Wound Closure Strips Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

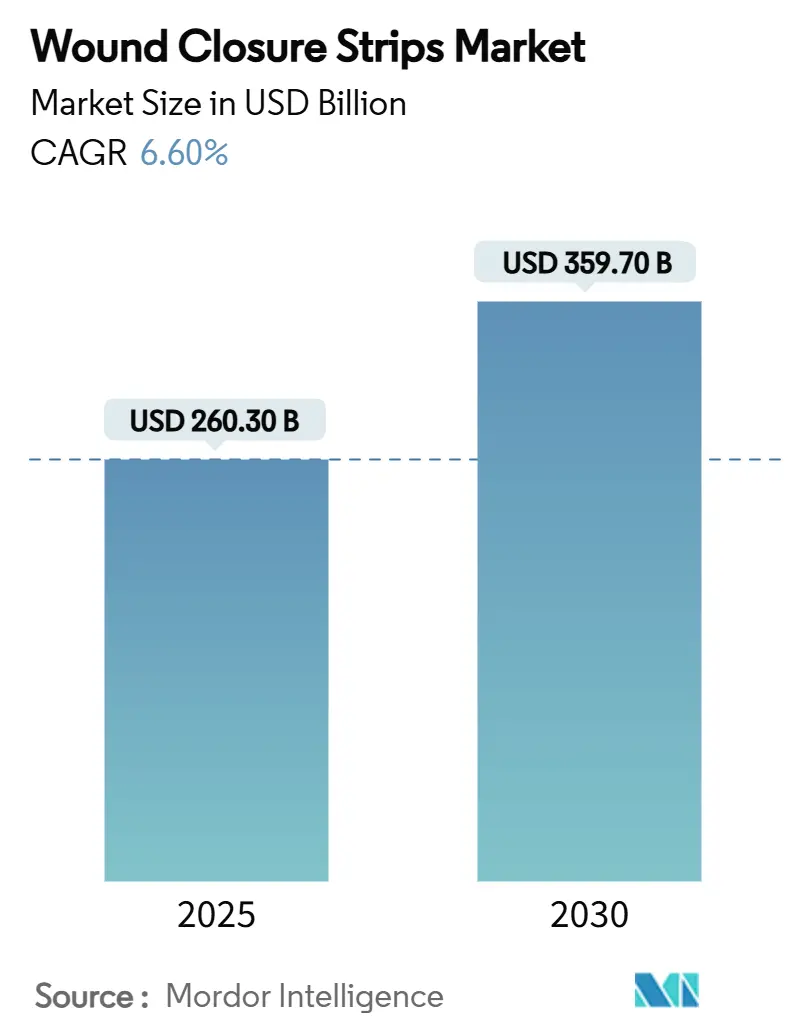

| Market Size (2025) | USD 260.30 Billion |

| Market Size (2030) | USD 359.70 Billion |

| Growth Rate (2025 - 2030) | 6.60% CAGR |

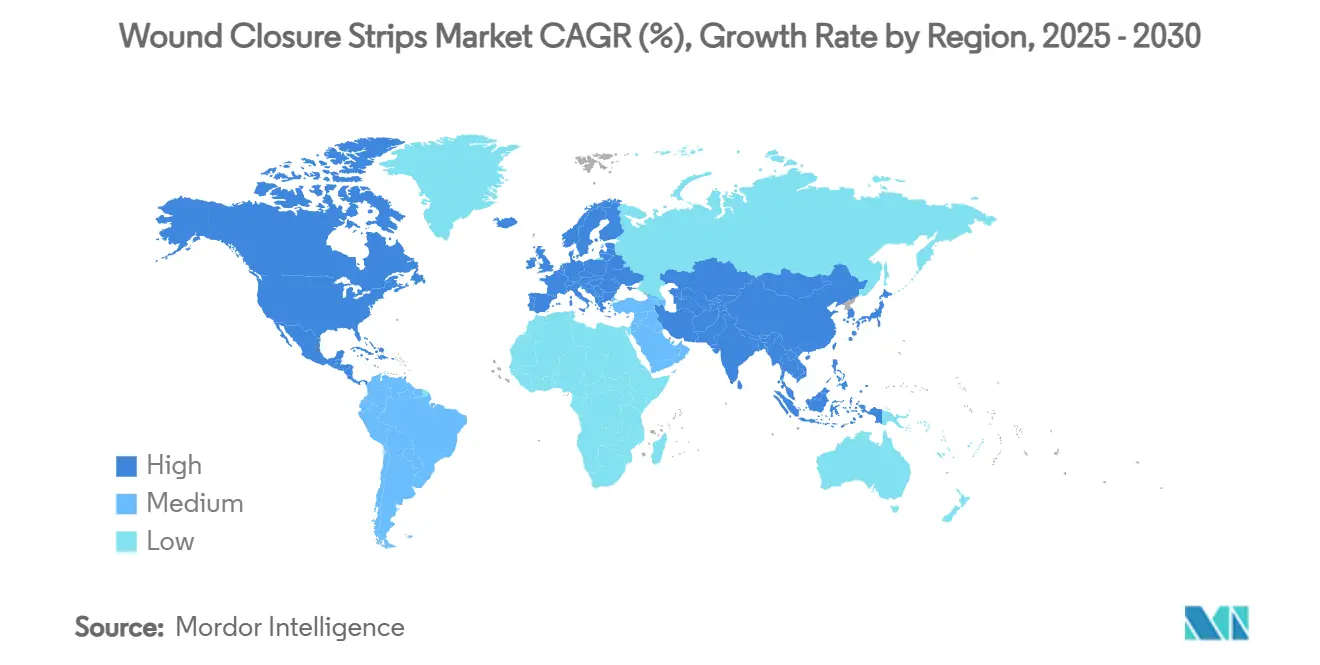

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wound Closure Strips Market Analysis by Mordor Intelligence

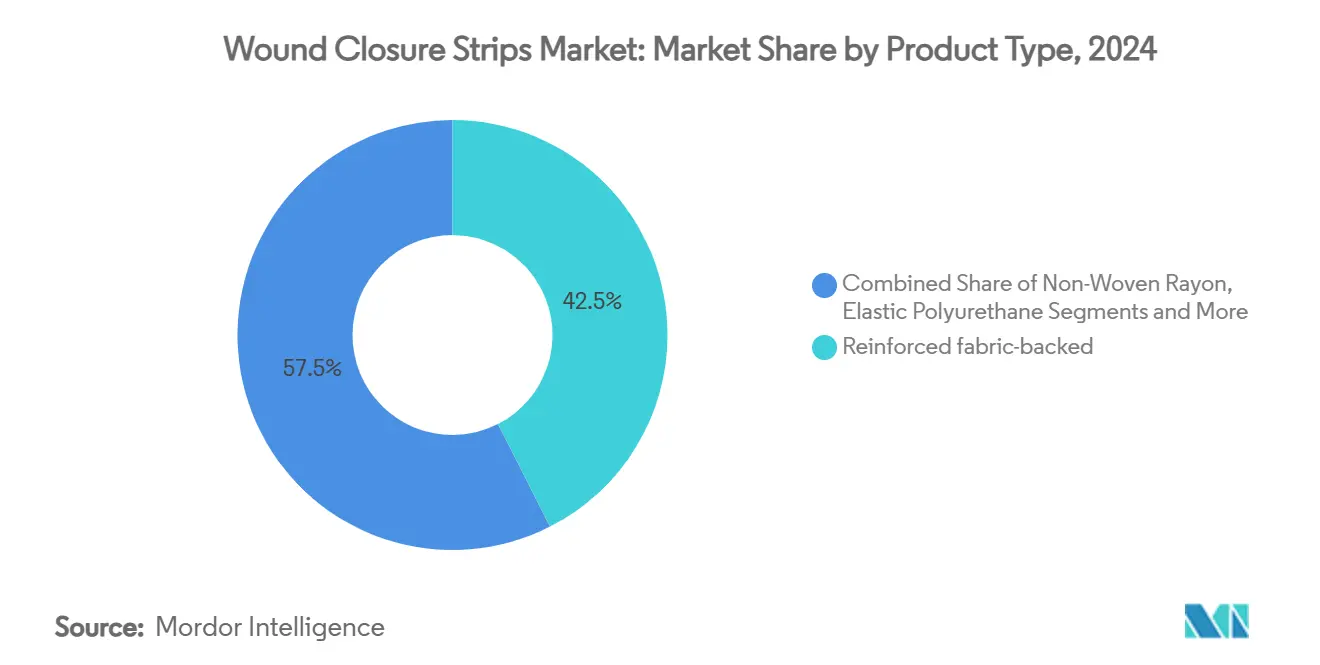

The wound closure strips market size is USD 260.3 million in 2025 and is on track to reach USD 359.7 million by 2030 at a 6.60% CAGR, underscoring resilient demand for advanced skin-closure solutions in operating rooms, emergency departments, and home-care settings. Heightened surgical procedure volumes, the rising incidence of chronic wounds, and sustained innovation in antimicrobial coatings keep the wound closure strips market firmly on a growth trajectory. North America accounts for the largest 38.1% share thanks to an extensive surgical infrastructure and favorable reimbursement. At the same time, Asia Pacific is the fastest-growing region at a 7.2% CAGR as diabetes and population aging accelerate regional demand. Reinforced fabric-backed products command 42.5% of the 2024 wound closure strips market share because surgeons value tensile strength in high-stress applications, yet antimicrobial-coated strips are the breakout offering with a 9.8% CAGR as hospitals intensify infection-prevention efforts. Acrylic adhesive chemistry remains dominant at 54.1% market share, though silicone-based alternatives are rising at 8.5% CAGR by minimizing medical adhesive–related skin injuries (MARSI) in fragile-skin cohorts.

Key Report Takeaways

- By product type, reinforced fabric-backed strips held 42.5% of the wound closure strips market share in 2024, and antimicrobial-coated variants are expanding at a 9.8% CAGR through 2030.

- By adhesive chemistry, acrylic formulations captured 54.1% of the wound closure strips market size in 2024, and silicone-based products are advancing at an 8.5% CAGR to 2030.

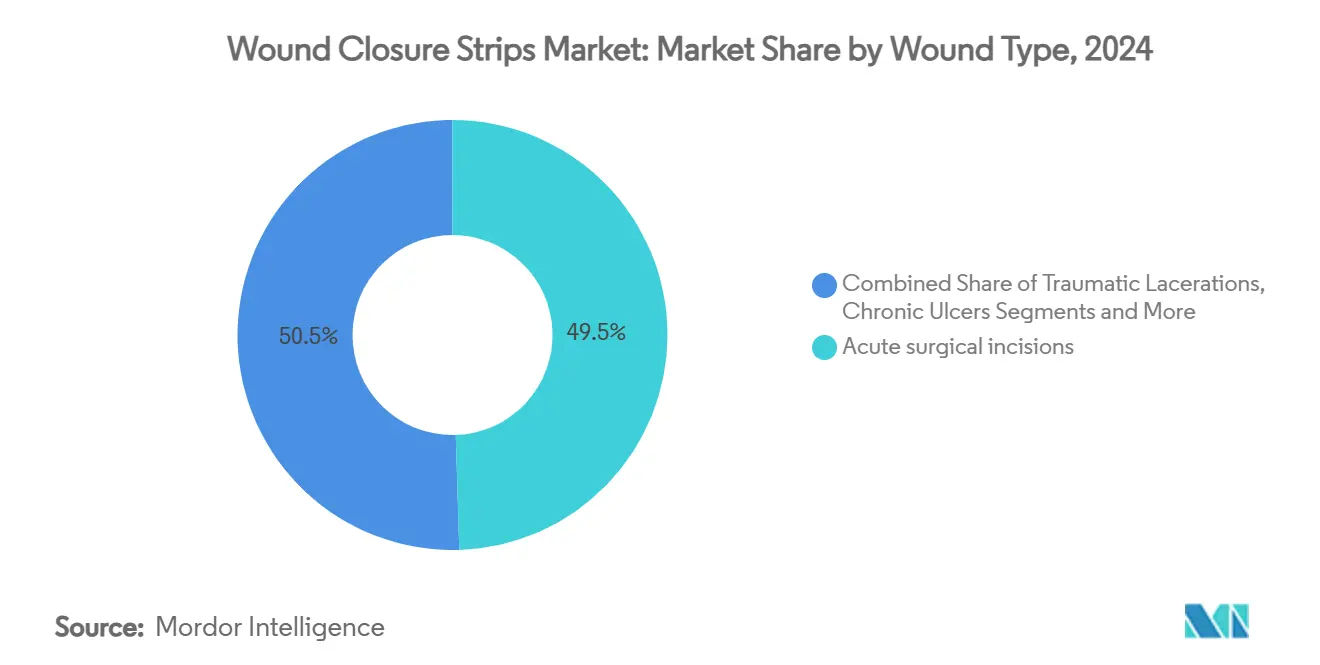

- By wound type, acute surgical incisions represented 49.5% of the wound closure strips market in 2024, and chronic ulcers were the fastest-growing segment, growing at 9.9% CAGR.

- By end user, hospitals accounted for 61.3% of the wound closure strips market size in 2024, while home-care settings are progressing at a 10.4% CAGR.

- By distribution channel, direct hospital supply maintained a 58.2% share in 2024, and e-commerce is growing at a 12.1% CAGR to 2030.

- By geography, North America led with a 38.1% share in 2024, and Asia Pacific is set to compound at a 7.2% CAGR through 2030.

Global Wound Closure Strips Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising surgical procedure volumes | +1.20% | North America, Europe, Global | Medium term (2-4 years) |

| Shift toward minimally invasive skin-closure | +0.90% | Developed markets, Global | Long term (≥ 4 years) |

| Growing burden of chronic & diabetic wounds | +1.50% | Asia Pacific, Global | Long term (≥ 4 years) |

| Expansion of outpatient & home-care settings | +1.10% | North America, Europe | Medium term (2-4 years) |

| Adoption of antimicrobial-impregnated strips | +0.80% | Developed markets, Global | Short term (≤ 2 years) |

| Integration with wearable wound sensors | +0.50% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Procedure Volumes

More than 3.3 million Medicare beneficiaries underwent ambulatory surgery in 2022, generating USD 6.1 billion in ASC spend and affirming sustained procedure growth that bolsters the wound closure strips market.[1]Medicare Payment Advisory Commission, “Report to the Congress: Medicare Payment Policy,” medpac.gov Hospitals and ASCs increasingly favor reinforced fabric-backed strips that deliver reliability in orthopedic and cardiovascular cases while decreasing closure time when compared with traditional sutures. The reimbursement differential between ASCs and hospital outpatient departments drives demand for cost-effective closures that reduce total procedure expenditure. As outpatient volumes continue to rise, manufacturers that offer bundled closure solutions and simplified clinical workflows are positioned to capture recurring revenue streams. The trend synchronizes with payer pressures to shorten inpatient stays without compromising wound healing quality.

Shift Toward Minimally Invasive Skin-Closure

Clinical studies show that liquid adhesives lower postoperative pain scores and analgesic intake versus conventional strips, leading to higher patient satisfaction regarding scar appearance. Novel zipper-type devices cut closure time by 298 seconds compared with sutures, which improves operating-room productivity in high-volume centers. Regulators have cleared next-generation cyanoacrylate adhesives for traumatic lacerations, and 3M is running multi-center trials to validate efficacy against existing products.[2]Centers for Medicare & Medicaid Services, “G230165-NCT06217081 Study Approval Notice,” cms.gov Minimal handling, faster application, and superior cosmetic outcomes align with surgeon priorities, sustaining momentum behind innovative closure chemistries. The demand for products that support early discharge and telehealth follow-up continues to climb, especially within same-day surgery programs.

Growing Burden of Chronic & Diabetic Wounds

Diabetic foot ulcers add USD 8.33 billion in yearly treatment outlays and carry a 17% amputation risk, driving the health-economic argument for infection-mitigating wound closure strips.[3]Ajaytaj Singh Sidhu, “Emerging Technologies for the Management of Diabetic Foot Ulceration: A Review,” Frontiers in Clinical Diabetes and Healthcare, frontiersin.org Infected ulcers cost EUR 4,888 (USD 5,350) per hospitalization and extend stays to 10 days. Chronic wounds now affect 88.7 per 10,000 inhabitants in primary care, costing EUR 34.99 million (USD 38.3 million) across three years in southern Barcelona alone. Antimicrobial-coated strips that curb bacterial colonization thus present clinicians with clinically and economically compelling benefits. Payers and providers increasingly emphasize early intervention to lower the probability of costly amputations and readmissions, channeling investment into advanced closure technologies.

Expansion of Outpatient & Home-Care Settings

CMS introduced specific payment codes for disposable negative-pressure wound therapy devices in the 2025 Home Health PPS, cementing advanced wound care’s role in community settings. Home-health nurses cite relationship continuity as a linchpin in wound healing, reinforcing the need for closure strips that are easy to monitor and adjust without clinical visits. Tele-wound platforms give remote specialists real-time visibility, and value-based payment models incentivize products that cut readmissions. With CMS imposing a 4.067% rate cut on 2025 home-health reimbursement, providers gravitate toward cost-efficient strips that still safeguard skin integrity. Growth in home-based chronic-wound programs remains strongest in urban hubs where nursing shortages make remote oversight critical.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement & price pressure | -1.80% | Developed markets, Global | Short term (≤ 2 years) |

| Adhesive-related dermatitis & allergies | -0.70% | Global | Medium term (2-4 years) |

| Supply risk for medical-grade non-wovens | -0.90% | Asia Pacific, Global | Short term (≤ 2 years) |

| Single-use plastic disposal regulations | -0.60% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reimbursement & Price Pressure

Medicare will cap skin-substitute graft use at 8 applications per 16 weeks starting February 2025, curbing overall wound-care billings and driving buyers toward lower-cost closure strips. The CY 2025 Physician Fee Schedule trims wound-care payments by 2.93%, creating immediate margin strain for providers. Group purchasing organizations consolidate orders, extracting deeper discounts and squeezing manufacturer pricing flexibility. Vendors that substantiate improved healing economics with real-world data will offset pricing pressure most effectively. Those dependent on premium list prices without demonstrable savings face formulary exclusion.

Adhesive-Related Dermatitis & Allergies

MARSI affects up to 1.5 million U.S. patients annually, and 10.4% of Steri-Strip users developed blisters, while none occurred with silk-based alternatives. Biomimetic and silk-fiber adhesives under development leverage natural polymers to cut dermatitis risk. Hospitals mandating MARSI-prevention protocols increasingly substitute silicone formulations for traditional acrylics. Additional costs from dermatitis include extended healing and infection susceptibility, elevating risk-management scrutiny in purchasing decisions. Pediatric and geriatric wards adopt hypoallergenic closures as soon as possible due to heightened skin fragility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Antimicrobial Innovation Drives Premium Growth

Reinforced fabric-backed strips delivered 42.5% market share in the 2024 wound closure strips market due to tensile performance in orthopedic and cardiothoracic incisions. Their reliability under high tension keeps them the preferred option where wound dehiscence risk is high. Cost-effective non-woven rayon products retain institutional appeal in routine applications while flexible polyurethane designs occupy niches requiring conformability across joints. In contrast, antimicrobial-coated strips are registering the fastest 9.8% CAGR as infection-prevention imperatives align with payer quality metrics. Bio-resorbable innovations further disrupt the wound closure strips market by removing procedure costs and aligning with sustainability goals.

Emerging tough adhesive puncture sealing (TAPS) constructs integrate swelling-triggered bioadhesion, combining suturing strength with rapid application advantages. Hospitals blending antimicrobial additives with reinforced substrates generate premium SKUs attractive to infection-control committees. Suppliers offering modular portfolios that enable surgeons to match tensile requirements and antimicrobial protection in a single SKU will enjoy stronger formulary positioning.

By Adhesive Chemistry: Silicone Gains Ground Despite Acrylic Dominance

Acrylic formulations anchored 54.1% market share in the wound closure strips market, leveraging decades of manufacturing scale and hospital acceptance. They remain the bulk choice where cost sensitivity prevails and patient skin is resilient. Hybrid dual-chemistry designs seek to merge acrylic holding power with silicone gentleness, underscoring the value of differentiation in a crowded shelf. Cyanoacrylate overlays are securing emergency-room shares as clinicians emphasize rapid barrier formation against contaminants.

Silicone products accelerate at 8.5% CAGR as health systems campaign against MARSI. Pediatric and geriatric units catalyze this switch because skin fragility amplifies adhesive trauma risk. Hydrocolloid variants remain pivotal in exudative chronic wounds that require moisture management. Vendors that document silicone’s lower total cost of care by avoiding dermatitis complications stand to penetrate value-based purchasing frameworks quickly.

By Wound Type: Chronic Ulcer Management Drives Innovation

Acute surgical incisions occupied 49.5% market share in the 2024 wound closure strips market size, reflecting procedures’ predictability and standardized protocols. Traumatic lacerations contribute steady revenue through emergency departments and urgent-care clinics. Chronic ulcers, however, post the highest 9.9% CAGR as diabetes prevalence multiplies and population aging elevates venous and pressure ulcer incidence. Infection-resistant strips that sustain closure across prolonged healing timelines gain prominence in diabetic foot and venous leg ulcers.

Burns and aesthetic procedures demand skin-tone-matching and minimally scarring adhesives for cosmetic satisfaction. FDA guidance encouraging pharma-device convergence in diabetic foot infection treatment invites hybrid therapeutic strip concepts that marry closure with localized antimicrobial or growth-factor delivery.

By End User: Home-Care Settings Reshape Market Dynamics

Direct hospital supply still represents 61.3% market share in the 2024 wound closure strips market size thanks to integrated inventory systems and consolidated spend. Group purchasing organizations scale leverage, lowering per-unit prices and raising entry barriers for small entrants. Retail and hospital pharmacies bridge institutional and over-the-counter demand for minor injuries.

E-commerce records a 12.1% CAGR, spurred by pandemic-era normalization of online medical procurement and heightened price transparency. Digital platforms allow vendors to reach home-health patients directly, bypassing traditional intermediaries and offering subscription replenishment models for chronic users. Manufacturers must fortify last-mile cold-chain and sterile-pack fulfillment capabilities to preserve integrity during parcel transit.

Geography Analysis

North America commands 38.1% revenue share in 2024 as surgeons adopt premium antimicrobial strips and health plans reimburse advanced wound closure technologies. Europe follows closely, underpinned by aging demographics and universal coverage schemes that guarantee baseline access. The wound closure strips market size for Asia Pacific is USD 66.4 million in 2024 and is primed to expand to USD 100.2 million by 2030 on a 7.2% CAGR.

China and India jointly contribute more than half of the regional volume as surgical capacity scales nationwide and diabetes prevalence escalates. Japan differentiates itself with rigorous clinical guidelines that incorporate imaging and systemic antibiotic stewardship for diabetic ulcers, spurring uptake of infection-defense closures.

Middle East & Africa and South America remain nascent, yet gradual infrastructure build-out and growing awareness of chronic-wound burdens are set to unlock demand, particularly through public-sector tenders.

Competitive Landscape

Moderate fragmentation defines the wound closure strips market as global majors 3M, Johnson & Johnson (Ethicon), and Smith & Nephew compete on technology breadth, clinical validation, and supply dependability. 3M’s USD 8.2 billion spin-off, Solventum, dedicates capital to wound-closure R&D, enabling faster go-to-market cycles for sensor-integrated strips. Johnson & Johnson leverages its Ethicon suture legacy to cross-sell hybrid adhesive-suture offerings in integrated procedural bundles. Smith & Nephew’s 12-Point Plan prioritizes margin recovery and product launches such as GRAFIX Plus, broadening its advanced wound portfolio.

Mid-tier suppliers pursue acquisitive growth: H.B. Fuller acquired Medifill and agreed to buy GEM S.r.l. to secure European production bases in medical adhesives. OptMed’s TearRepair skin protectant targets MARSI prevention, highlighting niche specialists’ focus on unaddressed pain points. Competitive intensity is rising as smart-bandage startups partner with established strip makers to leverage distribution reach while supplying sensor IP. Market participants differentiating through integrated digital monitoring or superior biocompatibility will carve out a durable share in hospital value-analysis committees.

Strategic alliances with research institutions advance next-generation chemistries. For example, Penn State’s graphene sensor collaboration positions early movers to commercialize telemetry-enabled closures. Successful players will translate R&D into scalable manufacturing—an area where conglomerates with sterilization networks and global logistics have an advantage.

Wound Closure Strips Industry Leaders

3M Company

Smith & Nephew plc

Medtronic plc

Johnson & Johnson

B. Braun Melsungen AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The FDA classified bacterial-protease sensors in chronic wound fluid as Class II devices, streamlining smart-bandage approvals.

- December 2024: H.B. Fuller completed the acquisition of Medifill Ltd. and signed a provisional agreement to buy GEM S.r.l. to build a European medical-adhesive hub.

- October 2024: OptMed received FDA 510(k) clearance for TearRepair Liquid Skin Protectant aimed at MARSI prevention.

- August 2024: FDA approved Resivant Medical’s tissue adhesive platform, expanding physician choice in rapid skin-closure alternatives.

Global Wound Closure Strips Market Report Scope

| Reinforced Fabric-Backed Strips |

| Non-Woven Rayon Strips |

| Elastic Polyurethane Strips |

| Antimicrobial-Coated Strips |

| Bio-Resorbable Strips |

| Acrylic |

| Silicone |

| Hydrocolloid |

| Hybrid (Dual-Acrylic/Silicone) |

| Cyanoacrylate Overlay |

| Acute Surgical Incisions |

| Traumatic Lacerations |

| Chronic Ulcers |

| Burns |

| Cosmetic Procedures |

| Hospitals |

| Ambulatory Surgical Centers (ASCs) |

| Specialty Clinics |

| Home-Care Settings |

| Military & Emergency Services |

| Direct Hospital Supply |

| Retail & Hospital Pharmacies |

| E-Commerce & Online Pharmacies |

| Group Purchasing Organizations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Reinforced Fabric-Backed Strips | |

| Non-Woven Rayon Strips | ||

| Elastic Polyurethane Strips | ||

| Antimicrobial-Coated Strips | ||

| Bio-Resorbable Strips | ||

| By Adhesive Chemistry | Acrylic | |

| Silicone | ||

| Hydrocolloid | ||

| Hybrid (Dual-Acrylic/Silicone) | ||

| Cyanoacrylate Overlay | ||

| By Wound Type | Acute Surgical Incisions | |

| Traumatic Lacerations | ||

| Chronic Ulcers | ||

| Burns | ||

| Cosmetic Procedures | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers (ASCs) | ||

| Specialty Clinics | ||

| Home-Care Settings | ||

| Military & Emergency Services | ||

| By Distribution Channel | Direct Hospital Supply | |

| Retail & Hospital Pharmacies | ||

| E-Commerce & Online Pharmacies | ||

| Group Purchasing Organizations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected wound closure strips market size by 2030?

The wound closure strips market is expected to reach USD 359.7 million by 2030 on a 6.60% CAGR.

Which product category is growing the fastest in the wound closure strips market?

Antimicrobial-coated strips lead growth with a 9.8% CAGR through 2030 as hospitals prioritize infection prevention.

Why are silicone-based adhesives gaining traction over acrylic formulations?

Silicone reduces medical adhesive–related skin injuries, making it the preferred option for fragile-skin patients while still expanding at an 8.5% CAGR.

Which geographic region offers the highest growth potential?

Asia Pacific shows the fastest expansion at a 7.2% CAGR, driven by rising diabetes prevalence and healthcare modernization.

How are home-care trends influencing demand?

CMS incentives for community-based wound management are pushing home-care settings to a 10.4% CAGR, boosting demand for user-friendly closure strips.

What competitive strategies are market leaders using to maintain share?

Key players invest in antimicrobial technologies, sensor-integrated strips, and strategic acquisitions to widen product portfolios and reinforce global distribution.

Page last updated on: