Wireless Charging IC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

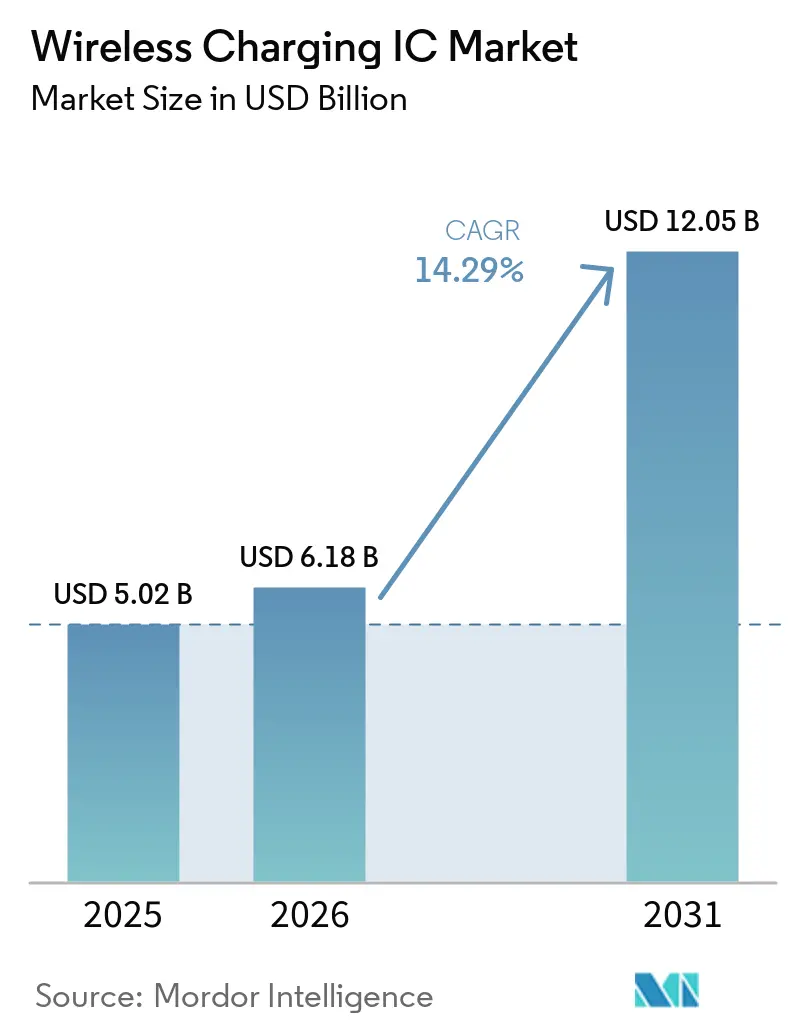

| Market Size (2026) | USD 6.18 Billion |

| Market Size (2031) | USD 12.05 Billion |

| Growth Rate (2026 - 2031) | 14.29% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wireless Charging IC Market Analysis by Mordor Intelligence

The wireless charging IC market size was valued at USD 5.02 billion in 2025 and estimated to grow from USD 6.18 billion in 2026 to reach USD 12.05 billion by 2031, at a CAGR of 14.29% during the forecast period (2026-2031). Mainstream smartphone platforms, factory-floor robots, and in-cabin automotive systems are moving rapidly from optional cordless power to default designs, compressing product cycles and increasing annual unit volumes. Receiver IC miniaturization, the launch of the Qi2 25 W profile, and regulatory support for port-less devices are heightening demand in cost-sensitive mid-tier handsets, while industrial integrators are paying premium prices for ruggedized transmitters that eliminate downtime. Vendors are also benefiting from automakers standardizing 15 W pads across 2026 model years, a trend that stabilizes long-term supply contracts and locks in AEC-Q100-qualified portfolios. Venture-funded far-field startups and gallium nitride power stages are expanding the technology stack, yet electromagnetic interference hurdles above 65 W continue to slow notebook adoption and keep high-power sockets in the proof-of-concept stage.

Key Report Takeaways

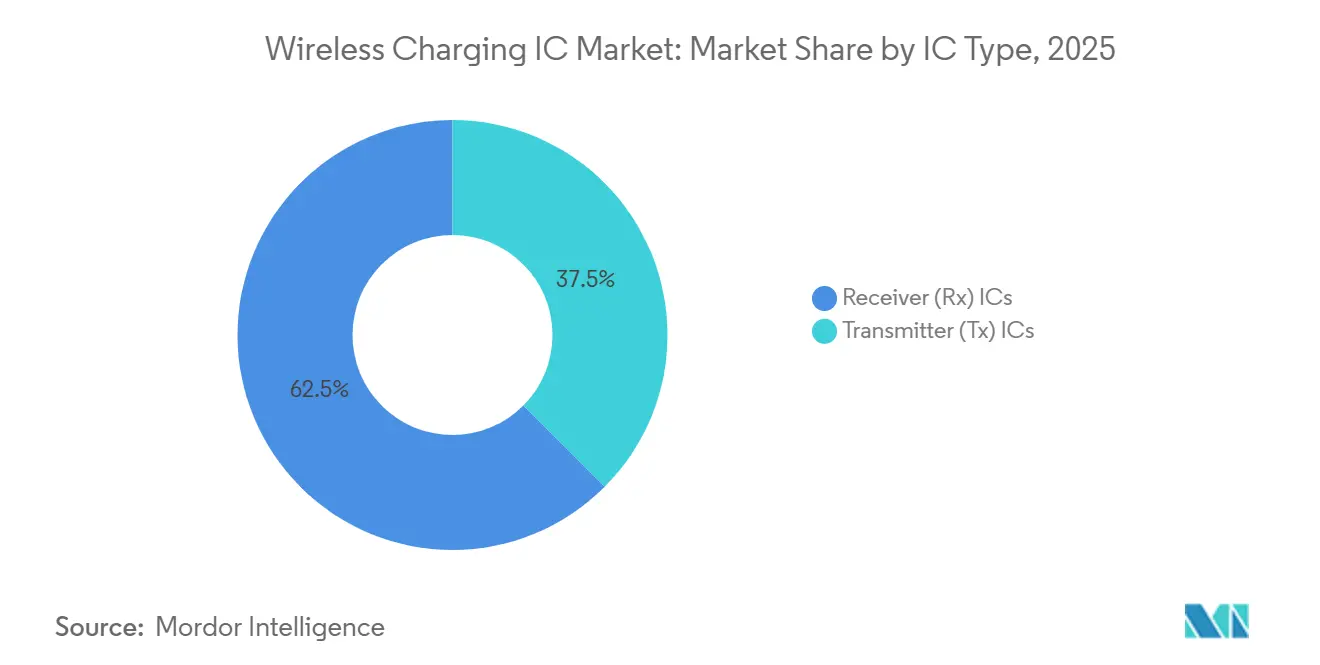

- By IC type, receiver ICs led the wireless charging IC market with 62.52% market share in 2025, posting a CAGR of 15.4%.

- By power rating, low-power solutions below 20 W captured 46.56% of the wireless charging IC market in 2025, and the high-power (more than 100 W) segment is likely to grow at a CAGR of 18.6%.

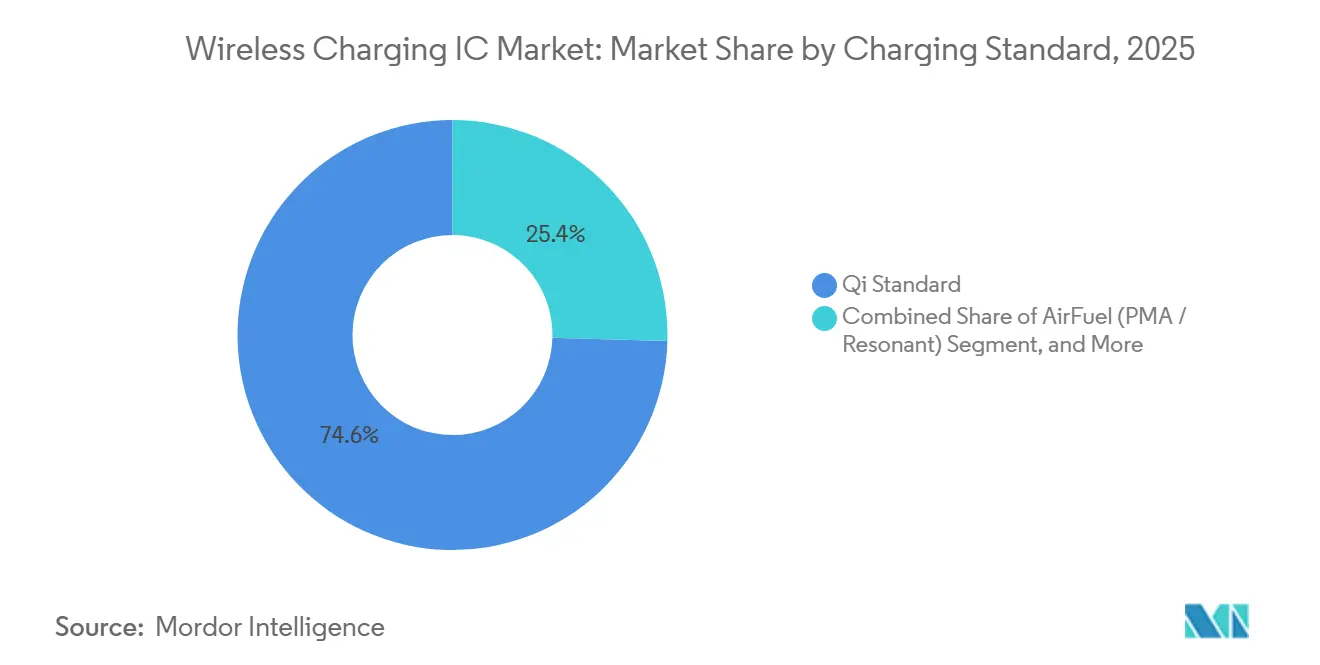

- By charging standard, the Qi standard commanded 75.31% of the wireless charging IC market in 2025, while AirFuel is expanding at a 16.2% CAGR through 2031.

- By application, smartphones and tablets accounted for 50.73% of the wireless charging IC market size in 2025, and industrial and IoT devices are advancing at a 14.8% CAGR through 2031.

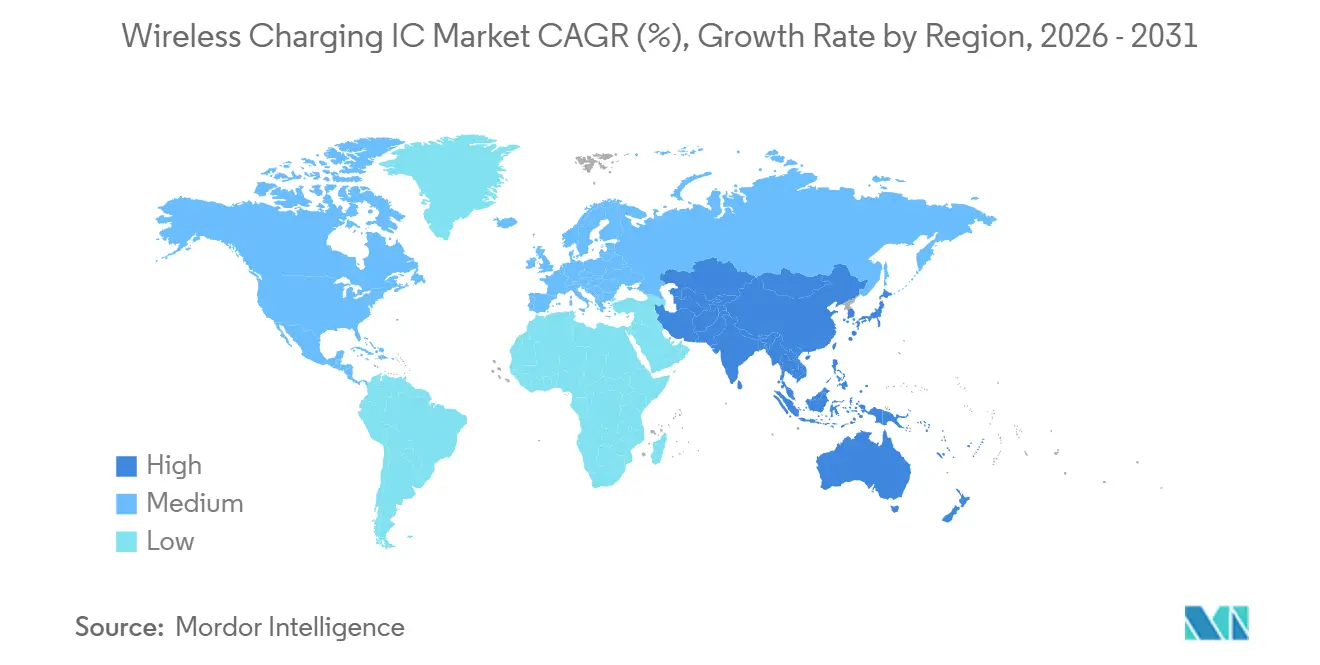

- By geography, Asia-Pacific held 47.81% of the wireless charging IC market share in 2025 and is expected to grow at the fastest 15.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wireless Charging IC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Attach-Rates of Wireless Charging in Flagship and Mid-Tier Smartphones | +3.5% | Global, highest in Asia-Pacific and North America | Medium term (2-4 years) |

| Regulatory Push for Port-Less Devices, EU Common Charger Directive and China IPX8 Compliance | +2.8% | Europe and China core, spillover to North America | Short term (≤ 2 years) |

| Automakers Adopting In-Cabin Inductive Pads as a Standard Comfort Feature | +2.5% | Global, early gains in North America, Europe and Japan | Medium term (2-4 years) |

| Rapid Adoption of 15-50 W Wireless Charging in Industrial Handhelds and AMRs | +2.0% | North America and Europe hubs, expanding to Asia-Pacific | Medium term (2-4 years) |

| Miniaturized Rx ICs Enabling Sub-1 W Trickle Charging for Wearables and Hearables | +1.8% | Global, led by Asia-Pacific manufacturing | Short term (- 2 years) |

| Venture Funding into mm-Wave Far-Field Power-Beaming Startups | +1.2% | North America and Europe venture ecosystems | Long term (-4 years) |

| Source: Mordor Intelligence | |||

Expanding Attach-Rates of Wireless Charging in Flagship and Mid-Tier Smartphones

The Wireless Power Consortium certified more than 1,200 Qi2 products in 2025, enabling magnetic alignment that reduces misposition losses to under 5% and allows receiver ICs to shrink without thermal penalties.[1]Wireless Power Consortium, “Qi2 Certification and Product Database,” WIRELESSPOWERCONSORTIUM.COM Samsung, Google, and Apple each committed to Qi2 across their 2026 portfolios, normalizing feature sets and moving competition toward software-defined power profiles and foreign-object detection. China’s Xiaomi, OPPO, and vivo are pushing 50 W pads into devices priced below USD 500, multiplying receiver volumes while compressing average selling prices. Silicon Source’s 2.0 mm-square GY5502 enables boards to power batteries from true wireless stereo earbuds to tablets without redesign, reinforcing economies of scale.[2]Silicon Source, “GY5502 Datasheet,” SILICONSOURCE.COM As attach-rates percolate through mid-tier lines, shipment elasticity more than offsets unit price erosion, sustaining revenue momentum for the wireless charging IC market.

Regulatory Push for Port-Less Devices, EU Common Charger Directive and China IPX8 Compliance

Mandate M/607 sets a March 2027 deadline for interoperable cordless charging across the European Union, driving transmitter IC vendors to prioritize Qi2 certification over proprietary extensions.[3]European Commission, “Mandate M/607 for Wireless Charging Standardization,” EC.EUROPA.EU Ecodesign Regulation 2025/2052 further caps standby power at 0.80 W, compelling integrated controllers with sub-µA quiescent current and dynamic load detection.[4]Official Journal of the European Union, “Regulation 2025/2052 on Ecodesign Requirements,” EUR-LEX.EUROPA.EU China’s updated EMC project 20240568-T-339 tightens emission limits and accelerates the shift to sealed, IPX8-rated enclosures that can only recharge wirelessly. These converging statutes raise barriers for legacy wired connectors and fix wireless power as the default energy pathway for next-generation portable electronics. Vendors with multi-protocol negotiation stacks gain leverage because OEMs now require single-chip solutions that span Qi1.x, Qi2, and emerging AirFuel extensions without redesign.

Automakers Adopting In-Cabin Inductive Pads as a Standard Comfort Feature

Nissan confirmed 15 W Qi2 pads with active cooling for the 2026 Pathfinder and Murano, turning a premium add-on into a mass-market baseline. Panasonic Automotive’s moving-coil architecture removes two passive coils, cuts bill-of-materials costs by roughly 25%, and lets drivers drop phones at any angle. Infineon’s silicon-carbide modules demonstrated 200 kW dynamic charging for buses in December 2025, hinting at a continuum between cabin convenience and road-embedded infrastructure. Carmakers favor AEC-Q100-qualified chipsets and ISO 26262 support, discouraging small fabless entrants and reinforcing scale economics for incumbents. As 12 V auxiliary batteries migrate to 48 V architectures, transmitter ICs that integrate gallium nitride drivers capture additional value by simplifying power-domain design.

Rapid adoption of 15 W-50 W wireless charging in industrial handhelds and AMRs

Delta Electronics’ MOOVair suite, spanning 1 kW-30 kW, posted high efficiency in 24/7 factory duty, underpinning the business case for connector-less robots. Wiferion’s 1 kW CW1000 slashed downtime for automotive assembly AMRs from the higher side to below 5% during 2025 deployments. OMRON’s OL-450S pushes 60 A to ruggedized scanners, matching wired throughput while halving maintenance visits. KUKA documented 99% robot availability after removing plug-in charging, bringing payback to under 18 months for high-utilization cells. Industrial buyers are willing to pay three to five times consumer IC prices to secure MIL-STD-810 qualification and IEC 61000 immunity, yielding high-margin niches that insulate the wireless charging IC market from smartphone seasonality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EMI Compliance Failures Above 65 W Limiting Notebook Design Wins | -1.5% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Fragmented Proprietary Standards Leading to OEM Supply-Chain Lock-Ins | -1.8% | Global | Medium term (2-4 years) |

| Thermal Runaway Incidents in High-Density Coil IC Stacks Greater Than 30 W | -1.0% | Global, high-power pockets | Short term (≤ 2 years) |

| Raw-Material Price Volatility for GaN and Litz-Wire Substrates | -0.9% | Global, Asia-Pacific supply chain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EMI Compliance Failures Above 65 W Limiting Notebook Design Wins

Thin-profile laptops that target 65 W cordless fast-charge struggle to meet FCC Part 15 and CISPR 32 Class B harmonics because metal chassis amplify 80-300 kHz coil switching energies. Spread-spectrum and active-cancellation silicon pushes die size up to 20%, lifting transmitter IC cost curves while still failing to pass radiated immunity on the first attempt. Certification cycles can double to 20 weeks, eroding OEM release calendars and tilting preference back toward USB-C Power Delivery. Transmitter suppliers that master embedded shielding and intelligent phase dithering will secure early wins, yet most road maps now defer 100 W inductive notebooks until at least 2028, trimming near-term growth for the wireless charging IC market.

Fragmented Proprietary Standards Leading to OEM Supply-Chain Lock-Ins

Qualcomm Quick Charge, Samsung Fast Wireless 2.0, and Xiaomi 50 W protocols each mandate distinct handshake algorithms, forcing accessory makers either to license multiple stacks or risk consumer confusion. A multi-mode receiver controller inflates material bills by approximately USD 2.50, a painful surcharge in mid-tier smartphones. x devices demand backward compatibility for another five to seven years, perpetuating protocol bloat. Until the Institute of Electrical and Electronics Engineers or the International Telecommunication Union mandates a single global scheme, OEMs will juggle diverse firmware branches and carry redundant inventories, which chips away at the long-run CAGR for the wireless charging IC market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By IC Type: Receiver Dominance Anchors Smartphone Volumes

Receiver ICs accounted for 62.52% of the wireless charging IC market share in 2025 and are set to grow at a 15.4% CAGR through 2031. That trajectory stems from billions of smartphones, smartwatches, and in-cabin modules that refresh every 18-24 months, compared with five-year cycles for pads and docks. Receiver miniaturization now extends to 2.0 × 2.0 mm chip-scale packages, allowing designers to embed power management into smart rings without enlarging the enclosure. Epson’s 0.1 W wafer-level die extends the reach to energy-harvesting sensors. Transmitter ICs command premium prices because they integrate gallium-nitride drivers, metal-oxide sensors for foreign-object detection, and sometimes Bluetooth Low Energy links for pad-to-phone authentication, but their numbers scale with furniture and automotive production, not handset volumes. Gallium-nitride devices boost efficiency from 88% to 95% while requiring smaller heat sinks, yet they expose OEMs to GaN wafer price swings that test hedging strategies.

A small pool of automotive-qualified suppliers limits choice for cabin transmitters, raising margins but increasing qualification lead times. In wearables, designers must comply with IEEE C95.1-specific absorption limits, putting pressure on receiver firmware to throttle current gracefully during near-field exposure. These contrasting design constraints keep the wireless charging IC market balanced: transmitter vendors pursue value over volume, while receiver vendors chase scale and wafer cost reductions. The asymmetry should persist until road-embedded inductive infrastructure deploys widely, at which point high-power transmitters may overtake hand-held receivers in revenue terms.

By Power Rating: High-Power Segment Leads Growth Despite Technical Hurdles

Low-power sub-20 W devices accounted for 46.56% of the wireless charging IC market in 2025, driven by smartphones and earbuds that charge daily on bedroom pads. Medium-power systems between 20 W and 100 W cater to tablets and automotive consoles and benefit from mature thermal stacks. High-power classes above 100 W will post the fastest 18.6% CAGR through 2031, as industrial robots and electric buses demand kilowatt-scale top-ups. Delta Electronics’ 30 kW MOOVair dock sustained 95% efficiency in 2025 trials, matching cable benchmarks. Infineon’s WLC1150 transmitter integrates active EMI cancellation, reducing radiated noise by 10 dB, and meets automotive EMC requirements without external shields. Yet thermal runaway events in 30-60 W smartphone stacks forced redesigns that delayed several 2025 flagships, proving that heat density remains a gating factor.

Notebook programs aiming for 65 W pads still fail FCC radiated tests half the time, provoking an industry-wide pivot toward 45 W “safe-harbor” modes. Vendors are combining power negotiation, foreign-object detection, and temperature telemetry in a single microcontroller to shorten validation loops, but silicon real estate increases by 15% as a result. Succeeding in high-power categories, therefore, depends on multidisciplinary expertise thermals, EMC, and firmware not just silicon scaling, a barrier that consolidates opportunity among diversified semiconductor houses.

By Charging Standard: Qi Dominance Faces AirFuel Disruption in Industrial Niches

The Qi ecosystem maintained a 75.31% share of the wireless charging IC market in 2025, propelled by more than 1,200 certified accessories and the marketing clout of Apple, Samsung, and Google. July 2025’s Qi2 launch added 25 W magnetic alignment, shrinking mis-position losses to under 5%. AirFuel resonant coupling, operating at 6.78 MHz, tolerates wider gaps and multiple receivers, making it attractive for mobile robots that dock imprecisely. Consequently, AirFuel chipsets are forecast to expand at a 16.2% CAGR to 2031, albeit from a small base. Panasonic Automotive has shown that its moving-coil transmitter can achieve Qi2 active alignment with a single coil rather than three, slashing pad costs and narrowing AirFuel’s spatial-freedom advantage.

Proprietary 50 W extensions from Xiaomi or Quick Charge Wireless from Qualcomm offer headline speed but fracture aftermarket compatibility, compelling IC vendors to embed multi-protocol handshakes, which raise firmware complexity and patent-royalty overhead. Looking ahead, Europe’s harmonization drive under mandate M/607 could unify consumer standards by 2027, but medical and industrial verticals may still favor AirFuel for its multi-device coverage and looser alignment requirements, preserving a dual-standard landscape for the wireless charging IC industry.

By Application: Industrial IoT Outpaces Smartphones in Growth Velocity

Smartphones and tablets captured 50.50% of 2025 revenue, yet their annual unit growth is single-digit, whereas industrial and IoT nodes are accelerating at a 14.8% CAGR to 2031. Autonomous mobile robots recharge opportunistically throughout a shift, quadrupling pad utilization compared with overnight phone charging. WIFERION demonstrated that AMRs reach 99% availability once inductive docks replace plug-in bays, a payback that convinces factory managers to absorb higher IC costs. Wearables rely on miniaturized receivers such as INVENTVM’s IVM5300, which delivers 97% efficiency and extends ring battery autonomy by leveraging sub-1 W trickle modes. Medical devices from Implantica harness cordless power to avoid infection pathways, with IEEE researchers recording 75% efficiency for 3 W pacemaker links.

Automotive cabins transition from optional accessory to standard equipment, illustrated by Nissan’s 2026 Pathfinder rollout. Tablets fixed on forklift dashboards and rugged scanners in distribution centers recharge at 50 W through sealed housings, cutting maintenance hours. Collectively, these use cases diversify the wireless charging IC market beyond consumer gadgets and provide revenue ballast when handset refresh rates dip.

Geography Analysis

Asia-Pacific dominated the wireless charging IC market with 47.81% share in 2025, underpinned by China’s handset assembly clusters, Japan’s tier-one automotive suppliers, and South Korea’s vertically integrated electronics champions. Xiaomi, OPPO, and vivo keep pushing 50 W standards into sub-USD 500 phones, multiplying receiver demand while squeezing gross margins. Panasonic Automotive, headquartered in Japan, has shipped more than 10 million moving-coil units and stands to scale further as Qi2 permeates 2026 automotive refresh cycles. Samsung’s pledge for full-portfolio Qi2 adoption reorganizes the supply base toward software-centric power management. Raw-copper volatility, however, can swing Litz-wire coil costs by double-digit percentages each quarter, prompting Asian suppliers to secure multi-year contracts and explore aluminum-clad alternatives.

Asia-Pacific is projected to register the fastest CAGR of 15.30% through 2031, supported by the region's dominant smartphone manufacturing ecosystem, expanding electric vehicle production, and increasing adoption of Qi-enabled consumer devices. China, South Korea, Taiwan, and Japan continue to strengthen demand for wireless charging ICs through investments in semiconductor manufacturing, premium consumer electronics, and automotive electronics. Additionally, the growing deployment of wireless charging in wearables, industrial IoT devices, and smart home products is reinforcing Asia-Pacific's position as the largest and fastest-growing regional market.

Europe accelerates cordless adoption through the Common Charger Directive and the 0.80 W Ecodesign standby cap, yet repeated EMI failures above 65 W delay notebook launches. Mandate M/607 forces chipmakers to prove multi-standard interoperability, lifting research and development intensity and favoring firms with large compliance budgets. Infineon’s silicon-carbide modules powering Electreon’s 200 kW road strips in Sweden exemplify the region’s ambition to bring inductive charging to fleet infrastructure. While the Middle East and Africa grow from a smaller base at a significant CAGR, smart-city pilots in Dubai and Riyadh include cord-free bus stops and street furniture. Latin America gains from automotive manufacturing in Brazil and Mexico, where crossover SUVs now list Qi2 pads as standard; nonetheless, currency swings temper consumer electronics penetration.

Competitive Landscape

Texas Instruments, NXP Semiconductors, STMicroelectronics, Renesas Electronics, and Infineon Technologies collectively accounted for more than half of revenue in 2025, giving the market moderate concentration and ensuring incumbents retain pricing leverage for automotive-grade and Qi-certified receivers. Texas Instruments’ plan to absorb Silicon Labs extends its reach from power management into connectivity microcontrollers, creating integrated reference designs that may raise switching costs for OEMs. Renesas, propelled by its Dialog Semiconductor and Panthronics acquisitions, now cross-sells NFC and Qi2 controllers into payment terminals, diversifying beyond smartphone cyclicality.

High-power and far-field niches remain fragmented. NuVolta claims a 100 W smartphone chipset that regulators have yet to clear above 30 W due to thermal concerns, underscoring the difficulty of scaling while adhering to IEC 62368 safety envelopes. Energous and Powercast lead sub-watt RF beaming, having secured FCC nods, but still face consumer skepticism over efficiency and health. Ossia’s Cota platform secured a rare FCC approval without distance limits, yet delivers microwatt-level power, restricting it to low-duty sensors. Compliance overhead under ISO 26262 for vehicles and IEC 60601 for medical gear pushes startups to partner with larger fabs that already maintain safety infrastructure, reinforcing the advantage of established houses in the wireless charging IC industry.

Incumbents invest heavily in gallium-nitride fabrication, foreign-object detection algorithms and integrated thermal monitors. Such vertical depth shortens validation for OEMs and consolidates wallet share, even as tier-two fabless entrants target cost-sensitive Android mid-tiers with minimalist dies. The outcome is a bifurcated field: a concentrated premium cluster dominating automotive and industrial sockets, and a long tail competing on die area and package footprint.

Wireless Charging IC Industry Leaders

Renesas Electronics Corporation

NXP Semiconductors N.V.

Texas Instruments Incorporated

Infineon Technologies AG

Qualcomm Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ROHM Semiconductor released the ML7670 and ML7671, a single-die fusion of 250 mW wireless charging and NFC aimed at payment terminals and access-control readers.

- February 2026: Texas Instruments unveiled a USD 7.5 billion cash agreement to acquire Silicon Labs, positioning the merged entity to integrate wireless power with connectivity chipsets.

- February 2026: Nissan confirmed Qi2 pads with active cooling in the 2026 Pathfinder and Murano, moving 15 W wireless charging into mainstream SUV trims.

- December 2025: Energous secured EU conformity for its 2 W PowerBridge Pro far-field transmitter, opening room-scale beaming for IoT sensors.

Global Wireless Charging IC Market Report Scope

The Wireless Charging IC Market Report is Segmented by IC Type (Receiver ICs and Transmitter ICs), Power Rating (Low Power (Less Than 20W), Medium Power 20-100W, and High Power (More Than 100W)), Charging Standard (Qi Standard, Airfuel PMA/Resonant, and Other Charging Standards), Application (Smartphones/Tablets, Automotive In-Cabin, Industrial and IoT Devices, and Medical Devices), and Geography (North America, Europe, Asia-Pacific, and Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Receiver (Rx) ICs |

| Transmitter (Tx) ICs |

| Low Power (Less than 20 W) |

| Medium Power (20-100 W) |

| High Power (More than 100 W) |

| Qi Standard |

| AirFuel (PMA / Resonant) |

| Other Charging Standards |

| Smartphones and Tablets |

| Wearables and Hearables |

| Automotive (In-cabin) |

| Industrial and IoT Devices |

| Medical Devices |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | |

| South America |

| By IC Type | Receiver (Rx) ICs | |

| Transmitter (Tx) ICs | ||

| By Power Rating | Low Power (Less than 20 W) | |

| Medium Power (20-100 W) | ||

| High Power (More than 100 W) | ||

| By Charging Standard | Qi Standard | |

| AirFuel (PMA / Resonant) | ||

| Other Charging Standards | ||

| By Application | Smartphones and Tablets | |

| Wearables and Hearables | ||

| Automotive (In-cabin) | ||

| Industrial and IoT Devices | ||

| Medical Devices | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | ||

| South America | ||

Key Questions Answered in the Report

How large will the wireless charging IC market be by 2031?

The wireless charging IC market size is projected to reach USD 12.05 billion by 2031, expanding at a 14.29% CAGR from 2026 to 2031.

Which segment currently ships the most wireless charging ICs?

Receiver ICs, embedded in smartphones and wearables, captured 62.52% wireless charging IC market share in 2025.

What is the fastest-growing power class within wireless charging ICs?

High-power solutions above 100 W are forecast to rise at a 18.6% CAGR to 2031, driven by industrial robots and electric-vehicle infrastructure.

Which standard dominates wireless charging today?

The Qi standard controlled 75.31% of 2025 revenue, and its Qi2 update with 25 W magnetic alignment is widening that ecosystem.

Why is North America attractive for suppliers?

Automotive OEM adoption of Qi2, industrial AMR deployments and VC-backed far-field startups are expected to lift North Americas revenue through 2031.

Which companies lead the competitive landscape?

Texas Instruments, NXP Semiconductors, STMicroelectronics, Renesas Electronics and Infineon Technologies together held 65% of 2025 revenue, giving them scale advantages in automotive and industrial sockets.

Page last updated on: