Veterinary Antimicrobial Susceptibility Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

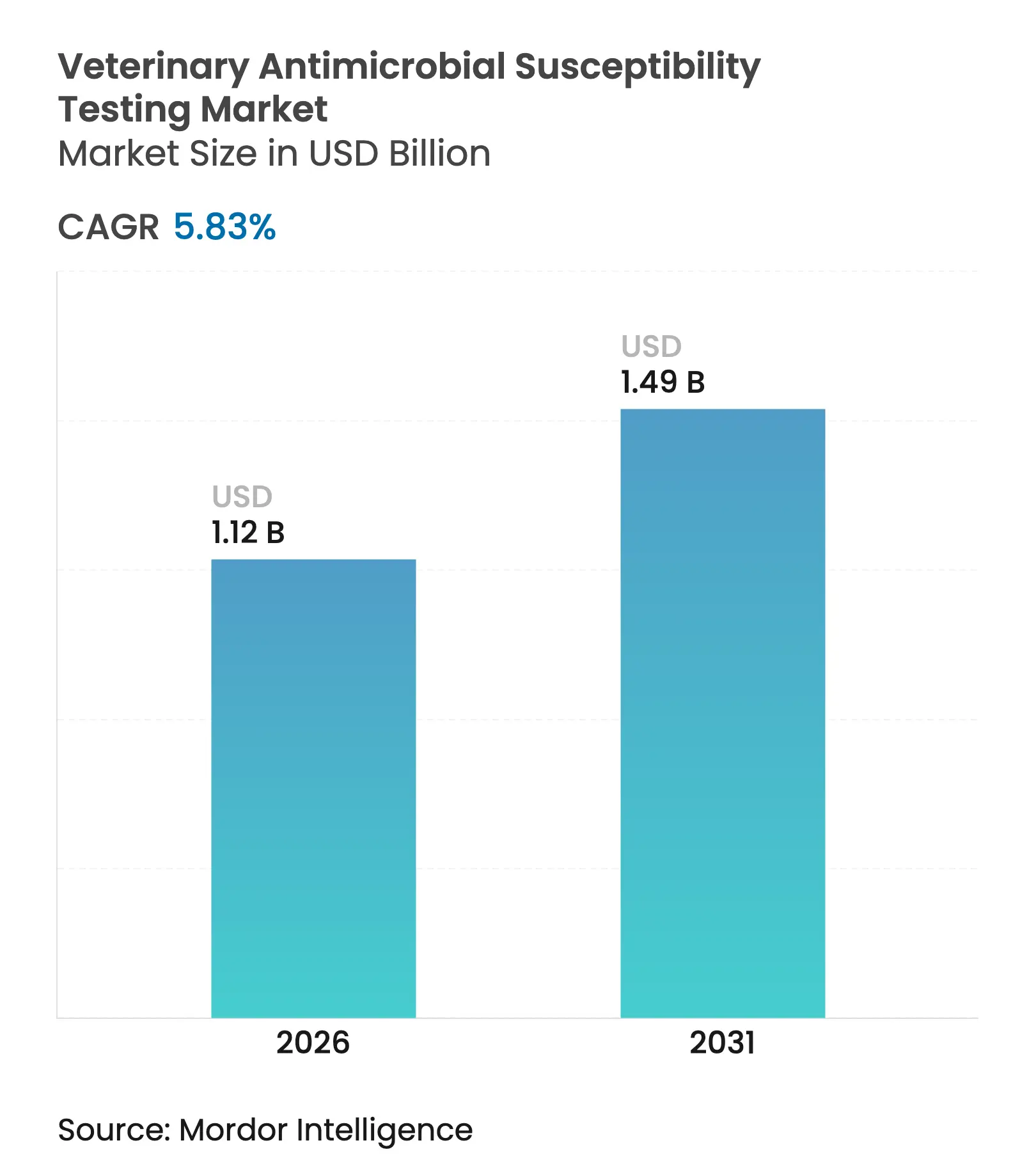

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 1.49 Billion |

| Growth Rate (2026 - 2031) | 5.83 % CAGR |

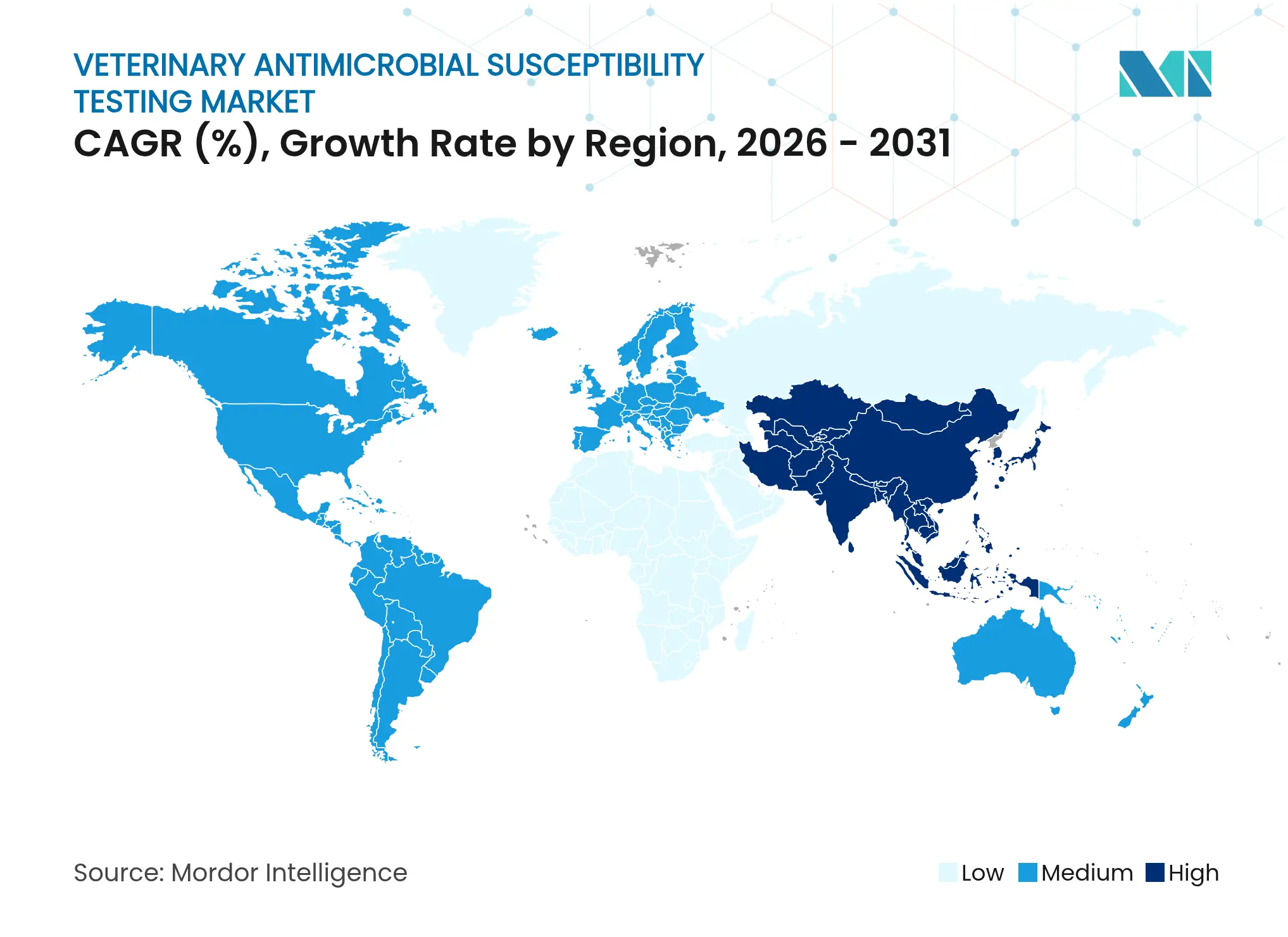

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Veterinary Antimicrobial Susceptibility Testing Market Analysis by Mordor Intelligence

Veterinary Antimicrobial Susceptibility Testing Market size market size in 2026 is estimated at USD 1.12 billion, growing from 2025 value of USD 1.06 billion with 2031 projections showing USD 1.49 billion, growing at 5.83% CAGR over 2026-2031. Heightened global concern over antimicrobial resistance, regulatory mandates that tie antibiotic use to confirmed sensitivity data, and the fast-growing preference for automated laboratory workflows are expanding routine testing volumes. The livestock segment dominates current demand because intensive farming amplifies infection risk, while the companion-animal segment advances more quickly as owners spend more on preventive diagnostics. Automated systems that combine artificial intelligence with micro-dilution or disk diffusion protocols offer laboratories shorter turn-around times and standardized quality control, helping them win price-sensitive clients in both developed and emerging economies. Meanwhile, rapidly expanding AMR surveillance networks in Asia-Pacific and Latin America underpin longer-term demand by making periodic sensitivity monitoring compulsory for aquaculture and terrestrial species alike.[1]Source: World Health Organization, “2025 Edition of Global Survey to Track Antimicrobial Resistance Launches,” WHO News, who.int

Key Report Takeaways

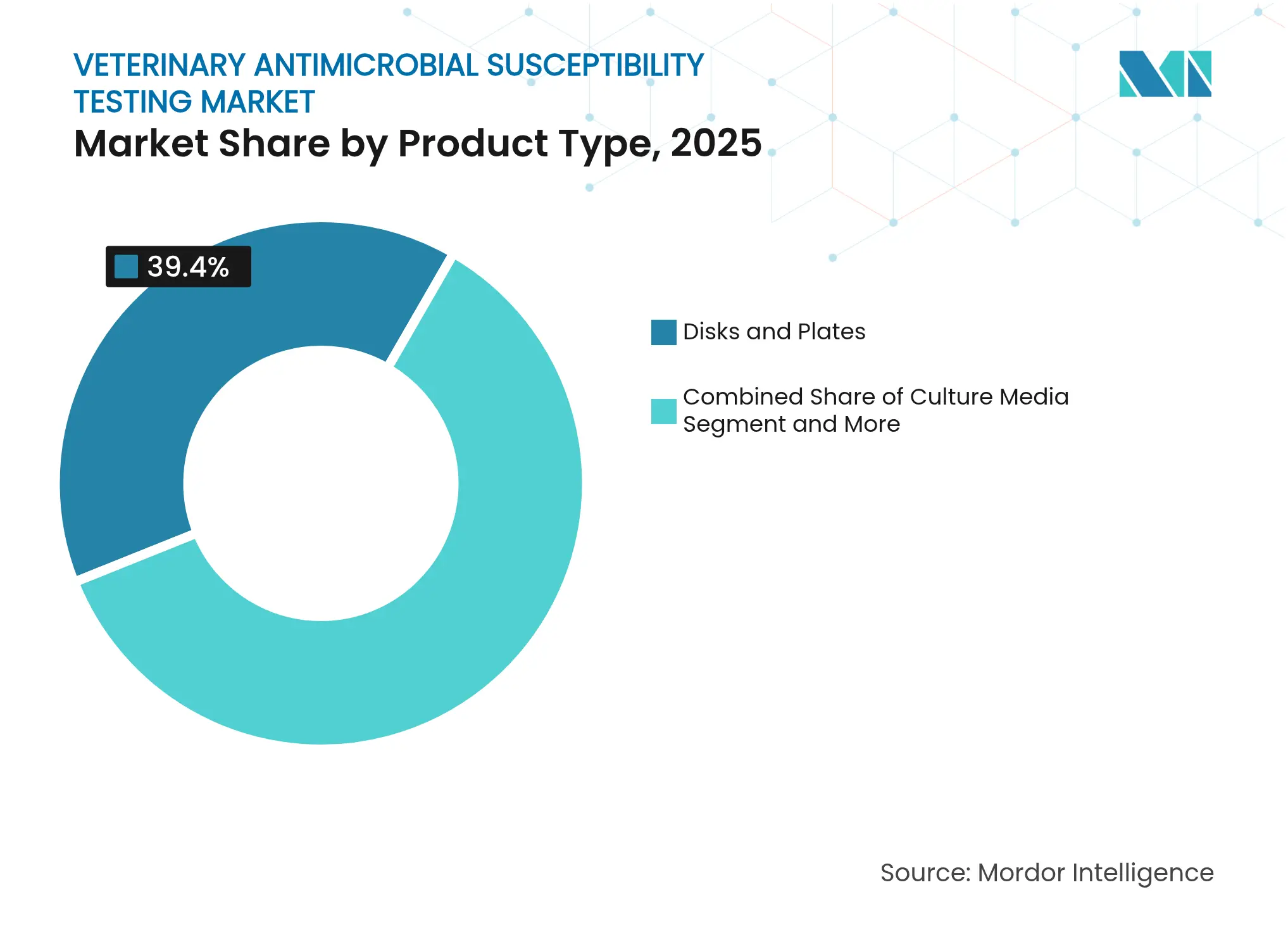

- By product type, disks and plates captured 39.40% revenue share in 2025, whereas automated testing systems are projected to expand at 6.92% CAGR through 2031.

- By testing method, disk diffusion held 44.70% share in 2025, while broth micro-dilution is expected to grow at 7.34% CAGR to 2031.

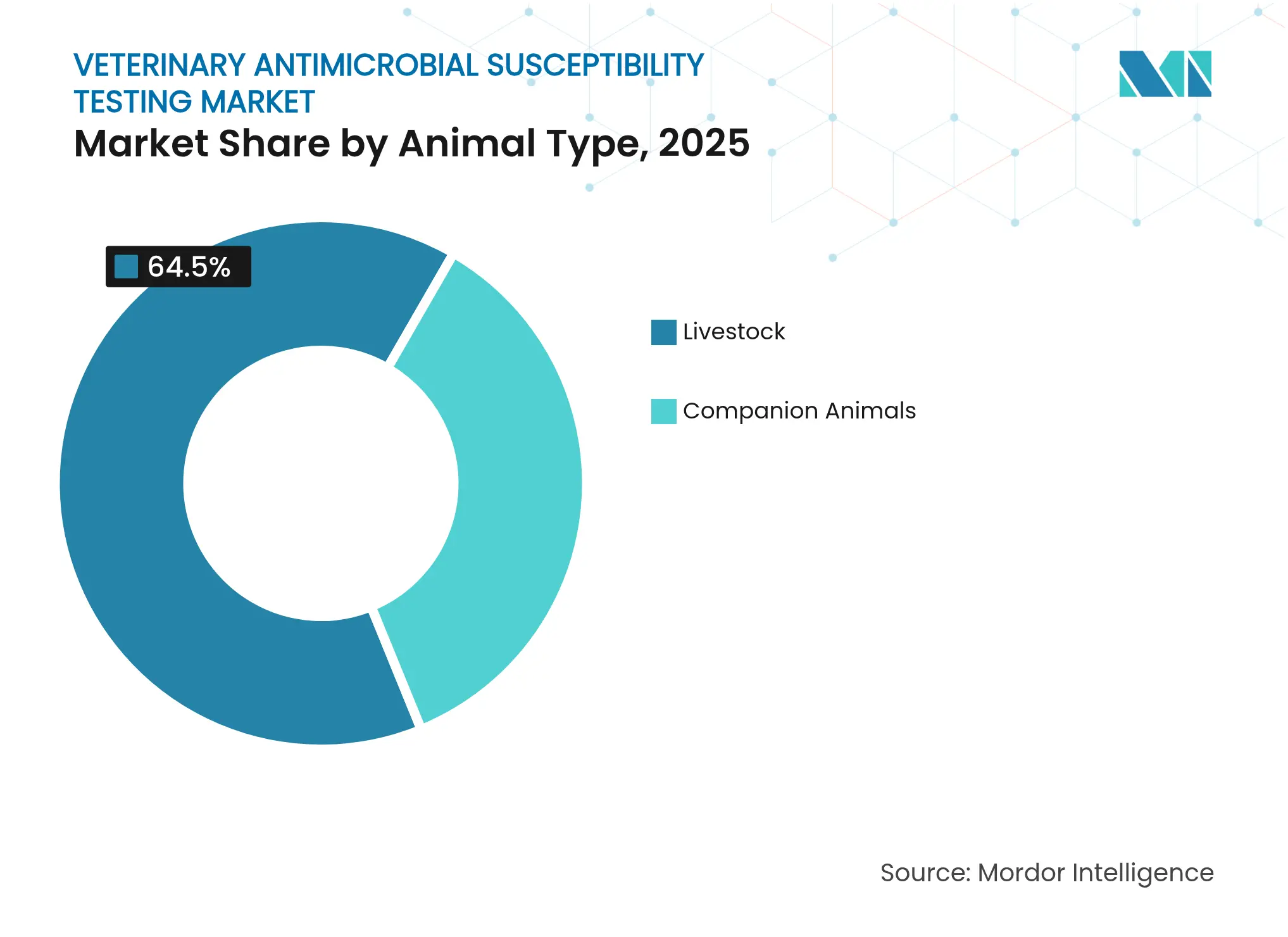

- By animal type, livestock accounted for 64.50% of the veterinary antimicrobial susceptibility testing market share in 2025; companion animals are forecast to post a 6.55% CAGR through 2031.

- By end user, veterinary reference laboratories held 55.70% of the veterinary antimicrobial susceptibility testing market size in 2025 and veterinary teaching and research institutes are projected to rise at 6.49% CAGR to 2031.

- By geography, North America contributed 35.80% of global revenue in 2025, while Asia-Pacific is likely to register the fastest growth at 7.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Antimicrobial Susceptibility Testing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Concerns about Antimicrobial Resistance (AMR)

Rising Concerns about Antimicrobial Resistance (AMR)

| +1.2% | Global | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Global

|

Impact Timeline

:

Long term (≥ 4 years)

|

Expanding Companion-Animal Diagnostics Spending

Expanding Companion-Animal Diagnostics Spending

| +0.9% | North America & Europe | Medium term (2-4 years) | |||

Growth of National AMR Surveillance Mandates

Growth of National AMR Surveillance Mandates

| +0.8% | Global, with early gains in EU, North America | Short term (≤ 2 years) | |||

Rapid Adoption of Automated AST Instruments

Rapid Adoption of Automated AST Instruments

| +0.7% | North America, Europe, APAC core | Medium term (2-4 years) | |||

Big-Data Integration with Herd-Management Software

Big-Data Integration with Herd-Management Software

| +0.5% | North America, Europe, spill-over to APAC | Long term (≥ 4 years) | |||

Aquaculture-Health Regulations Driving Fish-Pathogen AST

Aquaculture-Health Regulations Driving Fish-Pathogen AST

| +0.4% | APAC core, Europe, spill-over to MEA | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Concerns about Antimicrobial Resistance (AMR)

Worsening resistance patterns in food-borne and zoonotic pathogens have pushed governments to enshrine susceptibility testing in animal-health rules. The 2025 World Health Organization TrACSS survey shows 186 countries now tracking veterinary resistance trends, up from 157 in 2021, proving that AST is no longer optional. The United Kingdom’s VARSS 2023 report recorded a 43% increase in fully susceptible E. coli isolates since 2014, linking improved outcomes to mandatory testing in livestock. In contrast, a Nigerian field study found that although 89.8% of veterinarians recognize AST value, only 4.4% routinely request tests because of cost barriers.[2]Source: B. Adebowale et al., “Barriers to Effective Antimicrobial Resistance Management in Nigerian Livestock,” BMC Veterinary Research, biomedcentral.com These discrepancies show a two-tier market that favors vendors able to deliver affordable services. Continued alignment of animal and human health agendas under the One-Health framework ensures AMR will remain a core growth lever for the veterinary antimicrobial susceptibility testing market during the forecast horizon.

Expanding Companion-Animal Diagnostics Spending

Millennial and Generation Z pet owners now treat routine laboratory work as preventive care, lifting practice revenues. IDEXX reported 7% year-on-year recurring revenue growth in its companion-animal diagnostics arm for Q3 2024, reflecting higher test uptake per visit. New guidelines from the American Animal Hospital Association require culture and susceptibility panels before prescribing selected antimicrobials, institutionalizing demand. Zoetis has responded by adding AI-driven urine sediment analysis to its Vetscan Imagyst platform, reducing sample-to-answer time and broadening in-clinic test menus. These innovations encourage more clinicians to confirm pathogen susceptibility instead of using empirical therapy. As emotional bonds with pets translate into a willingness to pay for advanced care, the veterinary antimicrobial susceptibility testing market enjoys a resilient revenue stream insulated from livestock-cycle volatility.

Growth of National AMR Surveillance Mandates

Regulators are moving from voluntary to compulsory monitoring. The European Union ran its first baseline survey for antimicrobial resistance in aquaculture species in 2024, creating uniform sampling and reporting rules across 27 countries.[3]Source: European Food Safety Authority, “EU-Wide Baseline Survey of Antimicrobial Resistance in Aquaculture Animals,” pmc.ncbi.nlm.nih.gov In the United States, the Food and Drug Administration funded four Animal and Veterinary Innovation Centers in 2024 to fast-track resistance research and improve diagnostic capacity. Academic institutions participate as well: the University of Minnesota now coordinates a multi-country point prevalence survey that standardizes data collection for small-animal antibiotic use. Mandatory reporting requirements create baseline volumes that buffer laboratories against economic downturns and heighten barriers for suppliers lacking accredited methods. These programs also accelerate migration toward automated platforms able to process larger sample batches with traceable quality control.

Rapid Adoption of Automated AST Instruments

Short staffing in diagnostic facilities and the need for same-day results are steering budgets toward fully automated systems. Total Laboratory Automation platforms demonstrate 99% categorical agreement with conventional workflows while cutting throughput times, enabling veterinary labs to release final reports within 24 hours. When the Clinical and Laboratory Standards Institute updated fluoroquinolone breakpoints for canine isolates in 2023, labs equipped with automated micro-dilution panels adjusted cut-offs overnight, whereas users of manual disks required weeks to re-validate methods. Zoetis now bundles cloud-based AI to interpret plate images, lowering operator skill thresholds and attracting smaller clinics. Although initial capital outlays remain high, service contracts and leasing models are spreading those costs across multi-year budgets. Collectively, these factors lift automated adoption rates and reinforce long-run demand for consumables, software, and instrumentation inside the veterinary antimicrobial susceptibility testing market.

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Cost of Advanced AST Systems and Consumables

High Cost of Advanced AST Systems and Consumables

| -0.8% | Global, particularly emerging markets | Short term (≤ 2 years) |

% Impact on CAGR Forecast

:

-0.8%

|

Geographic Relevance

:

Global, particularly emerging markets

|

Impact Timeline

:

Short term (≤ 2 years)

|

Skills and Awareness Gaps in Emerging Countries

Skills and Awareness Gaps in Emerging Countries

| -0.6% | APAC emerging, MEA, South America | Medium term (2-4 years) | |||

Lack of Harmonised Veterinary Clinical Break-Points

Lack of Harmonised Veterinary Clinical Break-Points

| -0.4% | Global | Long term (≥ 4 years) | |||

Shift To "Antibiotic-Free" Meat Reducing

Prophylactic Tests

Shift To "Antibiotic-Free" Meat Reducing

Prophylactic Tests

| -0.3% | North America, Europe | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Cost of Advanced AST Systems and Consumables

A complete mid-range automated analyzer can exceed USD 100,000 before service contracts, placing it beyond the reach of many mixed-animal clinics. Even in mature settings, Cornell University increased its 2025 fee for systemic panels to USD 35, reflecting inflation in reagent and plastic costs. The Nigerian study cited earlier revealed that 95.6% of clinicians skip AST because of client cost sensitivity despite recognizing its clinical value. This economic friction is sharper in livestock, where producers operate on thin margins and often favor empirical treatments. Subscription-based testing networks and shared laboratory hubs are emerging to pool equipment and expertise, but uptake will take time, keeping price as a short-term drag on the veterinary antimicrobial susceptibility testing market.

Skills and Awareness Gaps in Emerging Countries

Accurate susceptibility reporting depends on correct sample collection, breakpoint selection, and result interpretation. A 2025 Malawi survey showed that although 85.5% of animal-health workers possessed solid theoretical understanding of stewardship, limited access to formal guidelines restricted best-practice adoption. Laboratory audits across North America and Canada uncovered inconsistent breakpoint usage even among accredited facilities, underlining the challenge of harmonization. Industry associations recommend continuous training, yet rural regions struggle to fund such programs. Until knowledge parity improves, under-utilization will temper growth potential, especially in lower-income economies where the veterinary antimicrobial susceptibility testing market remains nascent.

Segment Analysis

By Product Type: Automated Systems Drive Innovation

Automated analyzers are the fastest-rising product category, projected to advance at 6.92% CAGR to 2031, while disks and plates retained the highest revenue share of 39.40% in 2025 because of their low unit cost and entrenched protocols. Across many developing laboratories, disk diffusion remains the default option since it requires minimal capital and allows flexible panel design. Culture media sales move in tandem, providing growth ballast as vendors launch formulations optimized for veterinary pathogens.

Automated systems excel where throughput, traceability, and rapid turnaround justify higher fees. Vendors integrate robotics, bar coding, and AI-powered imaging that cut hands-on time and lower error rates, making them attractive for reference labs handling thousands of samples weekly. These efficiencies reinforce consumable pull-through, enlarging the installed base and anchoring the veterinary antimicrobial susceptibility testing market. As evidence of 99% agreement between total laboratory automation and manual methods gains visibility, resource-rich clinics in Asia-Pacific are jumping directly to automated platforms, bypassing incremental upgrades.

Note: Segment shares of all individual segments available upon report purchase

By Testing Method: Broth Micro-dilution Gains Momentum

Disk diffusion dominated with 44.70% share in 2025 because it suits mixed-species practices that process low volumes and need flexible panels. The method is embedded in veterinary curricula worldwide, ensuring a steady supply of trained technicians. Yet broth micro-dilution is forecast to deliver the highest 7.34% CAGR, buoyed by regulators that now seek numerical MIC data to guide dosing and resistance trending.

Automated platforms largely rely on micro-dilution trays, reinforcing mutual growth. The California Department of Food and Agriculture encourages practitioners to adopt MIC-based testing for precision therapy, signaling a policy tilt toward quantitative techniques. Agar dilution retains relevance for research isolates but remains labor-intensive and niche. Overall, method diversification supports supplier revenue resilience, underpinning the veterinary antimicrobial susceptibility testing market size.

By Animal Type: Companion Animals Accelerate Growth

Livestock accounted for 64.50% of veterinary antimicrobial susceptibility testing market share in 2025 because national monitoring programs predominantly target food animals. Poultry, swine, and cattle producers rely on periodic testing to preserve antibiotic efficacy and meet export rules. Companion animals, however, are posting the fastest 6.55% CAGR as pet owners embrace preventive care plans and insurers reimburse diagnostics more readily.

IDEXX attributes 91% of its corporate revenue to companion-animal diagnostics, underscoring the spending power of this group. Guidelines from AAHA mandate culture and sensitivity tests for recurring urinary and skin infections, converting clinical recommendations into routine orders. This regulatory pull, combined with rising pet numbers in urban China and India, accelerates segment expansion and strengthens overall momentum for the veterinary antimicrobial susceptibility testing market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Reference Labs Lead Market

Reference laboratories represented 55.70% of the veterinary antimicrobial susceptibility testing market size in 2025 because they pool high sample volumes, spread equipment depreciation, and offer specialized panels that individual clinics cannot. IDEXX runs the largest network globally, giving it economies of scale and bargaining power with suppliers.

Veterinary teaching and research institutes are forecast to grow at 6.49% CAGR as funders channel grants toward AMR projects and governments encourage academia to lead surveillance pilots. The FDA-backed Animal and Veterinary Innovation Centers exemplify this shift, providing shared infrastructure that extends beyond local referral caseloads. The upshot is a diversified customer mix that cushions vendors against cyclical spending swings and fortifies long-term growth for the veterinary antimicrobial susceptibility testing market.

Geography Analysis

North America contributed 35.80% of 2025 global revenue, supported by mature reimbursement models for companion-animal testing, a dense network of reference laboratories, and vigorous enforcement of AMR monitoring rules. The United States leads volumes as the FDA funds academic surveillance consortia and updates breakpoint guidance, keeping laboratories on a continuous upgrade cycle. Canada mirrors these dynamics through federal stewardship programs, while Mexico’s growing poultry and swine sectors adopt similar controls to maintain export eligibility.

Europe is a close second in value terms, propelled by harmonized legislation that mandates standardized susceptibility reporting across member states. The 2023 UK-VARSS report demonstrated tangible success, recording the lowest antibiotic sales to date and correlating the drop with wider AST use. Germany, France, and the Netherlands invest heavily in automation to manage sample throughput, whereas Italy and Spain show incremental uptake among dairy cooperatives.

Asia-Pacific is the fastest-growing region at 7.08% CAGR as China upgrades its veterinary infrastructure, India expands dairy diagnostics, and ASEAN nations roll out aquaculture AMR rules. Australia and Japan serve as technology hubs that export best practices to their neighbors. Skills deficits and pricing constraints persist in frontier economies, but multilateral grants and private investment are shrinking the gap. Continued regulatory tightening is expected to enlarge the regional veterinary antimicrobial susceptibility testing market.

Competitive Landscape

Market Concentration

The veterinary antimicrobial susceptibility testing market features moderate fragmentation. Bio-Rad Laboratories, Inc. and bioMérieux leverage extensive reference-lab networks and integrated software to safeguard share. IDEXX, for example, derives 91% of revenue from companion-animal diagnostics, which funds R&D scale beyond the reach of niche suppliers.

Strategy trends center on automation, artificial intelligence, and connected data platforms. Zoetis broadened its Vetscan Imagyst capabilities to include AI urine sediment analysis in January 2024, thereby expanding its slide-reader installed base. bioMérieux partners with cloud LIMS vendors to feed susceptibility results directly into herd-management apps, creating sticky ecosystems that discourage practice switching.

Emerging challengers target cost-sensitive markets with compact microfluidic cartridges and molecular panels that deliver results within hours. Regulatory hurdles for breakpoint updates favor incumbents that maintain dedicated compliance teams, yet disruptive point-of-care formats continue to attract venture funding. Overall, sustained investment in automation and data integration points to a steady but dynamic competitive environment in the veterinary antimicrobial susceptibility testing market.

Veterinary Antimicrobial Susceptibility Testing Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Kazakhstan hosted its first FAO-backed laboratory training on international AST standards for veterinary specialists, signaling Central Asia’s entry into structured AMR surveillance.

- January 2024: The AVMA Committee on Antimicrobials released six rapid-reference documents and a stewardship checklist to help veterinarians decide when to order AST.

- November 2023: The United Kingdom reported the lowest recorded sales of veterinary antibiotics and linked the decline to falling resistance metrics.

- November 2023: The Gambia adopted a fully costed National Action Plan on Antimicrobial Resistance for 2023–2027, setting measurable AST adoption targets.

Table of Contents for Veterinary Antimicrobial Susceptibility Testing Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Concerns about Antimicrobial Resistance (AMR)

- 4.2.2Expanding Companion-Animal Diagnostics Spending

- 4.2.3Growth of National AMR Surveillance Mandates

- 4.2.4Rapid Adoption of Automated AST Instruments

- 4.2.5Big-Data Integration with Herd-Management Software

- 4.2.6Aquaculture-Health Regulations Driving Fish-Pathogen AST

- 4.3Market Restraints

- 4.3.1High Cost of Advanced AST Systems and Consumables

- 4.3.2Skills and Awareness Gaps in Emerging Countries

- 4.3.3Lack of Harmonised Veterinary Clinical Break-Points

- 4.3.4Shift To “Antibiotic-Free” Meat Reducing Prophylactic Tests

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product Type

- 5.1.1Disks & Plates

- 5.1.2Culture Media

- 5.1.3Automated Testing Systems

- 5.1.4Other Products

- 5.2By Testing Method

- 5.2.1Disk Diffusion

- 5.2.2Broth Micro-dilution

- 5.2.3Agar Dilution

- 5.2.4Automated/Instrument-based

- 5.3By Animal Type

- 5.3.1Companion Animals

- 5.3.1.1Dog

- 5.3.1.2Cat

- 5.3.1.3Others

- 5.3.2Livestock

- 5.3.2.1Cattle

- 5.3.2.2Pigs

- 5.3.2.3Poultry

- 5.3.2.4Others

- 5.4By End User

- 5.4.1Veterinary Reference Labs

- 5.4.2Veterinary Teaching & Research Institutes

- 5.4.3Other End Users

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Merck KGaA

- 6.3.2Bio-Rad Laboratories

- 6.3.3Thermo Fisher Scientific Inc.

- 6.3.4bioMérieux SA

- 6.3.5Bruker Corporation

- 6.3.6Neogen Corporation

- 6.3.7Becton, Dickinson & Co.

- 6.3.8Danaher Corporation

- 6.3.9Alveo Technologies

- 6.3.10HiMedia Laboratories

- 6.3.11IDEXX Laboratories

- 6.3.12Zoetis Inc.

- 6.3.13Liofilchem Srl

- 6.3.14Accelerate Diagnostics

- 6.3.15QuantaMatrix Inc.

- 6.3.16Trek Diagnostic Systems

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Veterinary Antimicrobial Susceptibility Testing Market Report Scope

Veterinary antimicrobial susceptibility testing involves the assessment of microbial susceptibility to antimicrobial agents in animals. It employs laboratory techniques to determine the effectiveness of antimicrobials against specific pathogens, aiding veterinarians in making informed decisions for effective treatment.

The veterinary antimicrobial susceptibility testing market is segmented by product type into disks and plates, culture media, automated testing systems, and other product types. By animal type, the market is segmented into companion animals [dog, cat, and others] and livestock [cattle, pigs, and others]). By end user, the market is segmented into veterinary reference labs, veterinary research institutes, and other end users. Geographically, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. The report offers market sizes and forecasts in terms of value (USD) for the above segments.