Adeno-Associated Virus (AAV) CDMO Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

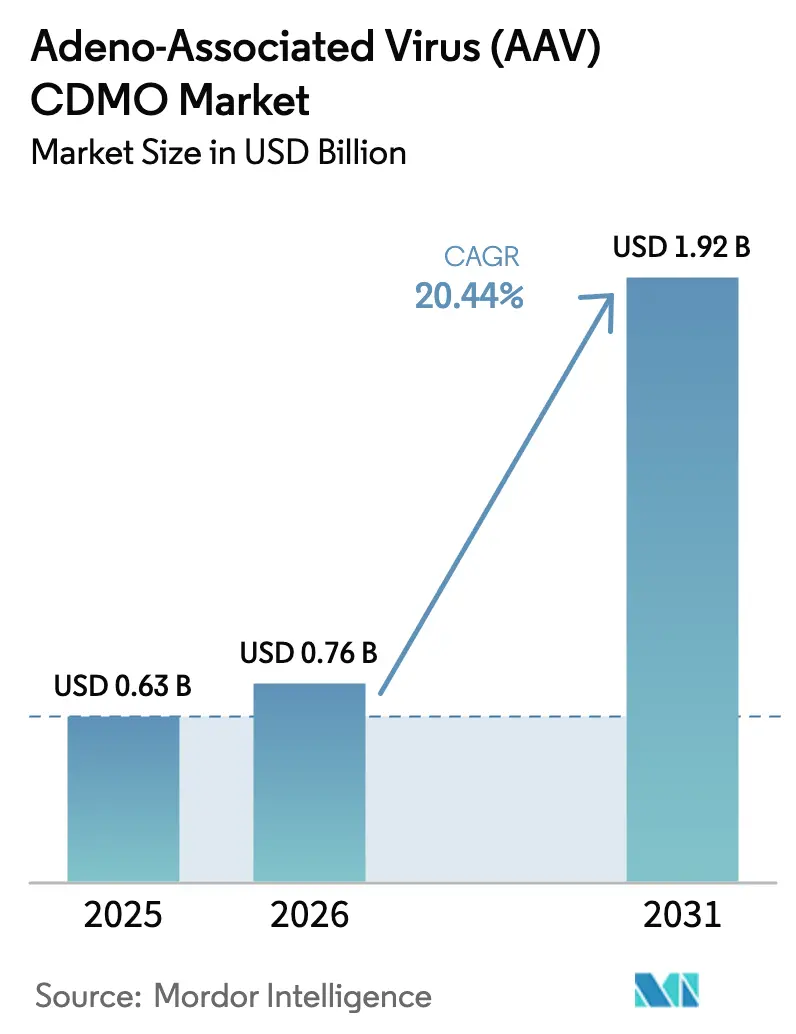

| Market Size (2026) | USD 0.76 Billion |

| Market Size (2031) | USD 1.92 Billion |

| Growth Rate (2026 - 2031) | 20.44% CAGR |

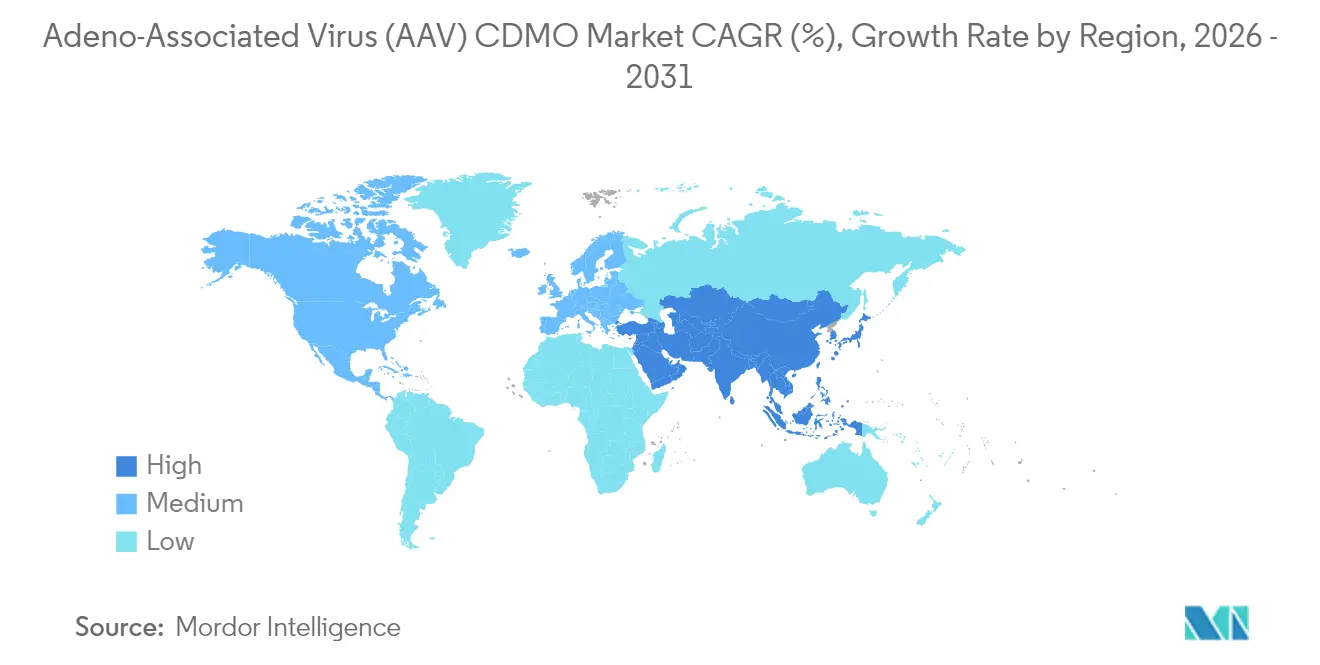

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Adeno-Associated Virus (AAV) CDMO Market Analysis by Mordor Intelligence

The Adeno associated virus (AAV) CDMO market size is expected to grow from USD 0.63 billion in 2025 to USD 0.76 billion in 2026 and is forecast to reach USD 1.92 billion by 2031 at 20.44% CAGR over 2026-2031. Maturing clinical pipelines, streamlined regulatory pathways and sustained capital deployment in next-generation biologics manufacturing support this expansion. North America retains scale advantages thanks to established infrastructure and FDA fast-track programs, while Asia–Pacific outpaces all regions as capacity additions accelerate. Clinical-scale projects dominate current revenues, yet commercial-scale demand is rising as late-stage assets transition to market supply. Service mix is shifting from pure capacity provision toward analytics and regulatory consulting, reflecting growing emphasis on quality-assured, compliance-ready production. Consolidation continues as large-scale CDMOs acquire specialist players to secure vector know-how and diversified customer bases.

Key Report Takeaways

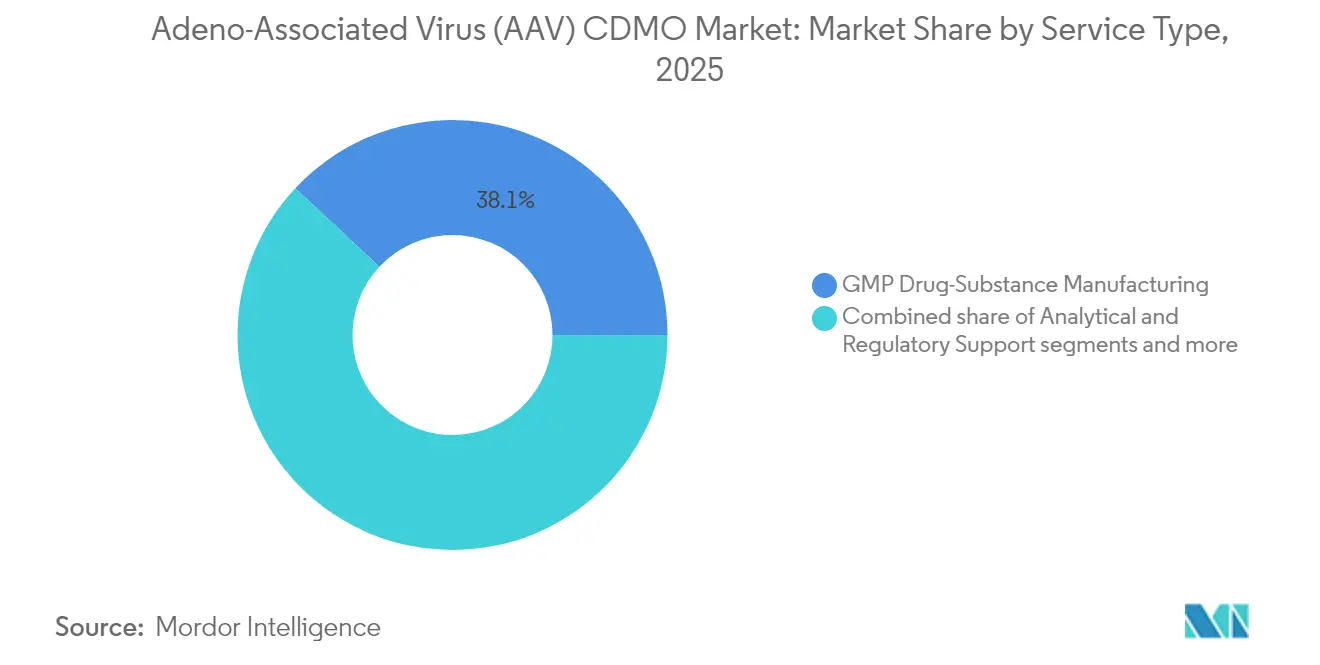

- GMP drug-substance manufacturing led with 38.05% of Adeno associated virus (AAV) CDMO market share in 2025; analytical & regulatory support is projected to advance at 20.89% CAGR through 2031.

- AAV9 captured 40.92% share of the Adeno associated virus (AAV) CDMO market size in 2025, whereas engineered capsids are poised to expand at 21.05% CAGR between 2026-2031.

- Clinical-scale projects accounted for 54.12% of the Adeno associated virus (AAV) CDMO market size in 2025 and commercial scale is forecast to grow at 20.73% CAGR to 2031.

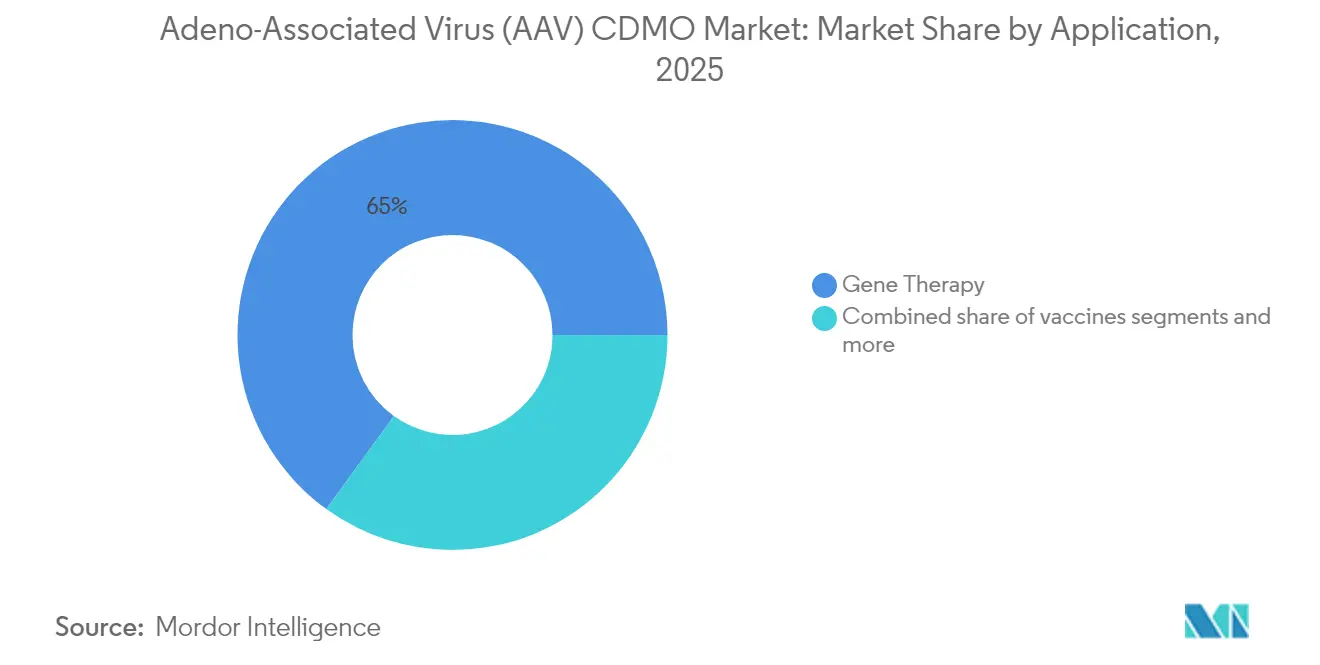

- Gene therapy commanded 65.02% revenue in 2025; vaccine programs represent the fastest-growing application with a 20.52% CAGR expected through 2031.

- Biotech start-ups represented 49.08% demand in 2025; large pharma displays the quickest trajectory at 20.81% CAGR as it internalizes gene therapy platforms.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Adeno-Associated Virus (AAV) CDMO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid clinical-stage pipeline expansion | +4.2% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| FDA/EMA fast-track designations for gene therapies | +3.8% | North America & EU, spillover to APAC | Short term (≤ 2 years) |

| Venture-capital inflow for rare-disease gene therapy | +3.1% | Global, with North America leading | Medium term (2-4 years) |

| Decentralised clean-room pods lowering CAPEX | +2.9% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| AI-guided capsid-engineering raising vector yields | +2.7% | Global, concentrated in innovation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Clinical-Stage Pipeline Expansion

Over 2,100 cell and gene therapy candidates were active worldwide in 2024, a level that keeps specialized CDMO suites near full utilization. The 54.68% clinical-scale revenue share demonstrates how innovators prioritize flexible external capacity. Recent FDA approvals of BEQVEZ and KEBILIDI validated AAV vectors and encouraged additional pipeline financing. Each program needs bespoke process development and analytical files, driving double-digit growth for those services. CDMOs that integrate upstream optimization with regulatory documentation capture repeat business as sponsors progress toward pivotal trials.

FDA/EMA Fast-Track Designations for Gene Therapies

The FDA created a dedicated “super office” inside CBER targeting 10-20 approvals annually by 2025, while EMA continues to refine PRIME and conditional approval tools. Such initiatives shorten time-to-market and shift manufacturing risk earlier in development. Yet 20% of CGT INDs still receive clinical holds within 30 days, underscoring the value of CDMOs with deep regulatory track records. North American projects benefit first, but consistent frameworks are lifting activity in Europe and creating technology-transfer work for APAC sites.

Venture-Capital Inflow for Rare-Disease Gene Therapy

AAVantgarde Bio closed a EUR 61 million (USD 65 million) Series A in 2024, and Sangamo arranged a USD 1.9 billion option deal with Genentech—transactions that kept sector financing above historic averages despite wider biotech retrenchment. Investors now screen CDMOs on scalability and compliance rather than price alone, pushing demand for facilities able to move from 2 L shake-flasks to 2,000 L bioreactors without re-validation. The pattern reinforces the Adeno associated virus (AAV) CDMO market as the operational backbone of emerging therapeutics.

Decentralized Clean-Room Pods Lowering CAPEX

Single-use, modular clean-room pods enable distributed manufacture close to clinical sites, trimming freight costs and mitigating import permits. Adoption began in Europe and the United States but is expanding to Asia as quality standards converge. Pods require advanced automation and inline QC, encouraging CDMOs to bundle digital process control with facility-as-a-service offerings. The approach favors smaller innovators that hold limited capital, reinforcing the current 49.53% biotech share of spending.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited global GMP-grade plasmid supply | -2.8% | Global, acute in Asia-Pacific | Short term (≤ 2 years) |

| Complex royalty stack inflating COGS | -2.1% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Community activism against high-dose AAV trials | -1.9% | North America & EU, spillover to developed markets | Medium term (2-4 years) |

| Carbon-intensity reporting requirements for bioreactors | -1.4% | EU leading, North America following, APAC emerging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Global GMP-Grade Plasmid Supply

End-to-end plasmid lead times of 6-12 months compress project schedules and divert working capital. ProBio’s guaranteed three-month delivery window signals improvement but total output still trails vector demand. Start-ups lacking long-standing vendor ties remain vulnerable to delays, while large CDMOs invest in captive plasmid suites to secure flow. Regulatory bodies move toward harmonized reference standards, yet those measures will not ease supply pressure before 2026.

Complex Royalty Stack Inflating COGS

Royalties on foundational AAV patents can reach 25% of product revenue, eroding margins for price-sensitive indications. Multilayered intellectual-property negotiations prolong commercialization and deter smaller sponsors. CDMOs that have already secured broad freedom-to-operate licenses gain an edge, but unit economics in chronic indications stay challenging until major patents expire or are successfully challenged.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Capacity Dominance Shifts Toward Analytics

GMP drug-substance suites generated 38.05% revenue in 2025, reflecting the capital intensity of upstream production where suspension HEK293 or Sf9 cultures demand specialized bioreactors and purification trains. The Adeno associated virus (AAV) CDMO market relies on these high-throughput operations to meet swiftly scaling batch requirements. Parallel process-development teams customize transfection ratios and downstream chromatography for each serotype, adding value beyond volume. Over the forecast period, analytical & regulatory support expands faster at 20.89% CAGR as regulators tighten expectations around empty/full ratios, potency assays and vector genome integrity. CDMOs responding with next-generation digital PCR, cryo-EM and mass-spectrometry platforms win recurring contracts because sponsors increasingly outsource dossier-ready analytics. Together, the two service clusters account for more than 60% of total spending in the Adeno associated virus (AAV) CDMO market.

In parallel, fill-finish and packaging offer differentiated opportunities. Small clinical batches traditionally used manual isolators, yet commercial-scale approvals demand fully automated aseptic lines compliant with Annex 1 revisions. Providers that integrate container-closure integrity testing and cold-chain engineering retain clients through launch. Quality control and release testing capabilities mature in tandem, ensuring multi-attribute methods are validated early, which in turn reduces regulatory review cycles. These developments sustain double-digit growth even for legacy service lines, reinforcing the Adeno associated virus (AAV) CDMO industry’s evolution from capacity-constrained vendor to full-stack compliance partner.

By Serotype: Natural Leaders and Engineered Contenders

AAV9 held 40.92% revenue in 2025 because of its unique blood-brain barrier crossover that underpins therapies for spinal muscular atrophy and aromatic L-amino acid decarboxylase deficiency. Its manufacturing processes are well characterized, lowering batch-failure risk and attracting risk-averse sponsors. AAV2, AAV5 and AAV8 together serve ophthalmic and hepatotropic use-cases, maintaining a healthy pipeline that ensures volumetric demand for established platforms. However, engineered capsids post the fastest 21.05% CAGR as computational design unlocks novel tissue tropisms and mitigates pre-existing immunity. Complex capsids often require proprietary plasmids and advanced analytical suites, deepening technical barriers and margin potential for specialized CDMOs.

Engineered capsids also modify downstream purification profiles, compelling re-optimization of affinity ligands and gradient conditions. CDMOs with integrated high-throughput screening shorten iteration cycles, thereby capturing premium fees. As more sponsors pivot to bespoke vectors, demand mix gradually shifts. Nevertheless, legacy natural serotypes maintain relevance for diseases where safety data sets are extensive and payers value long-term observational evidence. The resulting dual-track dynamic supports stable revenue for traditional platforms while boosting upside for innovation-driven offerings, a hallmark of the Adeno associated virus (AAV) CDMO market.

By Manufacturing Scale: Clinical Focus Progresses to Commercial Uptake

Clinical projects generated 54.12% revenue in 2025, mirroring a pipeline weighted to Phase I-III trials that require flexible, small-to-medium batches. Sponsors prize CDMOs able to switch vector constructs rapidly, minimizing costly idle time. The Adeno associated virus (AAV) CDMO market size for clinical supply will keep expanding, yet its share declines as approved therapies transition. Commercial manufacturing rises at 20.73% CAGR as payers reimburse curative treatments and inventory cycles lengthen. Scaling from 200 L to 2,000 L reactors involves significant process validation; CDMOs that invested early in large stainless-steel or hybrid facilities such as Samsung Biologics’ 784,000 L campus are positioned to capture those volumes.

Pre-clinical demand persists, especially for platform capsid libraries screened via in vivo selection, yet volume per candidate remains modest. CDMOs often treat this stage as customer acquisition, bundling early work at cost to secure downstream commercial rights. Economies of scale emerge when validated processes translate across multiple programs from the same sponsor, compressing unit costs and making AAV more competitive against rival technologies. Together, these trends form a virtuous cycle that underpins long-term expansion of the Adeno associated virus (AAV) CDMO market.

By Application: Gene Therapy Core with Rising Vaccine Interest

Gene therapy produced 65.02% of 2025 revenue because AAV vectors excel in delivering durable expression for monogenic disorders. Hemophilia, retinal dystrophies and neuromuscular diseases dominate current launches, each commanding price points that sustain manufacturing premiums. Ex-vivo cell therapy uses AAV to modify autologous cells in controlled settings, demanding ultra-clean environments and driving adoption of closed-system isolators. Although this segment is smaller, regulatory scrutiny is intense, motivating sponsors to partner with CDMOs holding track records in both viral vectors and cellular handling.

Vaccines harness AAV’s ability to stimulate balanced humoral and cellular immunity without integrating into host genomes. Academic groups and mid-cap pharma use the platform for infectious disease and oncology antigens, pushing vaccine CAGR to 20.52%. Batch configurations differ—higher titers but lower purity requirements—so CDMOs adapt resin selections and formulate stabilizers suited for field deployment. Successful proof-of-concept trials would diversify end-markets, cushioning revenue cycles as single-dose curative therapies achieve peak penetration. Consequently, application expansion strengthens the resilience of the Adeno associated virus (AAV) CDMO market.

By End User: Innovation Engines Meet Big-Pharma Scale

Biotech start-ups accounted for 49.08% demand in 2025 by pioneering first-in-class therapies that require speed and manufacturing agility. They outsource nearly all CMC functions, generating long project tails for CDMOs. Academic and non-profit institutes supply translational science, often through government-backed grants that subsidize early manufacturing costs. Their projects feed the future pipeline, ensuring continuity of demand even if venture cycles soften.

Large pharmaceutical companies now grow fastest at 20.81% CAGR. Roche’s multi-billion-dollar capsid deals and Novo Holdings’ Catalent buyout highlight a strategic shift from tentative licensing to platform ownership. Big-pharma sponsors bring supply-chain rigor and global launch footprints, raising compliance expectations across the vendor base. CDMOs that scale to enterprise-grade quality systems and harmonized digital batch records become preferred partners. This evolving buyer mix underlines a maturation phase for the Adeno associated virus (AAV) CDMO industry.

Geography Analysis

North America maintained 44.62% Adeno associated virus (AAV) CDMO market share in 2025 on the back of sizable venture capital, a deep talent pool and FDA accelerated pathways. The United States hosts over half of global CGT trials, driving constant demand for process development and GMP lots. Capacity additions by Thermo Fisher Scientific and Avid Bioservices broadened domestic options for sponsors seeking onshore manufacturing. Canada offers tax incentives and collaborative academic networks, while Mexico supports cost-effective ancillary operations such as plasmid supply.

Europe offers a mature, highly regulated environment that attracts multinational programs seeking EMA approval. Germany, the United Kingdom and France anchor regional vector production, leveraging strong academic links and government innovation grants. Lonza’s USD 1.2 billion Vacaville acquisition reinforced Europe-to-U.S. tech-transfer workflows, ensuring parallel supply chains. Brexit introduced documentation redundancies, yet skilled labor and supportive funding keep UK sites competitive. EU GMP frameworks and cross-border Qualified Person (QP) releases streamline multi-site strategies.

Asia–Pacific posts the quickest rise at 21.38% CAGR, reflecting aggressive investment by contract giants such as WuXi AppTec and Samsung Biologics. China prioritizes indigenous gene therapy manufacturing under its “Made in China 2025” plan, while Japan’s fast-track regenerative-medicine law grants conditional approval in as little as two years. South Korea’s biologics clusters combine fiscal incentives with seasoned workforce, attracting U.S. and EU sponsors for cost-optimised commercial runs. India and Australia add further nodes for regional clinical supply, although diverse local regulations necessitate flexible quality-system architectures. Together, these developments align global capacity with the shifting geography of demand, sustaining worldwide growth of the Adeno associated virus (AAV) CDMO market.

Competitive Landscape

The Adeno associated virus (AAV) CDMO market remains moderately fragmented, yet recent megadeals mark a consolidation phase. Novo Holdings’ USD 16.5 billion Catalent acquisition and GHO Capital’s USD 1.1 billion Avid Bioservices buyout reposition balance sheets for long-term asset utilization. Large CDMOs pursue platform breadth, combining viral vectors with mRNA, plasmids and fill-finish under one roof to secure multi-program contracts. Specialists such as Oxford Biomedica leverage proprietary cell lines and vector design expertise to win high-value niche work.

Strategic partnerships emphasize knowledge transfer in AI-enabled capsid design and continuous manufacturing. Samsung Biologics embeds digital twins across its 784,000 L network to optimize batch scheduling and deviation management. Lonza integrates Vacaville’s large-scale stainless-steel assets with European single-use suites, offering hybrid pathways from clinical to commercial. White-space opportunities exist in decentralized pod manufacturing and plasmid self-sufficiency, areas where emergent players such as Genezen and Matica Biotechnology target differentiation.

Competitive intensity is tempered by significant technical and regulatory barriers. Process validation for high-volume AAV runs can exceed USD 25 million, deterring new entrants. Intellectual-property minefields and long lead-time equipment reinforce incumbency. As a result, top-five vendors capture a steadily rising share of awarded projects, though smaller, innovation-focused CDMOs retain space by excelling in capsid engineering, high-potency suites and rapid analytics. The coexistence of scale and specialization defines the evolving structure of the Adeno associated virus (AAV) CDMO market.

Adeno-Associated Virus (AAV) CDMO Industry Leaders

Thermo Fischer Scientific Inc.

Creative Biogene

Catalent Inc.

Charles River Laboratories International Inc.

Aldevron

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Avid Bioservices finalized its USD 1.1 billion sale to GHO Capital Partners and Ampersand Capital Partners

- November 2024: FDA approved Kebilidi as the first brain-delivered AAV gene therapy for AADC deficiency

Global Adeno-Associated Virus (AAV) CDMO Market Report Scope

As per the scope of the report, AAV is a protein shell surrounding and protecting a small, single-stranded DNA genome. AAV CDMO refers to the contract manufacturing organizations that are involved in the development of AAV.

The AAV CDMO market is segmented by workflow, culture type, application, end user, and geography. By workflow, the market is segmented into upstream processing and downstream processing. By culture type, the market is segmented into adherent culture and suspension culture. By application, the market is segmented into cell & gene therapy development, vaccine development, biopharmaceutical & pharmaceutical discovery, and biomedical research. By end user, the market is segmented into pharmaceutical & biopharmaceutical companies and academic & research institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for all the above segments.

| Process Development |

| GMP Drug-Substance Manufacturing |

| Fill-Finish & Packaging |

| Quality Control & Release Testing |

| Analytical & Regulatory Support |

| AAV2 |

| AAV5 |

| AAV8 |

| AAV9 |

| Next-Gen / Engineered Capsids |

| Pre-clinical |

| Clinical |

| Commercial |

| Gene Therapy |

| Cell Therapy (ex-vivo) |

| Vaccine |

| Biotech Start-ups |

| Large Pharma |

| Academic & Non-Profit Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Service Type | Process Development | |

| GMP Drug-Substance Manufacturing | ||

| Fill-Finish & Packaging | ||

| Quality Control & Release Testing | ||

| Analytical & Regulatory Support | ||

| By Serotype | AAV2 | |

| AAV5 | ||

| AAV8 | ||

| AAV9 | ||

| Next-Gen / Engineered Capsids | ||

| By Manufacturing Scale | Pre-clinical | |

| Clinical | ||

| Commercial | ||

| By Application | Gene Therapy | |

| Cell Therapy (ex-vivo) | ||

| Vaccine | ||

| By End User | Biotech Start-ups | |

| Large Pharma | ||

| Academic & Non-Profit Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Adeno associated virus (AAV) CDMO market in 2026?

The Adeno associated virus (AAV) CDMO market size is USD 0.76 billion in 2026 and is projected to post a 20.44% CAGR over 2026-2031.

Which service segment generates the most revenue?

GMP drug-substance manufacturing holds 38.05% revenue because it encompasses capital-intensive upstream processes and stringent GMP compliance.

Which region is growing fastest for AAV CDMO services?

AsiaPacific leads growth with a forecast 21.38% CAGR through 2031 owing to capacity additions in China, South Korea and Japan.

Why are engineered capsids attracting interest?

AI-optimized engineered capsids improve tissue targeting and production yields, driving a 21.05% CAGR for that segment.

What is the main supply-chain constraint facing AAV manufacturers?

Limited availability of GMP-grade plasmid DNA continues to prolong lead times, despite new capacity coming online.

How concentrated is competition among AAV CDMOs?

The market earns a concentration score of 6, reflecting moderate consolidation following recent billion-dollar acquisitions yet with ample room for niche specialists

Page last updated on: