Veterinary Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

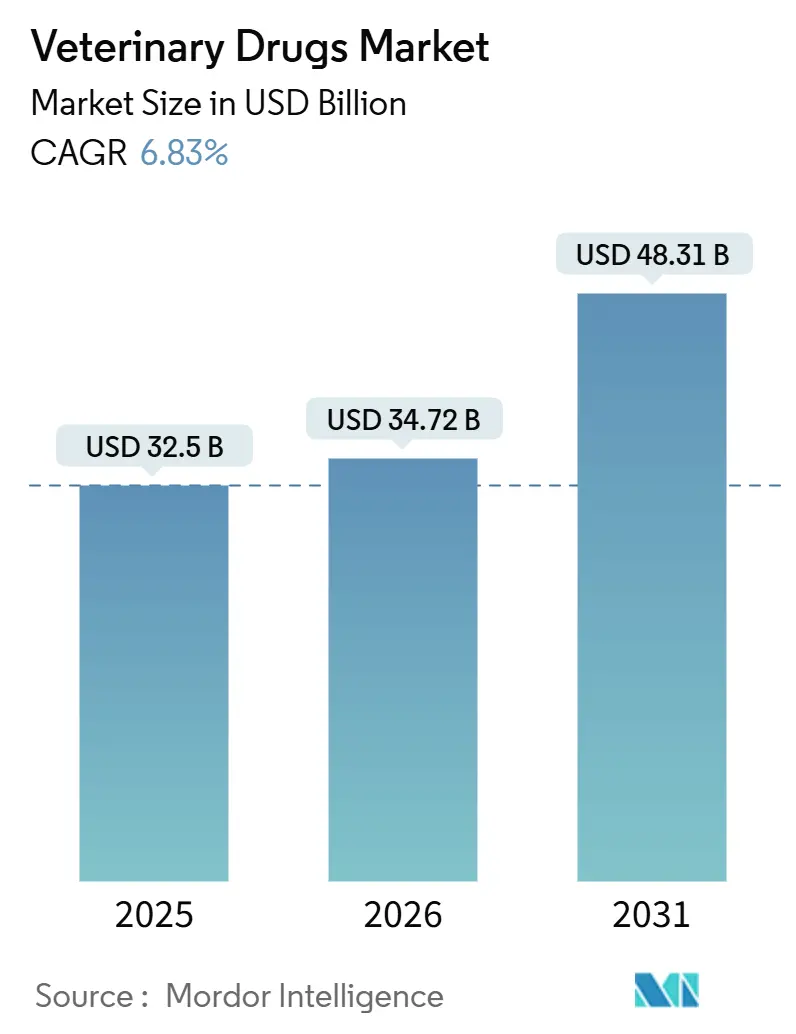

| Market Size (2026) | USD 34.72 Billion |

| Market Size (2031) | USD 48.31 Billion |

| Growth Rate (2026 - 2031) | 6.83% CAGR |

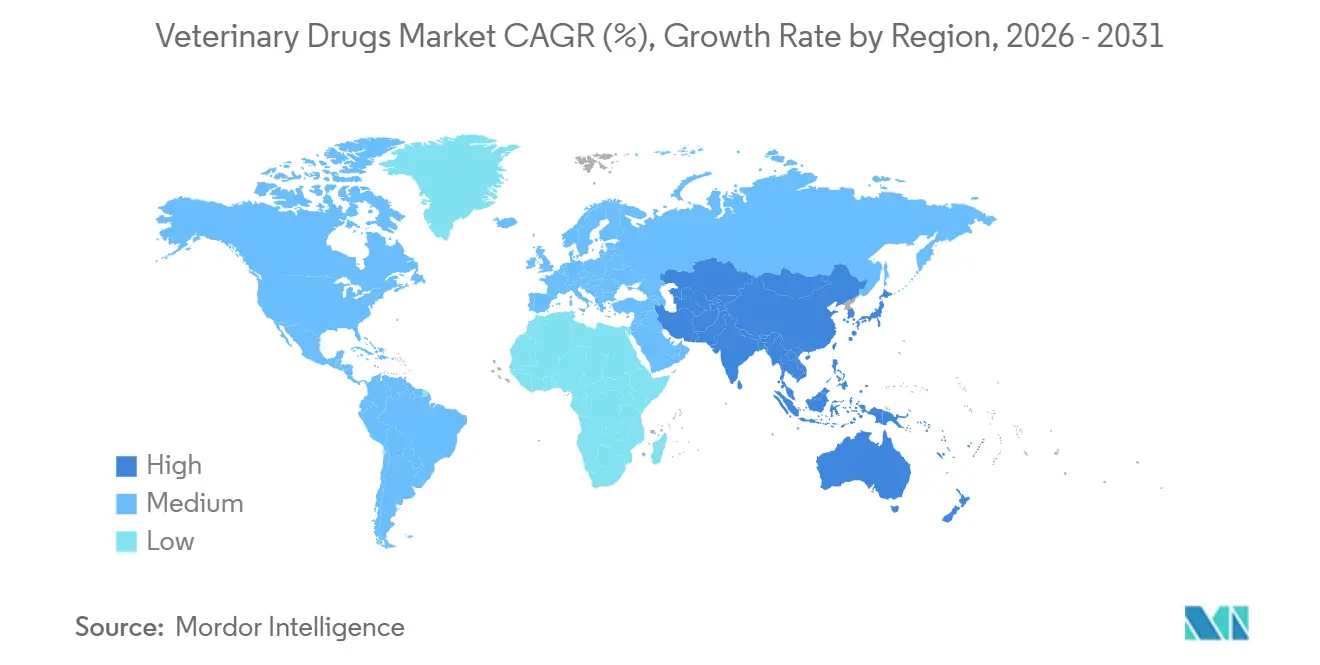

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Drugs Market Analysis by Mordor Intelligence

The veterinary drugs market size was valued at USD 32.5 billion in 2025 and estimated to grow from USD 34.72 billion in 2026 to reach USD 48.31 billion by 2031, at a CAGR of 6.83% during the forecast period (2026-2031). Sustained disease outbreaks in both food-animal and pet populations are lifting demand for rapid-response vaccines and specialty therapeutics, while regulatory agencies approved 24 new animal drugs in 2024, including several mRNA platforms that shorten development timelines[1]FDA Center for Veterinary Medicine, “Approved Animal Drugs 2024,” fda.gov . Heightened surveillance by the World Organisation for Animal Health logged a 12% rise in global disease notifications in 2024, steering procurement budgets toward preventive biologics and broad-spectrum anti-infectives. Producers are also adopting long-acting injectables that cut labor costs on large feedlots and dairies, helping parenteral products gain traction despite oral formulations retaining a majority share. Meanwhile, climate-linked parasite expansion is inflating R&D budgets for next-generation parasiticides, encouraging manufacturers to collaborate with academic consortia on novel modes of action.

Key Report Takeaways

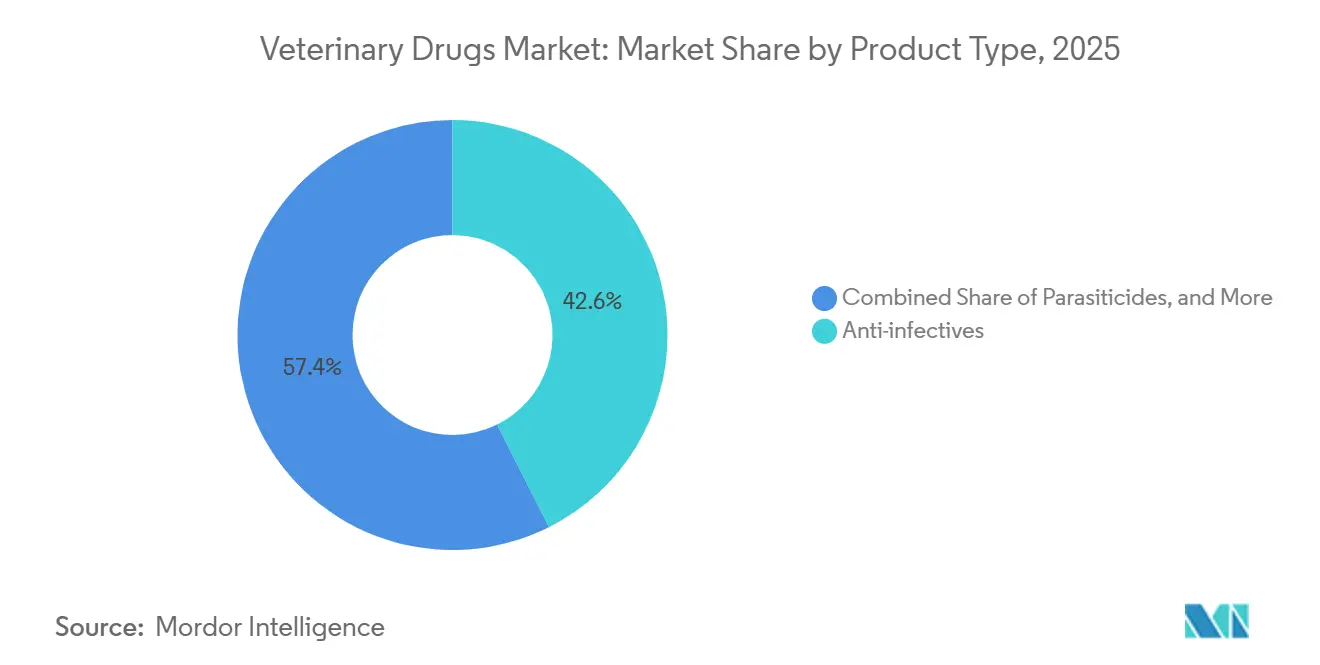

- By product type, anti-infectives captured 42.55% of the veterinary drugs market share in 2025, whereas vaccines are projected to expand at an 8.25% CAGR through 2031.

- By route of administration, oral formulations led with a 53.53% revenue share in 2025, while parenteral delivery is forecast to advance at a 7.75% CAGR between 2026 and 2031.

- By animal type, livestock accounted for 62.15% of 2025 revenue, but companion-animal therapeutics are on track to grow at a 7.82% CAGR to 2031.

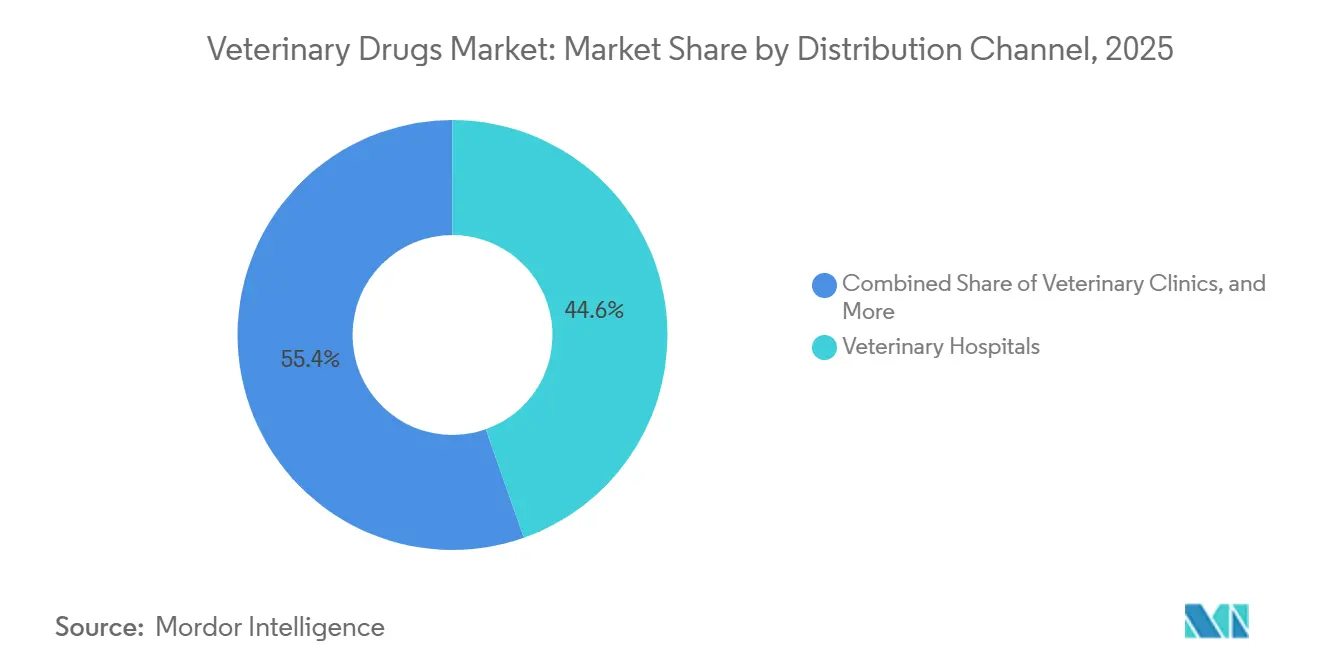

- By distribution channel, veterinary hospitals dominated with a 44.65% share in 2025, whereas online retail is expected to post an 8.32% CAGR over the same horizon.

- By geography, North America accounted for 38.55% of global sales in 2025, yet Asia-Pacific is poised to deliver a 7.22% CAGR through 2031 as livestock intensification accelerates in China, India, and Southeast Asia.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Veterinary Drugs Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in Prevalence of Infectious Diseases in Pets & Livestock | +1.4% | Global, with acute pressure in APAC and Sub-Saharan Africa | Short term (≤ 2 years) |

| Growing Demand for Animal-Sourced Protein | +1.2% | APAC core, spill-over to MEA and South America | Medium term (2-4 years) |

| Advances in Biologics & Novel Drug Delivery Platforms | +1.0% | North America & EU, early adoption in urban APAC markets | Medium term (2-4 years) |

| Pet-Humanization Boosting Preventive Care Spend | +0.9% | North America, EU, and affluent APAC urban centers | Long term (≥ 4 years) |

| Long-Acting Injectable & Precision-Dosing Technologies | +0.7% | Global, with fastest uptake in North America and EU livestock operations | Medium term (2-4 years) |

| AI-Driven Disease Surveillance Accelerating Demand Spikes | +0.5% | North America and EU, pilot deployments in China and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Prevalence of Infectious Diseases in Pets & Livestock

Soaring case counts of African swine fever, highly pathogenic avian influenza, and lumpy skin disease are reshuffling procurement priorities for the veterinary drugs market[2]World Organisation for Animal Health, “Disease Events Dashboard 2024,” woah.org. Emergency culls of 18 million U.S. poultry during 1H 2025 created a scramble for autogenous vaccines that match regional viral strains. Canine parvovirus variants that slip past legacy epitopes now oblige polyvalent boosters, which favors firms able to keep broad strain libraries. Rapid tech-transfer capability from research to fermentation gives suppliers an edge when regulators fast-track conditional licenses. Together, more frequent outbreaks and compressed response windows amplify product pull-through for broad-spectrum anti-infectives and customized biologics across the global veterinary drugs market.

Growing Demand for Animal-Sourced Protein

Projected meat output of 366 million t by 2030 is tightening the linkage between herd health and national food security[3]Food and Agriculture Organization, “World Livestock 2030 Projections,” fao.org . China’s pig herd recovery to 440 million head in 2024 reignited demand for vaccines, growth promoters, and prescription antibiotics under veterinary oversight, sustaining baseline volumes for the veterinary drugs market. India’s push to reach 300 million t of milk by 2028 widens the addressable market for mastitis therapies and reproductive hormones. Aquaculture hotspots in Vietnam and Indonesia now rely on medicated feeds to curb gill disease, illustrating how aquatic species are becoming a material revenue stream. Rising protein consumption, therefore, guarantees steady unit volumes even as stewardship rules restrain per-animal antibiotic intensity.

Advances in Biologics & Novel Drug-Delivery Platforms

Monoclonal antibodies for canine dermatology and osteoarthritis generated USD 420 million in 2024 revenue, validating premium pricing in the veterinary drugs market. FDA guidance on cell and gene therapies opened a route for autologous stem-cell treatments in equine injuries, expanding indications that previously lacked pharmacologic options. Recombinant cytokines under late-stage trials aim to treat bovine respiratory disease without prophylactic antibiotics, aligning with residue-reduction policy goals. Long-acting injectables that use poly(lactic-co-glycolic acid) microspheres extend dosing from weekly to quarterly, cutting labor hours on large dairies. Collectively, platform biologics and sustained-release carriers enhance therapeutic precision and diversify revenue away from commoditized small-molecule categories.

Pet-Humanization Boosting Preventive-Care Spend

Seventy-two percent of U.S. dog owners purchased at least one elective preventive-care service in 2024, a trend that supports the adoption of premium formularies in the veterinary drugs market. Companion-animal insurance policies climbed to 4.8 million by mid-2025, cushioning out-of-pocket shocks and normalizing high-value prescriptions. Tele-consultations surpassed 9.2 million in 2024, channeling electronic scripts directly to online pharmacies that can stock niche biologics without shelf-life risk. Portable PCR and immunoassay devices now deliver in-clinic results in minutes, accelerating evidence-based prescribing and boosting compliance. These behavioral shifts keep discretionary therapeutics on a growth path, even as macroeconomic cycles pressure household incomes.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened Antimicrobial-Residue Regulations Raising Costs | -0.7% | Global, with strictest enforcement in EU and North America | Short term (≤ 2 years) |

| Climate-Driven Parasite Resistance Escalating R&D Burden | -0.5% | Global, most acute in tropical and subtropical zones | Long term (≥ 4 years) |

| Global Shortage of Veterinarians | -0.4% | North America, EU, and rural areas across all regions | Medium term (2-4 years) |

| Proliferation of Counterfeit Medicines | -0.3% | APAC, MEA, and South America markets with weak enforcement | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heightened Antimicrobial-Residue Regulations Raising Costs

EU sales of veterinary antimicrobials fell 23% between 2021 and 2024 after prophylactic bans and e-prescription mandates, directly trimming volume growth for traditional anti-infectives[4]European Medicines Agency, “Sales of Veterinary Antimicrobial Agents 2024,” ema.europa.eu. FDA Guidance #263 removed over-the-counter channels in 2024, forcing livestock operators to absorb additional veterinary consultation and record-keeping expenses. Compliance adds USD 12–18 per head in beef feedlots, squeezing margins in commodity chains where antibiotic-free premiums remain volatile. Drug makers must now fund residual trials and global surveillance programs, which are extending regulatory timelines. As margins thin, capital shifts toward alternatives like bacteriophages and immune-priming vaccines, slowing reinvestment in new small-molecule classes.

Climate-Driven Parasite Resistance Escalating R&D Burden

Ivermectin-resistant nematodes now prevail in 68% of sampled sheep flocks across Australia, New Zealand, and South Africa, proving that chemical rotation alone cannot halt resistance. Tick vectors, such as the Lone Star tick, are forecast to establish year-round populations in 14 additional states by 2030, raising the cost of year-round parasiticide regimens. Developing novel modes of action costs above USD 100 million per compound and can span a decade, straining R&D budgets. As efficacy windows shorten, producers must layer management tactics, such as rotational grazing, strategic deworming, and targeted selective treatment, to dampen immediate drug volumes. Elevated development risk therefore drags on the long-run growth profile of the global veterinary drugs market.

Segment Analysis

By Product Type: Prevention Accelerates Revenue Diversification

Vaccines are on track to expand at an 8.25% CAGR, outpacing every other therapeutic class and reshaping demand patterns inside the veterinary drugs market. Anti-infectives still held 42.55% of 2025 revenue, the highest single-category veterinary drugs market share, but growth now levels off as stewardship policies restrict prophylactic use. Parasiticides remain indispensable for both livestock and pets, yet mounting resistance obliges more frequent product rotation, which lifts unit volume but compresses margins. Anti-inflammatory drugs support surgical and chronic pain protocols, while reproductive hormones boost conception rates in beef and dairy herds, anchoring ancillary demand. Nutritional supplements and anesthetics create smaller but recurring revenue streams that support the clinic workflow.

Advances in platform biologics are repositioning vaccines beyond core viral targets into chronic disease management, as evidenced by a monoclonal antibody for canine dermatitis that generated USD 420 million in 2024 sales. Combination products such as antibiotic-NSAID injectables bundle convenience for veterinarians who face dosing-compliance constraints on large farms. As first-in-class molecules mature, biosimilar entrants are expected to temper pricing power after 2028, especially in the Asia-Pacific generics corridor. Overall, diversification toward prevention secures longer product life cycles and stabilizes the veterinary drugs market against antimicrobial-policy shocks.

Note: Segment shares of all individual segments available upon report purchase

By Route of Administration: Long-Acting Injectables Gain Momentum

Oral products captured 53.53% of 2025 revenue, the highest contribution to the veterinary drugs market size for any delivery format, by leveraging ease of mass medication in feed or treats. Tablets, chews, and soluble premixes set the convenience benchmark, yet palatability issues and variable gut absorption cap bioavailability in some molecules. Parenteral formulations are advancing at a 7.75% CAGR as long-acting microsphere-based injectables push dosing intervals from weekly to quarterly, cutting labor costs on intensive livestock systems. Topical spot-ons dominate ectoparasite control for cats and dogs, supplying targeted dermal delivery with low systemic exposure.

Pour-on insecticides remain popular in extensive grazing regions but are now subject to environmental reviews related to runoff in the EU. Intramammary tubes for bovine mastitis and intravaginal hormone devices fill niche but play essential roles in dairy management. An emerging micro-needle patch for small-ruminant vaccines passed Phase II trials in 2025, hinting at future label expansion that will clip market share from conventional syringes. Route innovation, therefore, acts as a latent growth lever that multiplies existing molecule value across the veterinary drugs market.

By Animal Type: Pets Outpace Food-Animal Growth

Livestock still supplied 62.15% of global revenue in 2025, but companion-animal categories are forecast to register a 7.82% CAGR through 2031, surpassing the overall veterinary drugs market trajectory. Dogs account for the largest pet sub-segment, with chronic diseases such as diabetes and osteoarthritis driving repeat scripts for insulin and anti-NGF monoclonal antibodies. Feline pharmacology advances more slowly because limited glucuronidation limits safe drug options, though targeted biotherapeutics are now entering late-stage trials.

Equine owners justify premium therapies—joint biologics and gastric ulcer drugs due to high individual animal value, but total volume remains niche. Aquaculture, the fastest-rising livestock niche, increases demand for water-soluble antibiotics and vaccines that minimize handling stress in high-density net pens. Minor-species (rabbits, ferrets, exotic birds) rely heavily on extra-label use, yet the FDA’s minor-use pathway introduced in 2024 could unlock tailored approvals by 2027. Species diversification, therefore, balances cyclical swings and widens the installed customer base within the veterinary drugs market.

By Distribution Channel: Digital Dispensing Rewrites Access

Veterinary hospitals retained 44.65% of 2025 revenue, anchoring the prescription-generation node for controlled injectables and specialty biologics. Yet online pharmacies are expanding at a 8.32% CAGR as owners embrace auto-ship subscriptions that improve refill compliance and transparency of prices. Independent clinics feel dual pressure: they must honor prescription-transfer rules issued in 2024 while competing against e-commerce on dispensing margins.

Farm-supply stores still dominate over-the-counter dewormers and vaccines for backyard flocks, but larger producers increasingly negotiate direct-volume contracts with manufacturers to secure supply. Tele-consult platforms now integrate e-prescribe APIs, enabling just-in-time fulfillment from centralized warehouses that carry deep SKU breadth without shelf-life risk. Geographic dispersion favors omnichannel hybrids, in which clinics partner with e-commerce portals to share fulfillment fees. Distribution flexibility, therefore, remains pivotal to winning incremental wallet share in the veterinary drugs market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America accounted for 38.55% of global revenue in 2025, with robust pet insurance adoption and intensive feedlot systems driving steady biologics uptake. The United States spearheads innovation, averaging 24 FDA veterinary drug approvals per year since 2024, which sustains premium pricing for early-cycle products. Canada benefits from regulatory harmonization and proximity to U.S. manufacturers, whereas Mexico’s generics expansion preserves regional cost competitiveness.

Asia-Pacific is projected to clock a 7.22% CAGR, surpassing the global veterinary drugs market size growth rate, fueled by China’s aggressive livestock vaccination drives and India’s formalization of veterinary pharmaceutical manufacturing. Japan commands high per-pet spending and pet insurance penetration above 15%, stabilizing premium-therapy sales. Australia’s stringent residue controls underpin demand for on-label antibiotics and vaccine programs aligned with export certification schemes.

Europe maintains a mature regulatory framework that enables centralized product launches, yet national reimbursement differences fragment uptake. Germany and the United Kingdom anchor EU sales, while Spain’s large swine sector consumes disproportionate volumes of respiratory-disease vaccines. The Middle East and Africa remain under-penetrated because of counterfeit risk and limited cold chain, although Gulf countries invest in modern dairy and poultry complexes that specify vetted suppliers. South America’s export-oriented beef and poultry chains depend on traceability-compliant therapeutics, with Brazil shipping 2.1 million t of beef in 2024 under strict residue surveillance.

Competitive Landscape

The global veterinary drugs market features a moderately concentrated competitive structure, where the five largest manufacturers hold a majority share while still competing with hundreds of regional formulators serving price-sensitive niches. Multinational leaders Zoetis, Elanco, Boehringer Ingelheim, Merck Animal Health, and Ceva Santé Animale anchor their advantage in integrated discovery pipelines, multi-species portfolios, and worldwide distribution footprints that shorten launch curves. Second-tier companies, including Vetoquinol and Virbac, focus on dermatology, parasitology, and companion-animal nutrition to secure differentiated channels that escape direct price competition with broad-spectrum anti-infectives. The rise of biosimilars is already compressing margins for first-generation monoclonal antibodies in Europe, where patent cliffs start in 2028, and local manufacturers can file abbreviated dossiers under the EMA’s streamlined biologics path.

Strategic innovation now gravitates toward biologics and precision-dosing technologies that reduce total antimicrobial use without sacrificing productivity. In 2024, Zoetis unveiled a single-shot, mRNA-based swine vaccine that can be re-sequenced within eight weeks when field strains shift, demonstrating platform agility that small manufacturers struggle to replicate. Elanco allocated 38% of its USD 680 million R&D budget to next-generation biologics, including recombinant cytokines for bovine respiratory disease and a Phase III monoclonal antibody for canine osteoarthritis that targets nerve growth factor pathways. Boehringer Ingelheim continues to extend its long-acting cattle parasiticide line by combining macrocyclic lactone bases with proprietary microsphere carriers that stretch efficacy to 120 days, trimming labor inputs on large feedlots.

Mergers, licensing agreements, and venture investments illustrate rising capital intensity. Ceva’s 2025 acquisition of the Swedish biotech SVAx, which owns a bacteriophage library for salmonella control in poultry, positions the firm to capitalize on antibiotic-reduction mandates in the EU and North America. Merck Animal Health’s minority stake in Aquabyte, an AI-based fish-health monitoring platform, integrates real-time biometric feeds with prescription triggers, inching the market toward outcome-based contracting models. Meanwhile, Asian generic makers in India and China are scaling U.S. FDA-approved facilities that churn out florfenicol and tylosin at cost points 15-20% below Western averages, intensifying price erosion in commodity molecules. Across all tiers, supply-chain authenticity remains a reputational differentiator, and firms invest heavily in serialization and blockchain pilots that certify origin and cold-chain integrity for high-value biologics.

Veterinary Drugs Industry Leaders

Merck Animal Health

Ceva Santé Animale

Zoetis Inc.

Elanco Animal Health

Boehringer Ingelheim International GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Veterinarians now have a new FDA-approved generic dewormer, Defendazole, for the treatment and control of multiple worm species in cattle and goats; the over-the-counter oral suspension, sponsored by Norbrook Laboratories, is available in 1-L and 5-L bottles.

- January 2026: The FDA approved nixiFLOR, the first generic florfenicol-flunixin injectable, for bovine respiratory disease treatment and fever control in beef and non-lactating dairy cattle.

Global Veterinary Drugs Market Report Scope

As per the scope of the report, veterinary drugs are used to treat numerous diseases in animals. Veterinary drugs such as antibiotics, antimicrobials, antihistamines, antiprotozoals, and hormones are developed to minimize the impact of harmful viruses and bacterial parasites on animals.

The veterinary drugs market is segmented by product type, route of administration, animal type, distribution channel, and geography. By product type, the market is segmented into anti-infectives, anti-inflammatories, parasiticides, vaccines, hormones, and others. By route of administration, the market is segmented into oral, parenteral, topical, and others. By animal type, the market is segmented into livestock (cattle, poultry, swine, sheep & goats) and companion animals (dogs, cats, horses, and other pets). By distribution channel, the market is segmented into veterinary hospitals, veterinary clinics, and pharmacies. online retail, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Anti-infectives |

| Parasiticides |

| Vaccines |

| Anti-inflammatory |

| Hormones |

| Other Product Types |

| Oral |

| Parenteral |

| Topical |

| Other Route of Administration |

| Livestock | Cattle |

| Poultry | |

| Swine | |

| Sheep & Goats | |

| Aquaculture | |

| Companion Animals | Dogs |

| Cats | |

| Horses | |

| Other Pets |

| Veterinary Hospitals |

| Veterinary Clinics |

| Pharmacies |

| Online Retail |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Anti-infectives | |

| Parasiticides | ||

| Vaccines | ||

| Anti-inflammatory | ||

| Hormones | ||

| Other Product Types | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Topical | ||

| Other Route of Administration | ||

| By Animal Type | Livestock | Cattle |

| Poultry | ||

| Swine | ||

| Sheep & Goats | ||

| Aquaculture | ||

| Companion Animals | Dogs | |

| Cats | ||

| Horses | ||

| Other Pets | ||

| By Distribution Channel | Veterinary Hospitals | |

| Veterinary Clinics | ||

| Pharmacies | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of global veterinary drug sales by 2031?

The market is forecast to reach USD 48.31 billion by 2031.

Which therapeutic class is growing fastest?

Vaccines are advancing at an 8.25% CAGR, outpacing all other categories.

Why are long-acting injectables attracting interest?

They cut labor costs by stretching dosing intervals from weekly to quarterly while maintaining therapeutic coverage.

Which region is expected to log the highest growth rate?

Asia-Pacific is poised for a 7.22% CAGR through 2031, propelled by livestock intensification and rising pet ownership.

How are residue regulations influencing product strategy?

Stewardship rules reduce prophylactic antibiotic volumes, pushing R&D investment toward biologics, bacteriophages, and immunomodulators.

What share do online pharmacies currently command?

Although veterinary hospitals remain dominant, online retail channels are expanding at an 8.32% CAGR and rapidly gaining share.