Forestry Machinery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

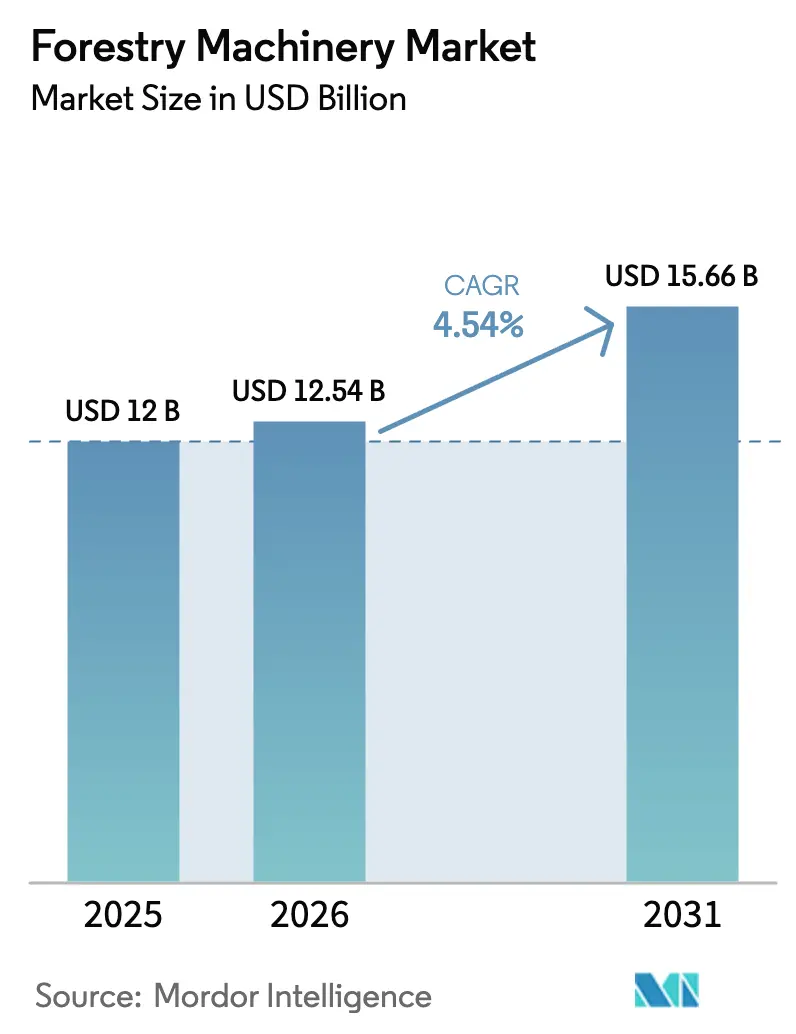

| Market Size (2026) | USD 12.54 Billion |

| Market Size (2031) | USD 15.66 Billion |

| Growth Rate (2026 - 2031) | 4.54% CAGR |

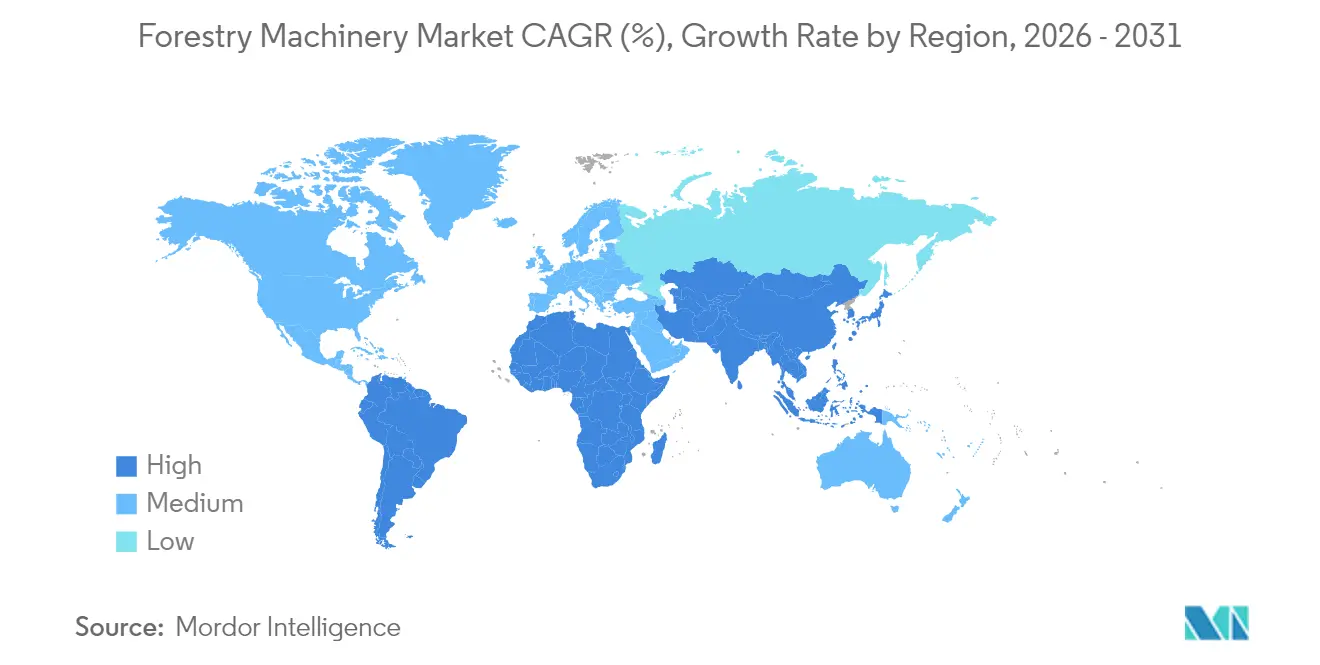

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Forestry Machinery Market Analysis by Mordor Intelligence

The forestry machinery market size in 2026 is estimated at USD 12.54 billion, growing from 2025 value of USD 12.0 billion with 2031 projections showing USD 15.66 billion, growing at 4.54% CAGR over 2026-2031. Market growth is driven by persistent labor shortages, which encourage the adoption of automation, stricter environmental regulations mandating low-emission equipment, and the necessity to replace aging machinery fleets in both developed and developing regions. The European Timber Trade Federation (ETTF) forecasts total European softwood consumption at 41 million cubic meters in 2024, with a 1.1% increase anticipated in 2025. This high production volume requires advanced forest machinery to meet the growing demand for wood products. North American and European operators are implementing integrated digital platforms to meet certification requirements and improve operational efficiency. In the Asia-Pacific and South America regions, producers are transitioning from manual logging to cut-to-length systems to meet export requirements for traceable chain-of-custody documentation. The market maintains competitive balance as forestry equipment producers focus on developing electric and autonomous solutions rather than engaging in price competition.

Key Report Takeaways

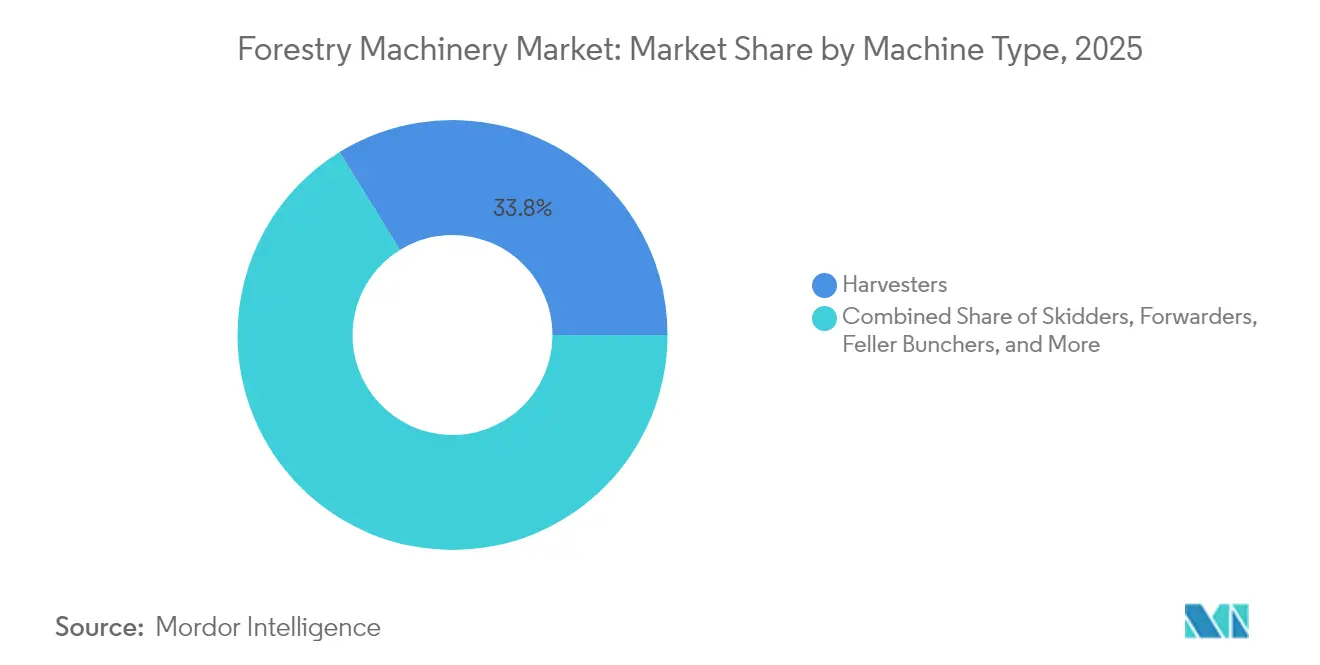

- By machine type, harvesters held 33.80% of the forestry machinery market share in 2025, while forwarders are projected to expand at a 7.65% CAGR through 2031.

- By power source, diesel systems accounted for 77.30% of the forestry machinery market size in 2025, and battery-electric solutions are forecast to grow at a 10.25% CAGR to 2031.

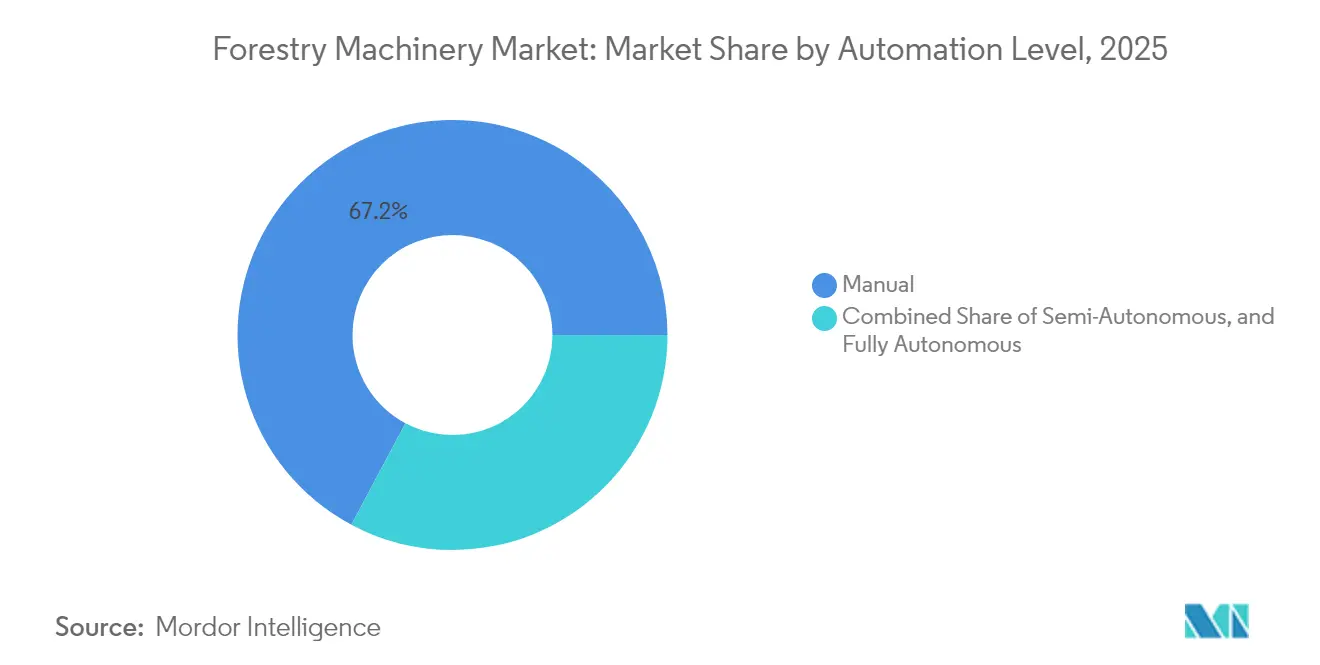

- By automation level, manual operations controlled a 67.20% share in 2025, whereas fully autonomous platforms are projected to rise at a 9.05% CAGR through 2031.

- By end user, contract logging firms captured a 41.10% share in 2025, while forest ownership groups are set to grow at a 9.75% CAGR between 2026 and 2031.

- By geography, North America commanded a 36.50% share in 2025, and Asia-Pacific is on track for a 7.05% CAGR through 2031.

- Market concentration is moderate, with the top five companies such as Deere & Company, Komatsu Ltd., Caterpillar Inc., Tigercat International Inc., and Ponsse Plc collectively holding majority of the market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Forestry Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in mechanized logging in emerging economies | +1.1% | Asia-Pacific, South America, and Africa | Medium term (2-4 years) |

| Rising global demand for certified timber products | +0.8% | Global, with emphasis on Europe and North America | Long term (≥ 4 years) |

| Government re-afforestation incentives and subsidies | +0.5% | North America, Europe, and China | Short term (≤ 2 years) |

| Electrification of off-highway machinery fleets | +1.0% | Europe, North America, and Scandinavia | Medium term (2-4 years) |

| Labor-shortage–led adoption of autonomous machineries | +0.6% | North America, Europe, and Australia | Short term (≤ 2 years) |

| Digital twin deployment for predictive maintenance | +0.4% | Global, led by developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Mechanized Logging in Emerging Economies

Mechanization rates in China increased as government mandates strengthened sustainable forest management requirements. Productivity gains in Brazilian eucalyptus plantations demonstrate measurable benefits - forwarder output reaches 60.97 m³ per effective work hour when individual tree volume exceeds 0.58 m³, compared to 42.06 m³ at lower volumes. Operational costs in developing regions have decreased, becoming lower than in several developed markets. Paraguay's plantation area quadrupled as investors targeted returns from mechanized eucalyptus stands. Equipment manufacturers developed lighter forwarders and oscillating bogies that reduce soil compaction for local terrain conditions, enabling emerging operators to achieve both productivity and environmental standards.

Rising Global Demand for Certified Timber Products

Forest Stewardship Council certification increased oak log prices by 19.28% and beech log prices by 12.30% in Turkey in 2023, demonstrating that certification premiums can offset investments in precision equipment. The European Deforestation Regulation, which takes effect in December 2024, requires exporters to provide geolocation and traceability data, necessitating the implementation of digital recorders and satellite systems[1]Source: Department of Agriculture, Fisheries and Forestry, “European Union Deforestation Regulation,” agriculture.gov.au. Certification requirements in Japan and Western Europe promote the use of selective cutting equipment and low-impact vehicles to maintain forest quality. Major buyers now incorporate audit systems that process data, making machine-generated logging records essential for market access.

Government Re-Afforestation Incentives and Subsidies

The United States Department of Agriculture's USD 80 million Wood Innovations Grants program for 2025 reduces the payback period for new harvesters to less than four years for eligible operators[2]Source: Council of Western State Foresters, “Policy Update July 2025,” westernforesters.org. North Carolina provides reimbursement to landowners for planting while permitting the use of federal Environmental Quality Incentive Program funds for precision thinning equipment. Federal tax deductions for reforestation expenses improve after-tax returns, encouraging family forest owners to purchase midsize forwarders rather than outsource timber transportation. Grant requirements typically include fuel consumption limits and digital reporting requirements, which encourage the adoption of hybrid drives and telematics systems.

Electrification of Off-Highway Machinery Fleets

Swedish Cellulose Corporation (SCA) deployed electric timber trucks, which covered 46,000 km in Sweden, resulting in a 55 metric tons reduction in CO₂ emissions annually. The company's second prototype, equipped with integrated cranes, aims to reduce emissions by 170 metric tons[3]Source: SCA, “Electric Timber Trucks,” sca.com. In May 2025, Volvo Construction Equipment introduced mid-size electric material handlers and an electric articulated hauler, advancing their battery technology beyond the testing phase. In 2024, Komatsu developed battery-electric drilling rigs, while Sennebogen implemented energy recovery systems. Manufacturers are focusing on modular battery packs and regenerative hydraulics to match diesel performance. Establishing charging infrastructure in remote locations remains a challenge. The inclusion of mobile charging trailers and depot micro-grids in tender specifications is contributing to increased adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront and lifecycle ownership costs | -1.1% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Volatility in soft-wood commodity prices | -0.7% | North America, Europe, and Russia | Medium term (2-4 years) |

| Shortage of skilled operators for advanced machines | -0.6% | Developed markets and rural regions | Long term (≥ 4 years) |

| Cyber-security gaps in telemetry-enabled equipment | -0.4% | Global, emphasis on connected fleets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront and Lifecycle Ownership Costs

Tracked harvesters in the southeastern United States range from USD 316,000 to USD 763,000. In Brazil, maintenance accounts for 33.5% of hourly operating costs for John Deere models with over 30,000 operating hours. Research from the Czech Republic indicates that personnel costs comprise 35-66% of forwarder operating expenses, making operator efficiency essential for return on investment. Machine size and brand influence value retention, with larger carriers maintaining higher resale values despite requiring greater initial capital. Financing packages combining telematics subscriptions and residual-value guarantees help manage costs, but small contractors continue to face limited credit availability.

Volatility in Soft-Wood Commodity Prices

Spruce prices increased due to export restrictions and supply chain disruptions, followed by a decline in lumber futures. Hardwood production faces potential supply constraints due to mill closures reducing capacity, which creates uncertainty in harvest agreements. Commercial companies plan their budgets, but regional factors such as wildfires and regulatory changes continue to affect demand patterns. These price fluctuations impact capital expenditure decisions, as operators remain cautious about long-term debt commitments during periods of volatile timber costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Demand Concentrates on Harvesters Yet Forwarders Accelerate

Harvesters generated 33.80% of the forestry machinery market share in 2025 as manufacturers embedded precision felling heads and real-time length-diameter optimization algorithms. The forwarder segment is projected to grow at a 7.65% CAGR through 2031, as plantation operators adopt integrated cut-to-length systems that minimize soil impact and reduce skidder usage. The technological advancement in the industry is exemplified by Deere's C7.1 twin turbo harvester engine, which delivers 30% higher swing torque while reducing maintenance time by 15%.

Feller bunchers maintain their market position in Southern pine operations due to specific tree characteristics and stand density requirements. Their market share may decline as harvesting heads develop enhanced multi-tree handling capabilities. Swing machines and loaders continue to serve specialized processing requirements at roadside locations, while mulchers maintain consistent demand from municipal wildfire prevention programs. Equipment manufacturers' order backlogs indicate increasing preference for versatile carriers that accommodate interchangeable harvesting, forwarding, and hoe-chucking attachments, helping operators manage market fluctuations effectively.

By Power Source: Battery-Electric Moves from Pilot to Procurement

Diesel engines maintain a 77.30% share in the forestry machinery market in 2025, primarily due to operational duty cycles exceeding current battery capabilities. Battery-electric solutions are growing at a 10.25% CAGR. The introduction of Volvo's EW240 Electric Material Handler demonstrates the viability of heavy battery-powered equipment, while mobile charging trailers become standard offerings in dealer catalogs. Hybrid systems function as transitional technology, with Sennebogen's Green Hybrid energy recovery system reducing fuel consumption by up to 30% in crane operations.

Financial institutions now incorporate carbon credit revenue streams in their equipment financing programs for low-emission machines. This shift has led to powertrain selection decisions based on total environmental ownership costs rather than initial purchase price. In Scandinavia, public land contract bids award additional points for zero-emission harvesters, indicating regulatory influences that may accelerate the transition away from diesel faster than economic factors alone would predict.

By Automation Level: Assisted Functions Evolve into Full Autonomy

Manual operations account for 67.20% of the forestry machinery market size in 2025, while fully autonomous systems are growing at a 9.05% CAGR due to advances in deep learning technology. Deere's Intelligent Boom Control reduces tree processing cycle times significantly while maintaining operator supervision. Ponsse's Thinning Density Assistant combines Global Navigation Satellite System (GNSS) waypoints and optical sensors to monitor and document residual stand conditions, integrating compliance requirements with operational efficiency.

Labor shortages and insurance cost reductions are driving automation adoption. Insurance providers in the Pacific Northwest offer reduced premiums for machines equipped with remote operation capabilities. Equipment suppliers now offer autonomy features through tiered software subscriptions, creating recurring revenue streams while reducing initial investment costs for smaller operations.

By End User: Ownership Patterns Shift Toward Forest Owners

Contract logging firms held 41.10% of the forest machinery market share in 2025, while forest ownership groups recorded a 9.75% CAGR as they integrated harvesting operations to maintain certified supply chains. Large timberland investment management organizations prefer to own machines directly to collect data for carbon credit verification models. Sawmills and pulp companies maintain limited fleets primarily for in-yard handling operations rather than forest harvesting.

Equipment owners without in-house maintenance capabilities prioritize extended warranty coverage and uptime guarantees. Original equipment manufacturers (OEMs) respond by offering 36-month preventive maintenance packages and predictive analytics dashboards, targeting owner-operators who prioritize operational transparency over hourly contract rates.

Geography Analysis

North America holds a 36.50% share in the forestry machinery market in 2025 due to established mechanized practices and autonomous harvester trials addressing labor shortages. The region benefits from USD 80 million in federal grants for 2025 and tax incentives that reduce payback periods for electrified carriers. Canada's fivefold increase in temporary foreign workers indicates persistent labor constraints, supporting automated equipment adoption. Dealers manage inventory against Deere's projected decline for 2025, and demand for telematics module retrofits remains strong as operators focus on equipment uptime.

Asia-Pacific shows the highest growth rate at 7.05% CAGR, with China's commercial harvest mechanization exceeding 60%. Komatsu anticipates continued market expansion based on wood demand, labor constraints, and enhanced safety requirements. Japanese certification premiums currently limit harvester upgrades, and domestic manufacturers identify export opportunities in the Asia Pacific's expanding plantation sector.

Europe maintains robust replacement cycles driven by certification requirements. The European Union Deforestation Regulation, effective December 2024, mandates GPS-accurate harvest data, increasing demand for modern cabs with StanForD-compatible logging systems. Sweden and Finland are pioneers in electric truck implementations, with SCA's timber haulers reducing their annual emissions by 55 metric tons. Ponsse reported EUR 336.0 million (USD 393.4 million) in order intake from Nordic countries during the first half of 2024, demonstrating stable replacement demand despite weakness in the construction sector.

South America optimizes operations through uniform eucalyptus plantations supporting high-capacity, automated fleets. Brazil sets productivity standards for cost efficiency, while Paraguay's expanding cultivation area creates opportunities for Original Equipment Manufacturers (OEM) financing services. The Middle East and Africa markets remain early-stage, with reforestation programs supported by donor funding creating specific opportunities for light skidders and multipurpose loaders.

Competitive Landscape

The market demonstrates moderate concentration, with the top 5 players holding a majority share in the forestry machinery market in 2024. These key players include Deere & Company, Komatsu Ltd., Caterpillar Inc., Tigercat International Inc., and Ponsse Plc. Deere & Company maintains market leadership through its agricultural machinery expertise and extensive North American dealer network. Komatsu Ltd. and Caterpillar Inc. leverage their forestry equipment capabilities and global manufacturing presence. Tigercat International Inc. and Ponsse Plc compete through specialized forestry equipment manufacturing, focusing on technological innovation and application-specific solutions.

The industry is experiencing significant changes through electric and autonomous systems. In 2024, Hitachi Construction Machinery's partnership with Dimaag for 1.7-metric tons zero-emission excavators demonstrates the industry's shift toward electrification. In 2025, Volvo CE partnered with Unicontrol to integrate 3D machine control technology, showcasing the trend of equipment manufacturers collaborating with software providers.

Umea University's development of a 16-metric-tons autonomous machine control system using deep reinforcement learning indicates potential disruption from non-traditional market entrants. Companies, including Komatsu, are investing in Smart Forestry digital platforms, incorporating predictive maintenance, precision harvesting, and integrated fleet management systems to enhance operational efficiency and equipment utilization.

Forestry Machinery Industry Leaders

Deere & Company

Komatsu Ltd.

Caterpillar Inc.

Tigercat International Inc.

Ponsse Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: John Deere introduced its H Series large wheeled machines, which include the 1270H and 1470H Harvesters and 2010H and 2510H Forwarders. These machines feature improved hydraulic systems, automated functions, and enhanced operator ergonomics. The H Series combines high performance with fuel efficiency to improve logging operations.

- April 2025: Volvo introduced the world’s first electric articulated haulers, further expanding zero-emission options for log haul roads. These vehicles are designed to minimize environmental impact while maintaining efficiency and performance, providing a sustainable solution for industries that rely heavily on heavy-duty transportation.

- February 2025: Caterpillar Inc. introduced the FM528 General Forestry/Log Loader, a machine engineered for forestry and mill-yard operations. The model delivers efficiency and durability while providing operator comfort in demanding work environments.

- February 2025: Kubota Corporation expanded its forestry equipment portfolio with three new machines such as the U17-5 and KX040-5 excavators, and the SVL97-3 compact track loader. These machines offer enhanced performance, operator comfort, and reliability for forestry operations.

Global Forestry Machinery Market Report Scope

Forestry machinery is a machine and power-driven equipment that aids in excavating, harvesting, and finishing a wooded area. The forestry machinery market is segmented by machinery into skidders, forwarders, swing machines, bunchers, harvesters, loaders, and other forestry machinery. By geography, it is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The report offers market sizing and forecasts in value (USD) for all the above segments.

| Skidders |

| Forwarders |

| Feller Bunchers |

| Harvesters |

| Swing Machines |

| Loaders |

| Other Machine Type |

| Diesel |

| Hybrid |

| Battery-Electric |

| Manual |

| Semi-Autonomous |

| Fully Autonomous |

| Contract Logging Firms |

| Forest Ownership Groups |

| Pulp and Paper Companies |

| Sawmills |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| Sweden | |

| Finland | |

| United Kingdom | |

| France | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Machine Type | Skidders | |

| Forwarders | ||

| Feller Bunchers | ||

| Harvesters | ||

| Swing Machines | ||

| Loaders | ||

| Other Machine Type | ||

| By Power Source | Diesel | |

| Hybrid | ||

| Battery-Electric | ||

| By Automation Level | Manual | |

| Semi-Autonomous | ||

| Fully Autonomous | ||

| By End User | Contract Logging Firms | |

| Forest Ownership Groups | ||

| Pulp and Paper Companies | ||

| Sawmills | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| Sweden | ||

| Finland | ||

| United Kingdom | ||

| France | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the forestry machinery market in 2026 and how fast is it growing?

The forestry machinery market size is USD 12.54 billion in 2026 and is projected to grow at a 4.54% CAGR to reach USD 15.66 billion by 2031.

Which machine category leads revenue today?

Harvesters account for 33.80% of the projected 2025 revenue, driven by the extensive adoption of cut-to-length methods in mechanized logging operations.

What power source is gaining traction fastest?

Battery-electric platforms are advancing at an 10.25% CAGR as fleets seek lower emissions and stable fuel costs.

Which region offers the strongest growth outlook to 2031?

Asia-Pacific is projected to post a 7.05% CAGR, driven by rapid mechanization in China and expanding plantations across the region.

How significant is autonomy in upcoming purchasing decisions?

Fully autonomous systems show the highest segment CAGR at 9.05% because operators need solutions that relieve labor shortages and enhance safety.

Who are the top industry players by revenue?

Deere & Company, Komatsu Ltd., Caterpillar Inc., Tigercat International Inc., and Ponsse Plc together hold majority of global revenue, reflecting a moderately concentrated supplier landscape.

Page last updated on: