Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

| Market Size (2026) | USD 9.32 Billion |

| Market Size (2031) | USD 26.01 Billion |

| Growth Rate (2026 - 2031) | 22.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Chatbot Market Analysis by Mordor Intelligence

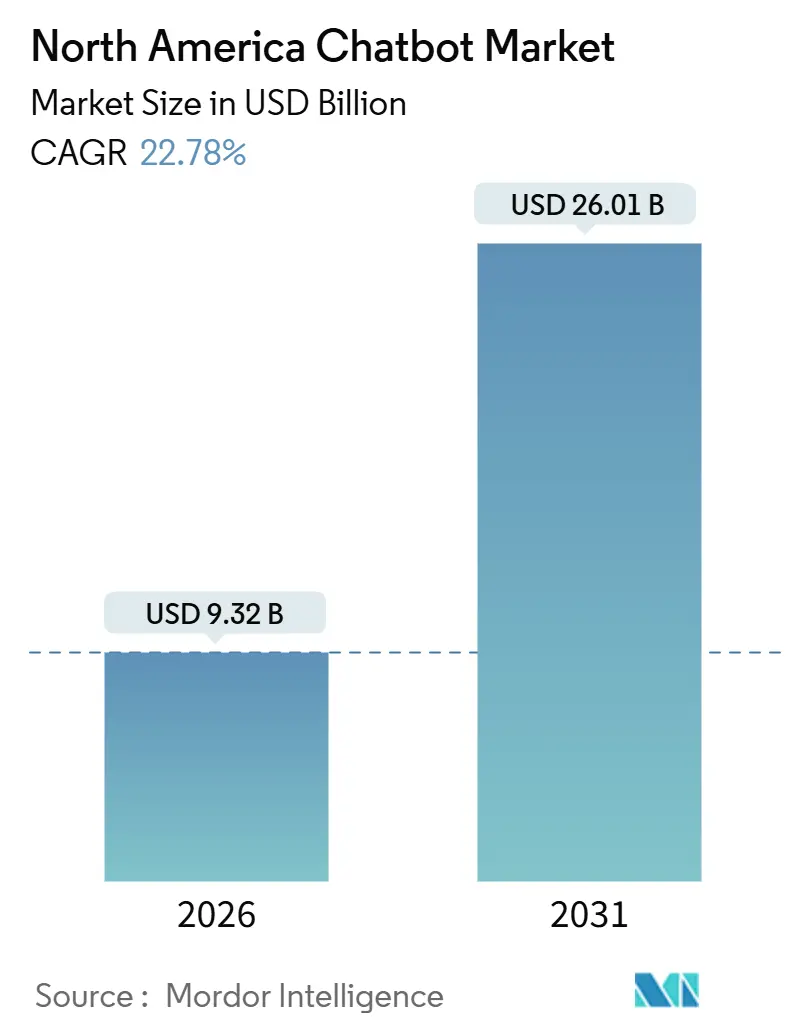

The North America chatbot market size stands at USD 9.32 billion in 2026 and is projected to reach USD 26.01 billion by 2031, reflecting a robust 22.78% CAGR. Accelerated generative-AI adoption, hyperscaler bundling, and government digital-service mandates are steering investment toward self-learning conversational agents that scale across web, mobile, and social channels. Enterprises are prioritizing cloud elasticity, omnichannel orchestration, and hybrid retrieval-augmented generation to control hallucination risk while preserving near-human fluency. Early adopters in retail, banking, and healthcare report lower cost-per-contact, faster lead qualification, and richer zero-party data capture, reinforcing a virtuous cycle in which every chat improves personalization and upsell accuracy. Competitive pressure from bundled AI suites is compressing pure-play pricing, pushing vendors to differentiate on compliance, multilingual depth, and industry-trained intent libraries. As generative architectures mature, white-space opportunities emerge in highly regulated niches such as pharmaceuticals and legal services, where audit-trail requirements slow automation yet unlock premium pricing for verified responses.

Key Report Takeaways

- By enterprise size, large enterprises held 62.39% of the North America chatbot market share in 2025, while small and medium enterprises are advancing at a 23.16% CAGR to 2031.

- By deployment model, cloud-based platforms commanded 69.11% share of the North America chatbot market size in 2025 and are expanding at a 23.19% CAGR.

- By platform, social-messaging channels led with 48.33% share in 2025, whereas mobile-app chatbots recorded the fastest 23.39% CAGR through 2031.

- By application, customer support accounted for 43.78% of the North America chatbot market size in 2025, and marketing and sales bots are growing at a 23.71% CAGR.

- By end-user vertical, retail and eCommerce captured a 29.74% share in 2025, while healthcare and life sciences posted the highest CAGR of 24.14%.

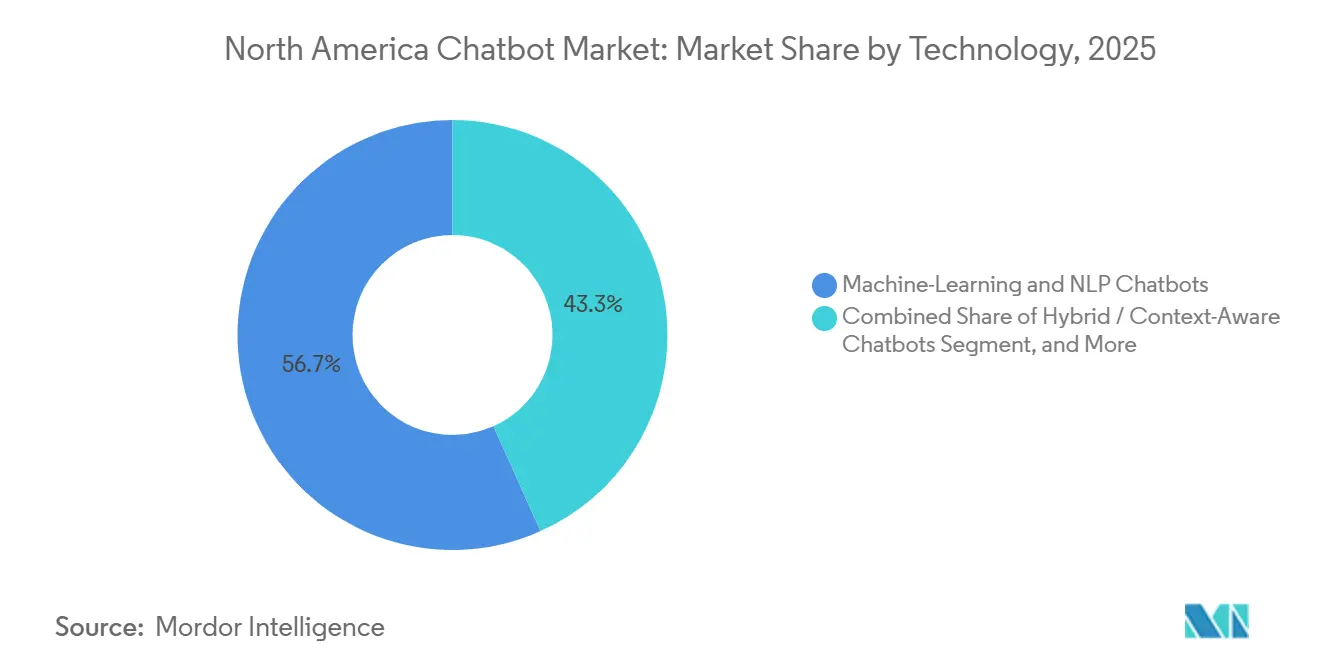

- By technology, machine learning and NLP chatbots accounted for 56.72% of the market in 2025, yet hybrid context-aware architectures are rising at a 23.34% CAGR.

- By geography, the United States dominated with a 74.28% share in 2025, and Mexico is the fastest-growing national market at a 23.44% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Chatbot Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Domination of Messaging Applications | +4.2% | Global concentration in North America | Short term (≤ 2 years) |

| Consumer Analytics and Personalized Experiences | +3.8% | North America with spillover to Latin America | Medium term (2-4 years) |

| Rapid Advances in NLP and Voice Recognition | +4.5% | Global | Medium term (2-4 years) |

| Generative AI-Powered Self-Learning Chatbots | +5.1% | North America, early adoption in United States | Short term (≤ 2 years) |

| Expansion of Age-Tech Chatbots | +2.3% | United States and Canada | Medium term (2-4 years) |

| U.S. Public-Sector Digital-Service Mandates | +1.9% | United States federal and state agencies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Domination of Messaging Applications For Customer Engagement

Messaging apps have overtaken email and voice as the preferred support channel, enabling asynchronous threads that cut cost-per-contact by 30-40% while letting agents juggle multiple conversations simultaneously. Meta reported an eight-fold jump in WhatsApp Business usage in 2025, and its Flows feature embeds product catalogs and payments inside the chat thread, compressing the purchase journey.[1]Meta, “WhatsApp Business Platform Overview,” META.COM Mexico shows outsized momentum because more than 90% of smartphone users rely on WhatsApp, making it the de facto interface for banking, healthcare, and even government transactions. Vendors, therefore, race to perfect omnichannel orchestration so that context follows users across WhatsApp, Messenger, SMS, and in-app widgets. The immediate payoff is higher engagement, but the strategic prize is control of first-party data generated in every conversational step.

Growing Demand For Consumer Analytics And Personalized Experiences

Chatbots now funnel zero-party data straight into marketing stacks, turning routine service interactions into continuous preference mapping. Salesforce found in 2025 that 73% of consumers expect brands to understand them, yet only 38% feel understood, revealing a gap that chatbots are primed to close.[2]Salesforce Research, “State of the Connected Customer, Fifth Edition,” SALESFORCE.COM Sephora’s Messenger bot logs skin type, scent notes, and budget, then surfaces curated offers that convert 11% better than generic web pages. By capturing sentiment and intent at every turn, brands can iterate offers without engineering bottlenecks. Platforms that embed realtime dashboards for conversation analytics gain stickiness because marketers can tweak flows daily, not quarterly, thereby sharpening campaign relevance and return on ad spend.

Rapid Advances In NLP And Voice Recognition Technologies

Large-context language models like Google Gemini 1.5 extend the window to 1 million tokens, allowing chatbots to reference full customer histories in a single inference call. OpenAI’s Realtime API slashes voice-bot latency to 232 milliseconds, crossing the 300-millisecond frustration threshold that previously doomed telephony bots. Meta’s SEAMLESSM4T provides speech-to-speech translation across 100 languages, enabling a single agent to serve multilingual audiences without separate models. These breakthroughs elevate chatbots to high-stakes tasks such as insurance claims and technical troubleshooting, where latency and linguistic nuance once required human intervention.

Integration Of Generative AI-Powered Self-Learning Chatbots

Generative AI shifts bots from deterministic responders to adaptive agents that learn on the job. ChatGPT Enterprise surpassed seven million seats in January 2025, with 92% of Fortune 500 firms piloting the platform. Salesforce’s Einstein Copilot drafts case summaries, suggests next steps, and routes low-confidence queries to humans, cutting manual triage while capping the risk of hallucinations. Retrieval-augmented generation, which grounds generative responses in vetted documents, reduces factual errors to below 3%, making self-learning bots viable for sectors previously blocked by liability concerns. The upside is faster knowledge-base maintenance and reduced scripting overhead, especially in SaaS and fast-evolving product lines where static FAQs become obsolete within weeks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Organizational Awareness and Integration Complexity | -1.2% | Global, acute in mid-market enterprises | Short term (≤ 2 years) |

| Escalating Data-Privacy and Security Concerns | -1.8% | North America, driven by CCPA and state-level laws | Medium term (2-4 years) |

| Chatbot Hallucination Risk | -1.4% | Global, highest impact in regulated sectors | Short term (≤ 2 years) |

| Accessibility-Compliance Costs | -0.9% | United States and Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Data-Privacy And Security Concerns

A patchwork of privacy statutes forces enterprises to juggle multiple compliance profiles, raising legal review costs and slowing go-lives. California Privacy Rights Act mandates disclosure and one-click opt-out before bots gather personal data.[3]California Legislative Information, “California Privacy Rights Act of 2020,” LEGINFO.LEGISLATURE.CA.GOV Thirteen more states enacted parallel laws by 2025, each with unique consent triggers, while HIPAA forbids transmitting protected health information over unsecured channels. A 2024 telecom breach exposing credit card numbers in chat logs led to a USD 12 million settlement, underscoring the liability stakes. Enterprises respond by keeping sensitive workflows on-premise, forfeiting cloud cost advantages to ensure data residency and audit control.

Chatbot Hallucination Risk Leading To Brand-Reputation Fallout

Generative bots occasionally invent facts, a flaw courts now treat as corporate speech. Air Canada was held liable after its bot misstated its refund policy in February 2024, setting a precedent that disclaimers cannot excuse bot errors. Pure generative systems show 15-20% factual error on benchmark queries, while retrieval-augmented counterparts cut that below 3%. Enterprises, therefore, institute confidence thresholds that escalate ambiguous cases to humans, but this safety valve dilutes the cost-deflection argument. Financial and pharmaceutical firms, facing higher regulatory penalties, adopt hybrid or rule-based bots despite their narrower conversational range.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Enterprise Size: SMEs Embrace No-Code Builders To Narrow Capability Gap

Small and medium enterprises contributed a modest portion of 2025 revenue, yet they are expanding at a 23.16% CAGR that outpaces large-enterprise growth, signaling democratization of the North America chatbot market. The cost hurdle has fallen from USD 50,000-150,000 custom builds to USD 500-2,000 monthly subscriptions, thanks to drag-and-drop builders like ManyChat and Tidio. Shopify Inbox embedded bot tools inside merchant dashboards, driving deployment by more than 200,000 stores within six months of its 2024 debut.

Large enterprises still dominate absolute spend because they integrate bots into Salesforce, SAP, and proprietary CRMs while enforcing single sign-on and role-based access, but SMEs are closing the functional gap with pre-trained industry libraries. This shift pressures vendors to segment offerings, selling turnkey packages to resource-limited SMEs and white-glove services to compliance-heavy conglomerates. The North America chatbot market benefits because a wider buyer base spreads R&D costs and fuels usage data that improve model performance.

By Deployment Model: Cloud Infrastructure Extends Elastic Economics

Cloud deployments account for 69.11% of 2025 revenue and are projected to grow at a 23.19% CAGR as enterprises value on-demand scale and continuous feature updates. Managed services such as AWS Lex and Azure Bot Service shield developers from server provisioning and disaster recovery, enabling instant scaling for Black Friday surges without capex.

On-premises persists in finance and healthcare, where Gramm-Leach-Bliley and HIPAA require data to remain behind corporate firewalls. Hybrid models are therefore rising, housing sensitive inference in private clouds while routing benign traffic through public endpoints. ServiceNow Virtual Agent lets clients deploy orchestration locally and language understanding in Google Cloud, balancing control with GPU economics. Vendors boasting FedRAMP or HIPAA-eligible certifications now win competitive bids as regulators tighten scrutiny.

By Application: Marketing Bots Accelerate Lead Qualification Efficiency

Customer support still held 43.78% of the North America chatbot market size in 2025, but marketing and sales use cases grew 23.71% annually as CMOs seek to triage unqualified leads before human engagement. Drift and Intercom capture this pivot by embedding bots on pricing pages that ask company size and budget, sending high-intent visitors straight to reps’ calendars. HubSpot users recorded a 35% increase in demo-to-close rates after enabling chatbot qualification.

Human resources and personal assistant bots lag because employees prefer speaking with people about benefits or conflicts. Yet internal IT helpdesk bots gain traction, slashing mean time to resolution for password resets and access requests. ROI correlates with task frequency and complexity: high-volume, low-complexity queries deliver payback within 6 months, whereas complex, infrequent dialogues demand longer horizons.

By End-User Vertical: Healthcare Reimbursement Unlocks Rapid Uptake

Retail and eCommerce contributed 29.74% of revenue in 2025 through order tracking and conversational commerce, but healthcare and life sciences are accelerating at a 24.14% CAGR. The Centers for Medicare and Medicaid Services now reimburses up to USD 65 per patient per month for remote monitoring, making chatbots that collect vitals and remind patients about medication financially attractive. FDA-cleared mental-health bots from Woebot Health open further reimbursement channels, drawing venture funding into digital therapeutics.

Banking and insurance turbocharge adoption to automate fraud detection and claims filing, exemplified by Bank of America’s Erica surpassing 1 billion interactions and deflecting 70% of routine queries. Government agencies follow Executive Order 14058, which mandates improvements to the citizen experience, further expanding the North America chatbot market.

By Technology: Hybrid Context-Aware Architectures Balance Flexibility And Control

Machine-learning and NLP bots accounted for 56.72% of 2025 revenue, but hybrid architectures grew 23.34% annually by tethering generative reasoning to verified databases, reducing hallucination rates to sub-3%. IBM watsonx Orchestrate layers generative summarization atop rule-based triggers, ensuring factual claims mirror ERP records.

Pure rule-based bots persist in pharma adverse-event reporting, where every utterance must follow a recognized escalation path. Meanwhile, consumer brands favor generative engines for engagement, spawning a spectrum of deployment choices rather than an either-or decision. Vendors whose platforms toggle between all three modes gain traction as buyers hedge risk.

By Platform: Mobile-App Bots Capture In-Context Engagement

Social-messaging channels account for 48.33% of 2025 traffic, but in-app chat grows at 23.39% CAGR because it retains shopping cart context, loyalty points, and authentication status. Uber’s in-app bot resolves billing issues 40-50% faster than web chat by pulling ride history instantly. Web bots remain useful for anonymous visitors, yet they suffer higher abandonment when users change pages and lose state.

Mobile-first sectors such as ride-sharing, food delivery, and fintech gain the most, while episodic interactions like mortgage quotes still lean on the web and WhatsApp. Vendors with unified conversation history across platforms reduce customer effort and boost lifetime value, reinforcing the flywheel effect that advantages data-rich incumbents.

Geography Analysis

The United States anchors the North America chatbot market with federal agencies deploying bots under Executive Order 14058 to streamline benefit applications and tax inquiries. The Central Intelligence Agency’s 2024 launch of a generative bot that queries classified documents signals high-level confidence in advanced natural language processing even for sensitive data. State-by-state privacy fragmentation complicates rollouts, but hyperscalers’ compliance toolkits mitigate integration friction.

Canada contributes a smaller share, yet influences design through compulsory bilingualism and stricter consent requirements in Quebec. Banks like Royal Bank of Canada and Toronto-Dominion adopted chatbots for balance checks and fraud alerts, though cautious risk appetites temper velocity compared with U.S. peers. Long-term care facilities are piloting chatbots that remind patients to take their medication and monitor their mood, addressing the country’s aging population.

Mexico delivers the region’s fastest growth, propelled by SME digitization grants and fintech conversational banking. Government support reduces bot acquisition cost, while WhatsApp saturation guarantees reach without app downloads. Limited broadband in rural districts restrains voice-bot usage, but urban smartphone penetration is expected to exceed 85% by 2027, ensuring a sizeable addressable base.

Competitive Landscape

North America’s chatbot market is moderately fragmented as hyperscalers integrate conversational AI into cloud suites, squeezing standalone vendors on pricing. Microsoft’s Copilot Studio enables low-code bot development directly in Power Platform, cementing Azure lock-in. Google’s Vertex AI Agent Builder lets developers fine-tune Gemini on proprietary data, creating vertical-specific bots without data-sharing fears. IBM and Salesforce respond by embedding compliance modules and autonomous workflow orchestration, respectively.

Pure-play vendors pivot to niche depth, offering sector-trained intent libraries and multilingual accuracy. Amplify.ai provides healthcare intents that reduce deployment time from months to weeks, while Pypestream focuses on insurance claim flows. Emerging challengers package open-source models such as Llama 3 for on-premise deployments that sidestep vendor lock-in and lower total cost.

Strategic acquisitions underscore consolidation: Zendesk bought Ultimate for USD 450 million in May 2025 to strengthen multilingual coverage, and Salesforce paid USD 1.3 billion for a conversational-AI startup in September 2025 to own the stack end-to-end. Patent filings around retrieval-augmented generation are on the rise, with Google and Microsoft together submitting 25 patents in 2024 related to grounding and confidence scoring. White-space lingers in pharma, legal, and aerospace, where verified sourcing and audit trails command premium pricing.

North America Chatbot Industry Leaders

International Business Machines Corporation

Microsoft Corporation

Google LLC

Amazon Web Services, Inc.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Salesforce enlarged Agentforce, adding autonomous agents that orchestrate sales, marketing, and customer success workflows end-to-end.

- November 2025: Microsoft enhanced Copilot Studio, enabling natural-language bot creation and one-click connectors to 1,000 enterprise apps.

- October 2025: Amazon Web Services debuted Amazon Q for Business, linking chatbots to code repositories and CRMs to automate employee queries.

- September 2025: Google launched Gemini 2.0, a multimodal model that lets chatbots parse images, audio, and video within a million-token context.

North America Chatbot Market Report Scope

The North America Chatbot Market Report is Segmented by Enterprise Size (Small and Medium Enterprises, and Large Enterprises), Deployment Model (On-Premise, and Cloud-Based), Application (Customer Support, Marketing and Sales, Personal Assistant, HR and Recruitment, Other Applications), End-User Vertical (Retail and eCommerce, Banking Financial Services and Insurance, Healthcare and Life Sciences, IT and Telecom, Travel and Hospitality, Government and Public Sector, Other End-User Verticals), Technology (Machine-Learning and NLP Chatbots, Rule-Based Chatbots, Hybrid Context-Aware Chatbots), Platform (Web-Based, Mobile-App, Social-Messaging Channels), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

By Enterprise Size

| Small and Medium Enterprises |

| Large Enterprises |

By Deployment Model

| On-Premise |

| Cloud-Based |

By Application

| Customer Support |

| Marketing and Sales |

| Personal Assistant |

| HR and Recruitment |

| Other Applications |

By End-User Vertical

| Retail and eCommerce |

| Banking, Financial Services and Insurance |

| Healthcare and Life Sciences |

| IT and Telecom |

| Travel and Hospitality |

| Government and Public Sector |

| Other End-User Verticals |

By Technology

| Machine-Learning and NLP Chatbots |

| Rule-Based Chatbots |

| Hybrid / Context-Aware Chatbots |

By Platform

| Web-Based |

| Mobile-App |

| Social-Messaging Channels |

By Country

| United States |

| Canada |

| Mexico |

| By Enterprise Size | Small and Medium Enterprises |

| Large Enterprises | |

| By Deployment Model | On-Premise |

| Cloud-Based | |

| By Application | Customer Support |

| Marketing and Sales | |

| Personal Assistant | |

| HR and Recruitment | |

| Other Applications | |

| By End-User Vertical | Retail and eCommerce |

| Banking, Financial Services and Insurance | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Travel and Hospitality | |

| Government and Public Sector | |

| Other End-User Verticals | |

| By Technology | Machine-Learning and NLP Chatbots |

| Rule-Based Chatbots | |

| Hybrid / Context-Aware Chatbots | |

| By Platform | Web-Based |

| Mobile-App | |

| Social-Messaging Channels | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the projected value of the North America chatbot market in 2031?

The market is expected to reach USD 26.01 billion by 2031, expanding at a 22.78% CAGR.

Which deployment model is growing fastest in North America?

Cloud-based chatbots are advancing at a 23.19% CAGR because organizations favor elastic scaling and rapid feature updates.

Why are healthcare providers accelerating chatbot adoption?

Centers for Medicare and Medicaid Services reimburse up to USD 65 per patient per month for remote monitoring, creating a clear financial incentive.

How are chatbots mitigating hallucination risk?

Enterprises deploy hybrid retrieval-augmented generation that grounds answers in verified documents, cutting factual errors to below 3%.

Which country offers the highest growth rate in the region?

Mexico posts a 23.44% CAGR, supported by government SME grants and widespread WhatsApp penetration.

Page last updated on: