Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

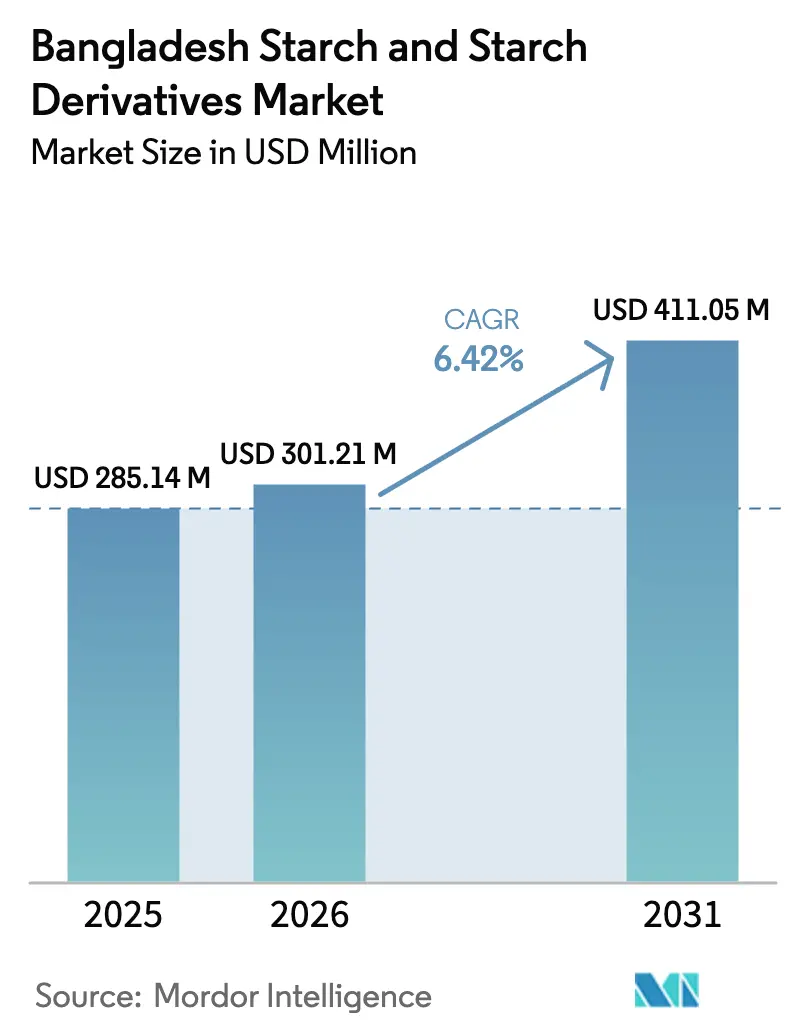

| Base Year Market Size (2025) | USD 285.14 Million |

| Market Size (2026) | USD 301.21 Million |

| Market Size (2031) | USD 411.05 Million |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bangladesh Starch And Starch Derivatives Market Analysis by Mordor Intelligence

The Bangladesh starch and starch derivatives market was valued at USD 285.14 million in 2025. It is projected to reach USD 301.21 million in 2026 and USD 411.05 million by 2031, registering a CAGR of 6.42% during the forecast period. This growth is driven by the country's rapid industrialization, expanding consumer goods manufacturing, and a shift toward higher-value derivatives that offer premium pricing compared to native starch granules. Key factors supporting demand include strong apparel exports, growth in packaged food production, and an expanding pharmaceutical manufacturing base. While multinational ingredient suppliers are increasing their presence, local processors maintain competitiveness by catering to smaller lot sizes and providing faster lead times. However, firms must address critical challenges such as feedstock availability, tariff differences between raw corn and finished products, and evolving sustainability requirements.

Key Report Takeaways

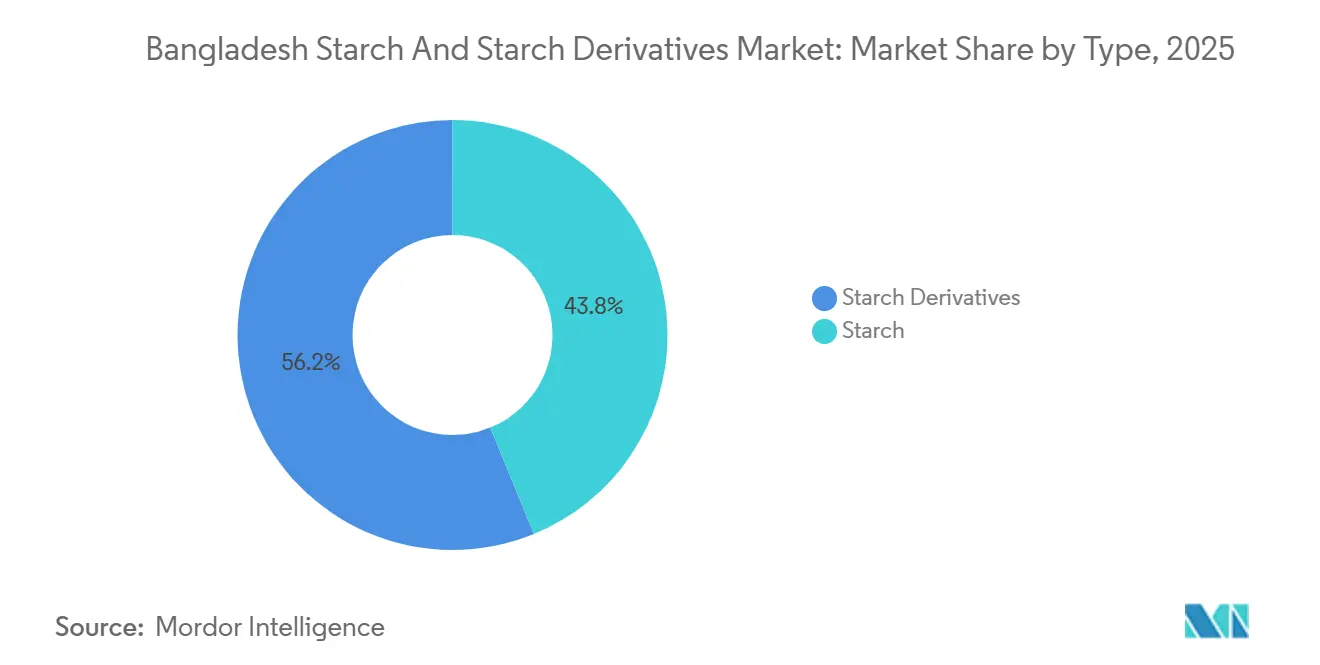

- By type, starch derivatives captured 56.18% of the Bangladesh starch and starch derivatives market share in 2025 and are forecast to expand at a 7.37% CAGR through 2031.

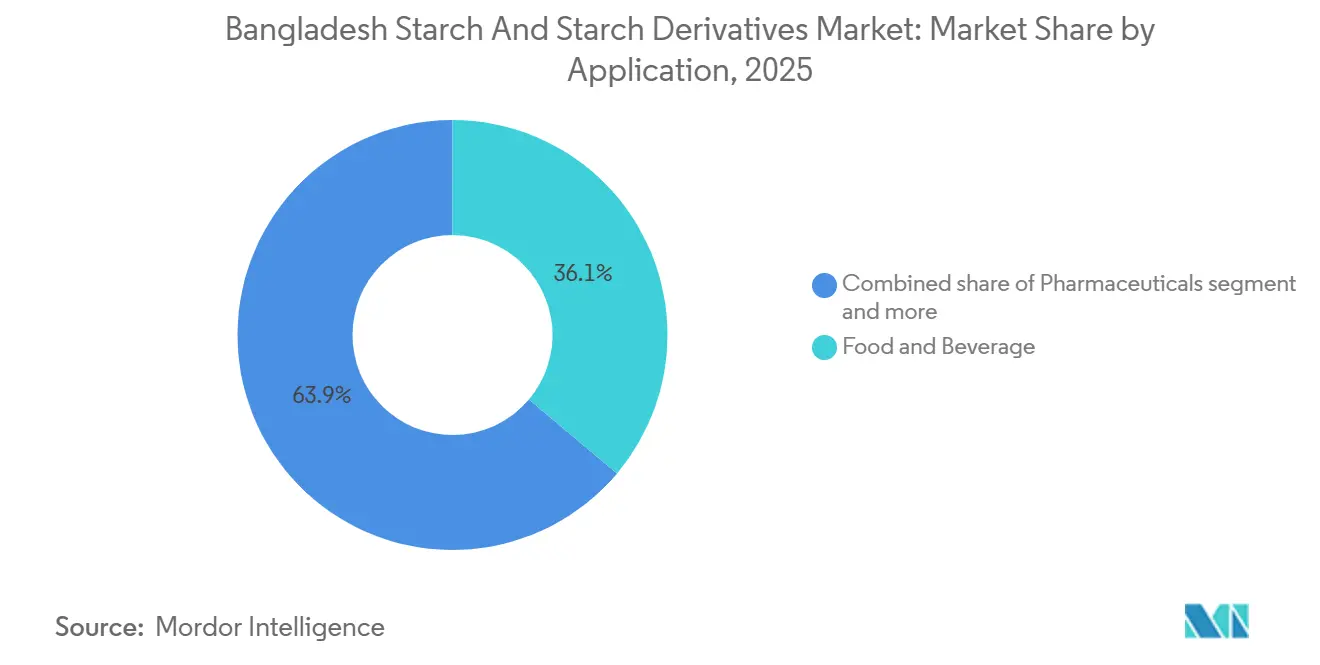

- By application, food and beverage held 36.14% of the Bangladesh starch and starch derivatives market size in 2025, while the pharmaceuticals segment is projected to grow the fastest at 9.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Bangladesh Starch And Starch Derivatives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding textile industry dominance | +1.8% | National, concentrated in Dhaka, Gazipur, Narayanganj, Chattogram | Long term (≥ 4 years) |

| Growth in food processing industry | +1.5% | National, with hubs in Dhaka, Chattogram, Bogura | Medium term (2-4 years) |

| Ongoing government initiatives in agriculture sector | +1.2% | National, emphasis on northern districts (Rangpur, Rajshahi) | Long term (≥ 4 years) |

| Rapid expansion of poultry and aquafeed industry | +1.0% | National, key clusters in Gazipur, Kishoreganj, Mymensingh | Medium term (2-4 years) |

| Adoption of clean-label and natural ingredients | +0.6% | Urban centers (Dhaka, Chattogram, Sylhet) | Short term (≤ 2 years) |

| Expansion of cosmetic and personal care segments | +0.4% | Urban centers, rising middle-affluent class | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding textile industry dominance

The rapid expansion of Bangladesh's textile and apparel industry is a significant driver for the demand for starch and starch derivatives, which play a crucial role in fabric finishing, sizing, and quality enhancement. In 2024, Bangladesh exported clothing worth USD 38,482 million, positioning it among the leading global apparel exporters, following China and the European Union [1]Source: World Trade Organization, wto.org. The growing domestic demand for raw materials further highlights the industry's expansion, with cotton consumption increasing to 7.6 million bales in 2024, compared to 6.9 million bales in 2020[2]Source: USDA Foreign Agricultural Service, "Cotton: World Market and Trade," usda.gov. This growth underscores the rising need for starch-based solutions to enhance processing efficiency, preserve fabric integrity, and improve the quality of finished products. The increasing scale and technological advancement of Bangladesh's textile manufacturing sector, supported by cost-efficient labor, upgraded facilities, and the adoption of modern technologies, has driven the utilization of modified starches, hydrolyzed starches, and other derivatives.

Growth in food processing industry

Bangladesh's growing food processing industry is a key driver for the demand for starch and starch derivatives, which are extensively used as thickeners, stabilizers, emulsifiers, and texturizing agents in processed foods. By 2024, the country is home to approximately 1,000 food processing companies, an increase from 700 in 2023, indicating rapid growth in the sector and rising domestic demand for convenience and packaged food products [3]Source: USDA Foreign Agricultural Service, "Exporter Guide Annual" usda.gov . This expansion in processing activities has heightened the demand for modified starches, glucose syrups, and other derivatives to improve product consistency, shelf life, and functional performance. The diversification of processed food products, including dairy, bakery, confectionery, and ready-to-eat meals, further drives the adoption of starch-based solutions. Factors such as urbanization, shifting consumer lifestyles, and increasing disposable incomes are prompting manufacturers to utilize starch derivatives to enhance production efficiency and meet evolving quality standards.

Ongoing government initiatives in agriculture sector

Bangladesh's agricultural sector plays a crucial role in its economy, contributing 11.2% to the Gross Domestic Product (GDP) and employing 36.9% of the workforce as of 2025, according to the Bangladesh Investment Summit. Government-led initiatives aimed at agricultural modernization and crop diversification have created favorable conditions for starch production. The country primarily derives starch from potato, corn, and cassava, with potato being the dominant source due to its high yield and versatility in both food and industrial applications. These initiatives focus on enhancing crop productivity, improving seed quality, and promoting sustainable farming practices to ensure a steady supply of starch-rich crops. Agricultural development programs prioritize high-value horticulture, crop processing, and seed innovation to address domestic demand and boost export potential. Specific programs, such as the Potato Export & Cold Storage Support initiative, strengthen the raw material base for various starch production types. Meanwhile, maize and cassava production benefit from efforts in crop diversification and climate-resilient agricultural practices. These government measures help mitigate supply risks, stabilize raw material prices, and uphold quality standards in starch processing.

Rapid expansion of poultry and aquafeed industry

The expanding poultry and aquaculture industries in Bangladesh are driving higher demand for starch and starch derivatives, which serve as binders, energy sources, and pelletizing agents in feed formulations. As livestock and fish farming scale up to meet the growing domestic demand for protein, feed manufacturers are increasingly utilizing modified starches and derivatives to enhance nutrient delivery, improve pellet stability, and optimize feed digestibility. The rise in urban populations and increasing per capita consumption of poultry and fish have contributed to the growth of commercial farming, resulting in sustained, large-scale demand for starch-based feed ingredients. Additionally, government initiatives promoting modern farming practices and feed efficiency are further supporting this trend, establishing the poultry and aquafeed sector as a significant driver of growth for the starch and starch derivatives market in Bangladesh.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exposure to international supply volatility and high international prices | -0.9% | National, import-dependent regions | Short term (≤ 2 years) |

| Feedstock price volatility | -0.7% | National, acute in processing hubs | Short term (≤ 2 years) |

| Competition from alternate hydrocolloids | -0.5% | National, pronounced in food and beverage segment | Medium term (2-4 years) |

| Port/customs delays and bonded-warehouse limits | -0.4% | Chattogram, Mongla port catchments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Exposure to international supply volatility and high international prices

Bangladesh's starch industry continues to face significant challenges due to international supply volatility and elevated global prices, a persistent structural issue despite efforts to enhance domestic production capacity. According to data from the Bangladesh Bureau of Statistics in December 2023, the country exported preparations of cereals, flour, and starch valued at Tk. 2,444.75 million, reflecting a 3.76% increase compared to the previous month. Meanwhile, imports amounted to Tk. 1,527.19 million, representing an 8.64% decline. This reduction in imports aligns with a broader trend in the country's food-grain trade, as wheat and rice imports dropped sharply during the July-February period of fiscal year 2023-24 compared to FY23. Traditionally a major importer of wheat from Ukraine, Bangladesh now sources wheat from Russia, Ukraine, Canada, and Australia, following disruptions in India's wheat exports since 2022. High international prices, coupled with rising domestic inflation and the depreciation of the local currency (taka), have further limited the country's ability to import rice and wheat at competitive costs.

Port/customs delays and bonded-warehouse limits

In 2025, the average import clearance time at Chattogram Port extended to 7 days, 7 hours, and 58 minutes, with some outlier shipments taking up to 19 days. These delays were attributed to factors such as multiple laboratory tests, disputes over harmonized-system classifications, and manual valuation procedures. Bonded-warehouse facilities, which defer duty payments until goods enter domestic circulation, remain predominantly available to ready-made-garment exporters. As a result, starch importers are required to pay the full 67 percent total tax incidence upfront, tying up working capital for extended periods. This liquidity constraint disproportionately impacts small and medium enterprises, which often lack access to trade finance, thereby allowing larger competitors with stronger balance sheets to gain market share by absorbing delayed reimbursements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Derivatives Drive Value Addition

Starch derivatives accounted for 56.18% of the market value in 2025 and are projected to grow at a rate of 7.37% through 2031. This growth reflects food manufacturers' increasing preference for glucose syrups, high-fructose corn syrup, and modified starches, which provide functionalities not achievable with native granules. Modified starches, developed through processes such as acid hydrolysis, enzymatic treatment, or cross-linking, offer enhanced freeze-thaw stability, shear resistance, and clarity. These properties make them essential in applications like dairy desserts, sauces, and ready-to-eat meals, where texture and shelf life are critical to consumer acceptance.

High-fructose corn syrup remains a niche segment due to limited domestic production capacity and consumer concerns regarding health implications. However, beverage formulators are experimenting with blends of high-fructose corn syrup and glucose syrup to replicate sucrose's sweetness profile while reducing ingredient costs by 10-12%. Potato starch, although a smaller segment, provides the highest hydration and swelling capacity, making it the preferred disintegrant in orally disintegrating tablets. This formulation is gaining popularity in Bangladesh's generic drug industry, particularly as manufacturers focus on pediatric and geriatric populations.

By Application: Pharmaceuticals Outpace Traditional Uses

In 2025, the food and beverage segment accounted for 36.14% of the market value, driven by applications in confectionery, bakery, dairy, and beverages, where starch derivatives are utilized as thickeners, stabilizers, and texturizers. The packaged food market is witnessing significant growth, primarily driven by urbanization and the expansion of modern retail channels. This growth is contributing to increased demand for glucose syrup and modified starch. However, competition from alternative hydrocolloids such as guar gum, xanthan gum, and carboxymethyl cellulose is creating margin pressures, prompting formulators to balance cost and performance effectively.

The pharmaceuticals segment, projected to grow at a CAGR of 9.89% through 2031, represents the fastest-growing application. Local tablet manufacturers are increasingly replacing imported excipients with maize starch and sodium starch glycolate, benefiting from Bangladesh's duty exemptions on pharmaceutical capital machinery and low labor costs ranging from USD 90 to USD 150 per month. This segment consumes several thousand tonnes annually, contributing to improved printability and box strength. Other applications, including construction adhesives, biodegradable packaging films, and oil-well drilling fluids, are still in the early stages but are attracting research and development investments. Government initiatives to phase out single-use plastics and promote jute-starch composite materials for export to environmentally conscious markets in Europe and North America are further driving interest in these applications.

Geography Analysis

Bangladesh's starch and starch derivatives market demonstrates significant regional concentration, with Dhaka, Gazipur, Narayanganj, and Chattogram accounting for approximately 70 to 75 percent of consumption. This is primarily due to the dominance of these regions in ready-made garments, food processing, and pharmaceutical manufacturing. The Dhaka Division, which includes the capital and surrounding industrial areas, hosts the majority of the country's 5,162 registered garment factories. Additionally, it serves as the main distribution hub for packaged foods, making it the largest regional market.

The government has initiated efforts to establish economic zones in secondary cities such as Bhola, Jamalpur, and Sylhet to decentralize industrial activity and alleviate the strain on Dhaka's overburdened infrastructure. However, progress in these initiatives has been inconsistent. Port logistics remain a critical factor influencing regional competitiveness. At Chattogram Port, the average import clearance time is 7 days, 7 hours, and 58 minutes, with some shipments taking up to 19 days. These delays impose working-capital challenges, favoring processors with bonded-warehouse access or those capable of negotiating extended payment terms with suppliers.

Mongla Port, the second-largest port in the country, handles a smaller volume compared to Chattogram and faces draft limitations that restrict the size of vessels it can accommodate. Despite these limitations, its proximity to the Khulna industrial belt and lower congestion levels make it an attractive option for bulk corn imports destined for feed mills in the southwestern region. Meanwhile, plans to develop Payra Port as a deep-water alternative have been delayed due to land acquisition disputes and financing challenges. As a result, Chattogram remains the dominant gateway, reinforcing the concentration of starch processing activities in its surrounding areas.

Regulatory Landscape

Bangladesh starch and starch derivatives suppliers work within a multi-agency compliance environment led by the Bangladesh Food Safety Authority (BFSA) for food safety and additive controls, and the Bangladesh Standards and Testing Institution (BSTI) for mandatory product standards and conformity assessment. The Use of Food Additives Regulations 2017 (under the Food Safety Act framework) defines requirements around classification, permitted use, and inspection for additives used in food formulations where modified starches and sweeteners are common functional ingredients.

Regulatory tightening and standard harmonization have also been reflected in BFSA notifications aligning national rules with Codex Alimentarius (GSFA, CODEX STAN 192-1995), including the draft Food Safety (Use of Food Additives) Regulation notified in 2023. On the product-standard side, BDS 154:2022 (Second Revision) sets national requirements for maize (corn) starch, and BSTI maintains a dedicated sectional committee covering starch, derivatives, and by-products. For importers, listed food items require a BSTI Clearance Certificate for customs release, which makes testing and documentation a practical gating item alongside tariff and HS-classification processes.

Value Chain Analysis

The value chain starts with feedstock sourcing (primarily potato and maize, with some cassava) through aggregators, traders, and, increasingly, more structured procurement by larger processors. This is followed by primary starch extraction and wet milling for maize-based starches and derivatives. Domestic processing involves local manufacturers and wet-mill operators, such as Glory Agro Products Ltd, which operates a maize starch wet milling facility in Habiganj serving food, textile, paper, and pharmaceutical end users. Multinational ingredient suppliers also complement local supply via imports of specialty modified starches and sweeteners.

Downstream demand is concentrated in food and beverage manufacturers, textile sizing and finishing units, paper and corrugating plants, and pharmaceutical formulators using starch and derivatives as binders, disintegrants, and functional excipients. Distribution typically runs through direct B2B supply to large industrial buyers and through ingredient distributors for smaller lots, with quality assurance tied to BSTI standards and BFSA food safety and additive compliance requirements. Friction points are import logistics and working-capital intensity linked to customs procedures and testing, as well as formulation compliance where additive permissions and limits require alignment to BFSA rules and Codex references. As processors target pharmaceutical and higher-spec food applications, technical service, documentation, and lab testing have become more visible throughout the chain.

Competitive Landscape

The Bangladesh starch and starch derivatives market is moderately consolidated. Global ingredient companies such as Cargill, Archer Daniels Midland, Ingredion, Tate & Lyle, and Roquette dominate the market by leveraging economies of scale, proprietary modification technologies, and established relationships with multinational food and pharmaceutical buyers. These factors enable them to command premium pricing. In contrast, local processors compete by offering proximity advantages, faster turnaround times, and the flexibility to supply smaller lot sizes, which are often uneconomical for multinational firms.

Tate & Lyle's strategic shift toward specialty food ingredients, as demonstrated by its divestment of commodity starch assets in other markets, highlights its focus on high-margin modified starches and sweeteners for premium food and beverage applications. This positioning may limit its involvement in Bangladesh's price-sensitive textile and paper industries. Opportunities for growth in the market include pharmaceutical excipients, biodegradable packaging, and export-oriented value-added products.

Local tablet manufacturers, facing challenges such as foreign-exchange shortages and import delays, are actively seeking domestic sources of maize starch and sodium starch glycolate that comply with USP and BP monograph standards. This creates opportunities for processors willing to invest in cleanroom production facilities and third-party analytical testing. Emerging disruptors in the market include small-scale processors exploring cassava and potato starches to mitigate feedstock risks. However, inconsistent agricultural practices and limited extension support hinder yield predictability and quality consistency, posing challenges to these efforts.

Bangladesh Starch And Starch Derivatives Industry Leaders

-

Cargill, Incorporated

-

Archer Daniels Midland (ADM)

-

Gulshan Polyols Limited

-

FLAMINGO AGRO-TECH LTD

-

JTA Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity is deeper penetration of higher-value starch derivatives in processed foods and export-facing agro-processing, supported by Bangladesh’s expanding agro-processing base and rising processed food exports (over USD 1 billion in FY2024, as highlighted in World Bank and national investment materials). As more processors organize direct supply chains with farmers to secure consistent raw materials, local ingredient manufacturers have room to supply consistent-spec glucose syrups and modified starches for bakery, confectionery, dairy, sauces, and convenience foods, where functionality and batch-to-batch uniformity matter alongside price.

A second opportunity is import substitution for regulated, documentation-heavy applications, particularly pharmaceutical excipients and high-spec food additives, where buyers weigh monograph compliance, traceability, and reliable local lead times. BFSA’s ongoing alignment toward Codex references, together with BSTI’s role in mandatory product standards, raises the premium on compliant local production and third-party testing support. At the same time, persistent port and clearance bottlenecks and the limited availability of bonded-warehouse benefits outside export-heavy sectors create a practical incentive for supply-chain solutions, including bonded-warehousing proposals by large commodity or ingredient players, that shorten cycles for imported inputs and specialty derivatives.

Recent Industry Developments

- June 2026: Elementa Bangladesh Limited announced availability of food starch solutions for applications such as sauces through a corporate communication. The move signals an active portfolio push by ingredient distributors toward higher-functionality starch use in processed foods, where application support and consistent supply influence supplier selection.

- May 2025: Cargill India sought permission from the National Board of Revenue (NBR) to establish bonded warehouses in Bangladesh to facilitate agricultural raw material supply. The proposal targets lead-time and cash-cycle constraints created by import clearance and duty-payment structures, which directly affect starch and derivative input availability for industrial users.

- November 2024: PRAN-RFL Group invested Tk750 crore to enter the essential goods category via a new industrial park in Kaliganj, Gazipur, with production starting for wheat-based and related products. The facility’s stated product slate includes starch alongside other staples, strengthening local manufacturing depth and widening potential domestic sourcing options for industrial and consumer-goods channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of starch and starch derivatives consumed in Bangladesh across major downstream uses, where demand is created by local manufacturing output and import availability, and values are expressed in USD for the defined time period.

Scope exclusions: We exclude household cooking flour substitutes and non-starch functional additives that are not derived from starch chemistry.

Segmentation Overview

-

By Type

- Starch

-

Starch Derivatives

- Modified Starch

- Glucose Syrups

- High Fructose Corn Syrup (HFCS)

- Others

-

By Application

- Food and Beverage

- Textile

- Pharmaceuticals

- Paper and Corrugating

- Other Applications

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the demand context for Bangladesh, then narrowing it to starch and derivative consumption. We used public sources such as Bangladesh Bureau of Statistics releases, Bangladesh Bank trade and FX indicators, National Board of Revenue customs and tariff schedules, and FAO-style crop balance statistics to understand feedstock availability and trade dependence.

We then cross-checked end-use pull signals using sources such as Bangladesh Export Promotion Bureau data for textiles, Bangladesh Food Safety Authority and BSTI references for food and quality requirements, and peer-reviewed papers that discuss starch modification and application performance. Company annual reports, importer and distributor websites, and business press were used to sanity check capacity changes, pricing direction, and application trends, supported by paid subscriptions for company financials and shipment-level import and export records where needed. These sources are illustrative, and additional public documents were also referred to for validation and clarification during the work.

Primary Interviews and Surveys

Primary discussions were run with manufacturers and importers of starch and starch derivatives, along with procurement and technical teams from textile processing, food manufacturing, paper and corrugation, and pharmaceutical formulation. We used these inputs to confirm application-wise usage patterns, typical pricing ranges by grade, and the practical split between locally produced and imported material. We then rechecked gaps where desk sources were not consistent.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 52% |

| Mid tier: 50% | Functional/Unit leaders: 31% | EMEA: 29% |

| Smaller Players: 22% | Managers: 56% | Americas: 19% |

Market-Sizing & Forecasting

Sizing is built using a top-down structure where we reconstruct demand from downstream activity indicators, then map them to starch and derivative consumption by application. For Bangladesh, the key anchors include textile processing output and export trends, packaged food and beverage manufacturing expansion, corrugated packaging demand tied to consumer goods movement, and pharmaceutical production trends, which are then converted into value using grade-level price bands.

After the demand pool is set, we use selective bottom-up approximations to check totals. These include supplier and importer roll-ups, sampled average selling price (ASP) times estimated volumes by application, and channel checks with distributors. When full coverage is not feasible for smaller importers or fragmented buyers, the remaining gap is handled using a calibrated uplift based on observed import concentration and typical buyer mix from interviews.

For forecasts, scenario analysis is applied around the same core drivers, then tightened with expert consensus on how starch substitution, quality upgrades (native to modified), and import pricing will evolve. Inputs that typically move the model include corn and cassava price direction, customs duty changes, USD to BDT movement, shifts in apparel export orders, and adoption of higher value derivatives in food and pharma formulations.

Data Validation & Update Cycle

Validation is done by checking the model against independent signals, including import value direction, application output indicators, and price reality checks from buyers and traders. Outliers are investigated, and the assumptions behind volumes, ASP ranges, and application splits are reviewed in more than one analyst pass before sign-off.

Reports are refreshed annually, and interim updates are triggered when material events occur, such as sharp currency movement, tariff revisions, or step-changes in major end-use output. Before delivery, we do a fresh review of key inputs so the numbers reflect the latest available public statistics and field feedback.

Mordor Intelligence's Bangladesh Starch and Starch Derivative Market Size Compared Against Other Published Estimates

Published market values for Bangladesh starch and starch derivatives can look different because each publisher locks assumptions at a different time, then applies its own price logic, currency conversion timing, and validation depth. These choices matter more in a market where import pricing and BDT to USD movement can shift the reported value even when volumes are steady.

The main gap drivers usually come from how starch versus derivatives are grouped, whether all industrial uses are counted in the same pool, and how application splits are estimated when buyer coverage is fragmented. When ASPs are refreshed with current import price ranges and then reconciled with end-use consumption checks, the spread normally narrows, which is the refresh-led reason the 2025 baseline used by Mordor Intelligence can land above or below other snapshots depending on their price date and currency assumptions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 285.14 M (2025) | |

| Industry Data Provider A | USD 239.70 M (2024) | Uses an earlier base year, and the value is sensitive to the specific USD conversion window and 2024 price bands. The scope also appears to introduce distribution-channel and sub-national splits, which can change how trade and local supply are allocated across the total. |

| Global Publisher B | USD 316.27 M (2026) | Reports a forward-year value, so the estimate already bakes in growth assumptions on downstream industries and price progression. Differences can also come from broader inclusion of derivative types and a faster assumed shift toward higher value modified grades in industrial applications. |

Overall, the spread is mostly explained by year selection and the timing of pricing and FX assumptions, followed by how tightly application demand is validated. By keeping the scope tied to Bangladesh end-use pull signals and rechecking ASP ranges against trade and buyer feedback, we arrive at a balanced number that can be traced back to practical variables.

Key Questions Answered in the Report

What was the value of the Bangladesh starch and starch derivatives market in 2026?

The market was valued at USD 301.21 million in 2026.

What CAGR is forecast for starch derivatives through 2031?

Starch derivatives are projected to grow at a 7.37% CAGR between 2026 and 2031.

Which application segment is expected to grow the fastest?

Pharmaceuticals, with a forecast 9.89% CAGR, is the fastest-growing segment.

How does the tariff structure affect domestic processors?

A 67% duty on finished corn starch versus 6.33% on feed residues compresses margins and favors imports of derivatives.

Page last updated on: