Wind Turbine Maintenance, Repair, And Overhaul (MRO) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

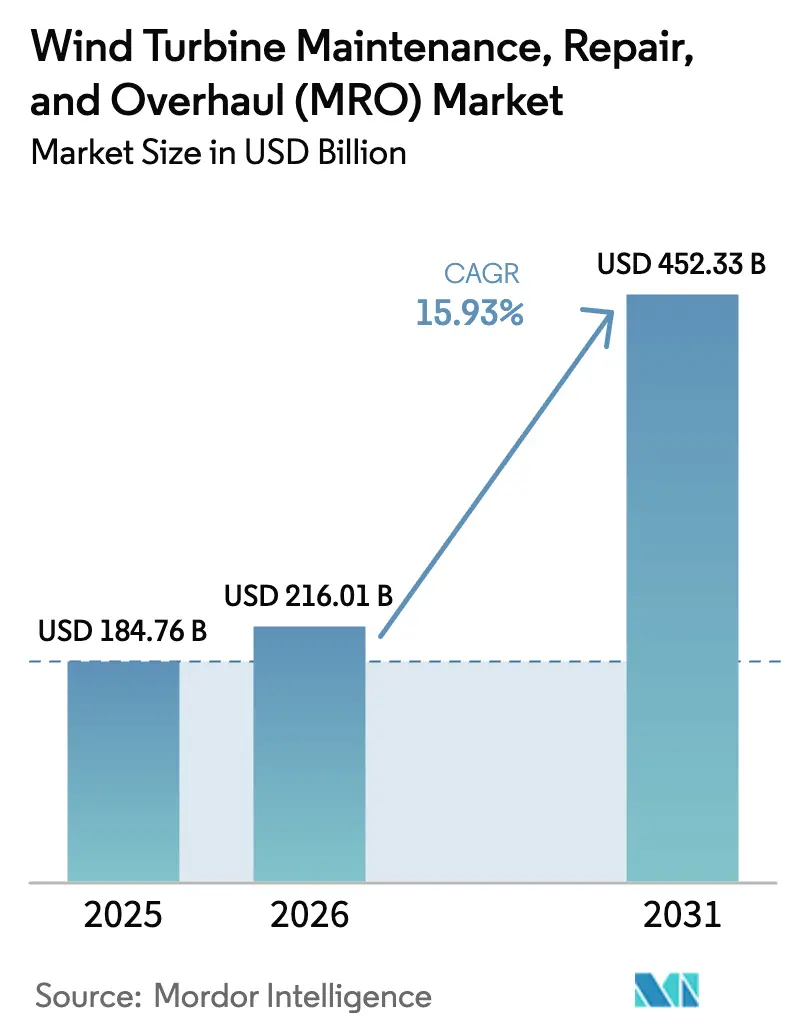

| Market Size (2026) | USD 216.01 Billion |

| Market Size (2031) | USD 452.33 Billion |

| Growth Rate (2026 - 2031) | 15.93% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wind Turbine Maintenance, Repair, And Overhaul (MRO) Market Analysis by Mordor Intelligence

The Wind Turbine Maintenance, Repair, And Overhaul Market size is projected to be USD 184.76 billion in 2025, USD 216.01 billion in 2026, and reach USD 452.33 billion by 2031, growing at a CAGR of 15.93% from 2026 to 2031.

Growth is fueled by an aging installed base that has now passed 1 terawatt, an upshift in OEM business models toward long-term availability contracts, and tightening grid-code mandates that push owners to retrofit power electronics, blades, and gearboxes. Asia-Pacific remains the revenue anchor, led by China’s directive to upgrade more than 50 GW of pre-2015 onshore capacity, while Europe drives complexity through expanding offshore fleets, especially floating platforms that require specialized vessels and real-time condition monitoring. Intensifying competition between OEMs and independent service providers (ISPs) is lowering transactional repair prices yet broadening the menu of risk-sharing contracts. Digital twins and AI-enabled predictive analytics are cutting unplanned downtime, but the market still contends with gearbox reliability issues in the >5 MW class, heavy-lift vessel shortages, and a global lack of certified blade-repair technicians.

Key Report Takeaways

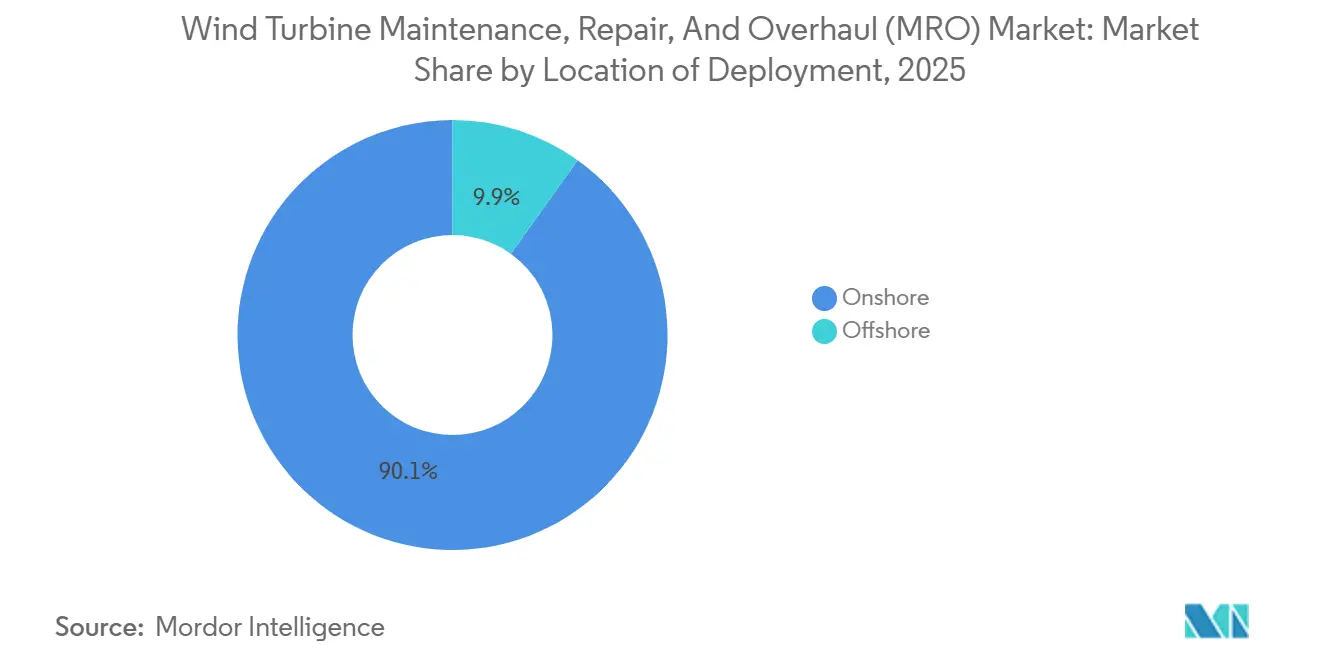

- By location of deployment, onshore sites captured 90.1% of 2025 revenue; offshore work is advancing at 28.3% CAGR on the back of larger >15 MW turbines and floating-wind rollouts.

- By service type, overhaul activities led with 46.4% of wind turbine maintenance, repair & overhaul (MRO) market share in 2025; the category is forecast to expand at a 20.4% CAGR through 2031.

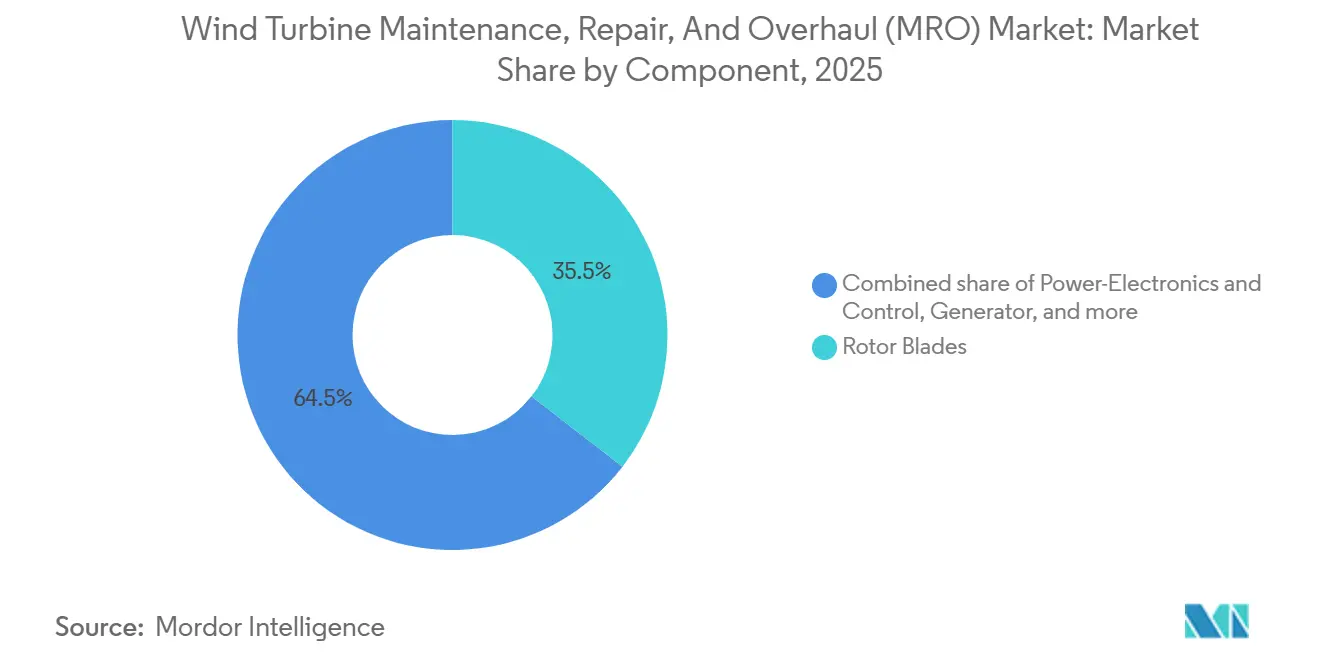

- By component, rotor blades accounted for 35.5% of spending in 2025, while power-electronics upgrades are projected to grow at 22.5% CAGR to 2031.

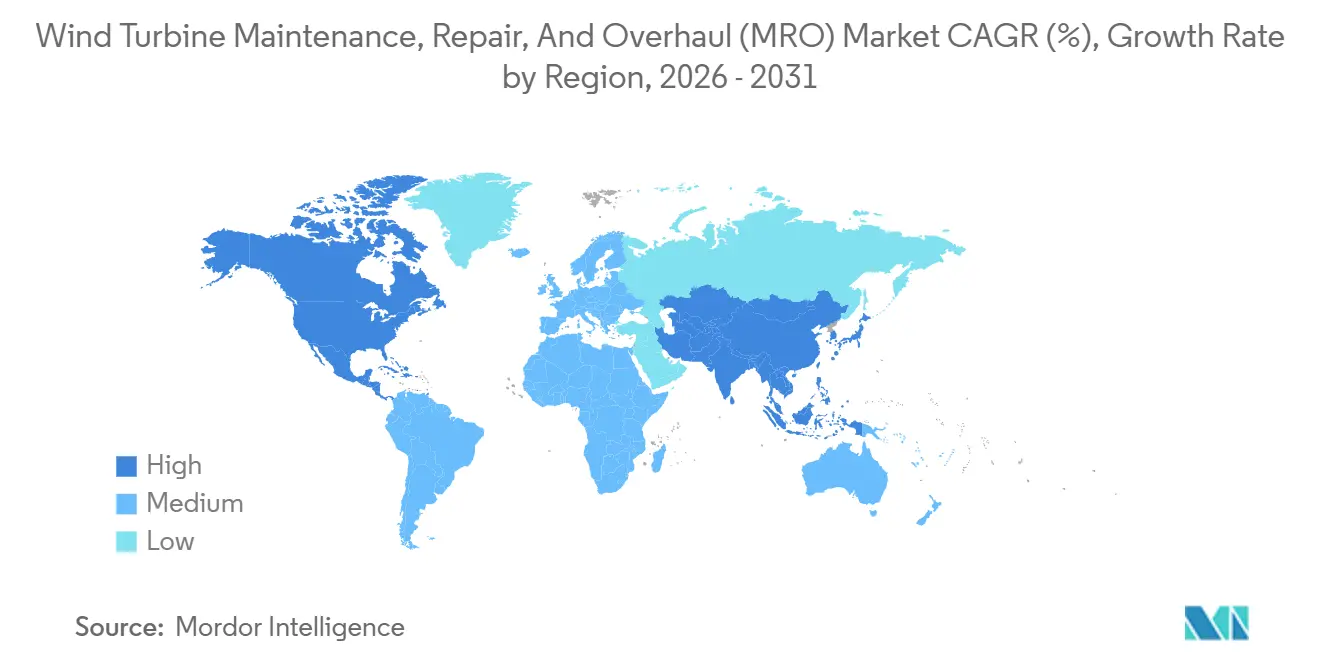

- By geography, Asia-Pacific commanded 53.9% of the 2025 total, driven by China’s retrofit mandate and India’s production-linked incentives; the region is forecast to post a 17.6% CAGR to 2031.

- Vestas, Siemens Gamesa, and GE Renewable Energy controlled close to 60% of the global service backlog in 2025, yet regional specialists such as Global Wind Service and B9 Energy are gaining share through multi-brand technician pools and faster mobilization.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wind Turbine Maintenance, Repair, And Overhaul (MRO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended turbine lifespans through life-extension retrofits | +3.2% | Global, concentrated in Europe & North America | Medium term (2-4 years) |

| AI-driven predictive analytics reduce unplanned downtime | +2.8% | Asia-Pacific core; spill-over to Europe & North America | Short term (≤2 years) |

| Service-oriented OEM business models (power-by-the-hour) | +2.5% | Global, led by Europe & North America | Medium term (2-4 years) |

| National repowering incentives for >10-yr-old fleets | +3.1% | North America & Europe, emerging in Asia-Pacific | Long term (≥4 years) |

| Floating-wind rollout creates specialized MRO demand | +1.9% | Europe (North Sea, Atlantic) & Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Extended Turbine Lifespans Through Life-Extension Retrofits

Operators are increasingly choosing retrofit programs that add 5–10 additional operating years at one-quarter the capital outlay of full repowering. Germany alone has extended more than 4 GW of pre-2005 capacity by reinforcing blade spars and replacing main bearings, circumventing the 24–36-month permitting cycle tied to new foundations. Project costs typically fall between USD 150,000 and USD 400,000 per turbine, compared with USD 1.2 million to USD 1.8 million for a complete replacement. Vestas reported that life-extension contracts reached 18% of its 2025 service revenue, up from 11% in 2023.[1]Vestas Wind Systems, “Annual Report 2025,” vestas.com The trend is accelerating in the United States because the Inflation Reduction Act’s production tax credit rewards incremental output from existing assets. Publication of DNV GL’s updated IEC 61400 lifetime-extension guidelines in 2024 has lowered certification risk and opened the door for ISPs to compete aggressively for retrofit work.

AI-Driven Predictive Analytics Reduce Unplanned Downtime

Machine-learning algorithms that parse SCADA streams, vibration data, and thermal imagery are detecting failures 4–8 weeks in advance, turning reactive work orders into condition-based tasks. Siemens Gamesa’s Digital Services platform, deployed across 25 GW by mid-2025, lowered unplanned downtime by 22% and trimmed emergency call-out costs by USD 35,000 per turbine per year.[2]Siemens Gamesa Renewable Energy, “Digital Services Expansion,” siemensgamesa.com GE’s Digital Wind Farm suite delivered a 15% availability gain across 18 GW of installations. Offshore owners value the technology most, using early alerts to cluster interventions into single campaigns and shave vessel charter budgets by up to 40%. Retrofits are limited by sparse sensor coverage on turbines built before 2018, creating an aftermarket for instrumentation upgrades.

Service-Oriented OEM Business Models (Power-by-the-Hour)

OEMs are migrating from transactional part sales to availability-based pricing that shifts performance risk onto the supplier and stabilizes cash flow. Under Active Output Management contracts, operators pay per megawatt-hour generated, while Vestas assumes full responsibility for spares, labor, and optimization. The firm covered 32 GW under these deals in 2025, generating USD 1.8 billion in service revenue and achieving a 68% renewal rate. Nordex mirrored the model by layering dynamic power-curve tuning and real-time yaw alignment into its Premium Service tier. Financial investors prefer the arrangement because it converts variable O&M cost into a fixed-fee profile, although it concentrates market power with OEMs that can hedge component-failure volatility.

National Repowering Incentives for >10-Year-Old Fleets

The U.S. Inflation Reduction Act extends a 30% investment tax credit for projects that raise capacity at least 20%, making it financially appealing to swap 2 MW machines from the early 2010s with 4–5 MW models. Germany earmarked EUR 1.2 billion in 2024 tenders for onshore repowering, while Spain trimmed permitting to six months for projects that keep grid-connection points. These carrots are driving demand for decommissioning, foundation diagnostics, and blade recycling, yet landfill bans across the EU underscore the urgency of scalable composite-recycling solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent gearbox reliability issues in >5 MW class | –2.1% | Global; acute offshore Europe & Asia-Pacific | Short term (≤2 years) |

| Scarcity of blade-repair technicians & composite materials | –1.8% | Global; most severe in Asia-Pacific & North America | Medium term (2-4 years) |

| Revenue squeeze from expiring 20-year service contracts | –1.4% | Europe & North America | Medium term (2-4 years) |

| Logistics bottlenecks for offshore heavy-lift vessels | –1.6% | Europe (North Sea) & Asia-Pacific (Taiwan, Japan) | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Persistent Gearbox Reliability Issues in >5 MW Class

Bearing micropitting, gear-tooth spalling, and lubrication contamination keep gearbox failures the largest single cause of downtime in the 6–8 MW fleet, driving emergency repairs that can reach USD 1.2 million when offshore crane mobilization and lost generation are counted. A 2024 peer-reviewed study covering 1,200 turbines found gearbox outages at 38% of total downtime hours despite representing only 12% of the component count. Siemens Gamesa increased warranty provisions by EUR 180 million after higher-than-expected bearing failures on its 8 MW platform. While ZF’s 2025 modular gearbox allows in-situ bearing swaps and trims intervention time by 40%, retrofitting legacy units remains uneconomical for most owners.

Scarcity of Blade-Repair Technicians & Composite Materials

Fewer than 8,000 technicians globally hold both rope-access and composite-layup credentials necessary for 70 m+ blade repairs, with vacancy rates at 18% in Europe and North America. Certification programs take 12–18 months, and turnover exceeds 25% as aerospace firms poach talent. Material shortages add another hurdle: Hexcel reported carbon-fiber lead times of 20 weeks in Q3 2025, up from 12 weeks a year earlier, because aerospace demand rebounded faster than production capacity. These twin constraints inflate repair costs by more than 30% and stretch maintenance backlogs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location of Deployment: Offshore Complexity Drives Premium Pricing

Onshore installations represented 90.1% of wind turbine maintenance, repair & overhaul (MRO) market revenue in 2025, reflecting easier road access and lower labor rates. The segment’s average annual spend per turbine hovers near USD 35,000, with two scheduled maintenance visits each year and minimal vessel costs. In contrast, the offshore share of the wind turbine maintenance, repair & overhaul (MRO) market size is rising quickly, advancing at 28.3% CAGR through 2031 as developers install >15 MW turbines farther from shore. A single offshore turbine typically consumes USD 95,000 annually in MRO outlays, with vessel logistics absorbing almost half of that bill.[3]Ørsted, “Hornsea 2 Operational Update,” orsted.com

Floating-wind adds yet another cost layer. Dynamic mooring systems, pitch-roll platform motion, and scarcer weather windows require motion-compensated gangways and autonomous inspection drones. Japan’s JPY 12 billion program to build robotic blade-repair tools underscores industry recognition that conventional rope-access methods will not suffice offshore. As offshore work claims a larger slice of global capacity, specialized marine contractors are expected to capture outsized margins and consolidate a young supply chain still short on vessels and certified technicians.

By Service Type: Overhaul Dominance Reflects Fleet Aging

Overhaul work led 2025 spend with 46.4% of wind turbine maintenance, repair & overhaul (MRO) market share and is projected to record a 20.4% CAGR to 2031. Gearbox rebuilds alone can cost USD 300,000–700,000 per machine; generator rewinds add another USD 150,000–350,000. As fleets installed from 2010-2015 enter their second decade, operators accept those costs to avoid multi-million-dollar repowering budgets, driving the wind turbine maintenance, repair & overhaul (MRO) market size for overhaul services sharply upward. Maintenance tasks, such as scheduled inspections and consumable swaps, remain mandatory for warranty compliance but face stiff price competition from ISPs that underbid on labor-intensive work. Repair services stay episodic, triggered by lightning strikes or control-system faults, prompting OEMs to wrap them into availability guarantees that flatten revenue volatility.[4]Vestas Wind Systems, “Annual Report 2025,” vestas.com

OEMs fine-tune service tiers to capture value: Vestas’ 2025 menu offers quarterly oil analysis and annual blade borescope inspections within a premium plan that fetches 10–15% higher fees. ISPs counter by pooling spare-part inventories across multiple brands, lowering cycle times by 30–50% and winning multiyear contracts once thought impenetrable.

By Component: Power Electronics Surge on Grid-Code Mandates

Rotor blades absorbed 35.5% of 2025 component spend, reflecting frequent leading-edge erosion fixes and lightning-protection upgrades. Automated repair rigs like LM Wind Power’s UV-cured system cut labor hours by 60% and shrink repair windows to two days, valuable when turbines stand idle at USD 30,000-plus per day revenue loss. Nonetheless, power electronics and control systems will be the fastest-growing slice, expanding at a 22.5% CAGR as grid operators worldwide impose voltage-ride-through and reactive power rules. Germany’s updated technical guidelines oblige inverter retrofits on 18 GW of legacy turbines by 2027. Each upgrade costs USD 120,000–280,000 but opens access to ancillary service revenues that can repay half the investment within five years. The wind turbine maintenance, repair & overhaul (MRO) market size for power electronics thus exhibits outsized momentum versus mechanical components like towers or yaw systems.

Geography Analysis

Asia-Pacific retained 53.9% of 2025 global revenue and is expected to clock a 17.6% CAGR through 2031. China’s 14th Five-Year Plan mandates controller upgrades and blade extensions across 50 GW of pre-2015 assets, lifting retrofit outlays and enlarging the wind turbine maintenance, repair & overhaul (MRO) market size in the region. Goldwind’s Inner Mongolia service hub, opened in October 2025, halves lead times for gearboxes and spares. India’s production-linked incentive grants INR 15 per kWh for overhauled turbines, encouraging owners to invest in multi-component rebuilds rather than decommission.

Europe remains a high-value arena owing to its 30 GW offshore fleet and strict operating codes. The UK’s Round 4 seabed awards compel developers to use domestic vessels for 60% of maintenance activity, spurring local supply-chain build-out. Germany and the Netherlands anchor demand for heavy-lift campaigns, while Spain accelerates onshore repowering with six-month permitting cycles.

North America benefits from the Inflation Reduction Act’s extended production tax credit, which keeps older turbines profitably spinning after gearbox, blade, and inverter upgrades. GE’s USD 320 million Indian onshore MRO contract in November 2025 illustrates OEM appetite for long-dated agreements that blend retrofit, overhaul, and analytics.

South America and the Middle East & Africa remain emerging contributors. Brazil’s ANEEL now enforces annual blade inspections and biennial oil analysis, spawning new ISP entrants. Morocco and South Africa are the first African markets to confront large-scale overhauls as 2017-2019 turbines approach mid-life.

Regulatory Landscape

Wind turbine MRO is increasingly shaped by formal life-extension and through-life management expectations. IEC TS 61400-28:2025 (published March 2025) offers a global technical reference for continued operation beyond original design life, aligning with the report focus on lifetime-extension retrofits and certification-driven overhaul work across aging fleets.

Offshore frameworks are also increasing plan-and-report obligations that carry through to service contracting and documentation workflows. In the United Kingdom, Statutory Instrument 2026/577 requires submission of an offshore operations and maintenance plan to the Marine Management Organisation (MMO) at least 6 months before operations begin, followed by periodic reviews and recurring maintenance reporting. The Netherlands January 2026 Development Framework (RVO) strengthens regulatory oversight of offshore grid and wind farm service life and technical specifications under the Electricity Act 1998, while Canada implemented Offshore Renewable Energy Regulations effective January 2025 under the Canadian Energy Regulator Act, defining lifecycle maintenance, safety, and environmental protection expectations for offshore activities.

Competitive Landscape

The wind turbine maintenance, repair & overhaul (MRO) market exhibits moderate concentration. The top five OEMs, Vestas, Siemens Gamesa, GE Renewable Energy, Goldwind, and Nordex, manage roughly 60% of global service backlogs via bundled contracts tied to equipment sales. Yet the expiration of 20-year agreements is loosening OEM grip, allowing ISPs such as Global Wind Service to win multibrand deals by fielding cross-trained technicians and stocking regional warehouses that cut part delivery by up to 50%.

Digitalization is the new battleground. Vestas’ 2024 purchase of Utopus Insights gave it proprietary analytics that integrate weather, price signals, and component health, optimizing maintenance for revenue yield rather than pure availability. Siemens Gamesa followed by buying a majority stake in Offshore Wind Services GmbH, securing scarce heavy-lift vessel capacity and marine expertise. GE and Envision push cloud-native digital twins that promise 18% reductions in unplanned downtime.

Barriers to entry are lower in niches such as blade recycling, gearbox oil analytics, and drone-based tower inspection. Venture-backed specialists leverage technology to offer risk-sharing contracts that guarantee sub-5-day response times. Yet skills deficits, especially in composite repairs, restrain market fragmentation by keeping high-complexity tasks with OEMs and large ISPs.

Wind Turbine Maintenance, Repair, And Overhaul (MRO) Industry Leaders

Vestas Wind Systems A/S

Siemens Gamesa Renewable Energy SA

General Electric Company

Suzlon Energy Ltd

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is emerging around localized major-component refurbishment and refurbishment-led life extension, as grid and permitting constraints push owners to recover additional years from existing assets while managing cost and downtime. In the United Kingdom, RenewableUK's April 2026 Onshore Wind Supply Chain Capability Assessment pointed to major component refurbishment as the most achievable near-term supply chain growth opportunity, which supports business cases for regional gearbox, generator, and blade repair capacity that can reduce lead times compared with centralized OEM networks.

Digital services and data-driven maintenance are also expanding MRO beyond routine site visits, especially for fleets with limited legacy instrumentation. Work on digital-twin approaches, including the e-PROA project findings presented at WindEurope 2026 (April 2026, IOP conference proceedings), reported surrogate modeling that reduces computation time for maintenance prediction versus full physics simulations, reinforcing a route to scalable condition monitoring, anomaly detection, and campaign planning. Combined with operator attention on long-term service agreements to handle offshore component constraints, the opportunity shifts toward service portfolios that bundle sensor retrofit, analytics, and availability-style contracting across both onshore life-extension programs and offshore interventions that are more technically constrained.

Recent Industry Developments

- July 2026: Suzlon Energy secured a 105 MW order from Sunsure Energy in Karnataka for its S175 5 MW turbine platform, including comprehensive operations and maintenance services. The bundled service scope supports OEM-led, long-duration O&M capture as India adds higher-rated turbines that require structured maintenance planning and spares readiness.

- May 2026: ABB dispatched the first locally manufactured wind power converter from its Nelamangala facility in Bengaluru, following its acquisition of Gamesa Electrics power electronics business in December 2025. Regional converter output strengthens supply availability for inverter upgrades and replacements, a key MRO spending area under tightening grid-code and reliability requirements.

- April 2026: Vestas received a 186 MW order for the Foret Domaniale project in Quebec, Canada, from EDF power solutions North America, featuring a 10-year Active Output Management (AOM) 5000 service agreement. The agreement expands Vestas contracted service backlog and reinforces the shift toward availability-oriented service models that combine performance guarantees, asset management, and long-term parts planning.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues earned from keeping wind turbines operating through maintenance, repair, and overhaul services across onshore and offshore wind farms, including routine service visits, corrective work, and major component refurbishment.

Scope exclusions: New wind turbine manufacturing and initial installation works are not counted, unless they are packaged as an after-sales service activity.

Segmentation Overview

- By Location of Deployment

- Onshore

- Offshore

- By Service Type

- Maintenance

- Repair

- Overhaul

- By Component

- Rotor Blades

- Nacelle and Drivetrain

- Generator

- Tower

- Power-Electronics and Control

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Spain

- Russia

- Finland

- Sweden

- Tukey

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Vietnam

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Egypt

- Morocco

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the global operating base of wind turbines and to understand the maintenance intensity that typically follows turbine aging and higher utilization. We relied on public datasets and technical references to ground inputs, such as IRENA statistics, IEA wind and power series, GWEC releases, NREL publications, and trade data from sources like UN Comtrade for relevant components.

Along with these, we reviewed company annual reports, investor presentations, service contract announcements, and credible press coverage to understand how the service mix shifts over time, how pricing is moving, and how offshore maintenance complexity can differ from onshore. For gap-filling on company-level context, we also used paid subscriptions focused on company financials and intelligence, plus patent databases to sanity-check the pace of condition monitoring and repair-related innovation. The desk sources cited above are illustrative only, and many other public and paid references were used during data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and surveys with service providers, wind farm owners, and supply chain participants who see how work scopes and pricing change by turbine age, site access constraints, and warranty conditions. We used these discussions to validate service frequency, typical repair triggers, downtime drivers, and the split between planned work and unplanned events across APAC, EMEA, and the Americas. Respondent inputs were also used to align assumptions on parts lead times, labor availability, and offshore logistics constraints, which then helped us triangulate the final totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 18% | APAC: 46% |

| Mid tier: 45% | Functional/Unit leaders: 34% | EMEA: 36% |

| Smaller Players: 20% | Managers: 48% | Americas: 18% |

Market-Sizing & Forecasting

Market sizing was built using top-down modeling where installed capacity and turbine counts by region and deployment type are converted into an annual service demand pool using intervention rates and spend curves that change with turbine age. Once the total was formed, we corroborated it with selective bottom-up approximations, such as sampled pricing for major work packs multiplied by expected intervention volumes, followed by checks on implied spend per turbine.

Key inputs used in the model included installed wind capacity and operating turbine counts, average fleet age and warranty coverage, intervention rates for blades, drivetrain, and generators, offshore access windows and logistics intensity, and average labor-hours and downtime per event. For forecasting, scenario analysis was used to connect new capacity additions, aging of the installed base, and expected shifts toward condition-based maintenance, and then assumptions were tuned using expert consensus from primary discussions. Where provider-level splits were not visible, gaps were handled by applying region-level turbine counts and validated service mix shares rather than forcing detailed supplier roll-ups.

Data Validation & Update Cycle

Model outputs were compared with independent signals like wind capacity additions, publicly discussed OPEX benchmarks, and offshore commissioning activity, and then variances were reviewed before sign-off. When anomalies appeared, the checks were run again at region and service-type levels, followed by a review of unit logic, currency conversion timing, and whether implied pricing trends stayed consistent with interview feedback.

The report is refreshed annually, with interim reviews triggered by material events such as sharp changes in offshore activity, policy moves that alter project pipelines, or disruptions that affect parts and labor. Before delivery, a final pass is completed so the numbers and near-term assumptions reflect the latest available updates.

Mordor Intelligence's Wind Turbine Maintenance Repair Overhaul MRO Market Size Compared Against Other Published Estimates

Published market sizes for wind turbine MRO can vary widely because the counted revenue pool is not always defined in the same way, and the base year, currency timing, and inflation treatment also differ. Gaps also come from how the installed base is measured, how turbine aging is translated into service events, and how offshore maintenance complexity is priced.

New turbine installation and EPC revenue sits outside Mordor Intelligence's scope, which helps explain why some broader energy services figures can look much larger even when the topic label sounds similar. Separately, certain estimates use flatter spend-per-MW assumptions that do not adjust for warranty coverage, major component repair cycles, or seasonal access limits offshore, which can pull the total down in earlier years.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 216.01 B (2026) | |

| Industry Research Publisher A | USD 24.44 B (2025) | This estimate appears to apply a narrower service revenue pool and a different base year, and it is not clear whether major overhauls and offshore logistics uplift are fully captured in the average spend assumptions. |

| Market Advisory B | USD 23.30 B (2024) | This figure is anchored to 2024 and can differ if the operating fleet and age profile are not scaled consistently across regions, and if currency conversion timing is applied differently for global roll-ups. |

Overall, the differences are mainly driven by scope edges and how the operating fleet is translated into repeatable service events, rather than simple arithmetic. When spend curves are tied to turbine age, offshore access constraints, and validated intervention rates, the resulting market size stays easier to trace back to visible demand indicators and to refresh as the installed base changes.

Key Questions Answered in the Report

How large is the wind turbine maintenance, repair & overhaul (MRO) market today?

The market generated USD 216.01 billion in 2026 and is forecast to reach USD 452.33 billion by 2031, reflecting a 15.93% CAGR.

Which segment grows fastest within wind turbine MRO?

Overhaul services, covering gearboxes, generators, and blades, are projected to expand at 20.4% CAGR as turbines commissioned between 2010-2015 enter major-repair cycles.

Why is Asia-Pacific the leading region?

China's mandate to retrofit over 50 GW of pre-2015 turbines and India's incentive program for life-extension projects together account for 53.9% of 2025 global revenue and drive a regional CAGR of 17.6%.

What is the main technical challenge facing offshore MRO?

A shortage of heavy-lift vessels and motion-compensated cranes pushes day rates above USD 150,000 and can delay blade or nacelle interventions by up to six months.

How are OEMs adapting their business models?

They are shifting toward availability-based 'power-by-the-hour' contracts that bundle spares, labor, and digital monitoring, offering predictable fees while taking on performance risk.

Which new technology delivers the biggest maintenance savings?

AI-enabled predictive analytics integrated with digital twins can cut unplanned downtime by 15-22%, saving roughly USD 35,000 per turbine each year on emergency call-outs.

Page last updated on: