribution Management System market share in 2025; the services segment is projected to expand at a 21.40% CAGR through 2031.

- By system type, distribution management systems led with a 35.20% revenue share in 2025, while energy management systems are on track for a 21.05% CAGR to 2031.

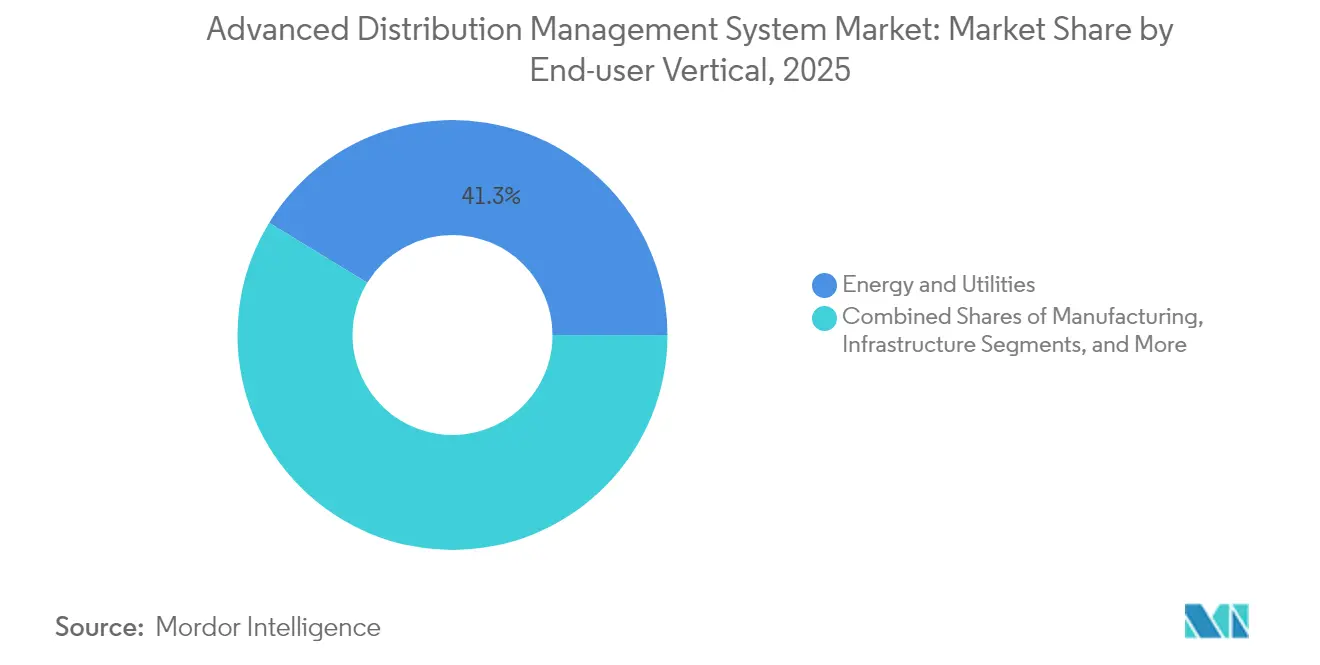

- By end-user vertical, the energy and utilities segment accounted for 41.25% of the Advanced Distribution Management System market size in 2025; IT and telecom is the fastest riser with a 22.60% CAGR to 2031.

- By deployment mode, on-premise installations represented 46.50% of the Advanced Distribution Management System market size in 2025 as cloud deployments race ahead at a 21.35% CAGR.

- By geography, North America controlled 39.30% of the Advanced Distribution Management System market in 2025; Asia-Pacific is projected to expand at a 21.70% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Advanced Distribution Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of smart-grid digitalisation | +7.2% | Global: strongest momentum in North America, Europe, and the Asia Pacific | Medium term (2–4 years) |

| Growing integration of distributed energy resources (DER) | +6.3% | Global, led by Europe and North America | Medium term (2–4 years) |

| Rising energy demand and outage-reduction priorities | +5.4% | Global; critical in emerging markets across Asia, Africa, and Latin America | Short term (≤ 2 years) |

| EV-charging load balancing requirements | +4.5% | Global; highest relevance in urban centers and EV-dense regions | Medium term (2–4 years) |

| Decarbonisation mandates (e.g., FERC 2222) accelerating ADMS roll-outs | +3.6% | North America and Europe; expanding to Asia Pacific | Long term (≥ 4 years) |

| Cloud-native ADMS lowering entry barriers for mid-size utilities | +3.0% | Global; especially impactful for utilities in developing and mid-tier markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rapid adoption of smart-grid digitalization

Utilities are fast-tracking digital control upgrades to replace legacy systems that lack real-time situational awareness. State Grid China earmarked USD 88.7 billion for 2025 distribution automation and advanced metering deployments, cementing the region’s leadership in large-scale smart-grid roll-outs. European network operators must lift annual distribution spending to EUR 67 billion (USD 75.7 billion) to cope with electrification targets, a mandate that is forcing immediate ADMS procurement. Early adopters report a 21% fall in network outage minutes and a 17% cut in restoration time after fully integrated ADMS launches, yielding annual savings near USD 150 million.[1]General Electric Vernova, “ADMS Value Realization Case Studies,” ge.com

Growing integration of distributed energy resources

Bidirectional power flows from rooftop solar, stationary batteries, and vehicle-to-grid assets overwhelm legacy distribution management workflows. India met a record 241 GW peak load in 2024 without deficit by leveraging advanced ADMS algorithms that co-optimize solar, hydro, and battery dispatch. In the United States, FERC Order 2222 forces market participation by aggregated distributed resources, compelling utilities to seek ADMS platforms that deliver synchronized DER visibility and dispatch.

Rising energy demand and outage-reduction priorities

Extreme weather, aging assets, and data-center build-outs amplify grid stress. Data-center electricity use may jump from 130 TWh in 2023 to 307 TWh by 2030, driving utilities toward AI-enabled failure prediction that can cut unplanned outages by 30-40%.[2]American Council for an Energy-Efficient Economy, “Data Center Energy Outlook,” aceee.org Regulators are tightening reliability penalties, turning predictive maintenance from an option into an operational prerequisite.

EV-charging load balancing requirements

Concentrated EV fast-charging clusters can overload distribution feeders unless actively managed. California alone could need 25 GW of feeder capacity upgrades by 2045 if unmanaged charging persists. ADMS algorithms that coordinate charging with renewable generation have demonstrated 16–34% peak-load shaving across scenarios with 1.5–5 million vehicles.[3]MDPI, “Coordinated EV Charging Strategies,” mdpi.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capex and integration complexity | -3.4% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Cyber-security and data-privacy concerns | -2.8% | Global, strictest in North America and EU | Medium term (2–4 years) |

| Shortage of ADMS-skilled workforce | -2.1% | Global, critical in mature markets | Long term (≥ 4 years) |

| Proprietary protocols limiting interoperability | -1.9% | Global, legacy system constraints | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High initial capex and integration complexity

Full-scale ADMS deployments can cost USD 5–50 million, excluding hardware. Long production lead times on transformers have stretched to 18–24 months, magnifying capital-allocation risk.[4]Siemens Energy, “Transformer Capacity Expansion Statement,” siemens-energy.com Interfaces to legacy SCADA and billing platforms often double project timelines, challenging smaller utilities that look for Software-as-a-Service options.

Cyber-security and data-privacy concerns

Digitization widens attack surfaces. Utilities now align with NIST, ISO/IEC 27001, and IEC 62443 frameworks, a compliance load that can delay projects by up to one year. Cloud deployments therefore follow a zero-trust architecture that encrypts data at rest and in transit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain Momentum in a Software-Led Market

Software accounted for 80.30% of the Advanced Distribution Management System market in 2025, affirming utilities’ preference for unified control suites. The services segment is tracking a 21.40% CAGR because long-tail integration, security hardening, and continuous optimization dictate specialist support. Schneider Electric booked EUR 38.2 billion (USD 43.2 billion) in 2024 revenue, with a sizable share tied to grid-software lifecycle services. Consulting engagements typically span 12–18 months and involve interoperability testing across metering, GIS, and outage systems. These immersive projects anchor recurring service contracts that smooth revenue cyclicality.

Rapid cloud adoption widens the addressable pool of mid-tier utilities that cannot fund large data-center refreshes. Managed service agreements now bundle hosting, patching, and real-time cyber monitoring, pushing the Advanced Distribution Management System market size for services toward USD 2.25 billion by 2031.

By System Type: Energy Management Systems Accelerate

Distribution management systems held the top position, accounting for 35.20% of the Advanced Distribution Management System market share in 2025. Energy management systems exhibit a 21.05% CAGR because utilities view holistic optimization across transmission, distribution, and generation as a single economic equation. DER management modules naturally integrate with EMS frameworks, creating an integrated control plane. When utilities incorporate probabilistic renewables forecasting, they can reduce the frequency of ramping conventional generation units by 12%, resulting in lower fuel and operational costs. Front-office market bids also improve because the platform refines locational marginal price forecasts.

Meter data management and advanced metering infrastructure provide granular visibility into consumption, which feeds EMS algorithms. India’s National Smart Grid Mission cleared 22 million additional smart meters in 2024, enlarging the data lake from which AI models learn. This linkage between meter data and EMS decision support underpins future energy-as-a-service propositions.

By End-User Vertical: IT and Telecom Outpaces Core Utility Spend

Utilities commanded 41.25% of 2025 revenue, but hyperscale data-center and telecom operations are the fastest movers at a 22.60% CAGR. Operators are converting backup generators into market-participating microgrids and monetizing flexibility on ancillary-service markets. Sophisticated ADMS deployments enable them to curtail or shift megawatt-scale loads within seconds, an attractive feature in power-price-volatile regions. Manufacturing adoption is driven by process electrification strategies that align production runs with real-time tariffs. Defense agencies are piloting resilient microgrids that island seamlessly during cyber or physical disruptions. Together, these non-utility verticals will exceed 30% of Advanced Distribution Management System industry revenue by 2031.

By Deployment Mode: Cloud and Hybrid Architectures Advance

On-premise remains prevalent at 46.50% of 2025 revenue due to security sensitivities. Yet cloud-based installations are growing at 21.35% annually as vendors certify systems on FedRAMP and comparable schemes, satisfying public-service cyber requirements. Hybrid architectures are emerging, locating latency-critical feeder automation onsite while streaming non-critical data to the cloud for heavy analytics. Connexus Energy completed such a transformation in December 2024, migrating its GIS and analytics workloads to the cloud while retaining real-time SCADA on secure local servers. This approach yields quicker feature updates and reduces on-premise hardware refresh cycles.

Geography Analysis

Asia-Pacific is on track for a 21.70% CAGR through 2031, propelled by State Grid China’s USD 88.7 billion 2025 allocation and strong Indian incentives for smart meters and feeder automation. Governments in the region prioritize distribution efficiency to integrate rooftop solar and a surging electric two-wheeler fleet. Europe faces mandatory annual distribution upgrades of USD 75.7 billion to honor fit-for-55 decarbonization rules. Advanced Distribution Management System market size in Europe will expand steadily as network operators front-load digital overlays before heavier conductor and transformer replacements.

North America, which controlled 39.30% of global revenue in 2025, continues to modernize under FERC Order 2222 and state resilience funding. Severe weather incidents justify real-time outage prediction analytics, and utilities are piloting AI-based network reconfiguration to trim public safety power shutoff events in wildfire-prone regions. Latin America is at an earlier stage, yet benefits from multilateral financing directed at loss reduction. African utilities focus first on revenue protection and feeder automation before rolling out full ADMS suites, but mobile-native cloud solutions could accelerate adoption.

Supply-chain friction is a universal constraint. Copperweld forecasts an 8 million-ton annual copper shortfall by 2034, which could inflate switchgear and conductor costs. Semiconductor shortages add delay to feeder automation hardware. Vendors now hedge by dual-sourcing custom ASICs and deploying flexible microcontroller designs that can accept alternative silicon.

Competitive Landscape

The market remains moderately consolidated. ABB, Siemens, Schneider Electric, and GE combine hardware, software, and services into turnkey propositions, raising customer switching costs. Hitachi Energy has committed USD 6 billion through 2027, including USD 4.5 billion for grid software and USD 1.5 billion for high-voltage products, to sharpen its competitiveness. Siemens Energy will open new U.S. transformer capacity by 2027 to alleviate bottlenecks and secure its hardware-software bundle.

Cloud-only challengers exploit subscription pricing to undercut large upfront licenses. Their differentiator lies in deployment speed and microservices architectures that integrate smoothly with GIS, AMI, and customer portals. Artificial intelligence is the emerging battleground. Vendors embed machine-learning models for outage prediction, topology optimization, and DER aggregation. Partnerships with hyperscale cloud providers accelerate the AI roadmap by tapping into advanced GPU resources and model-training pipelines.

Edge computing is a white-space opportunity. Several startups are embedding containerized ADMS agents in substation gateways to process phasor data locally, ensuring autonomous control if communications drop. Established suppliers respond by adding lightweight runtime versions of their ADMS engines.

Advanced Distribution Management System Industry Leaders

ABB Group

General Electric Company

Siemens AG

Schneider Electric SE

Eaton Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Siemens Energy confirmed plans for new U.S. transformer manufacturing capacity by 2027 to relieve supply-chain limitations and support ADMS roll-outs.

- March 2025: Copperweld highlighted a future 8 million-ton annual copper deficit and promoted bimetallic conductors that cut copper needs 40%.

- February 2025: Connexus Energy completed a cloud-enabled utility network and EcoStruxure ADMS integration, with full ADMS feature activation slated for early 2025.

- January 2025: The U.S. Department of Energy released a Vehicles-to-Grid Integration Assessment outlining a 10-year roadmap for bidirectional charging that hinges on ADMS orchestration.

Global Advanced Distribution Management System Market Report Scope

An advanced distribution management system is a software platform that provides a full suite of optimization and distribution management. It manages, controls, visualizes, optimizes, and automates distribution networks from state-wide to city-wide power distribution networks. It helps field operating personnel monitor and controls the electric distribution system effectively and improves safety, reliability, and quality of service.

The Advanced Distribution Management System Market is segmented by Offering (Software, Service, Consulting, System Integration, Support, and Maintenance), System Type (Distribution Management System (DMS), Automated Meter Reading/Advanced Metering Infrastructure (AMR/AMI), Distributed Energy Resources Management Systems (DERMS), Energy Management Systems (EMS), Customer Information Systems (CIS), Meter Data Management Systems (MDMS)), End-user Verticals (Energy & Utilities, IT and Telecommunications, Manufacturing, Defense and Government, Infrastructure, Transportation & Logistics, Others End-user Verticals), and by Geography ( North America, Europe, Asia Pacific, Middle East, and Africa).

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Software | Distribution Management System (core engine) |

| DER Management Module | |

| Outage Management Module | |

| Services | Consulting |

| System Integration | |

| Support and Maintenance |

| On-premise |

| Cloud |

| Hybrid |

| Distribution Management System (DMS) |

| AMR / AMI |

| DER Management System (DERMS) |

| Energy Management System (EMS) |

| Customer Information System (CIS) |

| Meter Data Management System (MDMS) |

| Energy and Utilities |

| IT and Telecom |

| Manufacturing |

| Defense and Government |

| Infrastructure |

| Transportation and Logistics |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Offering | Software | Distribution Management System (core engine) | |

| DER Management Module | |||

| Outage Management Module | |||

| Services | Consulting | ||

| System Integration | |||

| Support and Maintenance | |||

| By Deployment Mode | On-premise | ||

| Cloud | |||

| Hybrid | |||

| By System Type | Distribution Management System (DMS) | ||

| AMR / AMI | |||

| DER Management System (DERMS) | |||

| Energy Management System (EMS) | |||

| Customer Information System (CIS) | |||

| Meter Data Management System (MDMS) | |||

| By End-user Vertical | Energy and Utilities | ||

| IT and Telecom | |||

| Manufacturing | |||

| Defense and Government | |||

| Infrastructure | |||

| Transportation and Logistics | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the Advanced Distribution Management System market?

The Advanced Distribution Management System market is valued at USD 4.31 billion in 2026 and is projected to reach USD 10.53 billion by 2031 at a 19.60% CAGR.

Which region dominates revenue in 2025?

North America leads with 39.30% of global revenue thanks to regulatory mandates such as FERC Order 2222.

Why are services growing faster than software?

Utilities increasingly depend on integration, cyber-security, and continuous optimization expertise, pushing services toward a 21.40% CAGR through 2031.

How do electric vehicles influence ADMS demand

Coordinated EV charging requires real-time feeder balancing and bidirectional power flow control that only an advanced ADMS platform can deliver, driving new deployments.

What supply-chain risks could slow market growth?

Projected copper deficits, semiconductor scarcity, and a shrinking pool of skilled utility workers threaten project timelines and cost structures.

Who are the leading vendors?

ABB, Siemens, Schneider Electric, GE, and Hitachi Energy currently hold a majority share, though cloud-native entrants are gaining traction with subscription models.

Page last updated on: