X-ray Films Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

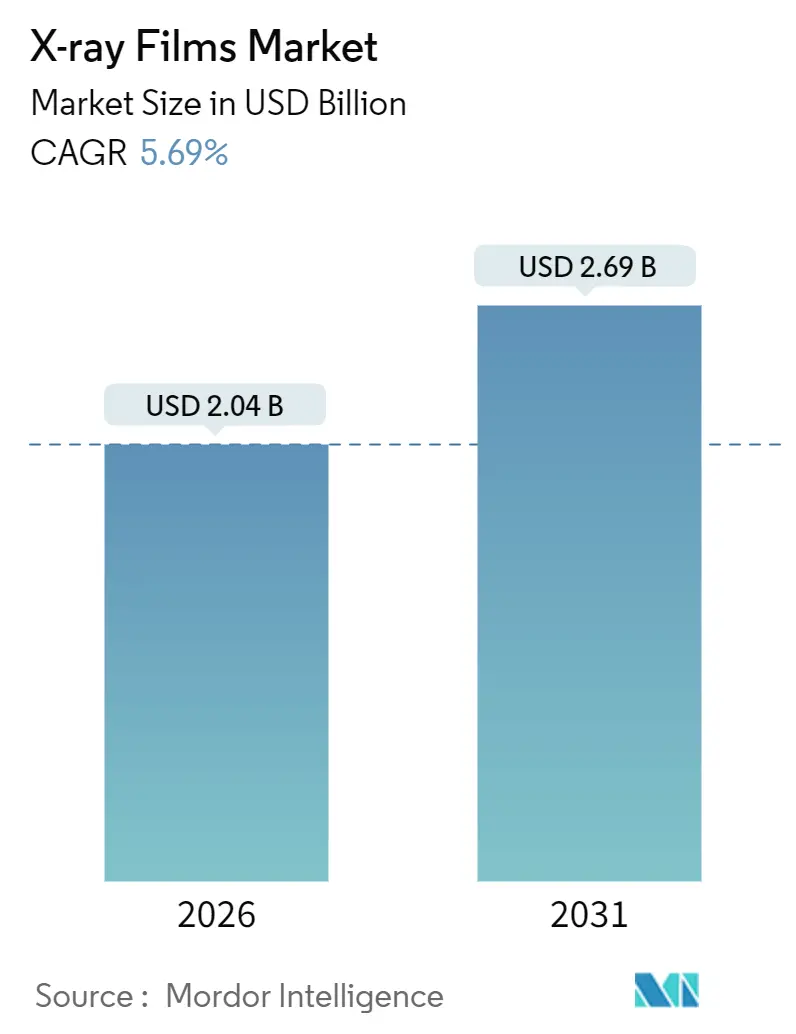

| Market Size (2026) | USD 2.04 Billion |

| Market Size (2031) | USD 2.69 Billion |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

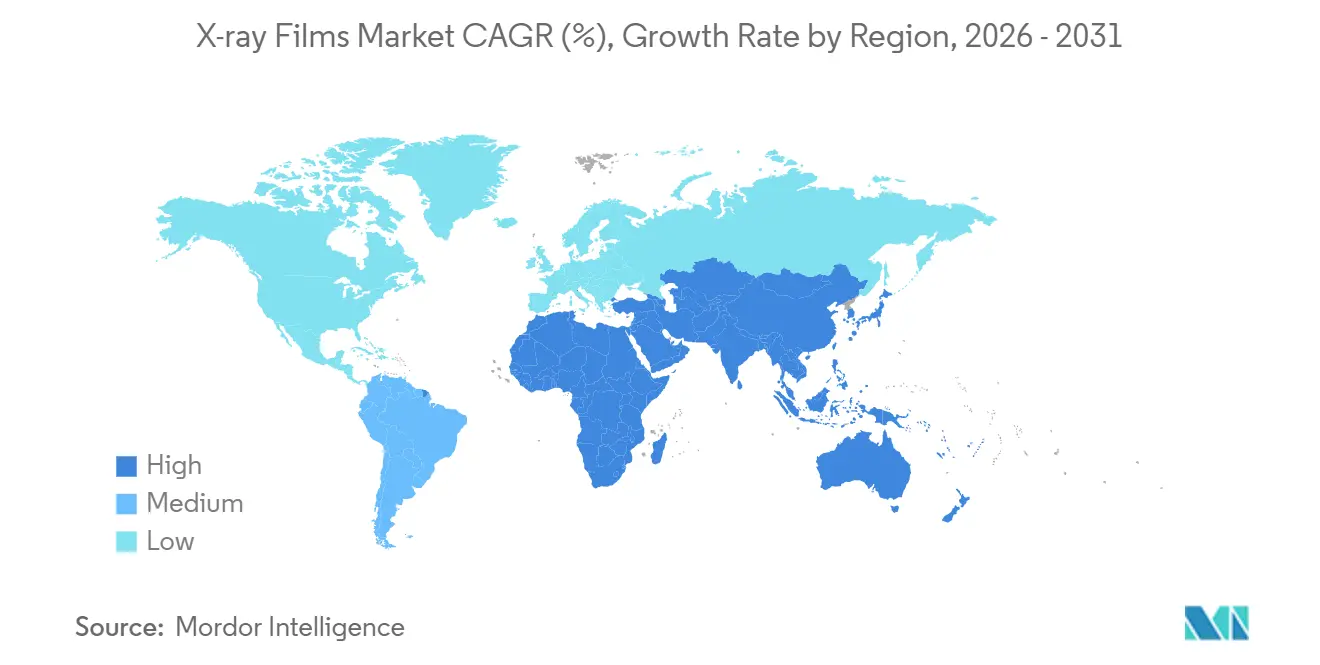

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

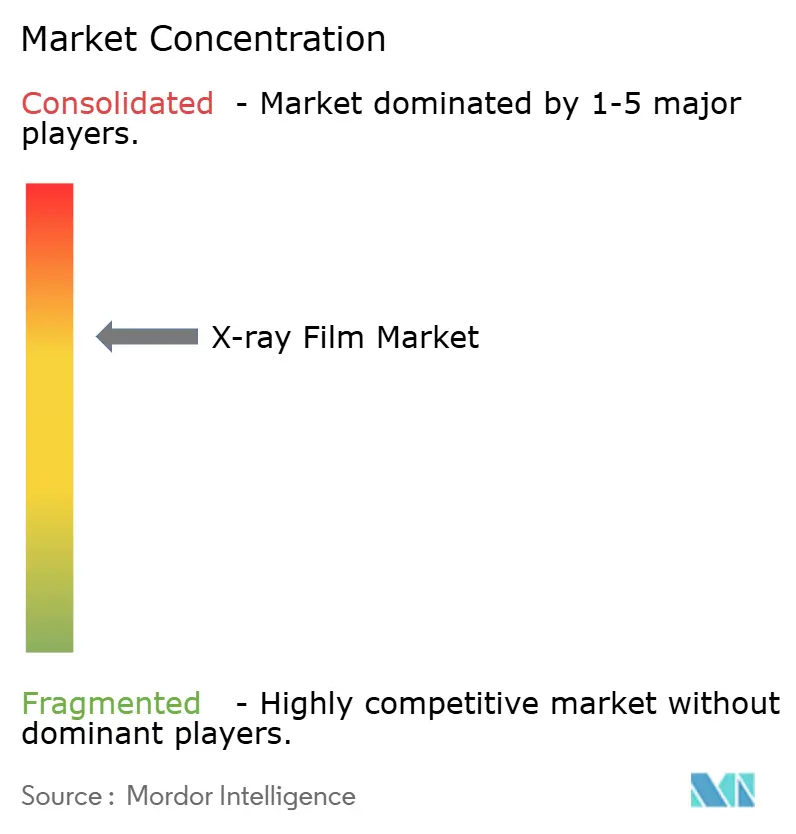

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

X-ray Films Market Analysis by Mordor Intelligence

The X-ray films market size is valued at USD 2.04 billion in 2026 and is projected to reach USD 2.69 billion by 2031, reflecting a 5.69% CAGR throughout the forecast period. Structural demand endures because capital-constrained hospitals in emerging economies cannot always finance flat-panel detectors, industrial codes still mandate film-based archives, and silver recovery offsets disposal costs. Hospitals keep legacy analog suites active while diagnostic centers expand outpatient volumes, and industrial users preserve film workflows for long-term traceability. Vendor strategies now blend digital portfolios with selective film lines, keeping consumables available for price-sensitive buyers. Environmental rules on silver discharge simultaneously raise compliance costs and heighten the economic case for closed-loop recovery systems.

Key Report Takeaways

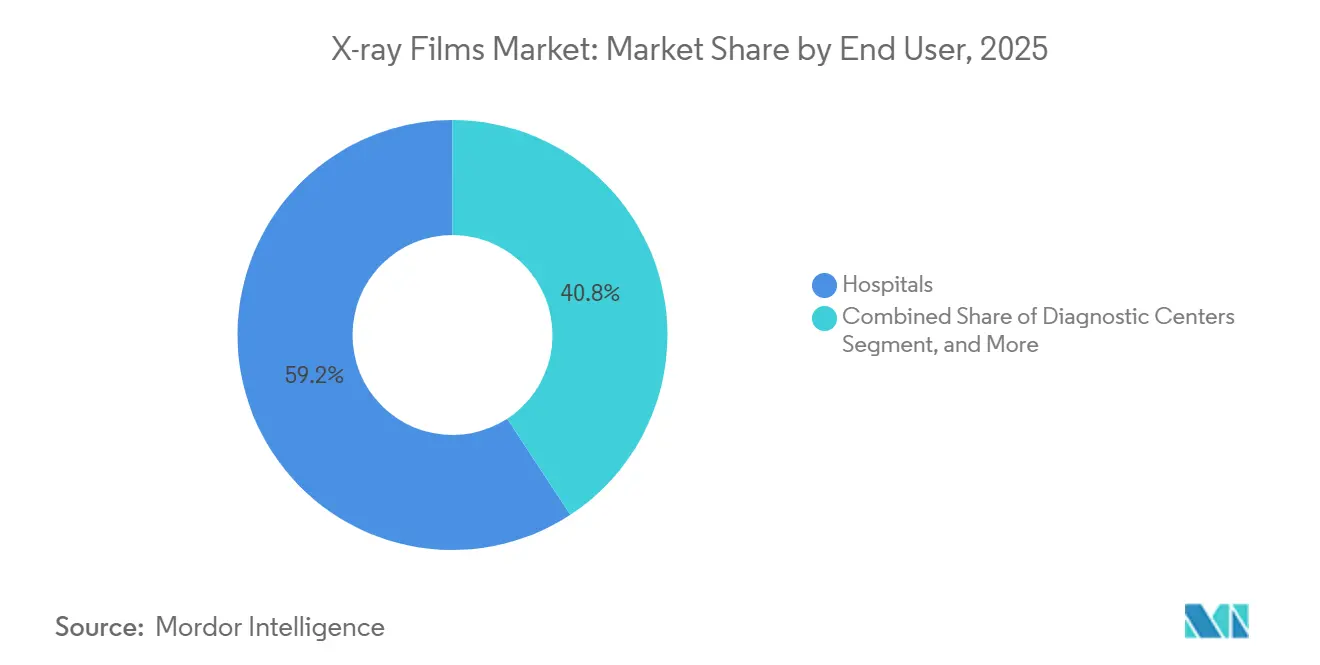

- By end user, hospitals accounted for 59.23% of the X-ray films market share in 2025, while diagnostic centers are advancing at a 6.72% CAGR through 2031.

- By film type, dry film led with 57.78% of the X-ray films market share in 2025 and is forecast to grow at a 5.82% CAGR.

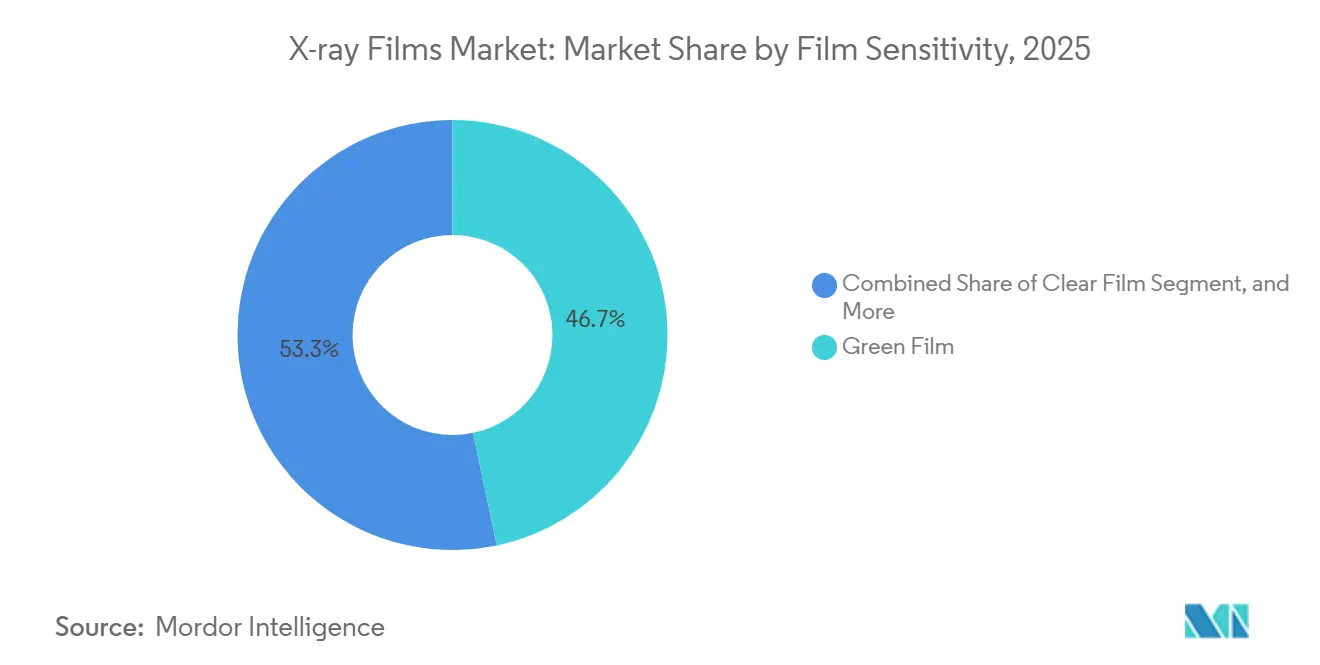

- By film sensitivity, green film captured 46.71% of 2025 sales, whereas clear film is set to expand at a 6.44% CAGR.

- By film size, the 14 × 17 inch format commanded 39.66% share in 2025, and the 8 × 10 inch segment is rising at a 6.67% CAGR.

- By geography, Asia-Pacific accounted for 52.39% of 2025 revenue, and Africa is poised to grow at a 6.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global X-ray Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continued adoption of traditional X-ray equipment in developing economies | +1.2% | Asia-Pacific, Africa, South America | Medium term (2-4 years) |

| Cost-effectiveness of film in low-resource settings | +0.9% | Africa, South Asia, Southeast Asia | Short term (≤ 2 years) |

| Ongoing demand for hard-copy imaging records for legal and clinical documentation | +0.6% | Global, concentrated in Middle East and Africa | Long term (≥ 4 years) |

| Expansion of industrial non-destructive testing requiring film radiography | +0.8% | North America, Europe, Asia-Pacific industrial hubs | Medium term (2-4 years) |

| Silver recovery economics improving film lifecycle value | +0.5% | Global, emphasis on Europe and North America | Long term (≥ 4 years) |

| Rising veterinary imaging volumes in emerging markets sustaining film demand | +0.4% | Asia-Pacific, South America, Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Continued Adoption of Traditional X-ray Equipment in Developing Economies

Limited capital, frequent power outages, and gaps in network infrastructure keep analog radiography viable in many hospitals across sub-Saharan Africa and rural South Asia. The World Health Organization reported in 2025 that fewer than half of facilities in the region had reliable electricity, making flat-panel detectors impractical.[1]World Health Organization, “Strengthening Medical Imaging Capacity in Resource-Limited Settings,” who.int Nigeria’s health authority noted that 82% of its functional X-ray units remained film-based in 2024 because digital conversion costs start at USD 80,000 per room. India’s Ayushman Bharat initiative links digital reports in urban centers, yet facilities in Uttar Pradesh, Bihar, and Jharkhand average under 12 hours of daily electricity, so film continues to bridge access gaps. Vendors that maintain local distribution and darkroom chemistry support, therefore, protect a durable segment of the X-ray films market. The result is a staggered adoption curve in which digital and analog technologies coexist well past 2031.

Cost-Effectiveness of Film in Low-Resource Settings

A complete film room, including a three-year supply of consumables, costs USD 25,000-40,000, far below the USD 80,000-350,000 outlay for computed or direct digital radiography, according to a 2024 IAEA guide.[2]International Atomic Energy Agency, “Implementation Guide for Diagnostic Radiology in Low- and Middle-Income Countries,” iaea.org Operating expenses for chemistry and silver recovery remain predictable, whereas digital suites impose annual software fees and hardware refresh cycles that exceed maintenance budgets in many public hospitals. The WHO found that only 28% of African countries run preventive maintenance programs for imaging equipment, resulting in 40-50% downtime on digital units, while film systems require only periodic cassette cleaning. Veterinary clinics and solo dental practices mirror this economics, keeping the X-ray film market active in service niches that large equipment suppliers seldom target. The financial delta strengthens short-term demand even as national procurement policies promote eventual digitization.

Expansion of Industrial Non-Destructive Testing Requiring Film Radiography

Regulated sectors such as aerospace, petrochemical, and nuclear power mandate film archives that must remain readable for up to 60 years. ASTM standards E1742 and E1815 specify film as the reference medium for weld inspection, turbine blade evaluation, and pressure vessel certification.[3]ASTM International, “Standard Practice for Radiographic Examination - E1742,” astm.org NASA’s inspection rules likewise call for film on critical launch-vehicle welds, and U.S. nuclear regulators retain film for reactor documentation. Field conditions heat, dust, and vibration, often degrade portable digital detectors, so contractors still load cassettes on pipelines from the Middle East to Southeast Asia. These codified requirements insulate a stable industrial slice of the X-ray films market and temper the pace of full digital substitution.

Silver Recovery Economics Improving Film Lifecycle Value

Radiographic film contains 1.5-2% silver, and closed-loop recovery yields 90-99% extraction efficiency. Spot silver averaged USD 24-28 per troy ounce in 2025, translating to USD 8-12 recovered per kilogram of processed film after costs. U.S. EPA rules cap silver in wastewater at 5 mg/L, prompting hospitals to hire recyclers that pay USD 3-6 per kilogram for exposed media, offsetting 15-25% of annual film purchases. European REACH regulations and China’s hazardous waste catalog further incentivize silver reclamation, making circular-economy economics a tangible tailwind for the X-ray films market. This revenue stream narrows the total cost gap with digital radiography and extends the relevance of film workflows, especially in industrial facilities that process high volumes of radiographs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift to digital radiography and flat-panel detector technology | -1.8% | North America, Europe, developed Asia-Pacific | Short term (≤ 2 years) |

| Environmental regulations on chemical processing and waste disposal | -0.7% | Europe, North America, Japan | Medium term (2-4 years) |

| Shrinking global supply chain for specialty film chemicals increasing costs | -0.5% | Global | Medium term (2-4 years) |

| Hospital decarbonization targets reducing film printer purchases | -0.4% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift to Digital Radiography and Flat-Panel Detector Technology

Digital radiography accounted for more than 70% of new installations in high-income regions by 2025, as hospitals prioritized faster workflows, lower patient dose, and cloud archiving. GE HealthCare’s planned USD 2.3 billion acquisition of Intelerad, announced in November 2025, underscores industry commitment to enterprise imaging platforms that bypass film entirely. Konica Minolta ended film production in 2015 and now codesigns AI algorithms with Vietnam’s National Innovation Center, illustrating a pivot from consumables to data-centric services. Reimbursement in the United States favors digital-ready outpatient centers, accelerating the retirement of analog rooms. These dynamics remove the highest-margin buyers from the X-ray films market and intensify price competition in remaining pockets of demand.

Environmental Regulations on Chemical Processing and Waste Disposal

Compliance burdens rise as regulators tighten limits on effluent from silver, lead, and cadmium. The European Union’s REACH framework requires closed-loop systems or costly licensed disposal, adding USD 0.15-0.30 per exposure to operating costs. Similar EPA thresholds in the United States force radiology departments that exceed 5 mg/L silver to register as hazardous-waste generators, with annual fees reaching USD 15,000 for mid-sized hospitals. Japan’s pollutant release law mandates public disclosure for facilities that fail to achieve 90% silver recovery, nudging them toward digital alternatives. These policies compress margins and challenge the long-term viability of wet-processing lines within the X-ray films market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Hospitals Dominate While Diagnostic Centers Accelerate

Hospitals commanded 59.23% of 2025 revenue, reflecting large analog installed bases and legal retention rules that still favor hard-copy records in many jurisdictions. Diagnostic centers, however, are advancing at a 6.72% CAGR as payers steer patients toward lower-cost outpatient imaging. This outpatient shift reallocates procedure volume and reshapes the demand profile for X-ray films.

Growth in independent diagnostic testing facilities from 7,000 units in 2018 to more than 11,000 in 2024 broadens the customer pool but also accelerates digital adoption, limiting upside from film. Research institutes and teaching hospitals preserve film rooms for protocol development, especially in low- and middle-income countries, while veterinary clinics in Asia-Pacific and South America use film because pet-owner reimbursements rarely cover digital upgrades. Industrial plants adhere to ASTM film standards, ensuring a stable, if specialized, slice of the X-ray films market for non-destructive testing applications.

By Film Type: Dry Film Expands Through Chemical-Free Processing

Dry film secured 57.78% of 2025 sales and is forecast to climb at a 5.82% CAGR as facilities retire darkrooms to meet environmental mandates. Thermal imaging removes developer and fixer chemicals, shortening turnaround times and aligning with hospital decarbonization targets set by organizations such as NHS England.

Wet film persists in resource-limited clinics that cannot fund USD 15,000-30,000 dry printers, and in industrial fieldwork where wet-processed images deliver marginally better contrast. Even so, dry film’s compliance advantages make it the preferred consumable in regulated markets, and its adoption supports a gradual yet steady shift in X-ray films market share from wet to dry modalities.

By Film Sensitivity: Clear Film Gains Ground in High-Resolution Tasks

Green film led the sensitivity segment in 2025, with a 46.71% share, as rare-earth screens paired with green emulsions reduced patient dose by up to 70%. Clear film, though, is advancing at a 6.44% CAGR, propelled by aerospace and dental practices that require 12-15 line pairs per millimeter resolution for micro-defect detection.

Industrial codes and NASA specifications call for clear film on critical welds, underscoring the demand, even as medical imaging tilts toward dose-efficient green emulsions. Half-speed and full-speed blue films decline as facilities upgrade their screens, yet veterinary and public health programs still consume blue stock where cost and throughput outweigh image-quality gains. The interplay of these preferences shapes the evolving dynamics of the X-ray films market size at the product level.

By Film Size: Standard Chest Format Still Leads, Small Cassettes Rise

The 14 × 17 inch sheet maintained a 39.66% share in 2025 because adult chest X-rays remain the world’s highest-volume radiographic exam. Smaller 8 × 10-inch sheets, however, are growing at a 6.67% CAGR, fueled by dental, extremity, and veterinary imaging, where reduced material use lowers per-study costs.

Intermediate sizes, such as 10 × 12 inches, support pediatric and portable imaging, while specialty dimensions cater to mammography and turbine-blade inspection. Format diversity enables suppliers to address niche use cases, preserving consumption across healthcare and industrial settings and reinforcing the overall resilience of the X-ray films market.

Geography Analysis

Asia-Pacific generated 52.39% of 2025 revenue, driven by China’s extensive stock of legacy X-ray units in rural hospitals and India’s ongoing reliance on film in states with unstable grids. Japan sustains demand through high imaging volumes, and local recyclers achieve silver recovery rates above 95%, which extends film economics.

Africa is the fastest-growing territory at a 6.61% CAGR. The African Development Bank highlights a USD 3-4 billion annual gap in imaging equipment, and WHO data show radiologist densities below 1 per million in one-third of nations, conditions that favor simple analog systems. Egypt recorded only 2.5 CT scanners per million in 2022, yet possessed 21 X-ray machines per million, underscoring the affordability advantage that supports the X-ray films market.

North America and Europe exhibit slower growth because digital penetration exceeds 70% of new sales, but industrial testing and veterinary practices still purchase film. South America, anchored by Brazil and Argentina, retains analog suites in public hospitals under budget constraints, and regulatory codes continue to recognize film as legal evidence. These regional contrasts ensure that no single adoption curve defines the global X-ray films market.

Competitive Landscape

The X-ray films market is moderately concentrated: Fujifilm Holdings, Agfa-Gevaert, Carestream Health, and Konica Minolta account for roughly 60-70% of global revenue. Fujifilm integrated Hitachi’s imaging business in 2021 for EUR 1.47 billion (USD 1.73 billion) to blend digital modalities with film consumables and service contracts. GE HealthCare’s 2025 agreement to buy Intelerad for USD 2.3 billion further pivots its portfolio toward cloud enterprise imaging and away from physical media.

Konica Minolta ceased film production in 2015, yet remains active in AI-enabled radiography, partnering with Vietnam’s innovation center in 2025 to develop digital respiratory diagnostics. Smaller suppliers, including China Lucky Film and Foma Bohemia, compete on price in emerging markets but lack regulatory credentials for aerospace and nuclear sectors. Canon Medical’s new U.S. headquarters in Cleveland will expedite research on X-ray systems, while Siemens Healthineers is expanding into molecular imaging, signaling long-term migration away from consumables.

Silver recovery contracts, industrial specifications, and veterinary demand still justify limited film lines, but overall strategic emphasis among multinationals is shifting toward detectors, software, and AI analytics. This dual approach keeps the X-ray films market viable in select segments while underscoring an inevitable tilt toward digital dominance.

X-ray Films Industry Leaders

Fujifilm Holdings Corporation

Konica Minolta Inc.

Agfa-Gevaert NV

Carestream Health Inc.

Sony Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: GE HealthCare agreed to acquire Intelerad Medical Systems for USD 2.3 billion, with closing expected in H1 2026.

- October 2025: Konica Minolta signed an MoU with Vietnam’s National Innovation Center and FPT Corporation to co-develop direct digital radiography and AI algorithms for respiratory care.

- February 2025: Canon Medical Systems purchased a Cleveland building to establish its U.S. headquarters and imaging innovation hub.

- February 2025: A multi-society position paper urged facilities to retire wet-film processing to cut carbon emissions by up to 2.5 kg CO₂-equivalent per exam.

Global X-ray Films Market Report Scope

The X-ray Films Market Report is Segmented by End User (Hospitals, Diagnostic Centers, Research and Academic Institutions, Veterinary Clinics, Industrial Facilities), Film Type (Dry Film, and Wet Film), Film Sensitivity (Green Film, Half-Speed Blue Film, Full-Speed Blue Film, Clear Film), Film Size (14×17 inch, 11×14 inch, 10×12 inch, 8×10 inch, Other Film Sizes), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Hospitals |

| Diagnostic Centers |

| Research and Academic Institutions |

| Veterinary Clinics |

| Industrial Facilities |

| Dry Film |

| Wet Film |

| Green Film |

| Half-Speed Blue Film |

| Full-Speed Blue Film |

| Clear Film |

| 14 × 17 inch |

| 11 × 14 inch |

| 10 × 12 inch |

| 8 × 10 inch |

| Other Film Sizes |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By End User | Hospitals | ||

| Diagnostic Centers | |||

| Research and Academic Institutions | |||

| Veterinary Clinics | |||

| Industrial Facilities | |||

| By Film Type | Dry Film | ||

| Wet Film | |||

| By Film Sensitivity | Green Film | ||

| Half-Speed Blue Film | |||

| Full-Speed Blue Film | |||

| Clear Film | |||

| By Film Size | 14 × 17 inch | ||

| 11 × 14 inch | |||

| 10 × 12 inch | |||

| 8 × 10 inch | |||

| Other Film Sizes | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the global X-ray film market in 2026?

The X-ray film market size stands at USD 2.04 billion in 2026.

What is the forecast CAGR for X-ray film through 2031?

Revenue is projected to rise at a 5.69% CAGR from 2026 to 2031.

Which region generates the most X-ray film revenue?

Asia-Pacific leads with 52.39% of global sales in 2025.

Which end-user segment is expanding the quickest?

Diagnostic centers are growing at a 6.72% CAGR as imaging shifts to outpatient settings.

Why does industry still use film despite digital alternatives?

Capital limits, industrial regulations that require archival films, and profitable silver recovery keep film economically relevant.

What environmental rules affect X-ray film users?

EPA and EU REACH regulations cap silver discharge and compel closed-loop recovery systems, raising compliance costs for wet processing.

Page last updated on: