Mobile Phone Semiconductor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 41.82 Billion |

| Market Size (2031) | USD 70.49 Billion |

| Growth Rate (2026 - 2031) | 11.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

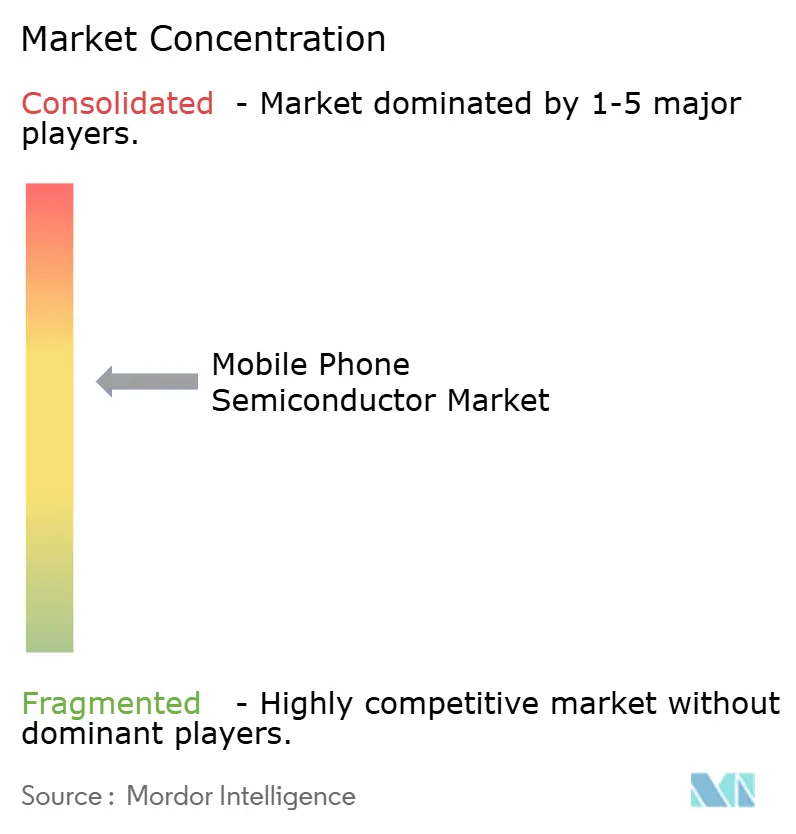

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mobile Phone Semiconductor Market Analysis by Mordor Intelligence

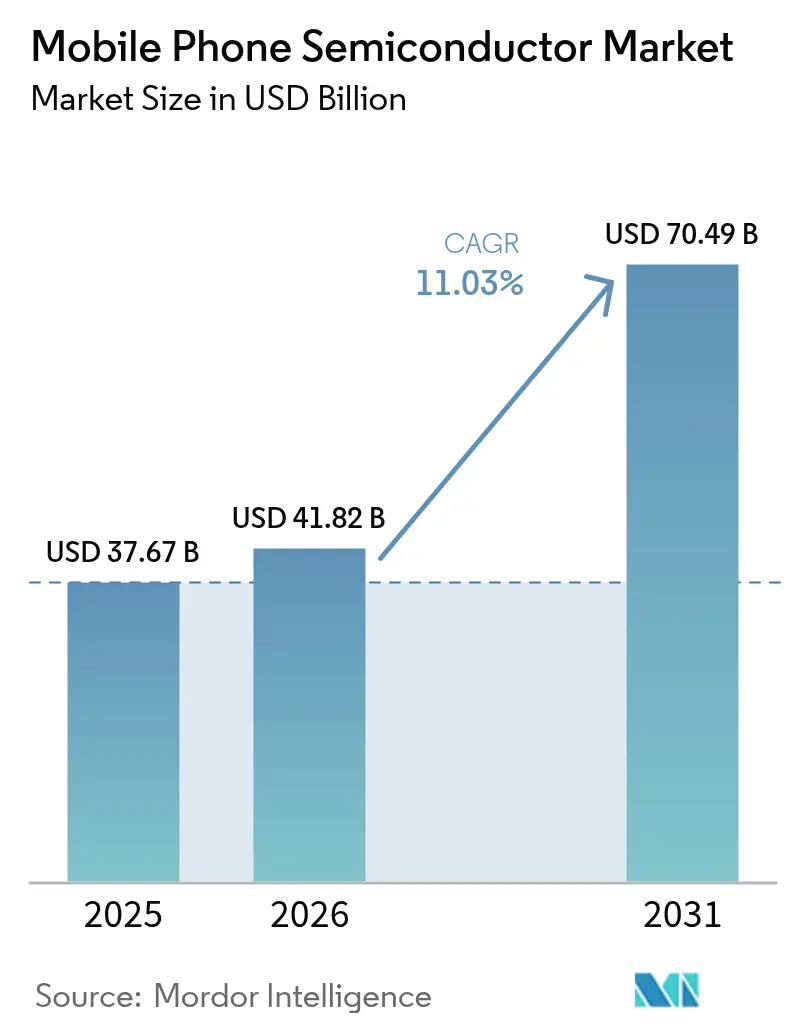

The mobile phone semiconductor market size in 2026 is estimated at USD 41.82 billion, growing from 2025 value of USD 37.67 billion with 2031 projections showing USD 70.49 billion, growing at 11.03% CAGR over 2026-2031. The rapid adoption of AI-native system-on-chip (SoC) designs, tighter integration of 5G radios, and escalating demand for specialized sub-3nm silicon form the backbone of this expansion. Foundry progress at 2 nm has enabled smartphone brands to embed neural processing units that deliver 45 TOPS of on-device inference without jeopardizing battery life. Memory density continues its upward trajectory as handset DRAM moves from 8 GB to 12 GB, while UFS 4.0 storage eases AI model loading constraints.[1]Samsung, “Corporate Website,” samsung.com The race to standardize satellite connectivity and Wi-Fi 7 further broadens silicon content per device, fueling the adoption of multi-chip packages in advanced packaging lines across the Asia-Pacific region.

Key Report Takeaways

- By component, mobile processors captured 32.80% of the mobile phone semiconductor market share in 2025, while sensors are projected to expand at a 12.60% CAGR through 2031.

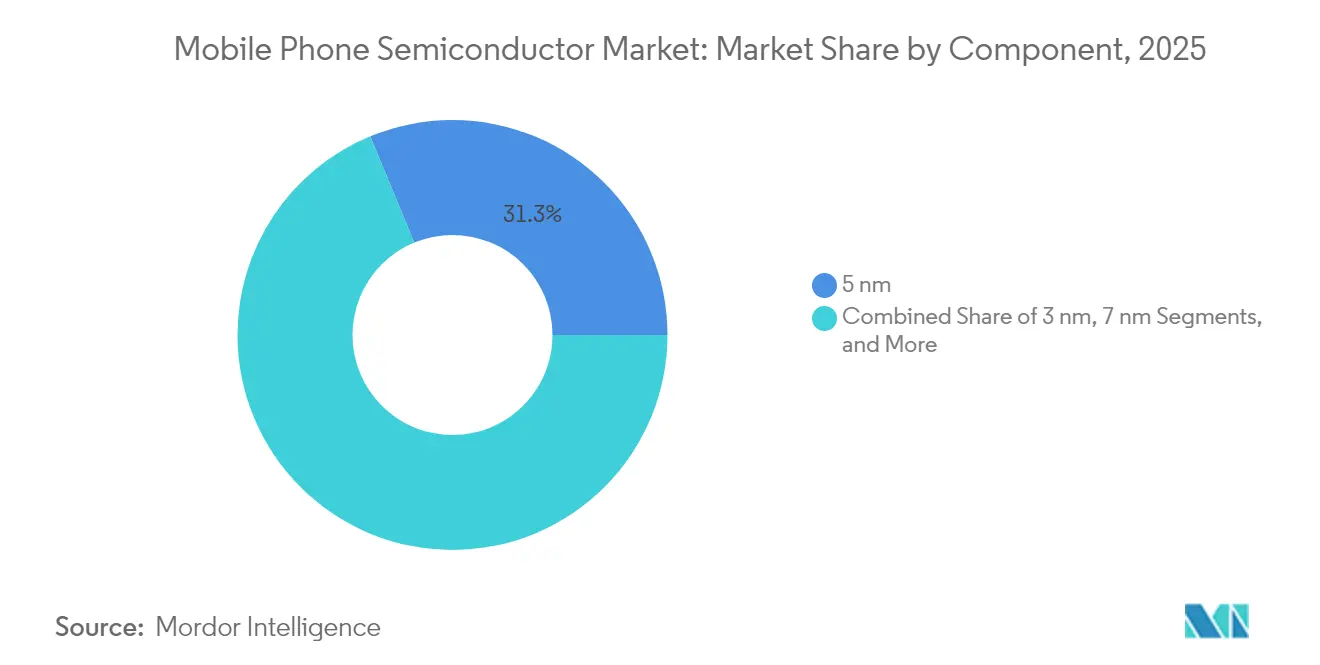

- By technology node, 5 nm devices accounted for 31.25% of the mobile phone semiconductor market size in 2025; sub-3 nm nodes are projected to achieve a 12.45% CAGR through 2031.

- By geography, the Asia-Pacific region held 53.90% of the mobile phone semiconductor market in 2025 and is expected to post a 12.05% CAGR through 2031.

- TSMC’s USD 42 billion capital spending plan, covering eight new fabs, highlights the investment intensity driving the mobile phone semiconductor market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mobile Phone Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of 5G smartphones | +2.8% | Global, with APAC leading adoption | Medium term (2-4 years) |

| Rising adoption of on-device AI/ML | +3.2% | North America and EU early adopters, APAC volume growth | Long term (≥ 4 years) |

| Growing memory content per handset | +1.9% | Global, driven by flagship segment expansion | Medium term (2-4 years) |

| High-refresh OLED displays | +1.4% | APAC manufacturing, global consumption | Short term (≤ 2 years) |

| Satellite connectivity enablement | +0.9% | North America and EU regulatory approval, global rollout | Long term (≥ 4 years) |

| Fan-out wafer-level SiP adoption | +0.8% | APAC manufacturing hubs, global implementation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of 5G Smartphones

Surging shipment volumes of 5G handsets continue to propel the mobile phone semiconductor market onto a high-growth trajectory. Qualcomm’s X85 modem delivers 10 Gbps peak throughput and incorporates AI-assisted signal processing, increasing RF front-end module dollar content by nearly 20% per unit.[2]Qorvo, “Corporate Website,” qorvo.com The leap from 4G to 5G requires multi-band power amplifiers, sub-6 GHz and mmWave antennas, and tighter thermal management, each of which adds die area. Samsung’s Exynos Modem 5400 introduced satellite fallback in 2024, ensuring continuous connectivity in remote areas. These requirements amplify wafer starts at 7 nm for modems and at mature 28 nm for companion RF transceivers, underlining how a single handset SKU often pulls wafers from four distinct process nodes. Consequently, fab utilization at APAC foundries remains elevated, sustaining supply pressure that benefits the mobile phone semiconductor market.

Rising Adoption of On-Device AI/ML

AI inferencing is migrating on-device to reduce latency and maintain privacy, thereby increasing compute density targets for application processors. MediaTek’s MT6825 demonstrated 40% energy savings compared to cloud-based inference, highlighting the cost advantages associated with local processing. Neural engines must coexist with CPUs, GPUs, image signal processors, and 5G basebands on a single substrate, driving chiplet-based SoC designs. Apple’s latest A-series processor integrates AI accelerators that execute large language models locally, prompting Android vendors to pivot toward dedicated tensor units that deliver 45 TOPS. This functionality utilizes more SRAM and high-speed inter-chip interconnects, driving demand for advanced packaging that keeps logic and memory in proximity. The outcome is a wider silicon footprint per handset, reinforcing double-digit revenue expansion for the mobile phone semiconductor market.

Growing Memory Content Per Handset

Handsets now function as AI workstations, demanding ample memory to stage large data sets. Samsung’s LPDDR5 at 12.7 GT/s meets the 2024 flagship needs, yet the roadmap to LPDDR6 at 17 GT/s in 2026 positions memory makers for a step-up in pricing. UFS 4.0 has entered mass deployment, with UFS 5.0 development achieving sequential read speeds of over 4.2 GB/s. As the median DRAM stack shifts from 8 GB to 12 GB, the dollar value of every mobile phone semiconductor market bill of materials expands. Rising bandwidth presents board-level challenges related to power rail stability and heat dissipation, driving an increased demand for power management ICs and thermal interface materials. Foundries benefit because LPDDR6 relies on process shrinks below 10 nm, locking incremental capacity into premium geometries where margins remain strongest.

High-Refresh OLED Displays

Mainstream phones now feature 120 Hz panels; gaming models are edging toward 144 Hz. Variable refresh logic necessitates agile timing controllers fabricated at 28 nm, while Samsung Display’s 22 nm driver IC cuts power by 40%. MagnaChip’s adaptive driver raised everyday battery life 25%. As foldable form factors proliferate, each hinge-based segment demands distinct controllers and touch-sensing ASICs, effectively doubling driver silicon content. These trends enhance the total available market for specialized analog and mixed-signal IC suppliers, tightening competition yet broadening revenue pools across the mobile phone semiconductor market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain cyclicality and pricing pressure | -1.8% | Global, with APAC manufacturing concentration | Short term (≤ 2 years) |

| Geopolitical export restrictions | -2.1% | US-China trade corridor, global supply chains | Long term (≥ 4 years) |

| Sub-5 nm thermal/yield challenges | -1.2% | Advanced foundries in Taiwan, Korea, US | Medium term (2-4 years) |

| OEM consolidation trimming TAM for tier-2 vendors | -0.7% | Global, concentrated in Android ecosystem | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Cyclicality and Pricing Pressure

Memory and analog cycles inject volatility into the mobile phone semiconductor market. Micron’s Q1 2025 revenue slipped 15% as DRAM prices softened, showing how a single quarter can erode margins across the value chain.[3]Micron Technology, “Corporate Website,” micron.com Seasonal handset ramps amplify boom-bust swings, leaving tier-2 suppliers exposed to inventory shocks. Capacity builds, often funded during peak demand, flood the market just as demand normalizes. The resultant oversupply compresses average selling prices, yet simultaneously sparks consolidation that nudges the market toward higher concentration ratios over time.

Geopolitical Export Restrictions

The January 2025 tightening by the U.S. Bureau of Industry and Security mandates licenses for advanced AI chips, fragmenting global supply webs. Chinese OEMs now dual-source between domestic 14 nm fabs and overseas 5 nm foundries, adding cost and complexity. Equipment embargoes slow yield-ramp for sub-10 nm lines inside China, widening performance gaps in premium tiers. Western brands, meanwhile, must validate separate hardware builds for sanctioned geographies, diverting limited engineering resources. These frictions temper the otherwise robust trajectory of the mobile phone semiconductor market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Processors Drive Integration Trends

Mobile processors retained a 32.80% market share of the mobile phone semiconductor market in 2025, underscoring their status as architectural hubs that coordinate AI inference, 5G connectivity, imaging pipelines, and sensor fusion within an increasingly compact board footprint. The mobile phone semiconductor market size associated with this component class is forecast to grow at an 10.88% CAGR through 2031, as chiplets and advanced packaging drive another wave of integration density. Sensors, the fastest-growing component group with a 12.60% CAGR, meet the rising demand for multimodal biometric authentication, air-quality tracking, and contextual awareness required by AI assistants.

Memory ICs anchor AI-native workloads through higher-bandwidth DRAM, while Logic ICs evolve into domain-specific accelerators that offload narrow AI kernels. Analog ICs still matter for signal conditioning even as digital take-over accelerates. Power management IC complexity increases with multi-standard fast charging and dynamic voltage scaling tailored to AI engines. RF and connectivity ICs now integrate Wi-Fi 7, Bluetooth 5.4, and soon satellite transceivers, swelling per-handset BOM. Display driver ICs incorporate variable refresh intelligence, and Audio ICs feature spatial playback and on-chip noise cancellation DSPs that align with trends in videogames and immersive media.

By Technology Node: Sub-3 nm Emergence Reshapes Economics

The 5 nm class accounted for 31.25% of the mobile phone semiconductor market size in 2025, striking a balance between performance and cost for flagship volumes. Yet sub-3 nm wafers are expanding at a 12.45% CAGR as TSMC’s N2 node enters mass production for Apple’s next-generation SoCs. The mobile phone semiconductor market now features a barbell cost curve: cutting-edge 2nm logic fetches premium margins, while mature 28nm lines churn out power-management and RF chips at scale.

7 nm remains the workhorse for mid-premium devices, whereas 16 nm and 28 nm processes anchor connectivity and analog functions where leakage trumps outright speed. Nodes above 28 nm persist for resilience-critical RF front ends. Samsung’s gate-all-around transistors at 3 nm promise a 35% power reduction but still struggle with yield issues. Intel’s foundry services entice U.S. brands seeking geographic diversification, though wafer pricing challenges the Asian incumbency. The economic backdrop illustrates why the mobile phone semiconductor market remains a tale of two cost structures rather than a monolithic curve.

Geography Analysis

The Asia-Pacific region held 53.90% of the mobile phone semiconductor market in 2025, driven by its deeply entrenched manufacturing clusters, government incentives, and proximity to handset assembly centers. China increased its installed wafer capacity by 13% to 8.6 million wafers per month in 2024, primarily at 28 nm nodes that supply power-management and connectivity devices. Taiwan dominates high-performance logic via TSMC, while Korea leads memory through Samsung and SK Hynix. India’s ascent as a large-scale assembly hub is creating adjacent demand for local test and packaging, stamping the region with a forecast 12.05% CAGR that exceeds the global baseline.

North America’s mobile phone semiconductor footprint hinges on design IP leadership and new fab investments catalyzed by the CHIPS Act. TSMC’s Arizona plant began 4 nm production in early 2025, offering capacity to premium U.S. handset brands. Intel’s USD 20 billion Ohio expansion envisions mobile-optimized capacity, although cost headwinds remain relatively higher compared to its Asian peers. The region benefits from tighter IP control and shorter R&D loops between design centers and advanced manufacturing lines.

Europe prioritizes strategic autonomy and environmental sustainability. The EU Chips Act aims for a 20% global market share by 2030, allocating more funds toward automotive and industrial chips than handsets. GlobalFoundries–UMC merger talks aim to consolidate 10% of othe worldwide contract capacity, providing a brand with geopolitical balance. The Middle East and Africa offer prospects for back-end assembly as mobile phone vendors diversify. South America remains a modest participant, capped at final assembly, yet improving trade pacts could eventually draw test and package operations.

Competitive Landscape

The mobile phone semiconductor market rivalry centers on integration depth, power efficiency, and AI feature density, rather than raw clock speed. Qualcomm remains the reference for premium Android processors but faces stiff price-performance competition from MediaTek’s Dimensity line. Apple’s vertical stack insulates its flagship share and reinforces exclusive access to TSMC’s leading nodes. Samsung juggles dual roles: internal chipset supply and merchant sales, creating strategic tensions when customers overlap with its handset division.

Platform-level selling is ascendant. Vendors are increasingly bundling processors, RF modules, power management, and reference software to reduce OEM design cycles. RF competition intensifies as satellite connectivity normalizes, handing white-space to niche players specializing in L-band and S-band front ends. Packaging advances, fan-out wafer-level, 2.5D interposers, and chip-on-wafer-on-substrate translate into new battlegrounds where ASE, Amkor, and Intel vie for design wins.

Foundry selection has become a strategic lever. TSMC’s first-mover edge at 2 nm gives early adopters a six-month performance window, but Samsung’s gate-all-around roadmap and Intel’s U.S. capacity threaten to dilute that lead by 2027. Patent cross-licensing with ARM remains foundational, as every flagship SoC taps ARM CPU cores in some form.[4]ARM Holdings, “Company News,” arm.com Consolidation pressures loom because a single process node now demands more than USD 1 billion in R&D, favoring deep-pocketed incumbents.

Mobile Phone Semiconductor Industry Leaders

-

Qualcomm Incorporated

-

MediaTek Inc.

-

Samsung Electronics Co., Ltd.

-

Apple Inc.

-

HiSilicon Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: TSMC outlined USD 42 billion capex for eight new fabs and one advanced packaging site to satisfy AI and smartphone silicon demand.

- July 2025: Synopsys closed its USD 35 billion ANSYS acquisition, merging EDA with multiphysics simulation to streamline sub-3 nm chip design.

- July 2025: Qualcomm reported USD 9.4 billion Q3 2025 revenue, citing 15% YoY growth in mobile SoCs.

- June 2025: Cirrus Logic unveiled a 22 nm smart codec, cutting audio power by 30%.

- May 2025: Samsung Electronics logged record Q1 2025 semiconductor revenue of KRW 28.6 trillion (USD 21.4 billion) on robust high-bandwidth memory and mobile SoC sales.

- May 2025: SK Hynix earmarked USD 3.9 billion for advanced memory packaging lines.

- April 2025: NXP launched Wi-Fi 6E front-end ICs optimized for 6 GHz spectrum.

- March 2025: Texas Instruments posted USD 3.8 billion Q1 2025 revenue as analog content per phone rose.

- February 2025: OmniVision introduced a 200 MP image sensor with embedded AI.

- January 2025: Skyworks Solutions booked USD 1.1 billion Q1 2025 revenue on 5G RF demand.

Global Mobile Phone Semiconductor Market Report Scope

The Mobile Phone Semiconductor Market Report segments the market by various components, including Mobile Processors, Memory ICs, Logic ICs, Analog ICs, Power Management ICs, RF ICs, Connectivity ICs, Display Driver ICs, Audio ICs, and a range of Sensors (such as Motion, Environmental, Positioning, Image, and Biometric Sensors). Additionally, the market categorizes technology nodes into < 3 nm, 3 nm, 5 nm, 7 nm, 16 nm, 28 nm, and > 28 nm. Geographically, the report spans North America (covering the United States, Canada, and Mexico), South America (including Brazil, Argentina, and the Rest of South America), Europe (with a focus on Germany, the United Kingdom, France, Italy, Spain, and the Rest of Europe), Asia-Pacific (highlighting China, Japan, South Korea, India, Singapore, Australia, and the Rest of Asia-Pacific), and the Middle East & Africa (featuring Saudi Arabia, the United Arab Emirates, Turkey, the Rest of the Middle East, South Africa, Nigeria, Egypt, and the Rest of Africa). All market forecasts are presented in terms of value (USD).

| Mobile Processors |

| Memory ICs |

| Logic ICs |

| Analog ICs |

| Power Management ICs |

| RF ICs and Connectivity ICs |

| Display Driver ICs |

| Audio ICs |

| Sensors (Motion sensors, Environmental Sensors, Positioning Sensors, Image Sensors, Biometric Sensors, etc.) |

| < 3 nm |

| 3 nm |

| 5 nm |

| 7 nm |

| 16 nm |

| 28 nm |

| > 28 nm |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Singapore | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Mobile Processors | ||

| Memory ICs | |||

| Logic ICs | |||

| Analog ICs | |||

| Power Management ICs | |||

| RF ICs and Connectivity ICs | |||

| Display Driver ICs | |||

| Audio ICs | |||

| Sensors (Motion sensors, Environmental Sensors, Positioning Sensors, Image Sensors, Biometric Sensors, etc.) | |||

| By Technology Node | < 3 nm | ||

| 3 nm | |||

| 5 nm | |||

| 7 nm | |||

| 16 nm | |||

| 28 nm | |||

| > 28 nm | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Singapore | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the expected value of the smartphone semiconductor market in 2031?

It is projected to reach USD 70.49 billion by 2031, expanding at an 11.03% CAGR.

Which component currently leads revenue contribution?

Mobile processors held 32.80% market share in 2025, the highest among all component groups.

Why are sub-3 nm nodes important for future smartphone chips?

They enable higher AI TOPS performance and lower power consumption, supporting advanced use cases like on-device large language models.

How does Asia-Pacific dominate manufacturing?

The region combines large-scale wafer fabs, established packaging houses, and proximity to handset assembly lines, securing 53.90% market share in 2025.

What impact do export controls have on Chinese smartphone OEMs?

They restrict access to cutting-edge memory and AI chips, forcing reliance on domestically produced components that lag by one to two generations.

Which new connectivity feature is driving RF IC demand?

Satellite connectivity integration in mainstream handsets is creating additional demand for multi-band RF front-end modules.

Page last updated on: