Chainsaw Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.92 Billion |

| Market Size (2031) | USD 5.99 Billion |

| Growth Rate (2026 - 2031) | 4.01% CAGR |

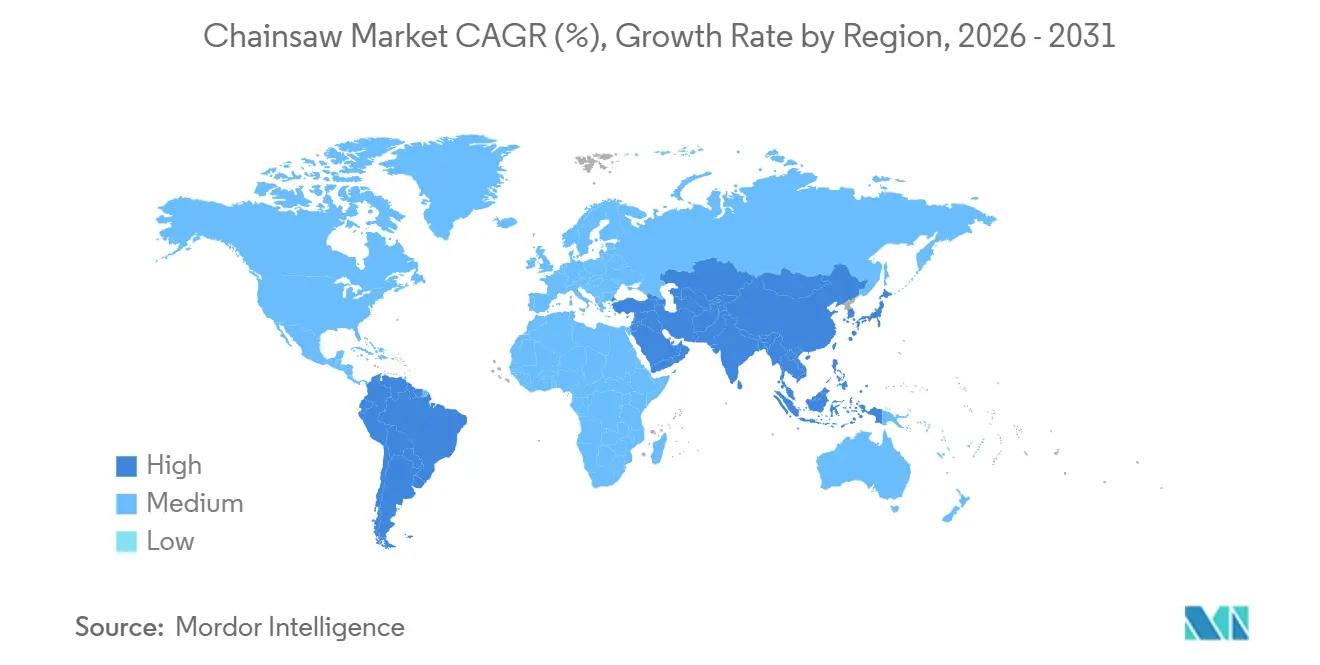

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chainsaw Market Analysis by Mordor Intelligence

The chainsaw market size was estimated at USD 4.78 billion in 2025 and is projected to reach USD 4.92 billion in 2026 and USD 5.99 billion by 2031, growing at a CAGR of 4.01% from 2026 to 2031. Purchasers are shifting from gas to battery platforms as California, New York, and Washington phase out small off-road gas engines, while California Air Resources Board vouchers cover up to 85% of the cost of 3,878 battery units in 2024. Disaster-related salvage logging, funded with USD 6.35 billion in United States Department of Agriculture supplemental appropriations, keeps demand elevated in hurricane- and wildfire-hit regions. Battery adoption is further encouraged by Section 301 tariffs that raised duties on lithium-ion cells to 25% and compressed margins for companies dependent on Asian supply, reinforcing the appeal of vertically integrated domestic battery production. North America currently dominates the value, yet Asia-Pacific is the fastest-growing region as Japan’s forestry mechanization subsidies accelerate electrification.

Key Report Takeaways

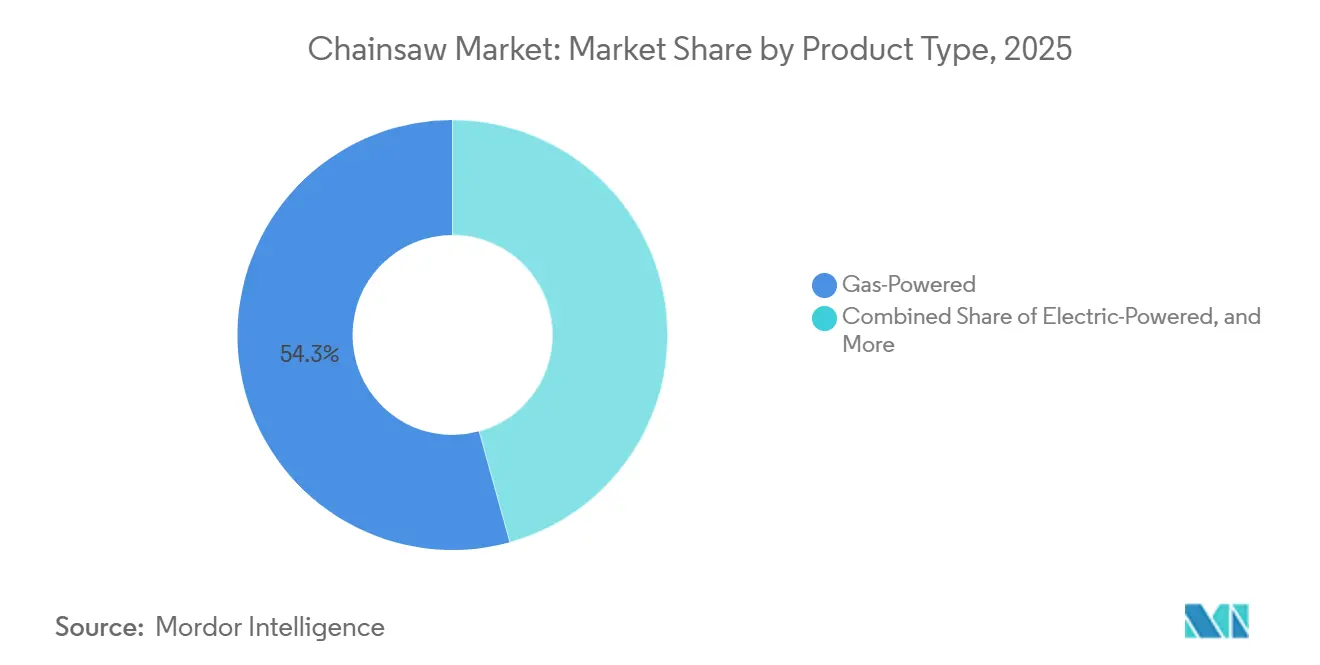

- By product type, gas-powered units held 54.3% of the chainsaw market share, and battery-powered models are forecast to expand at a 4.7% CAGR through 2031.

- By end-user, residential buyers accounted for 46.1% share of the chainsaw market in 2025, while commercial and professional fleets are projected to show the highest growth at a 5.1% CAGR through 2031.

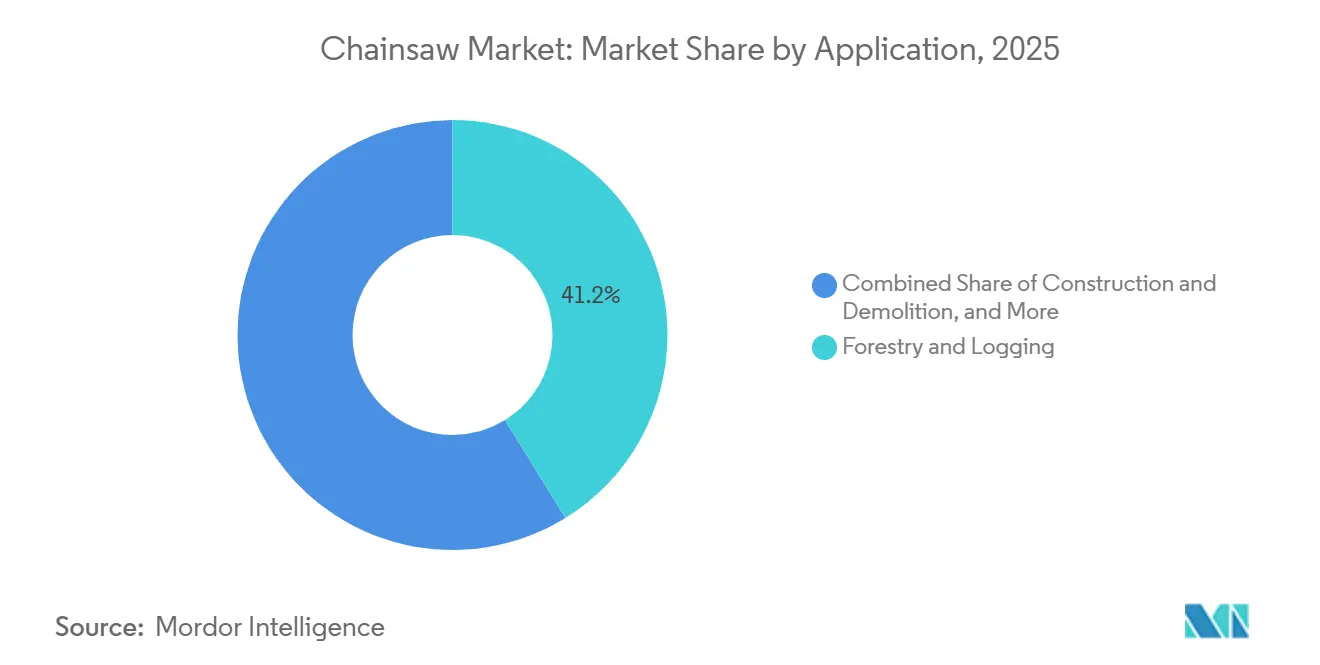

- By application, forestry and logging accounted for 41.2% of the chainsaw market size in 2025, and emergency and disaster relief is advancing at a 4.8% CAGR through 2031.

- By distribution channel, offline retail accounted for 63.2% of 2025 sales, but online platforms are growing the fastest, with a 5.3% CAGR to 2031.

- By bar length, 16–18 inch bars commanded 38% of the chainsaw market share, but bars less than 14 inches are growing the fastest, with a 5.4% CAGR to 2031.

- By geography, North America accounted for 40.2% of global value in 2025, while Asia-Pacific is projected to deliver the strongest regional CAGR of 5.0% through 2031.

- Market concentration is moderate, with the top five companies, ANDREAS STIHL AG & Co. KG (STIHL Holding AG & Co. KG), Husqvarna AB, Stanley Black & Decker, Inc., Makita Corporation, and Robert Bosch GmbH anticipated to collectively hold a majority of the market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Chainsaw Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Urban Wood Demand for Mass Timber Construction | +0.5% | North America and Europe | Medium term (2-4 years) |

| Growing Post-Storm Salvage Logging Activities | +0.6% | Central Europe | Short term (≤ 2 years) |

| Rising DIY Culture and E-commerce Tool Bundles | +0.5% | Global, highest in North America and Europe | Medium term (2-4 years) |

| Government Incentives for Low-Emission Battery Equipment | +0.7% | California, Oregon, Washington, Europe, and Japan | Long term (≥ 4 years) |

| Surge in Premium Outdoor Furniture Manufacturing | +0.4% | North America, Europe, and parts of Southeast Asia | Medium term (2-4 years) |

| Mandated Phase-Out of Small Off-Road Gas Engines in Key States | +0.8% | California, New York, Washington, and European Union | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Urban Wood Demand for Mass Timber Construction

The adoption of mass timber is driving increased demand for precision chainsaws in peri-urban sawmills, which are required to cut dimensional lumber for cross-laminated timber and glued-laminated panels. The Forest Products Laboratory projected in 2024 that this trend could increase softwood consumption in the United States by 2.1 million cubic meters annually, thereby supporting demand for mid-range bar-length chainsaws. European traceability regulations are prompting equipment upgrades, as smaller processors must document cut dimensions[1]Source: Forest Products Laboratory, “Mass Timber Construction Opportunities,” fpl.fs.fed.us. Additionally, the expansion of six-story mass-timber building codes in countries such as Canada, Germany, and Finland is broadening the addressable market for chainsaws. In the Asia-Pacific region, Japan’s early adoption of timber towers is anticipated to create a foundation for future demand. Collectively, these factors are contributing to growth in unit volumes and average selling prices, as well as to the overall adoption of advanced chainsaw technologies to meet evolving industry requirements.

Growing Post-Storm Salvage Logging Activities

The increasing frequency of hurricanes and wildfires in the North America and Gulf Coasts has led to emergency timber harvests, necessitating the swift deployment of professional crews equipped with durable chainsaws. These events have significantly impacted timber resources, requiring immediate action to mitigate losses and ensure resource recovery. In 2024, the United States allocated USD 6.35 billion in disaster supplemental funds to support salvage operations across southern states. Similarly, Europe reported 35 million cubic meters of storm-felled wood during the same year, highlighting the widespread impact of natural disasters on forestry[2]Source: United Nations Economic Commission for Europe, “Forest Products Annual Market Review 2024,” unece.org. Federal Emergency Management Agency (FEMA) reimbursements, capped at USD 219 per chainsaw for homeowners, have encouraged the purchase of compact battery-powered models for residential use. These episodic surges have replenished reseller inventories and increased spare parts consumption, further driving demand in the chainsaw market.

Government Incentives for Low Emission Battery Equipment

In 2024, California’s Clean Off-Road Equipment vouchers subsidized up to 85% of the purchase cost for battery chainsaws, supporting the transition to cleaner equipment in forestry and landscaping. During the same year, Japan’s Ministry of Agriculture, Forestry, and Fisheries increased forestry mechanization grants to promote the adoption of advanced machinery and improve operational efficiency. The European Union's Stage V regulations now prohibit non-compliant engines, establishing battery platforms as the standard for new equipment and driving innovation in battery technology. Manufacturers with local battery assembly operations benefit from avoiding import tariffs and complying with origin rules for public procurement, enhancing their competitiveness in regional markets.

Mandated Phase-Out of Small Off-Road Gas Engines in Key States

California implemented its zero-emission mandate starting with the 2024 model year, prohibiting the sale of new gas-powered chainsaws in the state. This initiative aims to reduce organic gas emissions by 2.7 metric tons per day by 2031. The mandate is part of broader efforts to address environmental concerns and transition to cleaner energy solutions. New York and Washington have adopted comparable timelines, collectively accounting for approximately 15% of the total demand in the United States. These states are setting a precedent for other regions to follow, potentially accelerating nationwide adoption of zero-emission equipment. Manufacturers with well-established battery product lines, such as ANDREAS STIHL AG & Co. KG and Stanley Black & Decker, Inc., are positioned to gain market share, while late adopters face the risk of being excluded. This regulatory shift is the most significant single driver of market growth, creating opportunities for innovation and investment in battery technology.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened End-User Safety Liability Insurance Costs | -0.5% | United States, Canada, United Kingdom, and Germany | Short term (≤ 2 years) |

| Noise-Abatement Bylaws in Peri-Urban Zones | -0.4% | California, Oregon, Virginia, Germany, and Netherlands | Medium term (2-4 years) |

| Tariff Volatility on Lithium-Ion Cells and Steel Components | -0.6% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Surge in Counterfeit Chains and Guide-Bars Undermining Equipment Manufacturer Revenue | -0.3% | Highest in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened End-User Safety Liability Insurance Costs

Insurance premiums for tree-service contractors and small logging firms are increasing due to the frequency of injury claims. In states like California, workers' compensation policies are priced at USD 18.50 per USD 100 of payroll in 2024, which is double the rate in Texas. These higher costs reduce net profit margins, discouraging investments in equipment upgrades and delaying fleet renewals. The financial strain is further exacerbated by rising compliance costs with safety regulations and the need for specialized training to mitigate workplace risks. While insurers have introduced modest premium credits for battery-powered models with advanced safety features, the high upfront purchase costs hinder adoption, reducing the projected CAGR by 0.5% points. Additionally, the limited availability of battery-powered equipment in certain regions further slows the transition to safer alternatives.

Tariff Volatility on Lithium-Ion Cells and Steel Components

Section 301 tariffs, implemented in May 2024 in the United States, increased duties on battery cells to 25% . This compelled import-dependent brands to either absorb cost inflation, raise prices, or consider reshoring production[3]Source: Office of the United States Trade Representative, “Section 301 Tariff Actions,” ustr.gov. The higher tariffs have significantly impacted the cost structures of companies relying on imported components, leading to strategic shifts in sourcing and manufacturing. Stanley Black & Decker’s Tools and Outdoor segment reported a gross margin erosion of up to 180 basis points for fiscal 2024. Additionally, currency fluctuations have amplified landed cost variances, while deferred product launches have slowed market refresh cycles, resulting in a 0.6%-point reduction in the compound annual growth rate (CAGR). These challenges underscore the broader implications of trade policies on market dynamics and operational strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gas-Powered Continues to Lead, Battery-Powered Climbs Faster

Gas-powered units dominated with a 54.3% of the chainsaw market share in 2025 due to established dealer networks, proven refueling convenience, and high torque suited for professional logging. Many forestry contractors retain gas fleets to avoid battery downtime during multi-shift harvest cycles, and disaster-relief agencies still stock gas models for rapid deployment, stabilizing baseline sales. However, Section 301 tariffs on steel and engine components have tightened margins for gas models, nudging manufacturers toward higher-value professional lines that can absorb cost inflation. The gas segment also benefits from slower replacement cycles in rural Asia-Pacific regions, where low fuel prices and limited charging infrastructure keep operating costs predictable, defending its core position in the global chainsaw market.

Battery-powered chainsaws represent the fastest-growing segment, advancing at a 4.7% CAGR through 2031 as voucher programs in California and subsidies in Japan compress payback periods for residential and commercial buyers. North American contractors serving noise-sensitive neighborhoods now view battery equipment as an operational necessity rather than a premium add-on, while European Union Stage V compliance effectively blocks new gas sales in many member states. ANDREAS STIHL AG & Co. KG reported that battery lines reached 25% of total revenue in 2024 and targets 35% by 2027, signaling a decisive pivot that other brands are racing to match. As battery chemistry improvements extend runtime and reduce charging lag, late adopters in forestry and construction are projected to convert, positioning battery units as the principal driver of incremental chainsaw market growth.

By End User: Commercial Fleets Accelerate Adoption

Residential owners were the largest end-user segment, accounting for 46.1% of the chainsaw market size in 2025, due to pandemic home-improvement habits and Federal Emergency Management Agency reimbursements that covered up to USD 219 per unit after Hurricane Francine. Homeowners gravitate to light 14-inch and 16-inch saws that handle yard debris yet fit inside budget bundles sold through online stores. Replacement cycles average eight to ten years, so the installed base of older gas saws remains high even as battery awareness grows. Safety concerns also limit frequent upgrades because many casual users cut branches only a few times per season. This long tail of legacy equipment tempers the speed of electrification in the residential arena.

Commercial and professional users are expanding at a 5.1% CAGR through 2031, making them the fastest-growing segment for incremental growth in the chainsaw market. Tree-care contractors must comply with local sound caps of 75 decibels at 50 feet in Los Angeles and similar rules elsewhere, so many now specify battery platforms when renewing fleets. Insurance carriers have begun offering 5 to 10% premium credits for tools that feature automatic chain brakes and low-kickback bars, nudging firms toward newer equipment. Disaster-relief grants from the United States Department of Agriculture also offset purchase prices for firms performing salvage logging in hurricane corridors. Faster depreciation schedules let businesses recover costs in three to five years, accelerating repeat purchases relative to the residential cycle.

By Distribution Channel: Online Platforms Wins Share from Dealers

Offline retail was the largest distribution channel, capturing 63.2% of chainsaw market revenue in 2025, as specialty dealers continue to bundle pre-delivery assembly, operator training, and in-house repair services valued by professional buyers. Dealer storefronts remain the preferred venue for high-horsepower saws and pneumatic units that require expert configuration before field deployment. Manufacturers such as ANDREAS STIHL AG & Co. KG leverage nearly 8,000 independent United States outlets to keep warranty turnaround times short, preserving loyalty among forestry crews that cannot risk downtime during harvest windows. Brick-and-mortar operations also stage seasonal promotions around hurricanes and wildfire cleanup when immediate availability trumps price.

Online platforms are growing fastest at a 5.3% CAGR through 2031, the strongest channel trajectory in the chainsaw market. Direct-to-consumer sites package saws with batteries, chargers, and accessory bundles, cutting effective entry costs by up to 40%, and free shipping narrows the convenience gap with local stores. Pandemic-era buying patterns normalized in 2023, yet e-commerce penetration remained structurally higher at 28% of United States outdoor power equipment sales, almost ten points above 2019 levels. Counterfeit parts on third-party marketplaces threaten brand trust, so leading manufacturers now embed serialization codes and smartphone authentication features to reassure shoppers. As warranty processes migrate online and same-day delivery spreads, smaller dealers may pivot toward service-only models while digital storefronts capture first-time residential buyers.

By Application: Emergency and Disaster Relief Leads Growth Spurts

Forestry and logging were the largest application segments, accounting for 41.2% of the chainsaw market in 2025, driven by sustained harvesting across the Canadian boreal region, Scandinavian softwood estates, and new eucalyptus plantations in Brazil. Professional squads require long-bar gas models to fell mature stems, and they consume a high volume of chains, bars, and fuel that boosts aftermarket value. Eastern European salvage campaigns targeting beetle-infested spruce expanded felling volumes through 2025, while North American mass-timber mills raise precision-cut lumber orders that favor mid-bar battery saws. Even with policy pressure to electrify, forestry crews operating in remote tracts keep gasoline units in rotation because charging options remain limited.

Emergency and disaster relief is the fastest-growing segment, with a 4.8% CAGR to 2031 as hurricanes, typhoons, and wildfires intensify worldwide. Federal grants and insurance payouts allow homeowners and municipal crews to replace damaged saws rapidly, often selecting compact battery models that are easier to start after long storage. The United States Department of Agriculture distributed USD 6.35 billion for forest disaster response in 2024, with a share earmarked for equipment grants that lifted fleet purchases across Gulf Coast states. Similar funding across Australia’s bushfire zones and European windthrow corridors replicates the pattern, fueling recurring demand spikes. Manufacturers respond by pre-positioning inventory in storm-prone logistics hubs so they can fill emergency tenders within days.

By Bar Length: Compact Models Capture New Users

Saws with 16- to 18-inch bars were the largest segment, commanding 38% of the chainsaw market share in 2025 because they balance cut capacity and maneuverability for both homeowners and mid-size commercial crews. Mass-timber panel factories and residential roofing teams prefer this range for dimensional accuracy and moderate weight. Manufacturers continue to add automatic chain tensioning and quick-stop brakes in this category, so unit prices carry modest premiums that retailers justify through safety messaging. Cross-tool battery compatibility also centers on the mid-bar class, enabling users to share packs with string trimmers and blowers, improving fleet economics.

Bars less than 14 inches will post the highest 5.4% CAGR through 2031 as first-time buyers, do-it-yourself hobbyists, and disaster-relief claimants embrace easy-handling designs. Voucher programs and Federal Emergency Management Agency reimbursements make compact battery saws almost cost-neutral for households clearing downed limbs after storms. Urban noise caps that penalize loud equipment further boost adoption, as short-bar saws pair with small brushless motors that run below municipal decibel limits. Manufacturers are racing to release sub-ten-pound models with tool-free chain adjustment, widening appeal to users previously intimidated by gasoline start-up procedures. In contrast, saws over 20 inches will stay niche outside commercial logging because battery torque cannot yet match the sustained output needed to mill large-diameter hardwoods.

Geography Analysis

North America accounted for largest segment with 40.2% of the chainsaw market revenue in 2025, driven by disaster relief spending that channeled USD 6.35 billion into salvage logging, debris removal, and homeowner reimbursement. California’s zero-emission rules, in effect since model year 2024, banned new gas chainsaws, shifting dealer inventories heavily toward battery-powered models and amplifying voucher uptake among disadvantaged communities. Canada’s boreal forest harvesting keeps demand robust for professional-grade gas units, yet British Columbia’s emerging emission standards foreshadow a gradual transition. Mexico’s construction boom, driven by nearshoring, advances mid-range bar-length sales despite limited regulatory pressure on engine emissions.

Asia-Pacific is projected to have the fastest CAGR of 5.0% through 2031, propelled by Japan’s USD 3.32 billion outdoor power equipment sector and generous forestry mechanization subsidies that prioritize battery-powered tools. China’s infrastructure expansion underpins substantial gas-powered demand in rural logging, but rising urban air-quality goals in Beijing, Shanghai, and Shenzhen are promoting battery adoption in landscaping. India’s restricted commercial logging narrows forestry demand, yet cyclone-driven emergency relief purchases offset part of the gap. Australia’s bushfire recovery programs and South Korea’s low-noise policies add incremental volumes, positioning Asia-Pacific as the most dynamic territory for the chainsaw market over the forecast horizon.

Europe remains the second-largest regional contributor, boosted by mandatory Stage V standards that outlaw non-compliant small engines in new equipment. The United Nations Economic Commission for Europe counted 35 million cubic meters of storm-felled wood in 2024, generating immediate salvage demand. Germany’s salvage logging from beetle-damaged spruce, France’s high-rise mass-timber construction, and the United Kingdom homeowner maintenance together sustain multichannel demand. Currency volatility and the European Union Battery Regulation, taking effect in 2026, encourage local battery assembly and recycling, giving European manufacturers a cost advantage over import-reliant competitors.

Competitive Landscape

Market concentration is moderate, with the top five companies, ANDREAS STIHL AG & Co. KG (STIHL Holding AG & Co. KG), Husqvarna AB, Stanley Black & Decker, Inc., Makita Corporation, and Robert Bosch GmbH collectively holding a majority of the market share in 2025. Stanley Black & Decker, Inc.'s Tools and Outdoor division reported revenue of USD 13.3 billion and is implementing a USD 2.0 billion cost-reduction initiative, redirecting the savings toward domestic battery assembly operations in Virginia.

Strategic moves focus on supply chain resilience. ANDREAS STIHL AG & Co. KG is finalizing a Romania battery-tool factory for an October 2025 start-up to mitigate Section 301 tariff exposure and meet European origin rules, while Husqvarna AB expanded lithium-ion pack production in Sweden to shorten fulfillment cycles across Europe. In parallel, several Chinese original equipment manufacturers, such as Changzhou Globe Tools Co., Ltd. and SUMEC Group, are launching branded battery chainsaws that undercut incumbents by up to 30%, though limited dealer networks restrict their penetration in North America and Europe. Intellectual property enforcement and serialized parts authentication have become priority countermeasures against the counterfeit aftermarket that erodes high-margin consumable sales.

Technology differentiation now centers on battery interoperability. Stanley Black & Decker, Inc.’s DEWALT POWERSHIFT system lets a single 60-volt pack power multiple tools, lowering effective per-tool cost and locking users into proprietary ecosystems. Husqvarna AB’s BLi-series batteries adopt a similar cross-platform approach that appeals to professional landscapers running multishift crews. As regulatory timelines tighten, brands that can bundle finance packages, training, and local service are anticipated to protect market share, while capital constraints could spur consolidation among smaller European and North American manufacturers over the next five years.

Chainsaw Industry Leaders

ANDREAS STIHL AG & Co. KG (STIHL Holding AG & Co. KG)

Husqvarna AB

Stanley Black & Decker, Inc.

Makita Corporation

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: ANDREAS STIHL AG & Co. KG has introduced a limited-edition MS 500i Centennial Edition chainsaw, featuring a distinctive black design. This model showcases the company's advanced electronic fuel injection technology, offering rapid acceleration (0-100 km/h in 0.25 seconds) and a high power-to-weight ratio, tailored for professional forestry applications globally.

- October 2025: Husqvarna AB has introduced five new chainsaws globally, featuring the 564 XP, the company's first fuel-injected 62.4cc professional model. This chainsaw is designed to provide 70cc-class power within a 50cc-sized chassis. The new lineup emphasizes improved maneuverability, reduced operator fatigue, and advanced technology tailored for forestry professionals.

- October 2025: ECHO has expanded its 56V battery-powered product range with new high-performance chainsaws that offer extended runtime. These include the DCS-3500T top-handle saw designed for professional use and updated, efficient models tailored for homeowners. The new tools are lighter, more durable, and engineered to enhance productivity and maneuverability during tree work.

- May 2025: Husqvarna AB has introduced the 564 XP, a 60cc professional chainsaw equipped with electronic fuel injection (EFI) in place of a traditional carburetor. It combines the compact, agile handling of a 50cc chainsaw with the power of a 70cc model (5.4 hp). The 564 XP delivers instant acceleration, optimized performance across varying altitudes and temperatures, and reduced emissions.

Global Chainsaw Market Report Scope

A chainsaw is a portable power tool featuring a rotating chain with sharp teeth, guided by a bar. It is primarily used in forestry and landscaping for tasks such as felling trees, removing branches, cutting logs, pruning, creating firebreaks for wildfire control, and preparing firewood.

The chainsaw market report is segmented by product type (gas-powered, electric-powered, and others), end-user (residential, industrial, and others), distribution channel (offline retail and online platforms), application (forestry and logging, and others), bar length (less than 14 inches, and others), and geography (North America, Europe, Asia-Pacific, and others). The market forecasts are provided in terms of value (USD).

| Gas-Powered |

| Electric-Powered |

| Battery-Powered |

| Pneumatic / Hydraulic |

| Residential |

| Commercial / Professional |

| Industrial (Forestry and Construction) |

| Offline Retail |

| Online Platforms |

| Forestry and Logging |

| Construction and Demolition |

| Landscaping and Arboriculture |

| Emergency and Disaster Relief |

| Less Than 14 inch |

| 16-18 inch |

| 20-24 inch |

| More Than 26 inch |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Type | Gas-Powered | |

| Electric-Powered | ||

| Battery-Powered | ||

| Pneumatic / Hydraulic | ||

| By End-User | Residential | |

| Commercial / Professional | ||

| Industrial (Forestry and Construction) | ||

| By Distribution Channel | Offline Retail | |

| Online Platforms | ||

| By Application | Forestry and Logging | |

| Construction and Demolition | ||

| Landscaping and Arboriculture | ||

| Emergency and Disaster Relief | ||

| By Bar Length | Less Than 14 inch | |

| 16-18 inch | ||

| 20-24 inch | ||

| More Than 26 inch | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the chainsaw market be by 2031?

The chainsaw market size is forecast to reach USD 5.99 billion by 2031, expanding at a 4.01% CAGR from 2026 to 2031.

Which product type leads current sales?

Gas-powered units held 54.3% of chainsaw market share in 2025, reflecting deep professional penetration and long runtime advantages.

What is the fastest growing product segment?

Battery-powered chainsaws are projected to grow at 4.7% CAGR to 2031, supported by zero-emission mandates and purchase incentives.

Which region is set for the highest growth?

Asia-Pacific is projected to record the fastest 5.0% CAGR through 2031, powered by Japanese subsidies and expanding urban landscaping demand.

Page last updated on: