Orthodontic Supplies Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

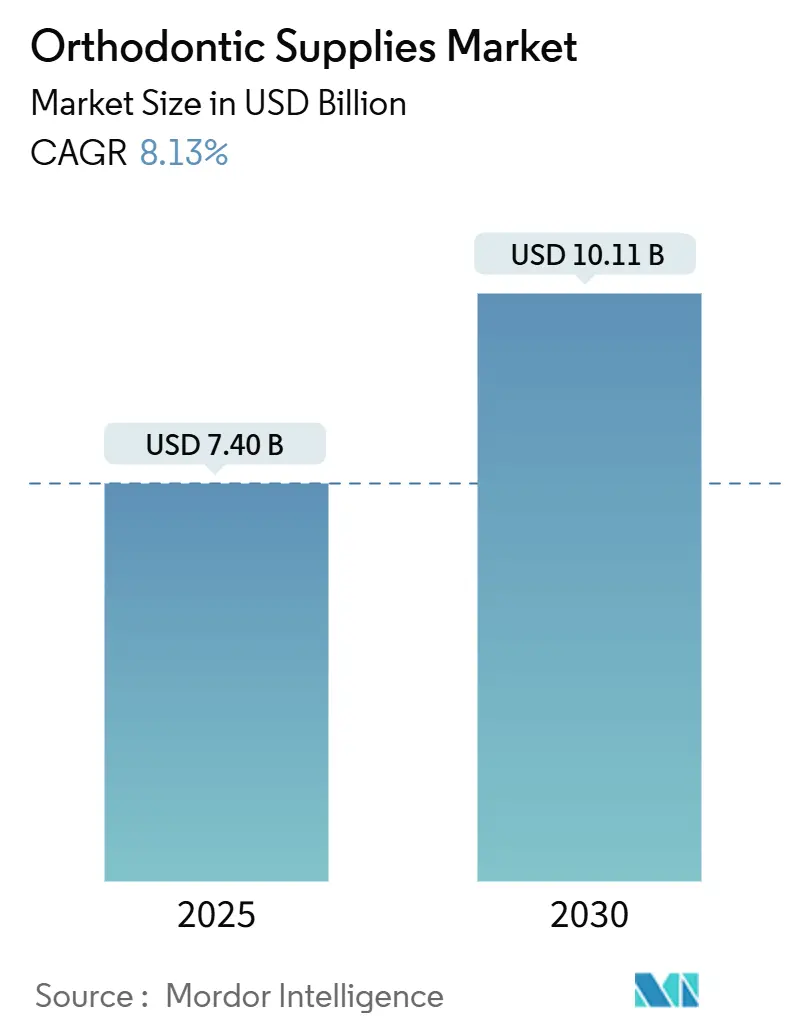

| Market Size (2025) | USD 7.40 Billion |

| Market Size (2030) | USD 10.11 Billion |

| Growth Rate (2025 - 2030) | 8.13% CAGR |

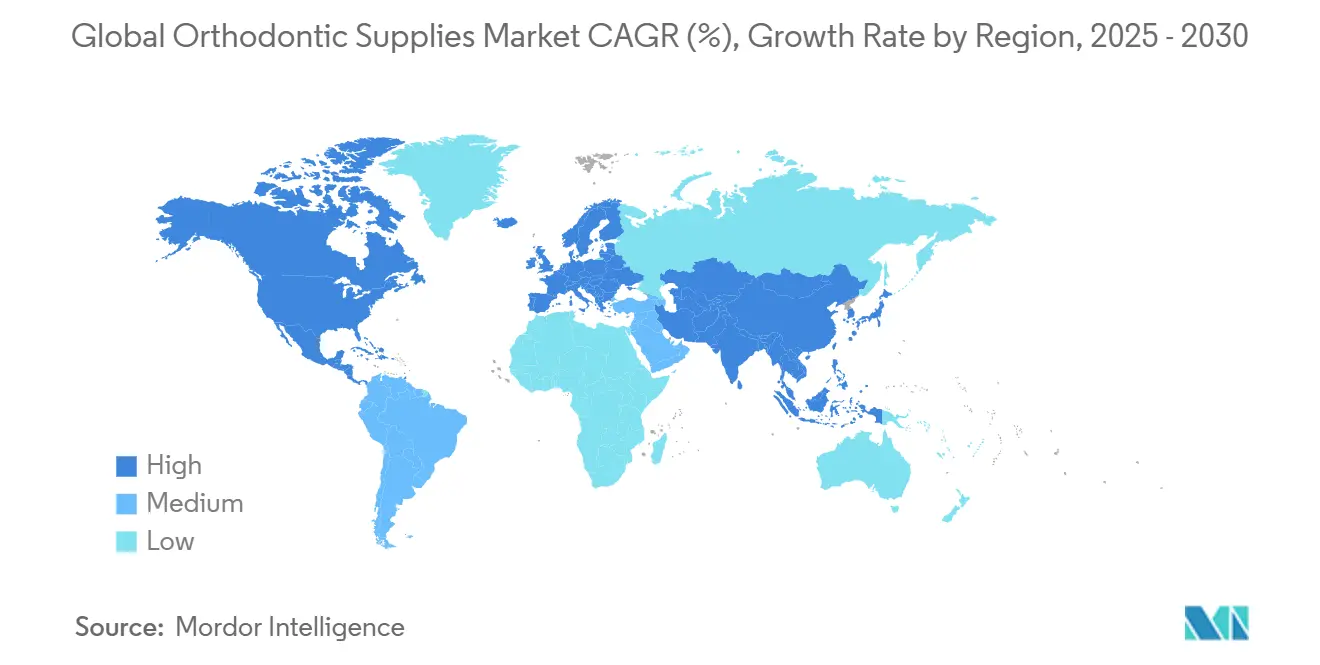

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

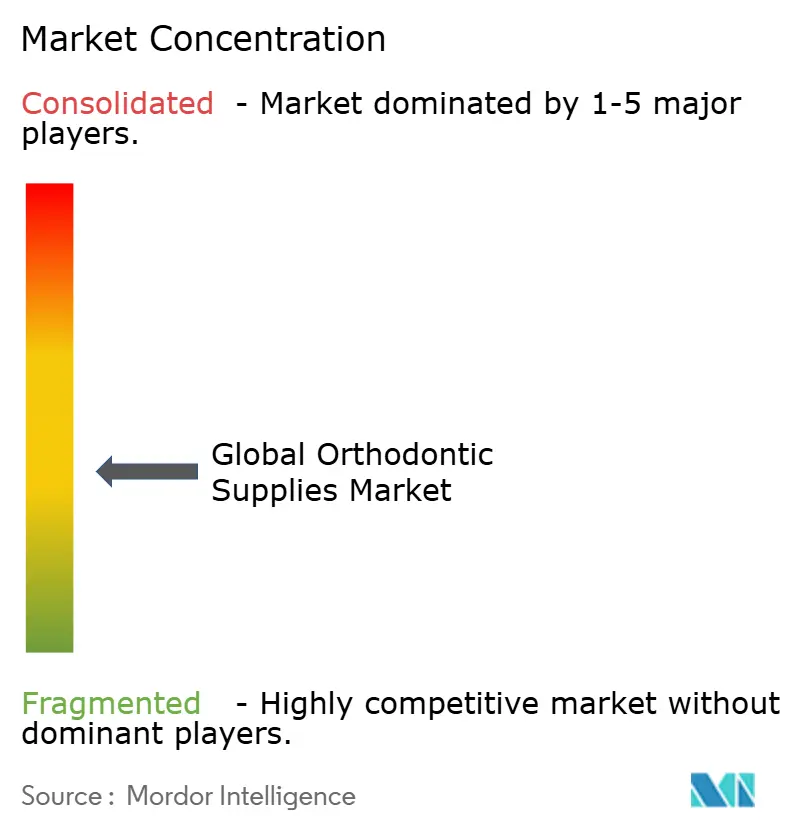

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Orthodontic Supplies Market Analysis by Mordor Intelligence

The Orthodontic Supplies Market size is estimated at USD 7.40 billion in 2025, and is expected to reach USD 10.11 billion by 2030, at a CAGR of 8.13% during the forecast period (2025-2030).

Clear aligner systems are expanding at a 20.3% CAGR, confirming the shift toward aesthetic, digitally enabled orthodontics. Artificial intelligence tools that create predictive treatment plans strengthen practice efficiency, and adult demand now rivals pediatric volumes as working professionals seek discreet options. Thermoplastic polyurethane’s 18.0% CAGR signals the importance of biocompatible, eco-friendly materials, while direct-to-consumer (DTC) platforms grow quickly despite tighter regulatory oversight. Consolidation among dental service organizations and AI-driven startups fuels competitive intensity, yet supply-chain risks in specialty alloys and uncertain rules around teledentistry temper long-term visibility.

Key Report Takeaways

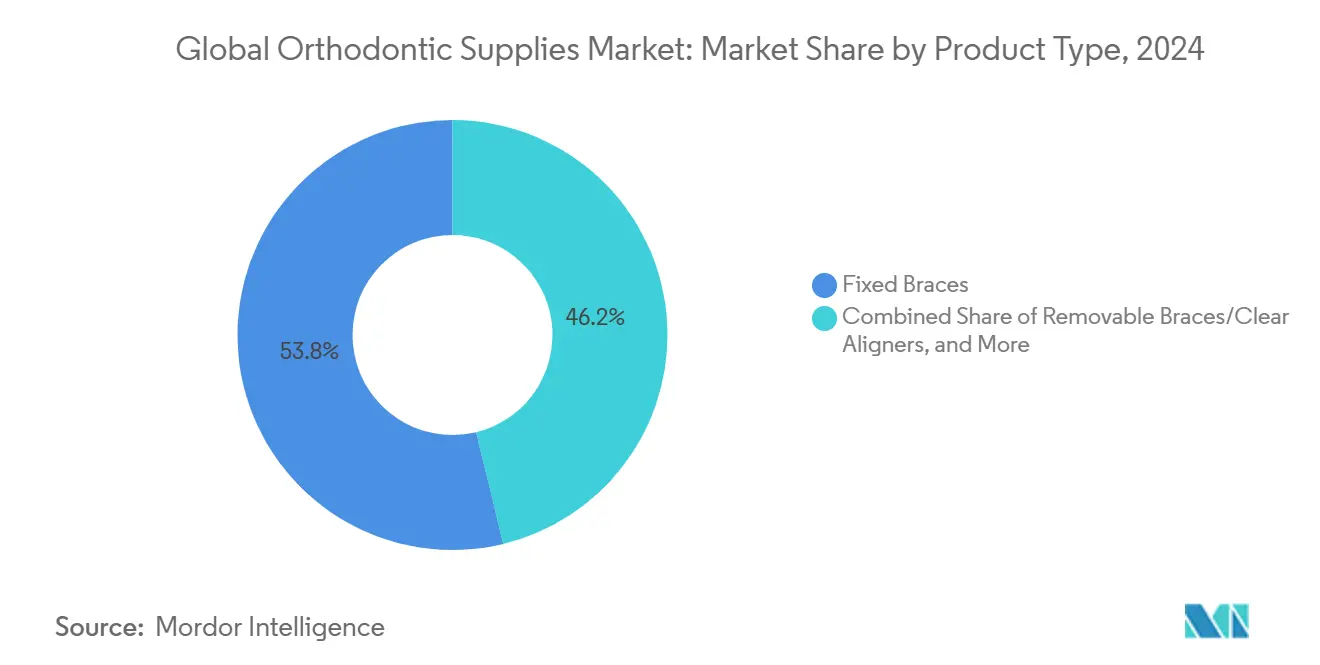

- By product type, fixed braces led the orthodontic supplies market with 53.8% of the share in 2024, whereas clear aligners are projected to post the fastest 20.3% CAGR through 2030.

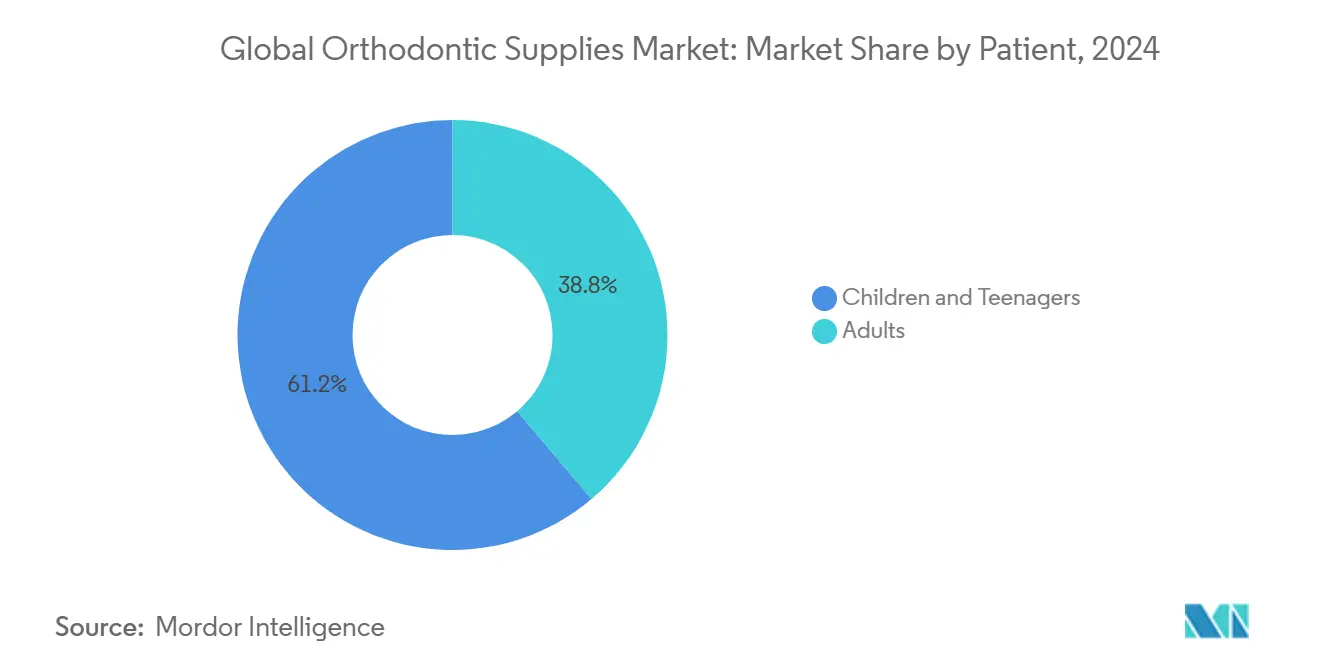

- By patient group, children and teenagers held 61.2% of the orthodontic supplies market size in 2024, but the adult segment is forecast to expand at a 13.0% CAGR to 2030.

- By end user, dental clinics retained 61.1% revenue share in 2024, while DTC platforms are advancing at a 16.6% CAGR over the same period.

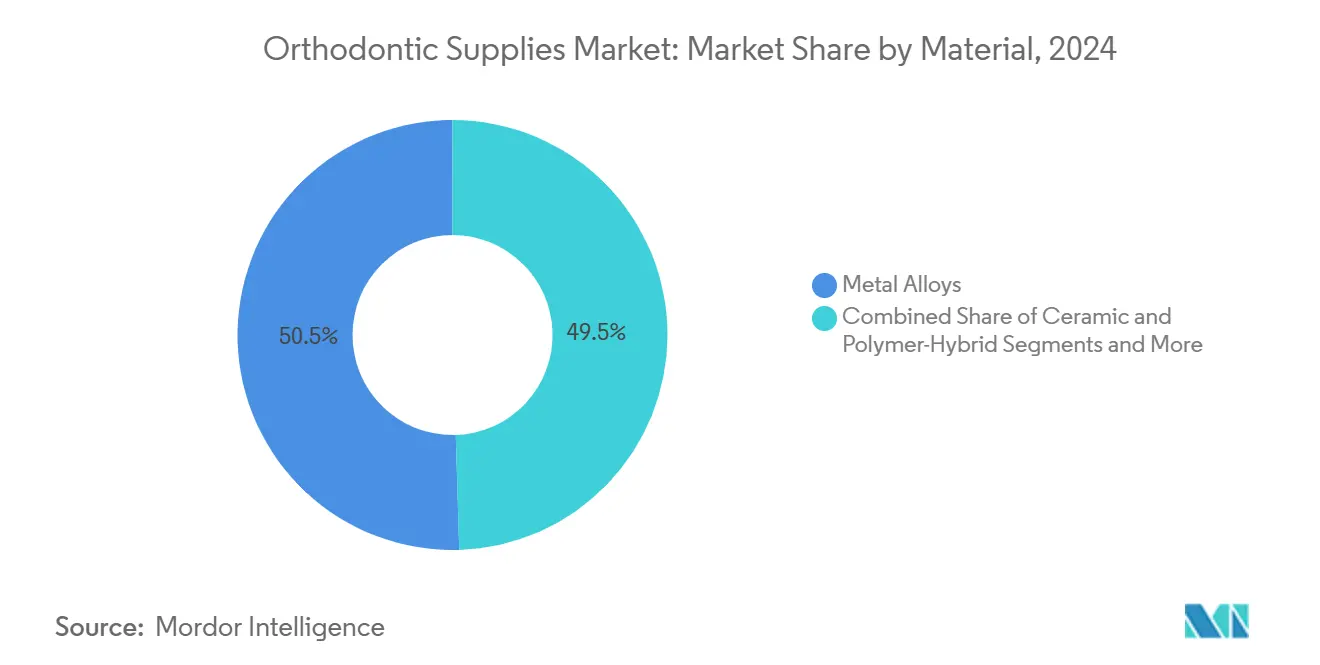

- By material, metal alloys captured 50.5% share of the orthodontic supplies market size in 2024, whereas thermoplastic polyurethane is growing at an 18.0% CAGR.

- By distribution channel, offline distributors commanded a 73.8% share in 2024; e-commerce is the fastest-growing channel, with an 18.0% CAGR to 2030.

- By geography, North America accounted for 34.5% of the orthodontic supplies market share in 2024, while Asia Pacific is set to log the highest 11.0% CAGR through 2030.

Global Orthodontic Supplies Market Trends and Insights

Drivers Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of malocclusion | +1.80% | Global, with higher impact in Asia Pacific | Long term (≥ 4 years) |

| Technological advances in digital orthodontics | +2.10% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Adult demand for aesthetic clear-aligner solutions | +1.50% | Global, concentrated in urban markets | Medium term (2-4 years) |

| Expansion of direct-to-consumer orthodontics | +1.20% | North America & EU primarily | Short term (≤ 2 years) |

| AI-driven chair-side treatment planning | +0.90% | North America & EU, early adoption in APAC | Long term (≥ 4 years) |

| Sustainable, bio-based orthodontic materials | +0.60% | EU leading, global adoption following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Malocclusion

Malocclusion affects up to 75% of the world’s population, and complex cases are more common in China than in the United States, widening the treatment gap. Urbanization and diet shifts toward ultra-processed foods aggravate occlusal problems, while prolonged screen time reduces natural masticatory activity required for healthy craniofacial growth. Health agencies now link untreated malocclusion to temporomandibular disorders and poor oral hygiene, prompting broader reimbursement eligibility. Public health messaging positions orthodontic therapy not only as a cosmetic choice but as a preventive tool, spurring demand in both developed and emerging economies. The result is sustained patient inflow beyond traditional pediatric windows, feeding multi-year pipeline visibility for practices.

Technological Advances in Digital Orthodontics

Artificial intelligence algorithms reach 92% sensitivity and 88% specificity for malocclusion detection, with 94% of AI-generated treatment plans aligning with clinical guidelines. Widespread adoption of intraoral scanning and 3D printing allows mass customization and shorter chair time, and CBCT imaging integrated with AI yields precise root and bone mapping. Nearly every orthodontic office in North America now operates a digital workflow, elevating treatment visualization to a key differentiator for patient acquisition. Practices able to deliver short, predictable appointment schedules report higher conversion rates and better word-of-mouth referrals. Investment payback periods are shrinking as scanner prices fall and software moves to subscription models.

Adult Demand for Aesthetic Clear-Aligner Solutions

Adults older than 35 represent 23% of new orthodontic cases, reflecting changing social attitudes and workplace acceptance. Clear aligners satisfy aesth etic expectations, with patient satisfaction at 78% versus 62% for metal brackets, encouraging premium price tolerance. Remote and hybrid work reduces day-to-day visibility concerns, further improving uptake. Higher compliance among adults translates to smoother case progression and fewer refinements, lowering overhead for practices. Influencer marketing on social media normalizes adult orthodontics, expanding the referral base and accelerating adoption among late entrants.

Expansion of Direct-to-Consumer Orthodontics

DTC aligner platforms deliver 16.8% CAGR even as professional bodies increase adverse-event reporting to the FDA’s MAUDE database.[1]American Association of Orthodontists, “Statement on Direct-to-Consumer Orthodontic Treatment,” aaoinfo.org Installment-based financing mitigates upfront cost barriers and expands eligibility to budget-sensitive cohorts. Hybrid care models now combine remote monitoring with periodic in-office scans to satisfy quality mandates while preserving convenience. Market shakeouts have begun: some players exited following quality lapses, whereas others pivoted to dentist-directed services, illustrating a race to balance scale with clinical credibility. Long-term winners are likely to integrate AI triage and retain a robust referral pathway for complex cases.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High treatment cost & limited reimbursement | -1.40% | Global, more pronounced in emerging markets | Medium term (2-4 years) |

| Clinical risks & complications | -0.80% | Global, regulatory focus in North America & EU | Short term (≤ 2 years) |

| Supply-chain volatility of specialty alloys | -0.70% | Global, critical impact in North America & EU | Medium term (2-4 years) |

| Regulatory pushback on teledentistry models | -0.50% | North America & EU primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Treatment Cost & Limited Reimbursement

Global dental spending hit USD 174 billion in 2023, yet orthodontic procedures often cost USD 3,000-10,000 each, a figure that exceeds coverage caps of many insurance plans.[2]American Dental Association, “Dental Expenditure Trends 2023,” ada.org Out-of-pocket payments still dominate in emerging regions, curbing adoption among middle-income households. Geographic price disparities foster treatment tourism, but inconsistent follow-up raises outcome variability. Economic downturns typically defer elective spending, pressuring practice revenues in cash-pay markets. Flexible financing and value-based insurance models are gaining traction but remain fragmented.

Clinical Risks & Complications

The FDA updated device standards under ISO 27020 and ANSI/ADA 105-2024 to tighten safety oversight, encouraging more robust post-market surveillance[3]U.S. Food and Drug Administration, “ANSI/ADA Standard No. 105-2024,” fda.gov. Complications such as root resorption and periodontal damage heighten liability concerns, especially for unsupervised DTC cases. Adult treatments present additional challenges due to prior restorations and bone density changes, generating longer chair-side time. Insurers respond by raising malpractice premiums, which can dissuade small practices from adopting accelerated or remote protocols until clear guidelines emerge.

Segment Analysis

By Product Type: Clear Aligners Reshape Treatment Paradigms

Clear aligners are advancing at a 20.3% CAGR, outpacing the overall orthodontic supplies market. Fixed braces still command 53.8% of the orthodontic supplies market share in 2024, supporting complex torque and root movements that aligners cannot yet rival. Align Technology’s Palatal Expander System approval in Turkey demonstrates clear aligners’ shift into early-intervention territory, rather than limited relapse correction. Mass-customized aligners manufactured via 3D printing lower per-tray costs and boost scalability, widening practice eligibility. Meanwhile, innovations in self-ligating brackets with smart sensors enable real-time force monitoring, shortening fixed-case timelines by 10-15%. Sustainability is emerging as a differentiator: 40% of prospective patients now ask about recyclable trays, pushing suppliers toward bio-based polymers.

Clear aligners are projected to treat 70% of new cases by 2025, redefining the orthodontic supplies market size hierarchy. Yet, fixed systems remain essential in cost-sensitive regions and for severe skeletal discrepancies. Advanced titanium-molybdenum archwires improve activation stability and reduce chair visits, sustaining relevance among budget-conscious populations. Ligature demand persists in emerging economies where material cost outweighs aesthetic preference, so the global sales mix keeps a balanced profile through 2030.

Note: Segment shares of all individual segments available upon report purchase

By Patient: Adult Segment Drives Premium Growth

Adults account for a growing slice of the orthodontic supplies market size, advancing at a 13.0% CAGR against 61.2% youth dominance in 2024. Professional adults seek discreet solutions that blend with their lifestyle, often opting for aligners priced at USD 6,500 on average. Their higher compliance lowers refinement rates, translating to predictable margins for clinics. Adult cases often include restorations and periodontal considerations, raising procedural complexity and billable chair time.

Pediatric and teenage cohorts keep volume leadership because early intervention remains clinically optimal. Preventive orthodontics, such as phase-one expansion, prevents severe malocclusion progression and lowers lifetime costs. Parents invest based on perceived long-term oral-health savings, maintaining a stable client base. Nevertheless, adult demand alters marketing strategies, pushing practices toward flexible scheduling and remote monitoring services.

By End User: Digital Platforms Disrupt Traditional Delivery

Dental clinics and DSOs hold 61.1% revenue share, yet the DTC segment is growing at 16.6% CAGR. Practices are digitizing check-in, imaging, and aligner ordering to match the convenience DTC platforms market aggressively. Hybrid models now dominate: patients start with virtual consultations and undergo periodic in-office scans, marrying accessibility with oversight. Cloud-based case management portals integrate AI staging, slashing planning time.

Hospitals focus on complex interdisciplinary cases, such as orthognathic surgery, that DTC providers cannot handle, ensuring demand for full-service providers. DSOs leverage scale to negotiate supplier contracts and deploy AI imaging across branches, shielding margins against rising labor costs. The DTC landscape is consolidating as sustainability concerns and regulatory actions elevate entry barriers.

By Material: Sustainable Innovation Drives Premium Segments

Metal alloys retain 50.5% market share because of proven strength and affordability, anchoring traditional fixed appliances. Thermoplastic polyurethane, registering 18.0% CAGR, underpins the clear-aligner boom. New silk fibroin composites combine antimicrobial properties with tensile strength, ideal for aligners and retainers. Ceramic and polymer hybrids provide tooth-colored aesthetics for patients preferring fixed solutions without metallic visuals.

Smart materials that respond to oral temperature gradually adjust force, potentially reducing manual wire change appointments. Rising alloy prices due to geopolitical supply constraints drive cost optimization research. Regulators in the European Union now emphasize lifecycle environmental impact, incentivizing manufacturers to adopt bioresorbable formulations. This sustainability push is a competitive lever in urban markets with eco-conscious consumers.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: E-Commerce Transforms Access Patterns

Offline distributors still serve 73.8% of product flow by leveraging technical support and longstanding relationships with practices. Yet e-commerce’s 18.0% CAGR is redrawing lines; direct manufacturer-to-clinic websites offer bulk discounts and just-in-time delivery, reducing storage costs. Digital procurement platforms integrate inventory analytics, guiding practices to reorder automatically when stock thresholds are triggered.

Traditional wholesalers are digitizing catalogs and bundling online training modules to maintain relevance. For new entrants, borderless logistics unlock emerging markets without local warehousing, but they must overcome regulatory variations in device registration. Practices in remote areas benefit most, accessing a broader range of appliances previously unavailable due to low local demand.

Geography Analysis

North America held 34.5% of the orthodontic supplies market share in 2024, buoyed by widespread insurance coverage and a high concentration of board-certified specialists. AI-driven scanners and chair-side 3D printers reach mainstream status, allowing U.S. and Canadian clinics to offer same-day aligner pickup. Consolidation accelerates as DSOs acquire solo practices, enhancing purchasing power and IT standardization. However, elevated labor costs and supply-chain risks in nickel-titanium alloys drive price inflation, pushing some patients toward phased treatment plans or DTC options.

Asia Pacific is the fastest-growing region with an 11.0% CAGR, adding fresh volume to the orthodontic supplies market. China’s high malocclusion prevalence and rapidly urbanizing middle class produce sustained patient queues, though reimbursement gaps persist. Japan and South Korea showcase early adoption of AI diagnostics and self-ligating ceramic braces. Australia benefits from robust private-insurance uptake and government standards that support digital workflows. India’s tier-one cities see rising adult demand, yet price sensitivity lengthens decision cycles, positioning installment plans as a key enabler.

Europe maintains steady mid-single-digit growth underpinned by universal dental coverage and a mature specialist network. Sustainability legislation moves the supply chain toward recyclable and bio-based aligner materials, giving European vendors a first-mover edge. Germany and the United Kingdom anchor regional revenue thanks to high per-capita dental spending and pioneering research hubs. France and Spain observe increasing adult treatment acceptance as financing products expand. Eastern European markets open new patient pools but require distributor-supported professional education to establish digital protocols.

Competitive Landscape

The orthodontic supplies market is moderately concentrated. Align Technology, 3M Oral Care, Dentsply Sirona, and Ormco anchor the traditional supplier tier, while LightForce Orthodontics spearheads a new wave of fully personalized 3D-printed brackets that can cut treatment time by 40%. Align Technology continues to refresh its Invisalign platform and expand iTero scanner capabilities, reinforcing customer lock-in with end-to-end workflow software. 3M invests in smart bracket sensors to capture data for AI monitoring, while Dentsply Sirona integrates intraoral scanning with chairside milling to streamline appliance delivery.

DSOs such as Heartland Dental and Canadian Orthodontic Partners scale purchasing and marketing, though debt-service costs trigger selective divestments. Startups leverage AI triage tools to automate simulation videos for prospective patients, lowering acquisition costs. Vertical integration trends proliferate: suppliers acquire software startups, and DSOs launch in-house aligner labs to capture margin and shorten turnaround. DTC firms pivot toward hybrid care, hiring orthodontists to address regulatory scrutiny and build credibility. In emerging regions, regional manufacturers partner with local distributors to comply with device registration laws while tapping untapped population bases.

White-space opportunities include eco-friendly material R&D and AI decision-support that mines multisource imaging to guide precise root movement. Companies able to fuse clinical efficacy, digital convenience, and sustainability are projected to secure stronger switching barriers. However, IP lawsuits around scanning workflows and aligner design remain an operational risk that could redirect R&D expenditure.

Orthodontic Supplies Industry Leaders

-

Align Technology Inc

-

3M Company

-

Envista Holdings

-

Dentsply Sirona Inc.

-

Straumann AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Align Technology expanded into Turkey with regulatory approval for the Invisalign Palatal Expander System by the Turkish Medicines and Medical Device Agency, targeting early orthodontic intervention markets.

- February 2025: DEXIS unveiled a new intraoral scanner and AI enhancements that connect more than 150,000 imaging devices in its digital ecosystem.

- January 2025: The FDA granted 510(k) clearance to Pearl Digital Inc. for the Pearl Clear Aligner, a Class II device for malocclusion treatment.

- August 2024: G&H Orthodontics upgraded its Tune clear aligner system for improved precision and comfort.

- July 2024: Biolux Technology launched OrthoPulse in the United States, a device intended to accelerate tooth movement and reduce treatment duration.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the orthodontic supplies market as sales of fixed braces components (brackets, archwires, anchorage devices, ligatures, others) and removable appliances such as clear aligners and retainers that are supplied to dental clinics, hospitals, and direct-to-consumer platforms worldwide. These figures are expressed in USD value for new products only, excluding after-care services or replacement parts.

Scope exclusion. We deliberately leave out practice revenues from orthodontic procedures and imaging equipment so our sizing reflects pure product demand.

Segmentation Overview

- By Product Type

- Fixed Braces

- Brackets

- Archwires

- Anchorage Appliances

- Ligatures

- Others

- Removable Braces / Clear Aligners

- Adhesives

- Accessories

- Fixed Braces

- By Patient

- Children & Teenagers

- Adults

- By End User

- Dental Clinics & DSOs

- Hospitals

- Direct-to-Consumer Platforms

- By Material

- Metal Alloys

- Ceramic & Polymer-Hybrid

- Thermoplastic Polyurethane (TPU)

- Bio-resorbable & Eco Materials

- By Distribution Channel

- Offline (Distributor / Retail)

- E-commerce Platforms

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed practicing orthodontists, procurement heads at large Dental Service Organizations, and regional distributors across North America, Europe, Asia, and Latin America. These discussions clarified average appliance counts per patient, emerging aligner adoption rates, and discount structures, which we then used to refine volume-to-value conversions and growth assumptions.

Desk Research

We began with structured reviews of open datasets from bodies such as the World Health Organization, FDI World Dental Federation, and national health ministries that report treated malocclusion cases and dentist density. Trade statistics from UN Comtrade and customs portals helped us understand cross-border flows of brackets and aligner kits. Company 10-Ks, investor decks, and dentistry association yearbooks gave price references and shipment clues, while news screening through Dow Jones Factiva provided event validation.

Patent analytics via Questel, together with clinical trial registries and peer-reviewed journals, added insight on material shifts from metal to ceramic and polymer hybrid designs. The sources cited are illustrative; several other public and subscription inputs were consulted to complete data collection and cross-checks.

Market-Sizing & Forecasting

A top-down treated-patient pool was built using malocclusion prevalence, treatment penetration, and retreatment cycles, which are then multiplied by appliance utilization and validated against sampled manufacturer shipments (bottom-up checkpoint). Key variables include average selling price by product group, number of active orthodontists, insurance reimbursement ratios, clear-aligner share, and demographic shifts in adult patients. Multivariate regression, combining health-spend per capita and aligner penetration trends, underpins the 2025-2030 forecast. Scenario analysis adjusts for technology price declines and macroeconomic swings.

Data Validation & Update Cycle

Models pass variance checks against independent shipment tallies, macro health indicators, and peer estimates, followed by multi-level analyst review. We refresh every twelve months, and interim updates are triggered when material events such as regulatory changes or major product launches occur.

Why Our Orthodontic Supplies Baseline Earns Maximum Trust

Published values often diverge because firms start from different patient pools, bundle accessories unevenly, or apply aggressive price curves.

Key gap drivers include inclusion of diagnostic equipment, omission of direct-to-consumer channels, use of static ASPs, and longer refresh cadences. Mordor's disciplined scope, yearly update rhythm, and dual-path (top-down with supplier roll-up checks) modeling minimize these distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.40 B (2025) | Mordor Intelligence | - |

| USD 14.8 B (2024) | Global Consultancy A | Bundles imaging systems and practice consumables |

| USD 6.67 B (2024) | Industry Analyst B | Excludes direct-to-consumer aligner sales and uses static ASP |

| USD 8.29 B (2025) | Trade Journal C | Applies uniform growth to all regions without prevalence weighting |

These comparisons show that our patient-based build, live price tracking, and annual refresh deliver a balanced, transparent baseline clients can rely on for strategic planning.

Key Questions Answered in the Report

How large is the orthodontic supplies market in 2025?

The orthodontic supplies market generated USD 7.40 billion in 2025 and is projected to reach USD 10.11 billion by 2030 at an 8.13% CAGR.

Which product segment is growing the fastest?

Clear aligners are expanding at a 20.3% CAGR, reflecting consumer preference for aesthetic, removable appliances and widespread digital workflow adoption.

Why is adult demand accelerating?

Adults seek discreet treatment backed by workplace acceptance and remote work flexibility, boosting the adult segment’s 13.0% CAGR and supporting premium aligner sales.

How will digital platforms influence future growth?

DTC and hybrid models deliver a 16.6% CAGR by combining remote convenience with in-office scans, forcing traditional clinics to digitize processes and financing options.

What role does sustainability play in material innovation?

Patient concern over environmental impact drives an 18.0% CAGR in thermoplastic polyurethane and stimulates R&D in bio-resorbable and recyclable aligner materials.

Which region offers the strongest growth prospects?

Asia Pacific leads with an 11.0% CAGR, driven by high malocclusion prevalence, rising disposable income, and rapid adoption of digital orthodontic technologies.

Page last updated on: