Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

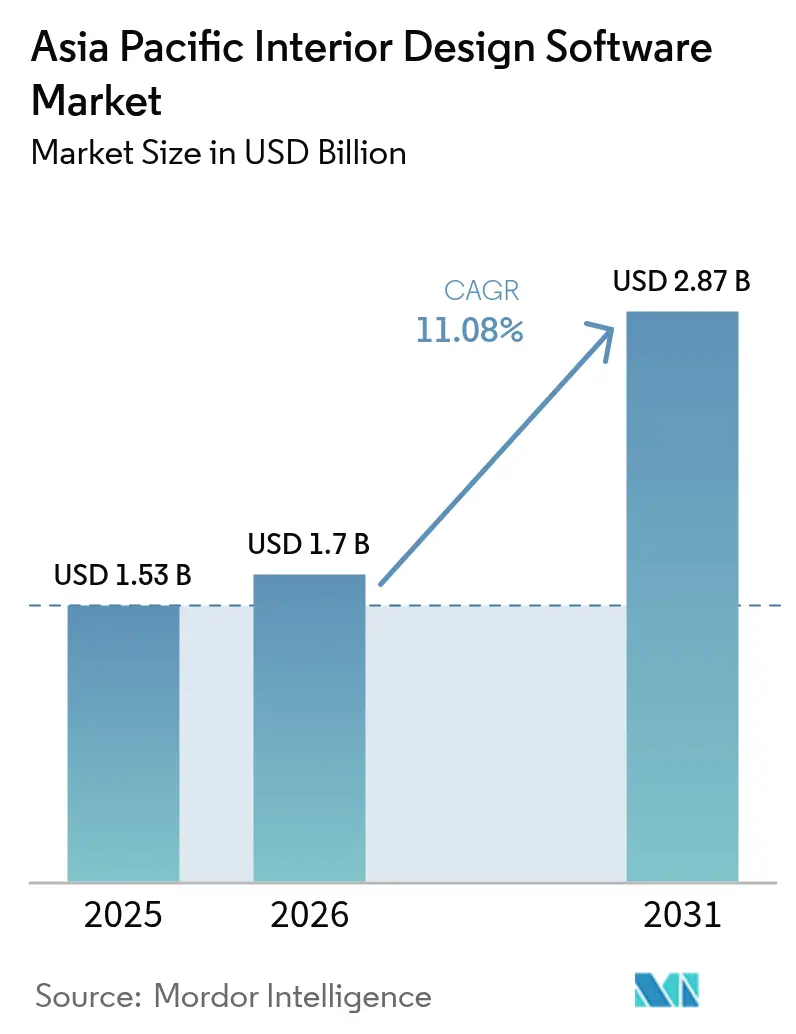

| Base Year Market Size (2025) | USD 1.53 Billion |

| Market Size (2026) | USD 1.7 Billion |

| Market Size (2031) | USD 2.87 Billion |

| Growth Rate (2026 - 2031) | 11.08% CAGR |

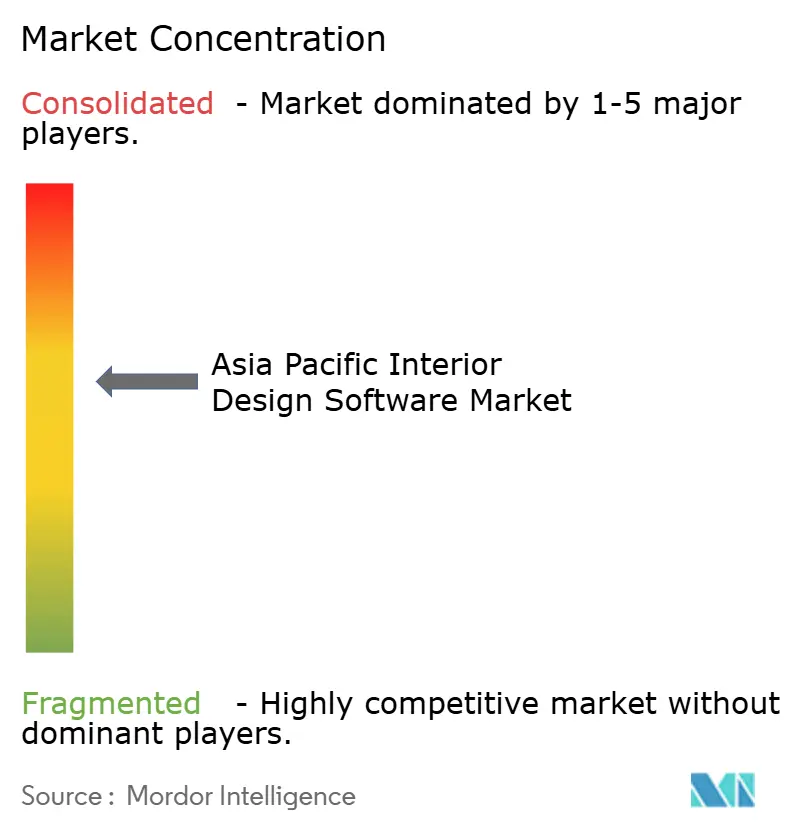

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Interior Design Software Market Analysis by Mordor Intelligence

The Asia Pacific interior design software market size in 2026 is estimated at USD 1.7 billion, growing from 2025 value of USD 1.53 billion with 2031 projections showing USD 2.87 billion, growing at 11.08% CAGR over 2026-2031. The expansion stems from an accelerating shift toward cloud-native subscriptions, real-time collaboration, and embedded artificial intelligence that automates space planning and photorealistic rendering.[1]Autodesk Investor Relations, “Fiscal Q3 2025 Earnings Release,” investors.autodesk.com Trimble’s SketchUp surpassed 1 million paid users by late 2024, marking a significant shift away from perpetual licenses. China’s e-commerce-led workflows, India’s Smart Cities build-out, and Southeast Asia’s mobile-first design culture are reshaping competitive priorities. Vendors that fuse visualization with procurement and cost estimation are capturing share, while hardware-driven desktop strategies face tariff-induced cost pressure.

Key Report Takeaways

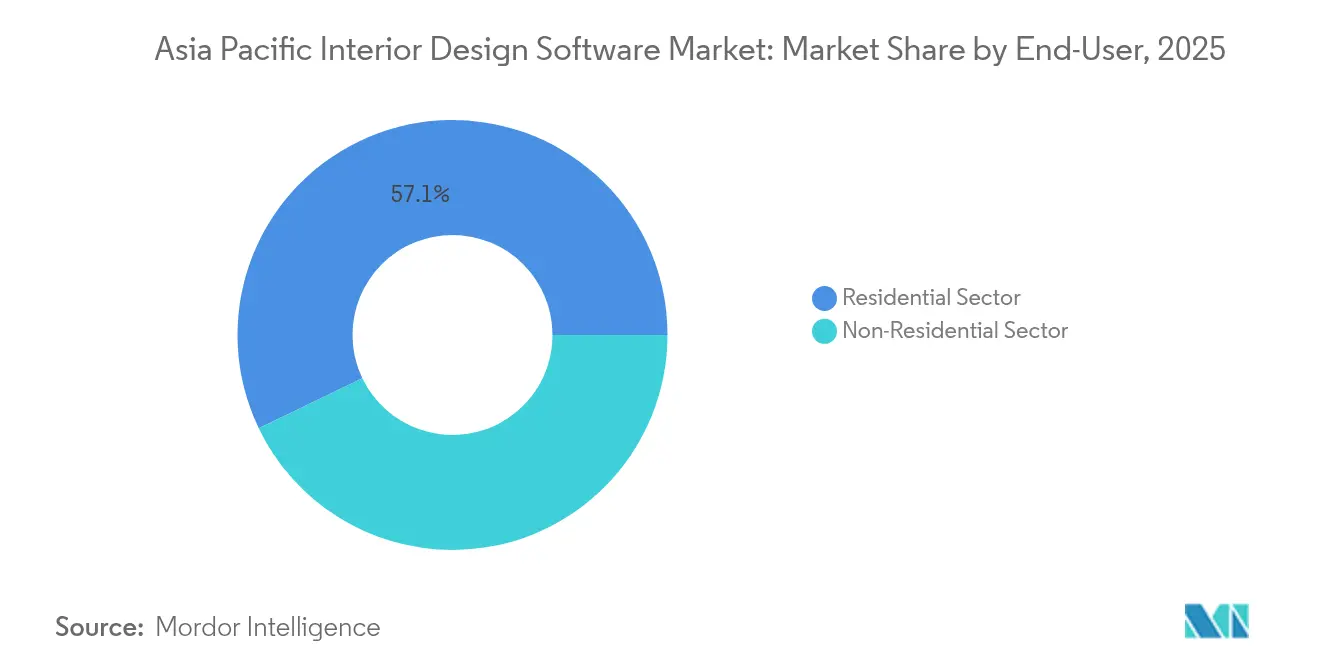

- By end-user, the residential segment led with a 57.13% share in 2025; non-residential design is projected to advance at a 13.52% CAGR through 2031.

- By deployment mode, cloud solutions held 62.52% of the Asia Pacific interior design software market share in 2025, and this segment is expected to expand at a 15.08% CAGR to 2031.

- By application, three-dimensional design and rendering accounted for 49.51% of the Asia Pacific interior design software market size in 2025, while virtual reality and augmented reality visualization are projected to show the fastest growth, with a 16.42% CAGR to 2031.

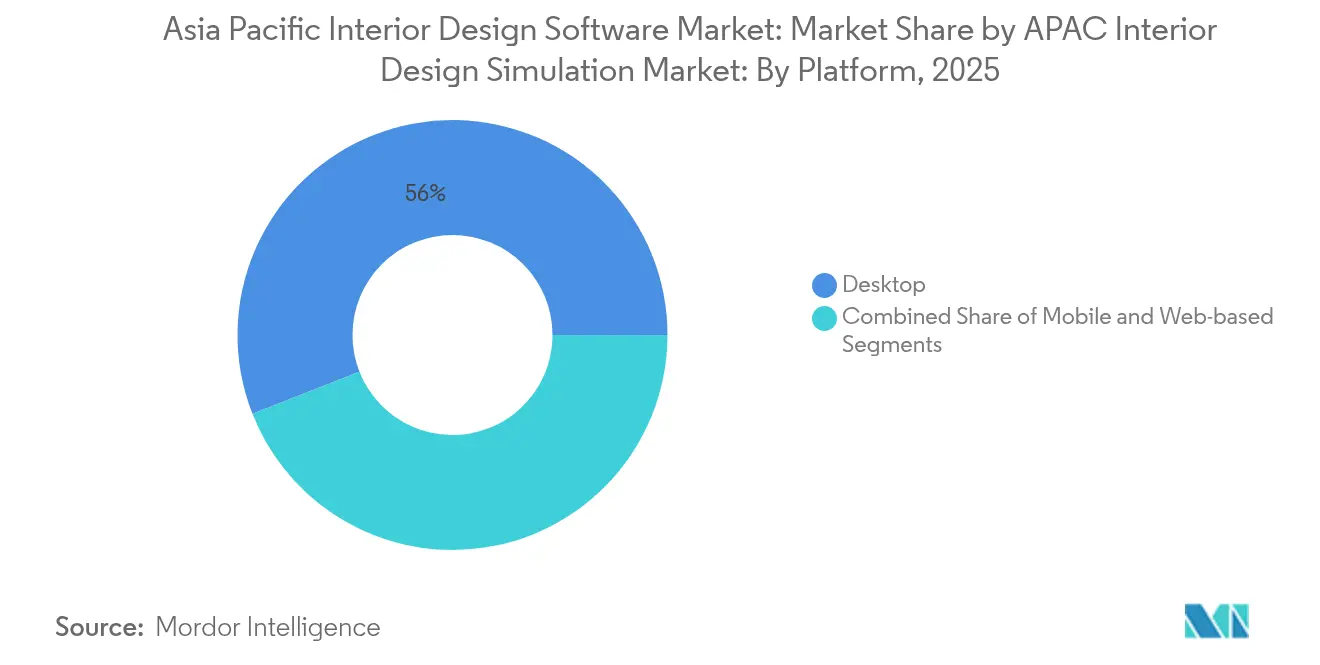

- By platform, desktop workflows secured a 55.97% revenue share in 2025; mobile platforms are projected to climb at a 15.65% CAGR through 2031.

- By license model, subscription SaaS contributed 63.02% of 2025 revenue; freemium and ad-supported tiers are forecast to grow at 16.84% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Interior Design Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for visualization-driven home renovation | +2.3% | China, Japan, Australia, South Korea | Medium term (2-4 years) |

| Government smart-city and housing initiatives | +1.8% | India, China, Thailand, Vietnam, Singapore | Long term (≥ 4 years) |

| Surge in cloud-based design collaboration adoption | +2.7% | Whole region, strongest in India and Southeast Asia | Short term (≤ 2 years) |

| Integration of AI for automated space planning | +1.9% | China, India, Japan urban centers | Medium term (2-4 years) |

| Expansion of virtual furniture e-commerce partnerships | +1.6% | China, Indonesia, Thailand, Vietnam | Short term (≤ 2 years) |

| Hardware tariff pressures accelerating cloud rendering shift | +1.4% | Region-wide, acute in India and Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Visualization-Driven Home Renovation

Homeowners now insist on photoreal previews before committing capital to remodels. Japan recorded JPY 7.2 trillion (USD 48.6 billion) renovation outlays in 2024, with 68% of projects using digital visualization.[2]Ministry of Land, Infrastructure, Transport and Tourism, “Housing Report 2024,” mlit.go.jpAustralian households followed suit as higher mortgage rates lengthened dwelling lifecycles. Software publishers responded by integrating material-pricing APIs with design canvases, allowing users to toggle finishes against live budgets. Platforms that unify visualization and purchasing are shortening decision cycles and gaining loyalty.

Government Smart-City and Housing Initiatives

Public digital-twin mandates spill into private practice. India’s Smart Cities Mission deployed INR 48,000 crore (USD 5.8 billion) and normalized Building Information Modeling tools for municipal contractors. China’s 290 pilot smart cities require cloud collaboration for cross-agency reviews. Thailand’s Digital Economy Promotion Agency and Dassault Systèmes are certifying 500 designers annually to support Eastern Economic Corridor projects.[3]Digital Economy Promotion Agency, “Dassault Systèmes Training Center Partnership,” depa.or.thSuch mandates set interoperability baselines and anchor long-run demand for compliant platforms.

Surge in Cloud-Based Design Collaboration Adoption

Cloud usage scales fastest where on-premise GPUs have become price-constrained. AWS opened a Malaysia region in 2024, cutting render latency by 40% for Southeast Asian firms.[4]Amazon Web Services, “AWS Asia Pacific Infrastructure Update,” press.aboutamazon.com Microsoft Azure added 60% more GPU capacity in India, halving per-hour costs. With cross-border data rules clarified under China’s Personal Information Protection Law, designers can route files through Singapore nodes while maintaining compliance. Reduced costs and legal clarity accelerate the uptake of multi-site collaboration.

Integration of AI for Automated Space Planning

Generative algorithms turn software into a design partner. Dassault’s HomeByMe concept reduced concept time by 40% by automatically placing furniture after scanning room metrics. SketchUp 2025 ships “Diffusion,” generating 3D assets from text prompts and improving IFC alignment with Revit. Coohom’s engine delivers ready-to-share renders in 90 seconds. As iteration becomes instantaneous, users gravitate to platforms that treat AI as core infrastructure, not a bolt-on.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability issues among design platforms | -1.4% | Global, sharpest where vendor mix is high | Medium term (2-4 years) |

| High subscription and training costs for SMEs | -1.8% | India, Southeast Asia, smaller Chinese cities | Short term (≤ 2 years) |

| Shortage of skilled 3D and VR designers | -1.2% | Region-wide, most acute in India, Vietnam, Indonesia | Long term (≥ 4 years) |

| Data-privacy and cybersecurity compliance gaps | -0.9% | China, India, Singapore | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Interoperability Issues Among Design Platforms

Disparate file structures require firms to invest in multiple tools and incur manual rework. The IFC 4.3 schema, finalized in 2024, still omits parametric furniture, so assets lose editability when moved between Revit, SketchUp, or Vectorworks. Japan’s BIM mandate lacks a unified national template, resulting in regional variations that hinder coordination. Time lost to translation inflates costs and tempers adoption where projects rely on mixed vendor stacks.

High Subscription and Training Costs for SMEs

For small studios, software fees often rival payroll costs. Autodesk AutoCAD costs USD 1,865 per user per year, equivalent to 40% of a junior designer’s monthly pay in tier-2 Indian cities. Structured parametric modeling courses run USD 800-1,200 in Vietnam and Indonesia, keeping many freelancers on basic 2D tools. Freemium tiers address the gap, yet conversion depends on affordable credentials and usage-based billing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Non-Residential Demand Outpaces Residential Maturity

The residential portion held 57.13% of 2025 revenue, reflecting early homeowner adoption of visualization for remodel budgeting. The Asia Pacific interior design software market size linked to non-residential clients is growing faster, with hospitality, retail, and co-working projects advancing at a 13.52% CAGR. Hotel builders in India used 3D walkthroughs for 62% of new rooms added in 2024. Japanese retailers repurposed physical stores as experiential showrooms, integrating VR configurators that lifted conversion by 18%.

Residential growth decelerates to 9.66% CAGR as penetration saturates tier-1 Chinese and Australian cities, though rural India and emerging Vietnamese metros remain greenfields. The Asia Pacific interior design software market is driving compliance in commercial real estate, with Singapore developers requiring BIM-ready submissions for projects exceeding SGD 50 million. Platforms able to align with building codes and procurement needs will dominate the expanding non-residential segment.

By Deployment Mode: Cloud Economics Rewrite Infrastructure Choices

Cloud deployments captured a 62.52% share in 2025 and are growing at a 15.08% CAGR, outpacing the Asia Pacific interior design software market by four points. GPU shortages pushed on-premise card prices above USD 2,200, while India’s import tariff added 28%. AWS render nodes now cost roughly USD 3 per hour, so a studio running 100 jobs a month spends USD 1,200 versus USD 18,000 annual amortization for local hardware.

Hybrid models are projected to rise at a 12.32% CAGR, where privacy laws require in-country storage, yet workloads must surge to the cloud during peaks. Autodesk’s Flex license allows toggling between desktop and cloud renders in a single SKU, shielding users from upfront capital and compliance friction. Vendors lacking seamless hybrid workflows risk losing customers as they recalibrate their cost structures.

By Application: VR and AR Visualization Disrupt Traditional Rendering

Three-dimensional design and rendering supplied 49.51% of the 2025 spend, anchoring the core workflow of the Asia Pacific interior design software market. Virtual reality and augmented reality, although smaller, are driving revenue growth at a 16.42% CAGR as retailers embed headset-based planners to shorten sales cycles. AiHouse and OPPEIN reported a 15% increase in conversions when customers manipulated layouts in mixed reality.

Two-dimensional drafting holds a 21.84% share but trails at a 7.69% CAGR because it cannot convey the spatial depth that clients expect. Standalone rendering packages face commoditization; growth now hinges on bundling cost estimation, task assignment, and version control into a single environment. Users gravitating toward platforms that consolidate design, approval, and procurement into a single session will reshape application priorities.

By Platform: Mobile-First Southeast Asia Redefines Interfaces

Desktop workflows still account for 55.97% of 2025 revenue, but mobile is adding users at a 15.65% CAGR. Indonesia has 204 million smartphone owners, yet only 68 million PC users. Consequently, designers are adopting Planner 5D and RoomSketcher for browser-based projects. Japan and South Korea cling to desktops for parametric precision, maintaining a regional share that remains elevated.

Web-based canvases grow 13.02% CAGR, favored by Vietnam’s freelancer-heavy firms that avoid licensing friction. Autodesk Forma stitched mobile photo capture to cloud terrain generation and desktop refinement into a coherent, device-agnostic loop. Vendors who ignore cross-device continuity risk irrelevance across Southeast Asia’s mobile-centric workforce.

By License Model: Freemium Unlocks Underserved Micro-Enterprises

Subscription SaaS held a 63.02% share in 2025 and remains the revenue anchor. The Asia Pacific interior design software market size tied to freemium tiers is, however, expanding at a 16.84% CAGR, the fastest lane, as India’s 63 million microenterprises test tools without upfront fees. Planner 5D reached 10 million Southeast Asian users on an ad-funded plan and converts at a 3% rate after firms grow beyond the hobby scale.

Perpetual licenses have declined by 2.29% annually since Autodesk discontinued perpetual AutoCAD in 2024. Conversion hinges on gentle paywalls: RoomSketcher caps the number of renders in its free tier, prompting upgrades once users exceed five projects per month. Coohom aligns charges with AI-generated variations, capturing value per output rather than per seat.

Geography Analysis

China controlled 41.78% of the 2025 spend, as furniture e-commerce embedded design was directly integrated into the checkout. Coohom, valued at USD 1 billion, alone holds a 23.2% local share by bundling photorealistic renders with instant purchase paths. Growth moderates to a 10.65% CAGR as tier-1 penetration nears saturation, but tier-3 cities and rural provinces still provide a runway.

India logs the fastest 14.56% CAGR, driven by Smart Cities mandates across 100 municipalities and an urban housing pipeline that added 1.2 million units in 2024. Small firms are embracing low-cost subscriptions that come with training credits, while cloud GPU expansions are reducing entry barriers.

Japan advances at an 11.12% CAGR in renovation subsidies for energy and seismic retrofits. Over 30% of homes are over 30 years old, spurring demand for design tools that model insulation and earthquake reinforcement. Local vendors who map to unique building codes gain an advantage.

Australia and South Korea each hold a 6.00-7.00% share and are growing at a near 9.85% CAGR, where replacement cycles, rather than first-time adoption, drive spending. Firms prioritize BIM interoperability with construction suites over flashy visualization.

Southeast Asia is projected to grow at a 13.18% CAGR, with Thailand, Vietnam, and Indonesia deploying AR showrooms and PropTech financing that mirrors China’s model. IKEA Thailand achieved a 12% conversion uplift by utilizing AR planners in 45 stores. Agile, mobile-first tools dominate freelancer-heavy ecosystems.

The rest of the Asia Pacific, including New Zealand and emerging South Asian states, advances at a 11.92% CAGR, driven by the cloud that eliminates infrastructure hurdles. Regional market approaches vary by location, with localized pricing strategies: freemium models for Indonesia, bundled training for India, and compliance certifications for China and Singapore.

Competitive Landscape

The top five players, Autodesk, Trimble, Dassault Systèmes, Coohom, and AiHouse, hold a prominent share, positioning the Asia Pacific interior design software market in a moderately fragmented landscape. Autodesk locks enterprise customers by linking AutoCAD, Revit, and BIM 360; switching costs exceed USD 50,000 for mid-size firms. Trimble’s SketchUp has surpassed 1 million paid users, driven by text-to-3D Diffusion AI and tighter IFC schemas that facilitate seamless Revit handoffs.

Chinese vendors grow through localized libraries. Coohom offers 2 million native SKUs, compared to 400,000 in SketchUp’s Asia catalog, accelerating the design of locally sourced furnishings. AiHouse blends mixed reality with cabinet makers to boost conversion. Regional newcomers, such as Foyr in India and Infurnia, are introducing API-first configurators that retailers embed in their e-commerce journeys, thereby bypassing traditional desktop interfaces.

Strategic alliances mark 2024-2025. Dassault and Thailand’s DEPA opened a BIM academy certifying 500 designers yearly. AWS’s Malaysia region slashed render latency by 40% in Southeast Asia. Microsoft doubled A100 and H100 GPU capacity in India. Firms that clear China and India data-privacy hurdles can serve regulated public projects, while agile start-ups capture the long tail of micro-enterprises with pay-as-you-go plans.

Asia Pacific Interior Design Software Industry Leaders

Dassault System SE

Autodesk Inc

Trimble, Inc.

Foyr LLC

Infurnia Technologies Pvt. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Trimble launched SketchUp 2025 with Diffusion AI, Chaos Cosmos material library, and improved IFC pathways.

- January 2025: Autodesk extended its Flex payment model across Asia Pacific, targeting cash-constrained SMEs.

- November 2024: Trimble's SketchUp has surpassed 1 million active subscribers, driven by its shift to a subscription model, new AI features (such as SketchUp Diffusion), and a focus on delivering value to the AEC industry, with strong growth fueled by easier entry and collaboration tools.

- October 2024: Dassault Systèmes and Thailand’s DEPA opened a 3DEXPERIENCE training center at Silpakorn University.

Asia Pacific Interior Design Software Market Report Scope

Interior design software enables architects to create floor plans and design spaces easily and efficiently. The solution has various combinations of features such as 2D space planning and floor plan creation, 3D designing, and modeling with rendering. The solution is typically downloaded or accessed via the internet.

The Asia Pacific Interior Design Software Market Report is Segmented by End-User Industries (Residential Sector, Non-Residential Sector), Deployment Mode (On-Premise, Cloud, Hybrid), Application Type (2D Design and Drafting, 3D Design and Rendering, VR and AR Visualization, Project Management and Collaboration), Platform (Desktop, Mobile, Web-Based), License Model (Perpetual One-Time License, Subscription SaaS, Freemium/Ad-Supported), and Geography (China, India, Japan, South Korea, Australia, Southeast Asia, Rest of Asia Pacific). The Market Forecasts are Provided in Terms of Value (USD).

By End-User Industries

| Residential Sector |

| Non-Residential Sector |

By Deployment Mode

| On-Premise |

| Cloud |

| Hybrid |

By Application Type

| 2D Design And Drafting |

| 3D Design And Rendering |

| VR And AR Visualization |

| Project Management And Collaboration |

By Platform

| Desktop |

| Mobile |

| Web-Based |

By License Model

| Perpetual One-Time License |

| Subscription SaaS |

| Freemium / Ad-Supported |

By Country

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Southeast Asia |

| Rest of Asia Pacific |

| By End-User Industries | Residential Sector |

| Non-Residential Sector | |

| By Deployment Mode | On-Premise |

| Cloud | |

| Hybrid | |

| By Application Type | 2D Design And Drafting |

| 3D Design And Rendering | |

| VR And AR Visualization | |

| Project Management And Collaboration | |

| By Platform | Desktop |

| Mobile | |

| Web-Based | |

| By License Model | Perpetual One-Time License |

| Subscription SaaS | |

| Freemium / Ad-Supported | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Southeast Asia | |

| Rest of Asia Pacific |

Key Questions Answered in the Report

How large is the Asia Pacific interior design software market in 2026?

The market stands at USD 1.7 billion in 2026 and is forecast to hit USD 2.87 billion by 2031.

Which deployment mode is expanding fastest across the region?

Cloud-based implementations lead with a 15.08% CAGR thanks to falling GPU cloud costs and regional data-center additions.

What is driving non-residential software uptake?

Hospitality, retail, and co-working renovations adopt 3D and VR tools to differentiate guest experience, pushing non-residential demand at 13.52% CAGR.

Which country shows the fastest growth?

India advances at 14.56% CAGR, propelled by Smart Cities mandates and an urban housing boom.

Page last updated on: