Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

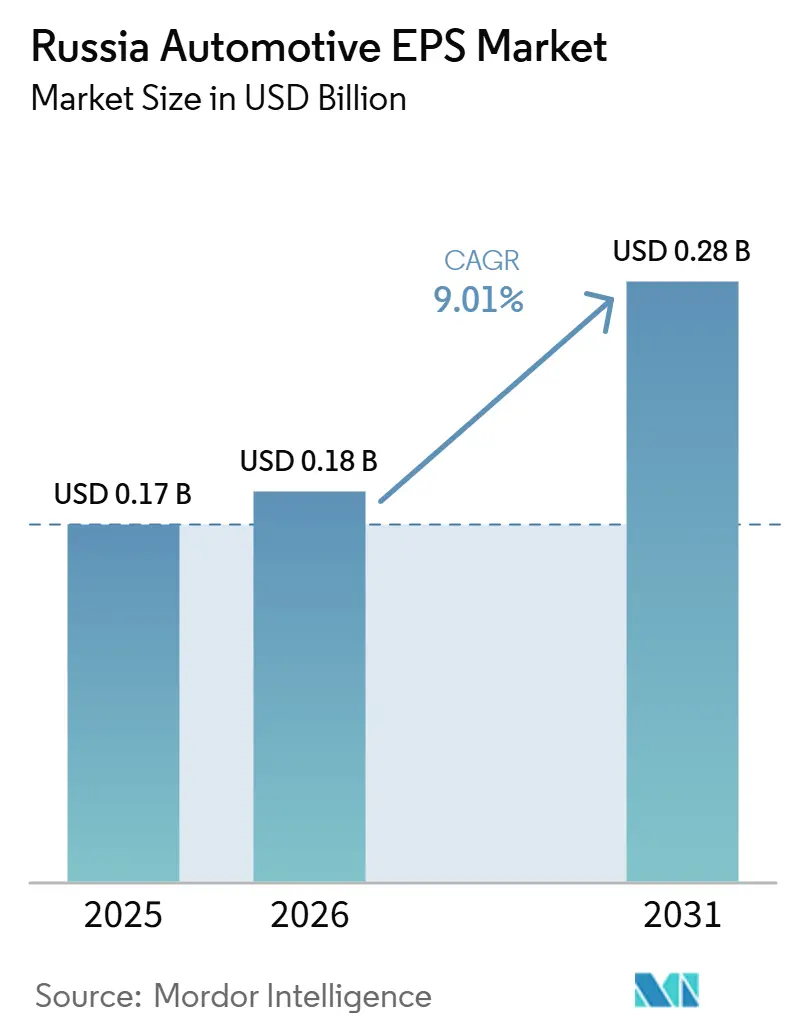

| Base Year Market Size (2025) | USD 0.17 Billion |

| Market Size (2026) | USD 0.18 Billion |

| Market Size (2031) | USD 0.28 Billion |

| Growth Rate (2026 - 2031) | 9.01% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Automotive EPS Market Analysis by Mordor Intelligence

The Russian Automotive EPS Market size is projected to expand from USD 0.17 billion in 2025 and USD 0.18 billion in 2026 to USD 0.28 billion by 2031, registering a CAGR of 9.01% between 2026 and 2031. Passenger car production in Russia fell by 11.8% to 673,000 units in 2025, yet the Russian automotive EPS market continues to grow because EPS penetration per vehicle is rising as OEMs focus on fuel economy and vehicle electrification even when output remains under pressure. The Russian automotive EPS market is also being reshaped by import substitution, and that shift still shows execution risk because Avtoelektronika JSC reported a 2.2-fold revenue decline to RUB 4.3 billion in 2025 after AvtoVAZ rejected nearly 21,000 EPS units due to design-related quality issues. Growth in the Russian automotive EPS market is therefore tied not only to unit recovery, but also to a steady move from column systems toward dual pinion and rack-assist layouts that carry a higher average selling price per vehicle. The competitive setting in the Russian automotive EPS market still splits between global technology leaders and domestic suppliers tied to captive programs, while the February 2026 joint venture between Wuhu Sterling Steering System and Rulevye Systemy adds a new Chinese-led manufacturing route in Togliatti. This leaves the Russian automotive EPS market with a clear opening for suppliers that can combine local production, stable quality, and ADAS-ready steering capability as Russia brings in more Chinese platforms and upgrades domestic vehicle programs.

Key Report Takeaways

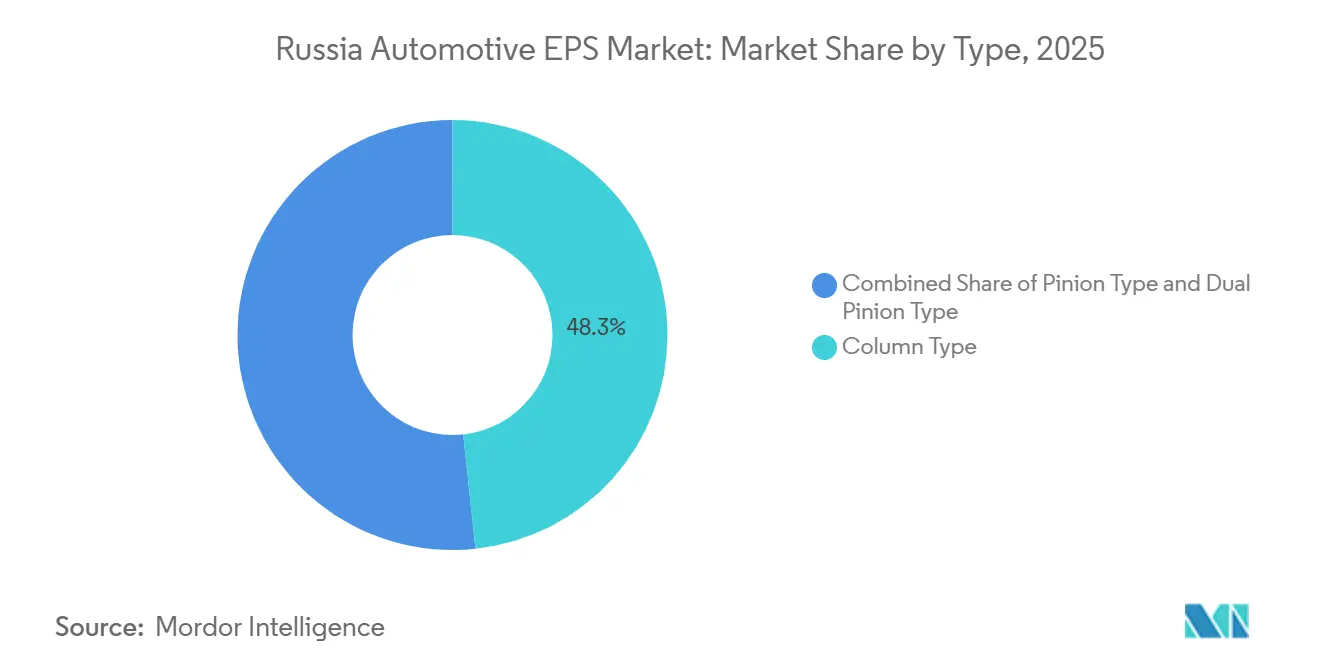

- By type, Column Type EPS held 48.27% of the Russian automotive EPS market share in 2025, while Dual Pinion Type is projected to grow at a 9.12% CAGR during 2025-2030.

- By component type, Steering Rack or Column accounted for 45.37% of the Russian automotive EPS market size in 2025, while Sensors are forecast to expand at a 9.23% CAGR during 2025-2030.

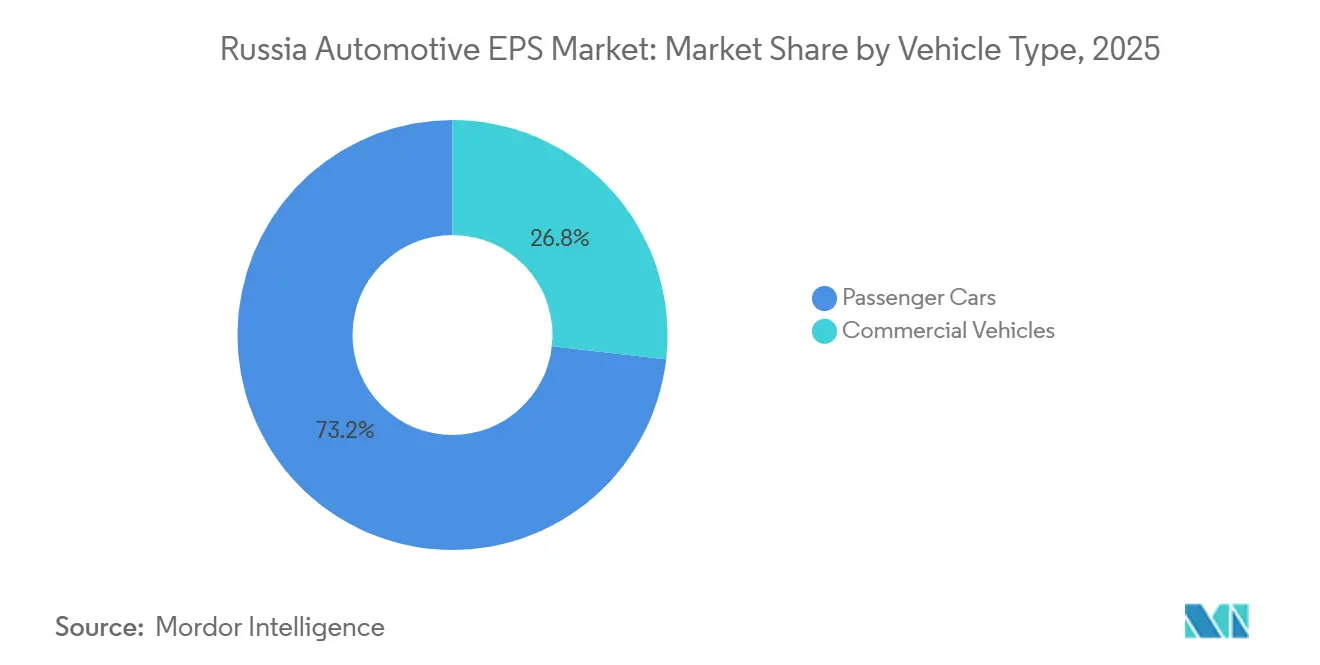

- By vehicle type, Passenger Cars held 73.15% of the Russian automotive EPS market share in 2025, while Commercial Vehicles are projected to grow at a 9.17% CAGR during 2025-2030.

- By propulsion type, ICE Vehicles accounted for 58.19% of the Russian automotive EPS market size in 2025, while Battery Electric Vehicles are projected to grow at a 9.32% CAGR during 2025-2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Russia Automotive EPS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid electrification of vehicle platforms | +1.8% | National, with concentration in Moscow, Togliatti, and Kaliningrad EV assembly clusters | Medium term (2-4 years) |

| Increasing demand for fuel efficiency and emission reduction | +1.5% | Global spill-over; Central and Volga Federal Districts lead domestic adoption | Short term (≤ 2 years) |

| Regulatory mandates for ADAS integration | +1.2% | National, with early compliance pressure on OEMs in the Moscow region | Medium term (2-4 years) |

| Steer-by-wire R&D breakthroughs | +0.8% | Global R&D, with pilot applications in premium Russian platforms (AURUS) | Long term (≥ 4 years) |

| Tier-1/2 collaboration on 48-V e-Powertrain modules | +0.7% | Asia-Pacific core, spill-over to Russia through localized Chinese OEM assembly | Medium term (2-4 years) |

| OTA software steering calibration for mass customization | +0.6% | National, centered on connected-vehicle OEM programs in Moscow | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification of Vehicle Platforms

Russia’s shift toward electrified powertrains is still small in absolute volume, but it carries direct importance for the Russian automotive EPS market because every local EV or hybrid platform increases the need for electronically controlled steering systems. Domestic production of EVs and hybrids tripled year over year to 15,000 units in 2025, and these vehicles represented 6% of total domestic vehicle output, which created a larger installed base for EPS than the headline production trend alone suggested [1]“Electric Vehicle and Auto Component Updates,” Ministry of Industry and Trade of the Russian Federation, minpromtorg.gov.ru . Battery electric vehicles do not use an engine-driven vacuum source, so hydraulic steering is not a workable choice on those platforms, and EPS becomes the required solution by design. Moskvich expanded that shift when it unveiled the M70 and M90 crossovers in February 2026 after production began in December 2025, and those launches added new demand for modern steering content inside locally built vehicles. This means the Russian automotive EPS market can keep advancing even if total light vehicle output remains uneven, because the content value per electrified vehicle is rising as new programs enter production.

Increasing Demand for Fuel Efficiency and Emission Reduction

Fuel efficiency remains a practical reason for EPS adoption in Russia because OEMs and buyers both respond to operating cost pressure, and EPS removes the constant drag created by hydraulic pump systems. The user-provided draft states that EPS can recover 3% to 5% in fuel efficiency, and that benefit matters in a market where ICE vehicles still represented 58.19% of EPS demand in 2025. AvtoVAZ produced 324,558 Lada vehicles in 2025 and already fits column-type EPS across virtually all current Lada models, which shows that the economic case for EPS over hydraulic steering has already been accepted on the country’s highest-volume passenger car programs. The Russian automotive EPS market also benefits from product redesign at the local level, as the input notes that Itelma Group developed an 8.8 kg column-type unit to replace an older 10.5 kg to 11 kg design for Lada Iskra programs, improving efficiency and lowering system weight. That shift keeps the Russian automotive EPS market tied not only to regulation, but also to everyday vehicle economics that reward lighter and more efficient steering assemblies.

Regulatory Mandates for ADAS Integration

Russia is building a regulatory path that supports automated driving, and that creates an earlier sourcing signal for steering systems that can handle electronic control, redundancy, and fail-safe operation. The Ministry of Transport is updating frameworks for highly automated vehicles and targets Level 4 and Level 5 unmanned operations on all Russian roads from September 1, 2027, which pushes OEMs to lock in compliant steering architectures well before that date. Rosstandart is also developing 5 GOST standards for automated vehicle safety and functionality, and the steering response requirements in that path align with electronically controlled EPS or steer-by-wire systems rather than hydraulic alternatives. The Russian automotive EPS market, therefore, gains from a longer effective demand cycle, because vehicle programs planned for 2027 to 2030 need ADAS-capable steering systems during the procurement stage taking place now [2]“GOST Standards for Automated Vehicles,” Federal Agency on Technical Regulating and Metrology, rst.gov.ru . Russia already had 90 Level 3 autonomous trucks on public roads in 2025, which shows that commercial vehicle ADAS is not theoretical and is already creating near-term pull for EPS systems with integrated sensing capability.

Steer-By-Wire R&D Breakthroughs

The move from conventional EPS toward steer-by-wire is becoming more relevant to the Russian automotive EPS market because the enabling technologies are already entering series production in supplier networks that reach Russia through global and Chinese OEM programs. ZF is already producing steer-by-wire systems for NIO’s ET9 and supplies both the steering wheel actuator and the redundant steering gear actuator, which shows how quickly the technology is moving from pilot work into commercial use. Nexteer expects to launch 2 steer-by-wire programs in the first half of 2026, while 50% of its 2025 bookings supported EV or split EV and ICE platforms, which confirms that software-led steering is moving into the mainstream product mix. The draft also notes that Chinese OEMs assembling vehicles in Russia are adopting 48V architecture, and that design path supports faster-response steering systems that can narrow the gap between advanced EPS and full steer-by-wire layouts. Murom Machine-Building Plant added another local step in February 2026 when it launched EPS rack production for AURUS premium vehicles, which shows that Russia is moving premium domestic programs toward rack-assist systems before wider steer-by-wire readiness emerges.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher unit cost vs. hydraulic systems in low-cost cars | -1.5% | National, most pronounced in the Volga and Ural Federal Districts, where entry-level vehicle demand is highest | Short term (≤ 2 years) |

| Semiconductor supply-chain volatility for motor controllers | -1.2% | Global, with disproportionate impact on Russia given import dependency exceeding 75% for automotive-grade MCUs | Medium term (2-4 years) |

| Limited steering feel and safety concerns in emerging markets | -0.8% | National, aftermarket, and low-specification OEM segments | Short term (≤ 2 years) |

| Cybersecurity risks in electronically actuated columns | -0.7% | National, amplified by Russia's electronic-warfare environment and UN R155/ISO 21434 compliance requirements. | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Unit Cost Vs. Hydraulic Systems in Low-Cost Cars

Unit cost remains the clearest brake on the Russian automotive EPS market because entry-level vehicle programs still compete on tight procurement budgets, and large-volume contracts magnify even small component premiums. Lada programs sit at the center of that pressure because AvtoVAZ produced 324,558 vehicles in 2025, and the cost discipline on these high-volume platforms limits how quickly higher-value steering systems can move down the price ladder. The draft also shows that localization has not solved the issue on its own, because Avtoelektronika’s 2025 revenue fell to RUB 4.3 billion after quality-related rejections reduced shipment acceptance. That outcome matters because a local supplier that fails on quality can raise total ownership cost through warranty exposure, rework, and production disruption, even if the nominal purchase price looks lower. Until defect rates and production yields improve, the Russian automotive EPS market will keep facing resistance in the lowest-cost car segment, where every sourcing decision is tested against immediate affordability.

Semiconductor Supply-Chain Volatility for Motor Controllers

Semiconductor exposure remains a structural weakness for the Russian automotive EPS market because motor control MCUs are still heavily import-dependent and sit at the core of every EPS unit. Russia’s Ministry of Industry and Trade confirmed in February 2025 that only 330 out of 740 critical automotive component categories had been localized, leaving MCU and power semiconductor gaps unresolved for domestic vehicle control systems. The draft states that automotive-grade MCU dependence still exceeded 75%, and it adds that a 20% disruption in allocation from major semiconductor suppliers could affect 40% to 50% of domestic vehicle control unit assembly volume. Lead times for automotive-grade SiC and MOSFET parts also stretched to 20 to 30 weeks during recent supply events, which means production planning can be disrupted long before physical stock runs out. Russia’s Electronics Development state program is meant to support domestic automotive-grade microcontrollers, but the qualification timeline still sits beyond most of the current forecast window, so the Russian automotive EPS market remains exposed through 2031.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Dual Pinion Gains Ground as Column EPS Matures

Column Type EPS held 48.27% of the Russian automotive EPS market share in 2025, which kept it firmly in the lead across steering system formats. That position came from sustained use on Lada Granta and Lada Vesta programs, where packaging limits and low-cost assembly still favor column-integrated actuation over more advanced layouts. Domestic supply also stayed centered on AvtoVAZ-linked platforms, which helped column systems retain the broadest installed base even as supplier quality issues complicated the localization story. The Russian automotive EPS industry still relies on column systems for mainstream passenger cars because they match the current needs of entry and mid-range programs better than higher-cost alternatives.

Dual Pinion Type is the fastest-growing format with a 9.12% CAGR during 2025-2030, and that gap reflects a change in platform requirements rather than a simple replacement cycle. Dual pinion layouts fit more naturally with ADAS-enabled vehicles that need stronger actuator response and greater redundancy for lane keeping and emergency steering support. Chinese OEM assembly programs in Russia are pulling that mix upward because mid-size crossover platforms use rack-and-pinion architectures more often and bring more advanced steering design into local production. This means the Russian automotive EPS market is shifting toward a higher-value type mix even before steer-by-wire becomes a broad production reality, and the Russian automotive EPS industry is likely to see the biggest step-up where Chinese-derived platforms scale further.

By Component Type: Sensors Become the Margin Driver

Steering Rack or Column components accounted for 45.37% of the Russian automotive EPS market size in 2025, which kept structural hardware as the largest value pool in the component mix. This category is also the most exposed to localization policy because it connects directly with domestic metalworking, assembly capability, and long-standing supplier ties around Togliatti and AvtoVAZ programs. Rulevye Systemy’s February 2026 joint venture with Wuhu Sterling directly targeted this space, which shows where the immediate local manufacturing opportunity sits inside the Russian automotive EPS market. Steering motors remained the next important value block because local vehicle programs increasingly specify brushless designs that support lower noise, better efficiency, and improved refinement on Chinese-linked passenger vehicles.

Sensors are the fastest-growing component type with a 9.23% CAGR during 2025-2030, and that rise is tied to the spread of ADAS-ready steering architectures rather than a broad increase in vehicle output. Every ADAS-capable steering system needs at least torque and angle sensing, while dual pinion and rack-assist systems add more sensing points on the road-wheel side and raise component intensity per unit. The draft states that Russia’s steering position sensor market covered 1.8 million to 2.5 million units annually in 2026 and that EPS penetration could rise from 70% toward 85% to 90% of new vehicles by 2035, which supports a strong volume path for sensing components. This lifts revenue faster than vehicle output because sensors carry a higher per-unit margin than structural parts, so the Russian automotive EPS market is gaining value from electronic content even when core assembly growth stays moderate.

By Vehicle Type: Fleet And Commercial Programs are the Sleeper Demand Category

Passenger cars held 73.15% of the Russian automotive EPS market share in 2025, which kept the segment at the center of all volume and sourcing decisions. That leadership was built on the Lada portfolio and on the expanding presence of Chinese-branded passenger cars assembled under localization arrangements in Russia. The user input also notes that the EAEU production bloc supplied 0.95 million vehicles for the Russian market in 2025 and that passenger cars represented 85% of that total, which confirms the demand base supporting the Russian automotive EPS market. Moskvich added 2 crossover launches in February 2026, and AvtoVAZ continues to integrate EPS across its current Lada range, so passenger cars remain the anchor segment for domestic and imported steering content.

Commercial vehicles are forecast to grow at a 9.17% CAGR during 2025-2030, and that pace looks modest only because the base is still much smaller than that of passenger cars. Russia had 90 Level 3 autonomous trucks on public roads in 2025 and planned Level 5 unmanned truck prototypes in 2026, which gives commercial steering programs a direct link to higher-spec electronic actuation. Murom Machine-Building Plant strengthened that path in February 2026 when it launched electric portal axles for KAMAZ electric buses alongside EPS racks for AURUS vehicles, showing that funded production activity is already in place. The Russian automotive EPS market could therefore see a sharper step-up in commercial applications if autonomous freight, electric buses, and high-mileage fleet economics keep pushing demand toward electronically managed steering systems.

By Propulsion Type: BEV Uplift Masks A More Complex Transition

ICE vehicles accounted for 58.19% of the Russian automotive EPS market size in 2025, which shows that the largest part of demand still came from conventional powertrains even as electrification gained attention. New EV registrations reached 12,500 units in 2025 and still represented less than 1% of the new car market, while BEV sales also declined year over year, so the base for full battery electric steering demand remained narrow in absolute terms. That kept ICE-platform EPS demand tied mainly to fuel efficiency gains, noise and vibration improvement, and ongoing replacement of hydraulic steering in mass-market vehicles rather than to powertrain electrification alone. Hybrid models formed the transition layer because domestic EV and hybrid production tripled to 15,000 units in 2025, which showed clear platform investment despite weak BEV sales volume.

Battery electric vehicles are the fastest-growing propulsion segment with a 9.32% CAGR during 2025-2030, and that outlook rests on a firm technical requirement because BEVs cannot use hydraulic steering systems. The draft notes that first-quarter 2026 EV demand rose 22.5% from first-quarter 2025 and that Evolute reported a 5.6-fold sales increase, which indicates that domestic electric platforms are gaining more traction than the 2025 full-year headline suggested. As AvtoVAZ and Moskvich widen their electric portfolios, the Russian automotive EPS market is likely to direct a larger share of future sourcing toward domestic and Sino-Russian supply routes that can support BEV-specific steering needs.

Geography Analysis

The Russian automotive EPS market is geographically concentrated in 2 federal districts that shape most supplier call-off volumes, local content decisions, and investment priorities. The Central Federal District leads the highest-specification vehicle mix through Moscow-region operations and the Moskvich program, while Kaliningrad adds industrial weight through Avtotor’s multi-site manufacturing footprint. Moskvich is producing the M70 and M90 crossovers in 2026, and these newer programs raise demand for more advanced steering content than older entry-level vehicle lines. Avtotor operates 7 production sites that include electronic control systems and electric motor manufacturing, which gives the western cluster more capability in adjacent vehicle systems that matter to EPS integration. This part of the Russian automotive EPS market, therefore, carries more exposure to newer platforms, higher electronic content, and imported design logic from Chinese vehicle programs.

The Volga Federal District remains the main volume center for the Russian automotive EPS market because Togliatti and the wider Samara corridor anchor AvtoVAZ assembly, steering component production, and new localization efforts. Rulevye Systemy operates within this industrial base, and its joint venture with Wuhu Sterling was registered in February 2026 with authorized capital of RUB 137.5 million and total investment commitments of RUB 1.2 billion, which shows how the area is becoming the focal point for new rack-and-column EPS localization. Procurement inertia also supports these established clusters because type-approval under EAEU TR CU 018/2011 keeps OEM sourcing aligned with proven suppliers and manufacturing centers. This gives the Volga cluster a stable role inside the Russian automotive EPS market, even while the supplier mix itself is changing.

Outside the 2 main hubs, the Vladimir region is becoming a focused production site after Murom Machine-Building Plant launched EPS racks for AURUS premium vehicles and electric portal axles for KAMAZ electric buses in February 2026, with support from Russia’s Industrial Development Fund. Kaluga remains strategically relevant because Avtoelektronika is still the largest domestic source of column-type EPS despite its 2025 revenue contraction, and AvtoVAZ’s use of Itelma as an alternative has not removed Kaluga from the supply map. Russia’s Far East, especially Vladivostok, still works more as a re-import and final-fitment point for Chinese vehicle kits than as a full steering manufacturing base. As those localization programs mature, the region is expected to move into more limited SKD assembly with higher EPS content requirements than it carries today. The wider pattern in the Russian automotive EPS market is an east-west split where domestic value capture still centers on assembly and localized hardware, while pricing power on many advanced subassemblies remains with APAC-origin suppliers serving Chinese-brand vehicles.

Competitive Landscape

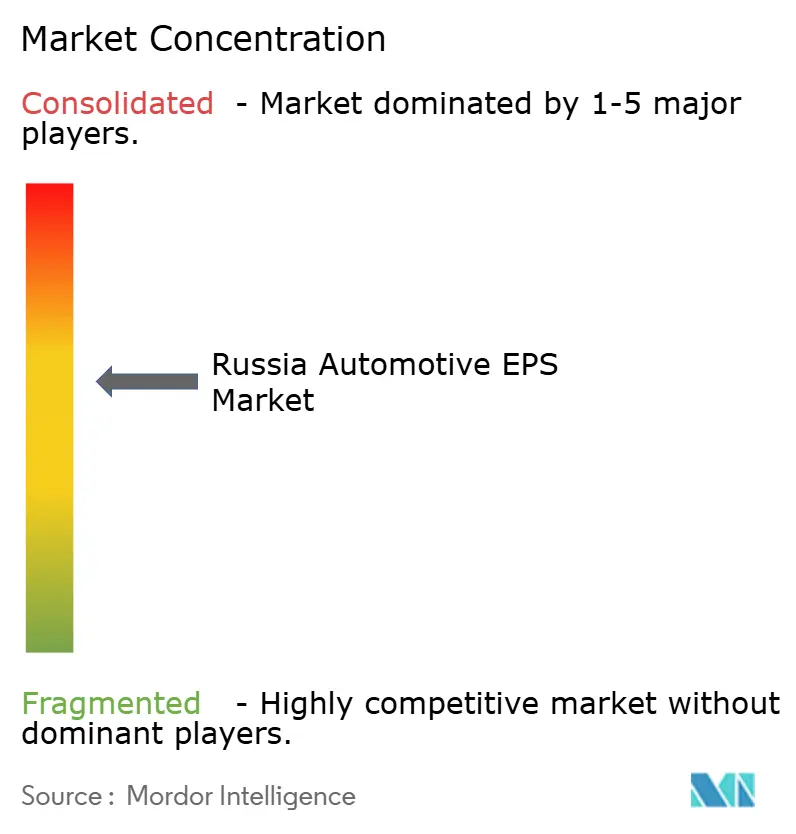

The Russian automotive EPS market shows moderate to high concentration at the technology tier because a small set of global suppliers still controls most advanced EPS program capability, software depth, and multi-platform experience. JTEKT Corporation, ZF Friedrichshafen AG, Robert Bosch GmbH, Nexteer Automotive, and NSK Ltd. remain the reference group for advanced steering awards that feed into Russian supply chains directly or through Chinese vehicle programs. JTEKT reported consolidated revenue of JPY 1.9249 trillion for the fiscal year ending March 2026, while Nexteer delivered record full-year 2025 revenue of USD 4.6 billion, which shows the scale gap between global Tier-1 suppliers and Russia’s domestic steering base. That scale matters in the Russian automotive EPS market because the next phase of competition depends less on basic mechanical supply and more on electronics, redundancy, software calibration, and production consistency.

Strategic moves in 2026 make that divide clear. ZF is already in series production with a steer-by-wire system for NIO’s ET9 and supplies both the steering wheel actuator and the redundant steering gear actuator, which demonstrates a fully commercial next-generation steering architecture. Nexteer expects to launch 2 steer-by-wire programs in the first half of 2026, which keeps pressure on the Russian automotive EPS market to move toward software-defined and ADAS-ready steering content over time. At the local manufacturing level, the Rulevye Sistemy and Wuhu Sterling joint venture is the clearest strategic move because it tries to bridge global-grade product design and Russian localization needs within one structure. The need for that bridge is reinforced by AvtoVAZ’s rejection of nearly 21,000 Avtoelektronika EPS units in 2025, which showed that local production presence alone does not guarantee acceptable quality.

The main gap in the Russian automotive EPS market lies between global technology leadership and domestic cost-led supply, because no player yet offers fully localized, ADAS-capable EPS at a meaningful scale with proven quality. Hyundai Mobis, Mando, and Mitsubishi Electric still have indirect exposure through supply chains that support Chinese OEM kits rather than through a broad local Russian steering footprint. A wider Chinese Tier-1 expansion into local production would pressure both global incumbents and Russian producers because it could combine lower cost with already proven product portfolios for Chery, Geely, and Li Auto-linked platforms. Compliance barriers still matter, since cybersecurity requirements under UN Regulation No. 155 and ISO 21434 are being folded into Russian standards work and make pure price competition less effective for suppliers without certified electronic safety capability [3]“Cybersecurity Methods for Steer-By-Wire Systems,” IEEE, ieee.org .

Russia Automotive EPS Industry Leaders

Delphi Technologies

Hitachi Astemo, Ltd.

Hyundai Mobis Co., Ltd.

JTEKT Corporation

ZF Friedrichshafen AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: EV brand Evolute showcased its newest all-wheel-drive electric crossover vehicles, pushing the demand for modern, high-torque EPS systems calibrated specifically for electric powertrains.

- February 2026: Murom Machine-Building Plant launched commercial production of electric power steering racks for AURUS premium vehicles and electric portal axles for KAMAZ electric buses in Russia's Vladimir region, supported by Russia's Industrial Development Fund. This marks the first volume EPS rack production program for a Russian-brand premium vehicle, expanding the addressable market for domestically manufactured rack-type EPS beyond the mass-market AvtoVAZ tier.

Russia Automotive EPS Market Report Scope

The scope of the report includes Type (Column Type, Pinion Type, and Dual Pinion Type), Component Type (Steering Rack/Column, Sensor, Steering Motor, and Other Component Types), Vehicle Type (Passenger Cars and Commercial Vehicles), and Propulsion Type (ICE Vehicles, Hybrid Vehicles, and Battery Electric Vehicles).

By Type

| Column Type |

| Pinion Type |

| Dual Pinion Type |

By Component Type

| Steering Rack/Column |

| Sensor |

| Steering Motor |

| Other Component Types |

By Vehicle Type

| Passenger Cars |

| Commercial Vehicles |

By Propulsion Type

| Internal Combustion Engine Vehicles |

| Hybrid Vehicles |

| Battery Electric Vehicles |

| By Type | Column Type |

| Pinion Type | |

| Dual Pinion Type | |

| By Component Type | Steering Rack/Column |

| Sensor | |

| Steering Motor | |

| Other Component Types | |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| By Propulsion Type | Internal Combustion Engine Vehicles |

| Hybrid Vehicles | |

| Battery Electric Vehicles |

Key Questions Answered in the Report

What is the 2031 outlook for electric power steering in Russia?

The Russian automotive EPS market is forecast to reach USD 0.28 billion by 2031 from USD 0.18 billion in 2026, growing at a 9.0% CAGR over 2026-2031.

Which steering type leads current demand in Russia?

Column Type EPS leads current demand with 48.27% share in 2025 because it is deeply embedded in AvtoVAZ-linked passenger vehicle programs.

Which segment is growing fastest in Russia’s EPS space?

Battery electric vehicles are growing fastest by propulsion at 9.32% CAGR during 2025-2030, while sensors lead component growth at 9.23% CAGR as ADAS-ready systems require more electronic content.

Why are Chinese vehicle programs important to steering suppliers in Russia?

Chinese OEM programs bring newer crossover platforms, stronger ADAS compatibility, and new localization partnerships such as the Wuhu Sterling and Rulevye Systemy venture in Togliatti.

What is the biggest near-term risk for EPS suppliers in Russia?

The main near-term risks are cost pressure in entry-level vehicles and semiconductor dependence, since automotive-grade MCUs still remain heavily import dependent, and localization gaps are unresolved.

How important are commercial vehicles for future steering demand in Russia?

Commercial vehicles are smaller currently, but they are projected to grow at a 9.17% CAGR during 2025-2030 as autonomous trucks, electric buses, and fleet electrification increase the need for advanced steering systems.

Page last updated on: