Adeno Associated Virus Vectors Manufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

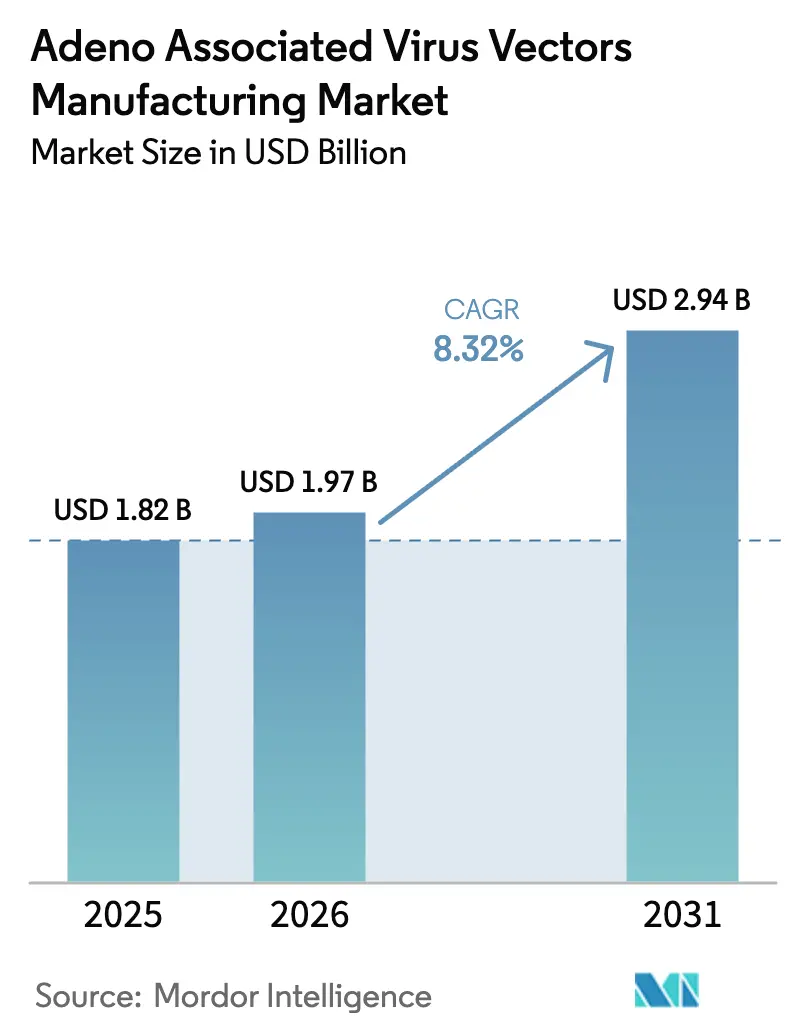

| Market Size (2026) | USD 1.97 Billion |

| Market Size (2031) | USD 2.94 Billion |

| Growth Rate (2026 - 2031) | 8.32% CAGR |

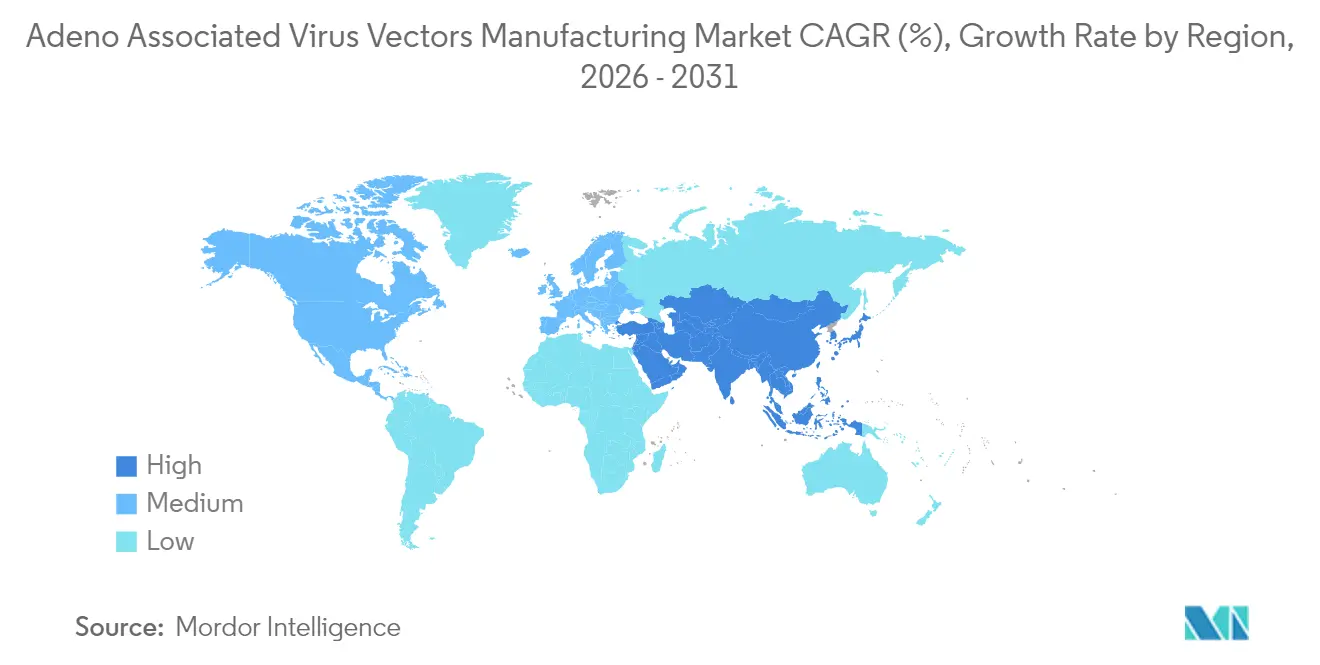

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Adeno Associated Virus Vectors Manufacturing Market Analysis by Mordor Intelligence

The adeno associated virus vectors manufacturing market size is expected to grow from USD 1.82 billion in 2025 to USD 1.97 billion in 2026 and is forecast to reach USD 2.94 billion by 2031 at 8.32% CAGR over 2026-2031. Robust regulatory support, exemplified by the FDA’s target of 10–20 gene-therapy approvals every year, reinforces investor confidence and drives sustained capacity additions across the supply chain. Strategic acquisitions such as Lonza’s USD 1.2 billion purchase of Roche’s Vacaville plant illustrate how contract development and manufacturing organizations secure large-scale assets to keep pace with demand. At the same time, portfolio realignment—seen in Thermo Fisher’s decision to shut viral-vector sites and reduce headcount—removes lower-margin capacity, tightening supply and supporting disciplined pricing. From a technology standpoint, self-complementary vectors, producer cell lines, and ion-exchange purification solutions gain share because they reduce cost per dose and shorten development timelines.

Key Report Takeaways

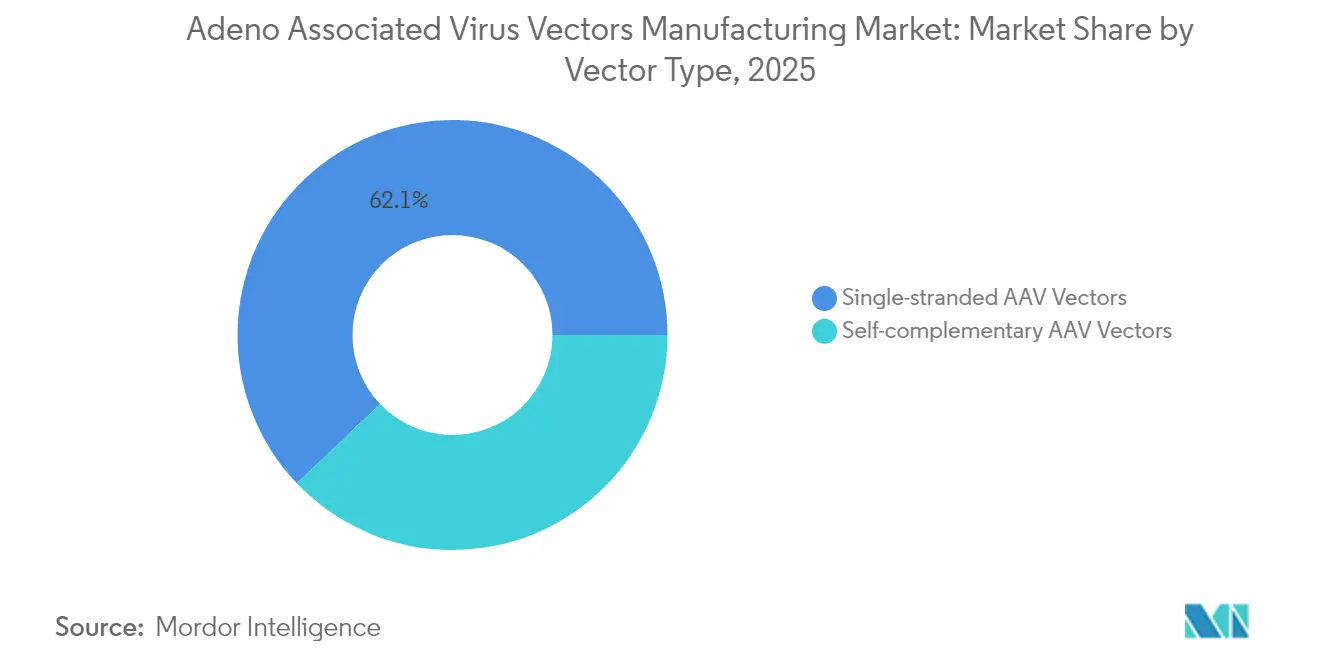

- By vector type, single-stranded formats led with 62.12% revenue share in 2025, while self-complementary variants are advancing at a 8.79% CAGR through 2031.

- By production platform, HEK293 systems held 46.55% of the adeno associated virus vectors manufacturing market share in 2025; producer cell lines record the highest 9.21% CAGR to 2031.

- By purification method, affinity chromatography captured 37.74% share in 2025, whereas ion-exchange chromatography is projected to rise at a 9.62% CAGR through 2031.

- By therapeutic area, ophthalmology commanded 46.12% of 2025 revenue, but neurology is set to expand at a 10.04% CAGR over the forecast horizon.

- By end-user, pharma and biotech companies accounted for 53.15% share in 2025, while CDMOs are growing fastest at 10.45% CAGR thanks to rising outsourcing demand.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Adeno Associated Virus Vectors Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gene-therapy approvals accelerating AAV demand | +2.1% | Global, with North America & EU leading | Medium term (2-4 years) |

| mRNA vaccine manufacturers repurposing capacity for AAV | +1.8% | North America & EU primarily | Short term (≤ 2 years) |

| Falling seroprevalence for next-gen serotypes expands patient pool | +1.5% | Global, with regional variations | Long term (≥ 4 years) |

| On-demand modular bioreactors cut capex needs | +1.2% | Global, with APAC adoption acceleration | Medium term (2-4 years) |

| VC funding shift toward rare-disease platform plays | +0.9% | North America & EU core markets | Short term (≤ 2 years) |

| Government pandemic biopreparedness budgets now include AAV stockpiles | +0.7% | North America primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Gene-therapy approvals accelerating AAV demand

A steady stream of green-lights from the FDA nurtures a virtuous cycle in which every successful launch de-risks the modality for investors and sponsors. The March 2025 clearance of KEBILIDI for AADC deficiency opened the door for direct central-nervous-system administration, a milestone that broadens the treatable disease spectrum. Comparable durability data for hemophilia B gene therapy BEQVEZ further validate long-term factor IX expression and minimize regulatory uncertainty around safety monitoring. Each approval tightens available production slots, encouraging premium pricing for slots at established CDMOs and intensifying consolidation among capacity holders. Demand tailwinds are most visible in ophthalmology, where safety records and immune-privileged anatomy enable rapid path-to-market approvals that now account for 46.78% of revenue. Collectively, these proof points lift investor sentiment, reinforce pipeline breadth, and push the adeno associated virus vectors manufacturing market toward capacity shortfalls by the decade’s end.

mRNA vaccine manufacturers repurposing capacity for AAV

Manufacturers that scaled messenger-RNA operations during the pandemic now face under-utilized infrastructure, prompting a shift into AAV vectors where sterile fill-finish suites and high-purity plasmid lines already exist. Adaptation costs remain modest relative to greenfield builds, allowing rapid entry and buoying near-term supply in Europe and the United States. Process commonalities extend to analytical platforms, creating operational synergies that compress learning curves and accelerate regulatory validation. European operators in particular view repurposing as an avenue to maintain employment, claw back capital expenses, and diversify revenue. This influx of seasoned biologics talent inculcates best-practice quality frameworks that lift baseline standards across the adeno associated virus vectors manufacturing market.

Falling seroprevalence for next-gen serotypes expands patient pool

Population studies indicate that only 30% of UK hemophilia B adults harbor neutralizing antibodies to AAV6, leaving most candidates eligible for therapy, with even lower rates in younger cohorts. Similar trends in Japan show age-stratified prevalence that supports broad adoption in pediatric populations while informing retreatment strategies in older adults. Engineered capsids such as STAC-BBB demonstrate efficient blood-brain-barrier penetration, opening large neurological indications that were previously inaccessible. This diversification lowers dependency on classic serotypes, mitigates immunity barriers, and ultimately enlarges total addressable demand. The broader patient base amplifies manufacturing volumes, inviting new entrants but also challenging upstream plasmid suppliers.

On-demand modular bioreactors cut capex needs

Next-generation single-use bioreactors built on modular skids allow developers to scale from 50 L to 5,000 L with minimal footprint changes, slashing time-to-capacity by months. Takara Bio’s deployment of DynaDrive systems clarifies the economic advantage: lower upfront investment, faster tech-transfer, and smoother scale-out rather than scale-up trajectories. This flexibility suits platform-therapy developers that need variable loads across pipelines, bypassing the risk of stranded assets. Global adoption accelerates as regulators accept disposable technologies that reduce cross-contamination risk and streamline validation. Overall, modular systems democratize access to industrial-scale AAV manufacturing and reinforce the upward trajectory of the adeno associated virus vectors manufacturing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of high-quality plasmid suppliers | -1.4% | Global, with acute impact in APAC | Short term (≤ 2 years) |

| Unresolved immunogenicity & redosing hurdles | -1.1% | Global, with regulatory focus in North America & EU | Long term (≥ 4 years) |

| Chromatography resin supply chain chokepoints | -0.8% | Global, with manufacturing concentration risks | Medium term (2-4 years) |

| EU Annex 1 sterility rules raise cost of goods | -0.6% | EU primarily, with global compliance spillover | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of high-quality plasmid suppliers

AAV production requires multiple plasmids with rigorous supercoiling and endotoxin thresholds that only a handful of providers can consistently meet. These facilities struggle to keep pace, pushing lead times to many months and diverting smaller sponsors to spot-market purchases that inflate cost of goods. The risk becomes most acute in Asia-Pacific, where booming demand collides with limited local plasmid capabilities, creating import dependence and regulatory delays. Vertical integration strategies by well-capitalized CDMOs aim to lock in captive plasmid capacity, but smaller biotech firms remain vulnerable. Unless new plants come online or producer-cell technologies reduce plasmid requirements, plasmid scarcity will continue to put downward pressure on the adeno associated virus vectors manufacturing market growth.

Unresolved immunogenicity and redosing hurdles

Pre-existing neutralizing antibodies and post-treatment T-cell responses constrain the eligible patient pool and complicate retreatment, especially for chronic conditions that may require dose adjustment. Roughly 46.9% of adult males with hemophilia possess antibodies to AAV8, effectively excluding nearly half of the would-be candidates. Immune responses add regulatory burdens, extend follow-up periods, and heighten safety-monitoring costs, collectively slowing market expansion. While engineered stealth capsids and transient immunosuppression regimens show promise, they remain early-stage and unproven at commercial scale. Until durable immune-evasion solutions emerge, repeat-dosing limitations will temper the underlying CAGR of the adeno associated virus vectors manufacturing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vector Type: Self-complementary Gains on Efficiency

The single-stranded format retains a 62.12% revenue hold in 2025, underpinned by legacy clinical data and widespread regulatory familiarity. In contrast, self-complementary constructs post a 8.79% CAGR as developers prize faster onset of expression and the ability to lower viral load per dose, a benefit that directly addresses immune-response risks and yields more efficient use of production slots. Higher transduction efficiency makes self-complementary vectors attractive for enzyme-replacement therapies and certain neurological disorders.

Competition between the two formats is not zero-sum. For ophthalmology, single-stranded vectors remain well-suited to small gene payloads and established dosing regimens. Yet in systemic enzymes, the self-complementary variant is increasingly favored for its rapid biochemical correction and manufacturing economy. This shift gradually transfers revenue toward efficiency-driven products, reinforcing cost-sensitive adopters across the adeno associated virus vectors manufacturing market.

By Production Platform: Producer Cell Lines Challenge HEK293 Dominance

HEK293 cells supplied 46.55% of output in 2025 and continue to anchor many commercial processes due to deep process knowledge, abundant vendor support, and straightforward regulatory dossiers. Producer cell lines, however, show a 9.21% CAGR because they eliminate the triple-transfection step and reduce reliance on scarce plasmid inputs. Their built-in genetic payloads streamline batch workflows, lower variability, and fit continuous-manufacturing aspirations.

The pace of adoption will accelerate as line-development toolkits mature, mitigating historic productivity concerns. Sponsor appetite for consistent, high-yield batches pushes investment into producer-line platforms despite upfront development effort. Over time, these gains compress cost differences and encourage broader integration, supporting scale-up in the adeno associated virus vectors manufacturing market.

By Purification Method: Ion Exchange Disrupts Affinity Dominance

Affinity chromatography captured 37.74% of 2025 throughput because it delivers high selectivity and viral recovery with well-established ligands. Yet ion-exchange systems are advancing at a 9.62% CAGR as resin shortages and cost pressures push operators toward more plentiful chemistries with competitive binding capacity. Process intensification strategies now pair ion-exchange polishing with ultrafiltration to achieve comparable purity at lower consumable cost.

Scalability further tilts the balance because ion-exchange columns can be packed at higher flow rates without sacrificing resolution, shortening campaign times and reducing per-liter operating expenditure. As regulatory comfort grows, ion-exchange columns will occupy a larger slice of the adeno associated virus vectors manufacturing market, providing hedges against affinity-resin supply disruptions.

By Therapeutic Area: Neurology Challenges Ophthalmology Leadership

Ophthalmology leads with 46.12% revenue in 2025 thanks to the eye’s immune-privileged environment and accumulated clinical precedent. Nevertheless, neurology vectors expand at a 10.04% CAGR because engineered capsids like STAC-BBB penetrate the blood-brain barrier, fueling programs in Parkinson’s disease, amyotrophic lateral sclerosis, and broader neurodegeneration. Breakthrough designations shorten timelines, and first-in-brain approvals demonstrate safety for direct CNS administration.

These milestones draw capital into neurological pipelines, progressively narrowing ophthalmology’s dominance. Concurrently, hematology retains steady volume through hemophilia applications, and metabolic disorders inch forward as vector capacities increase. The therapeutic mix diversifies revenue streams and mitigates single-indication concentration risk for the adeno associated virus vectors manufacturing market.

By End-User: CDMOs Capture Outsourcing Wave

Pharma and biotech sponsors held 53.15% of revenue in 2025 by virtue of in-house lines that protect intellectual property and support early launches. Yet CDMOs grow 10.45% annually as the complexity and capital intensity of large-scale viral-vector production shift economics toward specialized partners. Lonza’s Vacaville buyout typifies how capacity aggregation provides one-stop solutions that attract mid-cap biopharma lacking dedicated suites.

Academic centers remain essential in discovery and proof-of-concept work, seeding future commercial demand. Outsourcing momentum will likely continue because CDMOs can amortize continuous-improvement investments across multiple clients, creating a virtuous cycle that enhances their share in the adeno associated virus vectors manufacturing market size.

Geography Analysis

North America commands 41.78% revenue in 2025, reflecting early FDA engagement, robust venture capital flows, and fortified supply lines for raw materials. Federal preparedness budgets now earmark AAV manufacturing for strategic stockpiles, insulating domestic plants from utilization dips and sustaining a premium on qualified capacity. Continued investment commitments—such as Thermo Fisher’s USD 2 billion U.S. program—show industry conviction even as certain sites realign toward higher-margin portfolios.

Europe holds second position through an extensive biologics heritage, harmonized regulatory frameworks, and swift adoption of Annex 1 sterile standards that elevate baseline quality. While the new rules raise operating costs by up to 25%, they also create competitive moats for compliant facilities and drive upgrades that future-proof capacity. CSL Behring’s successful European launch of HEMGENIX underscores the region’s readiness to commercialize complex gene therapies. Collaborative grants—illustrated by the Innovate UK-backed process-intensification project—further energize regional innovation.

Asia-Pacific is the fastest-growing geography as governments channel multibillion-dollar funds into expanding bioprocess infrastructure. China’s 2025 biomanufacturing pledge catalyzes capacity builds, and the region’s lower cost base attracts global partners seeking dual-source strategies. Yet geopolitical uncertainty, including the BIOSECURE Act, could reroute some demand toward Japan, South Korea, and India. These countries are actively developing indigenous CDMO ecosystems, positioning the region to increase its slice of the adeno associated virus vectors manufacturing market over the forecast window.

Competitive Landscape

The market remains moderately concentrated. Scale leaders such as Lonza, Catalent, and Thermo Fisher combine multi-site networks, integrated analytics, and capital resources that reduce per-batch cost and attract late-stage programs. Strategic moves include Lonza’s 330,000-liter Vacaville acquisition and Catalent’s intensified focus on high-margin viral vector suites, both of which consolidate premium capacity slots and deepen supplier lock-in.

Mid-tier CDMOs, including Takara Bio and WuXi Advanced Therapies, differentiate through modular bioreactor deployments and bespoke capsid services. Technology specialists provide analytical advances—exemplified by the U.S. Pharmacopeia’s inclusion of mass photometry in draft AAV standards—which shorten release timelines and improve lot consistency. Upstream suppliers such as Purolite and GenScript race to expand plasmid and resin capacity, addressing critical bottlenecks and enhancing their negotiation leverage.

Emerging disruptors experiment with continuous manufacturing, AI-optimized production scheduling, and next-generation producer cell lines. These innovations promise step-changes in volumetric productivity and cost efficiency, but they also require significant validation to satisfy regulators. Collectively, the interplay among incumbents, specialists, and innovators fosters a dynamic environment that will continue shaping the adeno associated virus vectors manufacturing market.

Adeno Associated Virus Vectors Manufacturing Industry Leaders

Creative Biogene

F. Hoffmann-La Roche Ltd

GenScript

Lonza

WuXi AppTec

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The U.S. Pharmacopeia recognized mass photometry in its draft chapter for AAV reference standards

- April 2025: Thermo Fisher pledged USD 2 billion in U.S. manufacturing and R&D investment over four years to strengthen domestic bioprocess capabilities

Global Adeno Associated Virus Vectors Manufacturing Market Report Scope

As per the scope of the report, adeno-associated virus (AAV) vectors manufacturing market is that produces and purifies AAV vectors for use in gene therapy, vaccine development, and cell therapy.

The adeno-associated virus (AAV) vectors manufacturing market is segmented by scale of operations, therapeutic area, and application. In terms of scale of operations, the market is segmented as clinical and commercial. By therapeutic area, the market is segmented as hematological diseases, infectious diseases, genetic disorders, neurological disorders, and others. By application, the market is segmented as cell and gene therapy, and vaccine. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD) for the above segments.

| Single-stranded AAV Vectors |

| Self-complementary AAV Vectors |

| HEK293 Cell Platform |

| Sf9/Baculovirus System |

| Producer Cell Line (PCL) |

| Other Systems |

| Affinity Chromatography |

| Ion Exchange Chromatography |

| Ultrafiltration / Diafiltration |

| CsCl Gradient Centrifugation |

| Ophthalmology |

| Neurology |

| Hematology |

| Musculoskeletal |

| Metabolic Disorders |

| Oncology |

| Other Therapeutic Areas |

| Pharma & Biotech Companies |

| CDMOs / CMOs |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Vector Type | Single-stranded AAV Vectors | |

| Self-complementary AAV Vectors | ||

| By Production Platform | HEK293 Cell Platform | |

| Sf9/Baculovirus System | ||

| Producer Cell Line (PCL) | ||

| Other Systems | ||

| By Purification Method | Affinity Chromatography | |

| Ion Exchange Chromatography | ||

| Ultrafiltration / Diafiltration | ||

| CsCl Gradient Centrifugation | ||

| By Therapeutic Area | Ophthalmology | |

| Neurology | ||

| Hematology | ||

| Musculoskeletal | ||

| Metabolic Disorders | ||

| Oncology | ||

| Other Therapeutic Areas | ||

| By End-User | Pharma & Biotech Companies | |

| CDMOs / CMOs | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the adeno associated virus vectors manufacturing market?

The adeno associated virus vectors manufacturing market is worth USD 1.97 billion in 2026.

How fast is the market expected to grow?

It is projected to expand at an 8.32% CAGR over 2026-2031, reaching USD 2.94 billion by 2031.

Which vector type holds the largest revenue share?

Single-stranded formats commanded 62.12% of 2025 revenue, reflecting entrenched manufacturing protocols.

Why are producer cell lines gaining attention?

They remove the plasmid-heavy triple-transfection step, improving consistency and posting the fastest 9.21% CAGR among production platforms.

Page last updated on: