Facial Makeup Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

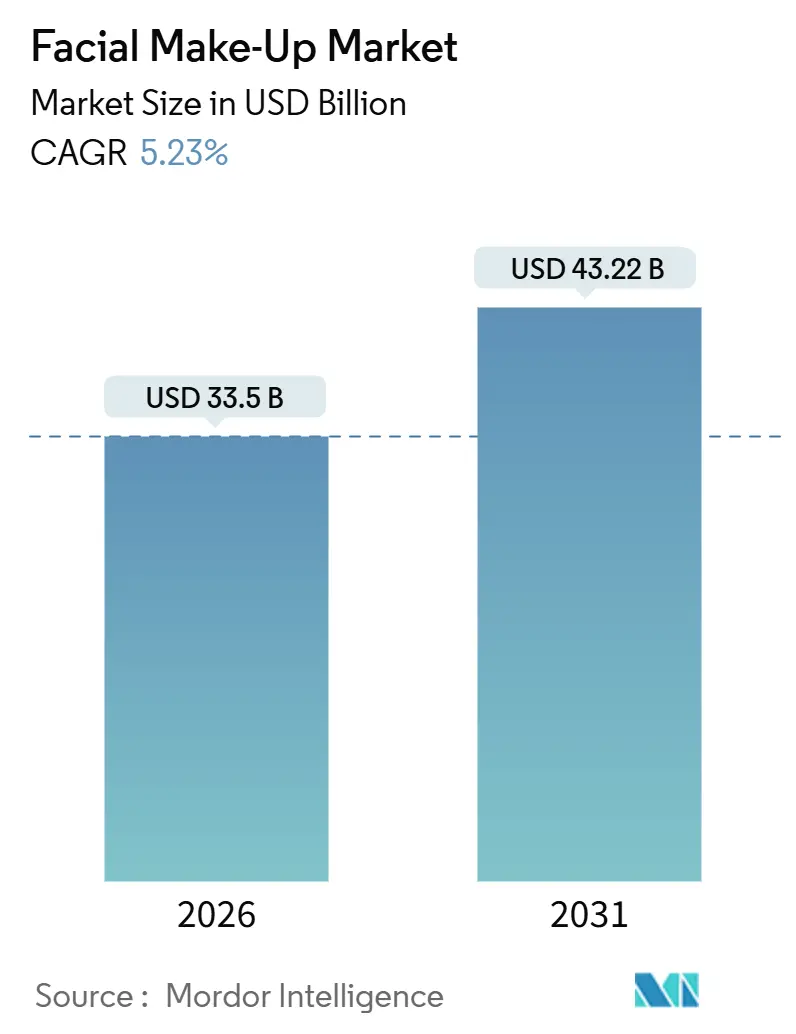

| Market Size (2026) | USD 33.5 Billion |

| Market Size (2031) | USD 43.22 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

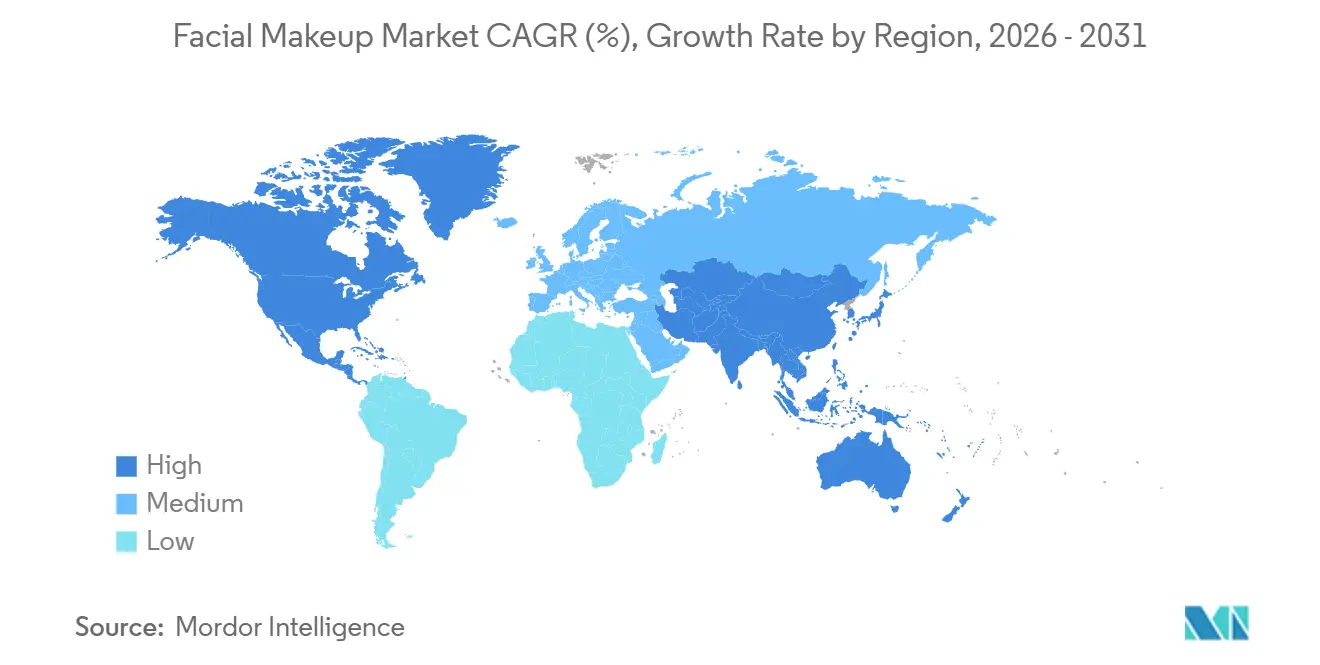

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Facial Makeup Market Analysis by Mordor Intelligence

The Facial makeup market size is estimated at USD 33.5 billion in 2026, and is expected to reach USD 43.22 billion by 2031, at a CAGR of 5.23% during the forecast period (2026-2031). This trajectory reflects a structural shift from consumption toward formulation sophistication, where brands embed active skincare ingredients, hyaluronic acid, peptides, and niacinamide into foundations and concealers to capture consumers who refuse to choose between coverage and treatment. Regulatory harmonization is accelerating this convergence; the European Union's Cosmetics Regulation 1223/2009 mandates safety assessments for novel ingredients, while the United States Modernization of Cosmetics Regulation Act of 2022 introduced facility registration and adverse-event reporting, narrowing the compliance gap that historically favored European formulators [1]Source: Food & Drug Administration, "Modernization of Cosmetics Regulation Act of 2022 (MoCRA)", fda.gov.

Key Report Takeaways

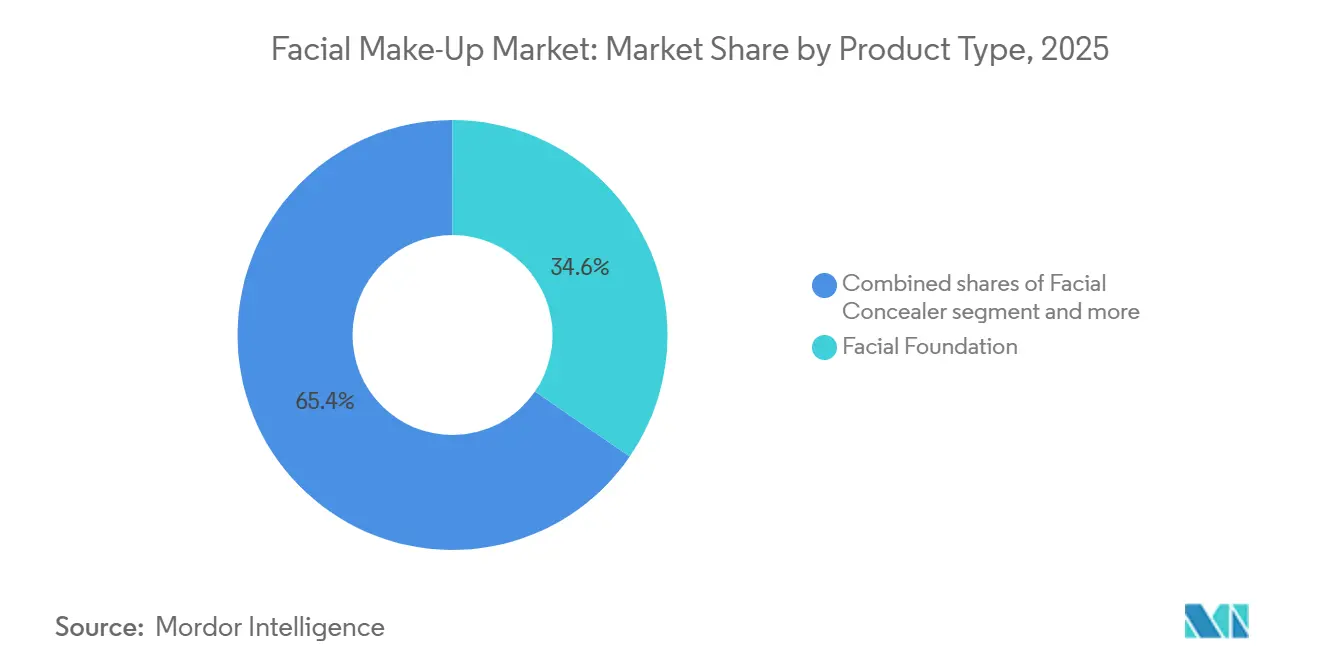

- By product type, facial foundation led with a 34.56% revenue share in 2025, while facial concealer is advancing at a 5.77% CAGR through 2031.

- By formulation, synthetic products commanded 78.94% of the face makeup market share in 2025; organic and natural alternatives are expanding at a 6.21% CAGR.

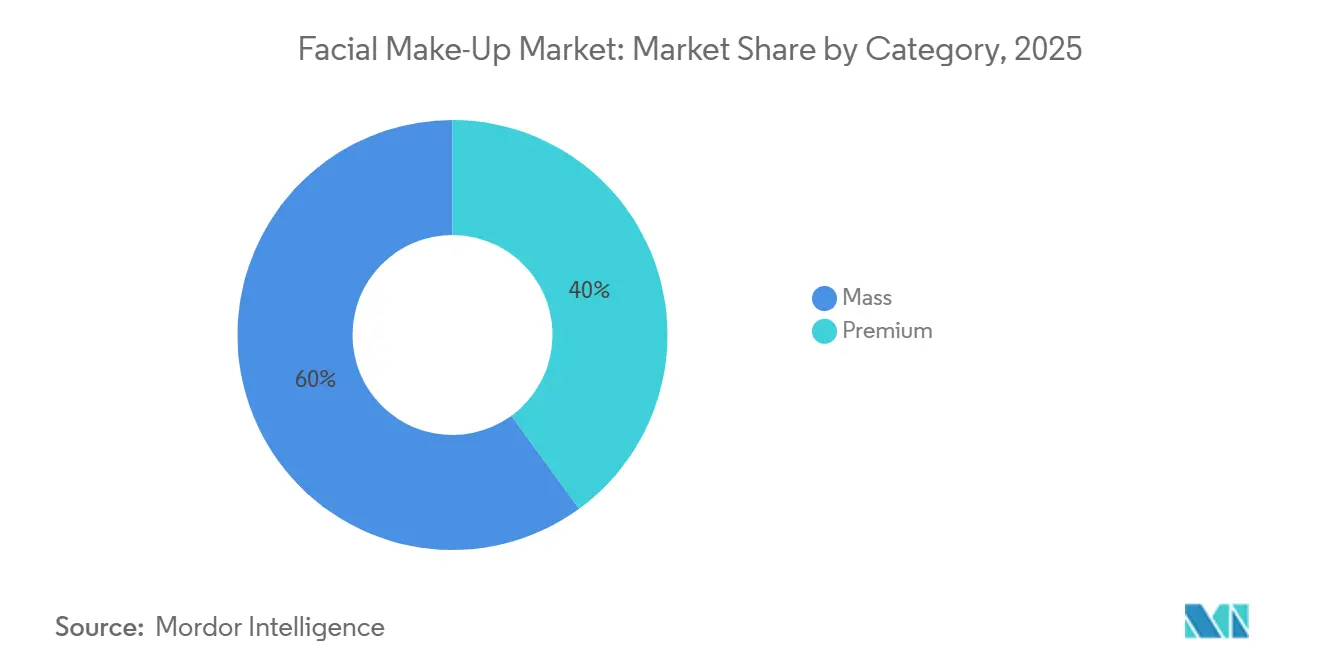

- By category, mass offerings held 60.03% of sales in 2025, whereas premium lines are projected to grow at a 7.36% CAGR.

- By distribution channel, beauty and health stores captured 49.33% of the 2025 value, yet online retail is rising at a 6.29% CAGR.

- By geography, North America controlled 32.68% of 2025 turnover, while Asia-Pacific is forecast to post the fastest 7.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Facial Makeup Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer Inclination Towards Organic and Natural Products | +0.8% | Global, with premium segments in North America and Europe leading adoption | Medium term (2-4 years) |

| Influence of Social Media and Celebrity Endorsement | +1.2% | Global, particularly strong in North America, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Technological Innovations in Product Formulations | +0.9% | North America, Europe, Japan, South Korea (innovation hubs) | Long term (≥ 4 years) |

| Urban Lifestyles Increasing Daily Makeup Routines | +0.7% | Asia-Pacific core (China, India, Indonesia), spillover to Middle East urban centers | Medium term (2-4 years) |

| Increasing Inclusivity with Diverse Shade Ranges | +0.5% | North America and Europe primary; expanding to Latin America and Middle East | Short term (≤ 2 years) |

| Rising Demand for Multifunctional Skincare-Infused Beauty Products | +1.0% | Global, with Asia-Pacific and North America showing highest penetration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer inclination towards organic and natural products

Certified-organic and natural-ingredient claims are reshaping formulation roadmaps, particularly in premium segments where consumers aged 18 to 29 exhibit more willingness to pay a markup for products free from synthetic preservatives and fragrances. The European Union's ban on 1,328 cosmetic substances, compared to the United States Food and Drug Administration's prohibition of only 11, creates a regulatory arbitrage that European brands exploit by marketing "EU-compliant" formulations as inherently safer, even when shipping to less-restrictive jurisdictions. This inclination extends beyond ingredient exclusion; brands now source plant-derived alternatives for traditionally synthetic components, such as castor oil-based emollients replacing silicones in liquid foundations. The shift is economically rational: NSF (National Sanitation Foundation) International's 2024 survey found 74% of respondents consider organic certification important when purchasing beauty products, and 45% actively seek such labels despite price premiums averaging 15% to 25% above conventional equivalents [2]Source: NSF International, "International's 2024 survey", nsf.org.

Influence of social media and celebrity endorsement

Social platforms have compressed the product-discovery cycle from months to days, with studies reporting that makeup-related video content generated more views and higher engagement year-over-year, driven by micro-influencers who demonstrate application techniques rather than simply endorsing finished looks. Coty's CoverGirl brand recalibrated its strategy in 2024 to prioritize creator partnerships over traditional advertising, allocating approximately 60% of its marketing budget to influencer collaborations that yield measurable conversions through affiliate links and promo codes. Celebrity-founded lines such as Rare Beauty by Selena Gomez and Haus Labs by Lady Gaga leverage existing fan bases to bypass the awareness-building phase that typically consumes a majority of a new brand's first-year budget. The economic impact is tangible: brands report that influencer-driven launches achieve breakeven 3 to 6 months faster than campaigns reliant on paid media alone, because social proof reduces the perceived risk of trying unfamiliar formulations.

Technological innovations in product formulations

Encapsulation technologies now enable time-release delivery of actives such as retinol and vitamin C within foundation matrices, addressing the historical trade-off between pigment stability and skincare efficacy. Shiseido's Synchro Skin line integrates responsive powder technology that adjusts to the skin's moisture levels throughout the day, a formulation approach validated through clinical trials showing 8-hour hydration retention. L'Oréal's acquisition of South Korean brand Gowoonsesang in 2024 for an undisclosed sum signals a strategic bet on fermentation-derived ingredients, galactomyces, and bifida ferment lysate, which Asian consumers associate with skin-barrier repair. SPF (Sun Protection Factor) integration remains a formulation frontier; Croda International reported in 2025 that its encapsulated UV-filter technology allows brands to achieve SPF 30 without the white cast or greasiness that historically deterred consumers from daily use. These innovations compress the boundary between makeup and skincare, enabling brands to command premium pricing by positioning products as dual-function investments rather than discretionary color cosmetics.

Urban lifestyles increasing daily makeup routines

Urbanization in Asia-Pacific, where megacities like Mumbai, Jakarta, and Manila are adding millions of middle-class consumers annually, correlates with higher makeup adoption rates as professional dress codes and social-media visibility norms elevate grooming standards. India's cosmetics market is expanding as disposable incomes rise and e-commerce platforms like Nykaa democratize access to international brands previously confined to metro-area department stores. China's "Healthy China 2030" initiative, while focused on wellness, indirectly supports cosmetics demand by promoting self-care routines that include skincare and makeup as components of holistic health [3]Source: National Health Commission of China, "Healthy China 2030", en.nhc.gov.cn. Urban consumers in these markets favor multi-step routines, primer, foundation, concealer, powder, bronzer, which drive per-capita spending above rural or suburban cohorts. The trend is self-reinforcing: as makeup becomes normalized in professional settings, non-users face implicit pressure to adopt minimal routines, expanding the addressable market beyond early adopters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Counterfeit Products | -0.6% | Global, with highest incidence in Asia-Pacific and Middle East e-commerce channels | Short term (≤ 2 years) |

| Health Concerns Over Chemical Ingredients | -0.4% | North America and Europe primary; spreading to educated urban consumers in Asia-Pacific | Medium term (2-4 years) |

| High Costs of Premium Makeup Products | -0.5% | Emerging markets in Latin America, Middle East, Africa; price-sensitive segments in developed markets | Long term (≥ 4 years) |

| Stringent Cosmetic Safety and Labeling Regulations | -0.3% | Europe (EU Regulation 1223/2009), North America (MoCRA), expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit products

The Organisation for Economic Co-operation and Development estimated global counterfeit trade at USD 464 billion in 2024, with cosmetics and personal care representing significant volume, eroding brand equity, and exposing consumers to untested formulations that bypass safety protocols. E-commerce platforms amplify the challenge; third-party sellers on marketplaces can list counterfeit products alongside authentic inventory, and consumers often lack the expertise to distinguish packaging differences. Brands are responding with blockchain-based authentication systems. L'Oréal piloted a QR-code verification program in China during 2025 that allows consumers to scan product packaging and confirm authenticity through a secure ledger. Regulatory enforcement remains inconsistent; the European Union's Intellectual Property Office seized 3.2 million counterfeit cosmetic items at borders in 2024, yet online channels continue to evade detection through dropshipping models that obscure supply-chain origins.

Health concerns over chemical ingredients

Consumer skepticism toward synthetic preservatives, fragrances, and colorants is reshaping formulation priorities, particularly in North America and Europe, where advocacy groups publicize ingredient risks through social media and mobile apps that rate product safety. Parabens, phthalates, and formaldehyde-releasing preservatives face the most scrutiny; brands reformulating to exclude these ingredients incur higher raw-material costs, a burden that mass-market players struggle to absorb without raising retail prices. The clean-beauty movement, defined by ingredient transparency and exclusion lists, has grown from a niche positioning to a mainstream expectation, with a significant portion of consumers in developed markets actively seeking "free-from" claims on packaging. This shift compresses margins for brands that cannot justify premium pricing, as reformulation expenses collide with consumer resistance to price increases in categories perceived as discretionary.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Concealer Outpaces Foundation Growth

Facial foundation held a 34.56% share in 2025, reflecting its role as the category anchor, yet facial concealer is expanding at 5.77% CAGR through 2031, faster than the overall market, as social-media tutorials normalize multi-step complexion routines that position concealer as essential rather than corrective. Influencers demonstrate techniques such as "baking" and "color correcting" that require dedicated concealer formulations with higher pigment loads and creamier textures than foundation, driving per-capita spending among engaged consumers. Face powder and blush maintain steady demand in mature markets but face headwinds in Asia-Pacific, where cream and liquid formats aligned with dewy-finish aesthetics are displacing powder compacts. Bronzer is experiencing a resurgence as contouring techniques popularized by beauty influencers migrate from professional makeup artistry to everyday routines, particularly among consumers aged 18 to 35 who view sculpting as a skill-building hobby rather than a time-intensive chore.

Other product types, BB creams, CC creams, primers, and contour sticks, are growing in line with the broader market as brands bundle multiple benefits into single SKUs to simplify routines for time-constrained consumers. L'Oréal's Infallible Pro-Glow Foundation integrates primer benefits, eliminating a separate step and appealing to consumers who prioritize efficiency over customization. The shift toward multifunctional products compresses the traditional product hierarchy, where consumers historically purchased 5 to 7 face-makeup items; current data suggests the average routine now includes 3 to 4 products, with each delivering broader functionality. This consolidation benefits brands with strong R&D (Research and Development) capabilities, Shiseido, Estée Lauder, and L'Oréal, that can embed actives and performance features into fewer SKUs, while smaller players struggle to match the formulation sophistication required to justify premium pricing.

By Formulation: Natural Segment Gains Despite Synthetic Dominance

Conventional synthetic formulations commanded a 78.94% share in 2025, sustained by cost advantages and performance consistency that organic alternatives struggle to match, yet natural and organic products are advancing at a 6.21% CAGR as younger consumers, particularly those aged 18 to 29, prioritize ingredient transparency and environmental impact over price. The natural segment faces formulation constraints; plant-derived preservatives often deliver shorter shelf lives than synthetic parabens, and mineral pigments may lack the color intensity of synthetic dyes, limiting appeal among consumers who prioritize full coverage. Brands are addressing these trade-offs through hybrid formulations that combine natural actives with synthetic stabilizers, positioning products as "clean" without sacrificing performance.

Regulatory frameworks influence formulation choices; the European Union's Cosmetics Regulation 1223/2009 mandates safety assessments for novel ingredients, raising the barrier for natural-ingredient innovation, while the United States Modernization of Cosmetics Regulation Act of 2022 introduced facility registration and adverse-event reporting, narrowing the compliance gap. Synthetic formulations retain dominance in mass-market channels where price sensitivity limits consumer willingness to pay premiums for organic claims, yet premium brands, Chanel, Dior, and Tom Ford, are incorporating natural extracts to differentiate luxury offerings. The formulation divide is likely to persist through 2031, with synthetic products maintaining volume leadership while natural alternatives capture disproportionate value growth.

By Category: Premium Segment Captures Value Migration

The mass category accounted for 60.03% of 2025 revenue, anchored by accessible price points and wide distribution through supermarkets and drugstores, yet the premium segment is growing at 7.36% CAGR, substantially faster than the 5.23% baseline, as consumers trade up to formulations with clinical-trial backing, luxury packaging, and prestige-brand cachet. Premium brands command price premiums above mass equivalents by embedding skincare actives, offering personalized shade-matching services, and leveraging heritage narratives that position products as investments rather than commodities. Estée Lauder's Double Wear Foundation retails at approximately USD 42 to USD 48 per ounce, compared to USD 8 to USD 12 for mass-market alternatives like Maybelline Fit Me, yet the premium product delivers 24-hour wear claims validated through independent testing, justifying the markup for consumers who prioritize longevity.

Mass brands are responding by launching "masstige" lines, premium-positioned sub-brands sold at mid-tier prices, to capture consumers unwilling to pay luxury rates but seeking formulations superior to traditional drugstore offerings. L'Oréal Paris introduced Infallible Pro-Glow at a USD 14 to USD 16 price point, bridging the gap between mass and prestige while maintaining drugstore distribution. The premium segment's growth is concentrated in North America and Europe, where disposable incomes support discretionary spending on beauty, yet Asia-Pacific is emerging as a high-growth opportunity as rising middle-class cohorts in China and India adopt premium products as status symbols. The category divide is self-reinforcing: premium brands invest revenue in R&D, double the mass-market average, enabling formulation innovations that justify price premiums and sustain competitive moats.

By Distribution Channel: Online Retail Disrupts Specialty-Store Dominance

Beauty and health stores captured 49.33% of 2025 sales, reflecting the enduring appeal of in-person shade matching and product testing, yet online retail channels are expanding at 6.29% CAGR as augmented-reality try-on tools reduce return rates and specialty retailers integrate digital and physical touchpoints. The retailer opened 17 new stores in the same quarter and targets 1,500 total locations by 2028, signalling a belief that omnichannel strategies, where consumers research online and purchase in-store, or vice versa, will define the next competitive era. Sephora's partnership with Kohl's department stores, launched in 2021 and expanded through 2025, embeds beauty specialty shops within mass-retail footprints, capturing consumers who might not visit standalone Sephora locations.

Supermarkets and hypermarkets retain relevance in emerging markets where beauty specialty infrastructure is underdeveloped, yet their share is eroding as e-commerce platforms like Nykaa in India and Tmall in China offer broader assortments and home delivery. Online channels benefit from lower overhead costs, no rent, minimal staffing, enabling direct-to-consumer brands like Glossier and Rare Beauty to undercut traditional retail markups while maintaining comparable margins. The distribution shift is compressing the role of department stores, which historically served as prestige-brand gatekeepers; brands now launch products simultaneously across online, specialty, and department channels, reducing the exclusivity that once justified department-store premiums. Other distribution channels, salons, spas, and direct sales, are growing modestly as brands explore experiential retail formats that combine product sales with service offerings.

Geography Analysis

North America held a 32.68% share in 2025, anchored by the United States' mature consumer base and Canada's aligned beauty preferences, yet the region's growth is moderating as market saturation limits new-user acquisition. Clean-beauty trends are most pronounced here; approximately 40% of consumers actively seek "free-from" claims, and brands reformulating to exclude parabens and phthalates incur higher raw-material costs that compress margins unless offset by premium pricing. Specialty retailers like Ulta Beauty and Sephora dominate distribution, yet their expansion is slowing as prime real estate becomes scarce and online channels capture incremental growth. Canada's market mirrors the United States in consumer preferences but operates on a smaller scale, with bilingual labelling requirements adding modest compliance costs.

Asia-Pacific is expanding at 7.39% CAGR through 2031, the fastest among all regions, driven by urbanization in China, India, and Southeast Asia, where rising middle-class cohorts adopt makeup as professional dress codes and social-media visibility norms elevate grooming standards. South Korea remains the innovation epicenter; cushion compacts, a liquid foundation format dispensed through a sponge applicator, are spreading to Japan, Thailand, and Vietnam. India's cosmetics market is expanding as e-commerce platforms like Nykaa democratize access to international brands previously confined to metro-area department stores, and local players like Lakmé leverage Bollywood endorsements to maintain relevance against multinational entrants.

Europe, South America, and the Middle East and Africa collectively represent the remaining market share, with Europe characterized by stringent regulations. The European Union's Cosmetics Regulation 1223/2009 bans 1,328 substances, which favors established brands with robust compliance infrastructure. Germany, the United Kingdom, France, Italy, and Spain anchor European demand, yet growth is modest as aging populations and economic uncertainty constrain discretionary spending. South America's largest markets, Brazil, Argentina, and Colombia, exhibit strong beauty cultures where makeup is embedded in daily routines, yet currency volatility and import tariffs limit access to international premium brands, creating opportunities for regional players like Natura & Co. The Middle East and Africa are emerging frontiers; the United Arab Emirates and Saudi Arabia's affluent consumers favor luxury brands, while Nigeria and South Africa's growing middle classes drive mass-market adoption. Turkey straddles Europe and the Middle East, serving as a manufacturing hub for brands targeting both regions.

Competitive Landscape

The face makeup market registers a concentration score, indicating moderate consolidation dominated by multinational conglomerates such as L'Oréal, Estée Lauder, and Shiseido. L'Oréal's acquisition of South Korean brand Gowoonsesang in 2024 signals a strategy of portfolio diversification across price tiers and geographic origins, enabling the conglomerate to address fragmented consumer preferences without cannibalizing core brands. Estée Lauder's Double Wear franchise generates an estimated USD 1 billion to USD 1.5 billion annually, demonstrating that hero products with decades-long track records can sustain growth through incremental innovation, shade-range expansions, and SPF integration, rather than disruptive reformulations.

White-space opportunities cluster around underserved demographics, men's makeup, older consumers seeking age-appropriate formulations, and emerging formats such as refillable compacts that reduce packaging waste while locking consumers into proprietary ecosystems. Technology adoption is reshaping competitive dynamics; L'Oréal's Modiface platform powers virtual try-on features for over 70 brands, creating a data moat that informs product development by tracking which shades and finishes consumers preview most frequently.

Indie brands like Rare Beauty and Haus Labs leverage celebrity founders' social-media reach to achieve breakeven 3 to 6 months faster than campaigns reliant on paid media, compressing the capital requirements for market entry and intensifying competition in premium segments. Regulatory compliance is becoming a competitive advantage; brands with in-house toxicology teams can navigate the European Union's Cosmetics Regulation 1223/2009 and the United States Modernization of Cosmetics Regulation Act of 2022 more efficiently than smaller players reliant on third-party consultants, raising barriers to entry and consolidating market share among established conglomerates.

Facial Makeup Industry Leaders

-

L’Oreal S.A.

-

Revlon

-

LVMH Moët Hennessy Louis Vuitton SE

-

Chanel, Inc.

-

Unilever

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Japan’s leading makeup brand KATE, under Kao Corporation, launched a new base makeup line called (Tsukiyo no Kurage)”, featuring products designed to create a radiant, long-lasting finish. The line includes jelly-linked formulations such as face primers and concealers geared toward enhanced coverage and glowy skin effects, and it debuted in Japan on October 25, 2025 before rolling out to select Asian regional markets.

- September 2025: Luxury house Louis Vuitton launched La Beauté Louis Vuitton, marking its first full makeup line globally, led by acclaimed makeup artist Pat McGrath as Creative Director. This major expansion includes a broad color cosmetic range (lipsticks, eyeshadows, and more) sold through flagship stores and select retailers worldwide, signaling luxury fashion brands’ push into color cosmetics.

- April 2025: WakeMake (via CJ Olive Young Japan) released a new “Stay Fixer Multi Color Powder” in April 2025 designed to correct tone and control shine while unifying complexion. This product expands the powder range available in Japan with an emphasis on color correction and lightweight finish.

Global Facial Makeup Market Report Scope

Facial makeup products are products used to color and highlight facial features. The facial makeup market is segmented by product type (face powder, facial foundation, facial concealer, face bronzer, blush, and other types), formulation (conventional and organic), category (mass and premium),

distribution channel (supermarkets/hypermarkets, convenience stores, specialty stores, online retail stores, and other distribution channels), and geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa). The market forecasts are provided in terms of value (USD).

| Face Powder |

| Facial Foundation |

| Facial Concealer |

| Face Bronzer |

| Blush |

| Other Types |

| Conventional/Synthetic |

| Organic/natural |

| Mass |

| Premium |

| Supermarkets/Hypermarkets |

| Beauty and Health Stores |

| Online Retail Stores |

| Others Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Face Powder | |

| Facial Foundation | ||

| Facial Concealer | ||

| Face Bronzer | ||

| Blush | ||

| Other Types | ||

| Formualtion | Conventional/Synthetic | |

| Organic/natural | ||

| Category | Mass | |

| Premium | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Beauty and Health Stores | ||

| Online Retail Stores | ||

| Others Distribution Channel | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the face makeup market in 2026 and what growth is expected by 2031?

The face makeup market size is USD 33.50 billion in 2026 and is forecast to reach USD 43.22 billion by 2031 at a 5.23% CAGR.

Which region is expanding fastest in face makeup through 2031?

Asia-Pacific leads growth with a projected 7.39% CAGR, fueled by urbanization, innovation hubs, and rising middle-class disposable incomes.

What product segment is growing quicker than the overall category?

Facial concealer is the fastest mover, advancing at a 5.77% CAGR compared with the broader 5.23% pace.

How are online channels influencing face makeup sales?

Online retail is rising at a 6.29% CAGR, helped by augmented-reality try-ons and social-commerce integrations that reduce product-selection risk.

Page last updated on: