Market Overview

| Study Period | 2017 - 2030 |

|---|---|

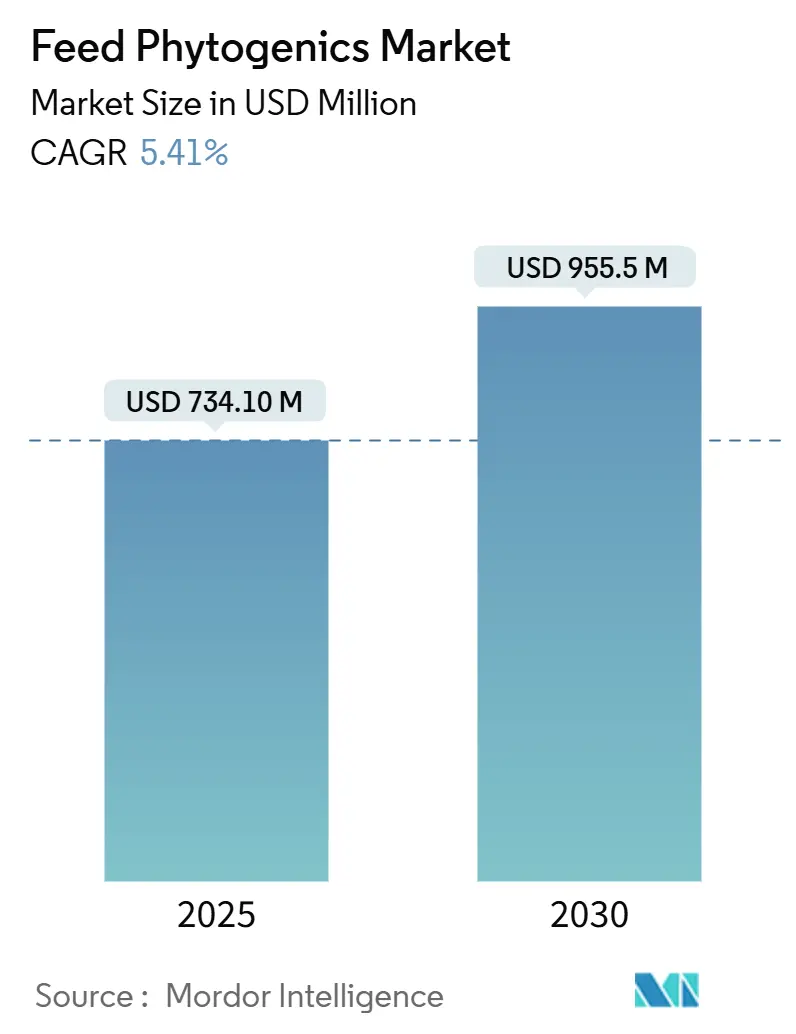

| Market Size (2025) | USD 734.10 Million |

| Market Size (2030) | USD 955.5 Million |

| Growth Rate (2025 - 2030) | 5.41% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Feed Phytogenics Market Analysis by Mordor Intelligence

The global feed phytogenics market size stands at USD 734.1 million in 2025 and is projected to reach USD 955.5 million by 2030, translating to a 5.41% CAGR across the forecast period. This outlook reflects rapid regulatory moves away from antibiotic growth promoters, robust livestock protein demand, and continuous innovation in botanical extraction and delivery technologies. Essential oils account for more than half of revenue because they deliver proven gut‐health and antimicrobial benefits while aligning with tightening residue standards. Poultry producers, especially in the Asia‐Pacific rapidly adopt phytogenic inclusion strategies because even fractional gains in feed conversion ratios drive profitability. Meanwhile, North American integrators capitalize on premium pricing for meat and dairy raised without routine antibiotics, positioning the feed phytogenics market for sustained value creation. Competitive intensity remains moderate where the top five companies control the majority of sales, yet hundreds of regional specialists bring niche formulations to market, especially for aquaculture, where tailored blends support water stability and disease management.

Key Report Takeaways

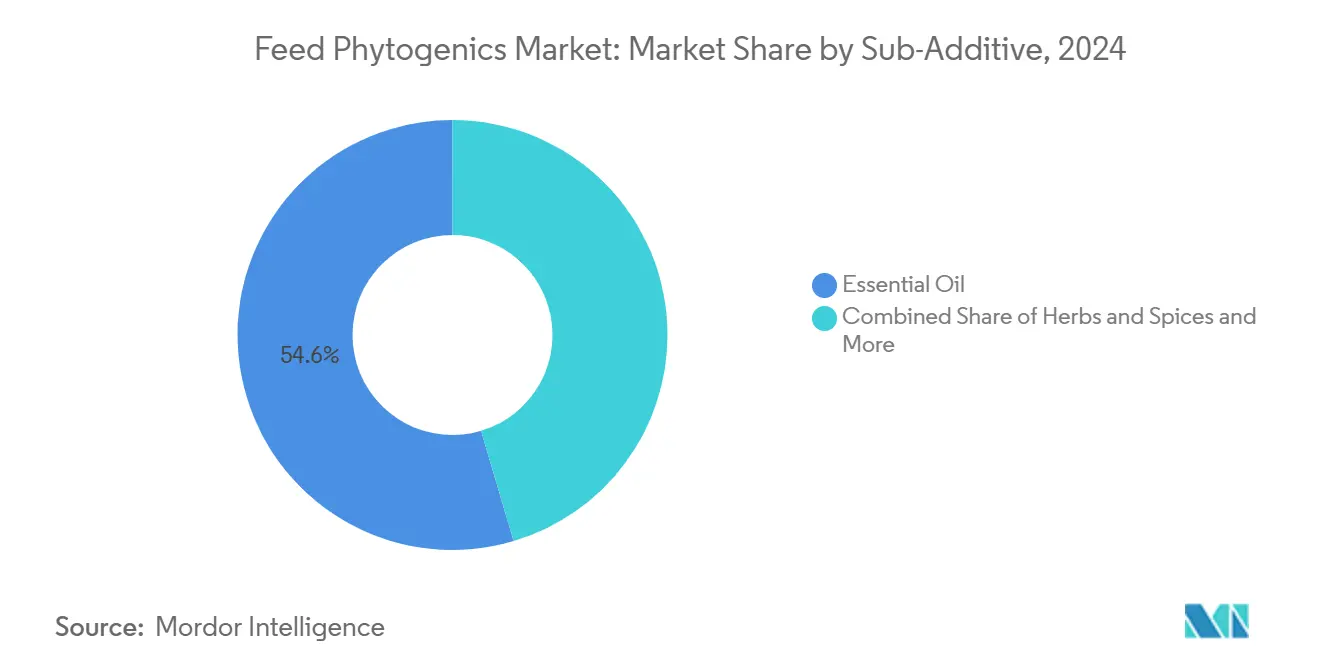

- By sub‐additive, essential oils captured 54.6% of feed phytogenics market share in 2024, whereas herbs and spices are projected to be the fastest growing at a 4.20% CAGR from 2025 to 2030.

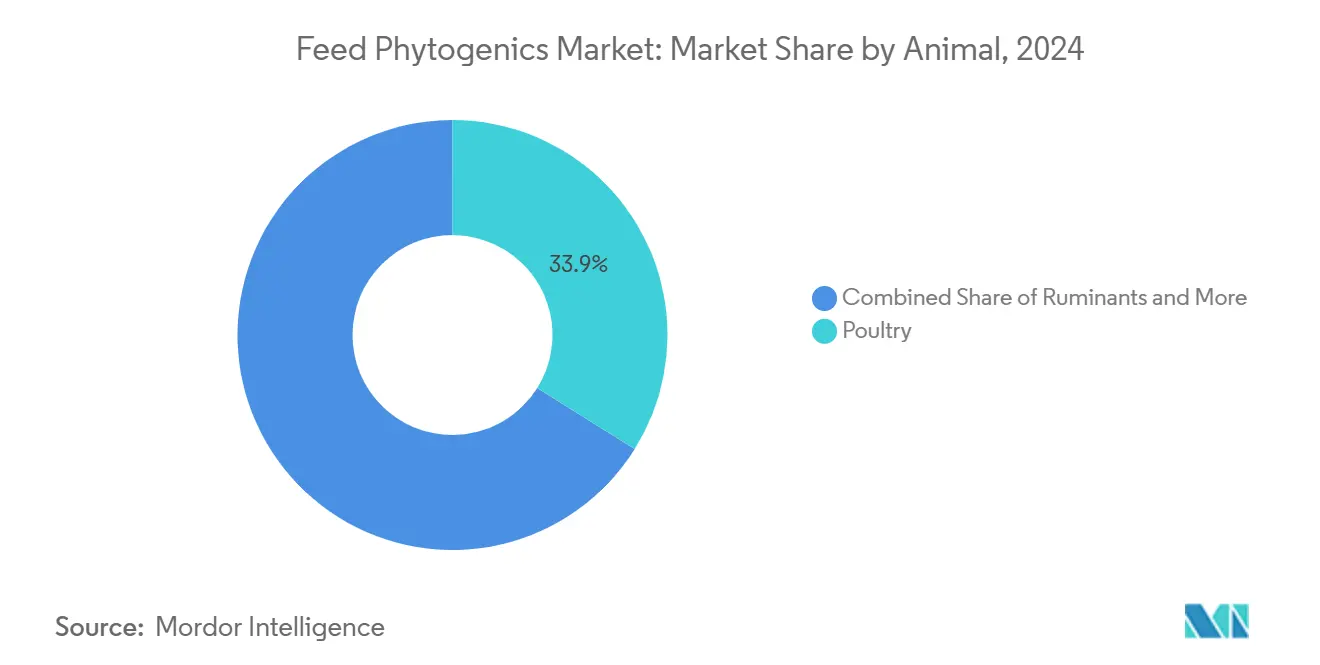

- By animal, poultry applications captured 33.9% of feed phytogenics market share in 2024, and are advancing at a 4.40% CAGR from 2025 to 2030.

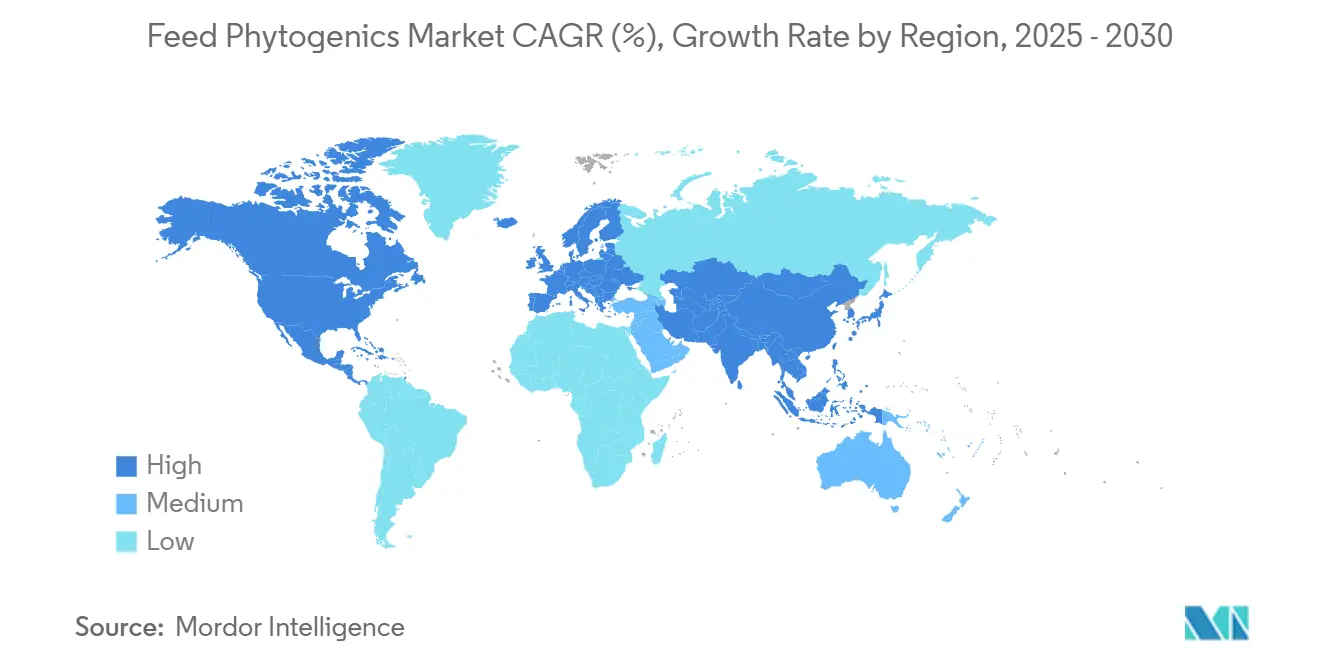

- By region, Asia-Pacific accounted for 22.8% of feed phytogenics market size in 2024, while North America is forecast to expand at a 4.05% CAGR through 2030.

Global Feed Phytogenics Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory bans on antibiotic growth promoters | +1.8% | Global, strongest in Europe and North America | Medium term (2–4 years) |

| Escalating global meat and dairy demand | +1.2% | Asia‐Pacific core, spill-over to Middle East and South America | Long term (≥ 4 years) |

| Heightened focus on animal welfare and gut-health management | +0.9% | North America and Europe, expanding to Asia‐Pacific | Medium term (2–4 years) |

| Precision micro-dosing technologies enabling phytogenic inclusion | +0.6% | Global, led by United States, and Germany | Short term (≤ 2 years) |

| Carbon-credit programs rewarding methane-curbing feed additives | +0.4% | Europe and California, pilot programs in Australia | Long term (≥ 4 years) |

| South-Asian botanical supply chains lowering essential-oil costs | +0.5% | Global sourcing, strongest in cost-sensitive markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Regulatory Bans on Antibiotic Growth Promoters

Sweeping prohibitions on antibiotic growth promoters have redefined feed formulation strategies in every major livestock hub. The European Union’s early restrictions set the legislative template now emulated worldwide, while the United States reinforced momentum through the Veterinary Feed Directive. China’s 2020 colistin ban unlocked the world’s largest poultry market for phytogenic solutions. In 2024, the FDA created the Animal Food Ingredient Center to streamline botanical approvals, accelerating commercialization cycles and catalyzing research investments. Formulators increasingly rely on essential‐oil blends rich in thymol, carvacrol, and eugenol to replicate or surpass antibiotic performance without residue or resistance concerns.

Escalating Global Meat and Dairy Demand

Global meat consumption is forecast to rise 14% by 2030, and aquaculture output is projected to climb 18% in the same window. This shift is concentrated in Asia‐Pacific economies where higher incomes expand per-capita animal protein intake. As grain prices stay volatile, producers search for additives that squeeze more weight gain from every kilogram of feed. Trials show oregano oil can improve broiler feed conversion ratios by 3–5% while curbing mortality. Similar gains in shrimp and tilapia intensify demand for water-stable botanical carriers.

Heightened Focus on Animal Welfare and Gut-Health Management

Consumer-driven animal welfare standards increasingly mandate natural health management approaches, creating market premiums for livestock raised without routine antibiotic use. Major food retailers including Walmart and McDonald's established antibiotic-free sourcing requirements, compelling producers to adopt alternative health management strategies. Phytogenics address multiple welfare concerns simultaneously by supporting digestive health, reducing stress responses, and improving overall animal comfort through natural bioactive compounds. Essential oil blends containing thymol and carvacrol demonstrate measurable reductions in intestinal inflammation markers while maintaining production performance Journal of Animal Science. European welfare certification programs increasingly recognize phytogenic feed additives as preferred alternatives to synthetic growth promoters, creating market differentiation opportunities for premium animal protein product. [1]Source: Journal of Applied Animal Science, “Effects of Oregano Oil on Broiler Performance and Feed Conversion,” AppliedAnimalScience.org

Precision Micro-Dosing Technologies Enabling Phytogenic Inclusion

Advanced encapsulation and micro-dosing technologies resolve historical challenges with phytogenic feed additive stability and bioavailability. Heat-stable encapsulation methods protect volatile compounds during pelleting processes, ensuring active ingredient delivery to target animals. Spray-drying and lipid encapsulation techniques developed by companies like Kemin Industries maintain essential oil potency through standard feed manufacturing processes. Precision dosing systems enable accurate inclusion rates as low as 50-100 grams per metric ton of feed, making phytogenics cost-competitive with synthetic alternatives. Nanotechnology applications in feed additive delivery systems show promise for targeted release in specific digestive tract segments, potentially improving efficacy while reducing inclusion rates.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost variability of plant extracts vs. synthetics | -0.8% | Global, most acute in price-sensitive markets | Short term (≤ 2 years) |

| Fragmented global standards for efficacy and labeling | -0.6% | Global, regulatory harmonization challenges | Medium term (2-4 years) |

| Climate-driven volatility in herb and spice raw material supply | -0.4% | Global sourcing regions, weather-dependent areas | Long term (≥ 4 years) |

| Limited global encapsulation capacity for heat-stable PFAs | -0.3% | Manufacturing hubs in United States, Europe, and Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost Variability of Plant Extracts vs. Synthetics

Plant extract pricing exhibits significantly higher volatility compared to synthetic alternatives, creating budget uncertainty for large-scale feed manufacturers. Essential oil prices fluctuate 20-40% annually based on harvest conditions, geopolitical factors, and currency exchange rates affecting key producing regions. Oregano oil prices ranged from USD 18-28 per kilogram in 2024, while synthetic alternatives maintained stable pricing around USD 12-15 per kilogram. This price differential becomes particularly pronounced during adverse weather events or supply chain disruptions affecting botanical source regions. Feed manufacturers require predictable input costs for annual contract negotiations with livestock producers, making synthetic alternatives more attractive despite regulatory pressures favoring natural products.

Fragmented Global Standards for Efficacy and Labeling

Inconsistent regulatory frameworks across major markets create compliance complexity for multinational feed additive suppliers. The European Food Safety Authority maintains the most stringent approval requirements for phytogenic feed additives, requiring extensive efficacy and safety documentation that can cost USD 2-5 million per product registration. In contrast, many developing markets lack specific regulatory frameworks for botanical feed ingredients, creating quality assurance challenges and market uncertainty. The absence of harmonized international standards for phytogenic feed additive potency, purity, and labeling requirements forces companies to maintain multiple product formulations and documentation systems for different regional markets, increasing operational complexity and costs.

Segment Analysis

By Sub-Additive: Essential Oils Lead Market Penetration

Essential oils dominate the sub-additive segmentation with 54.6% market share in 2024, reflecting their established efficacy profiles and regulatory acceptance across major markets. Herbs and spices represent the fastest-growing segment at 4.20% CAGR through 2030, driven by cost advantages and expanding research validating their bioactive properties. Oregano oil leads essential oil applications with proven antimicrobial efficacy, while thyme and rosemary oils gain traction in European markets following EFSA approvals in 2024. Oleoresins capture specialized applications requiring concentrated bioactive compounds, particularly in aquaculture feeds where water stability becomes critical.

The sub-additive landscape reflects evolving formulation strategies as manufacturers blend multiple botanical sources to achieve synergistic effects. Carvacrol and thymol combinations demonstrate enhanced antimicrobial activity compared to individual compounds, driving demand for standardized essential oil blends. Other phytogenics, including saponins and tannins, serve niche applications in ruminant nutrition where methane reduction capabilities align with environmental sustainability goals. Precision extraction technologies enable consistent potency across botanical raw materials, addressing historical quality variability concerns that limited commercial adoption.[2]Source: European Food Safety Authority, “Scientific Opinion on the Safety and Efficacy of Oregano Oil as Feed Additive,” EFSA.europa.eu

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Animal: Poultry Applications Drive Commercial Adoption

Poultry represents the largest animal segment with 33.9% market share in 2024, benefiting from intensive production systems where marginal performance improvements generate significant economic returns. The segment also demonstrates the fastest growth at 4.40% CAGR through 2030, reflecting continued expansion in developing markets and increasing adoption of antibiotic-free production systems. Broiler applications dominate within poultry, where feed conversion efficiency gains of 2-4% justify phytogenic inclusion costs. Layer operations increasingly adopt phytogenics for egg quality enhancement and hen welfare improvements, particularly in cage-free production systems.

Aquaculture emerges as a high-growth opportunity despite its smaller current market share, driven by expanding global fish and shrimp production and unique challenges with antibiotic resistance in aquatic environments. Ruminant applications focus on methane reduction capabilities of tannin-rich plant extracts, aligning with carbon footprint reduction initiatives across dairy and beef operations. Swine operations adopt phytogenics primarily for gut health management during weaning transitions, where digestive stress creates opportunities for natural health support solutions. Other animals, including companion animals and specialty livestock, represent emerging applications as pet food manufacturers seek natural ingredient positioning.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Asia-Pacific maintains its position as the largest regional market with 22.8% share in 2024, while North America is projected to be the fastest growing at 4.05% CAGR for 2025-2030. driven by massive livestock production volumes and regulatory transitions away from antibiotic growth promoters. China's implementation of antibiotic restrictions in 2020 opened significant opportunities for phytogenic alternatives, while India's expanding poultry sector creates demand for cost-effective natural solutions. The region benefits from proximity to botanical raw material sources, particularly essential oil production in India and Southeast Asia, reducing supply chain costs and improving ingredient availability. Japan and South Korea lead in premium applications where food safety concerns drive adoption of natural feed additives despite higher costs.

North America is reflecting stringent regulatory restrictions and consumer-driven demand for antibiotic-free animal proteins. The FDA's Veterinary Feed Directive and state-level restrictions in California create regulatory momentum favoring natural alternatives. Major food retailers' antibiotic-free sourcing requirements compel producers to adopt phytogenic solutions, creating market premiums that justify higher ingredient costs. Canada's organic livestock sector drives demand for certified natural feed additives, while Mexico's export-oriented poultry industry adopts phytogenics to meet international buyer specifications.

Europe maintains steady market development despite mature regulatory frameworks, with growth concentrated in organic and welfare-certified production systems. The European Food Safety Authority's rigorous approval processes create high barriers to entry but establish global standards for product efficacy and safety documentation. Germany and Netherlands lead in research and development activities, with companies like Phytobiotics and Orffa International developing innovative formulations and delivery systems. The region's leadership in animal welfare standards influences global market development, with European certification programs increasingly recognizing phytogenic feed additives as preferred alternatives to synthetic growth promoters. Regulatory frameworks established by EFSA continue to shape international product development and approval processes, creating competitive advantages for companies that navigate these complex requirements successfully.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The feed phytogenics market is consolidated, with the top five vendors accounting for roughly 59.4% of global sales, leaving ample room for regional specialists. DSM-Firmenich AG leads following its 2023 merger, channeling resources toward high-growth phytogenic and precision nutrition platforms. Cargill, Incorporated, integrated with Delacon’s botanical expertise into its worldwide distribution network, holding its position among the top 5.

Competitive positioning hinges on intellectual property around extraction and delivery technologies. Patent filings for heat-stable essential oil encapsulation rose sharply in 2024, with DSM-Firmenich AG and Kemin Industries, Inc registering multiple applications. Major players are focusing on developing novel phytogenics products through extensive research and development initiatives, particularly targeting alternatives to antibiotics in animal feed. Firms also partner with universities to substantiate efficacy claims under rigorous trial conditions, knowing successful EFSA or FDA approvals confer global credibility.[3]Source: United States Patent and Trademark Office, “Patent Applications for Heat-Stable Essential Oil Formulations,” USPTO.gov

Regional upstarts pursue niche angles such as aquaculture-specific blends or lignin-based carrier systems that appeal to sustainability-minded buyers. Supply security is becoming an emerging battlefield as alliances with Indian and Vietnamese oil distillers help partners lock in volume at competitive prices. These partnerships buffer cost spikes and ensure consistent potency across seasons.

Feed Phytogenics Industry Leaders

Adisseo

IFF(Danisco Animal Nutrition)

Land O'Lakes

DSM-Firmenich AG

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: HealthTech Bioactives partnered with Abolis Biotechnologies to co-develop precision fermentation routes for high-value phytogenic actives, aiming to shield customers from raw botanical price swings while matching natural compound profiles.

- February 2025: DSM-Firmenich AG divested its Twilmij feed premix unit to concentrate capital on advanced phytogenic and precision nutrition segments, aligning portfolio focus with regulatory demand for antibiotic alternatives.

- January 2025: The FDA rolled out its Animal Food Ingredient Center online portal, reducing botanical additive review times from 18–24 months to near 12 months, thereby lowering market entry barriers for innovators.

Global Feed Phytogenics Market Report Scope

Sub Additive

| Essential Oil |

| Herbs & Spices |

| Other Phytogenics |

Animal

| Aquaculture | By Sub Animal | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | By Sub Animal | Broiler |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | By Sub Animal | Beef Cattle |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals |

Geography

| Africa | By Country | Egypt |

| Kenya | ||

| South Africa | ||

| Rest of Africa | ||

| Asia-Pacific | By Country | Australia |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Philippines | ||

| South Korea | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Europe | By Country | France |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| Turkey | ||

| United Kingdom | ||

| Rest of Europe | ||

| Middle East | By Country | Iran |

| Saudi Arabia | ||

| Rest of Middle East | ||

| North America | By Country | Canada |

| Mexico | ||

| United States | ||

| Rest of North America | ||

| South America | By Country | Argentina |

| Brazil | ||

| Chile | ||

| Rest of South America |

| Sub Additive | Essential Oil | ||

| Herbs & Spices | |||

| Other Phytogenics | |||

| Animal | Aquaculture | By Sub Animal | Fish |

| Shrimp | |||

| Other Aquaculture Species | |||

| Poultry | By Sub Animal | Broiler | |

| Layer | |||

| Other Poultry Birds | |||

| Ruminants | By Sub Animal | Beef Cattle | |

| Dairy Cattle | |||

| Other Ruminants | |||

| Swine | |||

| Other Animals | |||

| Geography | Africa | By Country | Egypt |

| Kenya | |||

| South Africa | |||

| Rest of Africa | |||

| Asia-Pacific | By Country | Australia | |

| China | |||

| India | |||

| Indonesia | |||

| Japan | |||

| Philippines | |||

| South Korea | |||

| Thailand | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| Europe | By Country | France | |

| Germany | |||

| Italy | |||

| Netherlands | |||

| Russia | |||

| Spain | |||

| Turkey | |||

| United Kingdom | |||

| Rest of Europe | |||

| Middle East | By Country | Iran | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| North America | By Country | Canada | |

| Mexico | |||

| United States | |||

| Rest of North America | |||

| South America | By Country | Argentina | |

| Brazil | |||

| Chile | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Market Definition

- FUNCTIONS - For the study, feed additives are considered to be commercially manufactured products that are used to enhance characteristics such as weight gain, feed conversion ratio, and feed intake when fed in appropriate proportions.

- RESELLERS - Companies engaged in reselling feed additives without value addition have been excluded from the market scope, to avoid double counting.

- END CONSUMERS - Compound feed manufacturers are considered to be end-consumers in the market studied. The scope excludes farmers buying feed additives to be used directly as supplements or premixes.

- INTERNAL COMPANY CONSUMPTION - Companies engaged in the production of compound feed as well as the manufacturing of feed additives are part of the study. However, while estimating the market sizes, the internal consumption of feed additives by such companies has been excluded.

| Keyword | Definition |

|---|---|

| Feed additives | Feed additives are products used in animal nutrition for purposes of improving the quality of feed and the quality of food from animal origin, or to improve the animals’ performance and health. |

| Probiotics | Probiotics are microorganisms introduced into the body for their beneficial qualities. (It maintains or restores beneficial bacteria to the gut). |

| Antibiotics | Antibiotic is a drug that is specifically used to inhibit the growth of bacteria. |

| Prebiotics | A non-digestible food ingredient that promotes the growth of beneficial microorganisms in the intestines. |

| Antioxidants | Antioxidants are compounds that inhibit oxidation, a chemical reaction that produces free radicals. |

| Phytogenics | Phytogenics are a group of natural and non-antibiotic growth promoters derived from herbs, spices, essential oils, and oleoresins. |

| Vitamins | Vitamins are organic compounds, which are required for normal growth and maintenance of the body. |

| Metabolism | A chemical process that occurs within a living organism in order to maintain life. |

| Amino acids | Amino acids are the building blocks of proteins and play an important role in metabolic pathways. |

| Enzymes | Enzyme is a substance that acts as a catalyst to bring about a specific biochemical reaction. |

| Anti-microbial resistance | The ability of a microorganism to resist the effects of an antimicrobial agent. |

| Anti-microbial | Destroying or inhibiting the growth of microorganisms. |

| Osmotic balance | It is a process of maintaining salt and water balance across membranes within the body's fluids. |

| Bacteriocin | Bacteriocins are the toxins produced by bacteria to inhibit the growth of similar or closely related bacterial strains. |

| Biohydrogenation | It is a process that occurs in the rumen of an animal in which bacteria convert unsaturated fatty acids (USFA) to saturated fatty acids (SFA). |

| Oxidative rancidity | It is a reaction of fatty acids with oxygen, which generally causes unpleasant odors in animals. To prevent these, antioxidants were added. |

| Mycotoxicosis | Any condition or disease caused by fungal toxins, mainly due to contamination of animal feed with mycotoxins. |

| Mycotoxins | Mycotoxins are toxin compounds that are naturally produced by certain types of molds (fungi). |

| Feed Probiotics | Microbial feed supplements positively affect gastrointestinal microbial balance. |

| Probiotic yeast | Feed yeast (single-cell fungi) and other fungi used as probiotics. |

| Feed enzymes | They are used to supplement digestive enzymes in an animal’s stomach to break down food. Enzymes also ensure that meat and egg production is improved. |

| Mycotoxin detoxifiers | They are used to prevent fungal growth and to stop any harmful mold from being absorbed in the gut and blood. |

| Feed antibiotics | They are used both for the prevention and treatment of diseases but also for rapid growth and development. |

| Feed antioxidants | They are used to protect the deterioration of other feed nutrients in the feed such as fats, vitamins, pigments, and flavoring agents, thus providing nutrient security to the animals. |

| Feed phytogenics | Phytogenics are natural substances, added to livestock feed to promote growth, aid in digestion, and act as anti-microbial agents. |

| Feed vitamins | They are used to maintain the normal physiological function and normal growth and development of animals. |

| Feed flavors and sweetners | These flavors and sweeteners help to mask tastes and odors during changes in additives or medications and make them ideal for animal diets undergoing transition. |

| Feed acidifiers | Animal feed acidifiers are organic acids incorporated into the feed for nutritional or preservative purposes. Acidifiers enhance congestion and microbiological balance in the alimentary and digestive tracts of livestock. |

| Feed minerals | Feed minerals play an important role in the regular dietary requirements of animal feed. |

| Feed binders | Feed binders are the binding agents used in the manufacture of safe animal feed products. It enhances the taste of food and prolongs the storage period of the feed. |

| Key Terms | Abbreviation |

| LSDV | Lumpy Skin Disease Virus |

| ASF | African Swine Fever |

| GPA | Growth Promoter Antibiotics |

| NSP | Non-Starch Polysaccharides |

| PUFA | Polyunsaturated Fatty Acid |

| Afs | Aflatoxins |

| AGP | Antibiotic Growth Promoters |

| FAO | The Food And Agriculture Organization of the United Nations |

| USDA | The United States Department of Agriculture |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF