In Mold Labels Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.53 Billion |

| Market Size (2031) | USD 1.87 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

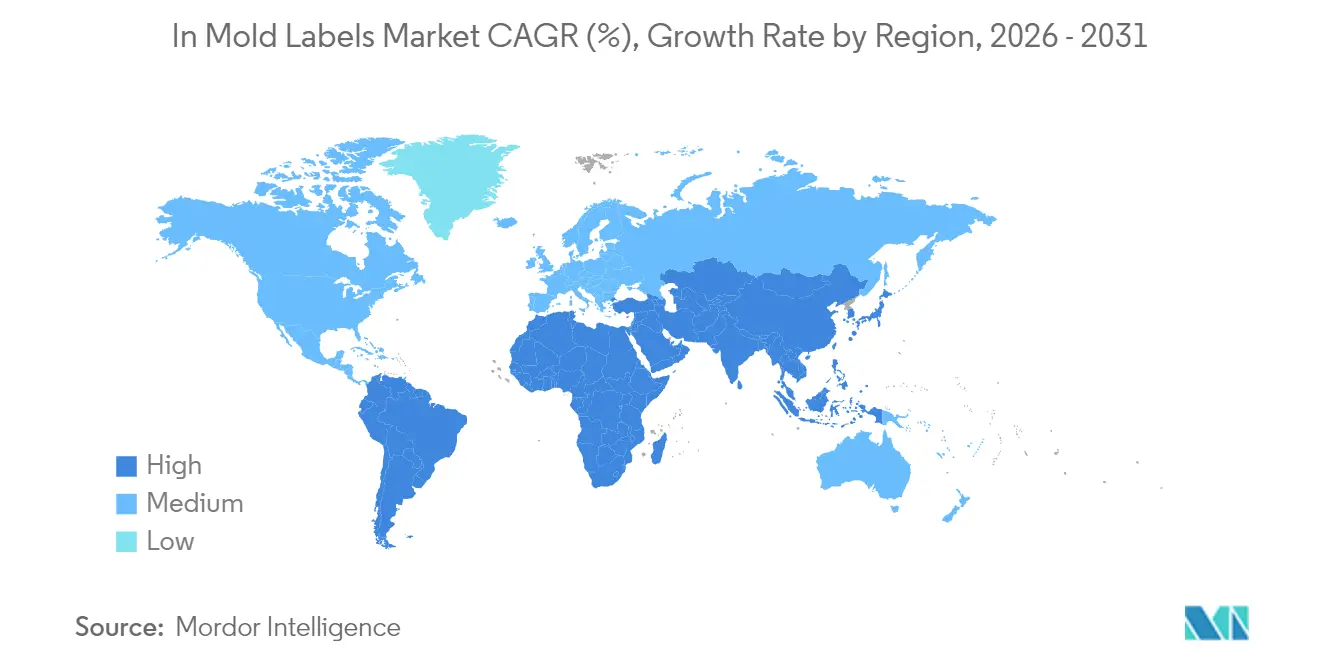

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

In Mold Labels Market Analysis by Mordor Intelligence

The in-mold labels market size was valued at USD 1.47 billion in 2025 and estimated to grow from USD 1.53 billion in 2026 to reach USD 1.87 billion by 2031, at a CAGR of 4.12% during the forecast period (2026-2031). Steady growth reflects the sector’s shift from capacity-driven expansion toward regulatory compliance, energy efficiency, and premium decoration. Europe’s Packaging and Packaging Waste Regulation (PPWR) is accelerating the transition to mono-material packaging that can be mechanically recycled in existing streams. Asia-Pacific manufacturers meanwhile leverage high-cavitation injection molding and lower operating costs to win global contracts, while North American converters focus on premium designs for cosmetics and food. Digital printing is unlocking cost-effective short runs and personalization, and polypropylene (PP) remains the preferred substrate as it balances processability with recyclability. Despite PP price volatility, capital spending on energy-efficient thermoformers and electric presses is expected to sustain competitiveness across the in-mold labels market.

Key Report Takeaways

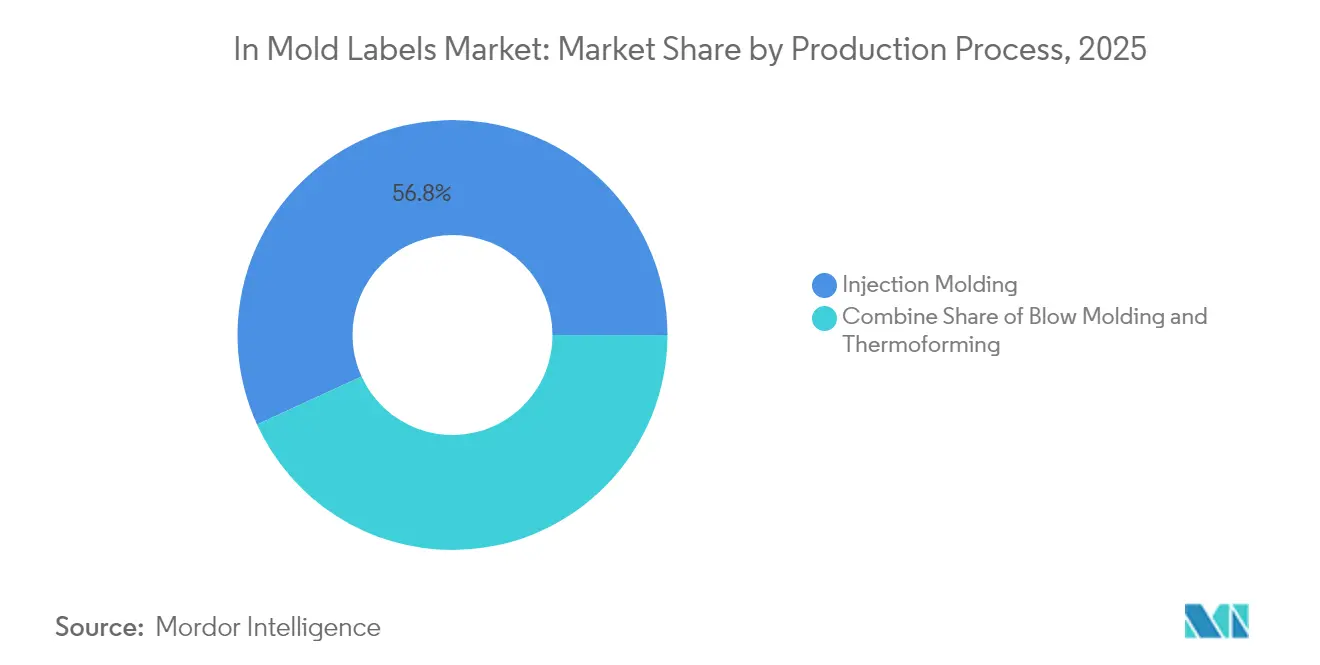

- By production process, injection molding led with 56.83% of in-mold labels market share in 2025, while thermoforming is projected to post the fastest 7.21% CAGR to 2031.

- By material, polypropylene commanded 44.92% share of the in-mold labels market size in 2025 and is growing at an 8.74% CAGR through 2031.

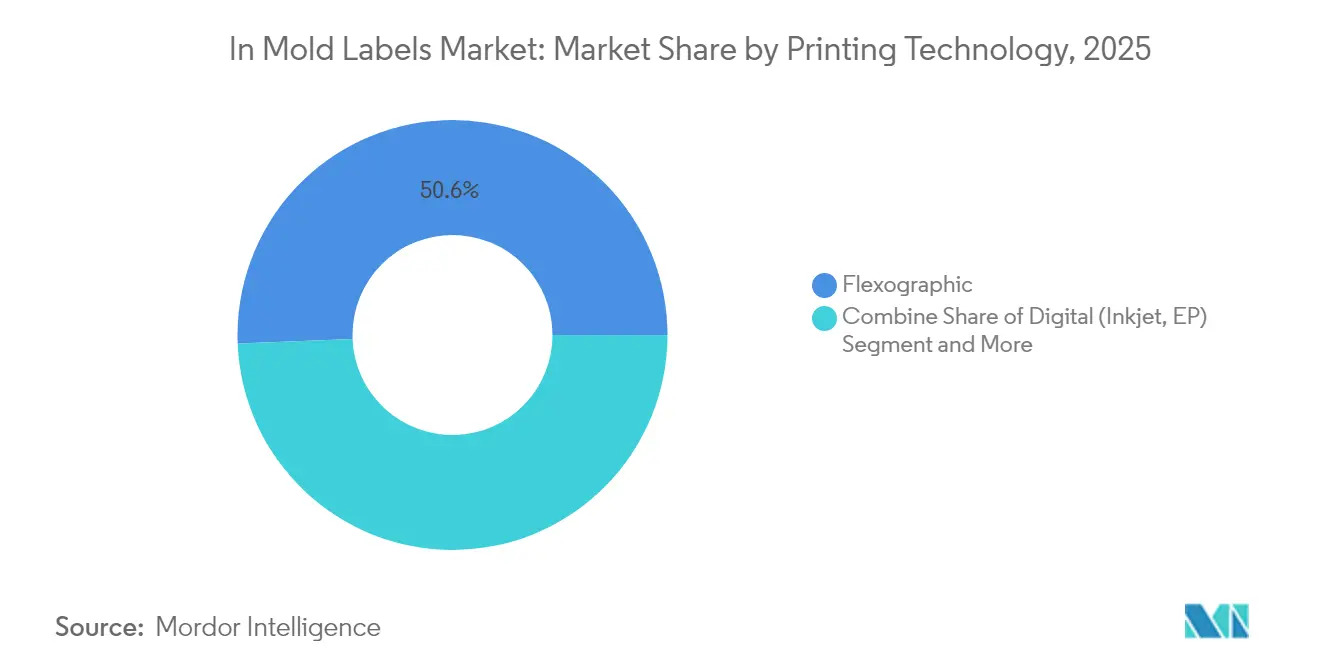

- By printing technology, flexography held 50.63% revenue in 2025; digital printing is expected to expand at a 9.27% CAGR to 2031.

- By end-user industry, food accounted for 28.02% of the in-mold labels market size in 2025, whereas cosmetics and personal care is forecast for the quickest 8.5% CAGR.

- By geography, Asia-Pacific captured 40.37% revenue in 2025 and is set to climb at a 7.83% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global In Mold Labels Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mono-material packaging for recycling | +1.2% | Global – EU leads | Medium term (2-4 years) |

| High-cavitation injection molding in Asia | +0.8% | APAC core | Long term (≥ 4 years) |

| Premium no-label-look decoration | +0.6% | North America & EU | Short term (≤ 2 years) |

| Digital IML for personalization | +0.5% | Global urban hubs | Medium term (2-4 years) |

| Tethered-cap rules and lightweight closures | +0.4% | EU first | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Mono-Material Packaging Enabling Easier Recycling

Mandatory recyclability from 2028 under the PPWR forces converters to redesign labels so container and decoration share the same polymer, eliminating separation steps and improving bale purity. MCC Verstraete’s NextCycle IML delivers a polypropylene label‐on-polypropylene container solution that passes mechanical recycling trials without ink bleed.Brand owners in beverages and dairy increasingly lock in three-year supply agreements that specify mono-material requirements, creating a predictable baseline for capex returns in the in-mold labels market. Asian resin makers respond with higher-clarity PP grades compatible with food contact, and US retailers introduce scorecards that penalize mixed-material decoration. As recycling targets tighten, converters that pre-qualify mono-material formats will be preferred partners, reinforcing first-mover advantage.

Expansion of High-Cavitation Injection Molding Capacity in Asia

China, Vietnam, and Thailand added more than 1,200 high-cavitation presses during 2023-2025. FCS Machinery alone booked tool sets that run up to 128 cavities, cutting unit labor costs by 28% and energy use by 30% against legacy hydraulic presses. Global brand owners shift safety-stock policies to align with this regional capacity, accelerating order visibility through 2026. Lower per-part costs allow converters to absorb PP price fluctuation without eroding margin, supporting long-term upside in the in-mold labels market. Skills programs jointly funded by local governments and multinational packaging groups further widen Asia-Pacific’s cost-quality gap over Western competitors, especially in food-grade applications.

Brand-Owner Shift Toward Premium, No-Label-Look Decoration

Dairy, nutraceutical, and luxury cosmetics marketers report 3-5 ppt lifts in off-shelf conversion when packaging appears label-free. Chobani’s Y-shaped IML cup integrates graphics across two compartments in a single shot, eliminating secondary sleeve steps and giving tamper evidence with zero adhesive. Rising adoption boosts tooling volumes for complex geometries, which in turn lowers cost per impression and expands addressable SKUs. Because the no-label-look supports freeze-thaw cycles, frozen desserts and ready-meals are new targets, keeping demand resilient even when macroeconomic conditions soften.

Growth of Digital IML Printing for Short Runs and Personalization

Digital presses add QR codes, variable images, and localized text at throughput exceeding 11,000 labels per hour, slashing time-to-market for limited editions and regional campaigns. [1] Konica Minolta, “Label and packaging industry predictions …,” konicaminolta.euMulti-Color Corporation’s scented Fanta label in Japan shows how digital inks deliver multi-sensory features that command shelf attention. [2]MCC Verstraete, “NextCycle IML,” iml.mcclabel.com Setup-free changeovers reduce waste by up to 18 kg per job, aligning with carbon-reduction scorecards. As e-commerce pushes SKU proliferation, digital IML solves the breakeven challenge of 15,000-to-50,000 unit lots that were previously cost-prohibitive in the in-mold labels market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PP price volatility squeezing converter margins | -0.7% | Global, acute in price-sensitive markets | Short term (≤ 2 years) |

| Limited barrier properties versus sleeve/PSL alternatives | -0.4% | Global, critical in food/pharma applications | Medium term (2-4 years) |

| Slow tool-changeover deterring very high SKU counts | -0.3% | Global, concentrated in high-variety markets | Medium term (2-4 years) |

| Stricter VOC limits on solvent-based inks in Europe | -0.2% | EU primary, spillover to export markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

PP Price Volatility Squeezing Converter Margins

Polypropylene spot prices in North America rose 9 cents per lb in Q1 2025, driven by propylene monomer shortages and higher recycled resin demand. Smaller converters lack hedging instruments, forcing them to renegotiate quarterly, which risks account churn. Some mitigate exposure by adopting thin-wall thermoforming, cutting gram weight by 11% without redesign. Others sign multi-year resin supply agreements indexed to Brent crude, smoothing cash flows but raising working-capital needs. Until feedstock capacity additions in Texas and Ningbo come onstream in 2027, margin pressure will temper aggressive expansion plans in the in-mold labels market.

Limited Barrier Properties Versus Sleeve/PSL Alternatives

Standard PP-on-PP IML gives oxygen transmission rates (OTR) near 30 cm³/m²·d·bar, well above the sub-1 cm³ thresholds that dairy probiotics and IV solutions demand. Alternative ORMOCER and PVOH coatings reduce OTR below 0.1 but currently add 27% to label cost and complicate recyclability. [3]MDPI, “Alternative Oxygen Barrier Coatings for PP Films,” mdpi.com Food processors thus keep ultra-high-barrier uses with sleeve labels or multilayer PET, limiting IML’s penetration in ambient milk, medical nutrition, and pharma diluent packs. Ongoing pilot lines in Germany target plasma-deposited silicon oxide on PP, but commercial viability is two to three years away. This property gap caps upside for the in-mold labels market in stringent barrier applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Process: Thermoforming Gains Momentum

Injection molding accounted for USD 0.84 billion of the in-mold labels market size in 2025, translating to 56.83% revenue. Thermoforming, however, is on pace to log a 7.21% CAGR, outstripping every other process. Brown Machine’s Quad Series machines cut energy draw by up to 35% while running 250,000 lids per hour, converting many dairy plants from injection to thermoforming. Blow molding remains vital for refillable beverage bottles where rib-strength and drop-impact resistance are critical.

Capital budgets show thermoforming lines integrating robotic stackers and camera inspection, raising overall equipment effectiveness (OEE) above 85%. Embedded analytics detect sheet temperature variation and auto-correct heater zones within 50 ms, enhancing yield. Converters note that thin-gauge PP rollstock lowers resin cost per thousand impressions by nearly 18 USD, cushioning PP price volatility. Injection molding still dominates complex closures and multi-component parts, but its share will plateau as sustainability audits favor thermoforming’s lower carbon intensity in the in-mold labels market.

By Material Type: PP Dominance Strengthens

Polypropylene supplied labels on USD 0.66 billion worth of containers in 2025, capturing 44.92% of in-mold labels market share and expanding at an 8.74% CAGR. Regulators endorse PP because it can be sorted with containers, eliminating detaching steps. New random copolymer grades achieve haze below 1% and impact strength beyond 35 kJ/m², widening their use in clear food pots. PE remains the choice for squeeze tubes that require flex-crack resistance, while PET is confined to high-clarity display jars.

Chinese resin majors fast-track meta-allocene catalysts that double melt-flow rate without compromising stiffness, aiding thin-wall parts. Post-consumer recycled PP now exceeds 60% inclusion in some cosmetic tubes, meeting premium brand pledges. Although bio-based PP trials show promise, feedstock supply is limited; thus, fossil-based PP with ISCC Plus certification will remain mainstream across the in-mold labels market.

By Printing Technology: Digital Revolution Accelerates

Flexography generated more than half of 2025 revenue but digital presses are slated to seize incremental share. Konica Minolta predicts digital will reach 9.7% of global label volume by 2029 as converters chase SKU agility. Inkjet heads rated at 1200 dpi now jet UV-curable white at press speeds of 75 m/min, matching flexo opacity. Near-line finishing modules cut label lead times from 10 days to 48 hours.

Software-driven color management ensures ΔE < 1.5 across run-run repeats, permitting cosmetics brands to harmonize global rollouts. Cloud-linked job tickets feed MIS systems, giving enterprise-wide visibility, a key differentiator as multinational CPGs consolidate vendor lists. Gravure retains ultra-high-volume detergent buckets, but as plate cylinder lead times elongate, hybrid presses that phase-switch between inkjet and flexo will underpin growth in the in-mold labels market.

By End-User Industry: Cosmetics Drives Premium Growth

Food represented USD 0.41 billion of revenue in 2025 and stays the anchor segment, yet cosmetics and personal care will show the fastest 8.5% CAGR. ICONS Beauty’s new Ohio plant pumps out PP IML tubes containing 60% PCR while retaining metallic effects demanded by prestige lines. Beverage converters pair peelable IML coupons with refillable popcorn buckets to spur theater concession sales, illustrating functional crossover.

In OTC pharma, interest rises for tamper-evident snap lids that integrate 2D codes for serialization. Automotive electronics housings adopt IML to combine ESD protection graphics with rugged polycarbonate skins. Such diversification supports volume resilience even if discretionary cosmetics spending softens, sustaining revenue visibility for participants in the in-mold labels market.

By Printing Technology: Gravure Maintains Niche Leadership

Gravure cylinders achieve line widths below 5 µm, delivering photo-real metallic images at runs exceeding 1 million units, a capability unmatched by other processes. Labels & Labeling notes gravure’s hold over fast-moving detergents where color fidelity drives brand equity. However, cylinder engraving costs limit adoption in mid-size SKUs.

AstroNova’s AQUAFLEX hybrid couples water-based gravure under-white with digital CMYK, allowing converters to hit Pantone solids plus personalization in one pass. Sustainability targets accelerate gravure’s water-based ink migration, cutting VOCs by 42%. While flexo and digital will take most share gains, gravure’s role in high-coverage metallics and extended color gamut ensures a durable niche within the in-mold labels market.

Geography Analysis

Asia-Pacific led the in-mold labels market with a 40.37% revenue share in 2025 and is forecast to post a 7.83% CAGR through 2031. Capacity additions in China drive tooling availability, while Japanese positive-list regulations harmonize food-contact compliance, easing market access. India’s Chemplast Sanmar invested INR 160 crore in specialty resins supporting local label demand and export contracts. Regional governments subsidize electric press retrofits, lowering greenhouse gas intensity per unit by 28%.

Europe remains the regulatory pacesetter. PPWR pushes for 30% PCR in PET food packs by 2030, catalyzing investment in removable barrier coatings and tethered closures. Switzerland’s ink ordinance adds transparency requirements, compelling suppliers to maintain exhaustive substance registers.These rules squeeze marginal players but reward converters with early-compliance track records, sustaining premium pricing in the in-mold labels market.

North America feels cost headwinds from PP volatility and labor shortages, yet consumer appetite for premium packaging keeps cosmetics and functional dairy lines vibrant. Reshoring grants for molding machinery under the CHIPS-and-FABS programs spur toolmakers to localize spare-parts hubs, trimming downtime. The Middle East and Africa see rising demand for fortified dairy and ready-meals, opening green-field plant opportunities in UAE logistics zones. South America’s soybean-oil derived PET investments widen substrate choices, albeit slower than APAC growth trajectories.

Competitive Landscape

The in-mold labels market features moderate fragmentation. The top five suppliers control an estimated 46% of global revenue, leaving room for regional specialists. CCL Industries lifted Q4 2024 sales by 9%, helped by cross-selling IML with pressure-sensitive labels in multi-format RFPs. TOPPAN’s USD 1.8 billion purchase of Sonoco’s thermoformed and flexible packaging assets furnishes barrier-enhanced IML platforms and extends reach into snack and healthcare.

Strategically, players push automation. Balluff’s guided change-over trims mold swap time by 70%, freeing 12 additional production days per year on four-shift operations. Sustainability remains a battleground: MCC Verstraete launched waterless offset IML inks that slash VOC emissions by 60%, while Amcor–Berry’s merger targets USD 650 million cost synergies and broadens PCR resin access. Mid-tier converters form alliances with digital press OEMs for turnkey mono-material lines, using SaaS dashboards to benchmark OEE across plants.

Downstream, brand owners consolidate preferred-supplier lists to manage compliance risk, intensifying price pressure but bolstering volumes for accredited converters. Entry barriers now hinge on ESG audits alongside food-safety certification. Start-ups focusing on enzyme-enhanced recycling or bio-PP blends find traction as co-development partners rather than direct competitors, ensuring technological diffusion across the in-mold labels market.

In Mold Labels Industry Leaders

-

Innovia Films (CCL Industries)

-

Multi-Color Corporation

-

Orianaa Decorpack

-

Taghleef Industries

-

WINNERS LABELS LLP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: TOPPAN Holdings completed its USD 1.8 billion acquisition of Sonoco’s Thermoformed & Flexible Packaging business, adding a combined USD 1.3 billion revenue platform for sustainable packs.

- April 2025: Amcor closed its merger with Berry Global, targeting USD 650 million cost savings and 12% EPS growth by 2026 through material-science synergy.

- February 2025: Mativ Holdings reported 7.5% sales growth in its Sustainable & Adhesive Solutions segment, reaching USD 290.8 million on volume gains across label films.

- September 2024: IMDA announced 2024 in-mold technology award winners, highlighting advances in sensory labels and barrier coatings.

Global In Mold Labels Market Report Scope

In-mold labels are a type of product decoration used in the packaging industry. These labels are placed inside a mold before forming the plastic container or product. The label becomes integral to the final product during molding, resulting in a seamless, durable, high-quality finish. This technique is commonly used for plastic containers, such as food packaging, cosmetic containers, and industrial products.

The in-mold labels market is segmented by end-user industry (food and beverage, cosmetics, pharmaceutical, and other end-user industries) and geography (North America, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Injection Molding |

| Blow Molding |

| Thermoforming |

| Polypropylene (PP) |

| Polyethylene (PE) |

| Polyethylene Terephthalate (PET) |

| Other Material Types |

| Flexographic |

| Digital (Inkjet, EP) |

| Gravure |

| Other Printing Technology |

| Food |

| Beverage |

| Cosmetics and Personal Care |

| Other End-user Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Production Process | Injection Molding | ||

| Blow Molding | |||

| Thermoforming | |||

| By Material Type | Polypropylene (PP) | ||

| Polyethylene (PE) | |||

| Polyethylene Terephthalate (PET) | |||

| Other Material Types | |||

| By Printing Technology | Flexographic | ||

| Digital (Inkjet, EP) | |||

| Gravure | |||

| Other Printing Technology | |||

| By End-user Industry | Food | ||

| Beverage | |||

| Cosmetics and Personal Care | |||

| Other End-user Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the in-mold labels market?

The in-mold labels market reached USD 1.53 billion in 2026 and is projected to climb to USD 1.87 billion by 2031.

Which region leads the in-mold labels market?

Asia-Pacific holds 40.37% revenue and is strengthening its lead thanks to high-cavitation capacity and lower production costs.

Why is polypropylene preferred for in-mold labels?

PP combines good impact strength with recyclability, aligns with mono-material regulations, and delivers the highest 8.74% CAGR among substrates.

How fast is digital printing growing in in-mold labeling?

Digital printing is forecast to advance at a 9.27% CAGR, driven by demand for personalization and short production runs.

What production process is gaining share?

Thermoforming is the fastest-growing process at 7.21% CAGR because it cuts energy use up to 35% and supports thin-wall parts.

What are the main restraints for the sector?

PP price volatility and limited barrier properties versus sleeve labels currently cap margins and penetration into oxygen-sensitive applications.

Page last updated on: