Battery Management IC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

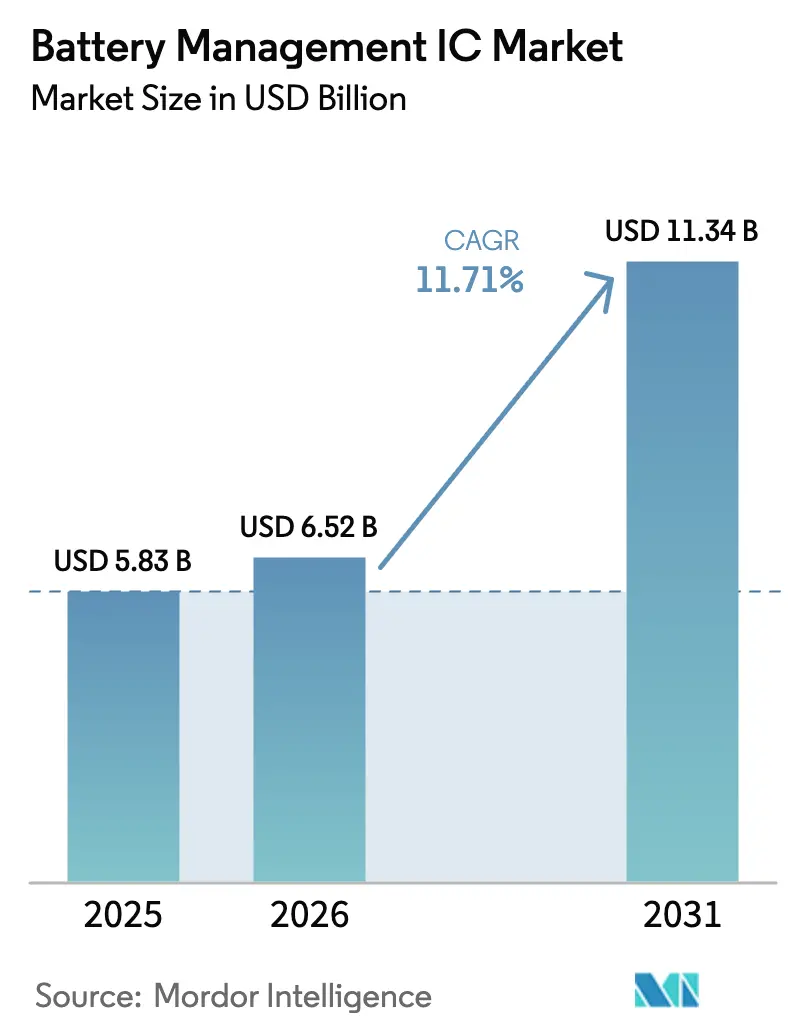

| Market Size (2026) | USD 6.52 Billion |

| Market Size (2031) | USD 11.34 Billion |

| Growth Rate (2026 - 2031) | 11.71% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players_(1).webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Battery Management IC Market Analysis by Mordor Intelligence

The battery management IC market size reached USD 6.52 billion in 2026 and is projected to advance to USD 11.34 billion by 2031, reflecting an 11.71% CAGR over the forecast period. Growth stems from rapid electric-vehicle adoption, a wider ecosystem of mobile and wearable devices, and the commercial viability of second-life energy-storage projects. Authentication IC demand is surging as automakers impose anti-counterfeit safeguards, while multi-cell monitor and charger ICs are being redesigned for 800-volt platforms that rely on silicon-carbide and gallium-nitride power semiconductors. A technology race among incumbents with deep analog expertise is underway to meet tighter functional-safety, cybersecurity, and voltage-handling requirements. Consequently, the battery management IC market is evolving into a platform-centric arena in which software, analytics, and wireless connectivity determine long-term differentiation.

Key Report Takeaways

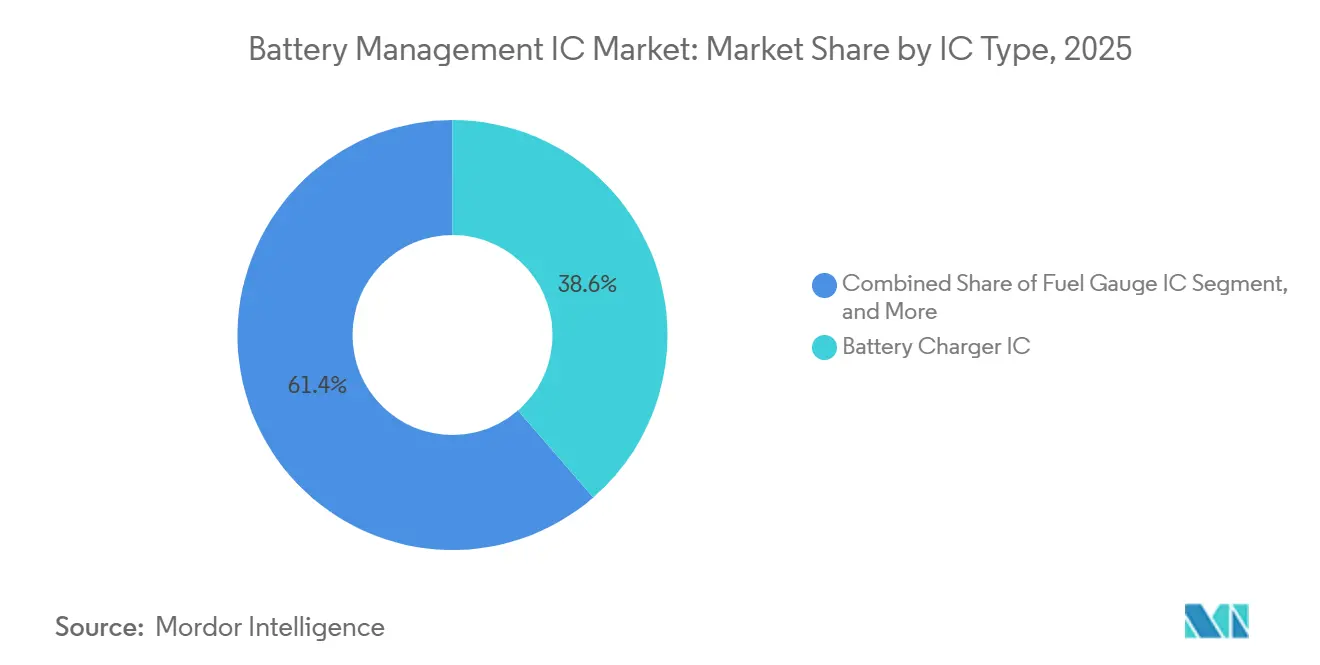

- By IC type, battery charger ICs led with a 38.63% share of the battery management IC market in 2025, whereas authentication ICs are set to expand at a 12.34% CAGR through 2031.

- By chemistry, lithium-ion accounted for 71.74% of the battery management IC market share in 2025 and is on track to grow at a 13.11% CAGR to 2031.

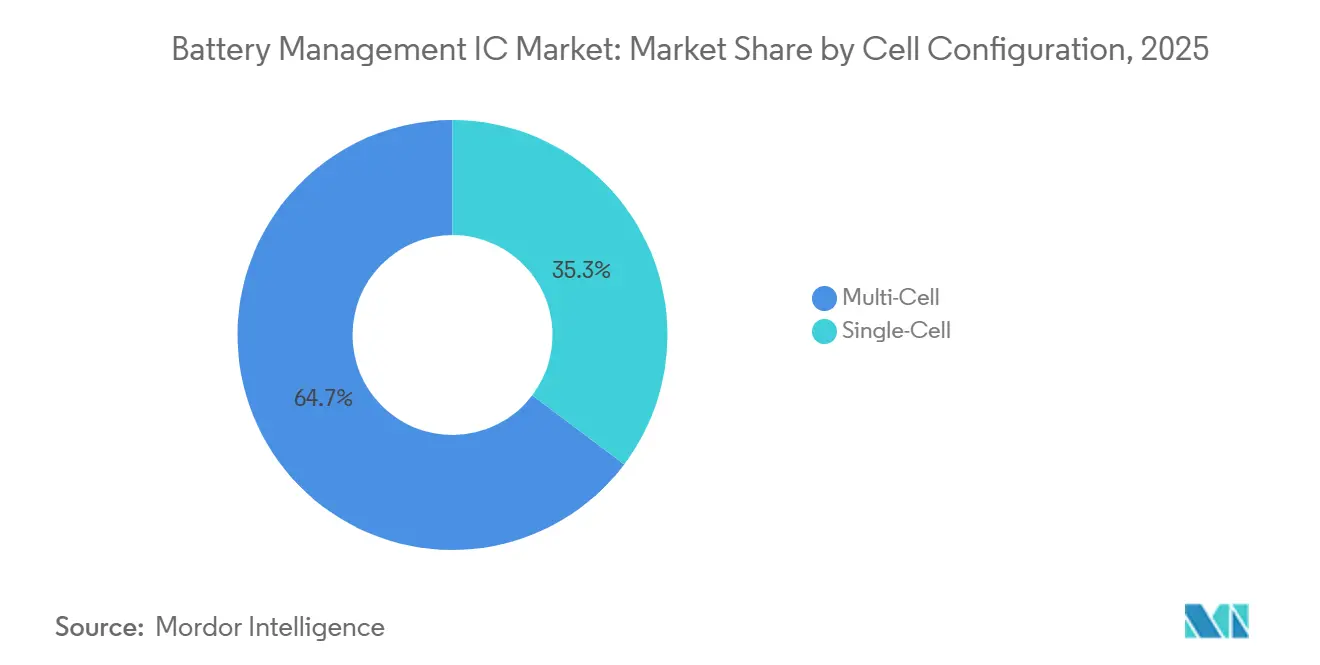

- By cell configuration, multi-cell systems captured 64.72% of the battery management IC market size in 2025 and will register a 12.78% CAGR over the forecast window.

- By end-use industry, the automotive sector held 28.73% of the battery management IC market share in 2025, while energy-storage systems represented the fastest-growing segment at a 12.66% CAGR from 2026 to 2031.

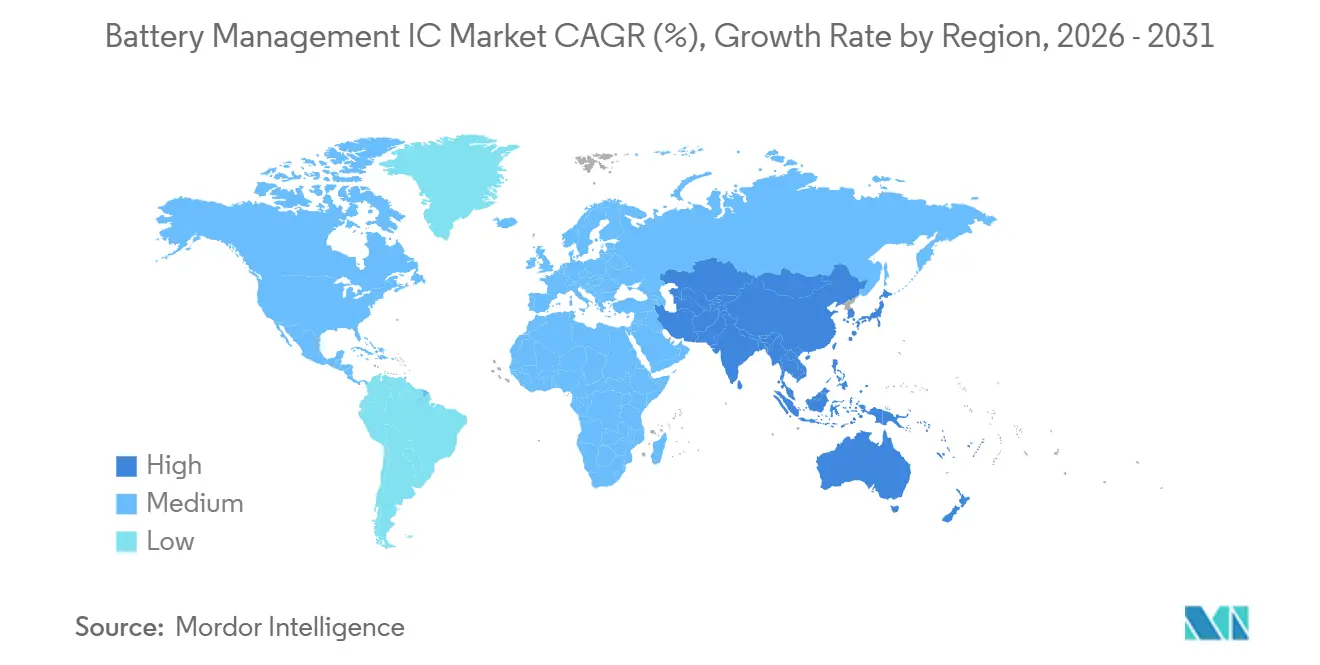

- By geography, North America held 38.73% of the battery management IC market share in 2025, while Asia-Pacific represents the fastest-rising user base at a 12.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Battery Management IC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging EV production commitments | +3.2% | Global, with concentration in China, Europe, North America | Medium term (2-4 years) |

| Rising adoption of mobile and wearable devices | +2.1% | Global, led by Asia Pacific and North America | Short term (≤ 2 years) |

| Regulatory push for battery-safety IC integration | +1.8% | Europe and North America, expanding to ASEAN | Medium term (2-4 years) |

| 48-volt mild-hybrid commercial vehicles boom | +1.5% | North America, Europe, China commercial-vehicle corridors | Short term (≤ 2 years) |

| Second-life stationary storage deployments | +1.3% | Europe, North America, Japan | Long term (≥ 4 years) |

| SiC/GaN transition enabling high-voltage chargers | +1.2% | Global, early adoption in premium EV segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging EV Production Commitments

Automakers publicly committed to building more than 30 million battery-electric vehicles per year by 2030. Fulfilling those targets requires roughly 120 million multi-cell controllers annually, as each pack integrates both module-level and pack-level devices. Original equipment manufacturers now specify cryptographic authentication ICs to exclude counterfeit cells that previously triggered costly warranty claims.[1]General Motors Company, “2024 Annual Report,” gm.com Cell-to-pack architectures, pioneered by Tesla, eliminate intermediate modules and consolidate battery-management intelligence into fewer yet more sophisticated ICs, capable of supervising as many as 400 series cells. Vendors able to blend high-voltage analog front-ends, digital signal processing, and wireless transceivers on the same die are increasingly preferred partners.

Rising Adoption of Mobile and Wearable Devices

Global smartphone shipments stabilized at more than 1 billion units during 2025, but higher energy demand from 5G radios and AI-enhanced imaging accelerated battery degradation. Device brands responded by integrating adaptive fuel-gauge ICs that learn from user behavior to tighten state-of-charge estimates. Apple extended the trend by requiring third-party repair shops to install batteries embedded with authentication ICs that interface with its iOS diagnostic framework. More than 500 million wearable devices shipped in 2025, each needing miniaturized protection and monitoring circuits to maximize runtime. Foldable phones and flexible batteries introduce new failure modes, driving demand for impedance-spectroscopy-enabled monitor ICs able to detect internal swelling before catastrophic events.

Regulatory Push for Battery-Safety IC Integration

The European Union Battery Regulation, phased in from 2024, requires portable batteries exceeding 2 kWh to incorporate management electronics that report the state of health and cycle count.[2]European Commission Directorate-General, “Battery Regulation Implementation,” ec.europa.eu California’s Right-to-Repair statute complements this mandate by granting service technicians data access while simultaneously compelling manufacturers to secure that pathway through authentication. Updated standards, such as IEC 62619, require fault interruption in under 200 milliseconds, a capability that is most easily achieved via integrated protection ICs. The upshot is a regulatory flywheel that turns compliance into design-win criteria for battery management IC vendors.

48-Volt Mild-Hybrid Commercial Vehicles Boom

With stricter emissions ceilings, truck and bus makers fitted 1.5 million vehicles with 48-volt systems in 2025, 40% more than in 2024. Belt-starter generators and dual-voltage accessories recoup braking energy, lowering diesel consumption by up to 5% on urban duty cycles.[3]Daimler Truck AG, “2024 Sustainability Report,” daimlertruck.com These hybrids rely on charger ICs that tolerate regenerative currents above 100 A and on multi-cell monitors that maintain millivolt-level balance across pouch cells exposed to vibration and temperature extremes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex integration in advanced SoCs | -1.4% | Global, pronounced in consumer electronics | Short term (≤ 2 years) |

| Raw-material price volatility | -1.1% | Global, supply-chain dependencies in Asia Pacific | Medium term (2-4 years) |

| Shortage of battery-test qualification capacity | -0.9% | North America, Europe, China | Short term (≤ 2 years) |

| Rising cybersecurity certification costs | -0.7% | Europe, North America, expanding to Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Integration in Advanced SoCs

Smartphone and notebook platforms have begun integrating battery-charging and gauging functions into application processors to conserve board space and reduce costs. Qualcomm’s Snapdragon and Apple’s M-series incorporate on-die power-management blocks, trimming external component count by as much as 15%. While the shift benefits large silicon houses capable of mixed-signal co-design, it squeezes stand-alone IC suppliers that lack tight foundry and ecosystem partnerships. Maintaining 1% coulomb-counting accuracy on digital-noise-heavy silicon remains challenging, necessitating iterative mask spins that increase R&D expenses.

Raw-Material Price Volatility

Spot prices for lithium carbonate swung between USD 10,000 and USD 25,000 per metric ton during 2024-2025. Sudden cost increases ripple down to battery-cell orders, dampening near-term IC demand because suppliers ship components several weeks before assembly. Cobalt and nickel price shocks compel cathode makers to reformulate chemistries, altering voltage profiles and accelerating validation cycles for monitor and protection ICs. Vendors must therefore hedge revenue exposure through diversified application portfolios able to absorb automotive slowdowns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By IC Type: Authentication IC Momentum Counters Counterfeits

Authentication devices are set to expand at a 12.34% CAGR, the fastest among all categories, as brands deploy cryptographic handshakes to block counterfeit batteries that triggered recalls and lawsuits in 2024. Battery charger ICs, while still holding the largest 2025 revenue slice at 38.63%, face slower growth because system-on-chip designs now integrate fundamental charging logic. Fuel-gauge ICs maintain relevance where 1% accuracy is life-critical, notably in infusion pumps and delivery drones monitored by aviation regulators.

Protection ICs, the oldest category, continue to serve single-cell applications in consumer electronics, yet their revenue is stagnant as device manufacturers shift to integrated solutions. Texas Instruments introduced an authentication IC in 2024 that employs SHA-256 cryptographic hashing to verify battery provenance, a feature that LG Energy Solution mandated for all replacement cells sold through authorized service centers. Consequently, the battery management IC market is rewarding suppliers that wrap silicon with secure firmware, reference designs, and cloud analytics, rather than those that ship catalog parts alone.

By Battery Chemistry: Lithium-Ion Dominance Deepens

Lithium-ion variants represented 71.74% of 2025 revenue and are on a trajectory to widen their footprint at a 13.11% CAGR. Energy-density gains, cost reductions, and improvements in recycling infrastructure reinforce the chemistry’s hegemony. Lithium iron phosphate blends, prized for their thermal stability, are widening their use in commercial trucks and stationary storage. However, their flatter voltage curves complicate state-of-charge estimation, prompting a demand for algorithm-rich monitor ICs.

Cutting-edge cells, such as CATL’s Qilin or Panasonic’s 4680, create new electrical signatures, including quicker transient responses and higher spine temperatures, that must be tracked every few milliseconds. IC vendors aligning early with those cell innovators can secure multi-year design wins that directly translate into gains in battery management IC market share. Solid-state batteries remain pre-commercial but underline the need for future-proof architectures that can measure impedance and ionic resistance, a capability a handful of suppliers are prototyping with university partners.

By Cell Configuration: Multi-Cell Platforms Gain Two-Thirds Share

Multi-cell designs captured 64.72% of the 2025 revenue and are expected to expand at a 12.78% CAGR, as 400-volt and 800-volt traction batteries dominate passenger-car and light-truck platforms. Tighter cell-to-cell matching down to 10 mV is crucial to unlocking the promised kilometers per charge, so automakers purchase monitor ICs that offer hardware balancing and redundant temperature sensing.

Single-cell consumer devices continue to use simpler protection ICs, yet emerging two-wheeler markets in Southeast Asia adopt 10- to 20-cell packs that sit between smartphone and EV complexity. Vendors are releasing cost-optimized monitor ICs targeting these mid-range voltages, aiming to defend margins in a segment where price elasticity is high. Wireless management, now headed toward automotive production, may cascade into power-tool and e-bike packs next, shaving gram-level weight from handheld devices and adding another layer of battery management IC market growth.

By End-Use Industry: Automotive Commands a Significant Share

Automotive’s 28.73% 2025 share is underpinned by 14-million unit global EV sales that are tracking toward 30 million units in 2030. High-voltage architectures, bidirectional charging and stringent functional-safety norms amplify controller complexity and dollar content per vehicle, reinforcing the centrality of automotive to the battery management IC market.

Consumer electronics remain the volume leader in units, but face slowed replacement cycles, nudging vendors to develop combo PMICs that bundle charging, gauging, and protection in a single die. Energy-storage systems represent the fastest-rising vertical, such as residential batteries attached to rooftop PV, while grid-scale projects mitigate renewable intermittency. Battery cabinets often employ Ethernet-based distributed architectures that rely on daisy-chained monitor ICs to coordinate megawatt-hour arrays. The convergence of vehicle-to-home functionality further blurs the boundary between industry and automotive, enabling cross-segment reuse of common silicon blocks.

Geography Analysis

North America commanded 38.73% of 2025 revenue, lifted by the Inflation Reduction Act’s local-content incentives that encourage U.S. battery cell production and provide certainty for semiconductor sourcing. Detroit-area automakers locked in multi-year supply agreements with Texas Instruments and Analog Devices, guaranteeing domestic fabrication capacity for Automotive Safety Integrity Level D devices. Canada’s lithium-hydroxide refineries and Mexico’s growing EV assembly base create regional supply-chain density that shortens lead times and lowers inventory buffers, stabilizing the North American battery management IC market.

Asia Pacific is projected to post a 12.74% CAGR, the fastest among regions, due to the sheer scale of China’s gigafactory pipeline and the technical leadership of Japanese and South Korean material suppliers. ASEAN nations add momentum as two-wheeler electrification gathers pace, favoring simplified monitor ICs tuned for tropical climates. India’s production-linked incentive program for advanced chemistry cells, budgeted at USD 2.4 billion, is set to spur domestic IC demand around 2027 when planned 20 GWh plants reach volume.

Europe enforces the strictest regulatory environment, mandating digital battery passports and recycled-content thresholds that require authentication and extensive logging. Gigafactory consortia such as Volkswagen PowerCo-Northvolt-ACC are building more than 200 GWh of capacity by 2030, a pipeline translating into tens of millions of high-voltage controllers per year. Meanwhile, Middle East and African microgrid deployments and African off-grid solar kits represent niche openings where cost-sensitive single-cell monitors dominate. Collectively, geographic diversification cushions suppliers against regional policy swings and commodity shocks, a resilience critical as the battery management IC market enters its next consolidation phase.

Competitive Landscape

The competitive field shows moderate concentration and the top five vendors held most of the 2025 revenue. Each maintains proprietary analog process nodes, functional-safety IP, and field-application-engineering teams that serve as entry barriers. Nevertheless, smaller fabless entrants exploit algorithmic differentiation, pushing machine-learning state-of-health analytics that outperform legacy coulomb counters under cell aging and variable temperature conditions. Patent filings in wireless battery monitoring increased 40% year-over-year in 2024, underscoring the anticipated shift away from heavy harnesses.

Established vendors are bundling silicon with cloud dashboards, calibration tools, and over-the-air firmware frameworks, turning one-time component sales into service subscriptions. Infineon’s partnership with software supplier Elektrobit typifies the shift toward complete platforms where secure boot, data logging, and functional-safety diagnostics come pre-integrated. Meanwhile, the rising cost of ISO 26262 and ISO 21434 compliance deters greenfield competition but also raises the capital intensity curve, encouraging joint ventures and IP licensing models.

Wireless battery management, authentication fusion and ultra-high-voltage compatibility constitute the next battlegrounds. Success will depend on mastering mixed-signal co-design, embedding encryption engines without heavy current draw, and proving lifetime accuracy in pack-level deployments well past 1,500 cycles. Companies that solve those challenges can convert design wins into durable battery management IC market share as electric mobility and energy storage scale over the decade.

Battery Management IC Industry Leaders

Renesas Electronics Corporation

NXP Semiconductors N.V

Analog Devices, Inc.

STMicroelectronics N.V.

Microchip Technology Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Texas Instruments allocated USD 300 million to expand its Richardson, Texas analog fab dedicated to ISO 26262-certified battery management ICs.

- November 2025: Analog Devices and General Motors began production ramp of wireless battery management on the Ultium platform, cutting pack wiring by 90% and assembly time by 25%.

- October 2025: STMicroelectronics released the L9963E multi-cell monitor supporting 14-series cells and 800-volt stacks with ASIL-D compliance.

- September 2025: NXP Semiconductors unveiled the MC33777 authentication IC using elliptic-curve cryptography, with design wins at three global automakers.

Global Battery Management IC Market Report Scope

The Battery Management IC Market Report is Segmented by IC Type (Fuel Gauge IC, Battery Charger IC, Authentication IC, Battery Monitor IC, Protection IC), Battery Chemistry (Lithium-Ion, Lithium-Polymer, Nickel-Metal Hydride, Lead-Acid), Cell Configuration (Single-Cell, Multi-Cell), End-Use Industry (Automotive, Consumer Electronics, Industrial, Telecom Equipment, Medical Devices, Energy Storage Systems, Other End-Use Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Fuel Gauge IC |

| Battery Charger IC |

| Authentication IC |

| Battery Monitor IC |

| Protection IC |

| Lithium-Ion |

| Lithium-Polymer |

| Nickel-Metal Hydride |

| Lead-Acid |

| Single-Cell |

| Multi-Cell |

| Automotive |

| Consumer Electronics |

| Industrial |

| Telecom Equipment |

| Medical Devices |

| Energy Storage Systems |

| Other End-Use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By IC Type | Fuel Gauge IC | ||

| Battery Charger IC | |||

| Authentication IC | |||

| Battery Monitor IC | |||

| Protection IC | |||

| By Battery Chemistry | Lithium-Ion | ||

| Lithium-Polymer | |||

| Nickel-Metal Hydride | |||

| Lead-Acid | |||

| By Cell Configuration | Single-Cell | ||

| Multi-Cell | |||

| By End-Use Industry | Automotive | ||

| Consumer Electronics | |||

| Industrial | |||

| Telecom Equipment | |||

| Medical Devices | |||

| Energy Storage Systems | |||

| Other End-Use Industries | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the battery management IC market?

The battery management IC market size stood at USD 6.52 billion in 2026.

How fast is the market expected to grow over the next five years?

It is forecast to register an 11.71% CAGR and reach USD 11.34 billion by 2031.

Which IC category is expanding the quickest?

Authentication ICs lead growth with a projected 12.34% CAGR through 2031 as manufacturers block counterfeit batteries.

Why are multi-cell monitor ICs critical for electric vehicles?

They balance up to 400 series cells within 10 mV, safeguarding battery life and enabling 800-volt fast-charging platforms.

Which region will grow the fastest, and why?

Asia Pacific is set to expand at a 12.74% CAGR thanks to China’s gigafactory build-out and ASEAN two-wheeler electrification.

Page last updated on: