Gluten Free Beverages Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

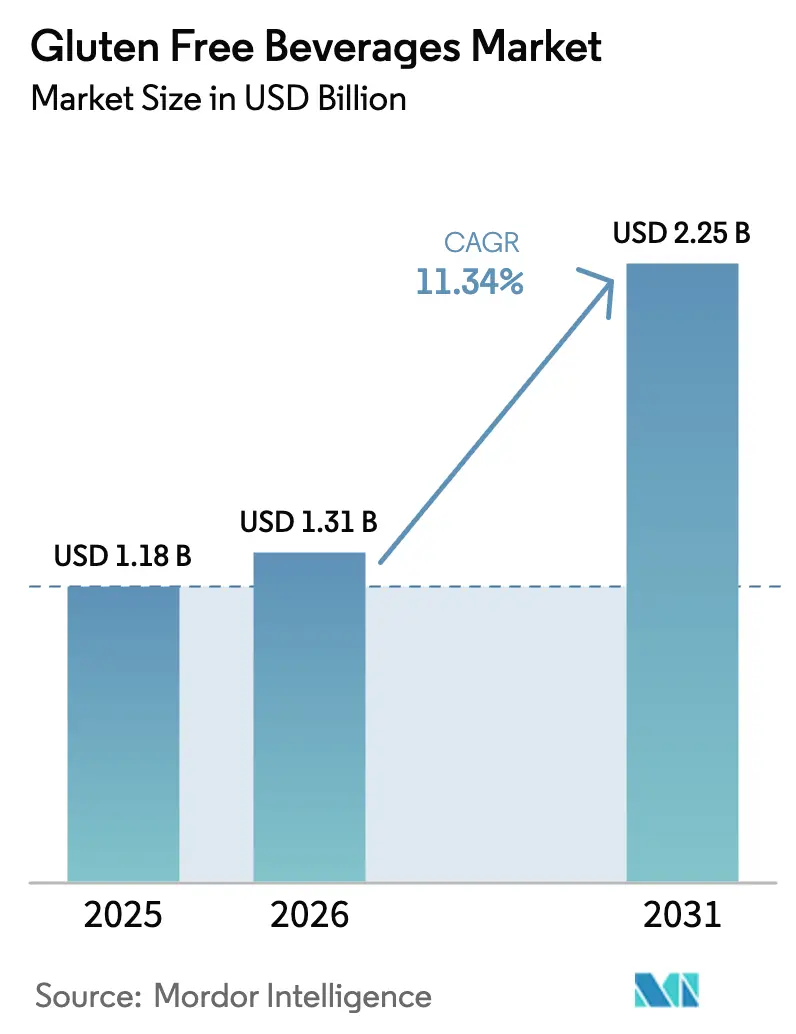

| Market Size (2026) | USD 1.31 Billion |

| Market Size (2031) | USD 2.25 Billion |

| Growth Rate (2026 - 2031) | 11.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

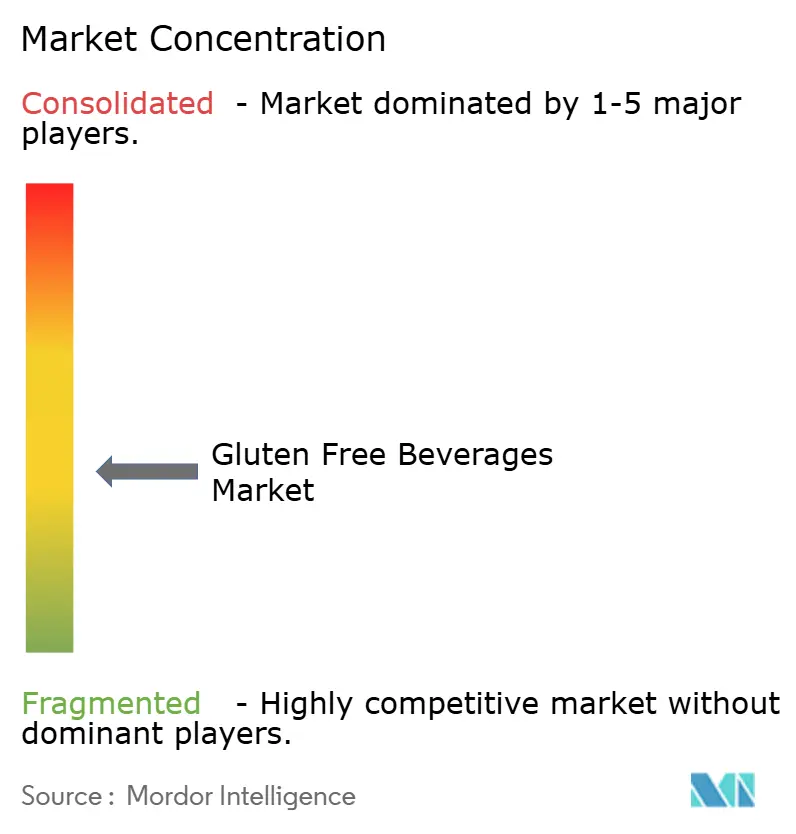

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gluten Free Beverages Market Analysis by Mordor Intelligence

The gluten-free beverages market was valued at USD 1.18 billion in 2025 and estimated to grow from USD 1.31 billion in 2026 to reach USD 2.25 billion by 2031, at a CAGR of 11.34% during the forecast period (2026-2031). As celiac disease and irritable bowel syndrome (IBS) diagnoses rise, clearer labeling in the U.S. and EU, coupled with innovative products that blend allergen-free claims and wellness attributes, drive structural demand. These developments have encouraged manufacturers to focus on creating products that cater to specific dietary needs while promoting overall health. While alcoholic SKUs continue to lead in value, non-alcoholic options are now outpacing them. This shift is largely driven by Gen-Z consumers, who, in their quest for clean-label hydration and functional ingredients, are increasingly abstaining from alcohol. The growing preference for non-alcoholic beverages has prompted companies to expand their portfolios with offerings that emphasize natural ingredients and health benefits. The rise of online retail is breaking down traditional shelf-space barriers. This shift enables micro-breweries and kombucha brands to connect with scattered celiac communities, all while enjoying reduced acquisition costs. By leveraging e-commerce platforms, these smaller players can reach niche markets more effectively, bypassing the limitations of physical retail. In a strategic move to mitigate climate and barley supply risks, major beverage multinationals are turning to drought-resistant sorghum and millet. This not only diversifies their grain contracts but also reduces their carbon footprint, aligning with sustainability goals and ensuring a more resilient supply chain.

Key Report Takeaways

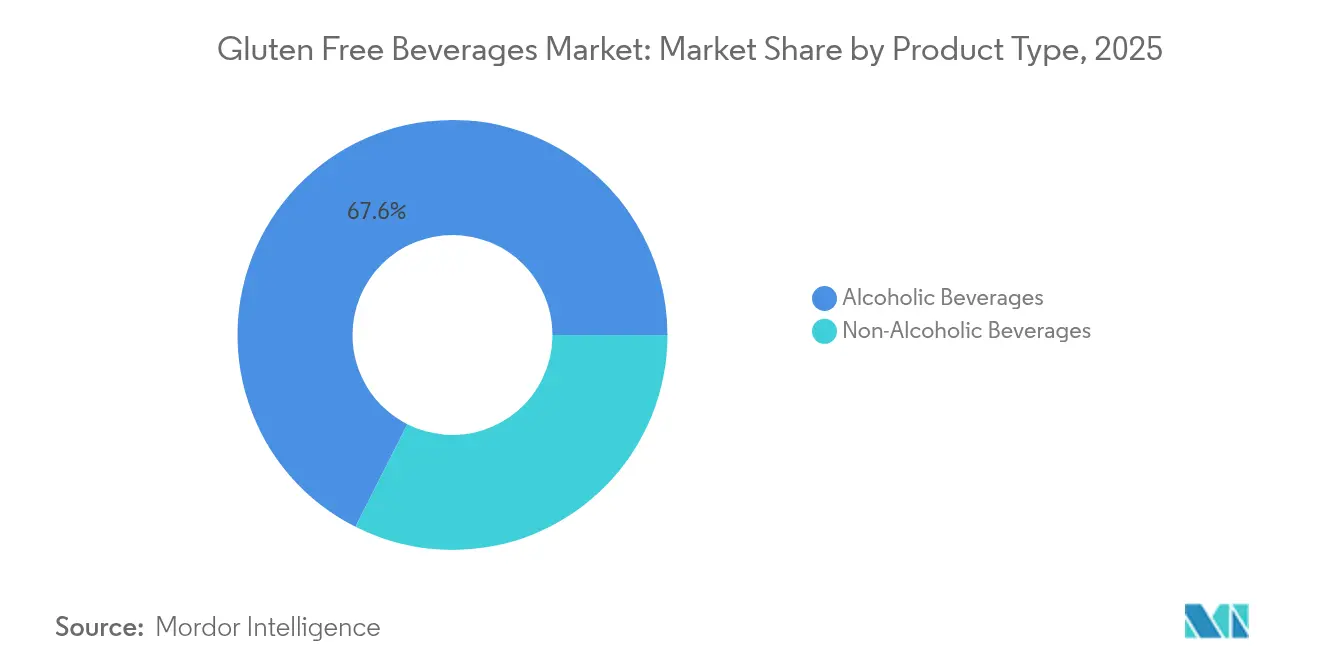

- By product type, alcoholic beverages led with 67.55% of 2025 revenue and non-alcoholic beverages are projected to expand at a 11.78% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets held 41.25% of 2025 sales, whereas online retail is set to grow at an 11.76% CAGR over the forecast period.

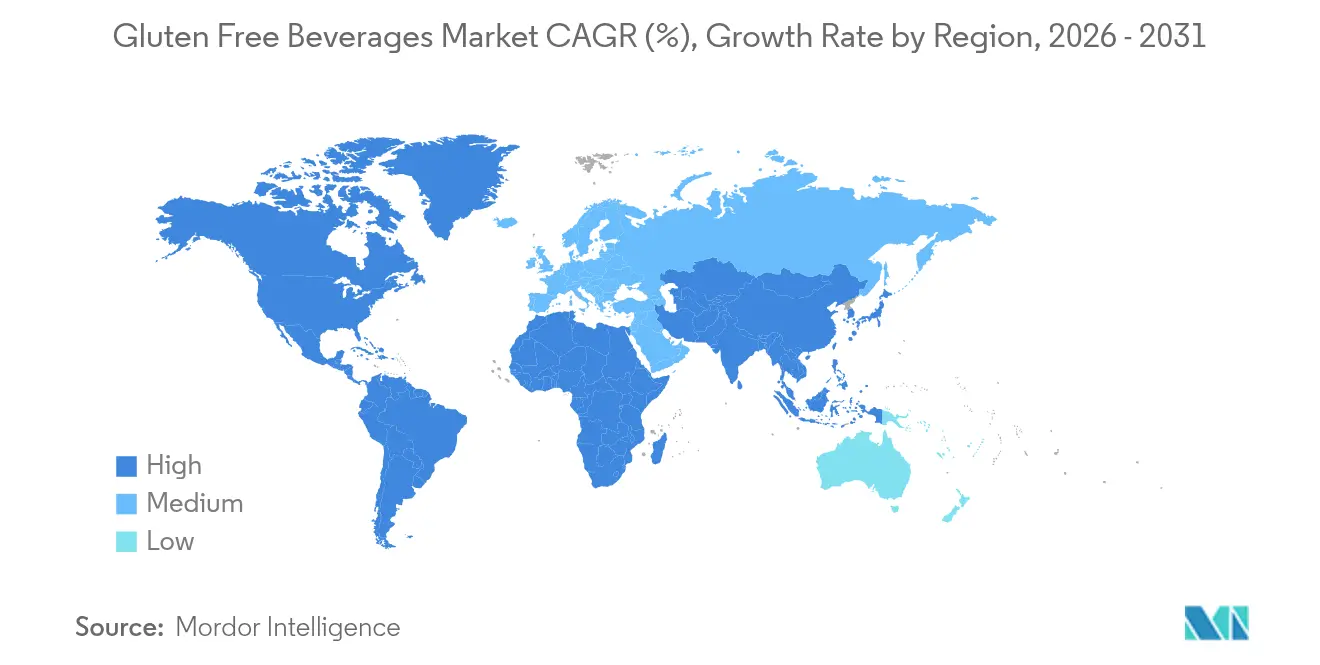

- By geography, North America commanded 37.95% of 2025 global value and Asia-Pacific is poised for the fastest regional expansion at an 11.56% CAGR until 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gluten Free Beverages Market Trends and Insights

Growth in diagnosed celiac and IBS population

In Scandinavia and North America, where tests receive reimbursement, primary care has made serological screening routine, leading to a significant surge in diagnoses. This trend highlights the growing emphasis on early detection and management of gluten-related disorders. From 2020 to 2024, pediatric diagnoses in Europe saw a 4.3% annual uptick, resulting in a new cohort reaching legal drinking age, already accustomed to avoiding gluten due to ingrained dietary habits. In 12 U.S. states, insurance now covers dietitian consultations, formally endorsing gluten-free diets as part of medical guidance, which further integrates gluten-free living into healthcare practices. An FDA update in August 2024 addressed labeling ambiguities for fermented beverages, providing clearer information and reducing consumer confusion[1]Source: Celiac Disease Foundation, " Label Reading & the FDA" , celiac.org. Collectively, these developments have shifted gluten avoidance from a discretionary choice to a medical necessity, driving consistent and recurring demand for gluten-free lagers, spirits, and functional drinks.

Rising demand for better-for-you alcoholic options

Millennials and Gen-Z are shifting their portfolios towards clean-label and lower-calorie alcohol, driven by moderation trends and a growing focus on health-conscious consumption. Brands are securing premium shelf space in U.S. liquor chains by aligning gluten-free positioning with organic and non-GMO badges, which resonate strongly with these demographics. Following a 2024 TTB ruling, spirits distillers are now certifying corn- and potato-based vodkas as gluten-free, broadening the category's reach beyond just beer and appealing to consumers with dietary restrictions or preferences. Data from the Brewer Association indicates that in 2024, gluten-free craft beers surpassed overall craft volumes, highlighting a growing health appeal and signaling a shift in consumer preferences. In response, retailers are clustering these 'better-for-you' SKUs in dedicated aisles, enhancing consumer navigation, simplifying the shopping experience, and boosting trial rates for these products.

Plant-based ingredient innovation

In 2024, sorghum, a drought-resistant crop, grew by 7%, driven by beverage-grade contracts offering farmers price premiums[2]Source: United States Department of Agriculture, "Crop Production" , usda.gov. Breweries are turning to sorghum and millet, drawn by their drought resilience and unique flavor profiles that enhance premium storytelling. Patagonia Provisions and Deschutes unveiled a Kernza-based lager, emphasizing the link between carbon sequestration and product credentials. While enzymatic efficiency on sorghum lags 15% behind barley, in addition to surging barley, surging barley prices post Europe’s 2023 harvest shortfall, underscores the value of crop diversification. With a focus on supply security, ESG alignment, as well as a unique flavor, plant-based grains are bolstered, shielded from commodity shocks.

E-commerce enabling niche gluten-free brands

In 2024, fourteen U.S. states took a significant step by liberalizing direct-to-consumer shipping. This regulatory change empowers craft breweries to bypass traditional distributors, allowing them to directly reach consumers in less populated and underserved regions. This shift not only enhances market access for small-scale producers but also fosters greater consumer choice. In North America, online alcohol sales witnessed an 18% year-on-year surge, driven by evolving consumer preferences and the convenience of e-commerce platforms[3]Source: Distilled Spirits Council of the United States, "Distilled Spirits Council Annual Economic Briefing: Spirits Industry Holds Steady in Market Share Amid Economic Challenges in 2024", distilledspirits.org . Notably, gluten-free SKUs reaped the rewards, enjoying heightened visibility and discoverability due to the long-tail effect of online retail. Subscription boxes emerged as a vital tool for small producers, stabilizing revenue streams, improving cash flow, and reducing working-capital pressures by ensuring predictable income. In a testament to the power of brand communities, Holidaily Brewing successfully crowdfunded USD 1.2 million in 2024 through its proprietary platform. This achievement highlights how engaged communities can provide not only growth capital but also foster deeper brand loyalty. Meanwhile, certified products found an expanded audience, with cross-border sales within the EU and across U.S. state lines enabling producers to extend their reach without incurring hefty retail fees, thereby improving profitability and market penetration.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher production cost and retail price | -1.4% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Shelf-life challenges for preservative-lite SKUs | -0.9% | North America, Europe, humid Asia-Pacific | Medium term (2-4 years) |

| Allergen cross-contact risk in co-packing | -0.7% | Global, shared facilities | Medium term (2-4 years) |

| Regulatory labeling disparities | -0.6% | Global, multi-region exporters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher production cost and retail price

In 2024 spot markets, beverage-grade sorghum commanded a price 35% higher than malting barley, intensifying gross-margin pressures for brewers. This price disparity has made sorghum a costlier alternative, further challenging profitability in the beverage industry. Dedicated sanitation processes, stretching line changeovers by 40%, have led to a contraction in asset turnover, as longer cleaning times reduce production efficiency. Retail premiums ranging from 25% to 45% are dissuading price-sensitive households, a trend particularly pronounced in emerging economies where affordability is a key purchasing factor. An early 2024 drought in West Africa drove sorghum costs up by 18%, further straining brewers already grappling with packaging inflation and rising input costs. Specialty malts, with their minimum order sizes, are tying up working capital and constraining SKU diversity for smaller brands, limiting their ability to compete effectively in a market increasingly dominated by larger players.

Shelf-life challenges for preservative-lite SKUs

Gluten-free beers, lacking sulfites, face quicker oxidation, limiting their shelf life to 90 days, compared to 180 days for traditional lagers. This shorter shelf life poses significant challenges for manufacturers in maintaining product quality and meeting consumer expectations. Meanwhile, non-alcoholic variants, devoid of natural fermentation inhibitors, grapple with even tighter distribution timelines, as the absence of these inhibitors accelerates spoilage. While retailers push for longer shelf lives to optimize inventory turnover, the clean-label trend restricts preservative usage, forcing brands to accept higher spoilage rates and operational inefficiencies. To combat this, some brands invest in nitrogen-flushed cans and UV-blocking glass, which inflate unit costs by up to 12%, adding to price premiums and impacting affordability for consumers. Moreover, cold-chain disruptions impacting 23% of U.S. shipments in 2024 hasten staling, further reducing product quality and tarnishing brand reputation, which can erode consumer trust and loyalty over time.

Segment Analysis

By Type: Enzymatic Tech Reshapes Alcoholic Dominance

In 2025, alcoholic beverages commanded the gluten-free beverages market, clinching 67.55% of total sales. Despite evolving consumer preferences, this segment is poised to uphold its dominant position through 2031. Beer, leveraging enzyme technologies, is at the forefront, allowing barley-based lagers and IPAs to meet regulatory standards, such as FDA thresholds, all while preserving their signature flavors. Spirits experienced a surge in popularity after a June 2024 clarification from the TTB, broadening the scope of certified gluten-free claims to encompass premium vodka and gin. While wine, being inherently gluten-free, bolsters portfolio diversity, it presents fewer differentiation avenues compared to its processed counterparts. This stronghold of alcoholic beverages underscores entrenched consumer habits and production advantages, highlighting that while gluten-free credentials add value, they don't fundamentally alter the category's core appeal.

Non-alcoholic offerings are emerging as the market's fastest-growing segment, projected to expand at a robust 11.78% CAGR. This surge is largely driven by health-conscious millennials and Gen Z, who are increasingly gravitating towards healthier alternatives. Products such as kombucha, cold-brew coffee, and botanical sodas are witnessing heightened demand, prompting U.S. natural grocery chains to allocate more cooler space for these functional beverages. Producers are setting themselves apart by not only emphasizing their gluten-free status but also incorporating added benefits like probiotics and electrolytes. Meanwhile, carbonated soft drinks are reformulating with cane sugar, aligning with trends driven by Europe's sugar tax. Ready-to-drink cocktails and hard seltzers are innovating, introducing millet-derived spirits to craft narratives that resonate with grain diversity, appealing to environmentally and socially conscious (ESG) consumers. Enzymatic advancements are not only slashing costs but also narrowing price disparities, ensuring sustained double-digit growth and posing a challenge to the dominance of alcoholic beverages.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: E-Commerce Disrupts Shelf Allocation

In 2025, supermarkets and hypermarkets dominated the gluten-free beverages market, capturing 41.25% of sales, thanks to their widespread reach and shopper trust. These brick-and-mortar outlets enhance consumer engagement with curated allergen-free end-caps and informative QR codes. While convenience stores cater to impulse buys, their limited shelf space often prioritizes widely distributed national brands. Specialty health stores and brewery taprooms play a pivotal role as trial points, with consumers often transitioning to other channels for repeat purchases, underscoring the value of physical retail touchpoints.

Online retail channels are on a rapid ascent, with projections indicating an 11.76% CAGR. Their growth is attributed to a wider assortment of products and the ability to cater to geographically dispersed celiac populations. Craft breweries, taking advantage of relaxed shipping laws, sidestep traditional distribution routes. This not only boosts their profit margins but also facilitates direct feedback from consumers. Subscription services play a dual role: enhancing customer retention and ensuring a steady revenue stream, both of which are crucial for driving innovation in the gluten-free beverages market. While cross-border e-commerce within the EU broadens varietal choices for consumers, navigating alcohol regulations remains a hurdle. As the market evolves, omnichannel strategies that blend physical and digital experiences will play a pivotal role in shaping market share dynamics.

Geography Analysis

In 2025, North America accounted for 37.95% of global revenues, buoyed by widespread celiac diagnostics, insurer-backed dietitian services, and FDA endorsements of gluten-free beer and spirits. Coastal metros see the deepest penetration, leaving room for growth in rural and Southern states with limited shelf presence. Canadians outspend Americans on gluten-free beverages by 22% per capita, thanks to a higher celiac prevalence and favorable exchange rates making imports more affordable. While Mexico's urban middle class leans towards premium imported gluten-free lagers, entry for smaller brands faces hurdles from three-tier structures and tariffs. A 2024 ruling by the TTB has expanded North America's opportunities, now reaching beyond just malt beverages.

Europe enjoys the benefits of standardized allergen labeling, boosting shopper confidence. Germany, the UK, and France together account for 58% of the region's sales. In Italy, government subsidies for diagnosed patients counterbalance retail premiums, fueling an 11% growth in 2024. Spain and the Netherlands are at the forefront of innovation, introducing teff and millet recipes that align with Mediterranean diets. While demand in Russia remains limited, Moscow's expatriate community ensures a market for high-margin imports. Belgium's abbey-style gluten-free ales fetch premium prices abroad, bolstering the region's esteemed reputation.

Asia-Pacific is on a rapid ascent, projected to grow at an 11.56% CAGR through 2031. Urbanization in tier-2 cities in China and increasing disposable incomes in India are shedding light on previously overlooked gluten intolerance. In Japan, strict labeling regulations limit the market for enzymatically treated beers, but rice-based products are flourishing in Tokyo's specialty outlets. Australia's higher celiac prevalence drives per-capita consumption, surpassing regional averages. South Korea is testing the waters with rice-based soju, targeting health-conscious millennials. Meanwhile, Singapore emerges as a pivotal distribution hub for Southeast Asia, mitigating market-entry risks. Although Latin America and Africa trail in awareness, Brazil and South Africa are poised for growth as diagnostic measures expand and ESG-driven grain sourcing bolsters local supply chains.

Competitive Landscape

The gluten-free beverages market remains fragmented, limiting any single firm's pricing power. While multinationals like Anheuser-Busch InBev, Heineken, Carlsberg, and Diageo leverage their distribution strength to introduce certified portfolios, regional craft brands such as Omission, Glutenberg, and Ghostfish cultivate loyalty through compelling provenance narratives, emphasizing local sourcing and unique brewing techniques.

Enzymatic technology stands as the focal point of competition; IFF’s Diazyme NOLO enables barley-based recipes, allowing brewers to cater to gluten-free consumers without abandoning traditional ingredients. Meanwhile, advocates of naturally gluten-free grains emphasize the authenticity and nutritional benefits of ancient grains like millet, sorghum, and quinoa. A notable 34% surge in patent filings in 2024 underscores the strategic importance of intellectual property, as companies seek to protect innovations and gain a competitive edge. Direct-to-consumer e-commerce platforms empower microbreweries to expand without relinquishing equity to venture capitalists. Holidaily Brewing’s successful USD 1.2 million community-driven fundraising exemplifies how grassroots support can alleviate traditional bank financing challenges, enabling smaller players to scale operations and enhance production capabilities.

By committing to ESG-centric sourcing, multinationals not only secure alternative grains but also mitigate climate risks, seamlessly integrating sustainability with dietary considerations. These commitments often involve partnerships with local farmers and investments in sustainable agricultural practices. The adoption of technology reveals a divide: while large brewers are retrofitting with enzymes to adapt existing facilities, micro-breweries are channeling investments into dedicated gluten-free facilities to ensure zero cross-contact, thereby maintaining the trust of their niche consumer base. As non-alcoholic functional formats draw interest from sectors like kombucha, sports drinks, and botanical sodas, the competitive landscape is set to intensify, with new entrants leveraging innovation and branding to capture market share.

Gluten Free Beverages Industry Leaders

-

The Coca-Cola Company

-

Anheuser-Busch InBev

-

PepsiCo Inc.

-

Danone S.A.

-

Heineken NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Plenish debuted the UK's inaugural zero-sugar oat drink, free from oils and additives, further broadening its plant-based offerings. Plenish Zero Sugar Oat M*lk, crafted from a quartet of natural ingredients water, gluten-free organic oats, plant-based calcium, and salt delivers a creamy, flavorful experience without converting oats into natural sugars. Exclusively available at Waitrose and online, this groundbreaking product caters to the rising consumer appetite for reduced sugar and clean-label offerings, all while ensuring transparency and taste in the dairy alternative realm.

- September 2025: Central Standard Craft Distillery introduced Delta Dawn, a fresh line of non-alcoholic beverages infused with THC. Flavors include Door County Cherry Lemonade and Fruit Punch. Each 12 oz can, boasting 10mg of THC, is both alcohol-free and gluten-free. Delta Dawn presents a crafted alternative to traditional spirits, delivering refreshing tastes reminiscent of tart local cherries and nostalgic fruit punch.

- August 2025: DioniLife, a pioneering non-alcoholic spirits company, unveiled two innovative products: La Borosa, an agave-based spirit reminiscent of Mexican tequila, and Pavari 17, a bittersweet aperitivo hailing from the Mediterranean. La Borosa captures the essence of authentic tequila, boasting flavors without the alcohol or sugar. Crafted from hand-harvested Blue Agave and aged in oak, it promises a genuine taste experience.

- January 2025: Kiitos Brewing etched its name in history by debuting the nation's first-ever 100% Fonio beer. This distinctive brew, crafted solely from fonio grain, taps into the legacy of an ancient West African cereal celebrated for its resilience to drought and minimal water requirements. The beer, with its near-translucent hue, tantalizes the palate with tropical undertones, prominently featuring lychee and white grape notes.

Global Gluten Free Beverages Market Report Scope

Gluten-free beverages are beverages that are claimed and made using gluten-free ingredients. The global gluten-free beverage market has been segmented by types (which includes alcoholic and non-alcoholic drinks), by distribution channel (which includes convenience stores, supermarket/hypermarket, specialty stores, online retailers, and others), and by geography (which includes North America, Europe, Asia-Pacific, South America and the Middle East and Africa).

| Alcoholic Beverages | Wine |

| Spirits | |

| Beer | |

| Others | |

| Non-Alcoholic Beverages |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Alcoholic Beverages | Wine |

| Spirits | ||

| Beer | ||

| Others | ||

| Non-Alcoholic Beverages | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Gluten Free Beverages Market size?

The gluten-free beverages market size is USD 1.31 billion in 2026.

How fast will demand grow over the next five years?

Global value is forecast to compound at an 11.34% CAGR between 2026 and 2031.

Which region buys the most gluten-free drinks today?

North America leads with 37.95% of global revenue, aided by mature labeling rules and high diagnosis rates.

Which product category expands the quickest?

Non-alcoholic gluten-free drinks are projected to grow at a 11.78% CAGR, outpacing alcoholic lines.

Why is online retail pivotal for gluten-free beverages?

E-commerce removes shelf-space limits, lets craft brands ship direct in 14 U.S. states, and drives an 11.76% CAGR for online sales.