Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

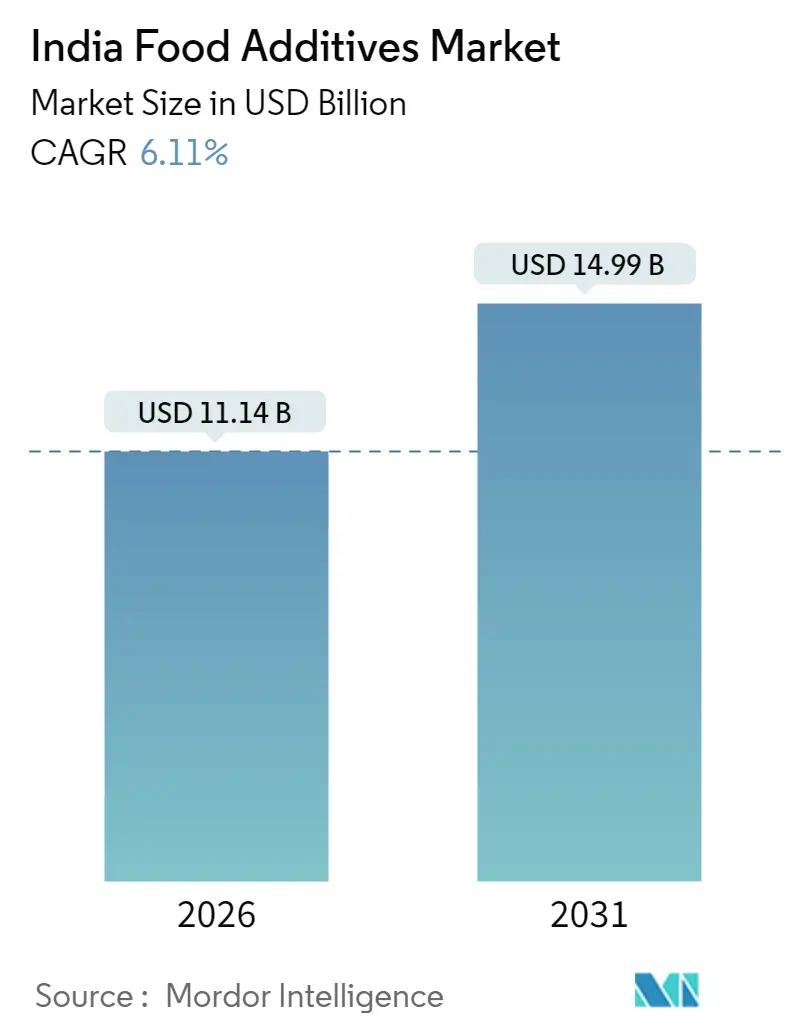

| Market Size (2026) | USD 11.14 Billion |

| Market Size (2031) | USD 14.99 Billion |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Food Additives Market Analysis by Mordor Intelligence

The Indian food additives market is expected to grow from USD 10.50 billion in 2025 to USD 11.14 billion in 2026 and is forecast to reach USD 14.99 billion by 2031 at 6.11% CAGR over 2026-2031. Rising urban incomes, shifting dietary habits, and sustained government incentives for food processing underpin this expansion trajectory. Manufacturers continue to scale capacity because packaged foods, quick-service restaurants, and e-commerce grocery platforms require dependable solutions that lengthen shelf life, optimize texture, and deliver consistent taste. At the same time, consumer scrutiny of labels is steering demand toward plant-based colorants, natural sweeteners, and fermentation-derived preservatives. Technology adoption—ranging from AI-assisted formulation to enzyme fermentation—enables producers to improve yields while meeting stricter quality norms. Collectively, these trends keep the Indian food additives market on a steady growth path even as raw-material cost swings and evolving safety regulations add complexity.

Key Report Takeaways

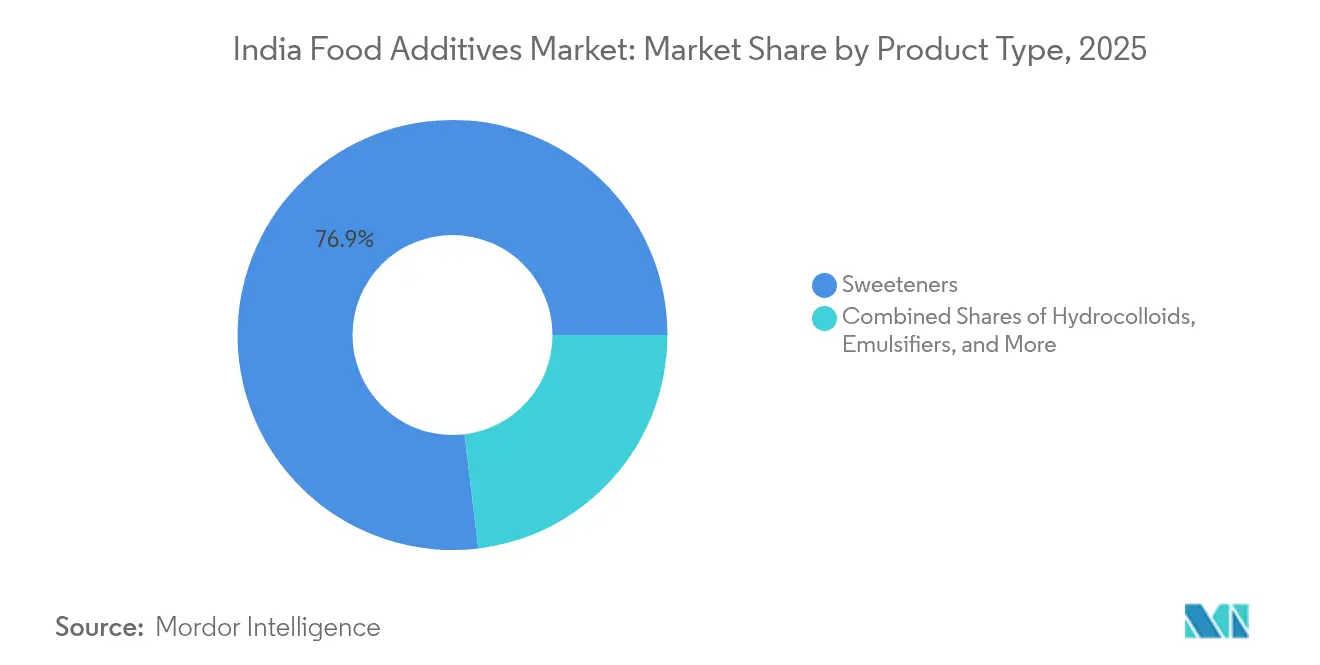

- By product type, sweeteners led with 76.92% of the Indian food additives market share in 2025, while food colorants are projected to expand at a 7.59% CAGR through 2031.

- By source, natural ingredients commanded 52.10% of the Indian food additives market in 2025 and are forecast to advance at a 7.42% CAGR between 2026 and 2031.

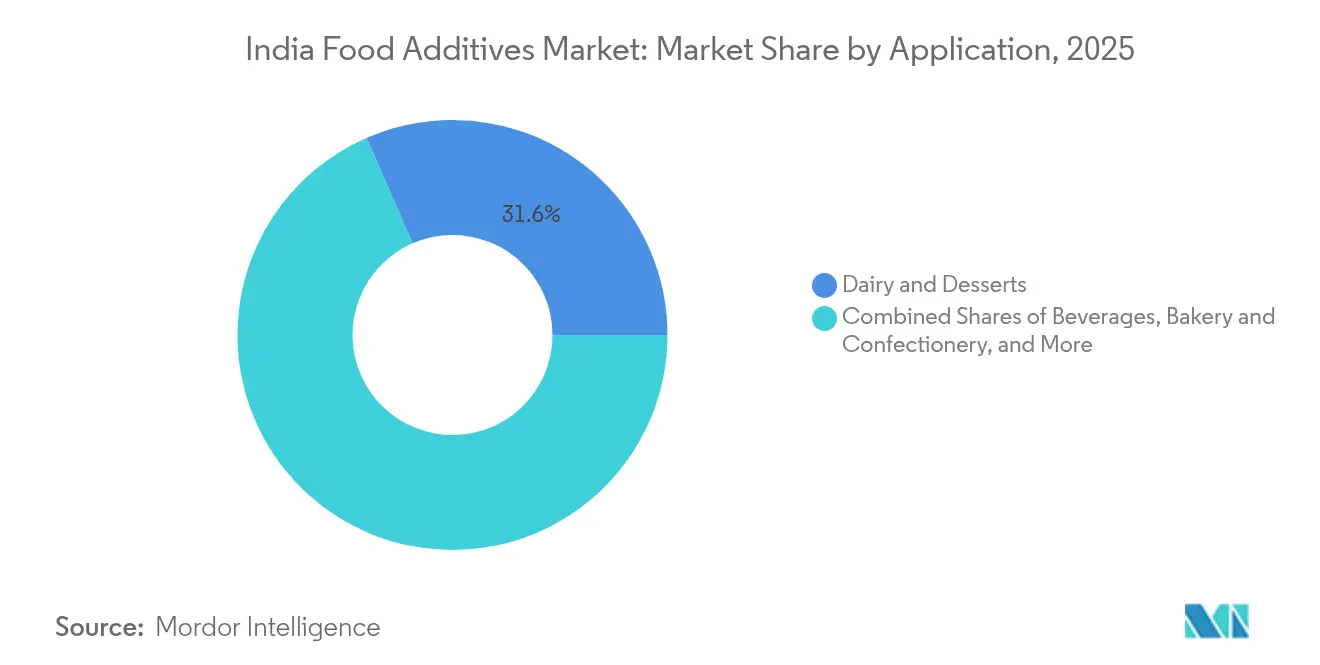

- By application, dairy and desserts accounted for a 31.55% share of the Indian food additives market in 2025; beverages represent the fastest-growing application and are poised for a 7.02% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Food Additives Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for processed and convenience foods | +1.2% | National, with concentration in urban centers and tier-1 cities | Medium term (2-4 years) |

| Rising demand for natural, clean-label, and organic food additives | +1.5% | National, with premium segments in metropolitan areas | Long term (≥ 4 years) |

| Government initiatives supporting food processing industry growth | +0.8% | National, with focus on food processing clusters and SEZs | Short term (≤ 2 years) |

| Technological advancements in additive formulation | +0.7% | Industrial hubs in Maharashtra, Gujarat, Tamil Nadu | Medium term (2-4 years) |

| Growing popularity of functional foods and fortified products | +0.6% | Urban markets with spillover to semi-urban areas | Long term (≥ 4 years) |

| Rising export opportunities | +0.4% | Coastal states and export-oriented manufacturing zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Processed and Convenience Foods

India's urbanization, now encompassing 35% of the population, is driving a significant rise in processed food consumption. Working professionals are increasingly opting for ready-to-eat meals and packaged snacks. In 2024, the organized food processing sector recorded an 8.2% growth, surpassing the overall manufacturing sector. This expansion is primarily due to companies investing in preservation technologies and shelf-life extension solutions, as noted by the Ministry of Statistics and Programme Implementation[1]Ministry of Statistics and Programme Implementation, “Annual Survey of Industries 2024,” mospi.gov.in. Quick-service restaurant chains and food delivery platforms are further boosting the demand for standardized food additives, which are essential for maintaining consistent taste, texture, and appearance across multiple preparation centers. Additionally, tier-2 cities are becoming key growth drivers, with household spending on packaged foods rising by 12% annually. This growth necessitates the use of preservatives, emulsifiers, and flavor enhancers to ensure product quality across extended distribution networks. The transition from traditional cooking to convenience foods is also increasing the demand for natural preservatives and clean-label solutions, as health-conscious consumers prioritize processed options that retain nutritional value.

Rising Demand for Natural, Clean-Label, and Organic Food Additives

With growing health consciousness, 67% of Indian consumers actively examine ingredient labels to avoid synthetic chemicals, as revealed by recent studies. The Food Safety and Standards Authority of India (FSSAI)[2]Food Safety and Standards Authority of India, “Food Additives Regulations and Standards,” fssai.gov.inhas implemented progressive regulations, introducing updated standards for plant-based colorants and organic preservatives, which are accelerating the adoption of natural additives. Leading food brands such as Britannia and Parle are spearheading this transition by reformulating products to incorporate natural alternatives and promoting clean-label initiatives that exclude artificial preservatives and synthetic colors. The organic food market, growing at an impressive 20% annually, is driving increased demand for certified organic additives, particularly in dairy, bakery, and beverage sectors, where natural ingredients command higher prices. Additionally, export-focused food manufacturers are adopting natural additives to comply with international certification standards and to cater to global markets that are increasingly rejecting synthetic food chemicals.

Government Initiatives Supporting Food Processing Industry Growth

To promote food ingredient manufacturing, state governments in Maharashtra, Gujarat, and Tamil Nadu provide incentives such as land subsidies and tax benefits, which help reduce operational costs for additive producers, as noted by Invest India. The National Mission on Food Processing is developing specialized clusters with shared infrastructure for testing, quality control, and regulatory compliance. This initiative lowers barriers for smaller additive manufacturers seeking FSSAI certification. Additionally, export promotion schemes offer financial assistance to food additive companies targeting international markets, with a strong focus on natural and organic ingredients that align with global clean-label trends. Meanwhile, the PM Gati Shakti initiative is driving infrastructure development, improving cold chain logistics, and reducing transportation costs. This enables additive manufacturers to reach broader geographic markets while ensuring product stability.

Technological Advancements in Additive Formulation

Indian companies are leveraging biotechnology to transform additive production through fermentation processes that develop natural substitutes for synthetic chemicals. The integration of artificial intelligence in food formulation facilitates precise additive dosing and predictive quality control, reducing waste and enhancing consistency in large-scale production, as noted by the Indian Institute of Food Processing Technology[3]Indian Institute of Food Processing Technology, “Technology Innovations in Food Processing,” iifpt.edu.in. Additionally, nanotechnology improves additive stability and enables controlled release, particularly for functional ingredients and nutraceuticals, where targeted delivery enhances effectiveness. Advanced extraction methods are increasing the yield and purity of plant-based additives while reducing environmental impact, supporting the shift toward natural additives with commercially viable production techniques. Moreover, automation in additive manufacturing is cutting labor costs and improving quality consistency, enabling Indian producers to compete with international suppliers on both price and quality metrics.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuations in raw material prices | -0.9% | National, with higher impact on import-dependent regions | Short term (≤ 2 years) |

| Health concerns over synthetic additives | -0.7% | Urban markets and health-conscious consumer segments | Medium term (2-4 years) |

| Supply chain complexities and infrastructure gaps | -0.5% | Rural and semi-urban manufacturing locations | Medium term (2-4 years) |

| Labeling challenges and transparency pressures | -0.3% | National, with focus on export-oriented manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fluctuations in Raw Material Prices

Key inputs in additive manufacturing, including citric acid, lecithin, and natural extracts, have experienced price fluctuations of 15-25%, driven by supply chain disruptions and weather-related crop yield variations. Indian manufacturers, who rely heavily on imports for specialized raw materials, are exposed to currency fluctuations and international trade policies. Approximately 40% of premium additive ingredients are sourced from regions such as China, Europe, and Southeast Asia. Additionally, energy costs for additive production, particularly for processes like spray-drying and fermentation, are influenced by crude oil prices and domestic coal availability, directly impacting profit margins for energy-intensive operations. Small and medium-scale additive manufacturers face difficulties in managing raw material inventory and price hedging, which limits their ability to compete with larger players that utilize economies of scale to mitigate short-term cost variations.

Health Concerns Over Synthetic Additives

Growing consumer awareness of potential health risks associated with artificial preservatives, colors, and flavor enhancers drives demand away from synthetic additives, forcing manufacturers to invest in more expensive natural alternatives. Regulatory scrutiny increases as FSSAI reviews safety standards for synthetic additives, with potential restrictions on certain artificial colors and preservatives creating uncertainty for manufacturers dependent on these ingredients. Media coverage of health studies linking synthetic additives to various health concerns influences consumer purchasing decisions, particularly among educated urban consumers who actively avoid products containing artificial ingredients. The premium pricing of natural alternatives creates market segmentation challenges, as price-sensitive consumers may reduce overall consumption of processed foods rather than accept higher costs for natural additive-based products.

Segment Analysis

By Product Type: Sweeteners Dominate Despite Colorant Innovation

In 2025, sweeteners hold a dominant 76.92% market share, highlighting India's role as a leading sugar producer and the extensive use of sugar alternatives in processed foods, beverages, and pharmaceuticals. Food colorants, driven by consumer preferences for visually appealing products and regulatory shifts favoring natural colorants like turmeric, beetroot, and spirulina, are the fastest-growing segment with a 7.59% CAGR through 2031, as supported by the Food Safety and Standards Authority of India. Preservatives continue to see stable demand in bakery and dairy applications, while emulsifiers benefit from the growth of processed food manufacturing and increasing texture requirements in convenience foods. Enzymes are gaining popularity in brewing, baking, and dairy processing as manufacturers focus on process optimization and natural alternatives to chemical treatments.

These segment trends reflect a broader industry movement toward natural ingredients. As regulatory approvals increase and consumer acceptance grows, synthetic sweetener demand is declining, paving the way for alternatives like stevia and monk fruit. Anti-caking agents are essential in spice processing and powdered food production. Hydrocolloids are increasingly used in gluten-free and plant-based food formulations. Food flavors and enhancers are experiencing growth due to the expanding snack food industry and the rising restaurant sector, particularly in tier-2 cities where organized food services are rapidly growing. Acidulants maintain steady demand in beverages and preservation applications, supporting the market's overall growth despite variations in adoption rates across segments.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Source: Natural Ingredients Lead Both Share and Growth

The Natural segment captures 52.10% market share in 2025 while simultaneously leading growth at 7.42% CAGR through 2031, indicating a fundamental market shift toward clean-label ingredients driven by health-conscious consumers and regulatory support for natural alternatives. This dual leadership position reflects consumer willingness to pay premium prices for natural additives, with organic and plant-based ingredients commanding 20-30% price premiums over synthetic alternatives. Synthetic additives retain significant market presence due to cost advantages and established supply chains, particularly in price-sensitive applications like bulk food processing and industrial bakery operations.

Biotechnology advances enable natural additive production at competitive costs, with fermentation-based processes creating natural alternatives that match synthetic additive performance characteristics. Companies like DSM-Firmenich invest in biotechnology platforms for natural ingredient production, while domestic manufacturers develop extraction capabilities for indigenous plants and herbs. The regulatory environment increasingly favors natural ingredients, with FSSAI streamlining approval processes for plant-based additives while maintaining stringent testing requirements for synthetic alternatives. Export market requirements drive natural additive adoption, as international buyers increasingly specify natural ingredients to meet consumer preferences in developed markets.

By Application: Dairy Leadership Meets Beverage Innovation

In 2025, Dairy and Desserts applications hold a 31.55% market share, supported by India's status as the world's largest milk producer. The organized dairy sector is increasingly focusing on value-added products such as flavored milk, yogurt, and ice cream. Beverages are the fastest-growing segment, with a 7.02% CAGR projected through 2031. This growth is attributed to rising soft drink consumption, the popularity of functional beverages, and the increasing adoption of packaged drinks in tier-2 and tier-3 cities, as highlighted by the Indian Beverage Association. Bakery and Confectionery applications continue to grow steadily, driven by the expansion of organized retail and changing snacking preferences that favor packaged baked goods and confectionery items.

Meat and Meat Products applications are benefiting from increased protein consumption and improvements in cold chain infrastructure. Soups, Sauces, and Dressings are gaining popularity due to the growing demand for cooking convenience in urban households. This application mix reflects India's dietary shift towards processed and convenience foods. Traditional cooking methods are increasingly being supplemented by packaged alternatives that rely on specialized additives to enhance taste, texture, and preservation. Regional preferences significantly influence application growth, with southern states showing higher demand for dairy additives and western regions leading in beverage and snack food applications. The 'Other Applications' category is also expanding, including plant-based foods, nutraceuticals, and specialty dietary products, which offer niche opportunities for innovative additive solutions.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

India's food additives market demonstrates distinct regional consumption trends. Maharashtra, Gujarat, and Tamil Nadu dominate both production and consumption due to their concentrated food processing industries and well-established manufacturing infrastructure. These states benefit from proximity to major ports, facilitating efficient raw material imports and finished product exports. They also host key multinational food companies and domestic manufacturers. The western region, particularly Gujarat and Maharashtra, leads in dairy additive consumption, supported by extensive milk processing facilities and cooperative dairy networks. In contrast, southern states like Tamil Nadu and Karnataka excel in beverage and processed food applications.

Urban centers are the primary drivers of premium additive demand, with metropolitan areas accounting for approximately 60% of natural and organic additive consumption, despite representing only 35% of the population. Meanwhile, rural and semi-urban markets are increasingly adopting processed foods, creating a demand for cost-effective preservatives and basic additives that enhance shelf life and ensure food safety, particularly in regions with limited cold chain infrastructure. The government's efforts to develop food processing clusters in states such as Uttar Pradesh, Punjab, and West Bengal are fostering new regional demand centers, especially for grain-based and agricultural product processing. Additionally, export-oriented manufacturing is concentrated in coastal states, where companies produce additives that meet international quality standards, catering to global food manufacturers seeking cost-effective ingredient sourcing from India.

Regional regulatory compliance varies in terms of implementation speed, with industrially advanced states often achieving faster FSSAI certification and adopting quality standards more quickly, providing manufacturers in these areas with a competitive advantage. Infrastructure improvements under national logistics programs are enhancing connectivity between production hubs and consumption markets, reducing transportation costs and expanding the geographic reach of additive manufacturers. Climate factors also influence regional demand patterns. Tropical regions require more robust preservative systems, while temperate areas focus on texture and flavor enhancements that align with local food preferences and processing traditions.

Competitive Landscape

The India Food Additives Market exhibits moderate concentration with a 6 out of 10 rating, reflecting a competitive landscape where established multinational corporations compete alongside emerging domestic manufacturers and specialized ingredient suppliers. Global players like Cargill, DSM-Firmenich, and BASF leverage advanced technology platforms and extensive R&D capabilities to introduce innovative natural additives and biotechnology-derived solutions, while domestic companies like Sunshine Chemicals and Vinayak Ingredients focus on cost-effective production and local market expertise.

Strategic partnerships between international technology providers and Indian manufacturers accelerate market development, with companies pursuing joint ventures for specialized applications like enzyme production and natural colorant extraction. Technology adoption drives competitive differentiation, with leading companies investing in fermentation capabilities, AI-driven formulation optimization, and sustainable production processes that reduce environmental impact while improving cost efficiency. Patent filings in biotechnology applications and natural extraction processes indicate intensifying innovation competition, particularly in areas like plant-based preservatives and functional ingredient development Indian Patent Office.

White-space opportunities emerge in specialized segments like clean-label solutions for traditional Indian foods, export-quality natural additives, and application-specific formulations for emerging food categories such as plant-based proteins and functional beverages. Smaller players increasingly focus on niche applications and regional specialization, creating a fragmented competitive environment that rewards innovation and customer-specific solutions over pure scale advantages.

India Food Additives Industry Leaders

Cargill, Incorporated

BASF SE

Ingredion Incorporated

Kerry Group Plc

DSM-Firmenich

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2024: In a strategic move to tap into India's vast potential, DSM-Firmenich earmarked an investment of over USD 100 million (exceeding Rs 835 crore) in the country. The investment primarily focuses on capacity expansion, which includes establishing a new manufacturing plant.

- March 2024: BASF introduced a new flavor from its Isobionics portfolio. The newly launched product, Natural Beta-caryophyllene 80, boasts an aromatic profile reminiscent of herbaceous notes, with hints of green parsley, black pepper, grapefruit, and a touch of clary sage.

- February 2024: Ingredion Incorporated rolled out its newest product, the NOVATION Indulge 2940 starch. Marking a significant milestone, this starch is the company's first non-GMO functional native corn starch in its clean-label texturizers lineup. Its unique texture is tailored for gelling and co-texturizing, making it an excellent choice for traditional and alternative dairy products, as well as desserts.

- October 2023: DSM-Firmenich announced the extension of its partnership with Azelis. Effective immediately, Azelis India is the sole distributor of DSM-Firmenich’s food enzymes and cultures range throughout India, a portfolio that includes dairy cultures, dairy enzymes, dairy test kits, and bakery enzymes.

India Food Additives Market Report Scope

Food additives enhance food safety, freshness, taste, texture, shelf life, and appearance during processing or manufacturing.

The food additives market in India is categorized by type and application. The types include preservatives, sweeteners, sugar substitutes, emulsifiers, anti-caking agents, enzymes, hydrocolloids, food flavors and enhancers, food colorants, and acidulants. Applications span dairy and frozen, bakery, meat and seafood, beverages, confectionery, and more.

Market sizing is presented in USD value terms for all segments mentioned above.

By Product Type

| Preservatives |

| Sweeteners |

| Sugar Substitutes |

| Emulsifiers |

| Anti-Caking Agents |

| Enzymes |

| Hydrocolloids |

| Food Flavors & Enhancers |

| Food Colorants |

| Acidulants |

By Source

| Natural |

| Synthetic |

By Application

| Bakery and Confectionery |

| Dairy and Desserts |

| Beverages |

| Meat and Meat Products |

| Soups, Sauces, and Dressings |

| Other Applications |

| By Product Type | Preservatives |

| Sweeteners | |

| Sugar Substitutes | |

| Emulsifiers | |

| Anti-Caking Agents | |

| Enzymes | |

| Hydrocolloids | |

| Food Flavors & Enhancers | |

| Food Colorants | |

| Acidulants | |

| By Source | Natural |

| Synthetic | |

| By Application | Bakery and Confectionery |

| Dairy and Desserts | |

| Beverages | |

| Meat and Meat Products | |

| Soups, Sauces, and Dressings | |

| Other Applications |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the India food additives market in 2026?

The market is valued at USD 11.14 billion in 2026 and is projected to reach USD 14.99 billion in 2031.

Which product type holds the biggest share?

Sweeteners command 76.92% of value, reflecting India’s sugar availability and the wide use of sugar substitutes.

Which segment is growing the fastest?

Food colorants are forecast to post a 7.59% CAGR through 2031 as natural pigments gain traction.

Which application drives additive demand the most?

Dairy and desserts lead with 31.55% share because of India’s large milk base and rising value-added dairy production.