India Telemedicine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

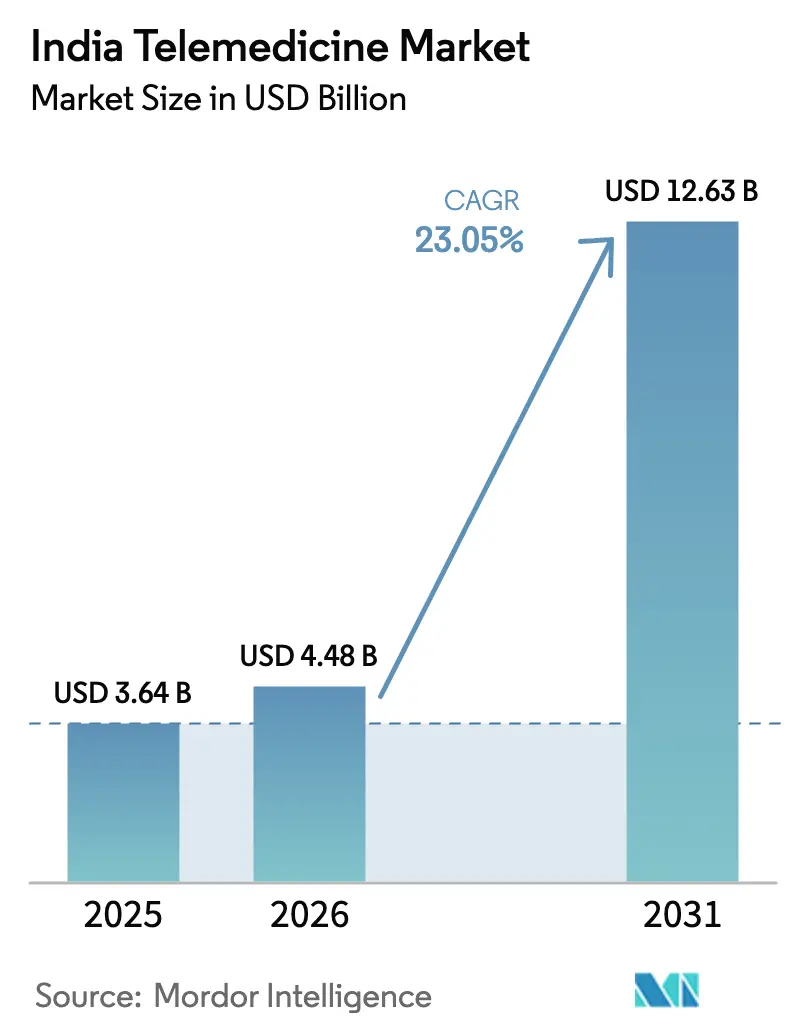

| Base Year Market Size (2025) | USD 3.64 Billion |

| Market Size (2026) | USD 4.48 Billion |

| Market Size (2031) | USD 12.63 Billion |

| Growth Rate (2026 - 2031) | 23.05% CAGR |

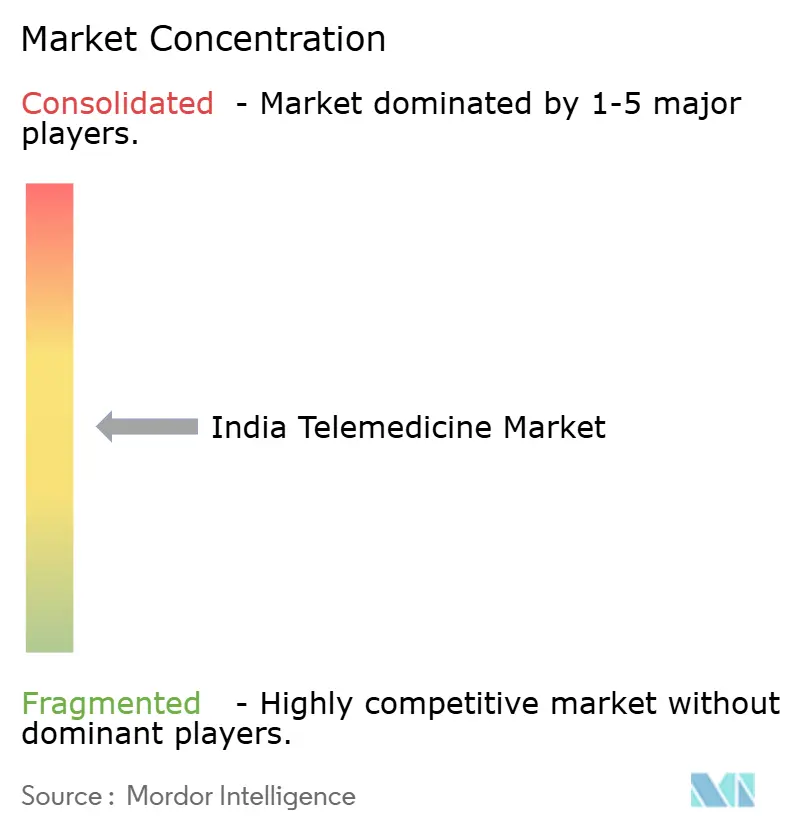

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Telemedicine Market Analysis by Mordor Intelligence

The Indian telemedicine market size is expected to grow from USD 3.64 billion in 2025 to USD 4.48 billion in 2026 and is forecast to reach USD 12.63 billion by 2031 at 23.05% CAGR over 2026-2031. Strong public-sector investment in broadband, the Ayushman Bharat Digital Mission’s 65 crore health IDs, and the eSanjeevani platform’s 34 crore consultations show that telehealth is now a structural component of national health delivery rather than a pandemic workaround.[1]Press Information Bureau, “Ayushman Bharat Digital Mission Update,” pib.gov.in Growing 5G penetration, cloud infrastructure, and artificial-intelligence tools expand the technical scope of care, while chronic-disease prevalence and an aging population widen the addressable patient pool. Private hospitals leverage existing brands to scale virtual services, mHealth apps deepen consumer engagement, and cloud deployment reduces capital barriers for smaller providers. At the same time, penalties under the Digital Personal Data Protection Act, medico-legal ambiguity, and clinician burnout temper growth prospects. Overall, the Indian telemedicine market demonstrates both vigorous top-line expansion and a shift from single-use consultations to integrated, data-rich care pathways.

Key Report Takeaways

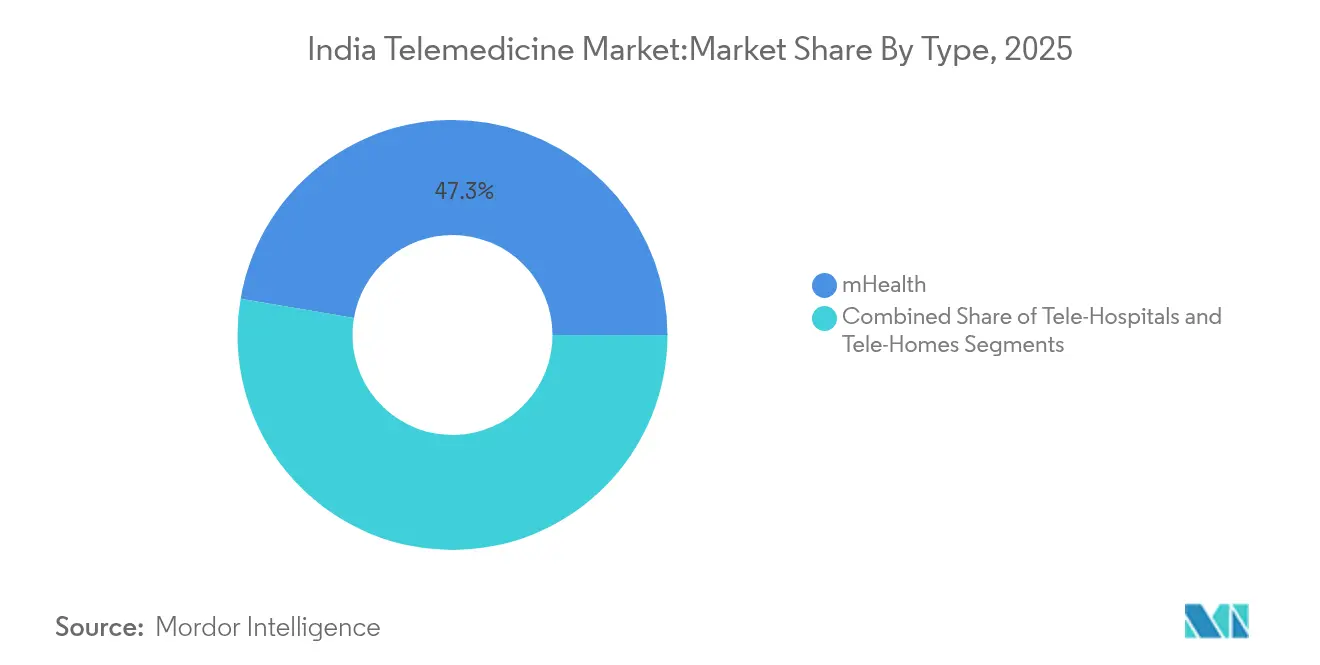

- By type, mHealth led with 47.30% revenue share in 2025; the tele-homes segment is forecast to expand at a 24.25% CAGR through 2031.

- By component, services held 67.55% of the India telemedicine market share in 2025; products are expected to trail services but still post a 21.65% CAGR to 2031.

- By mode of delivery, cloud platforms accounted for 72.85% of the Indian telemedicine market size in 2025 and are growing at 19.95% through 2031.

- By end user, private hospitals and clinics captured 55.05% of demand in 2025, while home-care users show a 23.12% CAGR to 2031.

- By application, chronic-disease management represented 47.70% of revenue in 2025; mental-health use cases are set to grow at 25.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Telemedicine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Smartphone & 4G/5G Penetration | +4.20% | National, with accelerated gains in Tier-2/3 cities | Medium term (2-4 years) |

| Ayushman Bharat Digital Mission Roll-Out | +3.80% | National, with concentrated impact in rural areas | Long term (≥ 4 years) |

| Rising Chronic-Disease Burden and Ageing Population | +5.10% | National, with higher prevalence in urban metros | Long term (≥ 4 years) |

| Surge In Tier-2/3 City Adoption Post-COVID | +3.20% | Tier-2/3 cities, spillover to rural areas | Short term (≤ 2 years) |

| E-Sanjeevani Integration Into State Insurance Schemes | +2.90% | State-specific, with early gains in progressive states | Medium term (2-4 years) |

| Technological Innovations and Rising Demand for Remote Patient Monitoring | +4.60% | National, with premium adoption in urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Smartphone & 4G/5G Penetration

Faster mobile networks now cover 84% of citizens, and 5G subscriptions are forecast to reach 1 billion by 2030, removing prior bandwidth bottlenecks to video consultation and AI-supported diagnostics.[2]Ministry of Communications, “5G Coverage Statistics,” dot.gov.in Low-cost smartphones allow patients in smaller cities to access cloud-hosted platforms, and the 5G Intelligent Village programme pilots live remote monitoring in 10 villages, validating rural feasibility. For providers, near-ubiquitous connectivity underpins continuous data streams from wearables, enabling proactive rather than episodic care. Pharmaceutical companies already package adherence apps with medications, illustrating how telecom reach converts to clinical engagement. The Indian telemedicine market thus gains a technology backbone that matches the scale of national health needs.

Ayushman Bharat Digital Mission Roll-Out

The mission has issued 65 crore ABHA IDs and linked 300 million health records, establishing an interoperable backbone that lets any licensed platform retrieve longitudinal data with patient consent.[3] Linkage with insurance schemes magnifies network effects, while AI research tie-ups with IIT Kanpur signal a pivot to predictive services. For clinicians, unified records shorten triage time and lower duplication of tests. For entrepreneurs, standardized APIs simplify product development. These factors elevate the Indian telemedicine market from ad-hoc video calls to integrated disease-management ecosystems.

Rising Chronic-Disease Burden and Ageing Population

Diabetes cases are expected to climb from 77 million to 134 million by 2045, and non-communicable diseases cause 60% of deaths nationwide.[3]World Health Organization, “Non-communicable Diseases Country Profile,” who.int Multi-morbidity prevalence among seniors is already 43.2%, creating sustained demand for remote monitoring devices that track vitals and medication adherence. Mental health disorders affect 56 million people; a budget allocation of INR 90 crore (USD 10 million) for the National Tele Mental Health Programme signals policy recognition of digital therapy’s value. As chronic conditions often require lifestyle coaching, tele-platforms that bundle nutrition and behavior insights with virtual consults gain a competitive advantage.

eSanjeevani Integration into State Insurance Schemes

The Ayushman Bharat PM-JAY card base stands at 35.4 crore, and the National Health Claims Exchange aims to streamline reimbursement across 50 insurers. States such as Karnataka now reimburse video consultations for hypertension under public insurance, creating a precedent for other disease areas. Standardized coding reduces claim rejection rates, improving provider cash flow. As out-of-pocket expenses decline, price sensitivity diminishes, broadening the paying user base beyond metropolitan elites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uncertain Reimbursement & Medico-Legal Clarity | -2.80% | National, with higher impact in private sector | Medium term (2-4 years) |

| Low Digital Literacy In Rural Populations | -1.90% | Rural areas, with concentrated impact in remote regions | Long term (≥ 4 years) |

| Data-Localisation Compliance Costs For Start-Ups | -1.50% | National, with disproportionate impact on startups | Short term (≤ 2 years) |

| Doctor Burnout From "Always-On" Virtual Workload | -1.20% | Urban centers, with spillover to specialist networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Uncertain Reimbursement & Medico-Legal Clarity

Although the National Health Claims Exchange promises unified processes, reimbursement codes for preventive consultants and AI-assisted diagnostics remain nascent, slowing provider monetization. Telemedicine guidelines clarify consent and prescription rules, yet liability for misdiagnosis during poor internet connectivity is unresolved. Private insurers hesitate to cover follow-up video visits, creating patient confusion. Until policy converges, investment flows may favor established hospital networks over start-ups, limiting overall dynamism.

Low Digital Literacy in Rural Populations

Seventy percent of citizens live rurally, but many lack confidence in app navigation or privacy settings. Studies show that effective use of tele-apps requires both digital and health literacy; without guidance, patients may misinterpret advice. Government-funded Bhashini language models and chatbot tutorials aim to narrow gaps, yet scaling culturally relevant content across 22 official languages is complex. The Indian telemedicine market must therefore pair technology with local facilitators, adding service costs and execution risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: mHealth Dominance Drives Consumer Engagement

mHealth commanded 47.30% of the Indian telemedicine market in 2025, reflecting rapid smartphone adoption and consumer preference for self-service health apps. Tele-homes, while smaller, record a blazing 24.25% CAGR as families embrace in-home monitoring devices for elderly care. Tele-hospitals focus on provider-to-provider consults, leveraging institutional bandwidth for complex imaging and second opinions. The convergence of AI diagnostics with mobile platforms expands service scope beyond chat and video to include vitals sensing, medication reminders, and lifestyle coaching. Providers that embed outcome tracking within apps retain users longer and unlock cross-selling of lab tests and pharmacy deliveries. Rising chronic-disease prevalence ensures sustained traffic to disease-specific apps, while gamification and vernacular interfaces deepen daily engagement.

In the second half of the forecast window, mHealth is expected to maintain the largest India telemedicine market size among type segments, even as tele-homes narrow the gap through hybrid models that mix nurse visits with cloud dashboards. Policy incentives for remote care of seniors should further lift tele-home revenue. Tele-hospital growth will hinge on specialist availability and reimbursement parity, but digital referral networks promise incremental gains. Interoperability standards under Ayushman Bharat allow data fluidity across these modes, encouraging integrated care pathways rather than isolated point solutions.

By Component: Services Innovation Outpaces Hardware Commoditization

Services held 67.55% of 2025 revenue and will outpace products through 2031 as providers monetize clinical expertise, analytics, and care coordination. Subscription models for diabetes coaching, mental-health therapy, and post-operative monitoring illustrate the shift from transaction fees to recurring revenue. Hardware ranging from kiosks to wearables faces margin pressure as global suppliers enter, but remains a necessary enabler for data capture. Software platforms have commoditised onboarding and scheduling; differentiation now lies in proprietary clinical protocols and specialist networks.

The India telemedicine market size for services is projected to expand steadily because insurers and employers increasingly reimburse digital programmes that demonstrate measurable outcomes. Tele-psychiatry, remote radiology, and AI-enabled triage present high-growth niches. Product vendors respond by bundling devices with subscription services, blurring component lines. Over the period, service providers that secure deep domain partnerships with hospitals and pharma companies will consolidate share, while hardware-only players may move upstream into analytics to stay relevant.

By Mode of Delivery: Cloud Infrastructure Enables Scalable Healthcare

Cloud deployments captured 72.85% of the India telemedicine market in 2025, underscoring the need for elastic compute and storage to manage national-scale datasets. Public-cloud compliance frameworks now cover health data, easing hospital CIO concerns. Start-ups prefer the cloud for speed and capital efficiency, while some large public hospitals keep sensitive archives on-premise due to sovereignty mandates. Hybrid architectures that store identifiers locally but perform analytics in the cloud gain traction.

As ABHA IDs proliferate, query loads on health exchanges will surge, favoring cloud-native microservices that auto-scale. AI inference workloads for imaging and language translation also require GPU clusters that are rarely affordable on-premise. Consequently, the India telemedicine market size linked to cloud delivery will widen its lead, though secure edge devices will complement central servers for latency-sensitive tasks. Vendors that offer pre-certified compliance toolkits lower entry barriers for innovators.

By End User: Private Sector Leadership Amid Home-Care Emergence

Private hospitals and clinics generated 55.05% of 2025 revenue, leveraging brand trust and multi-specialty rosters to cross-sell virtual follow-ups. Public facilities use telemedicine chiefly to extend reach into rural health centres, but budget limits cap their digital spend. Home-care users, fuelled by demographic shifts, exhibit the fastest 23.12% CAGR. Families value reduced travel costs and infection risk, while wearable-linked dashboards give doctors continuous visibility.

In metropolitan areas, insurers now bundle post-discharge video consults, accelerating home-care adoption. Tier-2 cities witness growing demand for virtual diabetes and cardiology programmes. The India telemedicine market share held by private providers will gradually ease as home-care platforms win loyalty with personalised plans. Yet synergy exists: many hospitals invest in or partner with home-care start-ups to secure continuum-of-care revenue.

By Application: Chronic Care Foundation Supports Mental-Health Expansion

Chronic-disease management held 47.70% of 2025 revenue, anchored by diabetes, hypertension, and COPD programmes that reduce inpatient costs through early intervention. Mental-health use cases register the highest 25.55% CAGR as societal stigma fades and Tele MANAS helplines prove scalability.

Acute-care follow-ups remain essential for surgical recovery but constitute a smaller share.Integrated platforms that treat physical and mental aspects of chronic illness record superior retention rates. AI chatbots triage routine queries, freeing psychiatrists for complex cases. The Indian telemedicine market size attached to mental health will expand sharply once reimbursement codes mature. Meanwhile, per-member-per-month models in chronic care gain insurer support owing to documented savings.

Geography Analysis

India’s urban metros accounted for the lion’s share of 2024 spending, propelled by dense private-hospital networks and higher disposable incomes. Cities such as Mumbai and Bengaluru show video-consult penetration above 50% among smartphone users, and corporate employers increasingly subsidise digital primary care packages. Network effects in these hubs accelerate innovation cycles and raise service-quality expectations that ripple nationwide.

Tier-2 and Tier-3 cities are poised to be the next growth engine. Population inflows, limited specialist availability, and improving 4G and 5G coverage create fertile conditions for remote cardiology, dermatology, and mental-health services. Providers that adapt vernacular interfaces and flexible payment plans have already doubled consult volumes year-on-year. For many operators, these mid-sized cities deliver lower acquisition costs than metros, enhancing unit economics in the Indian telemedicine market.

Rural regions, home to 70% of citizens, represent both challenge and opportunity. Government fibre-to-village programmes and 5G pilots are closing infrastructure gaps, yet digital literacy training remains essential. Community health workers often mediate video calls, indicating a blended model rather than pure self-service. Successful pilots show reductions in travel time and earlier disease detection. Over the forecast horizon, rural uptake could unlock transformative public-health gains and cement telehealth’s role in universal-health-coverage goals.

Competitive Landscape

Competition is moderate, with hospital chains, technology start-ups, and insurance-backed platforms vying for a share. Incumbent hospitals such as Apollo leverage established clinician rosters and pharmacy supply chains to push omnichannel engagement. Their partnership with Microsoft to build AI copilots exemplifies the move toward data-driven workflows that raise entry barriers. Meanwhile, pure-play platforms attract venture capital to scale fast, yet must navigate rising compliance costs.

Vertical integration is a clear trend. Tata 1mg bundles teleconsultation, e-pharmacy, and diagnostics, aiming for a closed-loop user journey. Insurer Acko’s acquisition of OneCare indicates payers’ interest in proactive disease management to lower claim ratios. Traditional TPAs like Medi Assist expand through mergers, building infrastructure to settle telehealth claims swiftly.

International collaborations add technological depth. TeleMedC’s AI eye-screening deal and Merago-Portea’s home-care alliance import advanced algorithms and operational know-how. Consolidation is likely as capital requirements grow; scale players with integrated services and strong compliance frameworks should command higher margins. Nonetheless, ecosystem openness under Ayushman Bharat widens niches for specialist apps, ensuring ongoing innovation within the India telemedicine market.

India Telemedicine Industry Leaders

Apollo Hospitals Enterprise Limited (AHEL)

Koninklijke Philips N.V.

Lybrate, Inc.

Practo

Prognosys

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: TeleMedC partnered with AND Healthcare Solutions to deploy AI eye-disease screening, which aims to assess 1 billion eyes over ten years.

- February 2025: Tata Digital sought USD 300 million to expand Tata 1mg’s integrated platform.

- January 2025: Apollo Hospitals and Microsoft announced four AI healthcare copilots under a “Hospital of the Future” vision.

- December 2024: Pristyn Care entered talks to raise USD 100 million for surgical-care expansion.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the India telemedicine market as the value generated by digital platforms that enable real-time or asynchronous clinical interactions, remote monitoring devices, and mHealth apps that connect licensed physicians with patients located anywhere in the country. Revenue is counted only when a paid medical service is delivered and recorded in India, irrespective of the headquarters of the platform operator.

Scope exclusion: preventive wellness apps, online pharmacies without clinician involvement, and international cross-border consultations are kept outside this scope.

Segmentation Overview

- By Type

- Tele-Hospitals

- Tele-Homes

- mHealth

- By Component

- Products

- Hardware

- Software

- Others

- Services

- Tele-consultation

- Tele-pathology

- Tele-radiology

- Tele-psychiatry

- Other Services

- Products

- By Mode of Delivery

- Cloud-based

- On-premise

- By End User

- Public Hospitals

- Private Hospitals & Clinics

- Home-care Users

- By Application

- Chronic Disease Management

- Acute Care & Follow-up

- Mental Health

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed clinicians across tertiary hospitals, start-up founders, state telemedicine nodal officers, and insurance executives spanning North, South, and tier-2 cities. These discussions validated patient mix assumptions, pricing dispersion, and likely uptake of AI-enabled remote monitoring over the next five years.

Desk Research

We began with statutory sources such as the National Health Authority's ABDM dashboard, the Ministry of Health's eSanjeevani data releases, Telecom Regulatory Authority mobile broadband reports, and Reserve Bank digital payment statistics, which anchor usage volumes, adoption rates, and average ticket values. Academic journals hosted on PubMed, peer-reviewed Indian telehealth outcome studies, and trade-association white papers (e.g., FICCI, NATHEALTH) sharpened disease prevalence inputs and reimbursement nuances. Paid databases that our team accessed, including D&B Hoovers for platform financials and Dow Jones Factiva for deal flows, helped align company-level volumes with macro totals. This list is illustrative; many additional documents informed our desk research.

Market-Sizing & Forecasting

Using a top-down build that converts eSanjeevani, private app, and hospital virtual-OPD consultation counts into paid encounter pools, we applied weighted average consultation prices, then overlaid remote patient monitoring kit shipments, chronic disease follow-up ratios, and smartphone penetration growth to capture ancillary revenue. Supplier roll-ups and sampled ASP × volume checks served as bottom-up sense tests before totals were finalized. A multivariate regression that links encounter volumes with internet subscribers, 60+ population, and non-communicable disease incidence underpins the 2025-2030 forecast; scenario analysis adjusts for regulatory or reimbursement shocks. Gaps in bottom-up inputs are bridged by calibrated proxies agreed during physician surveys.

Data Validation & Update Cycle

Outputs pass anomaly checks against historic growth corridors and external health-spend ratios. Senior reviewers sign off after reconciling any >5% variances. The dataset is refreshed each year, with interim tweaks when policy or funding changes materially alter use patterns.

Why Mordor's India Telemedicine Market Baseline Stands Firm

Published estimates often vary because each firm chooses distinct service mixes, pricing ladders, and refresh cadences.

Key gap drivers include whether non-clinical wellness services are pooled with clinical teleconsults, the treatment of hardware sales, and the frequency at which exchange rates and platform disclosures are updated.

Mordor's model reports the base-case 2025 market for paid clinical telemedicine only, uses verified domestic price points, and is refreshed annually, which keeps inflation, platform churn, and policy shifts current.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.64 B (2025) | Mordor Intelligence | - |

| USD 5.05 B (2024) | Regional Consultancy A | Bundles telehealth hardware and preventive wellness apps with clinical services |

| USD 4.29 B (2025) | Global Consultancy B | Counts cross-border consultations and applies uniform Asia ASP without India-specific adjustment |

| USD 1.54 B (2024) | Industry Association C | Limits coverage to public-sector platforms, excludes private hospital and mHealth revenue |

The comparison shows that when service scope widens, values climb, and when coverage narrows, figures drop. By selecting a clearly clinical scope, triangulating inputs, and updating annually, Mordor Intelligence delivers a balanced baseline that decision-makers can trace to transparent variables and repeatable steps.

Key Questions Answered in the Report

What is the current value of the India telemedicine market?

The India telemedicine market stands at USD 4.48 billion in 2026 and is on track to reach USD 12.63 billion by 2031.

Which segment holds the highest India telemedicine market share?

MHealth applications led the market with a 47.30% share in 2025.

How fast is the mental-health application segment growing?

Mental-health use cases are projected to expand at a 25.55% CAGR through 2031.

Why is cloud deployment important for telemedicine in India?

Cloud platforms already account for 72.85% of revenue because they provide elastic compute, compliance features, and scalability for national-level datasets.

What regulatory factor most influences telemedicine start-ups?

Data-localization mandates under the Digital Personal Data Protection Act impose significant compliance costs and fines of up to INR 250 crore.

How are Tier-2 and Tier-3 cities shaping future growth?

These mid-sized cities offer lower specialist density and rising digital adoption, driving rapid uptake of teleconsultations and expected to become a primary growth engine before 2030.

Page last updated on: