ZigBee Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

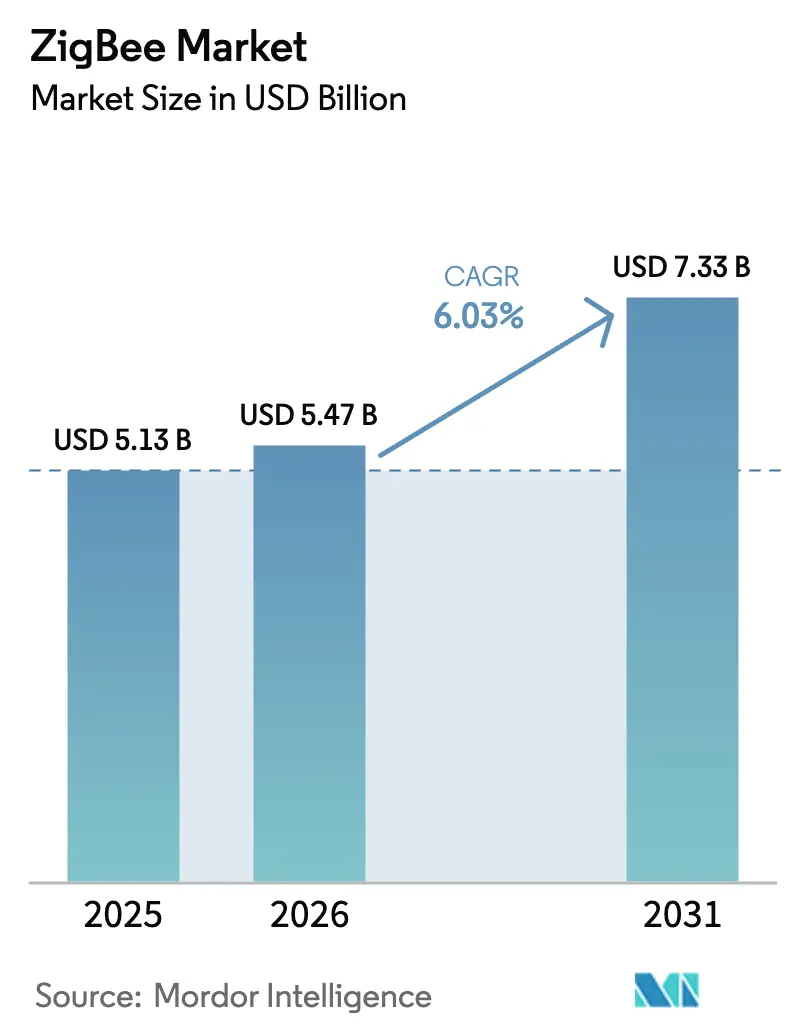

| Market Size (2026) | USD 5.47 Billion |

| Market Size (2031) | USD 7.33 Billion |

| Growth Rate (2026 - 2031) | 6.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ZigBee Market Analysis by Mordor Intelligence

The ZigBee Market size was valued at USD 5.13 billion in 2025 and is estimated to grow from USD 5.47 billion in 2026 to reach USD 7.33 billion by 2031, at a CAGR of 6.03% during the forecast period (2026-2031). After a decade focused on residential lighting, momentum is shifting toward the orchestration of distributed energy resources, factory retrofits, and vehicle-to-home energy hubs. Utilities are embedding IPv6-ready ZigBee IP radios into next-generation smart meters, while brownfield factories are adopting low-power mesh networks to stream vibration and temperature data that industrial Ethernet cannot carry cost-effectively. Gateway demand is rising because multi-protocol hubs now translate ZigBee, Thread, and Wi-Fi traffic for Matter controllers, and this hardware is increasingly bundled into mesh routers and smart speakers. Cost declines in multi-protocol system-on-chips are expanding the addressable base for end-device makers that previously had to choose between Bluetooth Low Energy or proprietary 2.4 GHz links. Competitive behavior is intensifying as Chinese module vendors are undercutting incumbents by 20% to 25%, prompting U.S. and European chipmakers to bundle full software stacks and cloud hooks to defend their gross margins.

Key Report Takeaways

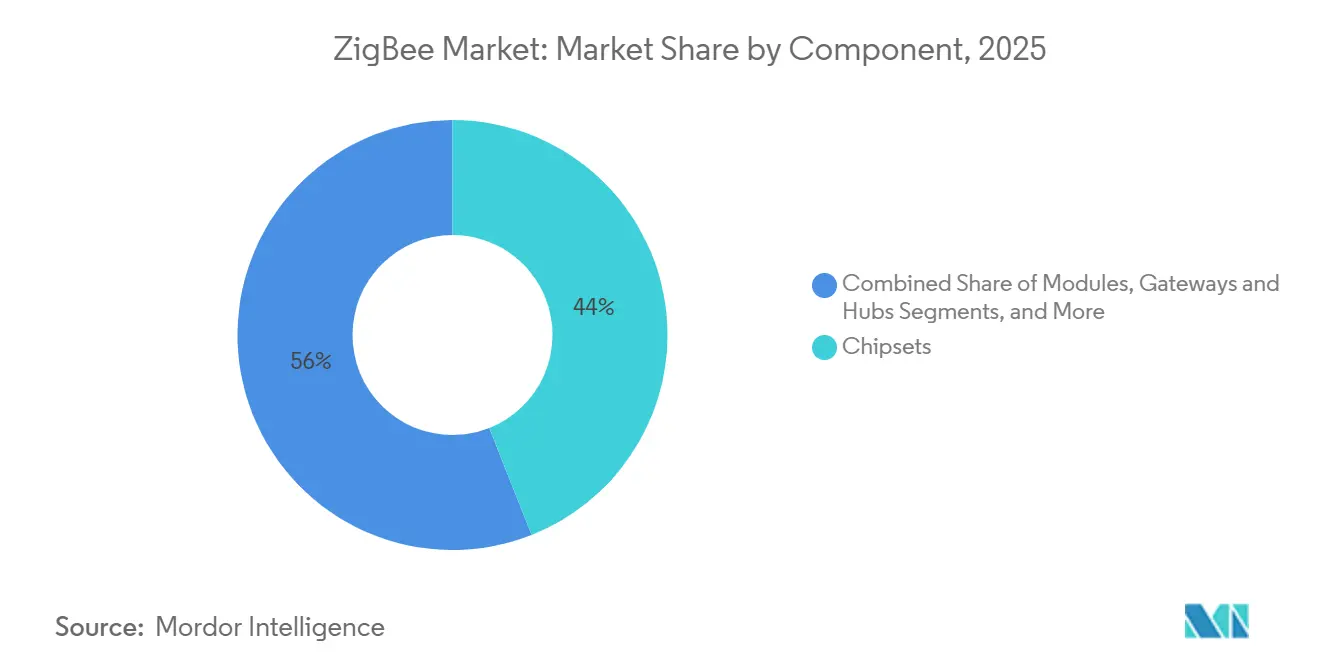

- By component, chipsets led with 44% ZigBee market share in 2025. Gateways and hubs are projected to expand at a 6.72% CAGR from 2026 to 2031.

- By end-user industry, residential automation commanded 38% revenue in 2025, while the energy and utilities segment is forecast to post the fastest 8.23% CAGR through 2031.

- By application, lighting control captured 41% of 2025 revenue, whereas EV-charging energy management is set to grow at a 7.69% CAGR to 2031.

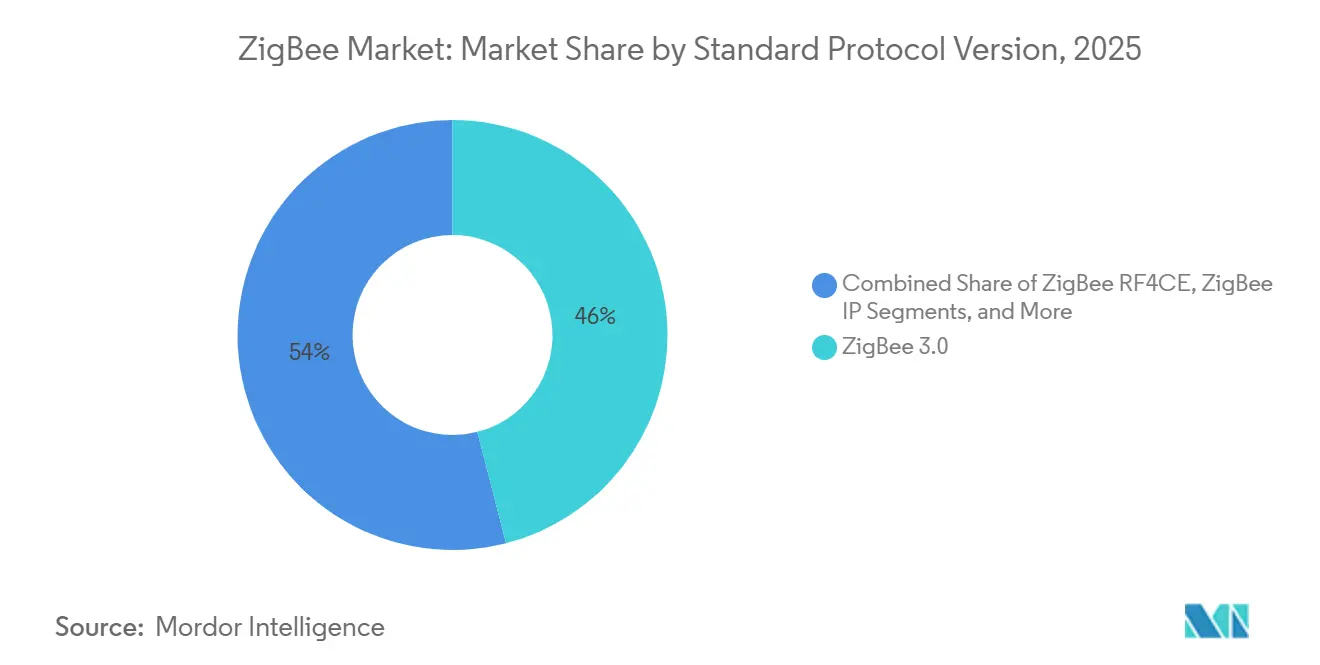

- By protocol version, ZigBee 3.0 held 46% revenue share in 2025, yet ZigBee IP is expected to rise at a 7.43% CAGR through 2031.

- By device type, coordinators dominated with 42% ZigBee market share in 2025, while end-devices/sensors are anticipated to register the fastest 7.12% CAGR through 2031.

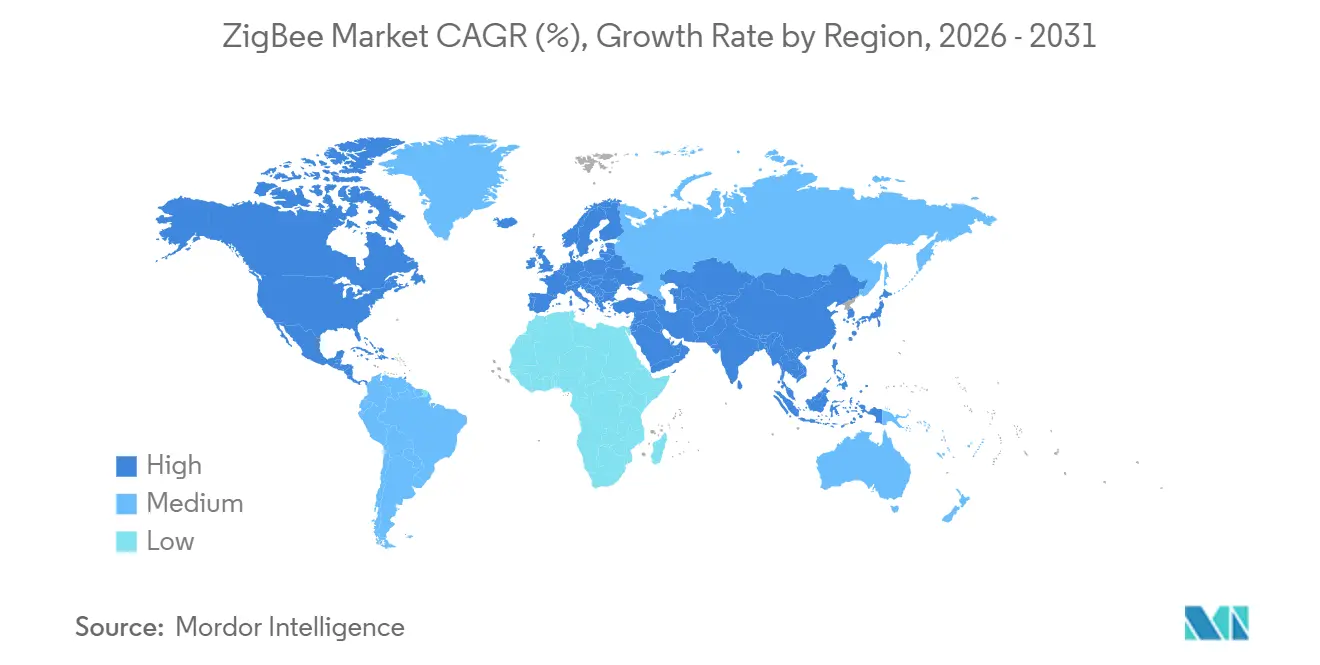

- By geography, North America accounted for 35% of 2025 revenue, but Asia-Pacific is poised for the highest 6.89% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global ZigBee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive Smart-Home Device Installations Worldwide | +1.20% | Global, concentrated in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Accelerating Industry 4.0 Retrofits in Brown-Field Factories | +0.90% | North America, Germany, Japan, South Korea | Medium term (2-4 years) |

| Government-Backed Smart-Meter Roll-outs in North America and Europe | +1.50% | North America and European Union, selective adoption in India and Brazil | Long term (≥4 years) |

| Multi-Protocol SoCs Lowering BOM Cost (ZigBee + BLE + Thread) | +0.80% | Global, led by North America and Asia-Pacific design wins | Short term (≤2 years) |

| EV-Charger to Home-Energy-Hub Integration Using ZigBee | +0.60% | North America, Western Europe, China | Medium term (2-4 years) |

| Utility Micro-Grid DER Orchestration Pilots Leveraging ZigBee Mesh | +0.40% | North America, European Union, Australia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Explosive Smart-Home Device Installations Worldwide

Global smart-home device shipments reached 1.1 billion units in 2024, but fewer than 18% shipped with ZigBee radios. Matter bridge certification is now extending the life of existing ZigBee sensors, and the Connectivity Standards Alliance confirmed 1,800 Matter-compatible products by November 2025. Echo smart speakers that embed a ZigBee hub made up 31% of Amazon’s North American sales, a nine-point jump from 2023, showing user appetite for single-gateway setups.[1]Amazon, “Q4 2024 Earnings Call Transcript,” amazon.com Property-management firms in the United States reported 40% lower installation labor when deploying ZigBee lighting networks because mesh self-healing cut truck rolls by 60%. Although the Federal Communications Commission is considering reallocating 2.4 GHz spectrum for 5G small cells, adaptive frequency-hopping algorithms specified in ZigBee 4.0 are designed to offset that risk.

Accelerating Industry 4.0 Retrofits in Brown-Field Factories

Factories erected before 2015 still account for 78% of global floor space, and most lack wireless sensor grids. Siemens logged EUR 340 million (USD 380 million) in ZigBee-based sensor revenue in fiscal 2025, up 28% year on year, driven by predictive-maintenance orders. The CC2652R7 radio from Texas Instruments samples legacy 4-20 mA loops directly, trimming installation time by 35%. Industrial Ethernet upgrades that added Time-Sensitive Networking between 2022 and 2024 now lean on ZigBee for low-priority telemetry, freeing deterministic bandwidth for motion control. The IEC amended its IEC 62591 standard in September 2024 to publish ZigBee frequency-hopping tables that shrink cross-protocol interference by 18 dB.

Government-Backed Smart-Meter Roll-outs in North America and Europe

Cumulative smart-meter deployments in the two regions climbed to 142 million by end-2025, and 54% used ZigBee radios for the home-area network. The United Kingdom had installed 33.7 million smart electricity meters by December 2024 and set a 75% national target for 2026. California investor-owned utilities already run 14.2 million ZigBee-enabled meters to dispatch time-of-use pricing and wildfire mitigation data. Utilities are repurposing the same mesh for grid-edge sensing; PG and E fitted 8,400 transformers with ZigBee sensors that transmit 15-minute environmental data, avoiding recurring cellular fees. The Clean Energy Package obliges European Union member states to reach 80% smart-meter coverage by 2027 under EN 50491-12-1, which references ZigBee Smart Energy 2.0.

Multi-Protocol SoCs Lowering BOM Cost (ZigBee + BLE + Thread)

The premium to add ZigBee to a Bluetooth Low Energy radio fell from USD 1.80 in 2022 to USD 0.45 in 2025 at 100,000-unit scale, as mask sets are spread across multi-protocol die. Nordic’s nRF5340 hosts two Cortex-M33 cores that run ZigBee, Thread, and Bluetooth simultaneously, enabling one SKU to serve Apple Home, Alexa, and Matter use cases. Qualcomm’s QCC730 added Wi-Fi 6E coexistence filters on the same die in January 2025, cutting external component count by 14 and shrinking modules 22%. Europe’s Radio Equipment Directive delegated act, active August 2025, requires every wireless consumer device to support an interoperable protocol, propelling multi-protocol adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Competition from BLE, Wi-Fi 6 and Matter | -0.90% | Global, acute in North America and Western Europe | Short term (≤2 years) |

| Persistent Interoperability Gaps Across Vendor Stacks | -0.60% | Global, fragmented in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Chronic Shortage of IEEE 802.15.4 Chip Foundry Capacity | -0.50% | Global, most acute in North America and Europe | Short term (≤2 years) |

| Looming Re-Allocation of 2.4 GHz ISM Spectrum in Urban Cores | -0.30% | Urban North America, European Union, select Asia-Pacific cities | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Intensifying Competition from BLE, Wi-Fi 6 and Matter

Matter treats the physical layer as abstract, letting one app supervise Thread, ZigBee, and Wi-Fi nodes over a unified IP stack, which blunts ZigBee’s historical lock-in. Apple withdrew native ZigBee support in iOS 18, compelling accessory makers to add a Matter bridge or adopt Thread. Bluetooth 5.4 extended advertising now offers comparable battery life and quadruple throughput, and Wi-Fi 6E chipsets below USD 3.00 at scale challenge ZigBee hubs on cost.[2]Bluetooth SIG, “Bluetooth 5.4 Core Specification,” bluetooth.com As 68% of Matter-certified products already prefer Thread for the mesh hop, ZigBee risks being relegated to a legacy endpoint protocol.

Persistent Interoperability Gaps Across Vendor Stacks

A 2024 National Institute of Standards and Technology audit reported 31% commissioning failures among 47 ZigBee-certified products from 19 vendors, often because the Trust Center key exchange was not uniformly implemented. Philips Hue locks third-party devices out unless they pass proprietary certification, adding six to nine months of testing for new entrants.[3]National Institute of Standards and Technology, “Interoperability Audit of ZigBee Devices,” nist.gov Asian hubs from Xiaomi and Aqara include custom cluster commands that break compatibility with European ecosystems, forcing distributors to stock separate SKUs and raising logistic costs 18% to 22%. Regulatory bodies certify only RF emissions, so the ZigBee Alliance’s voluntary program remains the sole means of enforcement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Chipsets Anchor Revenue, Gateways Surge on Edge Compute

Chipsets owned 44% ZigBee market share in 2025 because the radio continues to be the most valuable line item in the bill of materials. Average selling prices, however, declined 11% in 2024 as Telink and EBYTE flooded low-cost modules. Vendors are countering by folding application frameworks, network analyzers, and cloud provisioning into free toolchains to reinforce stickiness. Gateways and hubs are the growth engine at a 6.72% CAGR through 2031. Amazon’s Eero 6 router and Tuya Smart’s Matter hub combine ZigBee translation with neural processing that runs presence detection locally, cutting cloud latency to 85 milliseconds. Modules attract appliance makers without RF know-how because the radio, antenna, and certifications are prepackaged, and Telink reported module revenue of CNY 1.8 billion (USD 250 million) in 2024. Development software is migrating from perpetual to subscription, as seen when NXP moved the MCUXpresso SDK to a USD 499 annual plan in March 2025.

Gateways, routers, and modules are expected to capture incremental margin because their firmware unlocks Matter bridges and local analytics. Development software’s subscription shift smooths revenue, offsets margin erosion on silicon, and shortens customer time-to-market. Meanwhile, chip vendors are folding ultra-wideband and sub-GHz options onto the same die to future-proof designs, a trend that could lift blended average selling prices slightly after 2027 as customers demand centimeter-grade positioning and long-range backup links.

By End-User Industry: Residential Dominates, Utilities Accelerate

Residential automation in the ZigBee Market delivered 38% of 2025 revenue, primarily from lighting and HVAC retrofits, but its growth rate is plateauing in mature single-family markets. Expansion now hinges on multi-unit dwellings and emerging economies where device density is lower. Energy and utilities are forecast to lead with an 8.23% CAGR as smart meters evolve into distributed-energy resource controllers. PG and E’s rollout of transformer-mounted sensors illustrates the pivot from data collection to grid-edge actuation. Industrial automation, the second-largest revenue contributor, is adopting ZigBee routers within brown-field plants to offload non-critical data from Time-Sensitive Networking backbones. Healthcare uptake remains modest because the United States Food and Drug Administration favors licensed spectrum for life-critical monitoring.

Utilities conferring direct IP addressability favor ZigBee IP, which means software value migrates from proprietary stacks to open source middleware. Original-equipment makers in brown-field factories are bundling ZigBee with existing PLCs to support vibration and ambient monitoring, reducing downtime and minimizing CAPEX. Retail and digital commerce use cases such as electronic shelf labels are expanding moderately, while IT and telecommunications applications increasingly retreat to LoRaWAN in outdoor settings, confining ZigBee to indoor environments.

By Application: Lighting Leads, EV Energy Management Emerges

Lighting in the ZigBee Market held 41% of application revenue in 2025 amid global retrofit mandates that require occupancy-based dimming. ZigBee’s self-healing mesh avoids rewiring, so installation labor is lower than hardwired alternatives. EV-charging energy management is forecast to grow at a 7.69% CAGR through 2031 as vehicle-to-home bidirectional flows call for millisecond coordination among chargers, batteries, and meters. Ford’s Intelligent Backup Power system uses a ZigBee hub to prioritize circuits during outages. HVAC energy management benefits from ZigBee’s low duty cycle and multi-zone support, and Honeywell’s T10 Pro thermostat shows double-digit runtime savings in field trials.

Security devices such as locks and cameras are beginning to migrate toward Thread inside the Matter ecosystem, but ZigBee retains relevance in environments where a fixed wall controller is present. Asset and environmental monitoring in warehouses leverages ZigBee to overcome GPS dead zones, with European distribution centers reporting fewer mis-shipments after installing mesh location tags. Consumer electronics peripherals remain a minor slice because Bluetooth is native to smartphones.

By Standard / Protocol Version: ZigBee 3.0 Matures, ZigBee IP Gains Traction

ZigBee 3.0 provided 46% revenue in 2025 because it unified profiles without breaking backward compatibility, preserving the installed base of approximately 450 million devices. The ZigBee 4.0 release in October 2024 makes IPv6 native, which eliminates gateway address translation and trims latency by 140 milliseconds in micro-grid trials. ZigBee IP is forecast to expand at a 7.43% CAGR as utilities demand routable addressing for demand-response commands in the ZigBee market. Southern California Edison specified ZigBee IP in its 2025 meter refresh to push time-of-use pricing directly to thermostats and EV chargers. Legacy ZigBee PRO sensors stay relevant in factories that cannot afford network upgrades, and RF4CE remotes continue to decline as television brands pivot to Bluetooth Low Energy.

The European EN 50491-12-1 requirement that all home-area networks installed after January 2026 support IPv6 effectively sunsets non-IP ZigBee in the region. Chipmakers that add native IP stacks on-die reduce the need for application gateways, strengthening the business case for multi-protocol radios.

By Device Type: End-Devices Dominate Volumes, Coordinators Surge

The end-devices segment is anticipated to grow at a 7.12% CAGR, and the sensors segment represented 49% of 2025 shipments but contributes less revenue because its average selling price is under USD 8.00. Coordinators are the strategic linchpin because multi-protocol hubs now ship in smart speakers and mesh routers at minimal marginal cost. Embedded hubs in 28 million Echo devices create a de facto standard that third-party accessories must obey. Routers are shrinking as a distinct category because mains-powered bulbs and plugs now forward packets by default. ZigBee Green Power shifts battery-free sensor designs into production; EnOcean posted EUR 42 million (USD 47 million) sales in 2024 from kinetic-energy harvest modules that need no battery changes.

System-on-chip integration collapses bill-of-materials cost by roughly 30%, which unlocks price-sensitive markets such as smart plugs in emerging economies. Coordinator software, not hardware, is now the value driver because cloud hooks and over-the-air updates command support contracts, while hardware quickly commoditizes under Chinese price pressure.

Geography Analysis

North America contributed 35% revenue in 2025, powered by 18 million ZigBee-enabled smart-meter endpoints installed across California and Texas from 2023 to 2025 and by Amazon’s mass distribution of embedded hubs. The United States Energy Information Administration counted 107 million smart meters in service, and nearly half use ZigBee for home-area networks. Canadian adoption lags at 38% penetration because energy regulation remains provincial. Mexico is piloting 2.1 million smart meters through 2027 that integrate ZigBee demand-response links, paired with rooftop solar incentives.

Asia-Pacific is paced for a 6.89% CAGR, the highest among regions. China’s Tuya Smart controls 310 million devices, and its proprietary SoC undercuts Western rivals by 35%. India’s Revamped Distribution Sector Scheme aims to install 250 million smart meters by 2027, many of which will embed ZigBee for in-home displays. Japan’s Building Standard Law amendment requires energy-management systems in all new homes larger than 300 square meters, spurring retrofits across 8.2 million existing dwellings. South Korea’s smart-city projects in Songdo and Busan have already installed 1.4 million ZigBee streetlights and parking sensors, which curbed municipal energy use by 22%.

Europe held 28% of the 2025 total, anchored by the United Kingdom’s 33.7 million smart electricity meters and Germany’s energy-efficiency loan program. The United Kingdom mandated 75% smart-meter coverage by December 2026, while Germany requires households above 6,000 kWh to deploy meters by 2028, boosting ZigBee demand. France completed 35 million Linky installations that rely on power-line for backhaul but keep ZigBee for optional in-home displays, creating an aftermarket for third-party devices.

South America, Middle East, and Africa combine for 12% share. Brazil’s March 2025 ruling requires 10 million meters by 2028 with ZigBee home-area networks, worth an estimated USD 420 million module market. Saudi Arabia’s NEOM city already operates 340,000 ZigBee sensors for real-time resource tracking. South Africa issued a tender for 1.2 million ZigBee-capable meters in January 2025, targeting Johannesburg and Cape Town rollouts by 2027.

Regulatory Landscape

Regulation affecting ZigBee deployments covers radio authorization as well as a widening set of IoT cybersecurity and interoperability expectations. In the United States, ZigBee devices operate under FCC equipment authorization for unlicensed 2.4 GHz use, while in Europe the Radio Equipment Directive (RED) has raised security expectations for internet-connected radio products. Its delegated cybersecurity requirements apply from August 2025 and are often aligned to standards such as EN 18031. As a result, vendors of ZigBee hubs, meters, and sensors are increasingly documenting secure provisioning, software update processes, and vulnerability handling alongside RF/EMC testing.

National market-access rules are also tightening through more granular compliance documentation and import controls. Chile implemented SUBTEL Resolution 737 effective February 22, 2026, shifting certain 2.4 GHz device compliance toward a public, QR-linked compliance page model, and Vietnam introduced stricter import checks for ZigBee 3.0 devices effective June 1, 2026, including third-party laboratory full-temperature-range RF attenuation reporting. On the standards side, the Connectivity Standards Alliance (CSA) released Matter 1.6 and Product Security 1.1 in June 2026, and it continued advancing the ZigBee roadmap (including ZigBee 4.0 announced in late 2025). This has reinforced the certification and security frameworks that device makers and module vendors use to reduce cross-market compliance friction.

Value Chain Analysis

The ZigBee value chain begins with IP and standards development, including IEEE 802.15.4 at the PHY/MAC layer and the Connectivity Standards Alliance for ZigBee application and certification programs. Silicon suppliers then deliver multi-protocol SoCs and supporting software stacks, which semiconductor vendors provide to module makers packaging radios, antennas, and pre-certifications. Those modules flow to OEMs producing end devices such as lighting, sensors, thermostats, and locks, as well as to gateway and hub providers for utility and industrial endpoints. The last step involves ecosystem platforms and installers that integrate devices into smart-home controllers, industrial monitoring systems, and utility head-end and DER orchestration environments.

Certification, testing infrastructure, and commissioning tools are increasingly central to time-to-market and cost. The CSA has been expanding programs aimed at streamlining certification and lifecycle maintenance, including FastTrack Recertification and Portfolio Certification launched in 2025, and it has continued ecosystem education through ZigBee 4.0 technical sessions, including a 2026 webinar focused on security and commissioning. Supply-side constraints referenced in the market context, such as IEEE 802.15.4 chip capacity tightness, make foundry allocation, packaging, and module availability consequential. At the same time, multi-protocol designs (ZigBee plus Thread/BLE/Wi-Fi) are shifting differentiation toward firmware, cloud hooks, and certification support rather than radio hardware alone.

Competitive Landscape

The top five chipset vendors controlled 62% of 2025 shipments, pointing to moderate concentration. Silicon Labs’ USD 350 million acquisition of Qorvo’s portfolio in August 2024 consolidated 52% of IEEE 802.15.4 intellectual property. Chinese entrants such as Telink and EBYTE discount modules by up to 25% at high volume, driving incumbents to bundle turnkey stacks, over-the-air infrastructure, and certification support. Texas Instruments reports that its free SimpleLink SDK reduces customer development cycles by over four months, adding stickiness that pure hardware cannot deliver.

Matter threatens to commoditize the mesh layer because a single bridge can operate ZigBee, Thread, and Wi-Fi devices. As of November 2025, 1,800 products were Matter-certified, 68% of which default to Thread. Incumbents therefore position ZigBee as an endpoint protocol inside Matter ecosystems, shifting profit pools towards cloud services and analytics. The IEEE 802.15.4z amendment, published August 2024, added ultra-wideband ranging, and chipmakers are integrating that option to compete with Bluetooth angle-of-arrival. Vertical integrators like Tuya Smart are rolling their own silicon plus cloud stack, locking accessory makers into managed ecosystems in return for lower unit cost and faster time-to-market.

White-space remains in industrial predictive maintenance, where only 12% of brown-field factories have wireless sensors, and in distributed-energy resource management, where ZigBee IP’s IPv6 routing dovetails with grid-edge control systems. Vendors that couple open silicon with managed device clouds stand to capture the next wave of value.

ZigBee Industry Leaders

Silicon Laboratories Inc.

Texas Instruments Incorporated

NXP Semiconductors N.V.

Microchip Technology Inc.

Digi International Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White-space is most visible where ZigBee mesh economics and installed-base compatibility address gaps that are costly to cover with wired retrofits or higher-power radios. In brownfield industrial sensing, the report context points to limited wireless adoption, with only 12% of brownfield factories having wireless sensors, leaving room for ZigBee routers and end devices that offload non-critical telemetry from industrial Ethernet and TSN backbones. Utilities and DER orchestration also create pull-through for devices and gateways as ZigBee IP and IPv6-ready networks are embedded into next-generation smart meters and grid-edge sensors, supported by large smart-meter footprints already deployed across North America and Europe.

Adoption pathways are also shifting through product and ecosystem updates rather than replacing ZigBee outright. ZigBee 4.0 introduces ZigBee Direct as a standard feature, enabling BLE-based commissioning via smartphones and reducing hub dependency during onboarding, while its Suzi sub-GHz extension targets larger facilities and outdoor coverage in 800-900 MHz bands. On the demand side, the Connectivity Standards Alliance cited 1,800 Matter-compatible products by November 2025, and multi-protocol gateways translating ZigBee, Thread, and Wi-Fi for Matter controllers are being bundled into routers and smart speakers, positioning ZigBee as an endpoint protocol within broader IP ecosystems. Regulatory tightening around cybersecurity, including RED cybersecurity requirements active from August 2025 and CSA Product Security updates in 2026, supports opportunities for vendors that package secure stacks, compliance documentation, and fleet update tooling for device makers, utilities, and industrial integrators.

Recent Industry Developments

- June 2026: Silicon Labs announced a 200-node Matter-over-Thread validation network demonstrated at the Connectivity Standards Alliance Unify event, showcasing large-scale mesh validation in commercial and residential environments. The work reinforces demand for multi-protocol development and test infrastructure where ZigBee endpoint devices are bridged into Matter ecosystems via hubs and gateways.

- June 2026: Quectel introduced the FCM365X wireless module based on NXP Semiconductors RW612, combining Wi-Fi 6, Bluetooth LE 5.4, ZigBee, and Thread in a single module for smart home and industrial IoT designs. The launch supports faster OEM time-to-market by packaging multi-radio capability and reducing the need to qualify separate connectivity modules.

- August 2025: STMicroelectronics announced a USD 120 million expansion of its 40 nm production lines in Italy to address IEEE 802.15.4 component shortages, with completion scheduled for Q2 2026. The added capacity targets a key supply bottleneck for ZigBee-class radios and helps stabilize availability for module makers and device OEMs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market tracks revenue from Zigbee based wireless connectivity used to connect devices in smart home, building, industrial, and utility environments. We treat the market as the sale of Zigbee related components and enabling products that make these networks function in real deployments.

Scope exclusions: We exclude non-Zigbee connectivity stacks and devices that do not ship with Zigbee functionality even if they serve similar smart home or IoT end uses.

Segmentation Overview

- By Component

- Chipsets

- Modules

- Gateways and Hubs

- Development Tools and Software

- By End-User Industry

- Residential Automation

- Industrial Automation

- IT and Telecommunication

- Healthcare

- Retail and Digital Commerce

- Energy and Utilities (Smart Metering / Smart Grid)

- By Application

- Lighting Control

- HVAC and Energy Management

- Security and Access Control

- Asset and Environmental Monitoring

- Other Applications (Consumer Electronics Peripherals, and More)

- By Standard / Protocol Version

- ZigBee RF4CE

- ZigBee PRO

- ZigBee 3.0

- ZigBee IP

- ZigBee Remote Control 2.0

- By Device Type

- Coordinators

- Routers

- End-Devices / Sensors

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by anchoring the demand backdrop for connected devices and low power wireless, then narrowing it to Zigbee shipments and adoption indicators. For this, we lean on public sources such as IEEE standards documentation, the Connectivity Standards Alliance materials, and regulator and statistics portals such as the US FCC and Eurostat for device and wireless context.

We also use customs and trade statistics where available (for example, UN Comtrade style series) to sanity check directional movement in relevant device categories, and we review peer reviewed journals and conference proceedings for changes in protocol versions and security features. To keep assumptions realistic, company filings, product documentation, investor presentations, and reputed press are reviewed to understand where Zigbee is actually being specified. In a few places, we use paid subscriptions for company financials and patent databases to fill gaps on supplier exposure and innovation activity, which helps us avoid relying on one signal only. The sources listed here are illustrative, and many other public references were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and structured surveys are used to pressure test what desk research suggests on adoption, pricing, and where Zigbee is being designed in or designed out. We speak with a mix of chipset and module stakeholders, gateway and hub ecosystem participants, device makers, and system integrators, and we cross check the story across APAC, EMEA, and the Americas so one region does not drive the full result.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 14% | APAC: 42% |

| Mid tier: 46% | Functional/Unit leaders: 38% | EMEA: 35% |

| Smaller Players: 18% | Managers: 48% | Americas: 23% |

Market-Sizing & Forecasting

Sizing is built using a top-down logic where connected device deployment and use case penetration data are used to reconstruct the Zigbee enabled demand pool, which is then translated into value using observed pricing. The model is then corroborated with selective bottom-up approximations, such as sampled supplier revenue exposure, channel checks on common module and gateway price bands, and shipment proxies for high volume end devices, before totals are finalized.

A few inputs that matter in this market include the installed base trend of smart home and building automation devices, utility smart metering and grid modernization rollouts, the mix shift across protocol versions (for example, Zigbee 3.0 and Zigbee IP), gateway or hub attach rates, and typical ASP movement for chipsets, modules, and gateways as volumes scale. When a bottom-up cross check is incomplete, gaps are handled by applying adoption ratios validated in interviews and using conservative ranges for ASPs, and the midpoint is used only after inconsistencies are resolved.

For forecasting, we rely mostly on scenario analysis supported by a light multivariate regression view, where the key drivers are smart home device growth, industrial automation activity, and utility rollout timing. The final forecast path is adjusted after expert feedback confirms whether near term design cycles and certification timelines are expected to accelerate or slow down.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, and then checked for unusual jumps by region, component type, and use case before sign-off. If a variance is too large to explain with known drivers such as a protocol transition or a demand slowdown, we revisit assumptions, re-check currency conversion timing, and re-contact respondents when needed.

A multi step review is followed where one analyst builds the model, another analyst challenges the inputs and calculations, and only then does the final narrative get aligned to the numbers. The report is refreshed annually, and interim updates are done when material events occur (such as major certification changes or notable demand shocks). Right before delivery, a fresh pass is done so clients receive the latest updated view.

Mordor Intelligence's Zigbee Market Size Compared Against Other Published Estimates

Published market numbers for Zigbee do not always match, and that usually comes from how each study draws the line on what revenue is counted and which year is treated as the base. Differences also show up when firms use different price assumptions, apply faster or slower adoption curves, or update their model at different times.

Zigbee Alliance membership signals, protocol version mix (such as Zigbee 3.0 versus Zigbee IP), and gateway attach rates are the kinds of checks that keep our model grounded, but they are not always used the same way elsewhere. The spread is also influenced by whether adjacent connectivity categories get included, how device type buckets are grouped, and whether inflation and FX are applied using spot rates or annual averages, which can move USD totals meaningfully.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.13 B (2025) | |

| Global Consultancy A | USD 5.56 B (2025) | Often presented with a broader device type framing, which can pull in more value from end device bundles and solution level rollups, and that can lift the 2025 total versus a component and enabling product view. |

| Industry Research Group B | USD 5.22 B (2025) | Uses a different base year setup and growth window, and it can rely more on generalized IoT growth pacing, which may understate or overstate Zigbee specific attach rates in utilities and building automation. |

Non-Zigbee protocols and lookalike smart connectivity revenue sit outside Mordor Intelligence's scope, which is one reason the 2025 figure can land below studies that blend multiple low power wireless options into one pool. Once the scope is aligned, most of the remaining gap tends to come from ASP progression assumptions and how quickly protocol transitions are expected to happen in real product cycles.

Key Questions Answered in the Report

What is the current value of the ZigBee market size and its expected CAGR to 2031?

The ZigBee market size stands at USD 5.47 billion in 2026 and is forecast to grow at a 6.03% CAGR, reaching USD 7.33 billion by 2031.

Which component category is expected to post the fastest growth through 2031?

Gateways and hubs are projected to expand at a 6.72% CAGR because multi-protocol routers are embedded in smart speakers and mesh Wi-Fi systems.

Why is the energy and utilities segment important for ZigBee adoption?

Utilities are shifting from simple metering to distributed-energy resource orchestration, driving an 8.23% CAGR for ZigBee in this segment.

How does Matter influence the future of ZigBee devices?

Matter bridges allow one controller to manage ZigBee, Thread, and Wi-Fi devices, which repositions ZigBee as an endpoint protocol inside a broader IP ecosystem.

Which region is forecast to grow the fastest in ZigBee deployments?

Asia-Pacific is set for a 6.89% CAGR, fueled by China’s Tuya Smart platform and India’s 250 million smart-meter program.

What competitive moves are chip vendors making to defend margins in the ZigBee market?

Leading vendors bundle software stacks, over-the-air update tools, and cloud provisioning to add value beyond commoditized radio hardware. The combined share of the top five chipset suppliers is 62%, which yields a market concentration score of 6, indicating a moderately consolidated landscape where a handful of players hold meaningful influence but competitive entry remains viable.

Page last updated on: