Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

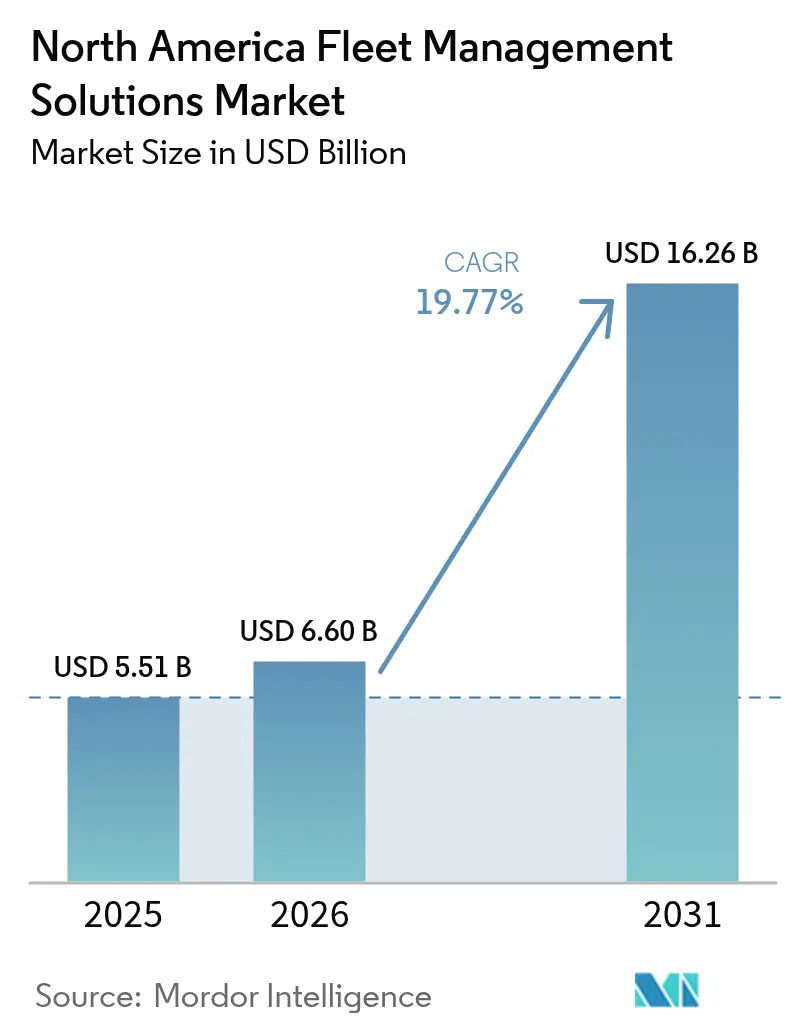

| Base Year Market Size (2025) | USD 5.51 Billion |

| Market Size (2026) | USD 6.6 Billion |

| Market Size (2031) | USD 16.26 Billion |

| Growth Rate (2026 - 2031) | 19.77% CAGR |

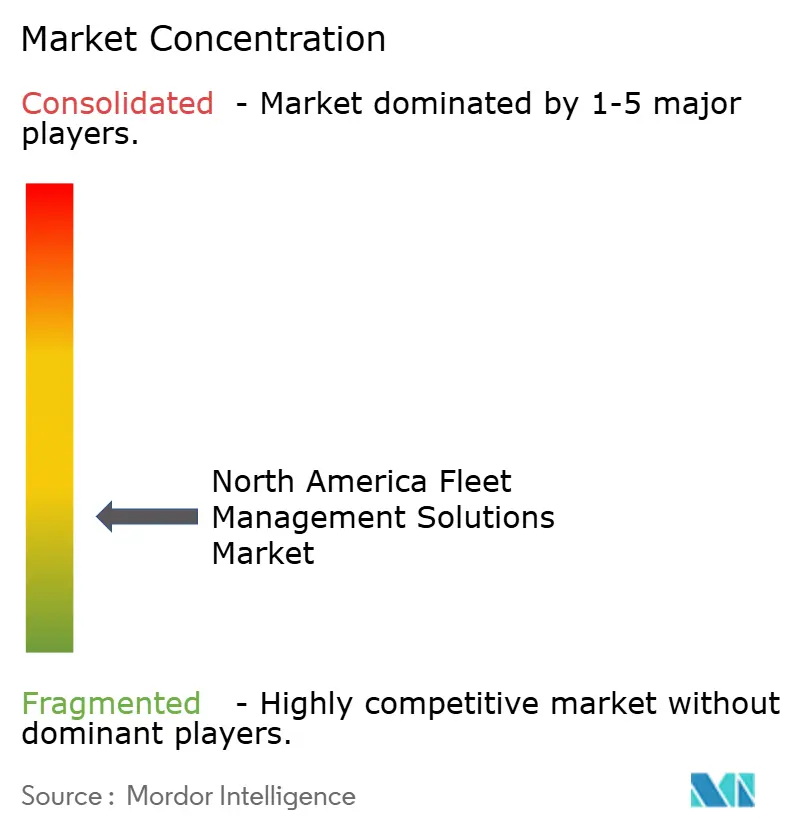

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Fleet Management Solutions Market Analysis by Mordor Intelligence

The North America fleet management solutions market size is expected to grow from USD 5.51 billion in 2025 to USD 6.6 billion in 2026 and is forecast to reach USD 16.26 billion by 2031 at 19.77% CAGR over 2026-2031. Robust federal safety mandates, expanding cloud telematics architectures, and corporate net-zero commitments are converging to accelerate platform adoption. Artificial-intelligence predictive maintenance and video-based driver analytics are shrinking downtime and insurance exposure, while EV-ready telematics help operators coordinate charging and carbon accounting. Nearshoring is lifting cross-border freight volumes, prompting demand for bilingual, scalable software that simplifies United States-Mexico-Canada trade corridor compliance. Heightened cybersecurity threats and evolving data-privacy rules are convincing vendors to hard-wire encryption, role-based access, and zero-trust policies into their roadmaps.[1]Volvo Group, “Predictive Maintenance Collaboration with Penske Truck Leasing,” volvogroup.com

Key Report Takeaways

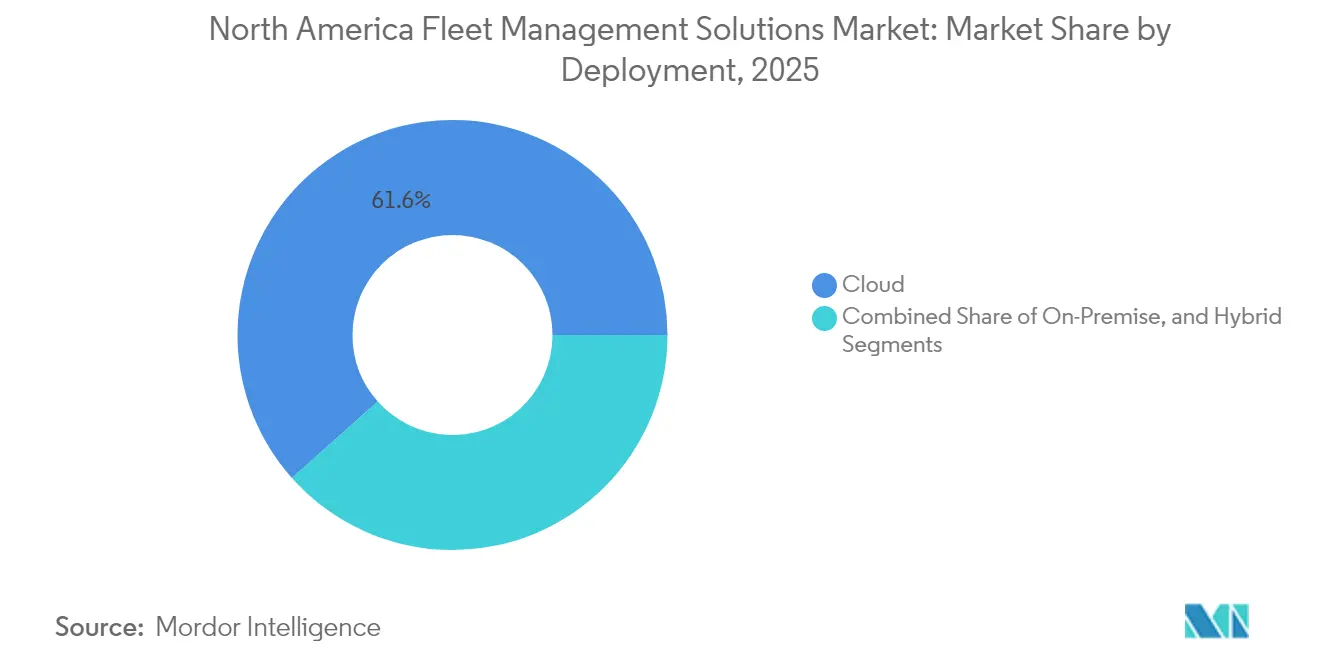

- By deployment, cloud captured 61.58% of the fleet management solutions market share in 2025, while hybrid deployment is projected to expand at 22.04% CAGR through 2031.

- By application, asset management accounted for 28.44% of the fleet management solutions market size in 2025, whereas safety and compliance management is advancing at 23.71% CAGR through 2031.

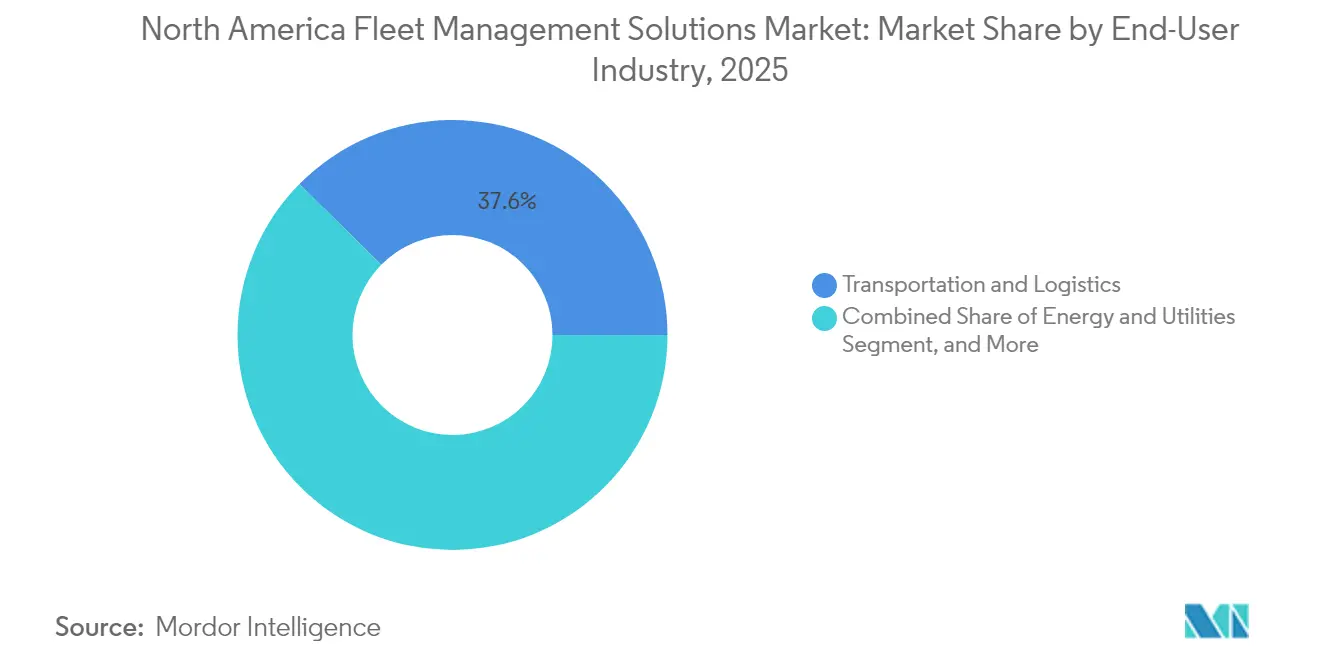

- By end-user industry, transportation and logistics held 37.62% of the fleet management solutions market in 2025; energy and utilities are forecast to grow at 22.35% CAGR to 2031.

- By fleet size, medium fleets represented 44.02% of the fleet management solutions market in 2025, while large fleets are expected to expand at 21.42% CAGR through 2031.

- By geography, the United States commanded 84.92% of the fleet management solutions market in 2025, yet Mexico is projected to register 22.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Fleet Management Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Favorable market regulations coupled with growing emphasis on operational efficiency | +3.20% | North America, with strongest impact in United States and Canada | Medium term (2-4 years) |

| Advent of Green Fleets and corporate net-zero targets | +4.10% | Global, with early adoption in United States, expanding to Mexico | Long term (≥ 4 years) |

| Technological advancements lowering total cost of ownership | +3.80% | North America, with technology leaders in United States and Canada | Short term (≤ 2 years) |

| Growing integration of video-based safety analytics | +2.90% | United States and Canada, emerging in Mexico | Medium term (2-4 years) |

| Uptake of EV-ready telematics platforms | +3.50% | United States and Canada leading, Mexico following | Long term (≥ 4 years) |

| AI-enabled predictive maintenance for mixed-asset fleets | +2.70% | United States and Canada, limited Mexico adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Favourable Market Regulations and Operational Efficiency

Electronic-logging-device and hours-of-service mandates are anchoring telematics adoption across the continental trucking network. As carriers integrate compliance modules, they unlock real-time visibility that improves routing, idle-time reduction, and fuel spend, enabling many fleets to shift cost-of-ownership to the top of the agenda. Consolidated rules under the USMCA are simplifying cross-border reporting, allowing platforms to harmonize safety and environmental data for tri-national operations.[2]U.S. Environmental Protection Agency, “SmartWay Transport Partnership,” epa.gov

Advent of Green Fleets and Net-Zero Targets

Climate commitments are reshaping acquisition strategies, with utilities and consumer brands publishing timelines to electrify light-duty and portioned heavy-duty assets. Federal clean-fleet incentives and state-level zero-emission truck regulations are pushing operators to blend EV scheduling, battery-health diagnostics, and renewable-energy sourcing into a single dashboard. The dual need to track both internal-combustion and electric metrics is a catalyst for mixed-powertrain modules within fleet management solutions market platforms.

Technological Advances Lowering Total Cost of Ownership

Machine-learning engines digest millions of sensors points to forecast part failures, slashing emergency repairs and service-bay queues. Coupled with automated route optimization and real-time driver coaching, the technology delivers quantifiable fuel and maintenance savings that narrow the payback window, particularly for medium and large fleets. Cloud scalability and subscription pricing further level the playing field for smaller operators.

Growing Integration of Video-Based Safety Analytics

Dual-lens and inward-facing cameras now embed edge compute that flags distraction, harsh braking, and tailgating in real time. Insurers in the United States are offering premium discounts for fleets that demonstrate sustained safety-score improvements, converting video telematics from discretionary spend to risk-management staple. The data also feeds driver-engagement programs that can boost retention in a tight labour environment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent data-privacy and driver surveillance concerns | -2.10% | United States and Canada, with varying provincial/state regulations | Short term (≤ 2 years) |

| Limited cellular coverage in rural/long-haul corridors | -1.80% | Rural areas across North America, particularly northern Canada and Mexico | Medium term (2-4 years) |

| Rising cybersecurity threats to connected vehicles | -2.40% | North America, with particular vulnerability in cross-border operations | Short term (≤ 2 years) |

| Fragmented regulatory landscape for cross-border fleets | -1.60% | United States-Mexico-Canada trade corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Data-Privacy and Driver Surveillance Concerns

Labor groups and provincial-level privacy statutes limit the capture and retention of driver-behaviour footage. Fleets deploying inward-facing cameras must negotiate union agreements outlining purpose, storage duration, and access rights. Vendors are countering with privacy-by-design architectures that segment personally identifiable information and provide anonymized scoreboards.

Rising Cybersecurity Threats to Connected Vehicles

Telematics gateways, OTA firmware, and third-party plug-ins enlarge the attack surface. Ransomware campaigns targeting fleet back-office servers and spoofed GPS data incidents have forced operators to add intrusion-detection systems, secure boot processes, and multi-factor authentication across the stack. Collaborative security audits with hardware suppliers are becoming table stakes during RFP cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Dominance Drives Scalability

Cloud services held the largest stake, delivering 61.58% fleet management solutions market share in 2025 as operators favoured subscription economics and instant feature updates. Hybrid architectures are forecast to post a leading 22.04% CAGR to 2031, combining edge processing for latency-sensitive safety alerts with cloud analytics for strategic planning. On-premises instances persist where data-sovereignty or intermittent connectivity requires local hosting, but the relative slice is expected to erode as cloud resilience and encryption standards mature.

Large shippers increasingly pilot hybrid nodes at depots to process high-bandwidth sensor feeds while synchronizing with regional data lakes overnight. Government agencies managing emergency vehicles still lean on private clouds vetted under FedRAMP or equivalent frameworks. The expansion of satellite-backhaul options is also easing cloud adoption along long-haul corridors previously deemed connectivity deserts.

By Application: Safety Solutions Accelerate Beyond Asset Tracking

While asset management retained 28.44% of the fleet management solutions market size in 2025, safety and compliance modules are charting the fastest expansion at 23.71% CAGR as dash-cam AI and electronic driver-vehicle-inspection-report automation gain traction. Driver coaching dashboards and risk-scoring matrices integrate seamlessly with insurer portals, reducing claims cycles.

Operational planners are layering congestion analytics and weather overlays atop core location data to carve fuel consumption by single-digit percentages. Sustainability reporting and battery-state-of-charge orchestration are emerging as premium add-ons, allowing vendors to upsell existing clients. Cross-suite dashboards improve data coherence, minimizing swivel-chair workflow fatigue for dispatchers.

By End-User Industry: Utilities Lead Growth Transformation

Transportation and logistics accounted for 37.62% of the fleet management solutions market in 2025, yet utilities are poised for the sharpest climb at 22.35% CAGR through 2031 as grid-modernization and vehicle-to-grid pilots multiply. Utilities treat telematics not only as an operational necessity but also as a grid-balancing enabler when electric bucket trucks and service vans act as mobile storage.

Construction, manufacturing, and public-sector fleets follow with specialized needs such as power-take-off monitoring or chain-of-custody documentation for hazardous goods. Industry-specific regulations, from OSHA site-safety logs to FDA cold-chain integrity, continue to influence module selection and customization budgets.

By Fleet Size: Large Fleets Propel Advanced Analytics Uptake

Medium fleets delivered 44.02% revenue during 2025, reflecting balanced complexity and budget flexibility. However, fleets exceeding 251 vehicles will see the quickest acceleration, growing at 21.42% CAGR as economies of scale justify predictive analytics, bespoke integrations, and multi-year SaaS commitments.

Conversely, micro fleets rely on stripped-down apps that bundle GPS, basic DVIR, and automated IFTA reporting under app-store pricing. Tiered licensing now allows upward mobility as operators surpass fleet-size thresholds, ensuring client stickiness for platform vendors.

Geography Analysis

The United States dominated with 84.92% of 2025 spend, anchored by stringent federal mandates and dense commercial-freight corridors that amplify ROI for data-rich solutions. Urban congestion tolling and clean-air-zone expansion are prompting metro fleets to track granular emissions, while California’s Advanced Clean Fleets rule sets a template other state may follow. Federal tax credits for alternative powertrains are channelling grant dollars into integrated EV-telematics rollouts.

Canada’s vast geography, severe winters, and provincial rule variations present unique hurdles, yet its large-distance haulers gain outsized value from predictive maintenance and fuel-tax automation. Provincial zero-emission-vehicle targets and Clean Fuel Regulations are steering utilities and municipal fleets toward dashboards that consolidate GHG reports with maintenance workflows. Satellite-enabled connectivity vendors are partnering with telecoms to plug rural gaps, opening new opportunities for the fleet management solutions market.

Mexico, forecast to advance at 22.56% CAGR, benefits from manufacturing relocation and heightened cross-border freight. Growing demand for Spanish-language interfaces, customs-document digitization, and peso-denominated invoicing has spurred regional ISVs to integrate with established North American platforms. Public-sector safety programs are also encouraging transport concessions to adopt ELD-equivalent devices, extending addressable market depth.

Competitive Landscape

The fleet management solutions market remains moderately fragmented, yet consolidation is accelerating as platform strategists seek scale in subscriber counts and data lakes. Recent transactions such as PowerFleet’s USD 200 million purchase of Fleet Complete and Platform Science’s takeover of Trimble’s telematics arm signal a push toward end-to-end ecosystem control. Acquirers aim to fold hardware, edge compute, and AI frameworks into unified brands that lower client onboarding friction.

Telecommunications carriers leverage existing SIM footprints and 5G rollouts to embed telematics as value-added services, creating cross-sell synergies with IoT business units. Meanwhile, truck OEMs introduce factory-installed connectivity suites, challenging aftermarket hardware vendors. Niche disruptors target untapped pockets EV-charging analytics, construction-equipment telematics, toll-and-toll-violation reconciliation to differentiate against generalist platforms.

Cybersecurity posture has emerged as a critical differentiator; providers with ISO 27001 and ISO 21434 certifications secure contract footholds among government buyers and multinationals. Vertical-specific feature depth, local-language support, and open APIs influence buying decisions as fleets prioritize futureproofing and integration agility.[4]PowerFleet, “Completion of Fleet Complete Acquisition,” powerfleet.com

North America Fleet Management Solutions Industry Leaders

PowerFleet, Inc.

Geotab, Inc.

Verizon Communications Inc. (Connect)

Omnitracs, LLC

GPS Trackit, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Fleetio secured USD 450 million in funding and agreed to acquire Auto Integrate, adding 110,000 repair-shop connections to its maintenance-authorization network.

- February 2025: Platform Science completed its purchase of Trimble’s transportation-telematics unit, merging hardware and software portfolios for 1.3 million connected assets.

- February 2025: Amerit Fleet Solutions acquired Vector Fleet Management to expand emergency-vehicle maintenance and onsite parts programs.

- January 2025: Konexial introduced construction-materials trucking packages bundling FMCSA-compliant ELD, AI dash cams, and commercial routing.

North America Fleet Management Solutions Market Report Scope

Fleet management solution is a system of technologies and procedures that allows companies to organize and coordinate work vehicles to reduce costs, improve efficiency, and ensure compliance with government regulations across an entire fleet operation. It includes a range of functions, such as vehicle financing, vehicle maintenance, vehicle telematics, such as tracking and diagnostics, driver management, speed management, fuel management, and health and safety management.

By Deployment

| On-Premise |

| Cloud |

| Hybrid |

By Application

| Asset Management |

| Information Management |

| Driver Management |

| Safety and Compliance Management |

| Risk Management |

| Operations Management |

| Other Applications |

By End-User Industry

| Transportation and Logistics |

| Energy and Utilities |

| Construction |

| Manufacturing |

| Other End-User Industries |

By Fleet Size

| Small Fleets (1-50 vehicles) |

| Medium Fleets (51-250 vehicles) |

| Large Fleets (251+ vehicles) |

By Country

| United States |

| Canada |

| Mexico |

| By Deployment | On-Premise |

| Cloud | |

| Hybrid | |

| By Application | Asset Management |

| Information Management | |

| Driver Management | |

| Safety and Compliance Management | |

| Risk Management | |

| Operations Management | |

| Other Applications | |

| By End-User Industry | Transportation and Logistics |

| Energy and Utilities | |

| Construction | |

| Manufacturing | |

| Other End-User Industries | |

| By Fleet Size | Small Fleets (1-50 vehicles) |

| Medium Fleets (51-250 vehicles) | |

| Large Fleets (251+ vehicles) | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How fast is the North America fleet management solutions market expected to grow?

The market is projected to post a 19.77% CAGR between 2026 and 2031, rising from USD 6.6 billion to USD 16.26 billion.

Which deployment model is most popular with North American fleets?

Cloud platforms dominate with 61.58% share, favored for scalability and automatic feature updates.

Which fleet application segment will grow the quickest?

Safety and compliance management solutions are forecast to expand at 23.71% CAGR as AI-based video analytics gain traction.

What end-user industry shows the strongest growth outlook?

Energy and utilities fleets are projected to record a 22.35% CAGR through 2031, driven by electrification and grid-modernization projects.

Why are large fleets adopting telematics faster than small fleets?

Fleets with more than 251 vehicles unlock economies of scale that justify predictive analytics, bespoke integrations, and multi-year SaaS contracts.

What is the biggest operational concern limiting broader adoption?

Rising cybersecurity threats to connected vehicles are prompting fleets to demand hardened, zero-trust telematics architectures before rollout.

Page last updated on: