Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 30.20 Billion |

| Market Size (2031) | USD 41.09 Billion |

| Growth Rate (2026 - 2031) | 6.35% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Respiratory Devices Market Analysis by Mordor Intelligence

The Respiratory Devices Market size is estimated at USD 30.20 billion in 2026, and is expected to reach USD 41.09 billion by 2031, at a CAGR of 6.35% during the forecast period (2026-2031).

Robust growth flows from three converging forces—population aging in high-income nations, deteriorating air quality in several emerging economies, and mainstream adoption of remote monitoring—which collectively pivot care toward continuous, home-based management. Therapeutic platforms that integrate real-time data exchange now influence formulary decisions, especially under value-based reimbursement contracts in the United States. At the same time, lithium-iron-phosphate batteries lengthen portable oxygen concentrator runtimes, enabling ambulatory use that was not feasible only a few years ago. Device makers are also racing to reduce the regulatory drag imposed by Europe’s CE-MDR backlog and China’s Class III reclassification, often by designing modular platforms that can be re-configured for multiple jurisdictions. These dynamics support a diversified pipeline of products capable of shifting therapy from episodic hospital interventions to continuous home settings, reinforcing the upward trajectory of the respiratory devices market.

Key Report Takeaways

- By device type, Therapeutic Devices commanded 47.55% of the respiratory devices market share in 2025, and their revenue is advancing at an 11.25% CAGR through 2031.

- By indication, Infectious Diseases is expanding at a 10.85% CAGR, the fastest among all clinical segments, while COPD retained 35.53% of 2025 revenue.

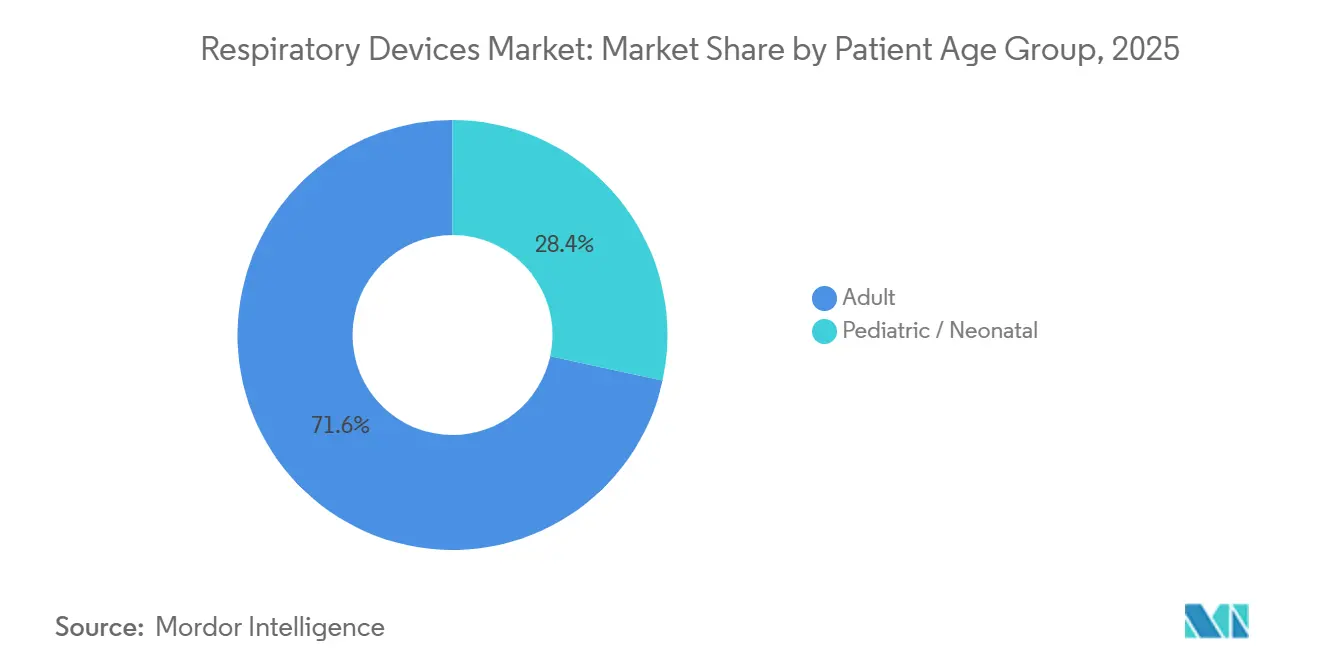

- By patient age group, the Adult segment accounted for 71.63% of 2025 demand; the Home Settings end-user category is scaling at 11.7% to 2031.

- By end user, hospitals commanded 56.23% share of the respiratory devices market size in 2025; home settings are expanding at a 11.7% CAGR during 2026-2031.

- By geography, North America led with 39.13% of 2025 sales, whereas Asia-Pacific is pacing the field at a 10.51% CAGR, supported by large-scale reimbursement programs in China and India.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Respiratory Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in prevalence of respiratory disorders | +1.8% | Global, acute in South Asia and Sub-Saharan Africa | Long term (≥ 4 years) |

| Technological advancements in devices | +1.5% | North America and Europe lead; APAC drives manufacturing | Medium term (2-4 years) |

| Home-healthcare equipment penetration | +1.4% | Core in North America and Western Europe; urban APAC rising | Medium term (2-4 years) |

| Government initiatives and reimbursement | +1.1% | United States, European Union, India | Short term (≤ 2 years) |

| Tele-connected respiratory care platforms | +0.9% | United States, Germany, Australia | Medium term (2-4 years) |

| Demand for ultra-portable oxygen concentrators | +0.7% | Global, highest in aging societies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Prevalence of Respiratory Disorders

More than 545 million people live with chronic respiratory diseases, and COPD caused 3.2 million deaths in 2024. Dual-exposure patterns magnify the burden: older adults in wealthy countries experience age-linked lung decline, whereas low-income settings face indoor biomass combustion and severe outdoor particulate pollution. India’s National Health Profile noted a 23% jump in asthma admissions among urban children under 15 during 2025 winter spikes of PM2.5 to 89 µg/m³. In the United States, sleep apnea prevalence reached 38% among adults over 50 in 2025, a trend tied to obesity plateaus and broader use of home sleep tests[1]Centers for Disease Control and Prevention, “Sleep and Sleep Disorders,” cdc.gov. Infectious diseases add to the load: tuberculosis recorded 10.8 million new cases in 2024, many requiring long nebulized regimens. These epidemiological realities keep demand high for diagnostic spirometers and therapeutic systems across the respiratory devices market.

Technological Advancements in Diagnostic & Therapeutic Devices

Miniaturization and connectivity shift sophisticated pulmonary testing from the lab to primary care. In 2025, the FDA cleared 14 AI-enabled spirometry platforms with 91% sensitivity for early COPD detection. Philips launched the DreamStation 3 CPAP in late 2024, integrating leak-compensation algorithms that reduced therapy abandonment by 19%. Mesh nebulizers attained 85% lung-deposit efficiency in 2025 trials, trimming medication waste. Portable oxygen concentrators now run eight hours at 2 l/min on lithium-iron-phosphate power packs. Ventilators featuring closed-loop automation cut ventilator-induced injury 27% in ICU environments, closing the performance gap between hospital and home devices.

Rapid Penetration of Home-Healthcare Respiratory Equipment

Coverage reform, not patient preference, drives the shift to home-based therapy. CMS removed prior authorization for home ventilators in 2025 and raised monthly rental caps to USD 850. Private insurers mirrored the move, linking reimbursement to readmission reduction. Germany approved home CPAP for mild sleep apnea in 2024, citing cardiovascular risk reduction. Japan now subsidizes 70% of device costs for adults over 75, aiming to migrate 120,000 ventilator users to home care by 2028. Fiscal math underpins adoption: home ventilation costs around USD 12,000 annually versus USD 180,000 in hospital settings. Infrastructure gaps in rural regions remain a constraint, but the economic imperative favors continued diffusion.

Government Initiatives & Reimbursement Expansion

Universal health programs increasingly embed respiratory devices to curb downstream acute-care expenditure. India’s Ayushman Bharat added nebulizers and pulse oximeters to its essential list in 2024, subsidizing 80% of costs for 500 million beneficiaries. China instituted provincial reimbursement for home oxygen in 2025, capping 5-liter concentrators at CNY 3,500 (USD 480). Australia’s Therapeutic Goods Administration halved clearance timelines for connected respiratory monitors, enabling faster commercialization. These measures widen access and accelerate revenue capture across the respiratory devices market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced devices | -0.9% | Emerging markets in Asia and Africa | Long term (≥ 4 years) |

| Multi-jurisdiction regulatory clearance | -0.7% | Europe (CE-MDR) and China (NMPA Class III) | Medium term (2-4 years) |

| Lithium-ion battery supply constraints | -0.5% | Global, especially portable oxygen concentrators | Short term (≤ 2 years) |

| Data-privacy concerns for connected devices | -0.4% | United States, Europe, Brazil, India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Devices

A hospital ICU ventilator lists for USD 25,000–50,000, while a home CPAP system ranges from USD 800–2,500—figures far above annual per-capita health budgets in many low-income nations. Only 18% of Indian COPD patients prescribed oxygen therapy actually acquire concentrators, underscoring affordability gaps. Tiered product lines aim to bridge the divide; ResMed’s USD 650 AirMini CPAP omits cellular connectivity to hit cash-pay price points. Pay-per-use leasing via Kenya’s M-TIBA lowers the barrier to USD 3 per day but still reaches less than 5% of potential users.

Stringent Multi-Jurisdiction Regulatory Clearance

Europe’s CE-MDR now mandates clinical investigations for Class IIb respiratory devices, pushing review cycles to 18–24 months and costing roughly USD 380,000 per submission[2]European Commission, “Medical Device Regulation (MDR),” ec.europa.eu . China’s NMPA reclassified connected nebulizers as Class III in 2025, adding 14 months to approvals. Although FDA 510(k) median review times remain near 150 days, software updates that alter clinical claims now require fresh submissions. Larger incumbents manage these burdens, but startups face capital and time hurdles that can slow innovation diffusion within the respiratory devices market.

Segment Analysis

By Device Type: Therapeutic Devices Extend Their Lead

Therapeutic platforms held 47.55% of revenue in 2025, and the segment is projected to grow 11.25% through 2031. The respiratory devices market size attributed to CPAP and BiPAP systems continues to swell on the back of rising obstructive sleep apnea diagnoses among adults over 50. Portable oxygen concentrators, now able to support eight-hour outdoor use, are also expanding access for ambulatory COPD patients. Home ventilators benefit from CMS reimbursement changes, while smart inhalers with Bluetooth dose logging reached 12% penetration in 2025.

Diagnostic and Monitoring systems captured 32% of 2025 revenue with a slower 5.8% CAGR as commoditization pressures margins. The respiratory devices market share for handheld, AI-guided spirometry is increasing, but average selling prices fell for pulse oximeters due to Chinese competition. Consumables such as single-use masks and tubing represented 20.45% of 2025 revenue and will track overall procedure volumes, especially as infection-control protocols remain stringent.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Indication: Infectious Diseases Gain Momentum

COPD generated 35.53% of 2025 sales, anchored by lifelong oxygen and bronchodilator needs. Yet Infectious Diseases—led by tuberculosis and pandemic preparedness spending—show the fastest 10.85% CAGR, lifting the respiratory devices market size allocated to mesh nebulizers and portable ventilators. Asthma retains a strong 28% share, with adherence-tracking inhalers now a payer focus. Sleep apnea remains significant in developed economies, while Other Respiratory Disorders, including cystic fibrosis, secure steady growth as survival rates improve.

By Patient Age Group: Adults Dominate, Pediatrics Trails

Adults contributed 71.63% of 2025 revenue and will grow 8.87% to 2031 as the global 65-plus population rises. Higher reimbursement ceilings and co-morbid obesity support demand for advanced BiPAP devices. Pediatric and neonatal segments grow at a slower 5.2%, constrained by declining birth rates in wealthier countries and stricter regulatory pathways. Neonatal ventilators still see incremental volume increases in emerging markets adding NICU beds.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: Home Settings Accelerate

Hospitals retained 56.23% of 2025 sales, but Home Settings are advancing at an 11.7% CAGR on the strength of tele-connected equipment and payer incentives to cut readmissions. Respiratory and sleep clinics remain important for diagnostic throughput, while ambulatory centers grow in tandem with same-day bronchoscopy volumes. Devices conceived for intuitive home use are best positioned to capture the high-growth end-user shift shaping the respiratory devices market.

Geography Analysis

North America generated 39.13% of 2025 revenue, with the United States alone spending USD 9.8 billion on respiratory equipment. Growth moderates to 6.2% as CPAP penetration approaches saturation, but software-enabled upgrades and home ventilator adoption still lift value. Canada’s Assistive Devices Program added portable concentrators, and Mexico’s social security institute widened CPAP coverage, adding incremental volumes.

Asia-Pacific is the fastest-growing region at a 10.51% CAGR. China’s provincial reimbursement for home oxygen aims at 100 million COPD patients, while India’s Ayushman Bharat subsidizes nebulizers for 500 million citizens. Japan’s subsidy covering 70% of device costs for seniors accelerates the move to home ventilation, and South Korea broadened CPAP coverage to mild cases. Australia’s expedited pathway for connected monitors further catalyzes product launches.

Europe accounted for 28% of 2025 revenue but grows at a muted 5.9% as CE-MDR bottlenecks slow new device rollouts. Germany remains the largest national market after approving home CPAP for mild cases. The United Kingdom boosted home respiratory allocations under its NHS Long Term Plan, and France raised monthly reimbursements for home ventilators, improving supplier economics.

Middle East and Africa held 6% of sales, powered by GCC hospital investments and South Africa’s public-sector purchase of concentrators. South America contributed 5.87% as Brazil’s SUS added home CPAP coverage for 1.2 million patients, offering fresh demand in a historically under-penetrated market.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The respiratory devices market shows moderate concentration: ResMed, Philips, Medtronic, GE HealthCare, and Fisher & Paykel collectively held a significant percentage of the 2025 revenue. ResMed leverages an installed base of 8 million cloud-connected CPAP users through its myAir platform, giving payers real-time adherence metrics. Philips secures hospital accounts with DreamMapper integration into electronic health records. Mindray and Beijing Aeonmed undercut Western rivals by 30–40% in China’s ventilator tenders, aided by local regulatory momentum.

Software and services differentiate premium offerings. Drägerwerk’s AI-guided SmartPilot View lowered ICU stays by 1.8 days in German trials, while Fisher & Paykel’s Optiflow high-flow nasal system now owns 34% of ICU support after reducing intubations 22%. New entrants such as React Health focus on cloud-native spirometry that bills per test, exploiting gaps in outpatient pulmonary diagnostics. ISO 13485 and IEC 60601 compliance costs continue to discourage smaller firms, reinforcing incumbents’ scale advantages and preserving their slice of the respiratory devices market.

Respiratory Devices Industry Leaders

Koninklijke Philips N.V.

Medtronic plc

GE HealthCare

ResMed

Fisher & Paykel Healthcare Limited.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Olympus partnered with the COPD Foundation to expand patient education on emphysema treatment options.

- May 2025: Trixeo Aerosphere gained U.K. approval as the first inhaled respiratory medicine using a near-zero global-warming-potential propellant.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the respiratory devices market as all diagnostic, monitoring, therapeutic, and single-use consumable equipment that supports or measures human respiration across hospitals, sleep clinics, and home-care settings. Typical products include spirometers, pulse oximeters, ventilators, oxygen concentrators, CPAP/BiPAP systems, nebulizers, and patient interfaces.

Accessories sold purely for anesthesia delivery or industrial respiratory protection fall outside this scope.

Segmentation Overview

- By Device Type

- Diagnostic & Monitoring Devices

- Spirometers

- Sleep Test Devices

- Peak Flow Meters

- Pulse Oximeters

- Capnographs

- Other Diagnostic & Monitoring Devices

- Therapeutic Devices

- CPAP Devices

- BiPAP Devices

- Humidifiers

- Nebulizers

- Oxygen Concentrators

- Ventilators

- Inhalers

- Other Therapeutic Devices

- Consumables & Disposables

- Masks

- Breathing Circuits & Tubing

- Other Disposables

- Diagnostic & Monitoring Devices

- By Indication

- COPD

- Asthma

- Sleep Apnea

- Infectious Diseases

- Other Respiratory Disorders

- By Patient Age Group

- Adult

- Pediatric / Neonatal

- By End User

- Hospitals

- Respiratory & Sleep Clinics

- Ambulatory Surgical & Emergency Centers

- Home Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with respiratory therapists, biomedical engineers, procurement heads, and home-oxygen distributors across North America, Europe, and key Asian markets helped us validate installed base estimates, average selling prices, and post-COVID demand shifts. Follow-up surveys captured patient migration toward home therapy and regional reimbursement nuances.

Desk Research

Mordor analysts first screened open datasets from bodies such as the World Health Organization, the Global Burden of Disease project, Eurostat, the US FDA 510(k) database, and UN Comtrade to size patient pools and trade flows. Industry position papers from groups like MedTech Europe, the American Association for Respiratory Care, and peer-reviewed journals added context on adoption curves. Financial signals were drawn from company 10-Ks and D&B Hoovers, while news trends were monitored through Dow Jones Factiva. This list is illustrative; many other public and subscription sources informed the desk work.

Market-Sizing & Forecasting

A top-down model rebuilt demand from the prevalence of COPD, asthma, sleep apnea, and critical-care admissions, which are then mapped to device penetration rates and average replacement cycles. Select bottom-up checks, supplier shipment tallies, hospital bed counts, and sampled ASP × volume refined totals. Core variables include ICU bed growth, home-care enrollment, ventilator density per 1,000 beds, disposable change-out frequency, and average oxygen concentrator life. A multivariate regression links these drivers to historical sales and projects them through 2030, with scenario analysis adjusting for policy or reimbursement shocks. Data gaps are bridged using regional proxies vetted through expert calls.

Data Validation & Update Cycle

Outputs undergo variance checks against independent import data and epidemiological series. Senior reviewers sign off after anomaly resolution. Reports refresh every twelve months, and we trigger interim updates when recalls, reimbursement changes, or pandemics materially alter demand.

Why Mordor's Respiratory Devices Baseline Commands Reliability

Published numbers often differ because firms pick unlike product baskets, inflate or dampen ASP growth, or refresh at uneven intervals. Mordor applies a patient-centric scope, annual refresh cadence, and dual-sourced price audits, so our 2025 baseline aligns closely with real device flows.

Key gap drivers include competitors omitting disposables, bundling anesthesia units, or using fixed exchange rates that distort multi-currency revenues.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 28.40 Bn (2025) | Mordor Intelligence | |

| USD 23.60 Bn (2025) | Regional Consultancy A | Drops home-care volumes and uses static ASP assumptions |

| USD 54.10 Bn (2024) | Global Consultancy B | Adds anesthesia devices and converts revenue at year-end rates only |

Taken together, the comparison shows that Mordor delivers a balanced, clearly scoped baseline grounded in patient need, validated device shipments, and transparent recalibration points, giving decision-makers a dependable reference for planning.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the respiratory devices market in 2026?

The respiratory devices market size stood at USD 30.20 billion in 2026 and is projected to reach USD 41.09 billion by 2031.

Which segment is expanding the fastest?

Therapeutic Devices are growing at an 11.25% CAGR, the highest among all product categories.

What drives Asia-Pacific demand?

Expanded public reimbursement in China and India plus aging demographics in Japan propel Asia-Pacific growth at a 10.51% CAGR.

How is home care affecting device demand?

Payer incentives and tele-monitoring systems are shifting therapy toward home settings, which are scaling at 11.7% annually.

What regulatory changes are most impactful?

Europe's CE-MDR and China's Class III reclassification lengthen approval timelines and raise compliance costs, influencing product launch strategies.