Peracetic Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

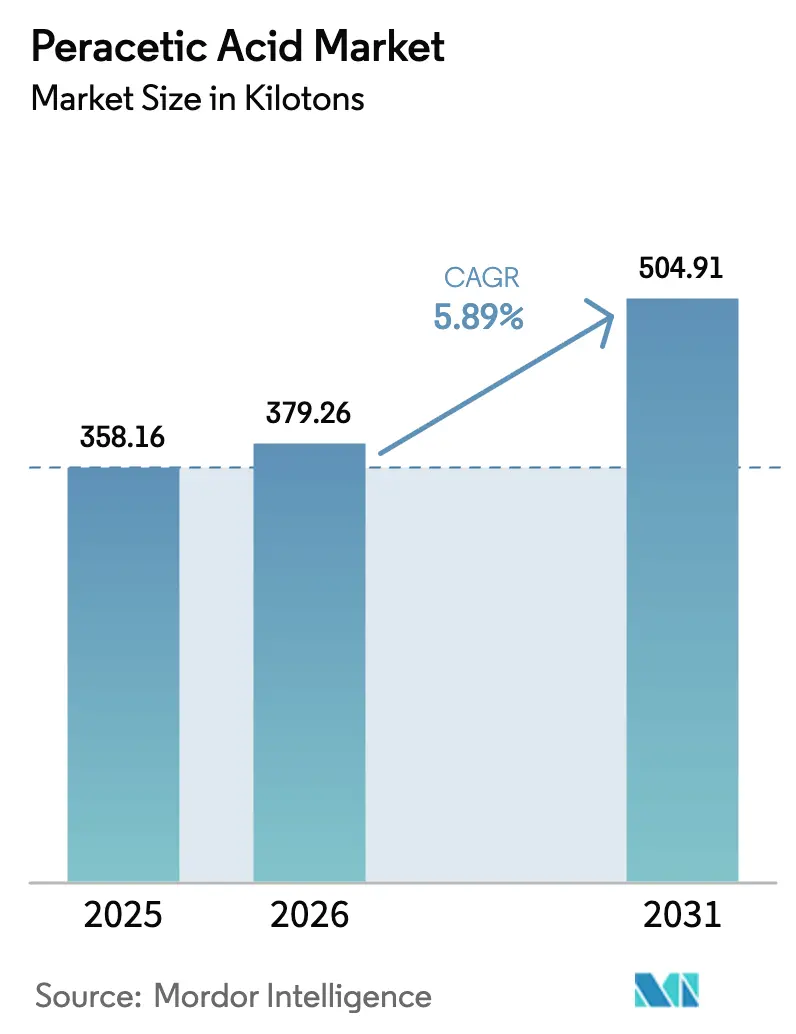

| Market Volume (2026) | 379.26 kilotons |

| Market Volume (2031) | 504.91 kilotons |

| Growth Rate (2026 - 2031) | 5.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peracetic Acid Market Analysis by Mordor Intelligence

The Peracetic Acid Market size is expected to increase from 358.16 kilotons in 2025 to 379.26 kilotons in 2026 and reach 504.91 kilotons by 2031, growing at a CAGR of 5.89% over 2026-2031. Heightened food-safety rules, stricter wastewater discharge limits, and the push toward non-halogenated chemistries have become the decisive growth engines. Large food and beverage processors, municipal utilities, and healthcare facilities are converting chlorine or chlorine-dioxide lines to liquid peracetic acid, which simplifies compliance with pathogen-control mandates and eliminates trihalomethanes. The shift also benefits from hydrogen-peroxide capacity additions in India and China that improve regional feedstock security. Competitive intensity sits at a moderate level because registered no-rinse formulations require significant regulatory investment, making it hard for small suppliers to penetrate branded food and pharmaceutical accounts.

Key Report Takeaways

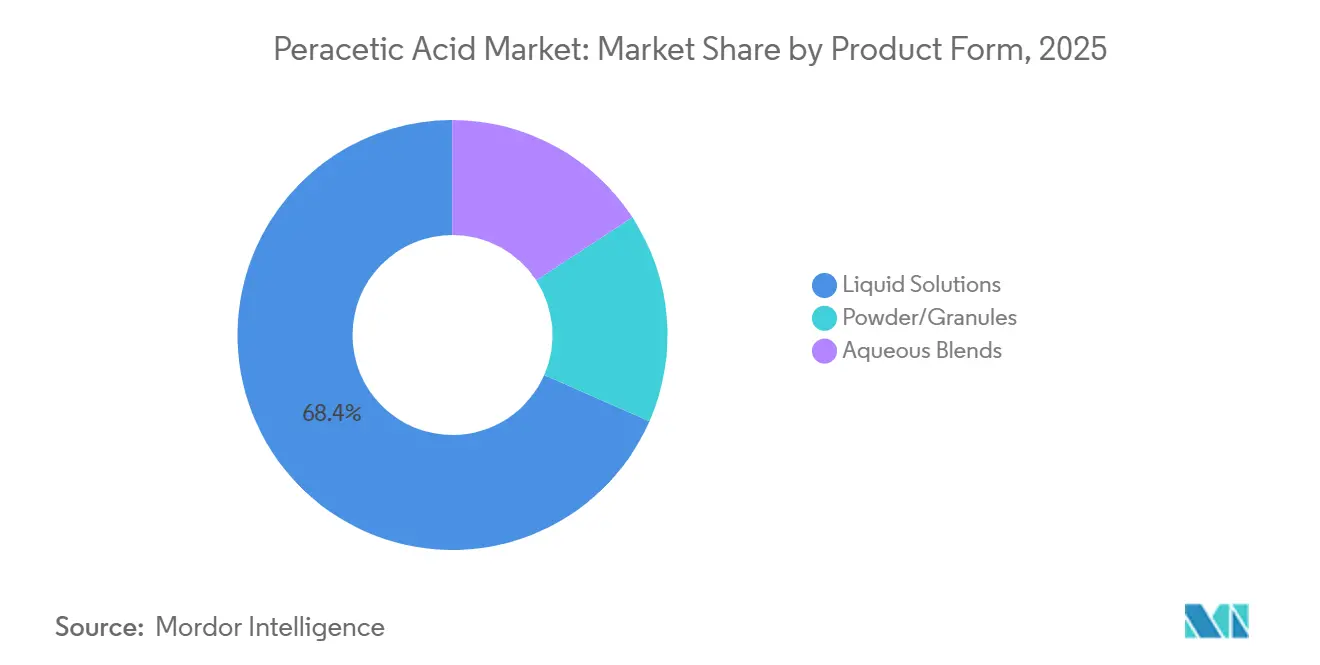

- By product form, liquid solutions led with 68.44% share in 2025; aqueous blends are projected to expand at a 6.12% CAGR to 2031.

- By concentration grade, medium range (5–15% PAA) products accounted for 54.31% of the peracetic acid market share in 2025, while the same grade is forecast to grow at a 6.23% CAGR through 2031.

- By application, disinfectants commanded a 45.89% share of the peracetic acid market size in 2025 and are advancing at a 6.45% CAGR to 2031.

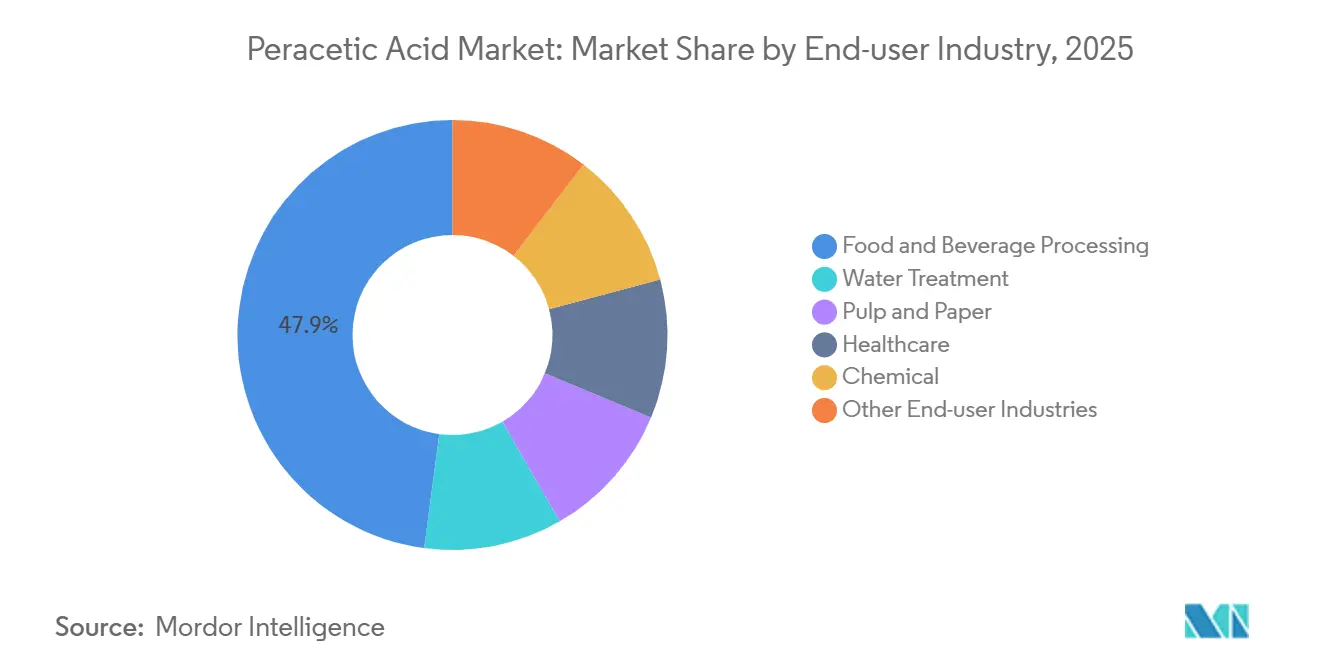

- By end-user industry, food and beverage processing captured a 47.89% share in 2025; the segment is expanding at a 6.44% CAGR to 2031.

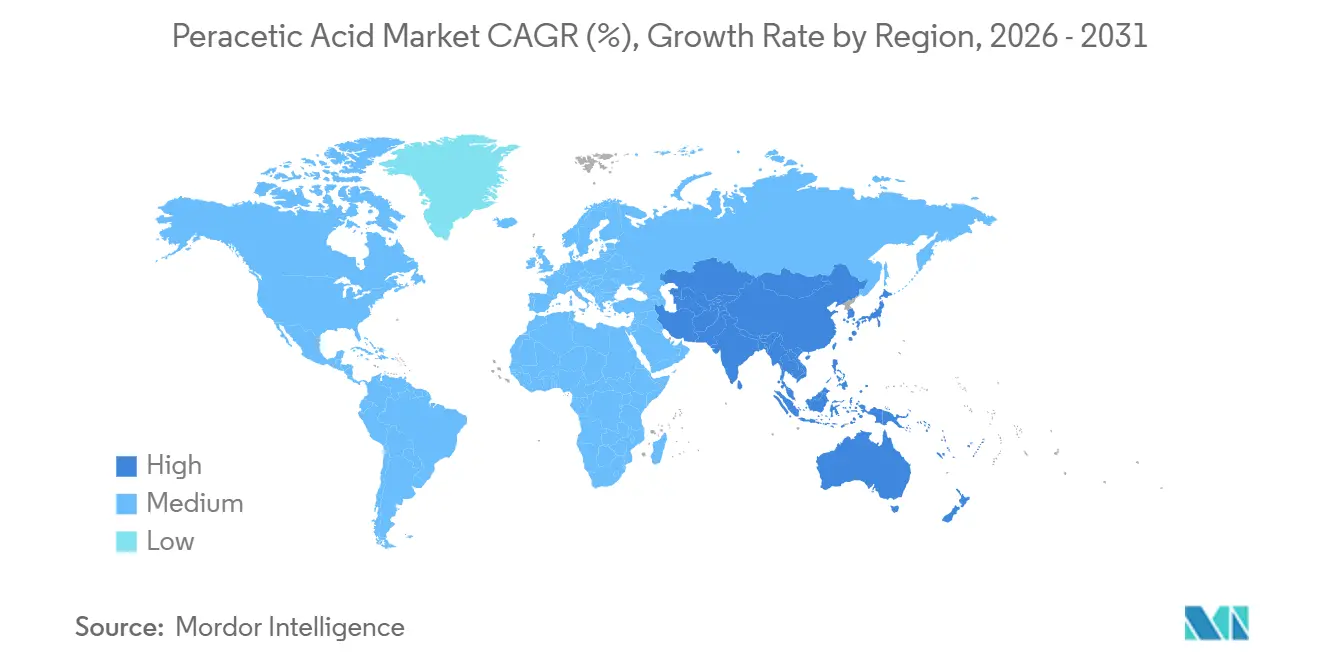

- By geography, Asia-Pacific contributed 38.67% volume in 2025 and is growing at 6.80% CAGR through 2031, outpacing all other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Peracetic Acid Market*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food-safety regulations boosting food and beverage sanitation | +1.8% | Global, with concentration in North America, EU, and APAC urban centers | Medium term (2-4 years) |

| Demand surge from municipal and industrial water treatment | +1.5% | North America, Europe, APAC coastal provinces | Long term (≥ 4 years) |

| Shift from chlorine to eco-friendly pulp bleaching agents | +0.9% | North America, Nordic Europe, Brazil | Long term (≥ 4 years) |

| Growth in low-temperature sterilization of medical devices | +1.1% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| Craft-brewery adoption in cold clean-in-place cycles | +0.6% | North America, Western Europe, Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Food-Safety Regulations Boosting Food and Beverage Sanitation

In 2024-2025, regulators revised rules for direct-contact sanitizers, mandating processors to present validated log-reduction data during third-party audits. The USDA's Food Safety and Inspection Service has now mandated proof of efficacy against Listeria on the surfaces of ready-to-eat meats. Meanwhile, the EU's Biocidal Products Regulation has set a cap on in-plant PAA usage, aligning with no-rinse lines.[1]European Commission, “Biocidal Products Regulation Active-Substance Review,” europa.eu Addressing spoilage losses, India's FSSAI has approved PAA for post-harvest produce. These collective regulations lean toward favoring liquid grades, as processors can utilize them in-line without the need for costly dilution equipment. In light of these developments, equipment manufacturers have integrated real-time sensors to monitor PAA strength, aiding plants in bridging audit gaps and accelerating the adoption of the disinfectant in high-throughput facilities.

Demand Surge from Municipal and Industrial Water Treatment

The U.S. Environmental Protection Agency lowered allowable chlorine residuals in 2024, pushing utilities toward a chemistry that breaks down into oxygen and acetic acid rather than halogenated by-products. Parallel moves in the EU and coastal China added momentum as aquaculture discharge began mixing with urban effluent, making non-halogenated disinfectants attractive. PAA offers 3-log Cryptosporidium control at contact times that match chlorine yet sidesteps trihalomethane limits. Industrial adopters in pulp and food plants also prefer PAA in cooling-tower loops where chlorine dioxide storage generates explosion risks. These factors jointly underpin the 6.45% CAGR projected for disinfectant use through 2031.

Shift from Chlorine to Eco-Friendly Pulp Bleaching Agents

North American and Nordic European mills have begun substituting chlorine dioxide stages with PAA, achieving a significant reduction in adsorbable organic halide loads. This move not only aligns with stringent discharge permits but also aids in securing premium certifications from the Forest Stewardship Council. Despite PAA's higher cost compared to in-situ chlorine dioxide, integrated mills, burdened by hefty environmental fees, deem the transition economically viable. Brazil's eucalyptus pulp producers conducted PAA trials to align with European Union deforestation compliance mandates. However, widespread adoption is contingent on the domestic availability of hydrogen peroxide. As a result, while there's a notable uptick in volume, it's predominantly seen in the high-margin specialty pulp sector, rather than in commodity grades.

Growth in Low-Temperature Sterilization of Medical Devices

In 2024, hospitals ramped up installations of automated PAA sterilizers. This shift was driven by the realization that steam autoclaves can degrade both flexible endoscopes and robotic tools. With cycle times below 55 °C, hospitals can now achieve same-day device turnarounds, effectively alleviating procedure backlogs. The CDC has reclassified PAA as a high-level disinfectant, endorsing its use for sterilization. Meanwhile, Japan’s health ministry has expanded PAA approvals to include pharmaceutical cleanrooms. In a strategic move, Mitsubishi Gas Chemical has restructured its hygiene group to target the hospital sector. However, overall consumption remains modest.

Restraints Impact Analysis of Peracetic Acid Market*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Occupational hazards and handling challenges | -0.7% | Global, acute in regions with limited industrial hygiene infrastructure | Short term (≤ 2 years) |

| High cost versus chlorine-based substitutes | -0.9% | Price-sensitive markets in South America, Middle East, Africa, and South Asia | Medium term (2-4 years) |

| Volatility of key precursors (acetic anhydride, H₂O₂) | -0.6% | Global, with supply concentration in China and Gulf Cooperation Council states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Occupational Hazards and Handling Challenges

Under OSHA rules, PAA concentrations exceeding 15% are deemed corrosive, necessitating secondary containment and personal protective equipment[2]Occupational Safety and Health Administration, “Peracetic Acid Safety Protocols,” osha.gov. Heat speeds up PAA decomposition, and retrofitting with vented storage tanks can inflate budgets. Such financial and safety challenges are particularly burdensome for small processors in emerging economies, hindering their global expansion.

High Cost Versus Chlorine-Based Substitutes

In 2025, liquid PAA commanded prices significantly higher than sodium hypochlorite. Despite this premium, many utilities across Latin America and the Middle East continue to favor hypochlorite. This preference stems from the total cost of ownership for PAA, which, when factoring in training and storage, remains higher over a decade. Furthermore, early 2024 price hikes in Europe exacerbated this price gap, leading to delays in transitioning to PAA for pulp bleaching and industrial water treatment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Peracetic Acid Market Segment Analysis

By Product Form (Liquid Solutions Dominate Ease of Use Applications)

Liquid solutions accounted for 68.44% volume in 2025, reflecting compatibility with legacy dosing pumps across food plants and wastewater treatment works. This dominance anchors the peracetic acid market size at the plant-level because retrofits involve little more than adjusting metering rates. Demand for aqueous blends is rising at a 6.12% CAGR because stabilizers inside these blends reduce corrosion on stainless steel in aseptic packaging lines.

Aqueous formats appeal to greenfield dairy, juice, and pharmaceutical plants that order integrated monitoring hardware. Powder and granule forms hold a niche share, mainly disaster-relief sanitation and seasonal pond treatment, where lower freight cost outweighs the need for on-site dissolution. Suppliers continue to focus research and development on extending blend shelf life, because longer storage pairs well with global shipping lanes and remote users. Consequently, liquid solutions will keep a majority share, though gains for blends will chip away at the margin as new installations favor corrosion-mitigated chemistries.

By Concentration Grade (Medium Range Balances Efficacy and Safety)

Medium Range (5–15% PAA) held 54.31% volume in 2025 and is projected to grow at a 6.23% CAGR through 2031, ensuring the highest peracetic acid market share among concentration tiers. The grade achieves a rapid microbial kill, sidestepping the stringent handling rules that come into play for concentrates exceeding 15%. In 2024, the FDA issued guidance indicating that processors can attain validated reductions in just 60 seconds with this concentration, underscoring its appeal for fast-paced meat and dairy operations.

Municipal plants, equipped with automated dilution skids, predominantly utilize high-concentration products. Lower-concentration grades are favored for washing post-harvest produce, thanks to their no-rinse properties and lenient transportation regulations. However, widespread adoption of high-concentration products faces hurdles; the need for additional ventilation and storage drives up net savings, making them less attractive. In the grand scheme, while medium concentrations are set to maintain their dominance, users are increasingly gravitating towards either end of the spectrum—dilute or concentrate—tailoring their choice to specific applications.

By Application (Disinfectants Lead Growth Across Water and Food Sectors)

Disinfectants occupied 45.89% of 2025 demand and are advancing at a 6.45% CAGR, anchoring the fastest-growing line within the peracetic acid market. Water utilities select PAA to meet 0.011 mg/L chlorine residual caps while maintaining 3-log Cryptosporidium control. In food plants, daily clean-in-place cycles consume liters of solution, dwarfing the milliliter volumes used for hospital sterilant cycles.

Sterilants, though smaller in tonnage, yield premium pricing due to stringent validation in hospitals and pharmaceutical suites. Oxidizer demand in pulp mills is rising only where discharge permits penalize chlorine dioxide. Bleaching agents for textiles and agriculture make up residual niches with flat volume trajectories. Suppliers, therefore, frame marketing around turnkey disinfectant packages that bundle real-time probes and cloud data logging, enabling end users to certify performance without adding headcount.

By End-User Industry (Food and Beverage Processing Anchors Demand)

Food and beverage processors controlled 47.89% of the 2025 volume and are set for a 6.44% CAGR through 2031, the fastest track among all industries. Daily sanitation frequency, strictly enforced hazard-analysis programs, and ample capital budgets allow rapid changeovers from chlorine to PAA. Cold clean-in-place adoption in craft breweries and energy-intensive dairy plants deepens chemical demand by eliminating the need for heated caustic rinses.

Water treatment ranks second, driven by municipal retrofit projects funded under state revolving loan programs in the United States and similar mechanisms in Europe. Pulp and paper, under pressure to cut AOX emissions, employs PAA for premium brightness grades but still represents smaller volumes. Healthcare’s device-reprocessing niche enjoys double-digit value growth; however, absolute tonnage remains low because a hospital uses only a few hundred liters per year. Aquaculture and agriculture form emerging micro-segments where residue-free treatment mitigates antibiotic resistance concerns.

Geography Analysis

APAC Peracetic Acid Market

Asia-Pacific captured 38.67% of the 2025 volume and is growing at a 6.80% CAGR, the fastest regional trajectory. New hydrogen-peroxide capacity in Gujarat and Shanghai shortens supply lines and trims delivered costs for local formulators. China’s tougher biochemical-oxygen-demand limits push coastal cities to favor PAA over sodium hypochlorite, especially where aquaculture discharge merges with municipal wastewater. India’s food regulators backed PAA for fruit and vegetable treatment, opening a high-volume channel because cold-chain gaps cause double-digit spoilage losses. Japan broadened pharmaceutical approvals, moving the chemistry into cleanroom disinfection work.

North America and Europe Peracetic Acid Market

North America and Europe represent mature but steady terrain. The U.S. EPA’s tighter residual-chlorine ceiling in 2024 triggered spending on injection skids, yet infrastructure turnover limits growth to mid-single digits. European suppliers face energy-linked cost inflation, slowing switches in price-sensitive pulp bleaching, although Article 95 listing under the EU Biocidal Products Regulation reinforces long-term confidence. Craft breweries on both continents improved efficiency by embracing cold PAA CIP, cutting energy and water use.

South America and MEA Peracetic Acid Market

South America, the Middle East, and Africa remain volume laggards because budget constraints favor cheaper chlorination. Brazil’s premium eucalyptus pulp segment is piloting PAA to satisfy European buyers wary of deforestation, yet full commercialization depends on affordable feedstock. Gulf State desalination projects allocated funds for PAA biocide dosing, indicating incremental gains where energy-free disinfection aligns with low-temperature reverse-osmosis pretreatment. Across these regions, regulatory gaps and capital scarcity temper the pace of adoption.

Competitive Landscape

The market is moderately fragmented. Integrated Asian producers leverage captive hydrogen-peroxide units to discount price, but they often lack the documentation and field support required by global beverage or hospital auditors. Pricing power fluctuates with feedstock. Evonik raised European tags by 8–12% in March 2024 after electricity costs inflated hydrogen-peroxide margins. Conversely, vertically integrated Indian and Chinese firms passed through only modest increases, capturing regional share. The strategic picture emphasizes product stewardship, real-time monitoring tech, and regulatory alignment over brute volume expansion.

Peracetic Acid Industry Leaders

Enviro Tech Chemical Services, Inc.

Solvay

Evonik Industries AG

Ecolab

Kemira

- *Disclaimer: Major Players sorted in no particular order

Peracetic Acid Market Companies Covered in this Report

- ACURO ORGANICS LIMITED

- Aditya Birla Chemicals

- Airedale Group

- Biosan

- Brainerd Chemical

- Christeyns

- Diversey, Inc.

- Ecolab

- Enviro Tech Chemical Services, Inc.

- Evonik Industries AG

- Hydrite Chemical

- Jubilant Pharmova Limited

- Kemira

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- Solvay

- STOCKMEIER Group

Recent Industry Developments in Peracetic Acid Market

- December 2023: Evonik has completed its acquisition of Thai Peroxide Company Limited, strengthening its portfolio of specialty-grade peracetic acid in the Asia-Pacific region. This strategic move is expected to enhance Evonik's market position and drive growth in the regional peracetic acid market.

- May 2023: Evonik has introduced VIGOROX Trident, a peracetic acid biocide approved by the U.S. EPA for use in recirculating aquaculture systems. This development is expected to strengthen the peracetic acid market by driving demand in the aquaculture industry and expanding its application scope.

Peracetic Acid Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the global peracetic acid market as all commercial grades of peroxyacetic acid that are shipped as stabilized liquid concentrates, aqueous blends, or generated on-site systems and sold into food and beverage sanitation, healthcare sterilization, water treatment, pulp and paper bleaching, and related industrial cleaning. According to Mordor Intelligence analysts, volumes are expressed in kilotons at one hundred percent active equivalent, which allows a fair comparison across grades.

Scope exclusion: Captive peracetic acid produced and consumed within integrated chemical complexes, mixed oxidizers containing under one percent PAA, and sales of precursor acetic acid or hydrogen peroxide are outside this study.

Segments Covered in This Report

- By Product Form

- Liquid Solutions

- Powder / Granules

- Aqueous Blends

- By Concentration Grade

- Less than 5% PAA (Low)

- 5–15% PAA (Medium)

- More than 15% PAA (High)

- By Application

- Disinfectant

- Oxidizer

- Sterilant

- Other Applications (Bleaching Agent, Sanitizer, etc.)

- By End-user Industry

- Food and Beverage Processing

- Water Treatment

- Pulp and Paper

- Healthcare (including Pharmaceutical)

- Chemical

- Other End-user Industries (Agriculture and Aquaculture, etc.)

- By Geography (Volume)

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Primary Research

Structured interviews with formulators, contract sanitation providers, plant managers, and regional safety inspectors across Asia-Pacific, Europe, and the Americas helped us confirm capacity-utilization shifts, average selling prices, and adoption triggers that secondary sources rarely quantify.

Desk Research

We gathered trade and regulatory statistics from tier-one public sources such as United States Environmental Protection Agency disinfectant registrations, Eurostat Prodcom chemical output panels, FAO hygiene codes, World Bank wastewater-treatment penetration series, and peer-reviewed articles on PubMed. Company 10-K filings, investor decks, and tender logs enriched business intelligence and were complemented by D and B Hoovers and Dow Jones Factiva screening. The sources named are illustrative, and many other references informed data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down demand pool was built from disinfectant and oxidizer spending in water treatment, food and beverage, and low-temperature medical sterilization and then converted to active-ingredient volumes through typical concentration factors. Supplier roll-ups and channel checks offered a bottom-up cross-check that adjusted for captive output leaks. Key variables such as municipal wastewater throughput, new beverage-bottling lines, surgical-procedure growth, median five-to-fifteen percent grade share, and spot acetic-acid price trends fed a multivariate regression forecast to 2030. Where supplier data were incomplete, regional trade flows bridged the gap.

Data Validation & Update Cycle

Model outputs pass variance checks against historical trade, price, and capacity curves and then move through a two-step peer review before sign-off. Reports refresh every twelve months, with interim updates for material regulatory or merger events, and a last-minute analyst sweep ensures clients receive the freshest view.

How Mordor Intelligence's Peracetic Acid Market Size Compares to Other Published Estimates

Published estimates frequently diverge because firms choose different grade mixes, currency years, and refresh speeds.

Mordor's disciplined scope, mixed-method model, and annual update cadence make our baseline dependable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 375.8 kt (2025) | Mordor Intelligence | - |

| USD 1.03 bn (2024) | Global Consultancy A | Reports value not volume and mixes blended oxidizers, inflating totals |

| USD 0.94 bn (2024) | Industry Journal B | Omits on-site generation units and relies on 2019 exchange rates |

| USD 1.11 bn (2025) | Regional Consultancy C | Counts captive production as merchant sales, risking double counting |

These contrasts show that the Mordor Intelligence baseline is balanced, transparent, and traceable to clear variables that are refreshed in a disciplined cycle, giving decision makers a reliable starting point.

Key Questions Answered in the Report

What is the current global demand for peracetic acid in 2026?

The peracetic acid market size in 2026 is 379.26 kilotons.

How fast is demand expected to grow through 2031?

Volume is projected to reach 504.91 kilotons by 2031, equating to a 5.89% CAGR.

Which application category is expanding the quickest?

Disinfectant use is advancing at a 6.45% CAGR as utilities and food plants replace chlorine.

Why do processors prefer medium-concentration products?

Grades in the 5–15% range balance rapid microbial kill with easier handling rules, holding 54.31% share in 2025.

Which region offers the strongest growth prospects?

Asia-Pacific leads with 6.80% CAGR through 2031 due to local feedstock expansion and tighter wastewater regulations.

Page last updated on: