Automotive Wheel Speed Sensor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

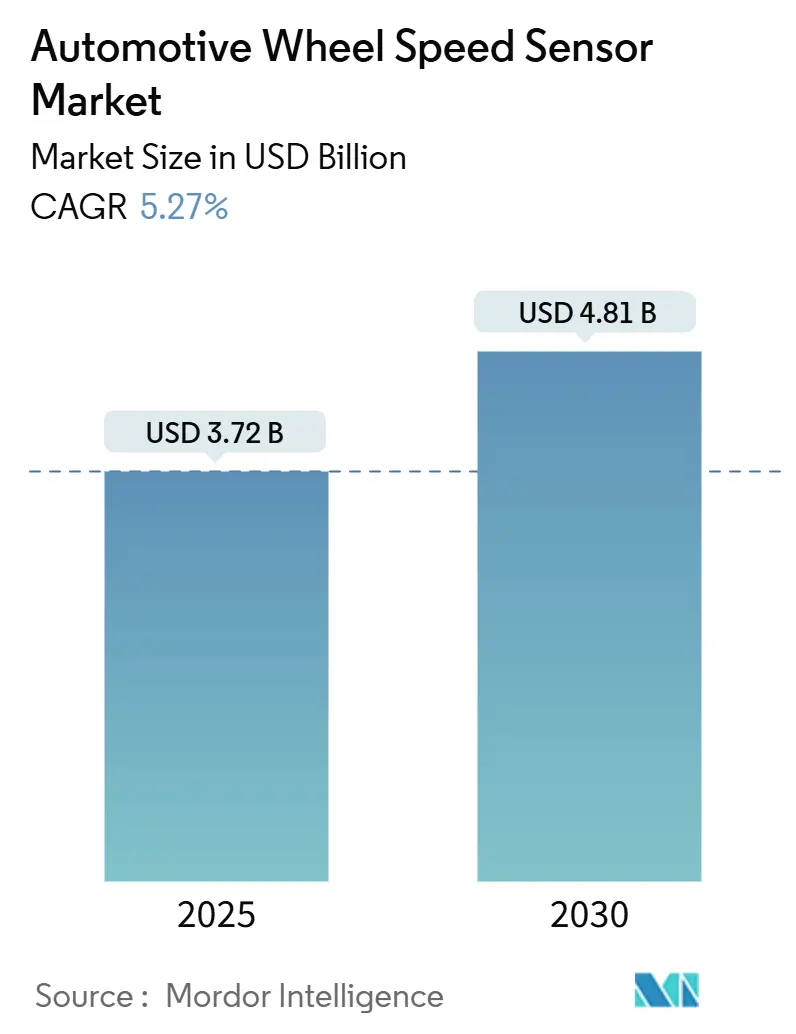

| Market Size (2025) | USD 3.72 Billion |

| Market Size (2030) | USD 4.81 Billion |

| Growth Rate (2025 - 2030) | 5.27% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Wheel Speed Sensor Market Analysis by Mordor Intelligence

The automotive wheel speed sensor market size stands at USD 3.72 billion in 2025 and, at a 5.27% CAGR, is forecast to reach USD 4.81 billion by 2030. The expansion reflects a maturing yet opportunity-rich space where regulatory pushes for active safety, rapid electrification, and software-defined vehicle architectures steadily raise sensor content per vehicle. Mandatory ABS and ESC fitment across emerging economies and stricter safety rules in the European Union and North America prevent demand volatility even as light-vehicle sales fluctuate. Battery-electric powertrains boost per-vehicle sensor counts because regenerative braking and torque-vectoring strategies depend on exact wheel speed data. Automakers are also consolidating wheel speed signals into central ADAS controllers, driving preference for sensors that combine higher accuracy, built-in diagnostics, and cyber-secure CAN-FD interfaces. Competitive intensity is moderate; legacy tier-1s hold sizable shares while semiconductor suppliers move upstream with magneto-resistive and inductive designs that withstand 800 V EMI environments.

Key Report Takeaways

- By sensor type, Hall effect sensors led with 54.22% of the automotive wheel speed sensor market share in 2024, while magneto-resistive sensors are projected to grow at a 6.32% CAGR through 2030.

- By application, anti-lock braking systems accounted for 58.81% of the automotive wheel speed sensor market share in 2024; electronic stability control is forecast to expand at a 6.98% CAGR to 2030.

- By vehicle type, passenger cars represented 63.87% of the automotive wheel speed sensor market share in 2024 and are projected to grow at a CAGR of 5.83% during the forecast period.

- By propulsion, internal-combustion vehicles retained 71.63% of the automotive wheel speed sensor market share in 2024, whereas battery-electric vehicles are expected to advance at a 7.74% CAGR through 2030.

- By distribution channel, OEM fitment captured 83.77% of the automotive wheel speed sensor market share in 2024, and the aftermarket is anticipated to rise at a 5.84% CAGR to 2030.

- By geography, Asia–Pacific dominated with a 46.31% of the automotive wheel speed sensor market share in 2024; the region is set to register the fastest 6.34% CAGR through 2030.

Global Automotive Wheel Speed Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Mandates for ABS/ESC Fitment | +1.2% | Asia–Pacific; spill-over to Middle East and Africa | Medium term (2-4 years) |

| Rapid Electrification Raising Sensor Content | +0.9% | Global | Long term (≥ 4 years) |

| OEM Shift Toward Sensor-Fusion ADAS | +0.7% | North America and Europe; expanding to Asia-Pacific | Medium term (2-4 years) |

| Supply-Chain Near-Shoring Incentives | +0.4% | North America and Europe | Short term (≤ 2 years) |

| Edge-AI Self-Diagnosing Sensors | +0.3% | Global; premium segments | Long term (≥ 4 years) |

| Cyber-Secure CAN-FD Interfaces | +0.2% | Global; premium OEMs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Mandates for ABS/ESC Fitment in Emerging Markets

Phased safety regulations in India, China, and other emerging economies create a guaranteed baseline for annual sensor volumes, insulating suppliers from cyclical light-vehicle sales swings. India’s mandate for ABS on motorcycles above 125 cc and trucks above 3.5 t, along with China’s rule that ESC be fitted to every new energy truck above the same weight class, quickly converted millions of vehicles to active safety-ready platforms. The European Union’s General Safety Regulation extends intelligent speed assistance and autonomous emergency braking to previously exempt categories, indirectly lifting wheel speed sensor demand for sensor-fusion braking stacks[1]“General Safety Regulation,”, European Commission, europa.eu. Such mandates also shorten replacement cycles because every vehicle entering the parc now carries at least four ABS sensors, boosting aftermarket prospects when warranties expire. Tier-1s view these regulations as volume stabilizers, allowing longer amortization of new manufacturing lines despite price pressures.

Rapid Electrification Increasing Per-Vehicle Sensor Content

Battery-electric drivetrains depend on ultra-accurate wheel slip feedback to balance regenerative braking torque on each axle. Higher voltage systems intensify electromagnetic interference, prompting a gradual transition from legacy Hall elements to magneto-resistive or inductive formats that maintain signal integrity. Honda earmarked USD 11 billion for North American EV production by 2030, ensuring multiyear demand visibility for automotive-grade sensing ICs in that region[2]“North America EV Investment Plan,”, Honda Motor Co., global.honda. These dynamics explain why the automotive wheel speed sensor market continues to expand even while overall vehicle builds plateau in mature economies.

OEM Shift Toward Sensor-Fusion ADAS Architectures

Carmakers are collapsing formerly discrete ABS, ESC, and traction control modules into centralized vehicle motion management domains. Bosch demonstrated such consolidation through its Vehicle Motion Management controller that fuses wheel speed with steering and chassis data to predict and pre-empt instability events. ZF’s Smart Chassis Sensor, now standard on a flagship luxury EV, embeds wheel position information inside ball joints, reducing harness runs and feeding richer data to domain controllers. Continental complements these moves with software libraries that ingest encrypted sensor streams for autonomous emergency braking. Centralized architectures raise the minimum spec: throughput, self-diagnostics, and cyber-secure firmware update paths are no longer optional, steering demand toward premium sensors that command higher ASPs.

Supply-Chain Near-Shoring Incentives in the United States and Europe

Tax credits under the Inflation Reduction Act and the CHIPS Act reward electronics built onshore, tugging sensor value chains from East Asia toward North America. Denso expanded local semiconductor packaging to satisfy proof-of-origin clauses, lowering lead-time risk for Detroit-based OEM programs. Similar dynamics prevail in Europe, where Continental is narrowing its supplier network to partners able to certify EU origin content. Although near-shoring raises fixed costs, it also compresses design-to-launch cycles for next-generation sensors with embedded diagnostics, reinforcing the dominance of incumbent tier-1 companies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commoditization of Hall Sensors | -0.8% | Global | Short term (≤ 2 years) |

| EMI Issues in EV Platforms | -0.6% | Global; premium EVs | Medium term (2-4 years) |

| Rare-Earth Magnet Price Volatility | -0.5% | Global; sourcing in China | Short term (≤ 2 years) |

| Cybersecurity Validation Cost For Tier-2s | -0.3% | EU initially; global roll-out | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Pressures from Commoditization of Hall Sensors

As fab nodes migrate from 0.35 µm to 0.18 µm, low-end Hall dies flood the market, slashing ASPs. Multiple Asian suppliers now sell automotive-qualified Hall sensors at price points once reserved for industrial-grade parts, compressing margins for incumbents. Texas Instruments and similar firms push price-performance messages to protect share, but differentiation increasingly hinges on built-in diagnostics and redundant output modes—features absent in bare-bones offerings. Tier-1s respond by bundling software and calibration services, yet cost erosion remains a headwind until market mix shifts toward higher-value xMR or inductive solutions.

Electromagnetic Interference Issues in 800 V EV Platforms

Silicon-carbide inverters switching at higher frequencies emit broad-spectrum noise that can distort Hall and inductive sensor outputs. Automakers counter with twisted-pair cabling, additional shielding, and differential signaling, but each adds weight and cost. Infineon’s latest gate drivers include spread-spectrum modulation to blunt EMI peaks, showing that system-level fixes are in progress[3]“EMI-Optimized Gate Drivers,”, Infineon Technologies AG, infineon.com. Still, qualification test loops lengthen, delaying start-of-production schedules and holding back volume rollout of next-generation platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Magneto-Resistive Precision Gains Traction

Hall devices held 54.22% of the automotive wheel speed sensor market share in 2024. Magneto-resistive units, however, are growing at a 6.32% CAGR and are projected to erode Hall leadership beyond 2030. The automotive wheel speed sensor market size for magneto-resistive designs will widen as OEMs prioritize EMI robustness on 800 V architectures. Inductive formats preserve relevance in heavy-duty vehicles where robust metal target wheels outweigh cost concerns. Passive sensor designs linger in basic ABS programs, but limited self-diagnosis restricts them from software-defined platforms.

Magneto-resistive accuracy lets ADAS stacks calibrate torque vectoring with finer granularity, helping EV makers claim performance leadership. Hall arrays keep shipping in volume thanks to proven temperature resilience and low cost. Infineon’s TLE4802 inductive family illustrates diversification; semiconductor majors now supply turnkey reference designs that link directly into CAN-FD cyber-secure networks. This migration phase favors suppliers offering mixed portfolios that let OEMs tailor cost-performance trade-offs by trim level.

By Application: ESC Outpaces ABS Foundation

Anti-lock braking still comprised 58.81% share of the automotive wheel speed sensor market in 2024, but electronic stability control is forecast for a 6.98% CAGR through 2030, the fastest among safety categories. Traction control retains share where commercial trucks face variable loads, yet most volume growth comes from ADAS packages that include forward-collision mitigation. Therefore, the automotive wheel speed sensor market size allocated to ESC modules will edge toward parity with ABS by the close of the decade.

Predictive algorithms housed in centralized vehicle dynamics controllers now act on wheel speed pre-emptively, blurring lines between ABS and ESC. Bosch’s Motion Management module runs feed-forward logic to mitigate under- or over-steer before the driver notices, a feature impossible without high-refresh wheel data. Such innovation shifts procurement criteria from component unit cost to system-level value, benefiting vendors with integrated software libraries.

By Vehicle Type: Commercial Fleets Drive Upgrade Cycles

Passenger cars hold a 63.87% share of the automotive wheel speed sensor market in 2024 and are projected to grow at a CAGR of 5.83% through 2030. Delivery vans and trucks demand high-accuracy sensors for adaptive cruise and load-sensitive braking that minimize tire wear and boost fuel economy. Heavy trucks in autonomous-ready corridors will require redundant wheel sensors, doubling addressable content per axle. For EMI reasons, EV makers in the pickup and van segments also lean toward magneto-resistive units, nudging the mix toward premium devices.

ZF’s Smart Chassis Sensor first appeared on a luxury sedan but is slated for commercialization in Class 8 trucks, where uptime economics justify cost. Fleet operators prize predictive maintenance; self-diagnosing sensors that feed telematics dashboards help schedule service during planned stops. Consequently, the automotive wheel speed sensor market develops two parallel tracks: volume-driven passenger platforms that squeeze pricing, and fleet-oriented programs that pay for extra diagnostics.

By Propulsion Type: BEVs Lead Sensor Value Upsell

Internal combustion vehicles still hold a 71.63% share of the automotive wheel speed sensor market in 2024, yet battery electrics will expand at a 7.74% CAGR by 2030. Regenerative braking calibration, traction split for dual-motor setups, and fine-grained torque vectoring rely on precise wheel data. BEVs generally specify magneto-resistive or advanced Hall arrays with redundancy. Therefore, the automotive wheel speed sensor market size tied to BEVs will climb disproportionately to vehicle count.

Fuel-cell powertrains, though niche, mirror BEV requirements for energy recovery, offering another high-value beachhead. Infineon’s supply pact with Stellantis covers SiC inverters plus AURIX MCUs that digest encrypted wheel sensor streams. As propulsion diversity broadens, tier-1s able to certify sensor performance across multiple voltage classes enjoy a strategic edge.

By Distribution Channel: Aftermarket Momentum Builds

OEM installations dominated 83.77% share of the automotive wheel speed sensor market in 2024, reflecting the factory-fit tradition. However, the aging of ten-year ABS fleets and early ADAS cohorts is opening a 5.84% CAGR aftermarket through 2030. Replacement parts must meet cybersecurity and functional safety benchmarks, prompting Continental to bundle calibration tools so independent repairers can pair new sensors with central ECUs. ZF sells workshop-grade ADAS alignment rigs, signaling service-channel monetization aligned with the sensor lifecycle.

Aftermarket share gains also stem from used-vehicle imports into Africa and Latin America, where ABS or ESC fail inspection without functioning sensors. The automotive wheel speed sensor market thus benefits from a virtuous cycle: regulatory adoption triggers OE volumes, which later convert into a rising installed base needing replacement.

Geography Analysis

Asia–Pacific held 46.31% share of the automotive wheel speed sensor market in 2024 and is on track for a 6.34% CAGR through 2030, the quickest among regions. China’s dominance in BEV manufacturing forces sensor suppliers to localize magneto-resistive and inductive lines near battery plants, shortening supply chains and easing compliance with carbon-footprint metrics. India’s staggered ABS rollout across two-wheelers and heavy trucks secures steady annual growth, while Japan and South Korea push precision requirements higher to support advanced ADAS for premium EV exports.

North America ranks second in value due to policy incentives favoring domestic sensor content. The Inflation Reduction Act also nudges commercial fleet electrification, further lifting sensor volumes, especially in last-mile vans. Cyber-secure CAN-FD implementations find early application in this region’s pilot autonomous truck fleets, adding software revenues for tier-1s.

Europe sustains its share thanks to regulatory leadership: the General Safety Regulation and UN R155 drive both quantity and complexity of sensors per vehicle. Continental’s headquarters restructuring to boost EU proximity reflects the need for a fast response to evolving technical standards. Eastern European plants serve as cost-balanced hubs feeding the wider region. The Middle East and Africa remain emergent, yet uptake improves as imported used vehicles gradually meet local inspection norms and local assembly lines scale.

Competitive Landscape

Global supply is moderately concentrated. Bosch, Continental, and Denso combine broad ABS heritage, ASIC design, and validation assets, enabling them to serve every major OEM program. Infineon realigned sensor and RF into the SURF unit to sell higher-level modules, not just die, seeking system revenue capture. Magneto-resistive innovators like NXP and Allegro Microsystems attract EV start-ups with EMI-resilient solutions.

Competitive tactics increasingly revolve around software stacks bundled with hardware. Bosch licenses “Motion Management” code to OEMs adopting its wheel sensors, creating lock-in. Continental invests in cybersecurity labs to certify sensor updates over the air, raising barriers for low-cost rivals. Meanwhile, Asian fabless entrants undercut on Hall pricing, intensifying the commoditization pinch, though struggling with UN R155 documentation loads. M&A is expected as tier-2s lacking cybersecurity bandwidth seek shelter under larger umbrellas.

Strategic moves center on 800 V readiness, edge AI, and regional manufacturing resilience. Suppliers capable of delivering all three—and backing them with rigorous functional-safety documentation—stand to capture disproportionate future share within the automotive wheel speed sensor market.

Automotive Wheel Speed Sensor Industry Leaders

Robert Bosch GmbH

Hella GmbH & Co. KGaA

Denso Corporation

ZF Friedrichshafen AG

Aisin Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: ZF began producing a series of its Smart Chassis Sensors on the Cadillac Celestiq luxury EV, embedding wheel positioning in ball joints to feed electronic damping and road-surface mapping.

- January 2025: At CES 2025, Infineon and Flex unveiled a modular zone controller platform that showcases software-defined vehicle power distribution and motor control.

Global Automotive Wheel Speed Sensor Market Report Scope

| Hall Effect Sensors |

| Magneto-Resistive Sensors |

| Inductive Sensors |

| Active Sensors |

| Passive Sensors |

| Anti-lock Braking System (ABS) |

| Electronic Stability Control (ESC) |

| Traction Control System (TCS) |

| Adaptive Cruise Control (ACC) |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

| Internal Combustion Engine Vehicles |

| Battery Electric Vehicles (BEV) |

| Hybrid Electric Vehicles (HEV) |

| Plug-In Hybrid Electric Vehicles (PHEV) |

| Fuel Cell Electric Vehicles (FCEV) |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Sensor Type | Hall Effect Sensors | |

| Magneto-Resistive Sensors | ||

| Inductive Sensors | ||

| Active Sensors | ||

| Passive Sensors | ||

| By Application | Anti-lock Braking System (ABS) | |

| Electronic Stability Control (ESC) | ||

| Traction Control System (TCS) | ||

| Adaptive Cruise Control (ACC) | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium & Heavy Commercial Vehicles | ||

| By Propulsion Type | Internal Combustion Engine Vehicles | |

| Battery Electric Vehicles (BEV) | ||

| Hybrid Electric Vehicles (HEV) | ||

| Plug-In Hybrid Electric Vehicles (PHEV) | ||

| Fuel Cell Electric Vehicles (FCEV) | ||

| By Distribution Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the automotive wheel speed sensor market in 2030?

The sector is forecast to reach USD 4.81 billion by 2030 as it expands at a 5.27% CAGR.

Which sensor technology is growing the fastest?

Magneto-resistive devices are expected to post the highest 6.32% CAGR due to superior EMI resilience needed in 800 V EVs.

Why do battery electric vehicles use more wheel speed sensors?

BEVs require precise slip detection for regenerative braking, torque vectoring, and thermal management, raising per-vehicle sensor counts.

How will UN R155 influence supplier dynamics?

The regulation raises cybersecurity validation costs, favoring tier-1s with specialized test labs and prompting consolidation among smaller vendors.

What is driving aftermarket growth in wheel speed sensors?

An aging global vehicle parc equipped with ABS and ESC is entering replacement cycles, lifting aftermarket demand at a 5.84% CAGR.

Page last updated on: