Feed Phosphate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

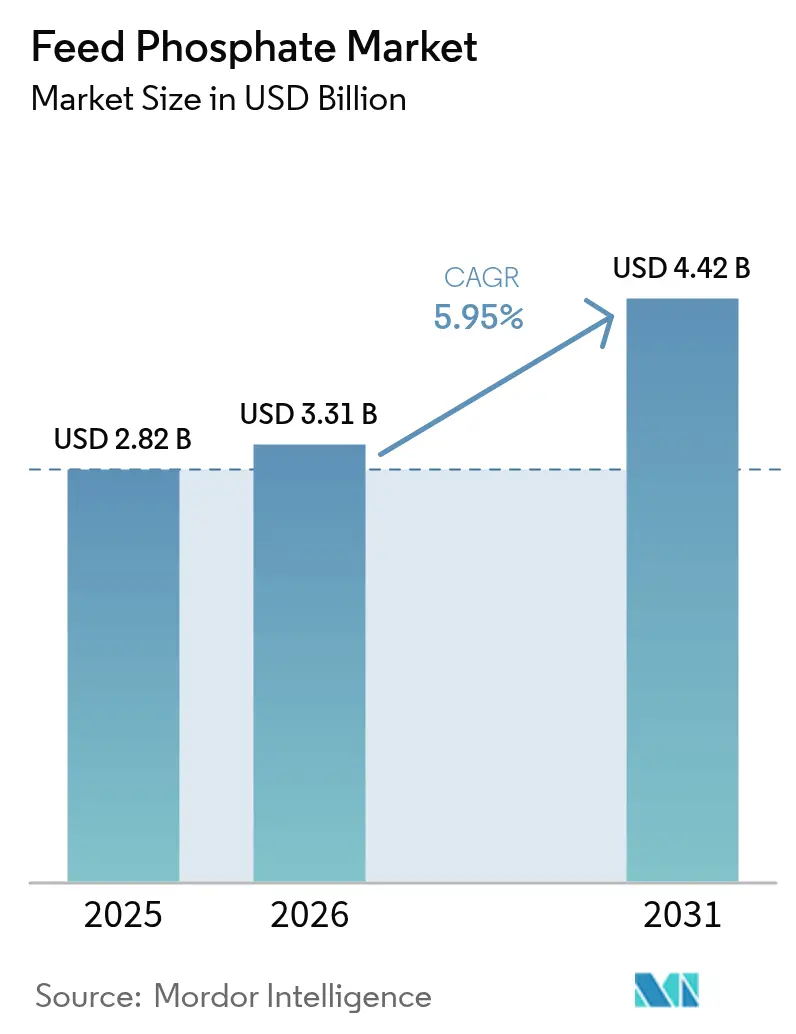

| Market Size (2026) | USD 3.31 Billion |

| Market Size (2031) | USD 4.42 Billion |

| Growth Rate (2026 - 2031) | 5.95% CAGR |

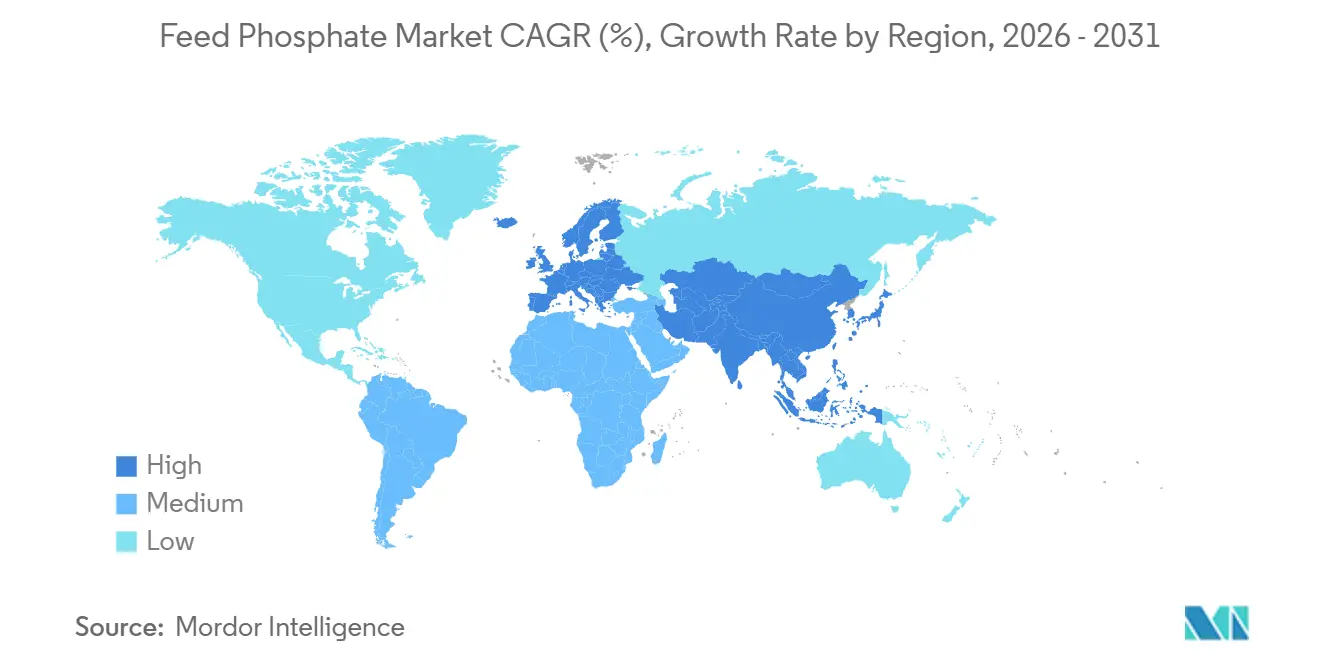

| Fastest Growing Market | Europe |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Feed Phosphate Market Analysis by Mordor Intelligence

The feed phosphate market size is projected to expand from USD 2.82 billion in 2025 and USD 3.31 billion in 2026 to USD 4.42 billion by 2031, registering a 5.95% CAGR between 2026 and 2031. The upward trajectory reflects surging demand for animal protein in emerging economies, consolidation of livestock production into large-scale units, and policy moves that favor recycled phosphorus inputs over mined rock. Producers are responding by shifting toward high-bioavailability monocalcium grades, investing in lower-carbon defluorination lines, and co-locating insect-protein capacity that supplies organically bound phosphorus. Artificial-intelligence dosing platforms and near-infrared sensors are trimming over-supplementation, a trend that tempers tonnage growth yet lifts product quality and price realization. Meanwhile, circular-phosphorus mandates in Europe and North America are catalyzing investment in struvite and manure-ash recovery, adding a new supply stream that changes competitive dynamics.

Key Report Takeaways

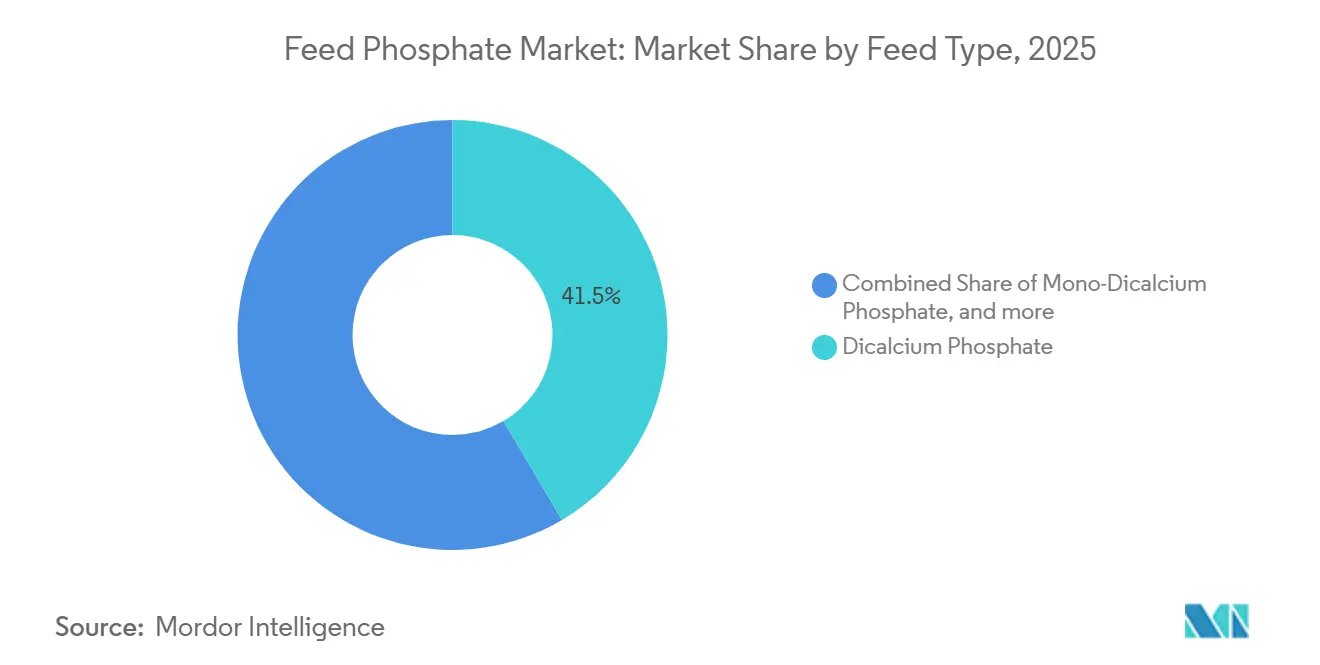

- By feed type, dicalcium phosphate led with 41.5% revenue share in 2025, mono-dicalcium phosphate is forecast to expand at a 6.1% CAGR through 2031.

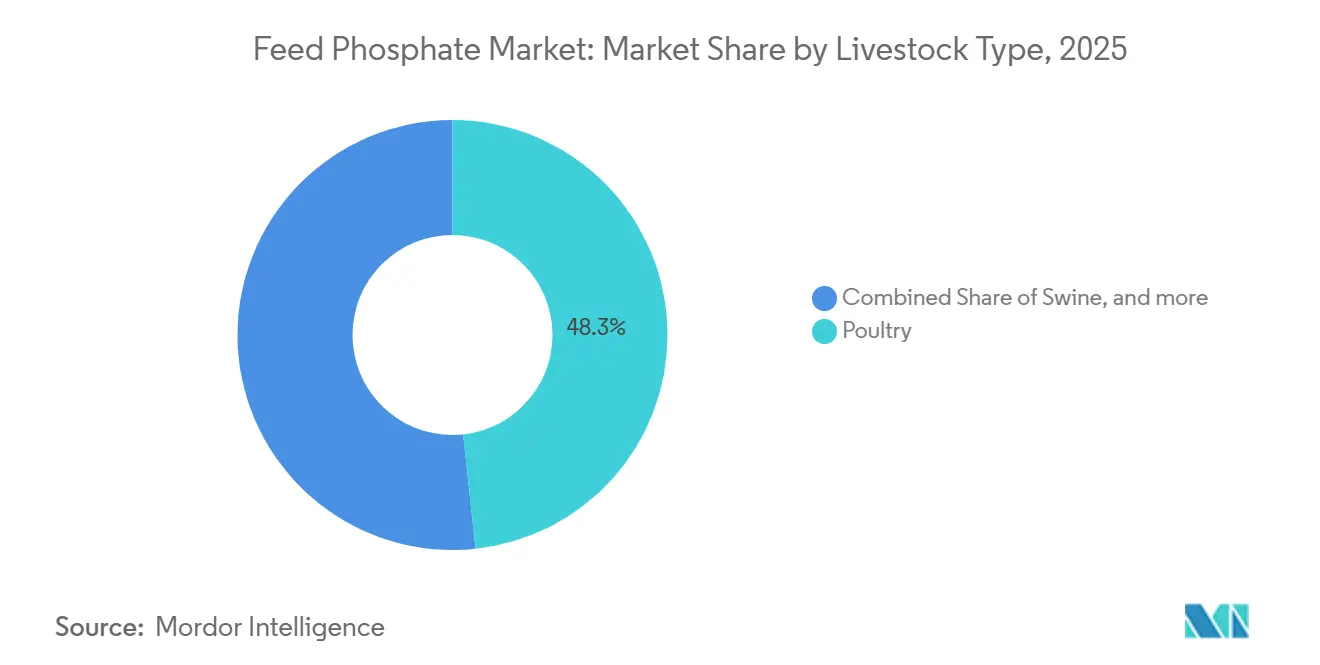

- By livestock type, poultry accounted for 48.3% of the feed phosphate market share in 2025, while aquatic animals are set to post the fastest growth at 5.4% CAGR to 2031.

- By geography, Asia-Pacific commanded a 34.2% share of the feed phosphate market size in 2025, whereas Europe is advancing at a 5.2% CAGR during the forecast period.

- The Mosaic Company, OCP S.A., Public Joint-Stock Company PhosAgro, Yara International ASA, and EuroChem Group AG accounted for significant revenue in the feed phosphate market in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Feed Phosphate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for meat and dairy proteins | +1.1% | Global, highest in Asia-Pacific and South America | Long term (≥ 4 years) |

| Expansion of industrial livestock operations | +1.0% | North America, Europe, and Asia-Pacific core | Medium term (2–4 years) |

| Technological advances in precision feed processing | +0.7% | North America and Europe, and spill-over to the Asia-Pacific | Medium term (2–4 years) |

| Insect-protein co-feeding improving phosphate utilization | +0.4% | Europe, North America, and early Asia-Pacific adoption | Long term (≥ 4 years) |

| Phosphorus-recycling mandates accelerating circular feed phosphates | +0.6% | Europe, North America, and pilot projects in Asia-Pacific | Long term (≥ 4 years) |

| Artificial Intelligence driven precision phosphorus dosing cutting wastage and cost | +0.5% | North America, Europe, and expanding to Asia-Pacific integrators | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Meat and Dairy Proteins

Total meat consumption is projected to grow by 47.9 metric tons over the next decade. Annual per capita consumption is projected to rise by 0.9 kg per capita per year (edible retail weight equivalent) by 2034. In high-income countries, concerns about animal welfare, environmental impact, and health are influencing consumer behavior, leading to stagnation in per capita meat consumption in some cases, with poultry and pork driving gains in Asia-Pacific and South America[1]Source: Meat, "OECD-FAO Agricultural Outlook 2025-2034," oecd.org. Urbanization in China and India pushes disposable incomes toward animal-protein diets that require phosphate-fortified rations for broilers, finishers, and high-yielding dairy cows. Brazil and Argentina expanded confined feeding to supply export markets, signing multi-year phosphate contracts that stabilize prices yet tighten spot availability. Demand remains resilient because minimum phosphorus thresholds cannot be breached without compromising bone integrity, even as precision tools shave inclusion rates. Consequently, the feed phosphate market continues to track the protein transition despite efficiency gains.

Expansion of Industrial Livestock Operations

Concentrated animal feeding operations in the United States housed 9.2 million cattle, 73 million hogs, and 1.8 billion broilers in 2025, channeling demand toward high-purity phosphates that ensure consistent growth and traceability[2]Source: United States Department of Agriculture, “Feed Composition Tables,” usda.gov. European farms with grew, a scale that rewards suppliers capable of producing uniform particle size and certified low heavy metals. China’s top pork producers controlled significant output in 2025, up four points in one year, and co-invested in dedicated phosphate blending lines that crowd out local mills. Larger herds intensify scrutiny of manure management, pushing integrators to prefer bioavailable phosphates that reduce excretion loads. Volume contracts signed by mega-integrators also compress margins for independent blenders, yet they provide demand visibility that encourages upstream investment in new kilns.

Insect-Protein Co-Feeding Improving Phosphate Utilization

Black soldier fly meal delivers 1.2% to 1.8% phosphorus at 85% digestibility, allowing integrators to reduce inorganic phosphate by one-fifth while retaining growth metrics. The European Union cleared seven insect species for use in poultry and aquaculture, lifting production to 120,000 metric tons in 2025[3]Source: European Food Safety Authority, “Insect Protein in Feed,” efsa.europa.eu. Retail chains link insect inclusion to eco-labels that command premiums, nudging feed formulators toward blended products. In the United States, regulators will finalize bioavailability guidance in 2026, a step that will broaden adoption among larger integrators. Co-feeding trials also improve gut health and reduce mortality, indirect savings that offset the price premium of insect meal. Suppliers of feed phosphate market products are therefore partnering with insect-protein firms to secure cross-functional cost advantages.

Phosphorus-Recycling Mandates Accelerating Circular Feed Phosphates

The European Fertilizers Regulation requires that a significant portion of feed phosphorus must be obtained from recycled materials by the end of the decade. In recent years, pilot struvite plants in countries such as the Netherlands and Denmark have successfully recovered substantial quantities of phosphorus, sufficient to cater to the requirements of specialized organic feed mills. In the United States, nutrient credit programs associated with Chesapeake Bay have significantly reduced the financial burden of installing manure struvite reactors, making these projects economically viable for large-scale integrators managing extensive livestock operations. Although recycled inputs remain more expensive than conventional alternatives, rising costs associated with carbon emissions and discharge fees are gradually narrowing the price gap. Industry forecasts suggest that the market for recycled feed phosphate will experience substantial growth in the coming years, with volumes projected to increase significantly as advancements in economies of scale and process efficiencies drive down production costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulations on phosphorus run-off | -0.8% | North America (Chesapeake Bay), Europe (Baltic Sea), and Asia-Pacific (Yangtze River) | Medium term (2–4 years) |

| Volatility in phosphate-rock prices | -0.5% | Global, strongest where import dependence is high | Short term (≤ 2 years) |

| Geo-political supply risk to Moroccan and Russian rock exports | -0.4% | Global, heightened in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Carbon-pricing schemes inflating high-energy thermal defluorination costs | -0.6% | Europe, North America, and trial programs in Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulations on Phosphorus Run-Off

The Chesapeake Bay Total Maximum Daily Load limits annual phosphorus discharge to 8.3 million kilograms and imposes fines of up to USD 500,000 for repeat violations, requiring producers to reduce dietary phosphorus by 12% to 18%[4]Source: Environmental Protection Agency, “Chesapeake Bay TMDL,” epa.gov. This regulation has driven significant changes in feed formulations and manure management practices to meet compliance standards. In the Baltic Sea region, a discharge limit has driven advancements in manure treatment technologies and precision feeding practices, enabling more efficient nutrient utilization. Compliance costs have tightened profit margins in price-sensitive markets, compelling producers to adopt cost-effective solutions. While the use of phytase and AI dosing provides some relief by improving phosphorus digestibility and reducing waste, overall phosphate volumes in regulated watersheds remain stable or decline, tempering growth in the broader feed phosphate market.

Carbon-Pricing Schemes Inflating High-Energy Thermal Defluorination Costs

Thermal defluorination requires significant energy, resulting in substantial carbon dioxide emissions. The European Union's carbon pricing mechanism has increased production costs for defluorinated phosphate, as the average price of carbon allowances has risen sharply. Similarly, in California, the implementation of the cap-and-trade program has further impacted operational costs, forcing some facilities to cease operations. Electric kilns, which can significantly reduce emissions, offer a viable alternative. However, the high initial investment required for installation poses a challenge, particularly for smaller companies. Meanwhile, in China, feed phosphate producers benefit from exemptions under the national carbon pricing scheme, which provides a cost advantage and shifts a portion of global production to the region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feed Type: Dicalcium Phosphate Dominance Holds for Layers

Dicalcium phosphate captured 41.5% of the feed phosphate market share in 2025, reflecting its balanced calcium-to-phosphorus ratio that simplifies formulation and supports eggshell strength in layer diets. Layers represent a steady, price-sensitive customer base that values cost predictability, enabling dicalcium suppliers to secure annual contracts that underpin base-load demand in the feed phosphate market. Integrators appreciate the product’s free-flowing granules, which reduce bin bridging and improve mixing uniformity in high-throughput mills. Vertical-integrated majors leverage rock ownership to offer competitive delivered pricing, keeping regional blenders at bay. Nonetheless, even dicalcium lines are upgrading to lower fluorine profiles to meet tightening limits in China and India.

Monocalcium phosphate is the fastest-growing feed type, projected to log a 6.1% CAGR and raise its share of the feed phosphate market by 2031. Its 90%-plus bioavailability lets formulators cut total phosphorus while still hitting performance targets, a powerful value proposition in regions that tax nutrient discharge. Precision sensors quantify this advantage, enabling real-time optimization that lights up on dashboards for mill managers. Supply is ramping in Morocco and Saudi Arabia, where new acid-route plants can swing between mono- and dicalcium grades to match seasonal pulls.

By Livestock Type: Poultry Remains the Workhorse

Poultry accounted for the largest share of the feed phosphate market in 2025, at 48.3%, driven by the broiler and layer industries, which require precise mineral nutrition to prevent skeletal disorders and shell breakage. Large integrators in China, the United States, and Brazil hold multi-year supply deals that guarantee product flow and hedge price volatility. Phytase adoption trims inclusion rates but cannot fully replace inorganic phosphorus during rapid growth phases, sustaining a significant base load for phosphate blenders. Heat-stable monocalcium grades have found traction in pelleted feeds, where conditioning temperatures can top 80 degrees Celsius, a niche that commands healthy margins.

Aquaculture is the fastest-expanding user segment, slated to clock a 5.4% CAGR to 2031, as intensive shrimp and finfish operations proliferate along Asian and South American coastlines. Aquafeed formulators demand phosphorus levels with digestibility above 85% to minimize water pollution fines, attributes that favor high-spec monocalcium and blended insect-monocalcium products. Vietnam’s shrimp expansion alone pulled in record phosphate imports, straining logistics during peak stocking months. Land-based salmon recirculating farms in Europe are also adopting on-site recovered phosphates, an innovation that could dent conventional demand but build service revenue for suppliers that design and maintain recovery units.

Geography Analysis

Asia-Pacific generated 34.2% of the feed phosphate market share in 2025, anchored by China’s 28 million metric tons poultry sector and India’s accelerating aquaculture output. China mandates phytase inclusion yet still imports premium phosphates to meet low-fluorine demands, lifting Moroccan and Saudi deliveries in 2025. Southeast Asia’s shrimp boom has shifted preference toward monocalcium grades with verified 90% digestibility, a specification that regional blenders cannot yet match, leading to increased reliance on imports. Japan and South Korea provide fertile test beds for circular-phosphorus pilots, and government subsidies covering capital costs draw new entrants into the recycled feed phosphate market.

Europe is anticipated to witness the fastest growth, with a 5.2% CAGR through 2031, supported by the Farm to Fork Strategy and increasing carbon prices shaping procurement decisions. Germany, France, and the Netherlands dominate demand for premium grades with fluorine content below 0.18%, while Poland and Spain drive volume growth through poultry expansion aimed at export markets. In the United Kingdom, policies now offer payments for ecosystem services linked to reduced nutrient loading, promoting precision dosing and benefiting suppliers with detailed bioavailability dossiers.

The demand in North America, South America, the Middle East, and Africa presents a mixed outlook. United States consumption edges lower in regulated watersheds such as Chesapeake Bay and California, but stays stable nationally due to hog and broiler growth in the Midwest. Brazil’s exports to Asia push poultry and swine producers to lock in phosphate imports despite currency swings, with new insect-protein joint ventures promising partial substitution in premium lines. Saudi Arabia’s Ma’aden ships hundreds of thousands of metric tons annually from Ras Al Khair, offering significant discounts to strengthen its market presence in Egypt and Jordan. In sub-Saharan Africa, Nigeria and South Africa lift volume from a low base, although forex volatility forces integrators to stockpile two to three months of inventory, inflating working capital.

Regulatory Landscape

Feed phosphate regulation increasingly ties market access to contaminant controls and validated nutritional function. In China, the GB 7300.312-2025 standard for tricalcium phosphate replaced GB 34457-2017, tightening lead limits to 20 mg/kg and strengthening fluorine monitoring requirements, which increases compliance pressure for producers serving premium poultry and aquafeed channels. In the United States, the FDA continues to govern inorganic phosphate additives under 21 CFR Part 573, including specific identity and safety requirements for diammonium phosphate in ruminant feed (for example, minimum phosphorus content and heavy metal limits). A May 2025 Federal Register update also amended color additive rules to provide for the safe use of calcium phosphate.

In the European Union, feed strategies to reduce phosphorus excretion are reinforced through repeated authorizations and renewals of phytase zootechnical additives, which support lower inorganic phosphate inclusion while maintaining performance. The European Commission Implementing Regulation (EU) 2026/91 (January 2026) renewed a 6-phytase authorization for AB Enzymes Finland Oy, and Implementing Regulation (EU) 2026/404 (February 2026) authorized a 6-phytase preparation for Victory Enzymes GmbH, following Implementing Regulation (EU) 2025/1392 (July 2025) authorizing a 3-phytase for Fertinagro Biotech S.L. Canada and the United Kingdom have also updated feed-related legislative frameworks (Feeds Regulations, 2024 in Canada and the Feed Additives (Authorisations) Regulations 2024 in the UK), supporting continued alignment around authorization, labeling, and safety documentation for mineral feed additives across major import markets.

Competitive Landscape

In 2025, major players such as The Mosaic Company, OCP S.A., Public Joint-Stock Company PhosAgro, Yara International ASA, and EuroChem Group AG dominated the feed phosphate market, indicating moderate industry concentration. EuroChem AG and Yara International ASA installed electric kilns that cut carbon by 60%, cushioning them against rising European Union emission prices and appealing to integrators chasing low-carbon egg and meat labels. Groupe Roullier S.A.’s TIMAB unit differentiates through customized blends that incorporate trace minerals and organic acids, attracting premium clients in the aquaculture sector.

Strategy now gravitates toward backward integration into insect-protein coproducts, circular-phosphorus recovery, and software partnerships that lock in formulation data flows. Nutrien Ltd. and J.R. Simplot Company are piloting manure-struvite units that could eventually supply 10% of their volumes, hedging rock-price risk and meeting carbon-intensity targets during the 2025-2026 period. Saudi Arabian Mining Company (Ma'aden) capitalizes on low-cost gas to undercut Moroccan and Russian exports into Middle Eastern and East African markets, shifting regional trade flows.

Emergent rivals include Chinese producers Guizhou Chia Tai Industry Co., Ltd. (Charoen Pokphand Group Co., Ltd.), Lomon Billions Group Co., Ltd., and WengFu Group Co., Ltd., which added 280,000 metric tons in 2025 but face heavy-metal hurdles that limit penetration into premium export channels. In India, Vishnupriya Chemicals Pvt. Ltd supplies budget dicalcium phosphate but lacks rock security, making margins hostage to spot volatility. Compliance with Association of American Feed Control Officials and European Feed Materials Register standards has become the ticket to tier-one integrators, spawning demand for third-party labs and reinforcing barriers to entry. Suppliers that bundle analytics, certificates, and supply guarantees are therefore best placed to defend and grow share in an increasingly data-driven feed phosphate market.

Feed Phosphate Industry Leaders

-

The Mosaic Company

-

OCP S.A.

-

Public Joint-Stock Company PhosAgro

-

EuroChem Group AG

-

Yara International ASA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary opportunity area sits at the intersection of purity compliance and nutrient-reduction programs. Higher-bioavailability grades (and enzyme-enabled formulations) can help producers address runoff constraints without compromising performance. European Commission renewals and authorizations for phytase products through 2025-2026 (for example, Implementing Regulations (EU) 2026/91 and 2026/404) lift the practical ceiling for enzyme-plus-phosphate optimization in poultry and swine rations. This supports differentiated offerings that pair consistent low-impurity phosphate supply with documentation and advisory services that quantify digestible phosphorus contribution.

Regional value-added manufacturing and circular-phosphorus sourcing also create whitespace, especially where import dependence, impurity limits, and logistics costs overlap. In Jordan, Jordan Phosphate Mines Company (JPMC) reported ongoing construction of a JD 25 million phosphate feed additives plant in Aqaba (started August 2025, production planned for Q1 2027), pointing to nearer-to-consumer conversion capacity in the Middle East. At the same time, tightening contaminant standards such as China GB 7300.312-2025 (Pb and fluorine monitoring) raise the need for upgraded processing, quality systems, and third-party testing. That, in turn, supports demand for suppliers that can demonstrate batch consistency across DCP, MCP, MDCP, and tricalcium phosphate while maintaining reliable delivery to integrated poultry and aquaculture customers.

Recent Industry Developments

- July 2026: The Mosaic Company expanded phosphate output curtailments across multiple North American plants and additional Brazilian facilities amid sulfur supply disruptions and elevated input costs. The action tightened availability across phosphate value chains, with knock-on effects for feed-grade phosphate pricing and contract coverage strategies.

- December 2025: Saudi Arabian Mining Company (Ma'aden) received approval from the Ministry of Energy for feedstock allocation to develop its Fourth Phosphate Project, adding 1.1 million metric tons of ammonia and 2.5 million metric tons of phosphate capacity per year. The decision strengthens Ma'aden's ability to supply incremental phosphate derivatives, supporting export-oriented availability into Middle Eastern and adjacent markets.

- February 2025: OCP S.A. increased its ownership in Spain's GlobalFeed S.L. to 75% through the acquisition of an additional 25% stake. The acquisition broadened OCP's downstream animal nutrition footprint in Europe and supported tighter integration between phosphate sourcing and the sales of feed-grade DCP, MCP, and MDCP portfolios.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the feed phosphate market includes inorganic phosphate additives sold for animal nutrition, where they are blended into compound feed to support growth, bone development, and better nutrient use.

Scope exclusions: We exclude human food phosphates, pharma grade phosphates, and industrial phosphate uses that are not intended for animal feed applications.

Segmentation Overview

-

By Feed Type

- Monocalcium Phosphate

- Dicalcium Phosphate

- Mono-Dicalcium Phosphate

- Tricalcium Phosphate

- Defluorinated Phosphate

- Other Feed Types

-

By Livestock Type

- Poultry

- Swine

- Cattle

- Aquatic Animals

- Other Livestock Types

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- France

- Russia

- Spain

- Rest of Europe

-

Asia-Pacific

- India

- China

- Japan

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

-

Africa

- South Africa

- Nigeria

- Rest of Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure for the model and to anchor it to measurable signals. We reviewed public sources such as FAOSTAT for livestock and feed indicators, UN Comtrade for trade flows of phosphate materials, and USDA and European Commission agriculture dashboards for animal production trends and feed demand context.

Alongside these, we scanned sources such as USGS phosphate rock statistics, selected peer-reviewed animal nutrition journals, and trade association publications that discuss feed additive usage and regulatory changes. Company annual reports, investor presentations, and reputable press were used to cross-check capacity announcements, plant utilization commentary, and regional revenue exposure. We then used a paid subscription source for company financials and a patent database selectively to fill in gaps on product activity and innovation direction. The sources listed here are illustrative, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating how demand is formed and priced in real buying cycles, since feed phosphates are sensitive to phosphate inputs and livestock feed economics. We spoke with producers, distributors, premix and feed formulators, and large end users across APAC, EMEA, and the Americas, and that input helped confirm inclusion boundaries, typical application rates, and how contract pricing and spot pricing move through the year.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 19% | APAC: 50% |

| Mid tier: 49% | Functional/Unit leaders: 29% | EMEA: 29% |

| Smaller Players: 22% | Managers: 52% | Americas: 21% |

Market-Sizing & Forecasting

Sizing started from a top-down demand pool build, where animal output and feed production signals were used to reconstruct feed phosphate consumption by region, and then translated into value using a blended pricing view. Once that picture was formed, selective bottom-up checks were used to keep totals realistic, including supplier roll-ups in key regions and sampled price by volume calculations from channel discussions.

To keep the model practical, a short list of inputs was prioritized and stress-tested, including livestock population and production trends, feed output and industrial feed mix shifts, typical phosphate inclusion rates in feed formulations, trade flows for phosphate intermediates, and observed price movement tied to phosphate raw materials and energy. Where a bottom-up check had missing coverage, for example limited visibility on smaller regional traders, gaps were handled using conservative penetration assumptions that were validated through interviews.

For forecasting, scenario analysis was used because the market is influenced by livestock cycle swings and input cost volatility. Growth paths were set using consensus ranges from primary experts, then adjusted for expected changes in animal protein demand, feed production expansion in APAC, and cost pass-through behavior that affects purchasing timing.

Data Validation & Update Cycle

Outputs were triangulated against independent signals so the value trend and the implied volumes made sense at the same time, and then anomaly checks were run at region level before sign-off. If a region showed an unusual jump, we re-checked the assumptions behind inclusion rates, price timing, and trade balance, and then re-contact was triggered with selected experts to confirm what changed.

The report is refreshed on an annual cycle, and interim updates are made when material events occur, such as major capacity changes or sharp moves in phosphate input pricing. Before delivery, an analyst completes a final pass to confirm currency conversion timing and to ensure the latest public releases are reflected in the model.

Mordor Intelligence's Feed Phosphate Market Size Compared Against Other Published Estimates

Published market sizes for feed phosphate can look different because the year used, the currency conversion timing, and the way average selling prices are blended across contracts and spot purchases are not handled the same way. Differences also come from what gets counted as feed grade phosphate versus adjacent phosphate chemicals, and how quickly the model is refreshed after price or livestock cycle changes.

In this study, the refresh cadence is tied to material price moves and regional demand signals, and the currency timing is kept consistent with the pricing window used for ASP blending. This is then verified through interview re-checks and trade-flow sanity tests, a pattern followed in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.31 B (2026) | |

| Industry Publisher A | USD 2.79 B (2025) | Uses an earlier base year and can understate the impact of later price resets, especially if currency conversion is applied on annual averages that do not match the pricing period in feed phosphate contracts. |

| Global Consultancy B | USD 2.79 B (2024) | A longer forecast frame is presented, and the value build can diverge if ASPs are smoothed without enough checks on livestock cycle timing, feed output shifts, and the split between spot and contract pricing across regions. |

The table shows that much of the spread is explained by base-year choice and how pricing is timed and blended into ASPs, which then changes the value even if the underlying demand picture is similar. By keeping assumptions traceable to livestock and feed indicators, and by re-checking pricing logic with market participants, we arrive at a balanced estimate that can be repeated and audited year over year.

Key Questions Answered in the Report

How large will global demand for feed phosphate become by 2031?

The feed phosphate market size is forecast to reach USD 4.42 billion by 2031, up from USD 3.31 billion in 2026.

Which feed type is gaining share the fastest?

Monocalcium phosphate is projected to grow at a 6.1% CAGR thanks to its superior bioavailability and compatibility with precision-nutrition programs.

Why is Europe the fastest-growing regional consumer?

European Union circular-phosphorus mandates, carbon pricing, and demand for premium protein exports are driving a projected 5.2% CAGR through 2031.

What is the main technology trend shaping phosphate inclusion rates?

Artificial-intelligence dosing systems coupled with near-infrared sensors enable real-time formulation, routinely cutting over-supplementation by 8% to 12%.

How are suppliers mitigating geopolitical rock-supply risks?

Strategies include securing long-term contracts with Moroccan producers, investing in circular phosphates such as struvite, and exploring deposits in Saudi Arabia and Australia.

Page last updated on: