Adhesive Dispensing System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 39.37 Billion |

| Market Size (2031) | USD 49.89 Billion |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

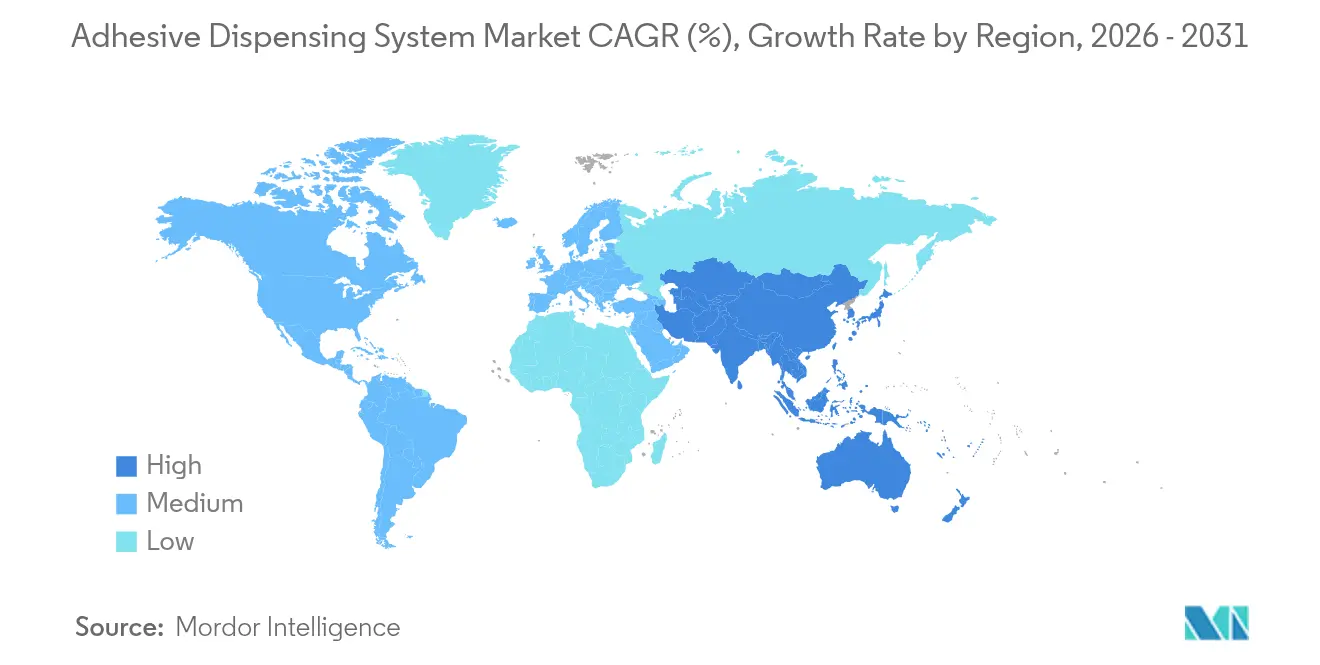

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Adhesive Dispensing System Market Analysis by Mordor Intelligence

The adhesive dispensing system market size is expected to grow from USD 37.55 billion in 2025 to USD 39.37 billion in 2026 and is forecast to reach USD 49.89 billion by 2031 at 4.85% CAGR over 2026-2031. This growth profile underscores the transition from manual adhesive application toward precision-controlled, automated platforms demanded by electric-vehicle (EV) battery assembly, advanced electronics, and Industry 4.0 rollouts. Demand for micrometer-level accuracy in EV battery packs, nanoliter deposits in semiconductor packaging, and hot-melt tank-free economics in e-commerce packaging all reinforce the positive outlook for the adhesive dispensing system market. Competitive intensity centers on piezo-jet and servo-electric innovation, while sustainability regulations in the European Union accelerate uptake of refillable cartridges and debonding-on-demand chemistries that reshape the adhesive dispensing system market europarl.europa.eu.

Key Report Takeaways

- By product type, volumetric systems accounted for 56.02% of the adhesive dispensing system market size in 2025; jetting and micro-dispensing platforms are forecast to expand at 8.21% CAGR through 2031.

- By end-use industry, automotive and e-mobility held 32.05% revenue share of the adhesive dispensing system market in 2025, while medical devices are expected to register the fastest 7.46% CAGR to 2031.

- By technology, pneumatic architectures held 39.85% share of the adhesive dispensing system market size in 2025, whereas piezo-jet solutions are projected to grow at 9.08% CAGR

- By automation level, semi-automatic platforms dominated with 45.10% share in 2025, yet fully robotic in-line systems are set to post the highest 8.32% CAGR to 2031

- By region, Asia-Pacific led with 39.12% adhesive dispensing system market share in 2025, and the region is projected to grow at 7.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Adhesive Dispensing System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV battery-pack growth demands micro-metering accuracy | +1.2% | Asia-Pacific core, spill-over to North America and EU | Medium term (2-4 years) |

| Electronics miniaturisation pushes jet-dispense adoption | +0.9% | Global, with concentration in Asia-Pacific | Short term (≤ 2 years) |

| Packaging shift to hot-melt tank-free applicators | +0.7% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Factory-floor automation and Industry 4.0 integration | +0.8% | Global | Long term (≥ 4 years) |

| Thermal-interface materials for data-centres and ADAS | +0.6% | North America and EU core, Asia-Pacific growth | Medium term (2-4 years) |

| EU EPR rules drive refillable cartridge innovations | +0.4% | EU primary, North America secondary | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV Battery-Pack Growth Demands Micro-Metering Accuracy

Gigafactory build-out places stringent accuracy targets on thermal-interface material placement, with many lines now demanding bond-line thickness below 25 µm to manage heat and improve vehicle range.[1]Jeremy Smith, “Thermal Paste Surface Application in Power Electronics Manufacturing,” Magna-Power, magna-power.comv Progressive cavity pumps and piezo-jet modules deliver shot-to-shot repeatability within ±0.5% tolerance, enabling weight savings of up to 15% when structural adhesives replace mechanical fasteners. EV leaders in Asia-Pacific deploy plasma-based surface activation that boosts adhesion without chemical primers, further elevating demand for precise dispensers . Graco’s dedicated EV battery platforms underscore how the adhesive dispensing system market pivots around cell-to-carrier bonding and fireproof coatings . As a result, battery OEMs view best-in-class dispensers as core yield enablers, not auxiliary tooling, sustaining long-term investment momentum for the adhesive dispensing system market.

Electronics Miniaturization Pushes Jet-Dispense Adoption

Next-generation wearables and implantable sensors now require deposits as tiny as 0.1 nL, levels unreachable with legacy pneumatic needles. [2]Staff Report, “Nordson EFD Wins 2024 Edge Award,” Nordson, nordson.comPiezo-driven jetting systems enable touch-free placement onto features under 25 µm wide while operating at cycle rates exceeding 1,000 Hz. Ball Grid Array and Chip-on-Board architectures boost demand for dispensers that manage rising thermal profiles without sacrificing speed Nordson’s PICO Nexus, featuring Industrial Ethernet and web-based dashboards, showcases how the adhesive dispensing system market integrates IIoT for remote programming and in-process analytics . ViscoTec’s endless piston principle addresses bubble-free delivery for optical bonding, proving essential for AR/VR displays.

Packaging Shift to Hot-Melt Tank-Free Applicators

Brand owners replacing heated tanks with tank-free hot-melt applicators enjoy up to 30% energy savings and 50% adhesive reduction, slashing total cost of ownership.[3]Press Office, “Graco Hot Melt Packaging Solutions,” Universal Adhesive Systems, universal-adhesives.co.uk First-In-First-Out melting eliminates charring and nozzle occlusion, cutting unplanned downtime in e-commerce fulfillment. Ten-minute warm-up times boost line agility, letting converters match the seasonality of online retail. Henkel and Packsize now supply bio-based hot melts, reducing greenhouse-gas emissions by 32% across 340 million corrugated boxes annually. Embedded sensors in tank-free platforms provide live viscosity data, enabling predictive maintenance and further anchoring growth for the adhesive dispensing system market.

Factory-Floor Automation and Industry 4.0 Integration

Low-cost cobot packages priced below USD 10,000 drive automation adoption among SMEs previously reliant on manual gluing. Vision-guided control, on-robot dispense software, and closed-loop feedback have shifted focus from simple XY systems to self-correcting cells. Volkswagen’s deployment of modular robots for battery consoles demonstrates how flexible dispensing lines cut re-tooling time when vehicle variants change. Real-time 3D inspection detects bead pattern deviations before cure, enhancing first-pass yield. FANUC’s servo dispensing modules integrate motion and fluid delivery on a single controller, trimming wiring and harmonizing speeds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex of multi-component dispensing cells | -0.8% | Global, more pronounced in emerging markets | Medium term (2-4 years) |

| Complex chemistries raise maintenance/clean-out time | -0.6% | Global | Short term (≤ 2 years) |

| Scarcity of calibration-skilled technicians | -0.5% | North America and EU primary, Asia-Pacific emerging | Long term (≥ 4 years) |

| Recycling hurdles for adhesive-bonded assemblies | -0.3% | EU primary, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex of Multi-Component Dispensing Cells

High-precision two-part metering lines with advanced gear pumps and static mix heads often top USD 100,000 per cell, slowing adoption among small and medium manufacturers. Zenith 2K precision systems exemplify the cost obstacle despite their unrivaled ratio control, and although modular leasing models and pay-per-shot contracts are emerging to spread the financial burden, many buyers defer investment until volumes justify the spend. Capital constraints restrain the adhesive dispensing system market in developing regions where financing terms remain prohibitive.

Complex Chemistries Raise Maintenance/Clean-Out Time

Filled epoxies, thermally conductive gels, and reactive acrylates extend purging cycles to 4 hours if lines must switch material. Temperature-control sleeves from Saint Clair Systems keep viscosity within ±1 °F, but cross-contamination risks persist. Specialty cleaners add chemical cost and hazardous-waste handling. Automated wash-through programs and self-cleaning valves curb downtime yet entail upfront software expenditure, tempering near-term uptake in the adhesive dispensing system market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Volumetric Systems Lead Despite Jetting Innovation

Volumetric platforms held 56.02% of the adhesive dispensing system market in 2025 amid proven reliability across packaging, automotive, and consumer-goods lines. Jetting and micro-dispensing units are forecast to expand at 8.21% CAGR as miniaturization propels demand for non-contact, nanoliter accuracy. The adhesive dispensing system market size for volumetric machines is expected to widen steadily, supported by large installed bases and recurring parts revenue.

The shift toward piezo-jet modules like Nordson’s Vulcan Jet, featuring dual heat zones and modular drive stacks, illustrates how precision challenges catalyze innovation. ITW Dynatec’s Vector platform enables slot, spray, or bead exchange within five minutes, enhancing line agility. Unity gantry cells combine vision guidance with ±0.02 mm repeatability, cementing value in high-performance sectors. Consumables such as nozzles and static mixers represent nearly 25% of lifecycle cost, providing vendors with stable aftermarket revenue streams and reinforcing the adhesive dispensing system market.

By End-Use Industry: Automotive Dominance Challenged by Medical Growth

Automotive and e-mobility retained 32.05% of the adhesive dispensing system market share in 2025 as battery pack designs embraced structural adhesives for weight savings. Medical devices, advancing at 7.46% CAGR, rely on nanoliter deposition for continuous glucose monitors, catheters, and diagnostic cartridges. Electronics, packaging, construction, and aerospace each contribute distinct performance demands, diversifying revenue drivers for the adhesive dispensing system market.

Medical-device OEMs adopt closed-loop dispensers validated under FDA guidelines, reinforcing sales of high-precision robots and in-line vision. Aerospace firms automate sealing and coating for extreme-temperature zones, widening the adhesive dispensing system market size among high-mix, low-volume niches. Packaging converters fuel hot-melt upgrades, while construction players focus on glazing beads and weatherproofing. Collectively, diverse end-user requirements sustain innovation pipelines across the adhesive dispensing system market.

By Technology: Pneumatic Leadership Faces Piezo-Jet Disruption

Pneumatic systems accounted for 39.85% of the adhesive dispensing system market in 2025, benefitting from low cost, simple maintenance, and ubiquitous air lines. Piezo-jet architectures are rising at 9.08% CAGR as contactless, high-speed accuracy trumps older needle-based formats. Electric-servo pumps gain ground in energy-sensitive plants, while progressive cavity designs excel in abrasive pastes.

Graco’s QUANTM electric diaphragm pumps reach 80% energy efficiency and shrink footprint, illustrating how electrification reshapes the adhesive dispensing system market. XTREME TORQUE motors reduce weight to ease robot-arm payload. Digital flow-control suites broadcast viscosity, temperature, and bead width in real time, letting operators adjust recipes via cloud dashboards, a hallmark of advanced adhesive dispensing system market offerings.

By Automation Level: Semi-Automatic Systems Bridge Manual-Robotic Gap

Semi-automatic benches controlled 45.10% of the adhesive dispensing system market in 2025 because they balance affordability with repeatability. Fully robotic in-line cells are projected to grow 8.32% CAGR as labor shortages and 24/7 production targets proliferate.

Start-up kits such as igus RBTX, priced from USD 9,647, democratize robotics for smaller factories, expanding the adhesive dispensing system market to new entrants. Nordson’s GVPlus retrieves CAD data for path generation, reaching 8 µm repeatability while carrying 4.5 kg tools. As programming complexity falls and ROI accelerates, fully automated platforms are expected to overtake semi-automatic cells in revenue beyond 2030, cementing a pivotal transition within the adhesive dispensing system market.

Geography Analysis

Asia-Pacific commanded 39.12% of the adhesive dispensing system market in 2025 and is forecast to compound at 7.98% CAGR to 2031, buoyed by surging EV, smartphone, and consumer-goods manufacturing. China’s giga-scale battery lines from CATL and BYD integrate plasma-assisted bonding and precision dispensers that sustain multi-shift output. India’s production-linked incentives catalyze micro-dispensing adoption in handset assembly, while Japan and South Korea leverage semiconductor know-how to pilot next-generation jetting.

North America ranks second, supported by aerospace, medical device, and advanced automotive programs requiring strict validation. United States FDA mandates for device traceability drive uptake of vision-guided dispensing robots capable of nanoliter deposits. Canada’s composite-rich aerospace sector and Mexico’s vehicle platforms further enlarge regional demand. Broad Industry 4.0 adoption favors connected dispensers broadcasting OEE metrics to enterprise dashboards.

Competitive Landscape

The adhesive dispensing system market remains moderately fragmented, with leading firms maintaining edge through R&D investment and global service coverage. Nordson, Graco, and ITW Dynatec harness wide portfolios and turnkey integration to capture high-value projects. Nordson’s PICO Nexus jetter, crowned Edge Award 2024, highlights the shift toward IIoT-ready hardware. Graco’s EUR 230 million purchase of Corob broadens paint and coatings dosing expertise, underscoring consolidation waves.

Disruptors focus on cost-effective cobots, AI-enabled inspection, and subscription pricing. igus RBTX packages simplify deployment at one-tenth traditional robot cost, while Coherix couples 3D machine vision with adaptive dispense control for zero-defect lines. tesa’s portfolio of 50-plus debonding patents illustrates IP’s strategic importance. Post-sales revenue from consumables, software licenses, and predictive analytics grows in prominence, nudging suppliers to shift from hardware to outcome-based contracts that secure annuity streams within the adhesive dispensing system market.

Adhesive Dispensing System Industry Leaders

Nordson Corporation

Dopag Group

Graco Inc.

ITW Dynatec

Schaefer Technologie GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: G. raco unveiled enhancements to its QUANTM electric diaphragm pump line featuring XTREME TORQUE motors and 80% energy efficiency

- March 2025: Nordson EFD introduced GVPlus and PROX automated dispensing platforms delivering 8 µm repeatability and 4.5 kg payload capacity.

- November 2024: Packsize partnered with Henkel to launch Eco-Pax bio-based hot-melt adhesive for 340 million boxes annually.

- October 2024: Nordson’s PICO Nexus jetting system won the 2024 Edge Award for Automation and IIoT.

Global Adhesive Dispensing System Market Report Scope

Adhesive dispensing systems are specialized tools or machines used to apply adhesives in a controlled and precise manner to surfaces in various manufacturing or assembly processes. They are commonly used in electronics, automotive, packaging, medical device manufacturing, and more. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The adhesive dispensing system market is segmented by type (Two-Part Volumetric Dispensing Dual Cartridge System, Two-Part Volumetric Dispensing Meter Mix, Handheld Hot Melt Applicators and Others), by end-use industry (Packaging, Electronics, Industrial, Automotive, Construction and Other End-Use Industries), and by geography (North America, Europe, Asia Pacific, South America and Middle East and Africa). The market sizing and forecasts are provided in terms of value (USD) for all the above segments.

| Volumetric Dispensing Systems |

| Jetting and Micro-Dispensing Systems |

| Hot Melt Applicators |

| Valve-Based Dispensing Systems |

| Accessories and Consumables |

| Packaging |

| Electronics and Semiconductors |

| Automotive and e-Mobility |

| Industrial Assembly and General Manufacturing |

| Construction |

| Medical Devices |

| Aerospace |

| Other End-Use Industry |

| Pneumatic Systems |

| Electric Servo Systems |

| Piezo-Jet Systems |

| Progressive Cavity Pumps |

| Digital Flow-Control Platforms |

| Bench-top/Manual |

| Semi-Automatic |

| Fully Robotic in-Line Systems |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | Volumetric Dispensing Systems | ||

| Jetting and Micro-Dispensing Systems | |||

| Hot Melt Applicators | |||

| Valve-Based Dispensing Systems | |||

| Accessories and Consumables | |||

| By End-Use Industry | Packaging | ||

| Electronics and Semiconductors | |||

| Automotive and e-Mobility | |||

| Industrial Assembly and General Manufacturing | |||

| Construction | |||

| Medical Devices | |||

| Aerospace | |||

| Other End-Use Industry | |||

| By Technology | Pneumatic Systems | ||

| Electric Servo Systems | |||

| Piezo-Jet Systems | |||

| Progressive Cavity Pumps | |||

| Digital Flow-Control Platforms | |||

| By Automation Level | Bench-top/Manual | ||

| Semi-Automatic | |||

| Fully Robotic in-Line Systems | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the adhesive dispensing system market?

The adhesive dispensing system market is valued at USD 39.37 billion in 2026 and is projected to reach USD 49.89 billion by 2031.

Which region leads the adhesive dispensing system market?

Asia-Pacific leads with 39.12% share in 2025 and is growing at an 7.98% CAGR through 2031, driven by EV and electronics manufacturing expansion.

Which product category is growing fastest within the adhesive dispensing system market?

Jetting and micro-dispensing systems are forecast to post the highest 8.21% CAGR through 2031 due to electronics miniaturization demands.

Why is medical device manufacturing important for market growth?

Medical devices require nanoliter-level precision for items like continuous glucose monitors and catheters, supporting a 7.46% CAGR for the segment.

How do EU sustainability rules affect dispensing equipment design?

Extended Producer Responsibility regulations push adoption of refillable cartridges and debonding-on-demand adhesives, prompting equipment makers to integrate refill tracking and recycling-friendly features.

Page last updated on: