Market Overview

| Study Period | 2021 - 2031 |

|---|---|

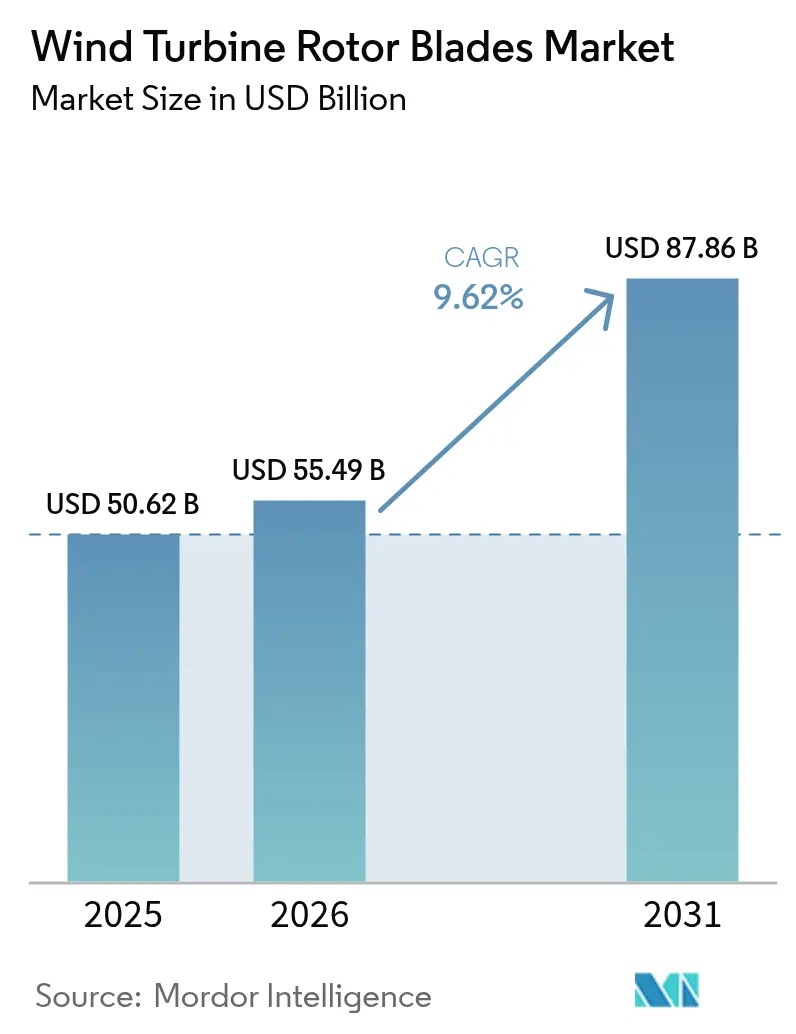

| Market Size (2026) | USD 55.49 Billion |

| Market Size (2031) | USD 87.86 Billion |

| Growth Rate (2026 - 2031) | 9.62% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wind Turbine Rotor Blades Market Analysis by Mordor Intelligence

Wind Turbine Rotor Blades Market size in 2026 is estimated at USD 55.49 billion, growing from 2025 value of USD 50.62 billion with 2031 projections showing USD 87.86 billion, growing at 9.62% CAGR over 2026-2031.

Capacity additions in offshore wind, the pivot toward 15 MW-plus turbines, and rapid advances in hybrid composites are shaping demand. Blade manufacturers are embracing segmented, 70 m+ formats to overcome road-haul limits, while policy incentives in the United States and Europe are stimulating localized production. Asia-Pacific retains a manufacturing cost edge, yet regional supply chains face pressure from chronic carbon-fiber shortages that inflate input costs. Opportunities are emerging for firms combining vertical integration with recyclable materials, advanced lightning protection, and remote monitoring solutions that reduce lifetime maintenance expenditure.

Key Report Takeaways

- By location of deployment, onshore retained 82.35% wind turbine rotor blade market share in 2025, whereas offshore blades are projected to expand at a 29.9% CAGR through 2031.

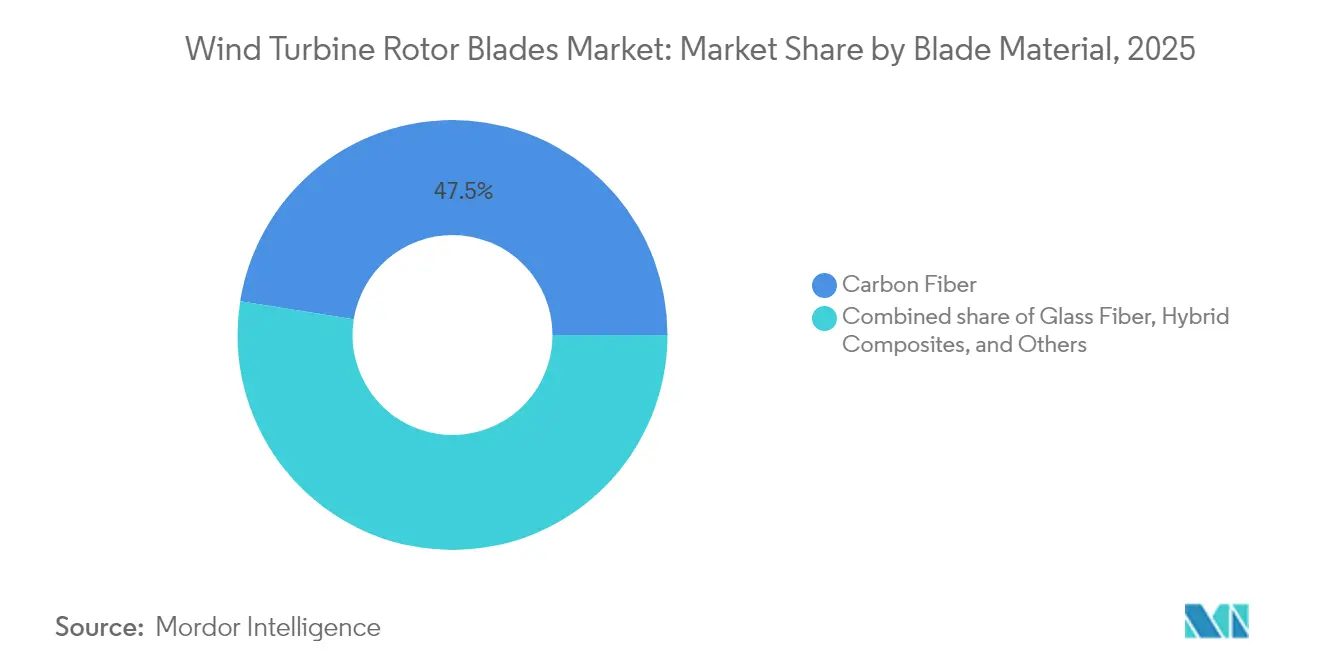

- By blade material, carbon fiber dominated with 47.50% share in 2025; hybrid composites are forecast to post 10.39% growth, the fastest among material types.

- By blade length, the 61-75 m category led with 44.30% share of the wind turbine rotor blade market size in 2025, while blades above 75 m are advancing at 12.85% CAGR to 2031.

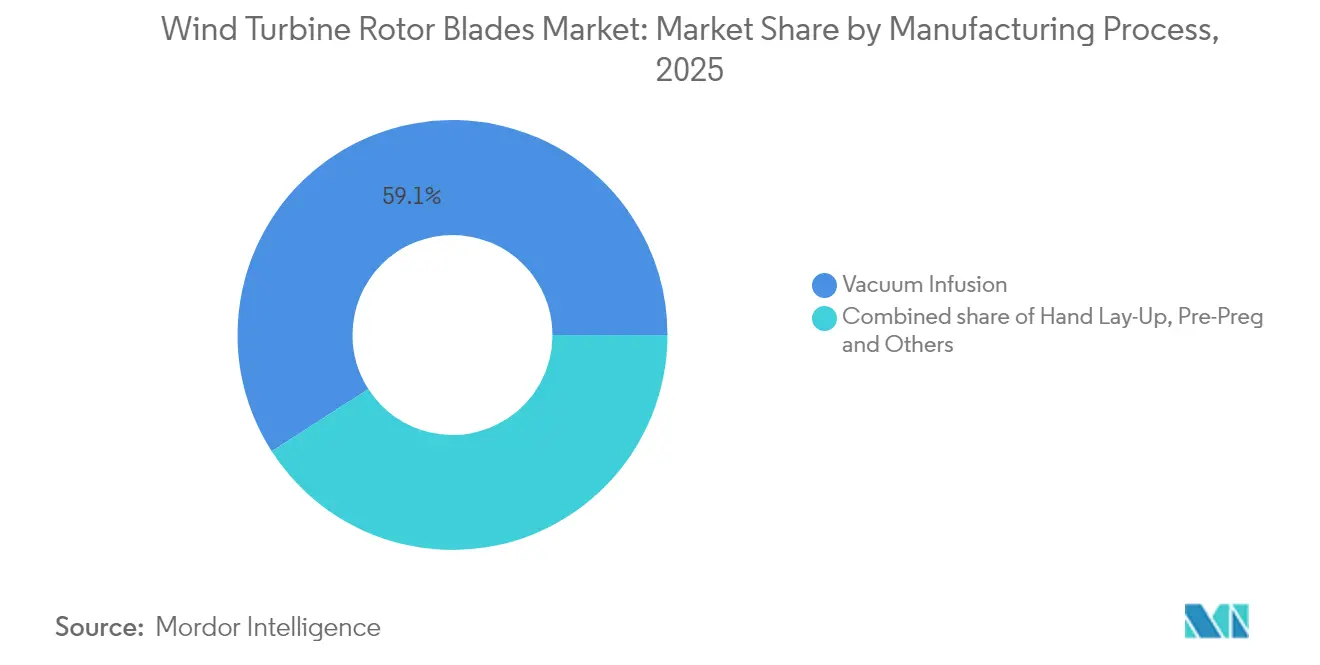

- By manufacturing process, vacuum infusion accounted for 59.10% of production in 2025; pre-preg lines are accelerating at a 10.24% CAGR amid tighter tolerances for offshore blades.

- By geography, Asia-Pacific commanded 52.40% of global revenue in 2025, whereas the Middle East and Africa wind turbine rotor blade market is projected to grow at a 28.15% CAGR to 2031.

- LM Wind Power, TPI Composites, and Siemens Gamesa jointly held more than 35% wind turbine rotor blade market share in 2025, underlining moderate consolidation within the sector.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wind Turbine Rotor Blades Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid scale-up of >5 MW turbines in Chinese coastal provinces | +1.5% | Asia-Pacific core, spill-over to global supply chains | Medium term (2-4 years) |

| US Inflation Reduction Act production tax credits catalyzing domestic blade output | +1.2% | North America & EU, indirect global impact | Short term (≤ 2 years) |

| EU REPowerEU plan accelerating repowering of post-2010 onshore fleets | +0.8% | Europe core, technology transfer to emerging markets | Medium term (2-4 years) |

| OEM demand for 70 m+ modular blades to cut transport bottlenecks | +0.6% | Global, with early gains in land-locked regions | Long term (≥ 4 years) |

| Brazil's FINAME green-financing unlocking local blade capacity | +0.5% | South America, potential replication in MEA | Medium term (2-4 years) |

| Floating-offshore demonstrators transitioning to serial 100 m blade orders | +0.4% | North America & EU, expansion to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid scale-up of Above 5 MW turbines in Chinese coastal provinces

China installed 31.4 GW of offshore capacity by 2024, and most new projects now specify 15 MW machines that need 100 m-plus blades.[1]Offshore Wind, “China Tops Global Offshore Wind Additions,” offshorewind.bizManufacturers such as Goldwind are expanding Jiangsu and Guangdong factories to build ultra-large composite structures. High domestic volumes shorten learning curves, lower per-unit costs, and accelerate technology diffusion to export markets. This dynamic allows Chinese suppliers to bid aggressively in global tenders, compelling European and US rivals to invest in cost-cutting automation. The resulting competition heightens the strategic importance of secure carbon-fiber supply and modular tooling that can handle 120 m form factors, reinforcing Asia-Pacific’s leadership in the wind turbine rotor blade market.

US Inflation Reduction Act production tax credits catalyzing domestic blade output

Section 45X grants USD 0.02 per blade produced in the United States, making local manufacturing viable despite higher labor costs.[2]U.S. Department of Energy, “Advanced Manufacturing Production Credits,” energy.gov TPI Composites has already reached its 100,000-blade milestone and is adding new US lines. The 10-year credit horizon reduces investment risk, attracting European and Asian partners that seek compliant supply chains. Rising domestic content thresholds encourage material suppliers to co-locate, reshaping logistics flows inside North America. Resultant spending boosts overall installations, reinforcing a virtuous circle for the wind turbine rotor blade market.

EU REPowerEU plan accelerating repowering of post-2010 onshore fleets

REPowerEU aims for 50% wind power by 2050, driving a wave of blade-only upgrades on turbines commissioned after 2010. Streamlined permits cut project timelines, with German and Danish farms swapping in longer, lighter blades that lift energy capture by up to 30%. The strategy maximizes output without new foundations, making retrofit economics attractive even in high-cost markets. Blade suppliers are designing “plug-and-play” formats that fit existing hub interfaces while embedding new aerofoil and lightning protection features. These niche products extend the revenue mix beyond greenfield installations, diversifying earnings across the wind turbine rotor blade market.

OEM demand for 70 m+ modular blades to cut transport bottlenecks

Segmented blade designs led by Nabrawind’s Nabrajoint let 100 m blades navigate standard roads, trimming USD 100 000–150 000 per load in logistics expense. The concept is gaining traction in landlocked Europe, India, and Latin America, where road curvature and bridge clearance limit conventional hauls. Modular assembly near the site reduces breakage risk and accelerates installation. Parallel innovations such as Radia’s WindRunner aircraft could move 300-foot blades directly to remote hubs, further opening high-yield wind corridors. Together, these breakthroughs expand geographical reach and sustain growth momentum for the wind turbine rotor blade market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic carbon-fiber supply tightness | -0.90% | Global, most acute in offshore segments | Short term (≤ 2 years) |

| Higher LCOE penalty for sub-2 MW turbine classes | -0.70% | Europe and North America legacy fleets | Medium term (2-4 years) |

| Logistics restrictions on >80 m blades in land-locked European regions | -0.5% | Europe core, emerging in mountainous regions globally | Long term (≥ 4 years) |

| Offshore de-commissioning liability tightening project bankability | -0.3% | North America & EU offshore markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic carbon-fiber supply tightness inflating input costs

Aerospace recovery and electric-vehicle growth have lifted carbon-fiber prices by 15-20% since 2024. Offshore blades now use carbon in spar caps and root sections that account for 40% of total weight, making supply bottlenecks critical. Chinese producers, who hold 60% of global capacity, prioritize higher-margin sectors, squeezing wind allocations. Blade makers respond with hybrid lay-ups that spare the scarcest grades, yet each redesign triggers new certification cycles and adds cost. Firms are eyeing backward integration into fiber production to control availability and stabilize margins across the wind turbine rotor blade market.

Higher LCOE penalty for sub-2 MW turbine classes suppressing blade retrofit

Lazard’s levelized cost models show a 20-30% penalty for maintaining turbines below 2 MW relative to modern 3-5 MW units.[4]Lazard, “Levelized Cost of Energy v17.0,” lazard.com Owners of early-2000s fleets face poor economics for blade-only upgrades and instead favor site redevelopment. This cuts the addressable refurbishment volume and redirects demand to full-scale replacements or greenfield builds. Blade suppliers concentrate R&D on larger formats and specialized offshore products, reshaping capacity planning throughout the wind turbine rotor blade market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location of Deployment: Offshore surge reshaping dynamics

Offshore blades posted a 29.9% CAGR between 2025 and 2031, even as onshore commanded 82.35% revenue in 2025. Floating prototypes are shifting into serial 100 m orders that require corrosion-resistant coatings and advanced lightning arrestors, adding 15-20% to build cost. Europe’s pipeline and China’s coastal megaprojects sustain large-scale demand. Conversely, onshore growth hinges on modular solutions that overcome road limits while tapping high-quality inland wind corridors. Cost-efficient series production under vacuum infusion helps protect margins in this high-volume part of the wind turbine rotor blade market.

Longer term, the offshore pipeline’s depth ensures continued share gains. North Sea leases, US Atlantic approvals, and Japanese floating tenders underpin multi-gigawatt orders for the next decade. Onshore will remain essential for market balance; yet its role increasingly revolves around retrofitting mature sites and serving emerging economies where quick-turn installations match policy timelines. Suppliers that align product roadmaps with these divergent needs can defend or expand their presence across the wind turbine rotor blade market.

By Blade Material: Hybrid composites challenging carbon fiber

Carbon fiber dominated 47.50% of the market share in 2025 owing to unmatched stiffness-to-weight ratios, but its supply issues and price volatility are steering OEMs to hybrid lay-ups. Hybrid composite blades grow 10.39% annually by strategically placing carbon only in load-critical webs while substituting cost-effective glass elsewhere. This design cuts weight by up to 12% over all-glass equivalents and maintains structural margins needed for 15 MW turbines.

Glass fiber remains relevant for onshore blades below 70 m, where transport and tower strength rather than weight drive economics. Meanwhile, research into thermoplastic matrices offers end-of-life recyclability and faster production cycles. Vestas's recyclable carbon fiber thermoplastics trials in 100 m blades illustrate progress. As regulation tightens around circularity, material breakthroughs will influence competitive positioning in the wind turbine rotor blade market.

By Blade Length: Mega-blades driving growth above 75 m

The 61-75 m category retained 44.30% wind turbine rotor blade market share in 2025 because it fits today’s mainstream land-based turbines. However, blades exceeding 75 m are growing at 12.85% CAGR as manufacturers chase 15+ MW ratings. Building blades over 100 m reshapes factory layouts, tooling, and quality regimes. Automated fiber placement and digital twins reduce defect risk while speeding production.

Logistics frames the next hurdle. Road limits and turning radii cap blade length for inland sites; hence, modular tech and novel carriers like the WindRunner aircraft become critical enablers. Under 45 m blades now serve only niche repowering jobs or community-scale turbines. The ongoing length race underscores the strategic weight of R&D capital in the wind turbine rotor blade market.

By Manufacturing Process: Pre-preg innovation accelerating

Vacuum infusion safeguarded a 59.10% share in 2025 by pairing cost efficiency with large-part capability. Yet pre-preg lines are rising 10.24% annually because they deliver tight resin control vital for offshore blades that face salt spray, dynamic loads, and ice accretion. Pre-preg sheets cut void content, so fatigue life improves, and surface finish smoothness lifts aerodynamic efficiency. The trade-off remains higher material and freezer storage costs.

Hand lay-up declines as automation advances. New infusion variants add robotic fabric placement to retain low cost but raise consistency. Thermoplastic tape winding and in-situ consolidation enter pilot scale, promising faster cycle times and recyclability. Selecting the optimal process now hinges on blade length, order volume, and target region, sharpening competitive edges within the wind turbine rotor blade market.

Geography Analysis

Asia-Pacific captured 52.40% of global demand in 2025, anchored by China’s 31.4 GW offshore base and its push toward 15 MW turbines that need 100 m-plus blades. Investments in automated sanding, resin infusion, and modular molds support rapid scaling. Japan and South Korea cultivate floating offshore pilots, while India’s onshore build-out benefits from hybrid composite cost savings. Rising wages and stricter environmental rules are nudging suppliers toward greater automation, yet the region’s scale keeps unit costs low, sustaining leadership in the wind turbine rotor blade market.

Europe’s mature fleet now pivots to repowering and deep-water projects. The REPowerEU drive accelerates blade upgrades on post-2010 turbines, and the UK alone targets 115 GW offshore by 2050 with 35% floating share. Landlocked Alpine and Balkan zones force the adoption of segmented blades that can move through tight passes. Regulation favors recyclability, spurring materials R&D partnerships between blade makers and chemical companies. European OEMs leverage advanced design and sustainability credentials to maintain a premium segment edge.

The Middle East and Africa’s 28.15% CAGR through 2031 reflects Saudi, Emirati, and Egyptian wind targets that could lift regional capacity to 131 GW. Harsh climates demand leading-edge coatings resistant to sand erosion. Domestic content clauses begin to surface, heralding new assembly plants near Red Sea and Gulf ports. North America’s trajectory centers on IRA incentives that relocalize supply chains, while South America’s Brazil-led momentum hinges on FINAME green finance. Collectively, these regional vectors diversify revenue streams and buffer suppliers against single-market shocks in the wind turbine rotor blade market.

Competitive Landscape

Competition is moderately concentrated. LM Wind Power, TPI Composites, and Siemens Gamesa accounted for over one-third of global deliveries in 2024, benefitting from scale economies and broad product portfolios. Consolidation continues as smaller firms struggle with rising certification costs and carbon-fiber shortages. Leaders pursue vertical integration into materials and structural testing to secure supply and cut lead times.

Strategically, localization shapes new investments. TPI’s US expansion exploits IRA credits, while CS Wind’s USD 200 million Vietnam plant underpins cost-competitive exports to Asia-Pacific and the Middle East. R&D pipelines focus on segmented blades, recyclable thermoplastics, and predictive maintenance sensors that flag lightning strikes or leading-edge erosion. Digital twin models track strain in real time, enabling condition-based maintenance and lowering lifetime cost per kWh.

White-space innovation attracts start-ups. Radia’s WindRunner targets remote onshore sites, and Nabrawind’s Nabrawind Nabrajoint modular interface gains OEM endorsements. Materials specialists scale bio-based resins that cure at lower temperatures, cutting energy usage. Success now hinges on balancing mass-production prowess with bespoke engineering, a dynamic that will continue to define hierarchy in the wind turbine rotor blade market.

Wind Turbine Rotor Blades Industry Leaders

LM Wind Power (GE Renewable Energy)

Siemens Gamesa Renewable Energy

TPI Composites Inc.

Vestas Wind Systems A/S

Nordex SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Energiequelle commissioned two Enercon turbines in Germany, illustrating Europe’s repowering focus. The project replaced older, less efficient turbines (E-58 models) with two new turbines, each with a capacity of 5.56 MW.

- May 2025: The USD 5 billion Empire Wind project off New York resumed construction, reaffirming US offshore momentum. The project, which the Trump administration previously delayed, is a significant renewable energy initiative for the United States.

- September 2024: CS Wind is pouring USD 200 million into a new wind turbine blade manufacturing facility in Long An Province's Southeast Asia Industrial Zone, Vietnam. This move bolsters their capacity in Southeast Asia and emphasizes their commitment to producing both onshore and offshore wind turbine towers.

- June 2024: Vestas, a prominent wind turbine manufacturer, is set to establish a new blade factory at Leith Docks in Scotland. This move aims to bolster North Sea offshore wind projects. The upcoming facility will specifically manufacture blades for the V236-15.0 MW offshore wind turbine, a pivotal element in the swiftly expanding offshore wind sector.

Global Wind Turbine Rotor Blades Market Report Scope

Wind turbine rotor blades are the key components of wind turbines, as they are in direct contact with high-speed winds. Rotor blades convert wind's kinetic energy into rotational energy, which is later converted into electrical energy. The global wind turbine rotor blade market is segmented by location of deployment, blade material, and geography. By location of deployment, the market is segmented into onshore and offshore. By blade material, the market is segmented by carbon fiber, glass fiber, and other blade materials. The report also covers the market size and forecasts for the wind turbine rotor blade market across major regions, namely North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done based on revenue (USD Billion).

By Location of Deployment

| Onshore |

| Offshore |

By Blade Material

| Glass Fiber |

| Carbon Fiber |

| Hybrid Composites |

| Others |

By Blade Length

| Below 45 m |

| 46 to 60 m |

| 61 to 75 m |

| Above 75 m |

By Manufacturing Process

| Hand Lay-Up |

| Vacuum Infusion |

| Pre-Preg |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Denmark | |

| Sweden | |

| Norway | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Location of Deployment | Onshore | |

| Offshore | ||

| By Blade Material | Glass Fiber | |

| Carbon Fiber | ||

| Hybrid Composites | ||

| Others | ||

| By Blade Length | Below 45 m | |

| 46 to 60 m | ||

| 61 to 75 m | ||

| Above 75 m | ||

| By Manufacturing Process | Hand Lay-Up | |

| Vacuum Infusion | ||

| Pre-Preg | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Denmark | ||

| Sweden | ||

| Norway | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the wind turbine rotor blade market today and how fast is it growing?

The market reached USD 55.49 billion in 2026 and is projected to rise to USD 87.86 billion by 2031, registering a 9.62% CAGR during 2026-2031.

Which region currently commands the greatest market share?

Asia-Pacific led with 52.40% of global revenue in 2025, driven by China’s rapid offshore build-out and established manufacturing base.

Why is the offshore segment expanding so quickly?

Commercial-scale projects now specify 15 MW-plus turbines that need 100 m-class blades, pushing offshore demand to a 29.9% CAGR through 2031 and spurring investments in precision manufacturing and corrosion-resistant designs.

How do carbon-fiber supply constraints affect blade producers?

Competing aerospace and automotive demand has lifted carbon-fiber prices by 15-20% since 2024, prompting blade makers to adopt hybrid composite lay-ups and consider backward integration to secure supply.

What policy incentives are reshaping blade manufacturing footprints?

The US Inflation Reduction Act’s Section 45X offers USD 0.02 per domestically produced blade, while the EU’s REPowerEU plan accelerates repowering projects-both driving manufacturers to localize production and upgrade product lines.

What innovations are easing transport bottlenecks for ever-longer blades?

Segmented 70 m-plus blades such as Nabrawind’s Nabrajoint can be hauled on standard roads, and Radia’s planned WindRunner aircraft aims to fly 300-foot blades directly to remote sites, cutting logistics costs and opening new onshore corridors.

Page last updated on: