Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

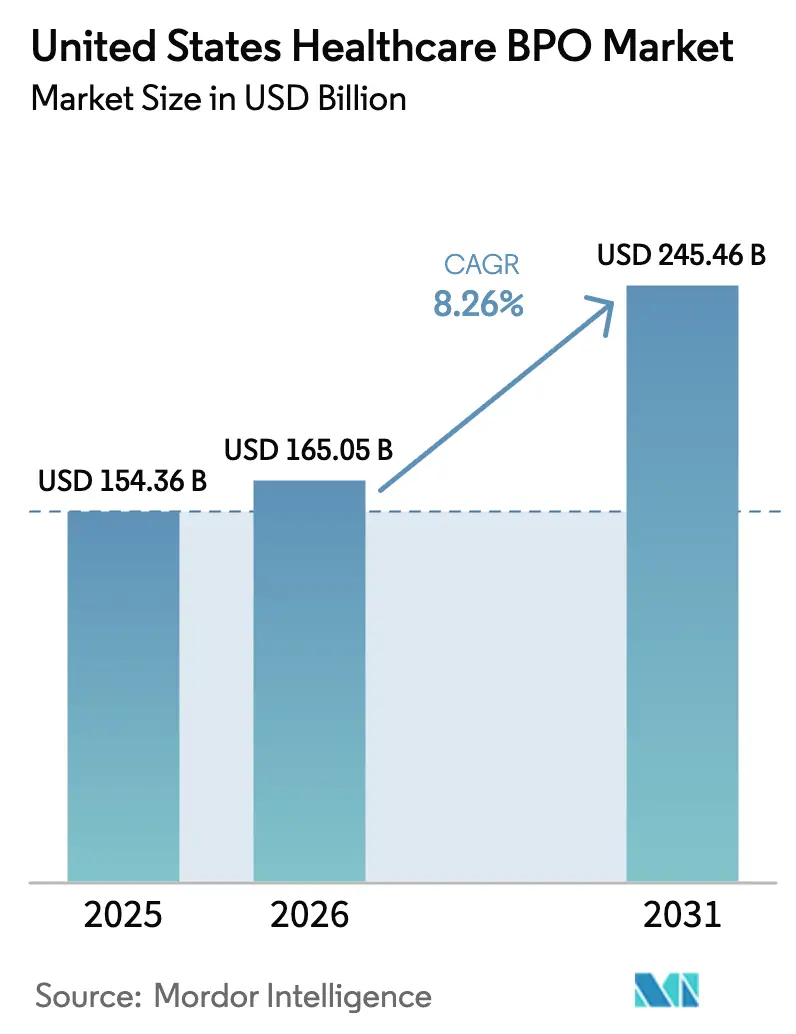

| Base Year Market Size (2025) | USD 154.36 Billion |

| Market Size (2026) | USD 165.05 Billion |

| Market Size (2031) | USD 245.46 Billion |

| Growth Rate (2026 - 2031) | 8.26% CAGR |

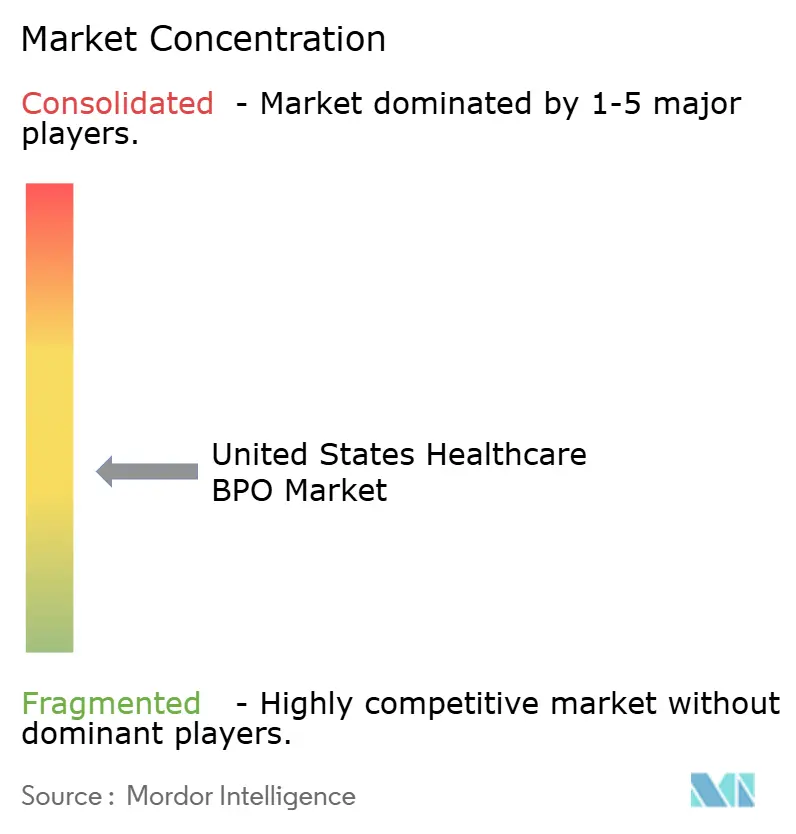

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Healthcare BPO Market Analysis by Mordor Intelligence

The United States Healthcare BPO Market size is expected to grow from USD 154.36 billion in 2025 to USD 165.05 billion in 2026 and is forecast to reach USD 245.46 billion by 2031 at 8.26% CAGR over 2026-2031.

The current expansion is driven by rising administrative complexity, broad AI adoption, and payer-provider cost pressures, all of which are steering spend toward specialized outsourcing partners. Organizations increasingly turn to offshore and nearshore vendors that combine real-time interoperability, robust cybersecurity, and large-scale automation to keep pace with tightening reimbursement cycles and growing volumes of eligibility verification, prior authorization, and claims adjudication. A surge in Medicaid reenrollments, escalating denial rates at hospitals, and new CMS interoperability rules are boosting demand for end-to-end eligibility processing and API-driven prior-authorization services. Private-equity investments and vendor consolidation are intensifying competition, prompting service providers to differentiate through generative-AI tooling, FHIR-compliant platforms, and hybrid engagement models that balance on-shore oversight with offshore execution. At the same time, wage inflation in India and the Philippines and new U.S. tariffs on IT hardware are eroding cost arbitrage, accelerating the pivot to nearshore centers in Mexico and Central America.

Key Report Takeaways

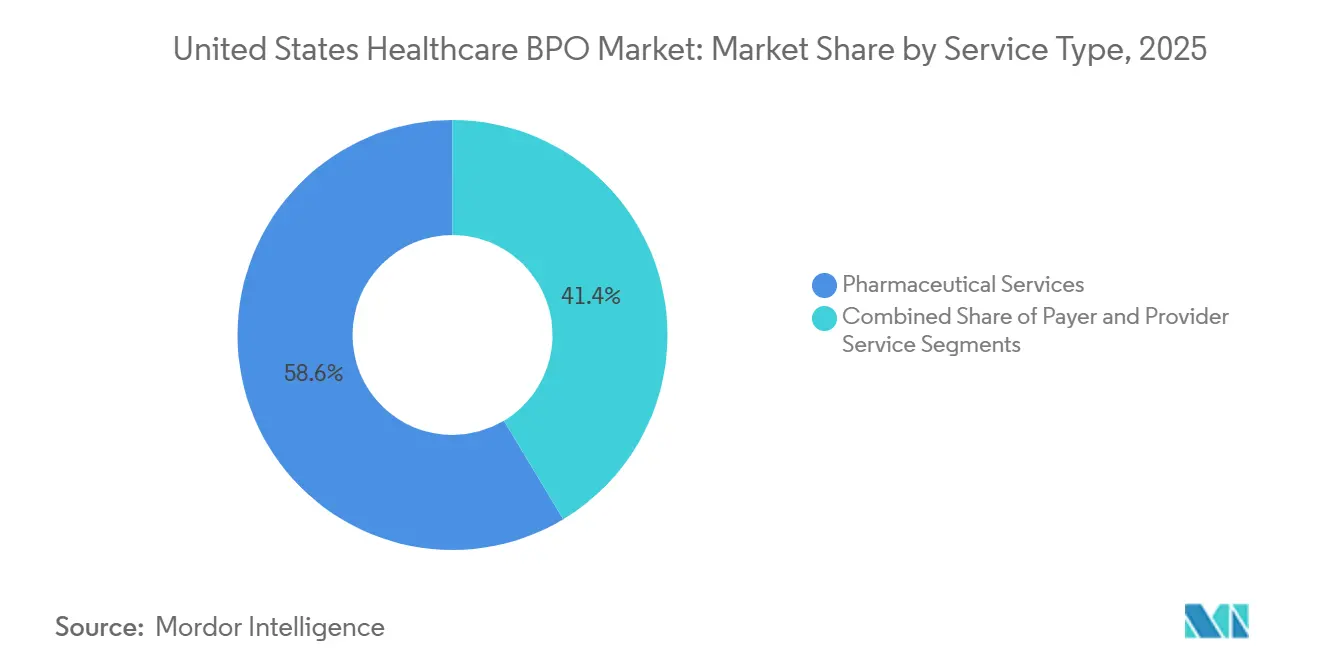

- By service type, Pharmaceutical Services led with 58.62% of United States healthcare BPO market share in 2025. Provider Services are forecast to expand at a 12.73% CAGR between 2026-2031.

- By delivery model, Offshore Delivery held 81.35% share of the United States healthcare BPO market size in 2025. Nearshore Delivery is projected to grow at a 12.32% CAGR through 2031.

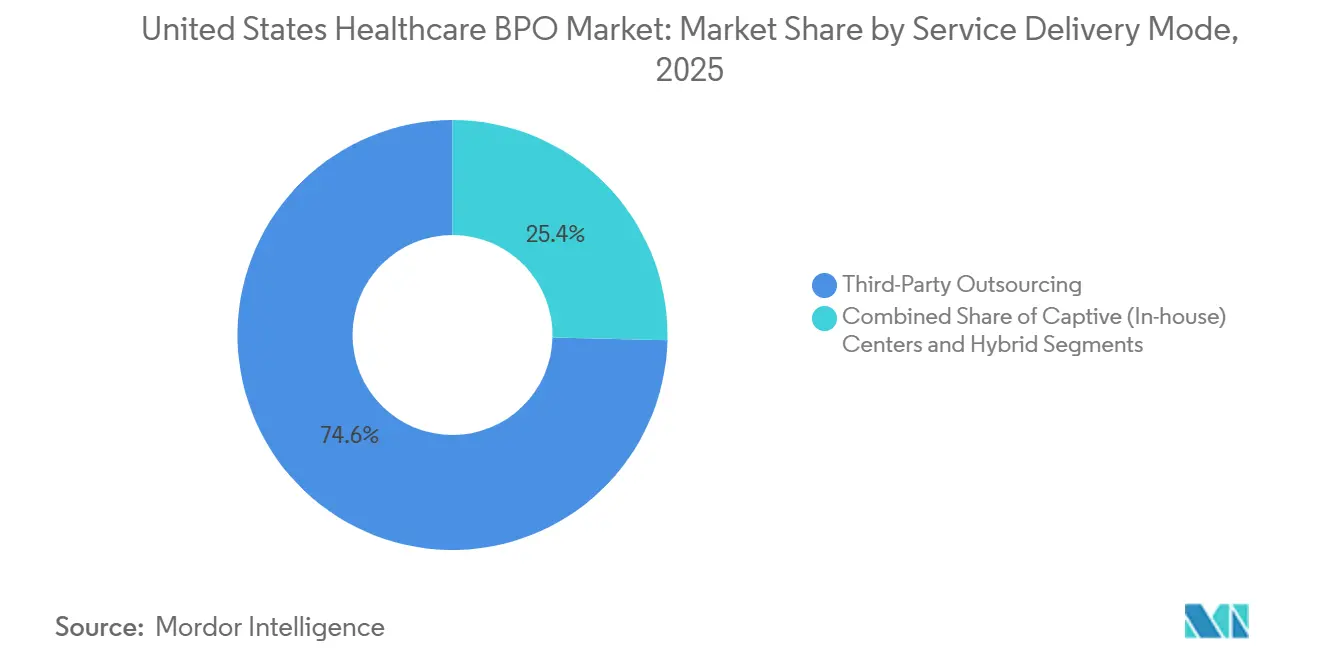

- By service delivery mode, Third-Party Outsourcing accounted for 74.62% share of the United States healthcare BPO market size in 2025. Hybrid Co-sourcing is advancing at an 11.63% CAGR through 2031.

- By end customer, Healthcare Payers held 44.22% of the United States healthcare BPO market share in 2025. Government Agencies are expected to register a 10.53% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Healthcare BPO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating administrative-cost pressure | +1.8% | National, highest in Northeast and West Coast markets | Medium term (2-4 years) |

| Advanced tech adoption (AI, RPA, analytics) | +2.1% | National, led by large integrated delivery networks and national payers | Short term (≤ 2 years) |

| Heightening regulatory complexity | +1.3% | National, acute in states with additional privacy laws | Long term (≥ 4 years) |

| Surge in BPaaS uptake by regional payers | +0.9% | Midwest and Southeast markets | Medium term (2-4 years) |

| Medicaid redetermination backlog | +1.0% | State-level, highest in Texas, Florida, North Carolina | Short term (≤ 2 years) |

| Generative-AI prior-auth & coding adoption | +1.5% | National, concentrated among multi-hospital health systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Administrative-Cost Pressure on Payers & Providers

Hospitals spend USD 19.7 billion each year disputing denied claims, with 2025 denial rates ranging from 11.8% to 19%, pushing CFOs to outsource revenue-cycle tasks to variable-fee partners that can cut fixed labor and improve cash collections. National health expenditure reached USD 4.9 trillion in 2023 and is projected to rise at 5.8% annually through 2033, magnifying workloads related to eligibility verification, prior authorization, and claims adjudication.[3]Centers for Medicare & Medicaid Services, “National Health Expenditure Data: Historical,” cms.gov Commercial reimbursement growth continues to lag medical-cost inflation by 150-200 basis points, squeezing provider margins and making non-clinical outsourcing unavoidable. Nearly half of rural hospitals posted operating losses in 2023-2024, and more than 600 facilities remain at high financial risk, so revenue-cycle BPO is becoming a lifeline for sustaining patient services. Payers face similar pressure as medical loss ratios hover near regulatory ceilings; nine of the 10 largest U.S. health plans already rely on Conduent for claims and member operations.

Advanced Tech Adoption (AI, RPA, Analytics) Unlocking Scale Efficiencies

Generative-AI is collapsing review cycle times and staff hours across prior authorization, appeals, and utilization-management workflows. HCLTech showed that its GenAI solution can cut clinical-review time from three hours to 20 minutes and reduce costs by 30% for a regional Blue Cross plan. A 1-million-member insurer typically spends USD 50-70 million on clinical-review labor and maintains 200-300 nurse FTEs; GenAI-powered extraction and summarization now let nurses validate decisions instead of gathering documents, shrinking staffing needs. Optum Real, rolled out in April 2024, enables instant coverage validation, and early pilots at Allina Health recorded lower administrative errors and better patient experience. Cognizant’s BPaaS platform blends RPA and machine learning to deliver 25-50% reductions in total cost of ownership, while EmblemHealth reported a 99% improvement in claims-first-pass yield after deployment. IBM Consulting says biopharma clients now close regulatory documentation cycles 50-75% faster by using generative AI for content-heavy workflows.

Heightening Regulatory Complexity

CMS finalized its Interoperability and Prior Authorization Rule in January 2024, compelling payers to provide urgent prior-authorization decisions within 72 hours and standard ones within seven days by January 2026, or outsource compliance to BPO partners with FHIR-ready APIs. Plans must also supply specific denial reasons and guidelines, triggering additional documentation overhead that favors automated clinical-review platforms offered by large vendors. State privacy laws in California, Virginia, and Colorado impose stricter timelines and consent requirements than HIPAA, so BPO providers now maintain jurisdiction-specific data-governance playbooks. The February 2024 Change Healthcare breach exposed 192.7 million records and cost UnitedHealth Group USD 2.4 billion, prompting payers to demand SOC 2 Type II reports, annual penetration tests, and USD 50-100 million cyber-insurance coverage from outsourcing partners. These mandates raise operating costs and create high entry barriers, tipping share toward vendors with dedicated security operations centers.

Surge in BPaaS Adoption by Small & Mid-Size Payers

Regional insurers with 100,000-500,000 members are shifting from FTE-based contracts to Business Process as a Service subscriptions that bundle automation, cloud platforms, and variable labor. Cognizant’s BPaaS suite unites policy administration, claims, and self-service on a single cloud instance, enabling payers to launch products without large capital outlays. Legacy on-premise platforms near end-of-life make in-house upgrades unaffordable; BPaaS vendors absorb licensing and infrastructure costs and pass them on through predictable per-member fees. Small payers also gain analytics tools they could not build internally; Cognizant’s BigDecisions provides claim-accuracy models once reserved for national carriers. Medicaid managed-care organizations see immediate benefit, yet long-term switching costs rise as workflows lock into proprietary stacks, reinforcing vendor stickiness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security and data-privacy concerns | -0.7% | National, heightened in California, New York, Massachusetts | Short term (≤ 2 years) |

| Shrinking offshore cost arbitrage | -0.5% | National, affecting vendors with >70% offshore FTE | Long term (≥ 4 years) |

| U.S. tariffs inflating imported IT hardware | -0.3% | National, indirect cost pass-through | Medium term (2-4 years) |

| Vendor consolidation raising lock-in risk | -0.4% | Regional, acute for rural hospital systems and small payers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security & Data-Privacy Concerns Post-Breach

The Change Healthcare ransomware attack disrupted claims for thousands of providers, exposed nearly 200 million records, and triggered a reassessment of vendor cyber-risk protocols. A 2024 JAMA study counted 566 breaches affecting 170 million records, with ransomware responsible for 69% of compromised data. HHS’s Office for Civil Rights issued HIPAA settlements totaling USD 875,000 in 2024 alone, underscoring rising enforcement. Payers now require vendors to hold SOC 2 Type II attestations, independent penetration tests, and high-limit cyber-insurance, raising the cost of entry for small offshore suppliers. Conduent’s January 2025 security incident heightened concerns and spotlighted the need for transparent incident-response playbooks. Several states are considering legislation mandating minimum cybersecurity standards for healthcare BPO vendors, which would further favor large providers with mature security operations.

Shrinking Offshore Cost Arbitrage Amid Tariffs

Wage inflation in India and the Philippines is chipping away at historical cost advantages, while Section 301 tariffs add 50% duties on semiconductors in 2025 and 100% on medical gloves by 2026, inflating offshore center operating expenses. These cost pressures narrow the gap versus nearshore facilities in Mexico and Costa Rica, where cultural affinity and time-zone alignment improve service quality. As a result, Nearshore Delivery is slated to grow 12.32% annually from 2026-2031. Offshore vendors are scrambling to open nearshore hubs, yet the capital outlay and workforce retraining required to pivot geographies will squeeze margins over the next two years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Pharma Dominance, Provider Momentum

Pharmaceutical Services accounted for 58.62% of United States healthcare BPO market share in 2025, anchored by clinical-trial management, regulatory documentation, and manufacturing quality assurance as sponsors accelerate drug-development timelines. IQVIA logged USD 15.4 billion in 2024 revenue and carried a USD 32 billion backlog, illustrating unrelenting demand for contract-research capacity. FDA guidance on decentralized clinical trials released in September 2024 expands the outsourcing remit to remote monitoring and home-health components, driving new use cases. Provider Services, however, are projected to grow fastest at a 12.73% CAGR between 2026-2031 as hospitals battle denial rates of up to 19% and rising cost-to-collect, pushing them toward full-service revenue-cycle partners. The United States healthcare BPO market size for provider-oriented deals is set to accelerate sharply as health systems seek end-to-end claims, coding, and patient-financial-engagement solutions.

Pharma outsourcing continues to diversify beyond clinical research into supply-chain logistics, batch-record reviews, and omnichannel sales enablement, responding to stricter 21 CFR Part 11 data-integrity enforcement. Manufacturing-support BPO is particularly attractive for small biotech firms that lack validated quality-assurance systems. Conversely, Payer Services remain a stable mid-market niche where entrenched relationships between national insurers and platform-centric vendors constrain churn. Cognizant’s TriZetto alone handles billions of transactions for 650 plans, reinforcing stickiness through deep system integration. Overall, the United States healthcare BPO market continues to reward vendors that marry domain expertise with scalable technology rather than pure labor arbitrage.

By Delivery Model: Offshore Stronghold, Nearshore Upswing

Offshore Delivery commanded 81.35% of 2025 spending, reflecting two decades of vendor investment in HIPAA-ready centers across India and the Philippines. Yet erosion in labor-cost differentials and tariff-driven hardware inflation are tilting growth toward nearshore locations, where the United States healthcare BPO market size is poised to expand swiftly. Nearshore centers offer same-day time-zone support, lowering hand-off latency between payers, providers, and BPO teams. The February 2024 breach intensified scrutiny of offshore cybersecurity controls, and payers now favor proximity for easier audits and real-time incident response.

Onshore Delivery remains essential for high-complexity clinical services that require licensed nurses and direct provider interaction. Optum blends onshore clinical oversight with offshore transaction processing to balance quality and cost. Offshore majors like Cognizant and Genpact are racing to establish nearshore hubs, yet capital investments in Mexico and Colombia will dampen margins in the short term. Hybrid delivery models that orchestrate onshore oversight, nearshore execution, and offshore bulk processing are becoming the norm, forcing vendors to invest in platform orchestration and real-time workflow management.

By Service Delivery Mode: Third-Party Scale, Hybrid Flexibility

Third-Party Outsourcing held 74.62% of 2025 spend because it gives payers and providers instant access to specialized talent and automation without heavy capital commitments. The United States healthcare BPO market is now witnessing a robust shift toward Hybrid Co-sourcing, forecast to grow 11.63% annually through 2031, as mid-tier insurers keep sensitive analytics in-house while offloading volume-driven transactions. Optum’s Q3 2024 Insight revenue of USD 5 billion, up 27% year-over-year, signals widening adoption of integrated analytics-plus-services contracts.

Captive centers still exist among mega-payers and integrated delivery networks that can afford end-to-end control; UnitedHealth Group’s Optum hubs in Hyderabad and Manila serve its internal claims platform at scale. Yet captives tie up capital and lack elasticity during seasonal surges, leading smaller organizations to favor variable-fee models. Vendor consolidation—R1 RCM’s USD 8.9 billion take-private in August 2024 and New Mountain Capital’s USD 2 billion acquisition of Access Healthcare in January 2025—gives top players the heft to offer SaaS-like BPaaS subscriptions that further blur the lines between software and services. As a result, hybrid engagements that mix client ownership of data science with outsourced transaction processing will dominate new deals.

By End Customer: Payers Lead, Government Accelerates

Healthcare Payers captured 44.22% of 2025 client spend, leveraging outsourcing to control administrative ratios as medical loss ratios approach regulatory caps. Cognizant’s TriZetto and Conduent’s MMIS solutions form the backbone for hundreds of plans, ensuring a steady revenue stream for platform-centric vendors. Government Agencies are the fastest-growing buyer cohort, with a 10.53% CAGR projected to 2031, propelled by state MMIS modernization and federal program-integrity outsourcing. Conduent’s wins in Alaska and New Mexico showcase government appetite for turnkey eligibility and payment-integrity contracts.

Providers continue to outsource revenue-cycle, patient-access, and care-coordination functions as denial rates climb and labor shortages intensify. Optum manages USD 75 billion in patient revenue, and Cognizant processes billions of transactions for more than 875,000 clinicians. Pharmaceutical and biotech companies outsource trial coordination, regulatory submissions, and supply-chain tasks to speed drug launches; IQVIA’s USD 32 billion backlog signals sustained momentum.

Geography Analysis

Regional dynamics play a decisive role in how the United States healthcare BPO market evolves. The Northeast and West Coast generate outsized demand due to high health-care costs and strict state privacy rules, such as California’s Consumer Privacy Act, which require specialized breach-notification and consent-management workflows. California, New York, and Massachusetts together account for more than 30% of national healthcare spending and host headquarters for many national payers and integrated delivery networks, creating dense outsourcing clusters. The Change Healthcare breach spurred stronger state enforcement, favoring vendors with advanced security apparatus.

The Midwest and Southeast, characterized by numerous regional plans and Medicaid managed-care organizations, are heavy adopters of BPaaS contracts. These regions saw the sharpest Medicaid disenrollments in 2024, driving urgent eligibility-processing deals. Texas, Florida, and North Carolina rely on BPO vendors for document verification and member outreach as they work through backlogs. Rural markets in the Great Plains, Appalachia, and the Deep South continue to grapple with financially distressed hospitals; revenue-cycle outsourcing offers a path to financial stabilization when local staff resources are scarce.

Academic medical centers in Boston, Philadelphia, Baltimore, and San Francisco are early adopters of generative-AI–powered revenue-cycle automation, piloting real-time claim adjudication and denial prevention with vendors such as Optum and Cognizant. Alaska and New Mexico illustrate the growing role of state governments in outsourcing; multi-year MMIS modernization contracts funnel large value pools toward a handful of compliant vendors. Uneven state-level privacy and cybersecurity enforcement underscore the need for BPO providers to maintain centralized compliance offices and multi-state credentials.

Competitive Landscape

The United States healthcare BPO market features moderate consolidation, with the 10 largest vendors—Optum, Cognizant, Conduent, R1 RCM, Genpact, IQVIA, EXL, Accenture, Firstsource, and HCLTech—controlling roughly half of the revenue. Meanwhile, hundreds of niche providers serve specialized functions or regional clients. Competition splits along two vectors: broad horizontal integration across payer, provider, and pharma segments versus deep vertical specialization. Optum exemplifies horizontal scale, generating USD 226.6 billion across its three divisions in 2024 and stewarding USD 75 billion in provider revenue. R1 RCM and IQVIA illustrate vertical dominance in revenue-cycle and clinical-research outsourcing, respectively, leveraging proprietary platforms and domain depth.

Technology remains the core differentiator. HCLTech’s GenAI slashed prior-authorization review times to 20 minutes, trimming costs by 30% for payer clients. Optum Real offers real-time data exchange, and early pilots processed thousands of encounters with fewer errors. Cognizant’s BPaaS delivered a 99% first-pass claims-yield gain for EmblemHealth. Private-equity capital continues to reshape the field; New Mountain Capital’s USD 2 billion purchase of Access Healthcare and Cardinal Health’s USD 1.12 billion acquisition of ION highlight investor appetite for automated-platform scale. Smaller AI-native startups are providing denial-management and documentation-automation point solutions that larger vendors often buy rather than build, accelerating the pace of tuck-in acquisitions.

United States Healthcare BPO Industry Leaders

- Accenture PLC

- Genpact Limited

- Cognizant

- UnitedHealth Group

- R1 RCM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: The U.S. Department of Health and Human Services released an RFI seeking public input on accelerating artificial-intelligence adoption across clinical care.

- October 2025: AGS Health launched a suite of agentic digital-workforce solutions using AI agents and intelligent automation to address rising claim-denial rates and staffing shortages.

- April 2025: Red Sky Health introduced Daniel, an AI platform that corrects errors, resubmits claims in real time, and recoups denied revenue for providers.

- February 2025: Capital Rx unveiled Judi Health, the first platform handling pharmacy and medical claims on a single system to reduce administrative waste for payers.

United States Healthcare BPO Market Report Scope

Healthcare BPO (business process outsourcing) refers to a process in which healthcare providers select the most suited third-party vendors for specific business processes. This enables hospitals and medical professionals to allocate their energy and valuable time to patient care.

As per the scope of the report, the US healthcare BPO market is segmented by service type, delivery model, service delivery mode, and end customer. By Service type, the market is segmented into payer service, provider service, and pharmaceutical service. By payer service, the market is segmented into human resource management, claims management, customer relationship management (CRM), operational/administrative management, care management, provider management, and other payer services. By provider service, the market is segmented into patient enrollment and strategic planning, patient care service, and revenue cycle management. By pharmaceutical service, the market is segmented into research and development, manufacturing, and non-clinical service. By Delivery Model, the market is segmented into Onshore, Nearshore, and Offshore. By Service Delivery Mode, the market is segmented into Captive, Third-Party, and Hybrid. By End Customer, the market is segmented into Payers, Providers, Pharmaceutical & Biotech, and Government Agencies. For each segment, the market size is provided in terms of value in USD.

By Service Type

| Payer Service | Human Resource Management | |

| Claims Management | ||

| Customer Relationship Management (CRM) | ||

| Operational / Administrative Management | ||

| Care Management | ||

| Provider Management | ||

| Other Payer Services | ||

| Provider Service | Patient Enrollment & Strategic Planning | |

| Patient Care Service | ||

| Revenue Cycle Management (RCM) | ||

| Pharmaceutical Service | Research & Development Support | |

| Manufacturing Support | ||

| Non-clinical Services | Supply Chain & Logistics | |

| Sales & Marketing Support | ||

| Other Non-clinical Services | ||

By Delivery Model

| Onshore Delivery |

| Nearshore Delivery |

| Offshore Delivery |

By Service Delivery Mode

| Captive (In-house) Centers |

| Third-Party Outsourcing |

| Hybrid / Co-sourcing |

By End Customer

| Healthcare Payers (Insurers & PBMs) |

| Healthcare Providers (Hospitals, Physician Groups) |

| Pharmaceutical & Biotech Companies |

| Government Agencies |

| By Service Type | Payer Service | Human Resource Management | |

| Claims Management | |||

| Customer Relationship Management (CRM) | |||

| Operational / Administrative Management | |||

| Care Management | |||

| Provider Management | |||

| Other Payer Services | |||

| Provider Service | Patient Enrollment & Strategic Planning | ||

| Patient Care Service | |||

| Revenue Cycle Management (RCM) | |||

| Pharmaceutical Service | Research & Development Support | ||

| Manufacturing Support | |||

| Non-clinical Services | Supply Chain & Logistics | ||

| Sales & Marketing Support | |||

| Other Non-clinical Services | |||

| By Delivery Model | Onshore Delivery | ||

| Nearshore Delivery | |||

| Offshore Delivery | |||

| By Service Delivery Mode | Captive (In-house) Centers | ||

| Third-Party Outsourcing | |||

| Hybrid / Co-sourcing | |||

| By End Customer | Healthcare Payers (Insurers & PBMs) | ||

| Healthcare Providers (Hospitals, Physician Groups) | |||

| Pharmaceutical & Biotech Companies | |||

| Government Agencies | |||

Key Questions Answered in the Report

How large is the United States healthcare BPO market in 2026?

It stands at USD 165.05 billion and is projected to grow at an 8.26% CAGR to 2031.

Which service type dominates U.S. healthcare outsourcing?

Pharmaceutical Services lead, holding 58.62% of 2025 spend thanks to extensive clinical-trial and regulatory-support needs.

Why is Nearshore Delivery growing faster than Offshore Delivery?

Tariff-driven hardware costs and wage inflation abroad, combined with time-zone and compliance advantages, are driving a 12.32% CAGR for nearshore locations.

What is driving provider demand for revenue-cycle outsourcing?

Denial rates of 11.8-19% and rising cost-to-collect spur hospitals to seek AI-enabled, variable-cost revenue-cycle partners.

How are cybersecurity concerns shaping vendor selection?

Post-breach scrutiny requires SOC 2 Type II reports, large cyber-insurance policies, and robust incident-response protocols, favoring established vendors with mature security operations.

Which customer group is the fastest-growing buyer segment?

Government agencies, led by state Medicaid MMIS modernization projects, are forecast to grow at 10.53% annually through 2031.

Page last updated on: