Wind Turbine Tower Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

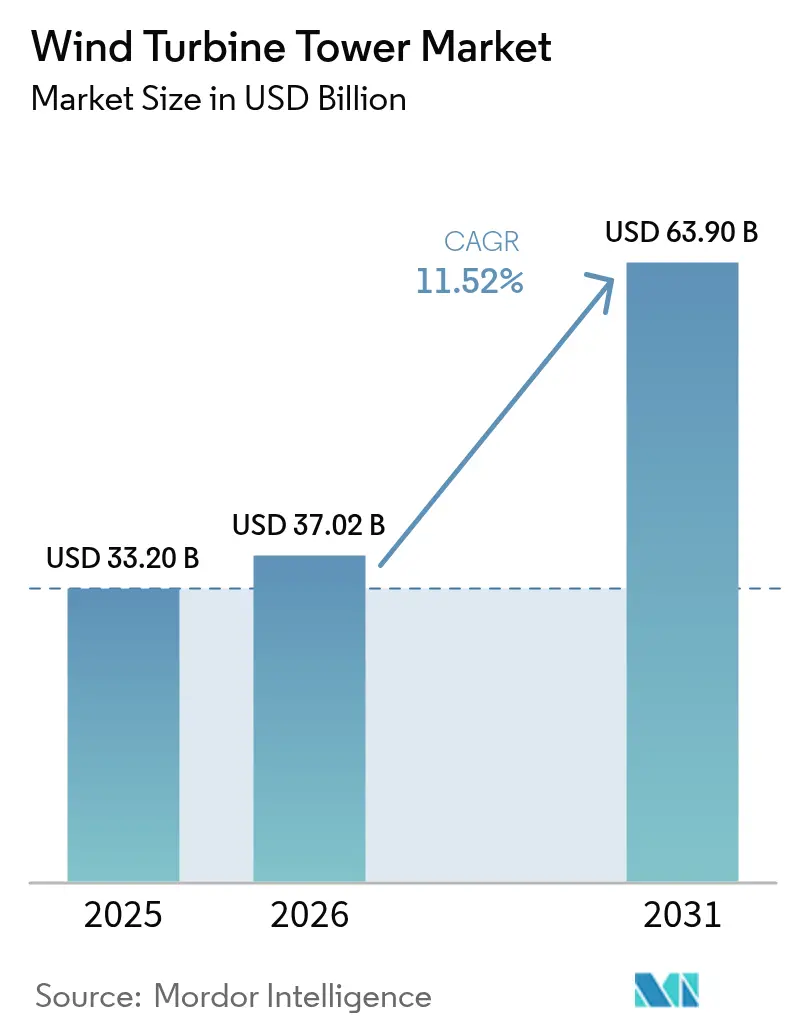

| Market Size (2026) | USD 37.02 Billion |

| Market Size (2031) | USD 63.9 Billion |

| Growth Rate (2026 - 2031) | 11.52% CAGR |

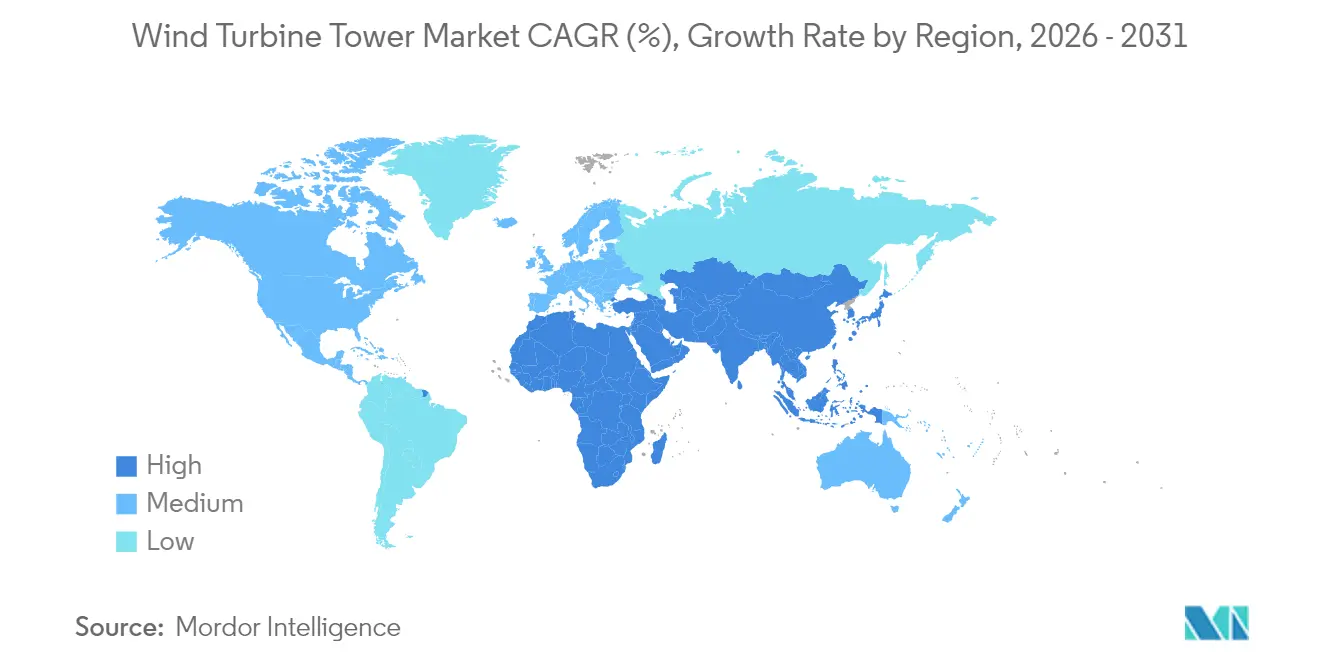

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wind Turbine Tower Market Analysis by Mordor Intelligence

The Wind Turbine Tower market size is expected to grow from USD 33.20 billion in 2025 to USD 37.02 billion in 2026 and is forecast to reach USD 63.9 billion by 2031 at 11.52% CAGR over 2026-2031.

Rapid adoption of towers taller than 160 m, growing hybrid steel-concrete architectures that cut logistics and material costs, and on-site 3D-printed concrete solutions that bypass transport limits are reshaping the competitive field. Localization policies under the United States’ Inflation Reduction Act (IRA) and the European Union’s Carbon Border Adjustment Mechanism redirect global supply chains toward domestic content and low-emission steel. Asia-Pacific retains cost leadership through vertically integrated manufacturing, while the Middle East and Africa record the fastest capacity build-out as sovereign wealth funds bankroll first-wave wind programs. Technology convergence—exemplified by OEMs integrating tower fabrication to secure supply and by heavy-lift logistics innovators targeting 105 m blades—continues to redefine market boundaries.

Key Report Takeaways

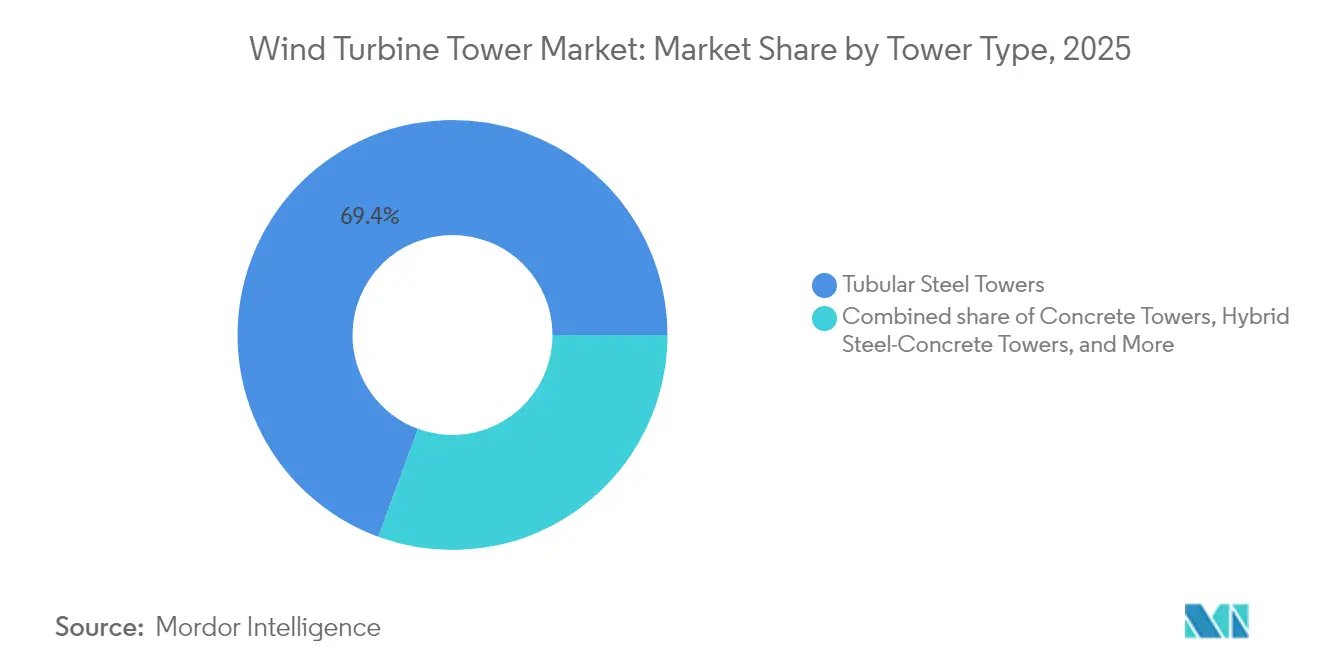

- By tower type, tubular steel led with 69.40% of the wind turbine tower market share in 2025, whereas hybrid steel-concrete towers are forecast to grow at a 12.68% CAGR through 2031.

- By deployment, onshore held 79.30% of the wind turbine tower market size in 2025, while offshore floating platforms are advancing at a 27.35% CAGR to 2031.

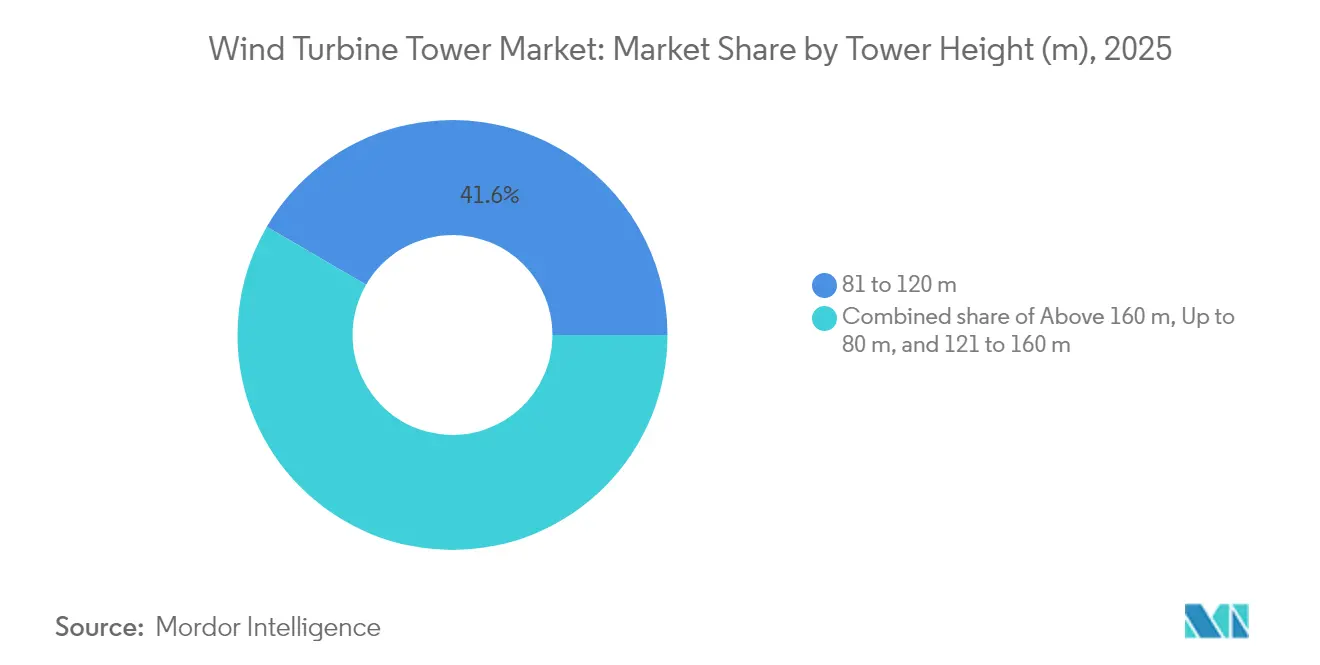

- By height, the 81–120 m segment accounted for a 41.60% share of the wind turbine tower market size in 2025; towers above 160 m deliver the highest growth at 12.88% CAGR.

- By geography, Asia-Pacific commanded 42.70% of 2025 revenue, and the Middle East and Africa wind turbine tower market is expanding at 22.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wind Turbine Tower Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IRA-Driven Localization of >100 m Steel Tower Manufacturing Capacity in the United States | 1.70% | North America, with spillover to Canada and Mexico | Medium term (2-4 years) |

| Permitting Reforms Enabling >160 m Towers in Germany & the Nordics | 1.30% | Europe, primarily Germany, Denmark, Sweden, Norway | Short term (≤ 2 years) |

| Hybrid Steel-Concrete Towers Cutting LCoE for Low-Wind Inland Sites in India & China | 2.00% | Asia-Pacific core, with adoption spreading to Southeast Asia | Medium term (2-4 years) |

| EU Carbon Border Adjustment Accelerating Adoption of Green-Steel Towers | 0.90% | Global, with primary impact in Europe and import-dependent regions | Long term (≥ 4 years) |

| Surging South-Korean & Japanese Offshore Targets for >150 m Corrosion-Resistant Towers | 1.60% | Asia-Pacific, with technology transfer to other offshore markets | Medium term (2-4 years) |

| On-site 3D-Printed Concrete Towers Slashing Logistics Costs in California & Spain Pilots | 1.10% | North America & Europe initially, global scaling potential | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

IRA-driven localization of Over 100 m steel tower capacity in the United States

Domestic-content rules embedded in the IRA have triggered USD 2 billion of tower factory announcements across the Midwest, drawing global leaders such as CS Wind and Arcosa into dual-shore production strategies that balance U.S. demand with Asian cost bases.[1]CS Wind Corporation, “Investor Presentation 2025,” cswind.comNew plants are engineered for >120 m sections, eliminating historical import dependence and raising regional competence for ultra-tall designs. Order inflows at Broadwind surged 85% in Q4 2024, demonstrating that localized supply now achieves competitive scale.

Permitting reforms enabling >160 m towers in Germany & the Nordics

Berlin’s 2024 “Onshore Wind Law” cut approval timelines by 40%, unleashing a queue of extreme-height projects, including the 364 m Lusatia installation now operational. Coordinated Nordic height caps allow developers to tap steadier high-altitude winds, compelling OEMs to refine load-management software and noise envelopes on next-generation turbines.[2]PNE Group, “Projects & Pipeline,” pne-ag.com

Hybrid steel-concrete towers cutting LCoE for low-wind inland sites in India & China

Hybrid architecture substitutes a concrete base for 40% of steel, enabling >160 m heights without oversize road freight, thus unlocking marginal inland wind resources. Suzlon’s record 5.1 GW order book—including a 1,166 MW contract from NTPC Green Energy—validates the economics of this design shift. Nordex’s 179 m hybrid model similarly targets Southeast Asian sites where wind speeds average <6 m/s.

EU carbon border adjustment accelerating adoption of green-steel towers

The upcoming levy prices embedded emissions, prompting OEMs and steelmakers to co-develop low-carbon plate. Vestas and ArcelorMittal delivered 66% emissions cuts on Baltic Power prototypes, while Ørsted and Dillinger secured ≥55% reductions for 2027 foundations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seaborne Logistics Bottlenecks for >15 m-Diameter Tower Sections on U.S. East Coast | -0.90% | North America, particularly US East Coast ports | Short term (≤ 2 years) |

| Volatility in Heavy-Plate Steel Prices Distorting Cost Models | -1.30% | Global, with acute impact in steel-import dependent regions | Medium term (2-4 years) |

| Delayed Type-Certification for Hybrid Towers in Emerging Markets | -0.70% | Emerging markets in Asia-Pacific, Latin America, and Africa | Medium term (2-4 years) |

| Local-Content Quotas Constraining Import of Low-Cost Asian Towers | -1.00% | Global, with varying intensity by country | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Seaborne logistics bottlenecks for >15 m-diameter tower sections on the U.S. East Coast

Jones Act rules limit foreign vessels, creating a scarcity of heavy-lift ships needed for XXL-diameter sections. Port staging yards and crane upgrades lag demand, forcing modular at-sea assembly or floating foundation workarounds that add cost and time.

Volatility in heavy-plate steel prices distorting cost models

Spot plate prices whipsawed ±40% between 2023-2025, eroding the reliability of fixed-price EPC bids. Valmont flagged steel tariffs as a top risk in its 2025 outlook, compelling developers to use index-linked contracts and layered hedges.[3]Valmont Industries, “Q1 2025 Results,” valmont.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tower Type: Hybrid innovation challenges steel dominance

Hybrid steel-concrete towers captured 18.20% of 2025 installations and are forecast to grow 12.68% annually to 2031 as transportation-friendly modules allow >160 m hub heights without escorted road convoys. Concrete savings of up to 40% improve economics, especially in India and China, where local content mandates reward cement sourcing. Nordex’s in-house hybrid line underpins the firm’s largest-ever 179 m tower deployment, while Vestas-backed Modvion’s laminated timber prototype signals a second material revolution beyond steel and concrete. The wind turbine tower market continues to lean on tubular steel for mass production, yet hybrid options are closing the cost gap as raw-plate volatility persists.

OEMs racing toward vertical integration highlight strategic value capture. GE Vernova’s Missouri plant retrofit now outputs flange-ready hybrid sections, shrinking supplier lists and tightening quality control. Independent fabricators respond by upgrading circumferential welding robots and shifting toward corrosion-resistant coatings to defend their share in the wind turbine tower market.

By Deployment: Floating offshore drives next growth wave

Onshore still represented 79.30% of 2025 builds, but floating foundations post a 27.35% CAGR as Japan targets 45 GW by 2040 and South Korea advances a 14-company consortium. Deeper water unlocks class-leading 11–15 m/s wind regimes, translating to higher capacity factors and longer revenue streams. Fixed-bottom offshore projects remain critical near-term, funneling experience and supply chains that derisk floating roll-outs. Saipem7’s EUR 43 billion backlog illustrates how marine EPC consolidation aligns with escalating project scale.

Logistics innovators are redefining deployment segmentation: Radia’s WindRunner aircraft plans to deliver 105-m blades directly to inland plateaus, potentially rebalancing the cost equation between coastal floating farms and high-resource onshore zones. Such advances broaden the addressable opportunity for the wind turbine tower market.

By Tower Height: Ultra-Tall Installations Reshape Economics

The 81–120 m band retained 41.60% of the wind turbine tower market share in 2025, balancing manufacturability and power output, while the above-160 m category recorded 12.88% growth as permitting reform in Europe unlocked extreme-height projects. Germany’s new 364 m prototype confirmed that towers once deemed uneconomic can now operate reliably, signaling a shift in developer risk appetite for taller structures. Installations shorter than 80 m remain confined to repowering or space-restricted sites, and the 121–160 m zone has become the tipping point where hybrid steel-concrete solutions outcompete all-steel designs on cost. Tower height is now tightly linked to wind resource quality because inland, low-wind locations need taller hubs to reach profitable capacity factors.

Regional differences mirror wind profiles and policy frameworks. Europe leads ultra-tall adoption thanks to streamlined approvals and deep supply chains, while Asia-Pacific scales mid-height hybrids for rapid inland rollout. GE Vernova’s 2.7 GW capacity expansion is geared to fabricate longer sections for projects exceeding 160 m, illustrating OEM commitment to the emerging size class. Growth above 160 m still hinges on upgraded roads, rail, and port cranes; limited infrastructure drives demand for modular segments and on-site assembly that lowers transport hurdles. The feedback loop between rising tower height and logistics innovation suggests continued polarization of design strategies at both the sub-80 m and ultra-tall ends of the spectrum, reinforcing diversification within the wind turbine tower market size and technology mix.

Geography Analysis

Asia-Pacific’s 42.70% share in 2025 flowed from China’s giga-scale steel plate mills and India’s rapid hybrid adoption. Yet the spotlight shifts to higher-margin offshore and tall-tower segments as land constraints tighten. Japan’s Round 3 auction launches 1.8 GW of 15 MW class turbines, mandating corrosion-resistant towers that elevate regional average selling prices. Simultaneously, South Korea allocates CAPEX to a 6 GW floating pilot cluster off Ulsan, accelerating demand for 160 m monopiles and 200 m hybrid towers.

Europe leverages regulatory foresight to punch above its weight. Streamlined German permitting shaved 18 months from project cycles, rewarding early movers PNE and RWE. EU carbon-border charges shift procurement towards green steel, letting Vestas lock in low-carbon plate at Baltic Power and Nordlicht. Such sustainability premiums buttress European export competitiveness as the wind turbine tower market globalizes.

The Middle East & Africa grows 22.90% annually from a low base as sovereign funds in Saudi Arabia and the UAE bankroll 1–3 GW clusters integrated with green hydrogen hubs. North America’s IRA-fuelled factory buildout is shrinking import dependence; CS Wind’s Texas ramp-up feeds both U.S. and Latin American demand. South America eyes grid upgrades—Brazil’s northeast state-run transmission plan alone frees 9 GW of interconnection—re-energizing the regional project pipeline.

Regulatory Landscape

Policy is tightening around origin, sustainability, and technical compliance for wind-tower supply chains. In the European Union, Regulation (EU) 2024/1735 (Net-Zero Industry Act) frames priority manufacturing in Europe for net-zero technology, while the Commission updated trade enforcement with Commission Implementing Regulation (EU) 2026/198 amending anti-dumping duties on Chinese utility-scale steel wind towers. Commission Implementing Regulation (EU) 2026/718 (published March 2026) also sets minimum environmental sustainability requirements for public procurement of net-zero technologies, applying to procurement procedures launched on or after 30 June 2026. This raises documentation needs around materials and emissions attributes for tower bids.

Standards and national rules are shifting tower design and materials qualification requirements. IEC updates for tower and foundation design (IEC 61400-6:2020+AMD1:2025) were approved for European adoption in 2025, and the wind turbine design standard update (IEC 61400-1:2019/A1:2026) became available in March 2026, tightening alignment between turbine loads and tower and foundation verification. In China, GB/T 28410-2025 for structural steel plate used in wind power towers implemented on 1 March 2026, influencing plate specifications and supplier qualification for domestic tower fabrication. In the United States, a Presidential Determination issued 23 April 2026 under the Defense Production Act (Section 303) signaled additional federal backing for energy infrastructure manufacturing, reinforcing the push to expand domestic capability alongside IRA-driven local-content requirements.

Competitive Landscape

The wind turbine tower market displays moderate fragmentation: the top five firms held roughly 45% revenue in 2024 as OEMs moved upstream. CS Wind and Titan Wind Energy excel at high-volume steel fabrication, while Vestas and Nordex pursue in-house hybrid lines to de-risk supply. GE Vernova’s 3D-printing alliance with COBOD and LafargeHolcim exemplifies technology-led differentiation that compresses logistics costs for 200 m units.

Strategic partnerships focus on material transitions. Vestas–ArcelorMittal and Ørsted–Dillinger embed low-carbon plate into flagship projects, creating brand equity around emissions intensity. Meanwhile, independent fabricator Windar leverages modular offshore tower kits to circumvent U.S. port constraints, signaling niche opportunities for flexible engineering. Market entry barriers remain moderate: capital outlays for automated rolling and welding lines run USD 120 million, yet software, certification, and logistics expertise increasingly define competitive advantage across the wind turbine tower market.

Wind Turbine Tower Industry Leaders

CS Wind Corporation

Titan Wind Energy

Vestas

Arcosa Wind Towers Inc.

Valmont Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

EU public procurement sustainability requirements apply to procedures launched from 30 June 2026, creating a compliance focus for suppliers that certify lower-embedded emissions, traceability, and compliant steel plate standards in tower procurement for onshore and offshore projects. A practical reference point is the Thor offshore wind farm in Denmark, where offshore turbines with CO2-reduced steel towers are being deployed, with Salzgitter AG supplying the steel.

Localization and automation for larger diameters and heavier plates required by 15 MW+ offshore builds and ultra-tall onshore towers are moving forward through capacity expansions and automated processes. The Baltica 2 offshore project illustrates this with a 200 million euro investment in a Gdansk manufacturing facility, supporting nearby buildouts and reducing transport lead times, while rolling-line upgrades and controls improve conical section precision for offshore towers and foundations.

Recent Industry Developments

- July 2026: Titan Wind Energy secured an offshore wind equipment contract for the Huaneng Yangjiang Sanshandao II project covering 19 jacket foundations and 16 pin piles. The award expands heavy offshore fabrication capacity for jacket and pin piles and aligns with demand for larger rolling capacity and marine-grade corrosion protection for offshore structures.

- March 2026: Baltic Towers and Siemens Gamesa announced a 200 million euro investment in a Gdansk manufacturing facility to support the Baltica 2 offshore project. The investment creates local production capacity for oversized components and reduces transport lead times by colocating critical fabrication steps near the Baltic Sea buildout.

- July 2025: ORLEN installed its first Baltic Power turbine, marking Poland's entry into large-scale offshore wind. The milestone advances the Baltic Sea supply chain and highlights the importance of regional manufacturing hubs such as Gdansk for oversized components.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue earned from supplying wind turbine towers used to support nacelles and rotor assemblies in onshore and offshore wind farms, including towers sold as part of new turbine installations and tower replacements.

Scope exclusions: It excludes foundations, blades, nacelles, generators, and civil works that are not part of the tower supply contract.

Segmentation Overview

- By Tower Type

- Tubular Steel Towers

- Concrete Towers

- Hybrid Steel-Concrete Towers

- Lattice Towers

- Guyed Pole Towers

- Modular/Stacked Composite Towers

- By Deployment

- Onshore

- Offshore (Fixed-Bottom)

- Offshore (Floating)

- By Tower Height (m)

- Up to 80 m

- 81 to 120 m

- 121 to 160 m

- Above 160 m

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Denmark

- Sweden

- Norway

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

We started with desk research to set the base demand pool and the main supply chain signals for wind turbine towers, since tower demand usually follows new wind capacity additions and repowering timing. Public sources were used to map annual wind installations and policy direction, such as IEA renewables statistics, IRENA datasets, Global Wind Energy Council releases, and national energy agencies that publish auction results and grid connection plans.

To translate installations into tower value, we reviewed engineering and trade signals that help anchor weights, materials, and pricing ranges, such as USGS steel data, customs import-export statistics for tower sections, and peer-reviewed papers on tower design trends and hub height shifts. Company filings, investor presentations, and reputable industry press were checked to confirm capacity expansions and regional shipment patterns. Where public disclosure was thin, we used a paid subscription for company financials and a shipment-level import-export database selectively. The sources mentioned are illustrative only, and many other public and paid references were also used for cross-checks and clarification.

Primary Interviews and Surveys

Primary work was used to test assumptions that desk sources do not explain well, especially tower ASP movement, localization levels, and how offshore fixed-bottom and floating towers are being priced and procured. We spoke with a mix of tower manufacturers, steel and plate processors, EPC and installation participants, and wind project owners across major wind build regions, so regional differences in transport constraints and tower height preferences could be reflected. Inputs from these discussions were then used to confirm demand splits, validate conversion ratios from GW additions to tower units, and tighten the model where public data showed gaps.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | APAC: 49% |

| Mid tier: 57% | Functional/Unit leaders: 32% | EMEA: 32% |

| Smaller Players: 18% | Managers: 55% | Americas: 19% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, where global and regional wind capacity additions and repowering plans were reconstructed and then translated into tower demand through average towers per turbine, typical tower heights, and the onshore versus offshore deployment mix. After setting the demand pool, pricing was applied using region-sensitive ASP bands that reflect steel input trends, transport distance penalties, local content rules, and the share of concrete or hybrid designs.

For validation, we ran selective bottom-up approximations, including supplier roll-ups from announced tower capacity, sampled contract pricing, and channel checks on tower section movements through ports for import-dependent markets. When a country-level data point was missing, we used nearby markets with similar turbine ratings and logistics constraints as proxies, then adjusted using expert feedback. Forecasts were generated using scenario analysis supported by multivariate regression checks, where drivers like annual wind additions, auction pipelines, offshore project FIDs, steel price indices, and average hub height progression were tested for sensitivity before finalizing the outlook.

Data Validation & Update Cycle

Before sign-off, outputs were checked against independent signals such as annual GW installed, turbine shipment trends, and regional tower manufacturing utilization, then any large variances were investigated at the country and segment level. We also ran anomaly checks on implied ASPs so the model did not drift away from what buyers and suppliers described as workable pricing under current steel and freight conditions.

A second analyst review was completed to re-check formulas, assumptions, and unit conversions, followed by targeted re-contacts when a number looked out of pattern for a region or deployment type. The report is refreshed annually, and interim updates are made when major policy shifts, large offshore awards, or material input shocks change the near-term market. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Wind Turbine Tower Market Size Compared Against Other Published Estimates

Different published market sizes for wind turbine towers can vary because the counted items, the year used for pricing, and how offshore projects are timed do not always align. Some studies also combine tower supply value with adjacent balance of plant packages, which can change the total quickly when large offshore projects are included.

Foundations and monopiles sit outside Mordor Intelligence's scope, which is one reason our 2026 value can look higher or lower than figures that bundle substructures or other wind hardware into a single tower line item. Other gaps usually come from how tower ASP escalation is handled during steel price swings, whether replacement towers for repowering are counted, and how currency conversion is timed for multi-region totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 37.02 B (2026) | |

| Global Consultancy A | USD 29.94 B (2024) | Uses an earlier base year and pricing set, and the tower value can be anchored closer to 2024 steel and freight conditions, which reduces the implied ASP for taller towers in high logistics cost regions. |

| Industry Research Group B | USD 28.00 B (2024) | Often presented as a broader wind tower view with different timing for offshore awards and commissioning, and repowering tower replacements can be treated inconsistently across regions, which shifts the total. |

Taken together, the spread is mainly explained by the counted scope items, the year used for pricing, and how offshore timing and repowering are treated. Our estimate stays traceable because each step is tied back to capacity additions, tower unit conversion, and region-level ASP checks that can be repeated and updated as new project and input cost data becomes available.

Key Questions Answered in the Report

What is the projected size of the wind turbine tower market by 2031?

The wind turbine tower market size is forecast to reach USD 63.9 billion by 2031.

Which region is growing fastest for tower installations?

The Middle East and Africa is the fastest, posting a 22.90% CAGR through 2031.

Why are hybrid steel-concrete towers gaining traction?

They enable Above 160 m hub heights while reducing steel use by up to 40%, improving economics on low-wind inland sites.

How is the IRA influencing U.S. tower manufacturing?

Domestic-content incentives have spurred USD 2 billion in new Midwestern factories designed for >120 m sections.

What technology trend could disrupt traditional fabrication?

On-site 3D-printed concrete towers are moving toward commercial deployment for 200 m structures, cutting logistics costs.

How are green steel initiatives affecting procurement?

EU carbon-border rules create a price differential that encourages OEMs to integrate low-emission plate into tower supply chains, reducing life-cycle emissions by more than 60%.

Page last updated on: